Abstract

This article estimates the effect of research and development (R&D) tax credits for small- and medium-sized enterprises (SMEs) by utilizing the propensity score matching method to correct any possible selection bias. This study also examines whether the impact of tax credits differs with firms’ characteristics such as their industry, size, and liquidity constraints. Empirical results show that R&D tax credits induce an increase in SMEs’ R&D expenditures. Moreover, we find that the effect of R&D tax credits on liquidity-constrained firms is much greater than on unconstrained firms.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

According to modern theories of economic growth, research and development (R&D) play a major role in sustainable growth. Technological progress is particularly important in Japan as the country is facing a rapidly decreasing population. However, R&D has spillover effects on other firms, and its social return is higher than its private return. In other words, since R&D has characteristics of a public good, R&D expenditures tend to be below desirable levels. Many governments offer tax credits or direct grants to foster private sector R&D. Tax credits are often favored because they are neutral with respect to industry and the nature of the firm. Compared to direct grants, they have the advantage of potentially minimizing discretionary decisions by government.

Numerous studies have evaluated the impact of tax credits on R&D. Hall and van Reenen (2000) comprehensively summarize the related literature and conclude that a $1 tax credit for R&D induces about $1 of additional R&D expenditures. Many studies, however, disregard the problem of selection bias. Recipients of tax credits might systematically differ from non-recipients. For instance, recipients might aspire to technological innovation and be more inclined than non-recipients to consolidate R&D systems. For this reason, recent studies such as Huang and Yang (2009) and Onishi and Nagata (2010) begin to estimate the effect of R&D tax credit after carefully correcting possible selection bias. While some of the above-mentioned studies estimate the effects of R&D tax credits on the basis of a careful correction of the selection bias, several issues remain, especially in small- and medium-sized enterprises (SMEs).

First, existing research that corrects for possible selection bias does not focus on SMEs. Many studies point out that innovation by SMEs is essential for economic growth. Acs and Audretsch (1990) and Audretsch (2006) find that SMEs’ contribution to technological progress through R&D and innovation has a crucial impact on economic growth. As R&D of SMEs plays a major role in innovation and technological progress, evaluating the impact of R&D tax credits on SMEs remains an important research issue.

Second, as SMEs tend to face liquidity constraints, their level of R&D expenditures may be less than that of larger firms. R&D expenditures are characterized by high cost and usually firm-specific investment. And they have little collateral value because the labor cost comprises a large portion of these expenditures.Footnote 1 Whether tax credits alleviate SMEs’ liquidity constraints is a significant research subject. If tax credits mitigate liquidity constraints, they may be an effective tool to induce SMEs’ R&D.

This article contributes to the empirical literature by estimating the effect of R&D tax credits on Japanese SMEs. To avoid selection bias as mentioned above, we employ the matching method introduced by Rubin (1974) to match tax credit recipients with non-recipients possessing the most similar characteristics. As we recently noted, the matching method need not assume specific functional forms and can address the systematic selection bias arising from the application of R&D tax credits. By subdividing our samples by industry, firm size, and liquidity constraint, we also examine the different effects of R&D tax credits according to firm characteristics.

Our empirical results show that offering R&D tax credits for Japanese SMEs more than doubled their R&D expenditures, and the effect is considerably large for SMEs facing liquidity constraints. Our findings thus indicate that R&D tax credits are effective policy instruments for inducing private R&D expenditures.

The article is organized as follows. Section 2 discuses the research background; Sect. 3 introduces preliminarily data and describes our empirical strategy. Section 4 presents the estimation results and a discussion. Section 5 concludes and proposes subjects for future study.

2 Research background

2.1 Literature review on the effect of R&D tax credits and the selection bias

As we described in Sect. 1, numerous studies have evaluated the impact of tax credits on R&D. Although effects of R&D tax credits are rarely estimated by utilizing microdata because of data availability, analyses using microdata are emerging. Koga (2003), for instance, examines whether the elasticity of R&D tax credits for Japanese manufacturers from 1989 to 1998 varies with firm size. He finds that tax credits primarily stimulate R&D in large rather than medium-size firms. Baghana and Mohnen (2009) examine tax price elasticity for Canadian manufacturers from 1997 to 2003. In contrast to Koga (2003), they find that estimated elasticity is significantly negative for small firms and insignificant for large firms.

Many studies, however, disregard the problem of selection bias. Recipients of tax credits might systematically differ from non-recipients. For instance, recipients might aspire to technological innovation and be more inclined than non-recipients to consolidate R&D systems. For this reason, merely estimating the difference in R&D between recipients and non-recipients may produce a biased estimate. Correcting any possible selection bias in the empirical analysis is important for assessing the effect of R&D tax credits.

Instead of evaluating the effects of tax credits on R&D expenditures, Czarnitzki et al. (2011) estimate their effects on innovation in their study of Canadian manufacturers from 1997 to 1999. To correct the selection bias, they use propensity score matching (PSM)Footnote 2 and find that tax credits encourage firms to conduct R&D and to create and sell new and improved products. Huang and Yang (2009) investigate the effect of tax incentives on R&D among Taiwanese manufacturers. As a result of estimation employing PSM, they show that recipients of R&D tax credits appear on average to spend 93.53 % more on R&D and have a 14.47 % higher growth rate of R&D expenditures compared to non-recipients with similar characteristics.Footnote 3Onishi and Nagata (2010) apply difference-in-differences-PSM (DID-PSM) to estimate the impact of R&D tax credits on Japanese firms capitalized at ¥1 billion or more. However, they find no evidence that R&D tax credits influence R&D expenditures.Footnote 4

While some existing research reveals the effect of R&D tax credits after carefully considering possible selection bias, these do not focus on SMEs. Since innovation by SMEs is the key factor for economic growth as we explain in next subsection, estimating the effect of tax credits on R&D of SMEs is an important remaining research issue.

2.2 The importance of SMEs’ R&D

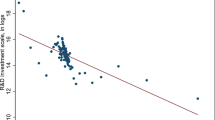

R&D of small- and medium-sized enterprises (SMEs) in particular has two important aspects. First, innovation by SMEs is essential for economic growth. Acs and Audretsch (1990) and Audretsch (2006) find that SMEs’ contribution to technological progress through R&D and innovation has a crucial impact on economic growth. Kim et al. (2010) attribute stagnation in Japan’s total factor productivity (TFP) growth during the “Two Lost Decades” to small firms’ low R&D expenditures. We confirm these observations statistically. Figure 1 shows long-term changes in the ratio of R&D expenditures to sales of large enterprises and SMEs in manufacturing. Although ratios for both have been increasing gradually, SMEs’ expenditures have grown a mere 1.7 times since 1970 versus three-fold for large enterprises. Figure 2 shows the ratio of R&D expenditures to sales with respect to the number of employees in Japan and the US. In the US, the ratio of R&D has no relation to the number of employees. In Japan, however, the smaller the workforce is, the lower the ratio of sales to R&D expenditures.

Changes in R&D expenditures of SMEs and large enterprises (manufacturing). Source Ministry of Internal Affairs and Communications, Survey of Research and Development. Notes Enterprises with workforces of 1–299 employees are considered SMEs, and those employing 300 or more are considered large enterprises. R&D expenditures include both internal and external expenditures. Data are for enterprises engaging in R&D

Ratio of R&D expenditures to sales by number of employees in Japan and the US (manufacturing). Source Small and Medium Enterprise Agency of Japan, 2009 White Paper on Small and Medium Enterprise in Japan. Notes Data for enterprises that responded about R&D in Japan and the US federal subsidies are not included for the US. To match the value definition of the US, R&D expenditures for outsourced work were excluded from R&D expenditures, and R&D expenditures for commissioned work were included in Japanese values

Second, as SMEs tend to face liquidity constraints, their level of R&D expenditures may be less than that of larger firms. R&D expenditures are characterized by high cost and, usually, firm-specific investment. At the same time, they have little collateral value because the labor cost comprises a large portion of these expenditures.Footnote 5 Stiglitz and Weiss (1981) also note the importance of internal funding for uncertain investments such as R&D because of asymmetric information. Although R&D requires abundant external funding, recent studies find that many SMEs face financial constraints (Petersen and Rajan 1994; Berger and Udell 2002; Carpenter and Peterson 2002; Czarnitzki 2006). A pioneering study by Czarnitzki and Hottenrott (2011) reveals that smaller firms have limited access to external funding, which impedes R&D of SMEs.

2.3 Japan’s system of R&D tax credits for SMEs

This subsection briefly introduces Japan’s system of R&D tax credits for SMEs. Japan introduced R&D tax credits in 1967. Initially, tax credits were applied only to incremental R&D expenditures from the previous year, and no preferences were included for SMEs. Since then, R&D tax credits have been expanded and preferences for SMEs introduced.

Table 1 summarizes Japan’s present system of R&D tax credits for SMEs. As the table shows, there are three types of credits: basic, incremental, and high-level. SMEs can receive a credit equaling 12 % of their total R&D expenditures and not exceeding an amount equal to 30 % of their corporate taxes. In addition, SMEs are eligible for an incremental credit if their R&D expenditures exceed “comparative R&D expenditures,” that is, average R&D expenditures over the past 3 years. The amount equals 5 % of the difference between R&D expenditures and “comparative R&D expenditures” and not exceeding an amount equal to 10 % of the company’s corporate taxes. The high-level credit permits companies to deduct an amount equal to 10 % of the firm’s corporate taxes if R&D expenditures surpass “average sales” for the past three years. Companies may not claim the incremental and high-level credits simultaneously.

Since our data set, described in detail in the next subsection, can identify firms receiving tax credits, we can estimate the effect of tax credits by employing it. Unfortunately, however, we can evaluate only the overall impact of whole R&D tax credits because of the inability to distinguish each types of tax credit.

3 Empirical strategy

3.1 Selection bias

When assessing the effect of R&D tax credits, it is important to correct for any possible selection bias in the empirical analysis. However, most studies that estimate elasticity of R&D tax credits regard them as an exogenous variable even though characteristics of recipients could differ from non-recipients. For example, a high level of R&D expenditures might reflect the firm’s characteristics and not the effect of tax credits. As a result, most research might be unable to identify the causal effects of the R&D credit.

Econometric evaluation techniques provide several estimation methods to correct for the selection bias, including DID estimation, selection model, instrumental variables estimation (IV), and the matching method. Because our data set is cross-sectional, we cannot utilize DID estimation, which requires panel data. Selection model and IV estimation need instrumental variables that correlate treatment variables and not output variables. Therefore, we apply the matching method introduced by Rubin (1974) and developed by Rosenbaum and Rubin (1983) and Heckman et al. (1997, 1998). Besides addressing endogeneity, the matching method has the advantage of not needing to assume a specific functional form.

3.2 Matching method

The matching method is summarized as follows.Footnote 6 Let a binary treatment indicator D i equal 1 if firm i receives R&D tax credits and 0 otherwise, where i = 1, …, N and N denote the total number of firms. The potential outcomes for each firm i are defined as Y i (D i ), where Y i denotes R&D expenditures. The treatment effect for firm i is expressed as

where \( \tau_{i} \) indicates the treatment effect.

However, we cannot observe \( Y_{i} (0) \), the counterfactual outcome. Hence, estimating the individual treatment effect \( \tau_{i} \) is impossible, and we must estimate the average treatment effect (ATE). ATE is the difference in the expected outcomes between recipients and non-recipients.

ATT indicates the expected effect on the outcome if firms in “the population” were randomly assigned for treatment. Nevertheless, as Heckman (1997) notes, ATE might lack relevance because it includes the effects on firms for which the program was never intended. Therefore, we estimate the average treatment effect on the treated (ATT), the effect on those for which the program is actually intended. ATT is expressed as

Because \( E\left[ {Y_{i} (0)|D_{i} = 1} \right] \) is the counterfactual mean, we cannot observe it. However, using the mean outcome of untreated firms \( E\left[ {Y_{i} (0)|D_{i} = 0} \right] \) instead can generate a selection bias.

The final two terms of Eq. (4) are the selection bias. \( \tau_{\text{ATT}} \) is precisely estimated in so far as \( E\left[ {Y_{i} \left( 0 \right)|D_{\text{i}} = 1 } \right] - E\left[ {Y_{i} (0)|D_{i} = 0} \right] = 0 \). This condition satisfies in experiments of random assignment but not in non-experimental studies. Rubin (1977) introduced the conditional independence assumption (CIA) to cope with the selection problem. CIA assumes that recipients and potential outcomes are independent for firms with identical exogenous covariates X i . Covariates X i consist of the set of characteristics that potentially affect receiving the R&D tax credit. If CIA is satisfied, we have the following equality.

This equality implies that the counterfactual outcome can be substituted for the outcomes of non-recipients provided there are no systematic differences between the recipient and non-recipient groups. Therefore, Eq. (3) can be rewritten as

To estimate the difference in the outcomes between recipients and non-recipients, we use the matching method introduced by Rubin (1974). Traditional matching estimators pair each recipient with an observable similar non-recipient and interpret the difference in outcomes as the effect of treatment. However, if we use many variables, matching recipients and similar non-recipients becomes difficult. To construct a valid control group, Rosenbaum and Rubin (1983) suggest matching on the basis of the propensity score [\( {\text{P}}\left( {D_{i} = 1 |X_{i} = x} \right) \)], with the probability of receiving a treatment conditional on the covariates. In effect, we use probit estimation that regresses D i on covariates X i . Using the estimated propensity score of firms choosing to receive R&D tax credits, we can execute the matching algorithm to find the proper counterfactual. The matching procedure is successful if the means of covariates X i among the two groups do not differ significantly (balancing property).

3.3 Several matching approaches

We use kernel matching, K-nearest-neighbor matching, and caliper matching. Kernel matching is a nonparametric method that uses the weighted average of non-recipients to construct the counterfactual outcome. We must choose the kernel function and the bandwidth in applying kernel matching. Econometricians acknowledge that the choice of kernel function is of slight importance but that of bandwidth is crucial because of the trade-off between bias and variance of estimates: high bandwidth induces large bias and small variance. We use Epanechnikov’s kernel function and 0.05 as a bandwidth. K-nearest-neighbor matching matches k-closest firms in terms of propensity score. Choice of k also imposes a trade-off between bias and variance: large k leads to large bias and small variance. On the basis of earlier studies, we use 5 as k. Caliper matching can avoid bad matches by imposing a tolerance level on the maximum propensity score distance (caliper). We use 0.05 as the tolerance level. While caliper matching has the advantage of small bias, variance of estimates increases when fewer matches are performed. Since there is no best matching approach, we use three alternative methods to compare estimation results.

3.4 Data and variables

We utilize cross-sectional firm-level data from The 2009 Basic Survey of Small and Medium Enterprises conducted by the Small and Medium Enterprise Agency of the Ministry of Economy, Trade and Industry. This survey collects information about SMEsFootnote 7 and covers construction, manufacturing, information and communications, wholesale and retail trade, and other industries. Sampling in this survey is based on the results of The 2006 Establishment and Enterprise Census from the Ministry of Internal Affairs and Communications. The valid response rate for this survey is 49.2 % based on 55,636 completed questionnaires.

Table 2 shows descriptive statistics for recipients and non-recipients.Footnote 8 ln(R&D expenditure) is log of R&D expenditure(thousands of yen). We realize that the average ln(R&D expenditure) among recipients is higher than among non-recipients. As discussed, however, this difference may result from the selection bias, which we must correct when evaluating the effects of R&D tax credits.

Other variables in Table 2 are exogenous covariates X. To satisfy CIA, covariate X must consist of variables that potentially affect receiving the credits. However, the determining factors of receiving R&D tax credits are not adequately revealed. We use the following variables, which may affect application of tax credits as covariates: ln(total workers), patent dummy, recurring profit margin, and dependence on debt.

Because larger firms are thought to afford conducting R&D, we use ln(total workers) as a covariate, which indicates firm size. Patent dummy is a variable that has unit value if a firm has patents and zero otherwise. Because a firm with patents is thought to undertake innovation, we utilize the patent dummy as the proxy variable for innovation. Unprofitable firms have little incentive to apply tax credits because they might not pay substantial corporate tax. Therefore, we use the recurring profit margin as a proxy variable for profitability. When firms do not hold sufficient internal funds, R&D investment may be restricted owing to financial constraints. We also exploit dependence on debt as a covariate.

Caliendo and Kopeinig (2008) recommend including as covariates only those variables that are unaffected by receiving the credits, such as fixed over time or measured before receiving. Unfortunately, we cannot utilize lagged variables as covariates because our data set is cross-sectional. Therefore, we use the following variables that are fixed over time as X: ln(capital fund), a dummy for the company’s founding year, a dummy for main financing bank, an industry dummy, and a region dummy.

Descriptive statistics of exogenous covariates as well are shown in Table 2. The average ln(total workers) among recipients is higher than among non-recipients, implying that recipients are relatively larger than non-recipients. Variables from D 1999–2003 and D after2004 are dummies that show the year in which the firm was founded, whose base category is founded before 1999.Footnote 9 Recipient firms are somewhat older than non-recipient firms. Variables ranging from the construction to other service dummies show the firm’s industry, and those from the Hokkaido–Tohoku to the Kyushu–Okinawa dummy indicate regions where a firm is located. The base category of region dummies is the Kanto District, which includes metropolitan Tokyo.

3.5 Sample separation

In addition to analyzing the whole sample, we subdivide it to examine the efficiency of R&D tax credits according to firm characteristics. Especially, we focus on the liquidity constraint because it dampens R&D of SMEs, as noted earlier.

First, we separate our sample by industry. Descriptive statistics of our sample shown in Table 2 confirm that manufacturers are more R&D intensive and more likely to apply R&D tax credits than are non-manufacturers. For this reason, examining the efficacy of R&D tax credits for manufacturers is highly significant for policy. For example, Huang and Yang (2009) ascertain whether the effect of R&D tax credits varies among hi-tech and non-high-tech Taiwanese manufacturers and find no significant difference.

Second, we focus on the effect of R&D tax credits by firm size. As mentioned, Koga (2003) finds that R&D tax credits have a greater effect on large than on small firms, whereas the elasticity estimated by Baghana and Mohnen (2009) is significantly negative for small firms, unlike for large firms. By dividing firms into subgroups with 51 or more employees and 50 or fewer, we reexamine the effectiveness of R&D tax credits by firm size. Table 3 presents summary statistics by firm size.

Finally, we split the sample according to whether firms face liquidity constraints. As noted, previous studies such as Czarnitzki and Hottenrott (2011) reveal that smaller firms suffer more from external constraints on R&D expenditures than do larger firms. Stiglitz and Weiss (1981) also note the importance of internal funding for uncertain investments such as R&D because of asymmetric information. This problem might be more serious for small firms that cannot access financial markets directly. As a result, R&D tax credits might be effective for liquidity-constrained firms.

Since Fazzari et al. (1988), empirical studies have sought to reveal financial constraints through two different approaches. The first approach uses cash flow indicators. As unconstrained firms were not expected to be sensitive to availability of internal financial resources, we can identify constrained firms by examining the sensitivity of R&D investment to internal funds. The second approach is to classify firms by size, financial marketing regimes, and governance structures. However, the literature has strongly criticized the relationship between cash flow and investment as a sufficient indication of overall financial constraints (see Kaplan and Zingales 1997, 2000 and the response by Fazzari et al. 2000).Footnote 10 Hence, we utilize the financial environment, which is faced by all firms, as a direct measure to group firms with respect to liquidity constraint. The 2009 Basic Survey of Small and Medium Enterprises, on which our data set is based, asked firms whether their main financial bank imposed conditions such as seeking guarantees from business managers or third parties, requiring property as collateral, or insisting on public credit guarantees. If so, we define them as liquidity constrained. Descriptive statistics by liquidity constraint appear in Table 3.

4 Estimation results

4.1 Probit estimation

4.1.1 Whole sample

We first estimate the probit model to obtain the propensity score. Table 4 presents the estimation results. The following covariates are found to have significant influence on a firm’s decision to apply for R&D tax credits.

Firms’ propensity to apply for R&D tax credits is positively associated with ln(total workers). This result indicates that large firms tend to use R&D tax credits. The patent dummy is also associated with applications for tax credits. Because firms holding patents are thought to pursue innovation actively, they are also deemed to utilize tax credits to cover some of the cost associated with R&D expenditures.

A recurring profit margin has a positive influence on applications for credit, and dependence on debt has a negative influence. These findings imply that firms applying for R&D tax credits are in good standing because loss-making enterprises cannot claim them.

Firms established as a limited company (yugengaisha) tend not to use R&D tax credits. Compared with kabushikigaisha (the base category), most yugengaisha are small companies. For this reason, we expect the coefficient of the yugengaisha dummy to be negative.

In contrast, dummies for the firm’s year of founding, the main bank dummies, industry dummies(excluding personal service dummy), and regional dummies (excluding the Hokkaido–Tohoku dummy) show no significant effects on applying for R&D tax credits. Covariates related to firm size, innovation, and finance are dominant in firms’ decisions to apply for R&D tax credits.

4.2 Subsamples

Estimation results of the probit model using subsamples are also shown in Table 4. Coefficients of some variables such as D 1999–2003 and the Hokkaido-Tohoku dummy are eliminated in Table 4. Some dummy variables perfectly predict the application of tax credits or take the same value in the estimations. However, eliminating these variables from the estimation means that firm would be regarded as the reference (base category). Therefore, we exclude such firms from the estimation.

Coefficients obtained by using different subsamples are similar. However, differences between subsamples are as follows. Among non-manufacturers, patent dummy and recurring profit margin show no positive influence on applying for R&D tax credits. Coefficients for other variables do not differ between manufacturers and non-manufacturers. This result might imply that patents are R&D’s important outcomes for manufacturing, but these are not for services.

Although a 1 % increase in the number of workers increases the probability of a large firm applying for the credit, this effect is lesser for small firms. In contrast, although the coefficient of dependence on debt is significantly negative for small firms, it is smaller for large firms. This result might imply that financial constraint prevents small firms from conducting R&D.

Similarly, while the coefficient of dependence on debt for firms without liquidity constraints is statistically insignificant, the coefficient for firm with liquidity constraints is significantly negative. This result might imply that R&D of firms with liquidity constraints is susceptible to scarcity of internal fund.

4.3 Effect of R&D tax credits

4.3.1 Whole sample

Table 5 shows the estimation results from matching estimators using the propensity score retrieved from the probit model. The upper section of the table displays the result from unmatched estimates, which shows the difference in ln(R&D expenditure) between recipients and non-recipients before matching. The lower section of the table displays the result from matching estimator. “ATT” exhibits the average treatment effect on the treated, which is estimated by using propensity score matching.

The first column of Table 5 presents the average ln(R&D expenditure) of the treated group (recipients), and the second column presents that of the control group (non-recipients). The third column shows the difference between the first and second columns. The fourth column provides the standard error of the differences, and the fifth column gives the t value for the equivalence of difference in means between the two groups.

In each matching method, all ATTs are smaller than the unmatched difference: the unmatched difference is 2.222, whereas ATTs are 1.251 (kernel), 1.268 (K-nearest-neighbor), and 0.996 (caliper). This implies that the unmatched difference, which disregards the selection bias, is overestimated.

However, after correcting the selection bias by using propensity score matching, estimated ATTs from all matching methods remain positive and statistically significant. Because the outcome variable is a natural logarithm of R&D expenditures, the estimated ATTs of 0.996–1.268 indicate that the application of R&D tax credits nearly doubles R&D expenditures. These estimates resemble those of Huang and Yang (2009), which are 0.898–0.960. These imply that R&D tax credits are important for inducing R&D expenditures among Japanese SMEs.

4.3.2 Subsamples

Turning to the estimates for subsamples, Table 6 lists treatment effects by industry. Estimated ATT for non-manufacturers is slightly smaller than that for manufacturers in each matching method. The average of three methods is 1.239 in manufacturers and 0.971 in non-manufacturers, respectively. Since manufacturers are more R&D intensive and tend to claim R&D tax credits, this finding means that R&D tax credits are more effective for manufacturers. This result might reflect a difference of characteristics between manufacturers and non-manufacturers. For instance, if non-manufacturers require more intangible assets to conduct R&D than manufacturers, R&D stock of non-manufacturers might have little collateral value. As a result, non-manufacturers might be reluctant to conduct R&D even if they could utilize tax credits.

Estimated results by firm size are shown in Table 7, and the estimated ATT for small firms is somewhat larger than that for large firms. An average of three methods is 1.059 in large firms and 1.362 in small firms, respectively. Existing studies focused on firm size, such as Koga (2003), Baghana and Mohnen (2009), and Kasahara et al. (2011), reveal that the elasticity of R&D tax credits varies with firm size. Our empirical results also confirm that the effect of tax credits differs with firm size.

Table 8 shows that estimates of ATT for firms with liquidity constraints are much larger than for firms without them. The average of three methods is 1.591 in the liquidity constraint and 0.887 in the non-liquidity constraint, respectively. These results imply that internal funding is important for making investments in activities with uncertain outcomes, such as R&D. Existing research reveals that smaller firms suffer more from external constraints on R&D expenditures than do larger firms, and such constraints prevent SMEs from R&D spending. These consequences are also supported by the estimation results above. Our results imply that tax credits for SMEs facing external funding constraints are considerably effective in stimulating their R&D expenditures.

4.4 Tests of balancing property

As discussed in Sect. 3.2, we must confirm that the means of covariates between the recipient and the non-recipient groups do not differ significantly from zero. If so, our matching results can be regarded as reliable.

Table 9 shows the average covariates of each group and the standard t test for the equity of mean sample values along with its p value before and after matching. Before matching, the means of many covariates among recipients differ statistically from non-recipients. This finding indicates that the treated and control groups generally do not exhibit similar characteristics prior to matching. After matching, however, we cannot reject the null hypothesis of the t test that the mean differences between recipients, and non-recipients are equal for almost all covariates in every matching method.

Table 10 lists the joint significance tests and pseudo R 2. In Table 10, “|%bias|” stands for the absolute percentage of the mean difference between recipients and non-recipients. Means of |%bias| decrease considerably after matching. The pseudo R 2 approaches zero if matching is successful. As the table shows, the pseudo R 2 and p value of the LR test approach zero.

In short, these statistical tests strongly support the legitimacy of our propensity matching estimates.Footnote 11

5 Discussions

This subsection discusses empirical results from two different viewpoints.

First is the difference of results between this article and previous studies, especially Onishi and Nagata (2010). While both our study and Onishi and Nagata (2010) estimate the effect of Japanese tax credits, these results are quite different. Onishi and Nagata (2010) estimate the impact of R&D tax credits on Japanese firms capitalized at ¥1 billion or more. They find no evidence that R&D tax credits influence R&D expenditures. On the contrary, our results show that tax credits significantly increase R&D expenditures of SMEs. The possible reasons why each study leads to different results are as follows. First is the firm size. Onishi and Nagata (2010) focus on large firms, but our study analyzes SMEs. As Baghana and Mohnen (2009) and Kasahara et al. (2011) reveal, small firms are likely to be more reactive to R&D tax credits since they have limited access to external funding. They have little collateral, and they may be young firms with little relationship to financial institutions. Second is the difference of the analyzing tax system. Onishi and Nagata (2010) estimate the change of effect from basic type tax credits to incremental type. On the other hand, this study estimates the effect of whole tax credits. Even though the change of the effect from basic type to incremental type does not differ significantly from zero, it does not mean that R&D tax credits as a whole have no influence on R&D expenditures. Third is the difference of the analytical method. Onishi and Nagata (2010) use propensity score matching in a manner similar to our estimates. However, several differences exist between this article and theirs. They utilize DID-PSM, whereas we use ordinary PSM. Heckman et al. (1997) show that DID-PSM often performs the best among the class of estimators they examine, especially when omitted time-invariant characteristics are important sources of bias. Regarding this point, estimates by Onishi and Nagata (2010) are more robust than ours. However, sample selection problems might arise in their analyses because their data set shrinks in the process of matching three different data sets.

The second viewpoint is the relationship between R&D tax credits and liquidity constraints. Though our empirical results show that estimates of ATT for firms with liquidity constraints are much larger than for firms without them, the theoretical background is not necessarily clear. Kasahara et al. (2011) construct a simple two-period model of R&D expenditure with financial constraint to reveal how tax credits alleviate financial constraint. Their theory implies that the effect of tax credits on R&D expenditure would be increasing in the liquidity constraint. The theoretical expectation is also empirically confirmed. However, their theoretical model does not explain why tax credits enlarge R&D expenditure more than increase of cash flow by tax credits. Constructing a theoretical framework is a future subject.

6 Conclusion

Dormant R&D by SMEs contributed to the slowdown in Japan’s TFP growth and its “Two Lost Decades.” Thus, it is especially important to induce an increase in R&D expenditures among SMEs. In many countries, R&D tax credits are a major policy tool to stimulate R&D. This article analyzed the effect of R&D tax credits on Japanese SMEs. We estimated ATT of R&D tax credits by propensity score matching to correct for the selection bias. Our empirical results revealed that tax credits positively influence SMEs’ decisions to conduct R&D, and application of tax credits more than doubles the R&D expenditures on average. Therefore, tax credits are an effective instrument to foster R&D among SMEs. Moreover, by estimating ATT using several subsamples, we found that ATT for firms with liquidity constraints is much larger than for those not facing liquidity constraints. This result might imply that providing R&D tax credits to liquidity-constrained firms is a more efficient policy because tax credits reinforce internal funds.

Our analyses have several limitations. First, even if R&D tax credits are effective policy instruments, their usefulness is limited if few firms apply them. In effect, SMEs’ ratio of application of R&D tax credits is a mere 0.26 %,Footnote 12 and SMEs’ R&D rate is 2.35 %. It is necessary to study the reasons behind this situation further. By doing so, we could also make matching estimates more accurate.

Second, in Sect. 4.4, we discussed possible reasons why our empirical results differ from previous studies. To clarify these reasons, mindful of these differences, research into the effect of R&D tax credits must be advanced. For example, if we utilize panel data, we obtain robust and detailed estimates. By using panel data, we can take advantage of DID-PSM as noted above. Furthermore, while we have no choice but to employ covariates of same-year R&D expenditures, using lags of covariates is preferable.

Third, we cannot determine the optimal level of R&D tax credits from our empirical results because our PSM analyses do not identify their general equilibrium effects and cost-benefit analysis. Further scholarship would benefit from general equilibrium analyses to determine socially optimum tax credits.

Finally, many existing researches confirmed the relationship between R&D and liquidity constraints. However, as discussed in Sect. 4.4, the theoretical relationship between R&D tax credits and liquidity constraints has not been clear yet. We need to construct a theoretical model explaining that relationship.

Notes

Hall (2002) surveys the relationship between R&D and financing constraints.

Huang and Yang (2009) employ a generalized method of moment (GMM) for panel data to correct endogeneity bias. They find results similar to those obtained by PSM analyses.

Kasahara et al. (2011), while not applying PSM, estimate the tax elasticity of R&D by utilizing the Japanese tax credit reform in 2003. Using the variation across firms in the changes in the effective rate of tax credits between 2002 and 2003, they attempt to correct for the selection bias. Their empirical result shows that the decrease in the effective rate of R&D tax credits induces an increase in R&D expenditures.

Hall (2002) surveys the relationship between R&D and financing constraints.

For example, SMEs in manufacturing are companies capitalized at ¥300 million or less or employ 300 or fewer persons. For a detailed definition of SMEs, consult the “Outline of the 2009 Basic Survey on Small and Medium Enterprises” on the web page of the Small and Medium Enterprise Agency.

We do not analyze individual proprietorships because few apply for R&D tax credits.

While it is preferable to use firm age as a substitute for a dummy for the foundation year, firm age is not available in our data set. However, our survey asks firms about the foundation year from choices: 2007, 2006, 2005, 2004, 2003, 2002, between 1999 and 2001, and before or on 1998. We utilize these as proxy variables for firm age. Since some dummy variables perfectly predict the application of tax credits in the estimations using subsamples, we combine these dummy variables into two categories.

Czarnitzki and Hottenrott (2011) employ a credit-rating index to reflect financing opportunities.

Balancing properties of subsamples are also satisfied in almost all estimations. We have abbreviated their statistical tests because of space constraints. However, the means of the main financing bank dummy between the recipient and the non-recipient groups in non-manufacturers and those of the Kyushu-Okinawa dummy in small firms differ significantly from zero in Caliper matching. Therefore, the ATT derived by this matching might be unreliable.

The 2009 Basic Survey on Small and Medium Enterprises.

References

Acs, Z., & Audretsch, D. (1990). Innovation and small firms. Boston: MIT Press.

Audretsch, D. (2006). Entrepreneurship, innovation, and economic growth. Chaltham: Edward Elgar Publishing.

Baghana, R., & Mohnen, P. (2009). Effectiveness of R&D tax incentives in small and large enterprises in Québec. Small Business Economics, 33, 91–107.

Berger, A. N., & Udell, G. F. (2002). Small business credit availability and relationship lending: The importance of bank organizational structure. Economic Journal, 112, 32–53.

Caliendo, M., & Kopeinig, S. (2008). Some practical guidance for the implementation of propensity score matching. Journal of Economic Surveys, 22(1), 31–72.

Cameron, A. C., & Trivedi, P. K. (2005). Microeconometrics. Cambridge: Cambridge University Press.

Carpenter, R. E., & Peterson, B. C. (2002). Capital market imperfections, high-tech investment, and new equity financing. Economic Journal, 112, 54–72.

Czarnitzki, D. (2006). Research and development in small and medium-sized enterprises: The role of financial constraints and public funding. Scottish Journal of Political Economy, 53(3), 335–357.

Czarnitzki, D., & Hottenrott, H. (2011). R&D investment and financing constraints of small and medium-sized firms. Small Business Economics, 36(1), 65–83.

Czarnitzki, D., Hanel, P., & Rosa, J. M. (2011). Evaluating the impact of R&D tax credits on innovation: A microeconometric study on canadian firms. Research Policy, 40(2), 217–229.

Duguet, E. (2005). Are R&D subsidies a substitute or a complement to privately funded R&D? Evidence from France using propensity score methods for non-experimental data. Revue d’Economie Politique, 114(2), 263–292.

Fazzari, S., Hubbard, R., & Petersen, B. (1988). Financing constraints and corporate investment. Brookings Papers on Economic Activity, 1996(1), 141–206.

Fazzari, S., Hubbard, R., & Petersen, B. (2000). Investment-cash flow sensitivity are useful: A comment on Kaplan and Zingales. Quarterly Journal of Economics, 115(2), 695–705.

González, X., & Pazó, C. (2008). Do public subsidies stimulate private R&D spending? Research Policy, 37(3), 371–389.

Guo, S., & Fraser, M. W. (2010). Propensity score analysis. Thousand Oaks: SAGA Publications.

Hall, B. H. (2002). The financing of research and development. Oxford Review of Economic Policy, 18(1), 35–51.

Hall, B. H., & van Reenen, J. (2000). How effective are fiscal incentives for R&D? A review of the evidence. Research Policy, 29, 449–469.

Heckman, J. D. (1997). Instrumental variables—A study of the implicit behavioral assumptions used in making program evaluation. Journal of Human Resources, 32(3), 441–462.

Heckman, J. D., Ichimura, H., & Todd, P. E. (1997). Matching as an econometric evaluation estimator: Evidence from evaluating a job training programme. Review of Economic Studies, 64, 605–654.

Heckman, J. D., Ichimura, H., & Todd, P. E. (1998). Matching as an econometric evaluation estimator. Review of Economic Studies, 65, 261–294.

Heshmati, A., & Lööf, H. (2007). The impact of public funds on private R&D investment: New evidence from a firm level innovation study. In A. Heshmati, Y. B. Sohn, & Y. R. Kim (Eds.), Technology transfer. New York: Nova Science Publisher.

Huang, C., & Yang, C. (2009). Tax incentives and R&D activity: Firm-level evidence from Taiwan. Global COE Hi-Stat Discussion Paper Series gd09-102, Institute of Economic Research, Hitotsubashi University.

Ito, B., Nakano, S. (2009). The impact of public R&D subsidies on firm’s R&D activities: Evidence from Japanese firm-level data. ESRI Discussion Paper Series No. 222 (in Japanese).

Kaplan, S., & Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? Quarterly Journal of Economics, 112(1), 169–215.

Kaplan, S., & Zingales, L. (2000). Investment-cash flow sensitivities are not valid measures of financing constraints. Quarterly Journal of Economics, 115(2), 707–712.

Kasahara, H., Shimotsu, K., & Suzuki, M. (2011). How much do R&D tax credits affect R&D expenditures? Japanese tax credit reform in 2003. RIETI Discussion Paper Series 11-E-072.

Kim, Y. G., Fukao, K., & Matsuno, T. (2010). The structural causes of Japan’s “two lost decades”. RIETI Policy Discussion Paper Series 10-P-004 (in Japanese).

Koga, T. (2003). Firm size and R&D tax incentives. Technovation, 23, 643–648.

Onishi, K., & Nagata, A. (2010). Does tax credit for R&D induce additional R&D investment? Analysis on the effects of gross R&D credit in Japan. Journal of Science Policy and Research Management, 24, 400–412. (in Japanese).

Petersen, M. A., & Rajan, R. G. (1994). The benefits of lending relationships: Evidence from small business data. Journal of Finance, 49(1), 3–37.

Rosenbaum, P. R., & Rubin, D. (1983). The central role of propensity score in observational studies for causal effects. Biometrika, 70, 41–55.

Rubin, D. (1974). Estimating causal effects of treatments in randomized and non-randomized studies. Journal of Educational Psychology, 66, 688–701.

Rubin, D. (1977). Assignment to treatment on the basis of covariate. Journal of Educational Statistics, 2, 1–26.

Stiglitz, J., & Weiss, A. (1981). Credit rationing in markets with imperfect information. American Economic Review, 71, 393–410.

Wooldridge, J. M. (2010). Econometric analysis of cross section and panel data (2nd ed.). Boston: MIT Press.

Acknowledgments

This research is a part of the project “Evaluation of Corporate Tax” at the Research Institute of Economy, Trade and Industry. The author thanks Makoto Nirei and Masaki Higurashi for providing an opportunity to conduct this research. The author is also grateful to Masahisa Fujita, Mitsuhiro Fukao, Masayoshi Hayashi, Keigo Hidaka, Masayuki Morikawa, Koichiro Onishi, Katsumi Shimotsu, Michio Suzuki, and two anonymous referees for their valuable comments. The author is solely responsible for any remaining errors.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Kobayashi, Y. Effect of R&D tax credits for SMEs in Japan: a microeconometric analysis focused on liquidity constraints. Small Bus Econ 42, 311–327 (2014). https://doi.org/10.1007/s11187-013-9477-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-013-9477-9