Abstract

A major shortcoming of capital structure studies on developing economies is that they generally restrict their analyses to large publicly-traded manufacturing firms. Consequently, we know little about the applicability of various capital structure theories to firms that are private, small, and/or outside the manufacturing industry in these economies. In this paper, we conduct a comparative test of the trade-off and pecking order theories using a comprehensive firm-level dataset that covers manufacturing, non-manufacturing, small, large, publicly-traded, and private firms in a major developing economy, Turkey. The trade-off theory provides a better description of the capital structures of all firm types than the pecking order theory. Moreover, the trade-off theory appears to be particularly suitable for understanding the financing choices of large private firms in the non-manufacturing sector and when the economic environment is relatively stable. By contrast, pecking order theory is most useful when it comes to small publicly-traded manufacturing firms, especially when the economic environment is relatively unstable.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Ever since the publication of Modigliani and Miller (1958)’s “irrelevance proposition”, there has been extensive theoretical work on the determinants of firms’ capital structures. Already by the early 1980s, these efforts culminated in the development of the two major theories of capital structure. In the (static) trade-off theory, firms trade off tax savings from debt financing against deadweight costs of possible bankruptcy. The pecking order theory, on the other hand, posits that, due to adverse selection, firms prefer internal to external financing and debt to equity if external financing is used. Even though neither theory is completely satisfactory, they have been instrumental in identifying many of the factors that govern firms’ actual financing decisions.

Beginning with the mid-1980s, there has been an outpouring of empirical research aimed at comparing and contrasting the predictive powers of the major theories of capital structure, often formulated as a contest between the trade-off theory and the pecking order theory. While the earlier work concentrated on the developed economies, particularly the United States, a major preoccupation of recent research has been to test these theories in the context of developing economies. The evidence coming from both the developed and developing economy capital structure studies thus far is decidedly mixed; while some studies provide support for the trade-off theory, others lend support for the pecking order theory. Often, studies report conflicting findings even for a given country. In the quest for resolving the contest between the trade-off and pecking order theories, researchers have subsequently taken a variety of routes that include modifying and/or improving the existing theories, developing new theories, and using better data and/or methods. Despite considerable progress, the issue is yet to be settled, both for developed and developing economies, and more so for the latter.

A major shortcoming in developing economy capital structure studies, including Turkey, is that they generally restrict their analyses to manufacturing firms listed on the stock exchanges, which incidentally tend to be relatively large firms. As such, these studies cannot speak to the capital structure choice of the average (or typical) non-financial firm, nor do they inform us about the capital structure choices of firms that are privately-held, firms outside the manufacturing industry, or firms that are relatively small. This also implies that, by design, comparative tests of the theory in such studies can be informative only in the specific context of large public manufacturing firms.

In this paper, we contribute to the capital structure literature on developing economies by investigating the capital structure choices of Turkish non-financial firms and also by doing a comparative test of the trade-off and pecking order theories. Our study differs from previous studies in that we utilize a unique and comprehensive dataset compiled by the Central Bank of the Republic of Turkey (CBRT) that provides financial information on small, large, public, private, manufacturing as well as non-manufacturing non-financial firms in Turkey for the past 20 years. The fact that our dataset is substantially more comprehensive in terms of firm types as well as leverage determinants suggested by theory compared to the datasets used in previous studies enables us to conduct a number of systematic analyses which, to our knowledge, are new in the context of capital structure research on developing economies. Specifically, since our dataset is considerably more representative of the universe of Turkish non-financial firms, it enables us to take a much more accurate picture of the capital structure of the average Turkish non-financial firm. It also allows us to investigate systematically the capital structure differences between firms of various kinds: manufacturing versus non-manufacturing firms, small versus large firms, and public versus private firms. Accordingly, we are able to carry out a considerably more comprehensive comparative test of the trade-off and pecking order theories than previous studies.

The extant literature reviewed in Sect. 2 has identified several factors that are correlated with firm leverage in both developed and developing countries. Following this body of work, we investigate concurrently the influences on leverage of four broad types of variables: Firm-specific, tax-related, industry-specific, and macroeconomic. Several results emerge from our empirical analysis. In particular, we find that, for the average Turkish non-financial firm, most of the independent variables have the signs that would be expected in light of previous theoretical work and the empirical findings obtained for other countries. Specifically, we provide evidence that leverage (short-term, long-term, and total) is positively correlated with firm size, potential debt tax shields, industry median debt ratios, and inflation, and negatively correlated with profitability, business risk, and real GDP growth. Asset tangibility is positively correlated with long-term and total leverage but negatively correlated with short-term leverage. Firm growth, on the other hand, does not seem to be related with firms’ leverage decisions. Our findings, therefore, confirm, from a capital structure point of view, the statistical relevance of tax-related, industry-related, and macroeconomic factors in addition to firm-level factors in the context of Turkish non-financial firms.

In addition to statistical significance, we analyze the economic significance of leverage determinants, a first in the capital structure literature on developing economies. Our findings indicate that each of the four broad types of leverage determinants does indeed play an economically important role in shaping the capital structure decisions of Turkish non-financial firms during our sample period. Specifically, we find that while potential debt tax shields are the most economically significant determinant of short-term and total leverage, tangibility is the most economically significant determinant of long-term leverage. Firm size is another major determinant of leverage, second only to tangibility and potential debt tax shields for long-term and total leverage, respectively. Industry median leverage and inflation also play a notable but smaller role when compared to firm size, profitability, tangibility, and tax-related determinants.

We next carry out a rare exercise in the literature on corporate capital structure in developing economies. Specifically, we investigate the capital structure differences between manufacturing and non-manufacturing, large and small, and public and private firms. One of our main findings is that regardless of their size, industrial membership, and stock market listing, firms’ short-term leverage is much larger than their long-term leverage. This indicates that short-term debt finance was and still is the norm for Turkish non-financial firms, which is not desirable both from economic efficiency and financial stability perspectives. We also find that while manufacturing firms have higher leverage (both short-term and long-term) than non-manufacturing firms, large firms and public firms have higher long-term leverage but lower short-term leverage than small firms and private firms, respectively. This implies that small private manufacturing firms are the firms with the greatest proportion of short-term debt in their capital structures. In addition to these differences in leverage patterns, firm types also differ in terms of how various determinants are related with leverage. The most significant differences appear to be neither between public and private firms nor between manufacturing and non-manufacturing firms but rather between small and large firms.

Another novel aspect of our paper is that we explore the implications of international capital flows for firms’ capital structures. Studying the capital structure implications of capital flows is interesting because capital flows exert, either directly or via domestic capital markets, a major influence on the availability and allocation of funds to various types of firms in many developing economies, including Turkey. Moreover, both the size and volatility of capital flows grew rapidly during the past two decades, particularly after the early 2000s, raising concerns over economic and financial stability in policy circles. Our results do in fact show that there is a strong positive correlation between capital flows and corporate leverage in Turkey, indicating that firms choose to intensify their usage of debt in response to a rise in the availability of foreign capital. Moreover, the debt-promoting effect of capital flows appears to be particularly strong during the dramatic rise in capital flows after the early 2000s. Our findings also indicate that capital flows influence the capital structures of different types of firms differently; increasing debt usage most in large private non-manufacturing firms.

On the whole, our empirical findings suggest that the trade-off theory is a better description of the capital structures of Turkish non-financial firms than the pecking-order theory. This contrasts sharply with the judgments of previous researchers on the Turkish economy, who typically take the opposite view. There are two main reasons behind this difference in judgments. First, our dataset is much larger (both within and across time) than the datasets used in past studies, which allows us to estimate the leverage effects of different leverage determinants much more precisely. Second, our dataset is much more comprehensive in terms of both firm types and leverage determinants, which enables us to do a much more comprehensive comparative test of the two theories. It is important to note the fact that our analysis of the relative economic significance of leverage determinants also strengthens the case for the trade-off theory.

Our findings also suggest where each of the two capital structure theories may be most fruitfully applied. In particular, we provide evidence that the trade-off theory is particularly successful in accounting for the capital structures of large private firms in the non-manufacturing sector. Moreover, the predictive power of the trade-off theory appears to be higher when the economic environment is relatively stable. Pecking order theory, on the other hand, although in our evaluation still not as powerful as the trade-off theory, appears to perform best for small public firms in the manufacturing sector and when the economic environment is relatively unstable.

The remainder of the paper proceeds as follows. Section 2 presents the links to the relevant theoretical and empirical literature on capital structure. Section 3 summarizes the hypotheses regarding the relationship between leverage and its determinants. Section 4 describes the data. Section 5 presents the main results and a number of robustness checks. Section 6 sheds light on the capital structure differences between firms of various types. Section 7 evaluates the predictive abilities of trade-off and pecking order theories in light of our empirical findings. Section 8 provides concluding remarks.

2 Main connections with the literature

The theory of corporate finance in a modern sense begins with the Modigliani and Miller (1958) theorem, which states that in a frictionless capital market a firm’s market value is independent of how it finances its operations. Subsequent research emphasized important departures from the Modigliani–Miller assumption of frictionless capital markets such taxes, transaction costs, agency costs, adverse selection, lack of separability between financing and operations, time varying financial market opportunities, and investor-clientele effects (Frank and Goyal 2008). These efforts led to the development of various capital structure theories, the two major theories being the trade-off and pecking order theories. Kraus and Litzenberger (1973) provides a classic statement of the theory that optimal capital structure reflects a single-period trade-off between the tax benefits of debt financing and the deadweight costs of potential bankruptcy. This standard version of the trade-off theory is referred to as the static trade-off theory.Footnote 1 The standard statement of the pecking order theory, on the other hand, is provided by Myers (1984) and Myers and Majluf (1984), according to which, firms follow a financing hierarchy in order to minimize the problem of asymmetric information between the firm’s insiders and the outsiders.

Thanks to the trade off, pecking order, and other theories, we now know a lot more about the factors that determine firms’ actual capital structure decisions. In particular, these theories have been helpful in identifying a large number of factors that seem to be correlated with firms’ debt ratios. Frank and Goyal (2009) lists as many as 36 variables that are correlated with the leverage decisions of U.S. firms (see, also, Harris and Raviv 1991). Empirical studies typically employ a variety of variables from this list that can be justified using any of the existing theoretical models.

Most of the earlier empirical research attempts to test various theories using the developed countries, mainly the United States, as a laboratory (e.g. Bradley et al. 1984; Taggart 1985; Pozdena 1987; Titman and Wessels 1988). In an influential study, Rajan and Zingales (1995) show that factors such as growth, size, profitability, and tangibility, which are correlated in the cross-section with firm leverage in the United States are similarly correlated in the other G-7 countries as well. Following Rajan and Zingales (1995), there has been an outpouring of empirical research on international comparisons of capital structure including, among others, Demirgüç-Kunt and Maksimovic (1996, 1999), Wald (1999), De Jong et al. (2008), and Antoniou et al. (2008). A particularly important study in this line of research has been Booth et al. (2001), which provides evidence that firms’ capital structure decisions in developing countries are affected by the same variables as in developed countries. Since at least the mid-1990s, there are also a growing number of studies that explore the determinants of capital structure in individual developing countries.Footnote 2

Our paper is most closely related to this last strand of literature since we analyze the capital structure of non-financial firms in a major developing economy, namely, Turkey.Footnote 3 This literature studies the capital structure choice of manufacturing firms listed on Borsa Istanbul (BIST) (as the Istanbul Stock Exchange is called since 2013) from various angles and for different time periods. There are three exceptions: Demirhan (2009) focuses on non-manufacturing firms on the ISE, Okuyan and Taşçı (2010) use a dataset compiled by Istanbul Chamber of Industry that provides information on the largest 1,000 manufacturing firms in Turkey, and Aydın et al. (2006) use the same dataset as ours but restrict themselves only to a descriptive analysis of firms’ capital structures. Cebenoyan et al. (1995) and Dinçergök and Yalçıner (2011), on the other hand, carry out comparative studies of Turkey, Greece, Canada, and the U.S., and of Turkey, Brazil, Argentina, and Indonesia, respectively, again using data on listed manufacturing firms.

In all empirical studies, including those on the Turkish economy, some of the findings turn out to be consistent with the trade-off theory and others with the pecking order theory.Footnote 4 One of the theories is judged to have greater explanatory power if more of the observed relationships are consistent with its predictions. What is clear, however, is that neither theory is uniformly better than the other theory. Therefore, our goal in this paper is to investigate the circumstances under which a given capital structure theory performs well, rather than look for “the theory” that captures reality in all possible circumstances. To achieve this goal, one must use a dataset that is comprehensive in terms of both firm types and leverage determinants suggested by theory. The dataset must also have a sufficiently long time span that will allow the researcher to analyze the effects of variations in the stability of the economic environment in which the firms operate. This is what we do in the present paper.

3 Hypothesis development

In this section, we develop the hypotheses about the nature of the relationships between leverage and various determinants through the lenses of the trade off and pecking order theories. Our discussion benefits, among others, from the reviews by Frank and Goyal (2008) and Harris and Raviv (1991). We first introduce our measures of leverage and then consider, in turn, firm-specific, tax-related, industry-specific, and macroeconomic determinants of leverage.

3.1 Measures of leverage

We consider three different measures of leverage: Short-term, long-term, and total debt over total assets. According to Rajan and Zingales (1995), this is a more appropriate measure of financial leverage than the ratio of liabilities (both short term and long term) to total assets because it provides a better indication of whether the firm is at risk of default any time soon and also a more accurate picture of past financing choices. Debt is classified as long-term if it has a maturity of at least 1 year and short-term otherwise.

Even though a complete analysis of debt maturity is beyond the scope of this paper,Footnote 5 it is still important for us to distinguish between short-term and long-term leverage for two reasons. First, the trade-off and pecking order theories sometimes have different implications for the different types of debt. Second, short-term debt carries a number of risks for the financial and economic health of a company. The main financial risk is the so called maturity risk (the potential lack of liquid assets at the time of repayment of the loan) which exposes the borrowing firm to potential rollover difficulties and interest rate fluctuations.Footnote 6 Moreover, the financial health of the corporate sector has serious implications for the health of the financial sector as well (Basel Committee on Banking Supervision 2011). On the other hand, when external finance is short term, it becomes more difficult for firms to improve their economic health by engaging in efficiency and capacity-enhancing investments. The fact that the majority of firms’ debt is short-term in developing economies (Demirgüç-Kunt and Maksimovic 1999) coupled with the weaknesses in institutional and financial infrastructures and the volatile nature of the economic environment imply that these risks are more pertinent for developing economies than more stable advanced economies. In fact, there is ample evidence that short term debt did play an important role in the crises of Mexico 1994–1995, East Asia 1997–1998, and Brazil 1998–1999 (Schmukler and Vesperoni 2006).

3.2 Determinants of leverage

3.2.1 Firm-specific determinants

Rajan and Zingales (1995) use four firm-specific independent variables in their study of capital structures: size, profitability, growth, and tangibility. Booth et al. (2001) add business risk to this list. We include all five firm-specific variables in our analyses.

3.2.1.1 Size

Trade-off theory predicts a positive relationship between firm size and leverage. This is because larger firms are more diversified and have lower default risk. The pecking order theory, on the other hand, is generally interpreted as predicting a negative relationship, since large firms face lower adverse selection and can more easily issue equity compared to small firms. An overwhelming majority of empirical studies finds a positive relation between leverage and size. Following Titman and Wessels (1988) and Rajan and Zingales (1995), among others, we define size as the natural logarithm of total sales, adjusted for inflation.Footnote 7

3.2.1.2 Profitability

Trade-off theory is generally interpreted as predicting a positive relation between firm profitability and leverage. This is because default risk is lower and interest tax shields of debt are more valuable for profitable firms. Pecking order theory, on the other hand, predicts a negative relation between leverage and profitability, as profitable firms can use earnings to fund investment opportunities and hence have less need for external debt. Empirical tests find the relation to be robustly negative. Following Titman and Wessels (1988) and De Jong et al. (2008), among others, we define profitability as operating income over total assets.

3.2.1.3 Tangibility

We use tangibility as a proxy for the type of assets. The trade-off theory predicts a positive relation between leverage and tangibility. This is because tangible assets are easier to collateralize and they suffer a smaller loss of value when firms go into distress. In addition, since firms tend to match the maturity of assets with that of liabilities (Stohs and Mauer 1996), tangibility should be positively correlated with long-term leverage. The pecking order theory, on the other hand, is generally interpreted as predicting a negative relation between leverage and tangibility, since the low information asymmetry associated with tangible assets makes the issuance of equity less costly (Harris and Raviv 1991). Empirical studies generally find a positive correlation between tangibility and total and long-term leverage. Following Rajan and Zingales (1995) and Demirgüç-Kunt and Maksimovic (1999), we define tangibility as the ratio of net fixed assets to total assets.

3.2.1.4 Growth

Trade-off theory predicts a negative relation between leverage and firm growth. Intangibility of the assets of growth firms implies that they lose more of their value in the event of financial distress. By contrast, the pecking order theory predicts a positive relation between leverage and growth. This is because internal funds are unlikely to be sufficient to support investment opportunities for high growth firms, which increases their demand for external debt. Although the results are mixed, most empirical work finds the relation between leverage and growth to be negative. Since our sample consists of both private and public firms, we cannot use market measures such as market-to-book ratios to proxy for growth. Our proxy is the percent change in sales as in Frank and Goyal (2009) and Schoubben and Van Hulle (2004).

3.2.1.5 Business risk

Both the trade-off and pecking order theories predict a negative relationship between leverage and business risk. The trade-off theory implies that the expected cost of financial distress increases with risk, at least for reasonable parameter values. In addition, the probability of wasting interest tax shields increases when earnings are less than tax shields (Frank and Goyal 2008). Both forces work to reduce leverage. From a pecking order perspective, business risk exacerbates the adverse selection between firms and creditors. Most empirical work finds a negative relation between leverage and risk. In this study, business risk is defined as the standard deviation of operating income over total assets over the past 3 years (including the current year) as in De Jong et al. (2008).

3.2.2 Tax-related determinants

The two tax-related determinants we consider are corporate taxes and non-debt tax shields.Footnote 8 These determinants naturally fit in with the trade-off theory.

3.2.2.1 Corporate taxes

Trade-off theory predicts a positive relationship between corporate tax rates and leverage. This is because features of the tax code allow interest payments to be deducted from the tax bill but not dividend payments, which provides a tax advantage for debt. The effect of taxes on debt ratios, however, has been difficult to clearly identify in the data and the available evidence is rather mixed (see, for example, Frank and Goyal 2008; Antoniou et al. 2008). One explanation for this might be the uncertainty about what would constitute a good proxy for tax effects. Another explanation is that transaction costs make it difficult to identify tax effects even when they are an element of the firm’s problem (Hennessy and Whited 2005).

3.2.2.2 Non-debt tax shields

DeAngelo and Masulis (1980) were probably the first to formally introduce the concept of non-debt tax shields to the literature. Examples of such shields include depreciation deductions, depletion allowances, and investment tax credits. These shields can be considered as substitutes for the corporate tax benefits of debt financing. Accordingly, firms with higher amounts of non-debt tax shields will choose to have lower levels of debt. Thus, the trade-off theory predicts a negative relationship between leverage and non-debt tax shields. More often than not, empirical studies find results that are supportive of this prediction.

Rather than including corporate taxes and non-debt tax shields separately in our analyses, we use a single indicator that simultaneously takes into account the presence of both effects. Whether a firm actually enjoys a positive tax advantage for debt financing depends on the trade-off between these two effects. Building on DeAngelo and Masulis (1980) and Titman and Wessels (1988), Shuetrim et al. (1993) propose a measure called the “potential debt tax shield (PDTS)” that captures the net effect of these two forces:

where \(I_{\text{it}}\) and \(T_{\text{it}}\) denote, respectively, interest payments and tax payments by firm i at time t and \(\tau_{t}\) denotes the statutory corporate tax rate at time t. PDTS is gross earnings minus non-debt tax shields and Shuetrim et al. (1993) show that it is equal to the sum of interest paid and taxable income after all non-debt tax deductions have been made as shown in the above expression.Footnote 9 They scale this sum by a firm’s total assets to get their final proxy of net tax shields. Note that when tax payments are zero (i.e. tax is exhausted), the relative proportions of income shielded by interest payments and by non-debt tax shields cannot be determined and hence PDTS is set to zero. In order to control for this possibility, we follow Shuetrim et al. (1993) and include firms’ state of tax exhaustion as a separate regressor in our analyses. It is a dummy variable that is equal to 1 for all observations when the tax paid by a firm is equal to zero. Its value can be interpreted as the mean effect of PDTS on leverage taken over all observations with zero tax payments. From a trade-off perspective, the predicted relation between this dummy variable and leverage is positive. Note that both PDTS and tax exhaust determinants can be calculated at the firm level.

3.2.3 Industry-specific determinants

The extant literature reviewed in articles such as Harris and Raviv (1991) and Frank and Goyal (2008) suggests that industry membership may be an important determinant of firms’ capital structures. According to Frank and Goyal (2009), this is mainly because industry reflects a number of otherwise omitted factors common to all firms. For example, supply and demand conditions or the extent of competition may differ from industry to industry. From a trade-off perspective, therefore, although imperfect, the industry median leverage is likely to be a proxy for firms’ target capital structure. Not entirely coincidentally, empirical evidence on industry effects is rather mixed. For instance, while Hovakimian et al. (2001) find that firms adjust their debt ratios towards industry median debt ratios, Mackay and Phillips (2005) provide evidence that there is significantly more variation in leverage within industries than across industries. For a given year, we define industry median leverage as the median of (short, long, or total) debt to total assets in that industry (that is, one for each of the two broad industry categories, manufacturing and non-manufacturing).

3.2.4 Macroeconomic determinants

Many studies including Deesomsak et al. (2004) and de Jong et al. (2008) show that the health and stability of the economic environment exert considerable effect on the firms’ capital structures. In order to explore the influence of the economic environment on firms’ capital structures, we include key macroeconomic variables in our analyses. Specifically, we include inflation and GDP growth as indicators of the general economic environment and the size of capital flows as an indicator of financial development.

3.2.4.1 Inflation

According to Taggart (1985), features of the tax code in the U.S. increases the real value of interest tax deductions on debt when inflation is expected to be high. Thus, the trade-off theory predicts a positive relationship between leverage and expected inflation. By contrast, it is hard to see why inflation would matter for firms’ leverage decisions in a model of pecking order (Frank and Goyal 2009). Empirical studies generally find a positive relation between leverage and inflation. In the absence of inflation expectations data that spans the whole sample period, we follow previous studies and use data on the realized inflation. Specifically, we use the percentage change in the annual consumer price index (CPI) as a rough proxy for expected inflation. It is important to note that the debt-bias in the U.S. tax system alluded to by Taggart (1985) is also a feature of the tax systems of many countries around the world, including that of Turkey.

3.2.4.2 GDP growth

Real Gross Domestic Product (GDP) growth can be viewed as a measure of the growth opportunities available to firms in an economy. In a high growth environment, the scarcity of firms’ tangible assets relative to available investment opportunities implies a higher loss of value when firms go into distress. Hence, the trade-off theory predicts a negative relation between leverage and GDP growth. By contrast, the pecking order theory predicts a positive relation between leverage and macroeconomic growth, since a high ratio of growth opportunities to internal funds would imply a greater need for external finance. Empirical studies generally find a negative association between leverage and macroeconomic growth (see, for example, Demirgüç-Kunt and Maksimovic 1996). Following common practice, we define GDP growth as the percent change in the annual real GDP.

3.2.4.3 Capital flows

Empirical studies such as Demirgüç-Kunt and Maksimovic (1996) and Antoniou et al. (2008), among others, provide evidence on the importance of capital markets for firms’ capital structures. The size and structure of capital markets play a key role in determining the availability and allocation of funds to various types of firms within an economy. Domestic capital markets, in turn, are heavily shaped by the flows of international capital in many developing economies, including that of Turkey (see, for example, Kose et al. 2009). While inflows of capital lead to increases in the size of domestic capital markets, outflows lead to declines. In order to study the impact of capital flows (and hence financial development) on firms’ capital structures, we include the ratio of net capital flows to GDP as an additional explanatory variable in our regression equations.

Table 1 summarizes the definitions of various leverage measures and leverage determinants as well as the theoretical predictions for the relations between the dependent and independent variables.

4 Data

Our firm- and industry-specific data come from the survey-based Sectoral Balance Sheets (SBS) dataset of the CBRT, which is the largest source of annual balance sheet and income statement data on Turkish non-financial firms.Footnote 10, Footnote 11 Our sample period covers the years 1996–2009. In our sample, there are on average about 9000 firms each year, of which roughly 2 percent are publicly traded firms. The sample includes nearly all large firms in Turkey as well as a large number of small and medium-sized enterprises (SMEs) and micro-sized firms.Footnote 12 Altogether our sample firms employ a total of about 1.5 million workers each year, accounting for roughly 11 % of employment in Turkey during 1996–2009.Footnote 13 This is substantially larger than the corresponding figure for non-financial firms listed on BIST during the same period (225 thousand workers), indicating that the SBS dataset is significantly more representative of the population of Turkish non-financial firms than BIST.

The two broad industry categories we use are ‘manufacturing’ and ‘non-manufacturing’. The manufacturing industry consists of 13 sub-industries (comprising roughly 53 % of all firms) whereas the non-manufacturing industry consists of 4 sub-industries (comprising roughly 47 % of all firms).Footnote 14 Our data on macroeconomic and tax-related variables, on the other hand, are collected from a variety of sources including SBS, BIST, Turkish Statistical Institute, Undersecretariat of Treasury of the Republic of Turkey, and World Development Indicators.

To minimize the effects of outliers in the data on our results, we use winsorization, in which the most extreme tails of the distribution are replaced by the most extreme value that has not been removed (Frank and Goyal 2008). Following common practice, we winsorize each tail at 0.5 percent. The final sample is an unbalanced panel of 11,726 firms with 74,155 firm-year observations. We do not have 14 years of data for all firms because each year some firms enter or exit the sample.Footnote 15

Table 2 presents the descriptive statistics for all of our variables during 1996–2009. The median is below the mean for all three debt ratios. The divergence between the mean and median debt ratios is larger for the long-term debt ratio as the majority of firms have little to no long-term debt. Moreover, firm growth rates have the largest variance, with the mean significantly greater than the median.

5 Empirical model and results

In this section, we present our empirical model, discuss the main results, and perform a number of robustness checks.

5.1 Empirical model

We model leverage as a function of various determinants discussed in the previous section. Specifically, we estimate the following fixed effects panel data model:

where \(L_{\rm it}\) is one of the three measures of leverage (short, long, or total leverage) of firm i in year t; \(F\) is the vector of the four types of leverage determinants (firm-specific, tax-related, industry-specific, and macroeconomic determinants); \(\mu_{i}\) are the time-invariant unobservable firm-specific effects; and \(\varepsilon_{it }\) is the error term. We estimate Eq. (1) using standard errors that are robust to heteroskedasticity and serial correlation. We calculate robust standard errors using Newey and West (1987)’s variance estimator which produces consistent estimates when there is heteroskedasticity and autocorrelation in standard errors.

5.2 Results

Table 3 presents the results from estimating Eq. (1). In what follows, we summarize the results and evaluate them in light of theoretical hypotheses and previous empirical findings.

5.2.1 Firm-specific determinants

The first five rows of Table 3 display the estimated coefficients for our firm-specific determinants. The coefficients of size, profitability, and tangibility are significant at the 1 % level in all leverage equations. Size is positively associated with all three debt ratios, suggesting that ceteris paribus large firms have more debt in their capital structures. By contrast, the relation between profitability and various debt ratios is negative, implying that more profitable firms have lower debt ratios. While our result on size is consistent with the prediction of trade-off theory, our result on profitability is consistent with the pecking order theory. These findings are also in line with the empirical evidence found in previous studies.

Tangibility is negatively associated with short-term leverage but positively associated with long-term and total leverage. Thus, firms with more tangible assets tend to have more long-term and less short-term debt in their capital structure. The fact that the signs of the estimated coefficients of the tangibility determinant are opposite in the short- and long-term leverage equations can be interpreted as evidence that firms in Turkey match the maturity of their assets with their liabilities. Demirgüç-Kunt and Maksimovic (1999) report similar findings in their sample of nineteen developed and developing countries (Turkey is included) and Gönenç (2003) for industrial firms listed on the ISE. Overall, the results are consistent with the prediction of trade-off theory but not with the pecking order theory.

Finally, while firm growth appears to be unrelated with leverage, the estimated coefficient of our business risk variable is significantly negative in the long-term and total leverage equations. So, increases in a firm’s riskiness reduce the level of long-term debt in its capital structure but does not have a significant effect on the level of short-term debt relative to total assets. This is consistent with the view that firms that are viewed as risky by creditors find it more difficult to borrow long-term (see, for example, Diamond 1991 or Demirgüç-Kunt and Maksimovic 1999). Our results concerning the business risk determinant can be understood within the framework of either trade-off or pecking order theories.

5.2.2 Tax-related determinants

The upper middle section of Table 3 presents the estimated coefficients for our PDTS and tax exhaustion variables. The coefficients of both variables are significant at the 1 percent level in all leverage equations and have the signs predicted by the trade-off theory. The positive and significant coefficient on PDTS suggests that the tax advantage of debt is greater than the tax advantage due to non-debt shields. The positive and significant coefficient on the tax exhaustion dummy, on the other hand, indicates that the tax distortions caused by the tax system are also important for firms that pay no tax.

5.2.3 Industry-specific determinants

The lower middle section of Table 3 presents the estimated coefficients for our industry median debt ratios. The coefficient of industry median leverage is positive and highly significant in all three leverage equations. Moreover, the association appears to be quantitatively strong: A 10 percentage point increase in the industry median short-term, long-term, and total leverage increases the average firm’s short-term, long-term, and total leverage by 3.29, 4.23, and 2.34 percentage points, respectively. From a trade-off perspective, these findings can be interpreted as evidence of target adjustment behavior in leverage.

5.2.4 Macroeconomic determinants

The bottom section of Table 3 presents the estimated coefficients for our macroeconomic determinants. In all equations, inflation is positively related with leverage and with coefficients that are significant at 1 percent. Therefore, firms’ indebtedness increases with inflation. This finding is consistent with the trade-off theory in which, given the tax-deductibility of nominal interest payments, an inflation-induced increase in nominal interest rates increases the tax advantage of debt financing. In addition, the impact of inflation appears to be quite strong: The fact that inflation has come down from over 80 percent to less than 10 percent between 1996 and 2009 would suggest roughly a 5 percent decline in the average firm’s total leverage due solely to the fall in inflation, all else equal.

On the other hand, the coefficient on GDP growth is negative and highly significant in the long-term and total leverage equations, but not the short-term leverage equation. One explanation of this finding might be that the scarcity of firms’ tangible assets relative to available investment opportunities is exacerbated in a high growth environment. The implied higher loss of value in the event of a distress, in turn, reduces firms’ ability to raise longer-term debt. Put differently, creditors reduce the amount of long-term debt they extend because it allows them to review the firms’ decisions more frequently and, if necessary, to vary the terms of financing before sufficient losses have accumulated to make default by the borrower optimal (Diamond 1991 and Demirgüç-Kunt and Maksimovic 1999). Overall, our findings on inflation and GDP growth appear to be consistent with the trade-off theory.

Finally, capital flows are positively and highly significantly correlated with all three measures of leverage, indicating that capital flows do in fact play an important role in shaping firms’ capital structures. Consistent with expectations, measures of leverage rise with inflows of capital and fall with outflows. While capital inflows are in principle beneficial for developing economies, particularly for those with low saving rates such as Turkey,Footnote 16 they can also lead to economic overheating, excessive currency appreciation, or pressures in particular sectors of the economy, such as sectoral credit booms or asset price bubbles (Ostry et al. 2011). In particular, rapid growth in private indebtedness induced by capital inflows might be characteristic of the early stages of financial instability (Mishkin 1997) and might cause banking crises (Reinhart and Rogoff 2011). Our results, therefore, indicate that the surge in international capital flows since the early 2000s, which were only briefly interrupted by the global financial crisis, continue to pose serious risks to economic and financial stability. Reflecting these concerns, policymakers in many developing economies have been very keen on finding appropriate ways to deal with the adverse effects of capital flows, particularly in the aftermath of the crisis. For example, Brazil and South Korea have chosen to implement capital control measures whereas Turkey and Indonesia have preferred macroprudential measures.

5.3 Economic significance of leverage determinants

In the previous subsection, we investigated whether a given leverage determinant, holding other determinants constant, was statistically significant in accounting for various debt ratios. However, statistical significance need not imply economic significance. In order to study the relative economic significance of various leverage determinants, we standardize all variables and rerun our regressions. Now, the estimated standardized coefficients show the impact of a one standard deviation change in an independent variable on the dependent variable. Accordingly, the magnitudes of the standardized coefficients are comparable across different leverage determinants for a given leverage equation (short-term, long-term, or total leverage). The left panel of Table 4 reports these results. The right panel of Table 4 sorts the leverage determinants according to their economic significance, where the ordering is based on the absolute value of the standardized coefficients.

The results indicate that PDTS, our tax-shield measure, is the most economically significant determinant for firms’ total leverage, with size a very close second. A one standard deviation increase in PDTS increases total leverage by 0.1595 standard deviations. PDTS is also the most important determinant for short-term leverage, followed by profitability. For long-term leverage, tangibility is by far the most economically important determinant, followed by size. Tax exhaust is consistently among the top three important determinants.

A few general lessons can be drawn from these results. Tax-related determinants are overall the most economically significant leverage determinants, suggesting that they in fact do play an important role in shaping firms’ capital structures. This finding is particularly interesting in light of the fact that tax effects on leverage have historically been notoriously difficult to detect in the data. A close second in terms of economic significance is firm-specific determinants such as size, tangibility, and profitability, while business risk and firm growth play little or no role. Industry median leverage, on the other hand, appears to have a fairly important influence on firms’ leverage decisions. Macro-level determinants generally score lower than firm-level (i.e. tax-related and firm-specific) determinants and industry-level determinants in the economic significance rankings, which is perhaps not surprising given that they have only a single observation per year. Among the macro-level determinants, inflation stands out both in terms of statistical and economic significance, even surpassing in ranking the industry median debt ratio in the total leverage equation. The only case in which inflation is not the highest ranking macro-level determinant is the long-term leverage equation, where it is second only to GDP growth and only by a small margin. These findings are particularly important in light of the fact that inflation in Turkey has only recently come down to single digits after decades of extremely high levels.

A second general lesson is that the economic importance of a given leverage determinant is different for different measures of leverage. For example, while tangibility appears to be a key determinant of long-term leverage, it is not as important for short-term leverage. A third and final lesson is that leverage determinants that are more closely associated with the trade-off theory such as tax-related determinants and size generally have higher rankings (in addition to having the correct signs and higher levels of statistical significance as shown in Sect. 5.2) than those that are more closely associated with the pecking order theory such as profitability. The evidence in favor of the trade-off theory is particularly strong for the long-term and total debt ratios.

5.4 Robustness checks

We perform a number of checks to confirm that our results are robust.Footnote 17 First, it doesn’t matter whether the data are winsorized or not; estimated coefficients are qualitatively and quantitatively very similar. This suggests that outliers in our dataset are not a significant problem for estimates.

Second, the fact that some firms in our dataset enter or exit the sample might potentially induce attrition bias in our estimations. To see if this is the case, we also estimate our empirical model only for those firms that have data for T years or more, where T = 2, 3,…,14 (T = 1 corresponds to the full sample results we report in Sect. 5.2). We find no evidence of the impact of attrition bias on our results.

Third, all the variables (i.e. dependent as well as independent) in our estimations are measured in year t, as is typically done in the capital structure literature. Nevertheless, in order to take the possibility that year t − 1 determinants are more relevant than year t determinants for a firm’s capital structure in year t, we re-estimate our equations this time replacing the current values of our independent variables with the lagged values. According to the results we do not report here, the results are qualitatively virtually the same as before, suggesting that from a capital structure perspective the information contents of year t and year t − 1 independent variables are qualitatively quite similar.

Fourth, apart from the net capital inflow, the supply of domestic capital can in principle also affect firms’ capital structure decisions. In order to explore this possibility, we also included as independent variables the size of debt markets (domestic credit to the private sector over GDP), the size of equity markets (stock market capitalization over GDP), and the size of government debt (total government debt over total domestic non-financial debt) in our regression equations. We find that the size of debt markets is positively correlated with long term leverage (at 5 percent significance level) and negatively correlated with short-term leverage (at 10 percent significance level). So, the deepening of debt markets appears to reduce firms’ short-term leverage while increasing long-term leverage. This finding is not surprising given the fact that banks have a comparative advantage in the provision of long-term debt. Second, unsurprisingly, we find that the size of equity markets is negatively correlated with all measures of leverage and its coefficients are highly significant (at the 1 percent level). Finally, we find that the size of government borrowing is unrelated with firms’ leverage decisions, suggesting that government borrowing does not crowd out private borrowing during our sample period. Unreported results also indicate that the relationships between leverage and the rest of the independent variables are both quantitatively and qualitatively very similar to the previous case.

Finally, we split the sample into two seven-year periods, namely, 1996–2002 and 2003–2009, to test for any structural breaks in the firms’ capital structure choices. Footnote 18 The results displayed in Table 5 indicate that firm-specific and tax-related leverage determinants generally have the same pattern of signs and significance as those we obtained for the full sample. The only significant change here is that the coefficient of firm growth turns significant in the short-term leverage equation in the 2003–2009 subsample, perhaps reflecting the improved growth prospects during this period. It is also interesting to note that the relative magnitude of the coefficient on tax exhaust (PDTS) is larger in the former (latter) period, which suggests that the tax distortions caused by the tax system during the earlier period are larger (smaller) for firms that pay no tax (pay tax). Also, the coefficient of business risk in the short-term leverage equation turns significant in the 1996–2002 subsample, most likely a reflection of the volatile state of the economy during this period. Finally, there are some changes in the signs and significance of some of the industry-level and macro-level determinant coefficients.Footnote 19 Specifically, the coefficient of industry median debt ratio turns insignificant in the long-term leverage equation in both subsamples and there is a loss of significance in the coefficients of inflation, GDP growth, and capital flow variables. In the case of capital flows, the contrast is particularly stark, where the coefficient is significant only in the 2003–2009 subsample, most likely reflecting the surge in capital inflows during this period. Overall, our results indicate that the predictive power of the trade-off theory is higher in the 2003–2009 period, during which the economic environment in Turkey was substantially more stable.

6 Capital structures of firms in various circumstances

Although both the trade-off theory and the pecking order theory have their strengths and weaknesses, our analysis thus far indicates that the former provides a considerably better framework than the latter to understand the capital structure of the average Turkish non-financial firm. However, as Myers (2003) argued, different factors might affect different types of firms in fundamentally different ways. To see if this is the case, we now systematically investigate the capital structure differences of three main types of firms: manufacturing versus non-manufacturing firms, large versus small firms, and public versus private firms. These exercises can also be viewed as additional robustness checks on our main results in Sect. 5.

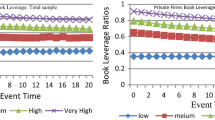

Figure 1 displays the ratios of short-term, long-term, and total indebtedness by industry membership, firm size, and stock market listing averaged over the whole sample period. Panel A of Fig. 1 shows that while manufacturing firms generally have higher debt ratios than non-manufacturing firms, the difference is more apparent in the short-term debt ratios. In Panel B of Fig. 1, firms are divided into quartiles by value of total assets and the average debt ratios of the smallest 25 %, the largest 25 %, and those in between are reported. This panel shows that larger firms have higher long-term leverage and lower short-term leverage than smaller firms. By contrast, there do not appear to be differences in total debt ratios across firm-size quartiles. Finally, Panel C shows that, overall, public firms are less levered. The figure also shows that public firms have higher long-term and lower short-term debt ratios than private firms, but that the difference is larger in the former. This appears to be due mainly to improved profitability (as we will see momentarily) and better access to equity markets, which allows public firms to substitute the debt in their capital structure with internal and external equity, respectively. However, improved access to debt markets allows public firms to also improve the maturity of debt in their capital structure.

Patterns of leverage for different types of firms. Panels a–c of this figure display the ratios of short-term, long-term, and total debt to total assets, respectively, by industry, firm size, and stock market listing averaged over the entire sample period. In panel b firms are divided into quartiles by value of total assets. A firm is classified as “small” if it is below the first quartile, “medium” if it is between the first and third quartiles, and “large” if it is above the third quartile

Examining panels A, B, and C of Fig. 1 simultaneously, we also determine a number of general themes. Specifically, we observe that regardless of firm size, industry, or stock market listing, firms’ short-term leverage is much higher than their long-term leverage, implying that the majority of firms’ debt is short-term. This seems to be particularly true for small private manufacturing firms. By contrast, large public manufacturing firms have the highest levels of long-term debt ratios, indicating that the usage of long-term debt is most pronounced in such firms.

6.1 Manufacturing firms versus non-manufacturing firms

As discussed previously in Sect. 3, industry membership may be an important determinant of firms’ capital structures. In order to investigate in detail the capital structure implications of industry membership, we re-run regressions separately for manufacturing and non-manufacturing firms. The results displayed in Table 6 suggest that manufacturing and non-manufacturing firms are in general quite similar in terms of their capital structures. Importantly, there are no material differences in the relations between debt ratios and the determinants that we identified in Sect. 5.3 as the most economically important such as size, profitability, tangibility, tax-related determinants, and inflation.

The few small differences relate to the remaining less economically important determinants. For instance, while firm growth is positively associated with long-term leverage for manufacturing firms (consistent with the pecking order theory), it is negatively correlated with short-term leverage for non-manufacturing firms (consistent with the trade-off theory). Also, comparison of the magnitudes of coefficients suggests that the debt ratios of manufacturing firms respond more to changes in size and profitability than non-manufacturing firms. The most striking difference relates to the impact of capital flows, however. In particular, the coefficient on capital flows is both much more significant and considerably larger in the non-manufacturing equations. This finding might suggest that international capital has tended to flow remarkably more to the sectors outside manufacturing, thereby influencing the financing patterns of the firms in such sectors to a greater extent during our sample period.

Overall, our findings on the relationships between leverage and various determinants appear to be more in line with the predictions of trade-off theory than with the pecking order theory, particularly in the case of non-manufacturing firms.

6.2 Large firms versus small firms

Previous research (e.g. Maksimovic and Zechner 1991, and Demirgüç-Kunt and Maksimovic 1999) provides evidence that small firms may follow financial policies that differ from those of large firms due to differences in, among other things, technology and access to financial markets and institutions. To see if this is the case, we re-run our regressions separately for the smallest and largest firms. Results displayed in Table 7 suggest that there are marked differences across firm sizes in how various determinants are related with debt ratios.

At the firm level, the most striking differences are in the effects of firm size and business risk variables. Specifically, for small firms, the association between leverage and size is relatively weak. In fact, firm size appears to become relevant for leverage decisions only when a firm is sufficiently large. This may be indicative of a “threshold effect” in size in the sense that marginal changes in the size of firms smaller than a certain threshold have little effect on such firms’ ability to raise external debt. The business risk variable, on the other hand, is highly significant in all leverage regressions for small firms but always insignificant for large firms. Thus, while small firms’ ability to raise debt seems very sensitive to their riskiness, large firms’ access to debt is not hindered by that at all. Finally, the debt ratios of large and small firms appear to be affected differently by firm growth rates. Specifically, while firm growth is not related with leverage for small firms, there is some evidence that short-term and total leverage go down with firm growth for large firms.

Our results in Table 7 also suggest that there are interesting differences between large and small firms in how industry-related and various macroeconomic determinants are related with debt ratios. For example, the coefficient on industry median leverage is much more significant and remarkably larger for large firms, suggesting that target adjustment is a much more pertinent phenomenon among large firms. One explanation of this finding could be that there are fundamental technological differences between small and large firms and hence naturally follow different financial policies a la Maksimovic and Zechner (1991). Or, as shown by Demirgüç-Kunt and Maksimovic (1999) and World Bank Group (2010), it could reflect differences between small and large firms in access to external finance, which prevent small firms from following an optimal financial policy.

With respect to macro-level determinants, the most striking difference between large and small firm capital structures is in inflation. Specifically, while inflation does not seem to be related with the leverage decisions of small firms, large firms’ leverage increases with inflation. This might suggest that, once the direct leverage impact of taxes is taken into account, inflation does not induce a further tax benefit for debt financing for small firms. Capital flows also appear to influence large and small firms differently, with capital flows having a remarkably greater importance for the leverage decisions of large firms. This might be explained by the fact that large firms are more diverse and informationally more transparent than small firms, which increases their ability to secure funds from domestic sources as well as directly from foreign sources. Finally, the association of leverage and GDP growth seems to be significantly stronger in the case of large firms, likely reflecting the fact that large firms are usually better equipped to capture the benefits of economic growth.

Overall, our findings on the relationships between leverage and various determinants appear to be more in line with the predictions of trade-off theory than with the pecking order theory, particularly in the case of large firms.

6.3 Publicly-traded firms versus private firms

Stock markets play a key role in managing conflicts of interest between various stakeholders in a firm, provide entrepreneurs with opportunities to diversify their portfolios, and transmit information about firms’ prospects to potential investors and creditors (see, for example, Allen, 1993, and Demirgüç-Kunt and Maksimovic 1996). As a result, compared to their private counterparts, public firms enjoy improved access to financial markets in terms of both debt and equity. This implies that whether a firm is privately-held or publicly-traded can have an important influence on the firm’s capital structure decisions.

In this subsection, we explore the capital structure differences between public and private firms. Toward this end, we re-run our capital structure regressions separately for public and private firms. The results are displayed in Table 8. The first thing that strikes the eye in Table 8 is that the estimated coefficients in the private firm regressions are qualitatively and quantitatively almost the same as those in the full-sample results reported in Sect. 5. This is probably not surprising in light of the fact that nearly 98 percent of the firms in our sample are private firms.

Table 8 also shows that there are as many differences as there are similarities between public and private firms in how various determinants are related with debt ratios. At the firm level, the most important differences are in the leverage effects of firm growth and business risk. In particular, while firm growth is not related with leverage for private firms, it is positively correlated with short-term leverage for public firms, a finding consistent with the pecking order theory. Also, in stark contrast with the case for private firms, business risk appears to be positively correlated with all measures of leverage for private firms, although the correlation is significant only in the total leverage equation and only at the 10 % level. Thus, unlike the private firms, business risk does not appear to impair the ability of public firms to secure debt, most likely reflecting reputational effects and/or the presence of alternative funding sources available to public firms. Also worth noting is the fact that the coefficients on profitability are quantitatively much larger in public firm equations, suggesting that public firms can (due to higher profitability) increase the use of internal equity to a greater extent in their capital structures than private firms.

There are also interesting differences between public and private firms in how debt ratios are related with industry median leverage. In particular, while industry median leverage is positively correlated with long-term leverage for both types of firms, it is negatively correlated with short-term leverage for public firms. Therefore, it can very well be the case that improved access to financial markets in general, and debt markets in particular, may be allowing public firms to reduce short-term debt and increase long-term debt in their capital structure. This improvement in the public firms’ maturity structure of debt manifests itself as a strong adjustment towards the industry median in long-term leverage coupled with a “negative” adjustment in short-term leverage.

Last but certainly not least, there is a sharp contrast between the impact of capital flows on the debt ratios of public firms and that of private firms. Specifically, while capital flows are positively correlated with leverage in all three equations for private firms, they appear to have no relation with the leverage choices of public firms. There might be a number of different explanations for this rather interesting finding. First, it might be that public firms already have nearly unlimited access to financial markets, domestic and foreign alike. If this is the case, then changes in the size and direction of capital flows would leave the capital structures of public firms unaffected. A second explanation could be that public firms are much more profitable than private firms. The availability of large internal resources, in turn, makes them less dependent on external finance and limits the impact of fluctuations in the availability of external finance on their capital structure choices.Footnote 20

At this point, it may be worthwhile to digress a little and summarize our findings on capital structure effects of international capital flows in light of our previous findings. We have the following facts. First, the impact of capital flows, if any, is to increase the proportion of debt (generally both short-term and long-term) in firms’ capital structure. Second, the importance of capital flows for firms’ capital structure decisions are considerably more apparent after the early 2000s, a period during which capital inflows to Turkey soared. Third, capital flows have a greater influence on the capital structures of (1) non-manufacturing firms compared to manufacturing firms, (2) large firms compared to small firms, (3) private firms compared to public firms, and in unreported results which are available upon request (4) mature firms than young firms. Put together, these findings suggest that the leverage-increasing impact of capital flows is most significant for large, mature, private, non-manufacturing firms after the early 2000s in Turkey. This result is in line with the findings of Falkenstein (1996) and Gompers and Metrick (2001) who find that international investors invest more in large and mature firms, and UNCTAD (2004) and Doytch and Uctum (2011) who show that in developing economies, there has been a large increase in the amount of foreign investment in services relative to that of manufacturing from the 1990s to the 2000s

Overall, our analyses of the public firm—private firm distinction suggest that the relationships between leverage and various determinants are more in line with the predictions of trade-off theory than with the pecking order theory. However, the support for the trade-off theory is weaker and that for the pecking order theory is somewhat stronger than before in the case of public firms. To see this, note that the coefficients on firm size in the long-term leverage equation as well as on tangibility in the total leverage equation are no longer significant, which are inconsistent with the trade-off theory. Furthermore, the coefficient on firm growth in the short-term leverage equation is now positive and borderline significant, which is consistent with the pecking order theory. Finally, although the coefficient of industry median is still positive in the long-term leverage equation, it is significantly negative in the short-term leverage equation, and insignificant in the total leverage equation, findings which are not entirely consistent with the trade-off theory.

7 Pecking order or static trade-off?

Which of the two major theories, pecking order and trade-off, is a better description of our findings? Our findings suggest that, on the whole, the trade-off theory provides a better account of the capital structure decisions of Turkish firms than the pecking order theory. Table 9 presents the predictions of the two theories alongside with our empirical findings. The table includes only those determinants for which at least one of the two theories has a prediction.

A simple comparison of the signs in Table 9 reveals that the trade-off theory has more correct predictions than the pecking order theory. The main advantage of pecking order theory over the trade-off theory is that it predicts the sign of profitability correctly. This is important because profitability is probably the only leverage determinant that has a robust (negative) association with leverage in the data in (nearly) all countries. Note, however, that a negative sign can also be rationalized in dynamic versions of the trade-off theory such as Fischer et al. (1989) and Hennessy and Whited (2005). On the other hand, the pecking order theory has difficulty accounting for the positive signs on size and tangibility as well as explaining the negative association between leverage and GDP growth. Perhaps as importantly, the theory does not generate predictions about some very key leverage determinants such as corporate debt tax shields, non-debt tax shields, and inflation for which the trade-off theory correctly predicts the nature of the association with leverage.

It is important to emphasize that our conclusion is in sharp contrast with the conclusions of previous capital structure studies on the Turkish economy in which the pecking order theory is often viewed as a better framework than the trade-off theory for understanding the capital structures of Turkish firms (see, for example, Acaravcı and Doğukanlı 2004; Korkmaz et al. 2007; and Yıldız et al. 2009). We have already alluded in the preceding paragraph to some of the reasons that may at least partly explain this divergence of conclusions. Some of the other main reasons can be uncovered by studying the capital structure differences between various types of firms. This becomes all the more important since almost all of the previous studies focus on public manufacturing firms whereas we consider a comprehensive and representative sample which includes manufacturing, non-manufacturing, small, large, public, and private firms. In our analyses, we have found that the trade-off theory is particularly successful (and pecking order theory particularly unsuccessful) in accounting for the capital structures of firms that are private, non-manufacturing, large, and/or mature. Pecking order theory, on the other hand, although in our evaluation still not as powerful as the trade-off theory, is at its best when it comes to public, manufacturing, small, and/or young firms.Footnote 21 Therefore, the reason some of the previous researchers have concluded the superiority of the pecking order theory over the trade-off theory is that they have considered only public manufacturing firms and included a very incomplete set of leverage determinants suggested by the two theories.Footnote 22

How do our findings compare with the findings on other economies? Examining the literature (some of which we discussed in Sect. 2), we see that there aren’t many empirical studies that claim the superiority of the pecking order theory for developed economies. For developing economies, “votes” seem to be split roughly in half, perhaps slightly in favor of the pecking order theory. Therefore, if we had to take a very rough rule of thumb sort of stance on the issue, we could say that the trade-off theory is probably more suited to explaining the situation in developed economies, while the pecking order theory may be slightly more suited for developing economies. Several empirical studies including Deesomsak et al. (2004) and de Jong et al. (2008) show that the health and stability of the economic environment exert considerable effect on firms’ capital structures. In the Turkish context, we found that in the 2003–2009 subsample where the economic environment was considerably more favorable, the predictive power of the trade-off theory was higher and that of the pecking order theory was lower compared with the case in the 1996–2002 subsample. Therefore, it might be that as the economy becomes more “healthy” and “stable”, the relevance of the trade-off theory increases and that of the pecking order theory decreases. In our opinion, this is an issue that deserves further and more thorough investigation.

8 Concluding remarks

In this paper, we examine the determinants of capital structure for non-financial firms in Turkey. The novelty of our paper comes from the fact that we use a new dataset that is substantially larger and more comprehensive in terms of both time and variable coverage than those used in previous studies on individual developing economies. Our dataset includes manufacturing, non-manufacturing, small, large, listed and unlisted firms, which enables us to take a more accurate picture of the capital structure choices of the average non-financial firm as well as to analyze capital structure differences between different types of firms. Building on these comprehensive analyses, we perform hitherto the most comprehensive comparative test of the trade-off and pecking order theories in a developing economy context.

Our results provide evidence that the trade-off theory is a better framework than the pecking order theory to understand the capital structures of Turkish non-financial firms. This seems to be true regardless of firm size, industry affiliation, and stock market listing. In other words, Turkish nonfinancial firms appear to trade-off the tax benefits of debt against deadweight costs of possible bankruptcy in order to attain an optimal capital structure. The trade-off theory seems to be particularly successful in explaining the financing choices of large private non-manufacturing firms, especially when the economic environment is more stable. The pecking order theory, on the other hand, although in our assessment still not as powerful as the trade-off theory, appears to perform best for small public firms in the manufacturing sector and when the economic environment is relatively unstable.

Our conclusion that the trade-off theory is a better framework than the pecking order theory to understand the capital structures of Turkish non-financial firms contrasts sharply with the previous studies on the Turkish economy, who generally take the opposite view. The presence of this divergence in judgments highlights the importance of conducting sufficiently comprehensive analyses in terms of both firm types and leverage determinants suggested by various capital structure theories.

Our results also indicate that neither the trade-off theory nor the pecking order theory can match all of the observed relationships in the data. For example, a main weakness of the more successful trade-off theory is that it cannot capture the inverse relationship between leverage and profitability. As shown by Fischer et al. (1989) and Hennessy and Whited (2005), however, an inverse relationship between leverage and profitability can be rationalized in dynamic versions of the trade-off theory. This implies that dynamic versions of the theory may provide an even better framework than the static versions to think about the capital structures of non-financial firms in Turkey. A dynamic framework can also enable the analyses of the costs and speeds of adjustment in debt ratios, thereby leading to a more complete understanding of firms’ target adjustment behavior than that provided in this paper. Therefore, testing the predictive ability of dynamic versions of the trade-off theory would be of great interest.

Our paper can be extended in a few other directions. First, a more in depth analysis of the leverage implications of industry affiliation would be quite valuable. In this paper, we consider two broad industry categories (manufacturing and non-manufacturing) and study leverage differences between the two. A more disaggregated industry analysis would also shed light on within-industry leverage variations as well as demonstrate whether within- or between-industry variations are the most significant. Second, our analyses in this paper provide some preliminary insights into firms’ choice between short-term and long-term debt. For example, we show that large public manufacturing firms have the most favorable debt maturity structure whereas small private manufacturing firms have the least favorable. We also provide evidence of maturity matching. Our analysis, however, falls short of providing a complete analysis of the determinants of debt maturity structure, which the future research can undertake. Last but not least, given the unprecedented rise in the size and volatility of international capital flows in the past decade, it would be worthwhile to investigate in greater detail how they influence firms’ capital structures.

Notes

Fischer et al. (1989) and Hennessy and Whited (2005) present different formulations of what is known as “dynamic trade-off theory”, where the firm has a target level of leverage and deviations from that target are gradually removed over time. In this paper, trade-off theory refers to static trade-off theory, unless stated otherwise.

For developed economies, support for the trade-off theory can be found, among others, in Antoniou et al. (2008) for for UK, US, Germany, France, and Japan, and Frank and Goyal (2009) for the US, whereas support for the pecking order theory can be found in Zoppa and McMahon (2002) for Australia. For developing economies, support for the trade-off theory can be found in Wiwattanakantang (1999) for Thailand, Huang and Song (2006) for China, and Espinosa et al. (2012) for Chile, whereas support for the pecking order theory can be found in Pandey (2004) for Malaysia, Korkmaz et al. (2007) for Turkey, Correa et al. (2007) for Brazil, and Qureshi (2009) for Pakistan.

Another important risk is the exchange rate mismatch, which may occur due to a rise in foreign currency debt, while the firm’s income is in domestic currency.

We use total sales rather than total assets to alleviate the problem of multicollinearity since many of our variables are scaled by total assets, including those for debt ratios. These two measures are highly correlated, indicating that each of them should be a sound proxy for size.

Studies such as Miller (1977) and Rajan and Zingales (1995) recommend including both personal and corporate taxes in studies of capital structure. However, in Turkey, tax rates on equity and debt income at the personal level are extremely complicated and have gone through several reforms during the past two decades. This makes it almost impossible to come up with good indicators of personal tax rates on different sources of income that would also be consistent over time. As a result, we are forced to do away with personal taxes in our analyses.