Abstract

This research seeks to add to our understanding about discouraged borrowers by examining the roots of discouragement. It examines the role of informal turndowns in which a commercial lender verbally informs a SME owner that if a formal loan application were to be advanced, it would likely be denied. This aspect of demand-side constraints to accessing finance has received scant attention in research. The presence of discouraged borrowers could be evidence of a market imperfection; however, informal turndowns represent an efficient mechanism in SME debt markets providing an explanation for a type of borrower discouragement. This research finds more established firms are more likely to suspend formal loan applications through informal talks with their banks rather than being discouraged by their own judgement. In addition, those small business owners who have a satisfactory relationship with their banks are more likely to self-ration themselves rather than conduct an informal inquiry with their banks before deciding not to apply.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

This research seeks to contribute to the emerging literature on demand-side constraints on access to finance among SMEs. It reflects on Kon and Storey’s (2003) definition of discouraged borrowers: good borrowers who need bank loans yet do not apply for a loan because they fear the application will be rejected. The research described here differentiates between those business owners discouraged out of a fear born of their own self-assessment and those business owners who eschew a loan application because they know they will be turned down because their lender had so informed them. While the profiles of these two groups arguably differ, previous research has not differentiated between them. This research seeks to address this difference, thereby adding to our understanding of demand-side constraints on access to finance.

It is widely understood that SMEs contribute disproportionately to economic prosperity, especially through the growth of young ventures (Audretsch 2012; Nightingale and Coad 2014). However, financing is central to this growth (Beck and Demirguc-Kunt 2006; Shane 2009; Wiklund and Shepherd 2003) and once internal capital is exhausted, SME owners typically turn to banks as lenders of choice (Cosh, Cumming and Hughes Cosh et al. 2009; Robb and Robinson 2014). Even though banks approve the majority of loan applications (Cole and Sokolyk 2016; Vos et al. 2007; Freel et al. 2012), accessing financial capital is often perceived as difficult among SMEs, and for new ventures in particular (Berger and Frame 2007; Cosh et al. 2009; Petersen and Rajan 1994; Robb and Robinson 2014). To business owners, the borrowing decision inherently involves some degree of uncertainty as to the outcome of their applications, which can involve financial and other less tangible costs that “can be considered as financial, in-kind, or psychic” (Kon and Storey 2003, p. 38). For some business owners, the perceived cost-benefit balance is such that tendering a formal application seems unreasonable. These “discouraged borrowers”, owners whose firms need financing but do not apply due to fear of rejection based on their self-assessment, face the same consequences as with credit rationing: firm viability and growth potential are compromised.

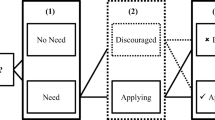

However, results of previous research differ widely regarding the profiles of discouraged borrowers and the reasons for fear of applying remain unclear. In particular, much of the existing empirical literature about “discouraged borrowers” ignores the reasons owners choose not to apply (see Brown et al. 2011; Chakravarty and Xiang 2013; Chandler 2010). Figure 1 (authors’ analysis of BDRC Continental 2015), for example, provides one listing of business owners’ main reasons for not applying for a loan. Arguably, the characteristics of these categories of firm are likely to differ one from the other and the composition of discouraged borrower samples used in previous research are hybrids and also likely to differ from each other. These differences potentially contribute to disagreements about our understanding of discouraged borrowers as presented by existing studies.

Structure of the data and scope of the analysis illustrating the main reasons of eschewing loan applications

This work addresses this contention by investigating empirically a category of business owners that would have been classified as “discouraged” by existing research but who, in reality, eschewed a loan application because their prospective lenders had informally advised them that a forthcoming loan application would be rejected. This concept, “informal turndown”, is neither new nor hypothetical. Based on interview data with SME bank customers, Wynant and Hatch (1991, 116) reported,

… a large number of financing requests are declined or discouraged after a meeting with the client … [and it] is only in those instances where the proposed financing involves a reasonable chance of being approved that a formal application results.

Even though Wynant and Hatch reported a high frequency of informal turndowns, the topic seems not to have been of interest to researchers.

Accordingly, this work argues that, for some segment of what previous research has defined as “discouraged borrowers” population, not applying is not justified by “fear”, but by knowledge information gleaned from SME owners’ relationships with their lenders. At the extreme, some lenders explicitly advise SME owners that, if they do apply for a loan, rejection is certain or likely. Less explicit situations might include a lender outlining unacceptable terms of lending or yet subtler signals of rejection in the context of the lender-borrower relationship. This study therefore separates non-applicants who avoid banks mainly because of fear of rejection from those who know they will be rejected (having experienced an informal turndown). This separation is important because the former potentially constitutes a market imperfection while the latter could be a sign of efficient sorting. This distinction also better operationalizes the term “discouraged borrower” as a grouping free from “contamination” by owners who are not motivated by fear, but by information they informally obtained. Arguably, by separating informal turndowns from discouraged borrowers, the remaining discouraged borrowers would be closer to Kon and Storey’s original definition (2003), one that focuses on unjustified fear of rejection based on their self-assessment. This allows us to draw a more accurate profile of discouraged borrowers closer to that defined by Kon and Storey.

This study draws upon data from the quarterly series of Surveys of Small- and Medium-Sized Enterprise Finance Monitor 2011–2015 (BDRC Continental 2015) in the UK.Footnote 1 It benefits from questions that report the main reasons why firm owners refrain from applying for bank loans even though they need financing. Accordingly, the first objective of this paper is to compare the profiles of selected sub-groups from within the discouraged borrower population. The second is to present insights about informal turndowns—a phenomenon about which little is known—thereby helping to develop a yet better understanding of the demand-side constraints on access to finance.

This paper continues with a critical review of the pertinent research literature and follows with the conceptual rationales behind the study hypotheses. A description of the data and methodological approaches ensues, followed by the empirical findings. The paper closes with a discussion of findings, their implications and limitations and directions for future research.

This study finds that more established firms are more likely to suspend formal loan applications through informal talks with their banks rather than being discouraged by their own judgement. In addition, business owners who have a satisfactory relationship with their banks are more likely to self-ration themselves rather than conduct an informal inquiry with their banks before deciding not to apply.

2 Previous research: discouraged borrowers and informal turndowns

Research about discouraged borrowers has attracted the particular attention of academics, practitioners and policy makers. One reason is that the high frequency of discouraged borrowers reported in previous research (for example, Cole and Sokolyk 2016; Freel et al. 2012) is such that discouraged borrowers outnumber actual turndowns. Another reason is that this phenomenon may imply market failure. As Han, Fraser and Storey (Han et al. 2009, p. 416) observe, discouraged borrowers constitute a “market imperfection” that holds implications for economic welfare if misplaced fears of rejection compromise either the viability, or the job-creating growth, of SMEs.

Accordingly, by studying the profiles of discouraged borrowers, previous research has sought explanations as to why owners whose firms need financing do not to apply (for example, Brown et al. 2011; Cavalluzzo et al. 2002; Chakravarty and Xiang 2013; Cole and Sokolyk 2016; Ferrando and Mulier 2015; Freel et al. 2012; Gama et al. 2017; Han et al. 2009; Levenson and Willard 2000). Much of the existing empirical literature uses a definition of “discouraged borrowers” that is broader than that specified by Kon and Storey (2003): firms that need financing but do not apply for any reason. However, there may be a variety of reasons for not applying in addition to fear of rejection. The UK Small- and Medium-Sized Enterprise Finance Monitor (2011–2015), for example, reveals that 47.2% of business owners who needed financing but who did not submit an application for a loan cited, as reasons for not applying, lack of time or knowledge or felt the process a “hassle”. Moreover, 13.6% of respondents reported having been turned down informally (see Fig. 1). Arguably, the characteristics of these firms are likely to differ across categories; so, their inclusion—in varying proportions—in samples used in previous research can be expected to prompt some of the disagreements seen in existing literature.

The research literature generally agrees that discouraged borrowers are indeed engaged in relatively riskier projects when compared with loan applicants (Cavalluzzo et al. 2002; Cole and Sokolyk 2016; Cowling et al. 2016; Ferrando and Mulier 2015; Han et al. 2009). That is, owners of firms with higher risk scores are—on average—more likely to feel discouraged from applying for credit. This is a finding consistent with the premise that previous samples included some proportion of informally turned down SMEs. That is, an alternative explanation is that the finding of higher risk among discouraged borrowers reflects that samples are “contaminated”, to an unknown extent, by owners that had experienced informal turndowns.

Firm size also features consistently as a key factor in the likelihood of discouragement, such that owners of larger firms are relatively less likely to be discouraged (Chandler 2010; Cole and Sokolyk 2016; Freel et al. 2012; Han et al. 2009; Robb and Wolken 2002). However, the estimated impacts of firm age are mixed within the existing literature. No impact is reported by some researchers (Chakravarty and Xiang 2013; Chandler 2010; Freel et al. 2012); others report negative (Cole and Sokolyk 2016; Cowling et al. 2016; Ferrando and Mulier 2015) or positive (Han et al. 2009) correlations of firm age with the likelihood of being discouraged. Similarly, there remains mixed evidence of the role of owner gender on the likelihood of discouragement (Gama et al. 2017). Arguably, these factors could differ between firms whose owners fear rejection and owners who have faced informal turndowns.

The literature also disagrees on other points, such as whether the banking relationship plays a role in discouragement. Freel et al. (2012) report that firms with banking relationships beyond financial transactions are relatively less likely to report discouragement. Conversely, Chandler (2010) reports that, compared to loan-denied applicants, discouraged borrowers have stronger relationships with their respective credit suppliers. Likewise, Han et al. (2009) report that, within the group of firms with longstanding relationships, discouragement is less likely among low-risk borrowers but more likely among high-risk borrowers. The finding that discouraged borrowers tend to have established lender relationships is consistent with the premise that, in some cases, decisions not to apply for a loan may reflect informal turndowns. Arguably, prospective borrowers and lenders are more comfortable with broaching and discussing the idea of a loan application within the context of a good-quality banking relationship than in the absence of such a relationship.

The prevalence of discouragement also remains unclear. Studies in the USA and the UK, Han et al. (2009), Cole and Sokolyk (2016), Freel et al. (2012), and Brown and Lee (2017) report high frequencies of discouragement among SME owners who declare a need for finance but do not apply. However, the frequency of discouragement in inter-country comparisons beyond the USA and the UK appears to vary significantly from as little as 1% to as much as 45% (Chakravarty and Xiang 2013; Ferrando and Mulier 2015; Gama et al. 2017).

The frequency and impact of informal turndowns have not, however, been considered, so the need for further research seems implicit.Footnote 2 This study addresses this gap in the literature while attempting to draw a more accurate profile using a more strict definition of discouraged borrowers, one that excludes those owners who had experienced being turned down informally. If business owners approach banks and, based on informal talks, decide to abandon loan applications, this ought not be considered as borrower discouragement and thus may not be a signal of potential market inefficiency.

3 A conceptual framework of informal turndowns

The conceptual framework for this research rests in the process by which commercial lenders adjudicate loan applications from SMEs. This process has been conceptually modelled in the context of lending relationships (Besanko and Thakor 1987; Petersen and Rajan 1994). In the interim, SME lending markets have changed in that requests for very small loans are typically adjudicated by credit scoring (Berger and Frame 2007). Nonetheless, bankers and SME owners continue to pursue professional relationships. According to Doering (2018) “personal relationships play an essential role in shaping financial transactions between intermediaries and clients”. Moro and Fink (2013) emphasise that lending to small firms “cannot be reduced to facts and figures … trust can also support and increase the amount of other soft and hard information … and, thus, help the loan manager to take decisions”. In addition, bank lenders remain a source of advice for owners just as they continue to do so for individuals.

The adjudication process may therefore be conceptualised as comprising two steps. The first stage is an informal phase situated within the lender-borrower relationship. The second, more formal, stage is typically characterised by submission of formal (written or on-line) documentation from the borrower and, for those applications that pass an initial review, is followed by costly due diligence conducted by the lender (Deakins and Freel 2009).Footnote 3

In this context, an initial informal discussion between borrower and prospective lender presents an opportunity for both sides to presage a contemplated loan application. This is an efficient process from both the lender and the borrower perspectives. It saves loan account managers’ time when a formal request is not well-considered, obviously too risky, or when considerable—and costly—due diligence may be required. In addition, some loan requests are simply too small to be economic from the lenders’ perspective. From the borrowers’ perspective, a formal application—especially if turned down—is costly in time and resources and, potentially, the applicant’s credit rating may be negatively affected by a “formal” turndown. Whereas borrower discouragement may be seen as a market imperfection, informal turndowns are arguably consistent with efficient operation of credit markets.

Perforce therefore, informal turndowns take place in the context of a banking relationship. If the potential applicant has an established personal or corporate relationship with the financial institution, the “soft” information gleaned from the relationship may provide lenders additional insights about the risk of the loan (if approved). Firms without banking relationships or with poor banking relationships would arguably either proceed directly to the formal application stage, or be discouraged based on their own judgement: the former approach potentially risks their reputations, and the latter may result in underinvestment. Therefore, it is argued that it is relatively easier for some SME owners, those who are satisfied with their banks, to make an unofficial inquiry about their prospects before making an official request. Hence, the first hypothesis is:

H1:Among non-applicants who need credit, owners of firms that report informal turndowns are relatively more likely than other discouraged borrowers to have a satisfactory relationship with their bank.

It makes sense for both sides of a transaction to employ informal discussions to reduce information asymmetry. However, for small loan requests—typically those advanced by firms at the small end of the size spectrum—applications tend to be adjudicated by means of algorithmic credit scoring models derived from statistical analyses of default histories (Berger and Udell 2006). The presence of credit scoring technologies suggests two reasons why owners of smaller firms are arguably more likely to feel discouraged. First, the scoring system is based on hard information but smaller firms are thought to be relatively informationally opaque. The disadvantages of small firm size in the context of credit scoring system can be ameliorated when banks use their discretion in interpreting the score: that is, when the bank decides to collect “soft” information through years of lending relationship with its clients. Arguably, therefore, benefits of relational lending are strongest for larger firms rather than smaller firms (Berger and Black 2011). Second, the conservatism of bank lenders is well known (Carey, Post and Sharpe Carey et al. 1998), so owners of smaller firms might choose to postpone their applications because they anticipate having their applications rejected. Conversely, owners of larger firms are less likely to be subject of lender conservatism. Accordingly, owners of large firms are arguably more likely, in the first instance, to expect a successful loan application but also may reconsider an application after advice from their lender. Thus, the second hypothesis is as follows:

H2: Among non-applicant firms that need credit, the likelihood of an informal turndown is proportional to firm size: larger firms are more likely to report informal turndowns than smaller firms are.

Within any given size stratum, age of firm is arguably a key factor in the likelihood of an informal turndown. Owners of young firms are often aware that, as start-ups, their firms are risky (Carpenter, Pollock and Leary 2003): that new firms often fail relatively soon after founding due to “the liability of newness” (Stinchcombe and March 1965); inexperienced entrepreneurs; inefficient operations; and unproven factor and product markets. It is also hypothesised that the owners of new firms are more likely to be aware of the high degree of information opacity in their firms and elect not to apply for loans. Conversely, information about older firms is usually more widely available. Similar to large firms, older ones are more likely to have established a banking relationship and less likely to be a subject of bank conservatism. Thus, business owners of older firms are arguably more likely to anticipate successful applications and proceed with an informal discussion. Accordingly, the third hypothesis is:

H3: Among non-applicant firms that need credit, the likelihood of an informal turndown is higher among older firms than among younger SMEs.

The following provides an outline of the data and methodological approaches used to investigate these hypotheses empirically.

4 Data and methodology

4.1 Data

The paper examines the profiles of two groups of firms who needed capital but did not formally apply for the credit: (1) borrowers discouraged due to subjective fear of rejection; and (2) prospective borrowers who did not apply for a loan because they had experienced informal turndowns. The investigation comprises a secondary analysis of cross-sectional data from the 18 iterations of the UK-based Small- and Medium-Sized Enterprise Finance Monitor (2011–2015) survey. The sample is stratified and all analyses employ sampling weights that correct for size, location, industry and the share of start-ups. The respondents are owners or primary managers of private firms, all within the UK, with fewer than 250 employees or less than £25 million in annual sales revenues.

4.2 Methodology

The methodological approach consists of estimating a series of binomial and multinomial probit regression models. These models suit the binary and categorical nature of the dependent variables. The universe of interest comprises firms that need credit.

4.2.1 Dependent variables

The first step of this research compares the profiles of applicants against those of non-applicants. The survey asked those who did not apply for loans, yet claimed they needed credit, to identify “the MAIN reason why [they] did not apply for a facility?” (BDRC Continental 2015). These reasons were classified in six groups illustrated in Fig. 1 (see Table 1 for description of responses).

The first dependent variable is developed to model a more accurate and consistent profiles of discouraged borrowers by employing multinomial probit analysis. A categorical variable was used to model three groups:

the probability of being discouraged because of fear of rejection;

the probability of not applying for any other reason (including an informal turndown (both groups expressed a need for debt capital); and,

the probability of making formal applications (reference category, model 2, Table 3).

The second categorical dependent variable employed in the second multinomial probit model tests the articulated hypotheses by using the following additional breakdowns among non-applicants who needed financing but did not apply:

= 1, for informal turndown (IT);

= 2, fear of rejection (DB: reference category, Table 4);

= 3, for any other reason.

4.2.2 Independent variables

To capture the effect of relational lending, entrepreneurs’ self-reported level of satisfaction with their main bank was used as an independent variable. Previous research often employs either the length of lender-borrower relationship or the presence of a relationship; however, this measure is not available in these data. We argue that the level of satisfaction is a reasonable measure of banking relationship in the context of discouraged borrowers and informal turndowns. These two groups of non-applicants differ with respect to the mechanism through which they learn about possible rejection. The main effect of a relationship is a reduction of information asymmetry for both parties. It therefore seems reasonable that client firms who are satisfied with their banks are more likely to provide information to, and be comfortable seeking counsel from, their lenders. The other two independent variables, age and size, are measured by categorical variables explained in Table 1.

4.2.3 Control variables

To control for attributes of the business and entrepreneur that might affect the likelihood of searching for finance-related information, several additional control variables are included. Innovative and exporting firms are more likely to face difficulty in raising finance (Freel 2007; Riding et al. 2012), yet more likely to seek financing (Lee 2014; Riding et al. 2012) or of seeking finance-related advice prior to making formal loan applications (Rostamkalaei and Freel 2017). To reflect these factors, the models include three dummy variables according to whether a firm is, respectively, an exporter, a product innovator or a process innovator.

The presence of outstanding credit from other sources of debt could have impacts on both the SME owner’s decision to apply and the lender’s response, possibly an informal turndown. The presence of outstanding debt approved by other financing sources informs the lender about the firm. In this case, SME owners, having successfully obtained such financing, maybe arguably more confident, less likely to be discouraged and less likely to be informally turned down. Moreover, SME owners who rely on high-cost debt (credit card, overdraft, etc.) have incentive to apply for lower-cost bank debt. It is therefore to be expected that the presence of outstanding debt has a positive impact on the likelihood of applying and of initiating informal discussions and a negative impact on the likelihood of being discouraged. Previous research findings confirm that success in obtaining other sources of finance is negatively correlated with the likelihood of discouragement (Xiang et al. 2015; Gama et al. 2017; Cole and Sokolyk 2016).Footnote 4

Legal status of the businesses such as single ownership, partnership or a limited liability company has been linked to the likelihood of discouragement (Freel et al. 2012). In addition, the owner’s gender, financial qualifications and having regular financial statements have also been found to be significant (Gama et al. 2017) and are, therefore, included among control variables. Business plans are often used as a basis to initiate informal discussion; therefore, we control for the effect of having a formal written business plan. A categorical variable based on Dun & Bradstreet and Experian credit scores was employed to control for the risk of the firm (Cole and Sokolyk 2016; Cowling et al. 2016; Han et al. 2009; Ferrando and Mulier 2015).

5 Empirical findings

5.1 Descriptive statistics

Table 2, which exhibits descriptive statistics, shows a total of 95,273 firms in the sample; subsamples comprise non-applicants who desire credit (N = 3587), discouraged borrowers (DBs; N = 1293) and informal turndowns (ITs, N = 577). Accounting for sample weights, these data show that, among non-applicants, 39.2% of firms are discouraged borrowers while 13.6% of firms cited being informally turndown as the main reason for relinquishing a formal loan application.

Table 2 shows that compared to DBs, ITs differed significantly in terms of size and age. That is, older firms, at least based on univariate comparisons, are relatively more likely to face informal turndowns. Smaller firms, those with no employees, reported a higher incidence of discouragement while firms with employees are more likely to report informal turndowns. In the full sample, 81.5% of firms are satisfied with their relationship with their banks. The proportion of satisfied firms is higher among DBs and the proportion of unsatisfied firms is higher among ITs.

Single-owner firms are more likely to be DBs while limited liability firms are more likely to face informal rejection. Female entrepreneurs are more likely to fear rejection and are less likely to contact their banks. ITs were more likely to be exporters and innovators. That is, based on univariate comparisons, firms that undertake these growth strategies are more likely to contact their banks searching for additional credit rather than to self-ration. Entrepreneurs with a business plan and regular financial statements are relatively less likely to be discouraged and more likely to inquire with their banks about the prospects of loan applications.

5.2 Multivariate analyses

5.2.1 Applicants and non-applicants

The first step in the analysis was to estimate multivariate models that compare the attributes of applicants with those of firms that needed credit but did not make an official request for any of the reasons listed in Fig. 1. Model 1 of Table 3 shows that size of firm is significant in determining the likelihood of making an application, with larger firms being more likely to make formal loan applications than smaller firms. Single-owner firms and firms with high risk ratings are significantly less likely to make formal applications. Firms with formal business plans are more likely to apply (however, such plans are often required as part of formal loan application packages). Use of overdrafts or credit cards increased the likelihood official applications for bank loans when credit was needed. This is consistent with the argument that outstanding debt reduces information asymmetry and encourages SMEs to apply.

5.2.2 DBs and applicants

Model 2 of Table 3 shows the results of estimating a multinomial probit model of the probability of making an application (reference category), being a DB, or of avoiding an application for any other reason. In line with the findings of model 1, the analysis shows that compared to applicants, firms whose owners fear rejection are more likely to be smaller and have higher risk rating. Having a formal business plan decreases, and being an exporter increases, the probability of being discouraged. Using credit cards is associated with a decrease in the likelihood of fearing rejection.

5.2.3 DBs and ITs

The final stage of the analysis is based on multinomial probit comparisons of sub-categories of non-applicants: informal turndown (IT); fear of rejection (DB) (reference category); and, other reasons. Table 4 represents the extract from this analysis that compares ITs relative to DBs. Model 1 includes only control variables and firms’ size and age. Model 2 shows the results of the estimation when the model is augmented with a measure of the banking relationship. The final panel, model 3, shows the additional impact of credit risk rating. (This variable is included in the final panel as the value of this variable is missing for 15% of observations in the dataset, especially among smaller and younger firms.)

These findings show that firm size does not seem to differentiate ITs from DBs. Although firm size is inversely associated with the probability of eschewing a loan application when the firm needs credit, it is not a discriminator between ITs and DBs. The second hypothesis, therefore, is not supported.

Older firms are significantly more likely than younger firms to report informal turndowns, rather than DBs. That is, older firms seem better able to informally seek their banks’ opinion before postponing a loan application. This finding confirms the third hypothesis: SME owners are aware that they are susceptible to information asymmetry, the liability of newness, and banks’ conservatism, and thus more likely to refrain from loan applications by their own judgement rather than seeking advice from banks. It also speaks to the debate about the link between relational lending and the probability of discouragement. Given that banks have more information on older SMEs gathered through longer relationships, the positive association of business age on the probability of ITs, compared to DBs, explains one reason that younger firms are more likely to self-ration.

Model 2 shows that entrepreneurs’ reported level of satisfaction with their banks is a statistically significant discriminator between informal turndowns and discouraged borrowers; however, the direction was opposite to that which was hypothesised. Business owners who reported a satisfactory relationship with their banks are more likely to report being a discouraged borrower. One possible explanation is that, among non-applicants, discouraged borrowers self-ration themselves before the bank (may) refuses their loan applications. Therefore, their restricted access to credit is based on their own expectation rather than hearing a rejection or going through the hardship of dealing with searching and information gathering.

Use of overdraft and credit card variables, which partially reflect the amount of information banks have about their customers, does not discriminate significantly between DBs and ITs. The result is consistent with the argument that the outstanding debt on credit card or overdraft is a sign of reduced information asymmetry (which predicts decreased probabilities of both DBs and ITs—Table 3, model 2). The statistically significant relationship between the level of satisfaction with banks and the probability of receiving informal turndown disappears once the credit risk rating is included in the model (model 3). It is worth noting that credit risk is missing mainly for smaller and younger firms. This effect implies that the effect of satisfactory relationship is stronger for small young firms than larger, more established ones.

From model 3, it seems that credit risk rating does not discriminate between ITs and DBs; however, higher risk firms are less likely to advance formal applications (Table 3). This supports the idea that business owners have some level of awareness of their firms’ credit risk.

Businesses owned by women are significantly less likely than those owned by men to report ITs. This implies that women tend to rely on their own self-assessments without verifying their views with their banks. However, the effect of gender diminishes when business risk is taken into account (model 3), suggesting joint impact of business risk and female ownership (as well as size and age, as credit risk is missing more often for smaller and younger firms). This potentially explains the disagreement in the literature about the role of gender on discouragement: whereas some findings show that female owners are more likely to fear of being declined (Cavalluzzo et al. 2002; Chakravarty and Xiang 2013; Ferrando and Mulier 2015); others claim no gender difference (Freel et al. 2012).

Finally, firms with formal business plans (models 1 and 2) are significantly more likely to report informal turndowns. It may be that having a business plan gives confidence to the owner to ask his or her bank’s opinion because of the business plan’s ability to reduce information asymmetry. We speculate that the business plan may be used as part of an informal loan application discussion. Alternatively, a business plan may comprise an informal substitute for a formal loan application, leading to an informal turndown. Compared to limited liability firms, single owners are more likely to be discouraged borrowers.

5.3 Robustness

To test the reliability of these findings, several additional tests were undertaken. First, the correlations among variables were reviewed, finding that no pair was closely correlated; all variance inflation factors (VIFs) were less than 10. Thus, multicollinearity does not seem to be a substantive issue within the multivariate modelling. The results have also been verified with alternative definitions of discouraged borrowers where only “I thought I would be turned down” was considered DB (SME owners who answered “This is not the right time to apply for borrowing” were excluded). In addition, multinomial probit regression was performed with dependent variables containing all the classifications listed in Fig. 1. The findings did not differ qualitatively from those reported here.

We acknowledge modelling non-applicants without considering the probability of needing capital could result in selection bias. Accordingly, Heckman’s (1979) two-stage model was employed to address potential selection bias using a selection equation with the dependent variable being a binomial variable corresponding to whether (= 1) or not (= 0) the firm needed external credit. Growth intention was considered as the exclusion criteria; however, estimates of the inverse Mill’s ratio in the second stage were not significant. Therefore, analyses were performed without Heckman’s (1979) two-stage procedure. Given this limitation, extending our results beyond the categories of non-applicants defined in Fig. 1 might be considered bold.Footnote 5

6 Conclusions and implications

Drawing upon the UK Small- and Medium-Sized Enterprise Finance Monitor Survey (2011–2015), this research compares the profile of SME owners who refrain from borrowing from their banks as a consequence of an informal loan turndown with those who do not apply due to a fear rejection. Although entrepreneurial finance has recently paid attention to the latent demand of loan markets, reasons for why it exists generally remain unclear. To this point, it appears that informal loan turndowns represent a non-trivial portion of this phenomenon.

This research compared the characteristics of firms that reported informal turndown (ITs) with those of firms that reported discouragement due to a subjective fear of rejection (DBs). While ITs rely on their banks’ opinions to avoid costs of application and the potential consequences of rejected applications, DB’s decisions are based on their own judgements. This work found that, contrary to the hypothesis, firm size was not significantly correlated with informal turndown. Conceptually, the scale of a loan seemed to be a reasonable precursor of the likelihood of informal turndown, but this was not supported by the empirical results.

An interesting finding of this research is the effect of business age in discriminating among the reasons for postponing formal loan applications. Business age shows mixed effects on discouragement in the existing literature. While some researchers do not find a significant effect of age in regard to the probability of discouragement (Chakravarty and Xiang 2013; Chandler 2010; M. Freel et al. 2012), others report negative effects (Cole and Sokolyk 2016; Cowling et al. 2016; Ferrando and Mulier 2015), or positive effect (Han et al. 2009). This study shows that firm age is a clear discriminator between being discouraged and being informally turned down. Within non-applicants, owners of older firms seek confidential opinions from their banks relatively more often, and therefore they are more likely to relinquish loan application through their banks other than any other reason. Younger firms, on the other hand, are more likely to fear rejection. This is consistent with the conceptual framework developed for the second hypothesis: the older a firm gets, the less likely it is to be the subject of lender conservatism and the less likely it is to face high degree of information asymmetry. On the other hand, younger firms are relatively more likely to be subject to information asymmetry, liabilities of newness and lender conservatism. They are aware of these drawbacks, so they are more likely to self-ration. In addition, younger firms tend not to have established relationships with their banks (or, perhaps, they do not yet have a specified account manager (Chandler 2010)), who helps to initiate informal discussions.

The existing studies do not agree about the impact of satisfaction with bank on the probability of discouragement. Some previous research has confirmed that having a better relationship with banks reduces the propensity of discouragement (Chakravarty and Yilmazer 2009; Freel et al. 2012), yet others are equivocal with some findings showing no significant or negative effects of relational lending on discouragement (Chakravarty and Xiang 2013; Chandler 2010; Cole and Sokolyk 2016; Cowling et al. 2016). Han et al. (2009) reported that longer term relationships with banks increase the probability of discouragement for bad borrowers and decrease the likelihood for good borrowers, implying that discouragement is an efficient sorting tool. We find that those firms, which are satisfied with their banks, are less likely to be informally turned down. Once the risk rating is included in the model, and sample is biased toward more established and larger firms, the effect of level of satisfaction on the probability of discouragement disappears. We argue that since discouraged borrowers self-ration themselves and they anticipate rejection if loan applications were to be advanced, they remain satisfied with their banks. Future research could nevertheless usefully examine the mechanism behind this negative association between the frequency of informal turndown and the level of lending relationship.

This study also attempts to draw a more accurate profile of discouraged borrowers using a stricter definition—owners whose firms need financing but did not apply solely due to fear of rejection. It finds that discouraged borrowers, compared to applicants, are smaller, higher risk SMEs that are more likely to be involved in exporting and who lack a formal business plan and outstanding credit card debt. This profile is consistent with previous research that reports that discouraged borrowers are indeed engaged in relatively riskier projects (Cavalluzzo et al. 2002; Cole and Sokolyk 2016; Cowling et al. 2016; Ferrando and Mulier 2015; Han et al. 2009).

The main limitation of this research is that there might be SME owners who applied for loans even though their applications were informally turned down; however, the data do not identify such applicants. Therefore, we cannot compare those applicants (who ignore an informal turndown) with those who gave up applying following informal rejection. Nor do we know the outcomes of those loan applications. In addition, while acknowledging the value of the data used in this research, there are limitations associated with analyses of secondary data—examples of which include the cross-sectional nature of the questionnaire that does not allow us to understand the sequences of events and that limit firm attribute variables (e.g., the propensities to innovate and to export variables are unavailable). In addition, measures of banking relationship usually used such as length or the extent of lending relationship are not captured in these data.

Distinguishing the reasons why an applicant decides not to approach financial institutions for external financing has implications for researchers. This work has established the presence of an additional category of SME owner who otherwise might have seemed to be a discouraged borrower, but who actually eschew loan applications for good reasons. This is a finding that, at the very least, reduces the scale and scope of what might otherwise be considered a market imperfection associated with the presence of discouraged borrowers. Moreover, the results of this study imply that both discouraged borrowers and informally turned down applications are riskier than firms that submitted formal applications for bank loans, suggesting that both might potentially be efficient mechanisms in the commercial lending market for SMEs.Footnote 6 The findings of this research suggest that addressing discouragement as a demand-side credit constraints would be more fruitful if the focus of attention shifts toward younger firms as they are more likely to fear rejection based solely on their own judgement.

This study presents initial insights about informal turndowns—a phenomenon about which little is known—thereby helping to develop a yet better understanding of the demand-side issues that relate to access to financial capital and the dynamics of the SME-commercial lender relationship. Further research is required to explore the full range of outcomes from informal discussions between potential borrowers and their banks and to advance a yet more robust theoretical framework for examining the efficiency of such informal discussions.

Notes

The data that support the findings of this study are available from https://discover.ukdataservice.ac.uk/catalogue/?sn=6888&type=Data%20catalogue

An exception is the work of Popov (2016) who mentions the possibility that discouraged firms might be informally rejected yet who considers discouraged firms and informally turned down firms to be equivalents.

Of course, firms may skip the first step and proceed directly to the second step: a formal application for a loan.

The low percentage of firms using financing sources other than overdrafts and credit cards does not merit inclusion in the analysis.

To capture the long-term effect of the 2008 financial crisis and as final robustness check, the year in which data was collected was included in the model. The results did not change in any material respect.

The following three observations imply that informally turned down applications are riskier than applicants: (1) non-applicants are riskier than applicants (model 1, Table 3); (2) discouraged borrowers are riskier than applicants (model 2, Table 3); and (3) there is no significant difference in risk levels between discouraged borrowers and informally turned down applications (Table 4). However, until further analyses are conducted, we cannot confirm the extent of the effectiveness of informal turndown as a mechanism of deterring bad borrowers and attracting good borrowers.

References

Audretsch, D. (2012). Determinants of high-growth entrepreneurship, Report prepared for the OECD/DBA International Workshop on High-growth firms: Local policies and local determinants (Report prepared for the OECD/DBA International Workshop on High-growth firms: Local policies and local determinants). Copenhagen,28 March 2012: Paris, OECD/Copenhagen, DBA.

BDRC Continental. (2015). Small- and medium-sized enterprise finance monitor, 2011-2015. [data collection]. 12th Edition. UK Data Service. BDRC Continental. Retrieved from https://discover.ukdataservice.ac.uk/doi?sn=6888#9

Beck, T., & Demirguc-Kunt, A. (2006). Small and medium-size enterprises: access to finance as a growth constraint. Journal of Banking & Finance, 30(11), 2931–2943. https://doi.org/10.1016/j.jbankfin.2006.05.009.

Berger, A. N., & Frame, W. (2007). Small business credit scoring and credit availability. Journal of Small Business Management, 45(1), 5–22. https://doi.org/10.1111/j.1540-627X.2007.00195.x.

Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking & Finance, 30(11), 2945–2966. https://doi.org/10.1016/j.jbankfin.2006.05.008.

Berger, A.N., & Black, L.K., (2011) Bank size, lending technologies, and small business finance. Journal of Banking & Finance, 35(3), 724–735.

Besanko, D., & Thakor, A. V. (1987). Collateral and rationing: sorting equilibria in monopolistic and competitive credit markets. International Economic Review, 28(3), 671–689. https://doi.org/10.2307/2526573.

Brown, Martin, & Lee, N. (2017). Reluctant borrowers? Examining the demand and supply of finance for high growth smes in the UK. INSTITUTE OF CHARTERED AC.

Brown, M., Ongena, S., Popov, A., & Yes,in, P. (2011). Who needs credit and who gets credit in Eastern Europe. Economic Policy, 26, 93–130.

Carey, M., Post, M., & Sharpe, S. A. (1998). Does corporate lending by banks and finance companies differ? Evidence on specialization in private debt contracting. The Journal of Finance, 53(3), 845–878. https://doi.org/10.1111/0022-1082.00037.

Carpenter, M.A., Pollock, T.G., & Leary, M.M. (2003) Testing a model of reasoned risk‐taking: governance, the experience of principals and agents, and global strategy in high‐technology IPO firms. Strategic Management Journal, 24(9), 803–820.

Cavalluzzo, K. S., Cavalluzzo, L. C., & Wolken, J. D. (2002). Competition, small business financing, and discrimination: evidence from a new survey. The Journal of Business, 75(4), 641–679. https://doi.org/10.1086/341638.

Chakravarty, S., & Xiang, M. (2013). The international evidence on discouraged small businesses. Journal of Empirical Finance, 20, 63–82. https://doi.org/10.1016/j.jempfin.2012.09.001.

Chakravarty, S., & Yilmazer, T. (2009). A multistage model of loans and the role of relationships. Financial Management, 38(4), 781–816.

Chandler, V. (2010). An interpretation of discouraged borrowers based on relationship lending working paper (working paper no. Iu188- 102/2010E- PDF). Ottawa, Ont.: Industry Canada, small business and tourism branch.

Cole, R., & Sokolyk, T. (2016). Who needs credit and who gets credit? Evidence from the surveys of small business finances. Journal of Financial Stability, 24, 40–60. https://doi.org/10.1016/j.jfs.2016.04.002.

Cosh, A., Cumming, D., & Hughes, A. (2009). Outside entrepreneurial capital. The Economic Journal, 119(540), 1494–1533. https://doi.org/10.1111/j.1468-0297.2009.02270.x.

Cowling, M., Liu, W., Minniti, M., & Zhang, N. (2016). UK credit and discouragement during the GFC. Small Business Economics, 47(4), 1–26. https://doi.org/10.1007/s11187-016-9745-6.

Deakins, D., & Freel, M. S. (2009). Entrepreneurship and small firms. McGraw-Hill College.

Ferrando, A., & Mulier, K. (2015). The real effects of credit constraints: evidence from discouraged borrowers in the euro area (Working paper No. 1842). European Central Bank.

Freel, M. S. (2007). Are small innovators credit rationed? Small Business Economics, 28(1), 23–35. https://doi.org/10.1007/s11187-005-6058-6.

Freel, M., Carter, S., Tagg, S., & Mason, C. (2012). The latent demand for bank debt: characterizing “discouraged borrowers.”. Small Business Economics, 38(4), 399–418. https://doi.org/10.1007/s11187-010-9283-6.

Gama, A. P. M., Duarte, F. D., & Esperança, J. P. (2017). Why discouraged borrowers exist? An empirical (re)examination from less developed countries. Emerging Markets Review. https://doi.org/10.1016/j.ememar.2017.08.003.

Han, L., Fraser, S., & Storey, D. J. (2009). Are good or bad borrowers discouraged from applying for loans? Evidence from US small business credit markets. Journal of Banking & Finance, 33(2), 415–424. https://doi.org/10.1016/j.jbankfin.2008.08.014.

Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47(1), 153–162. https://doi.org/10.2307/1912352.

Kon, Y., & Storey, D.J. (2003) A theory of discouraged borrowers. Small Business Economics, 21(1), 37–49.

Lee, N. (2014). What holds back high-growth firms? Evidence from UK SMEs. Small Business Economics, 43(1), 183–195. https://doi.org/10.1007/s11187-013-9525-5.

Levenson, A., & Willard, K. (2000). Do firms get the financing they want? Measuring credit rationing experienced by small businesses in the U.S. Small Business Economics, 14(2), 83–94.

Moro, A., & Fink, M. (2013) Loan managers’ trust and credit access for SMEs. Journal of Banking & Finance, 37(3), 927–936

Nightingale, P., & Coad, A. (2014). Muppets and gazelles: political and methodological biases in entrepreneurship research. Industrial and Corporate Change, 23(1), 113–143. https://doi.org/10.1093/icc/dtt057.

Petersen, M., & Rajan, R. (1994). The benefits of lending relationships: evidence from small business data. The Journal of Finance, XLIX(1), 3–37.

Riding, A., Orser, B. J., Spence, M., & Belanger, B. (2012). Financing new venture exporters. Small Business Economics, 38(2), 147–163. https://doi.org/10.1007/s11187-009-9259-6.

Robb, A., & Wolken, J. D. (2002). Firm, owner, and financing characteristics: differences between female- and male-owned small businesses (Working paper No. Federal Reserve working paper series: 2002–18). Washington D.C.: Federal Reserve. Retrieved from http://www.ssrn.com/abstract=306800

Robb, A.M., & Robinson, D.T. (2014) The capital structure decisions of new firms. The Review of Financial Studies, 27(1), 153–179.

Rostamkalaei, A., & Freel, M. (2017). Business advice and lending in small firms. Environment and Planning C: Politics and Space, 35(3), 537–555. https://doi.org/10.1177/0263774X16665620.

Shane, S. (2009). Why encouraging more people to become entrepreneurs is bad public policy. Small Business Economics, 33(2), 141–149. https://doi.org/10.1007/s11187-009-9215-5.

Stinchcombe, A., & March, J. (1965). Social structure and organizations. Advances in Strategic Management, 17, 229–259.

Vos, E., Yeh, A. J.-Y., Carter, S., & Tagg, S. (2007). The happy story of small business financing. Journal of Banking & Finance, 31(9), 2648–2672. https://doi.org/10.1016/j.jbankfin.2006.09.011.

Wiklund, J., & Shepherd, D. (2003). Aspiring for, and achieving growth: the moderating role of resources and opportunities*. Journal of Management Studies, 40(8), 1919–1941.

Wynant, L., & Hatch, J. (1991). Banks and small business borrowers : a 1990 research study. London, Ontario: Western Business School, University of Western Ontario.

Xiang, D., Worthington, A. C., & Higgs, H. (2015). Discouraged finance seekers: an analysis of Australian small and medium-sized enterprises. International Small Business Journal, 33(7), 689–707. https://doi.org/10.1177/0266242613516138.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Rights and permissions

About this article

Cite this article

Rostamkalaei, A., Nitani, M. & Riding, A. Borrower discouragement: the role of informal turndowns. Small Bus Econ 54, 173–188 (2020). https://doi.org/10.1007/s11187-018-0086-5

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-018-0086-5