Abstract

Motorists’ fatalities and the fatality rate (roadway deaths per vehicle-mile traveled (VMT)) tend to decrease during recessions. Using a novel data set of individual drivers, we establish that recessions have differential impacts on driving behavior by decreasing the VMT of observably risky drivers, such as those over age 60, and by increasing the VMT of observably safer drivers. The compositional shift toward safer drivers associated with a one percentage point increase in unemployment would save nearly 5000 lives per year nationwide. This finding suggests that policymakers could generate large benefits by targeting new driver-assistance technology at vulnerable groups.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Highway safety has steadily improved during the past several decades, but traffic fatalities, exceeding more than 30,000 annually, are still one of the leading causes of non-disease deaths in the United States. The United States also has the highest traffic accident fatality rate in developed countries among people of age 24 and younger, despite laws that ban drinking until the age of 21. In addition to those direct costs, traffic accidents account for a large share of highway congestion and delays (Winston and Mannering 2014) and increase insurance premiums for all motorists (Edlin and Karaca-Mandic 2006).

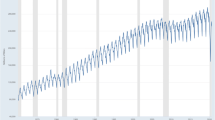

It is not an exaggeration to suggest that reducing traffic accidents and their associated costs should be among the nation’s most important policy goals. The top line in Fig. 1 shows that automobile fatalities have followed a downward trend since the 1970s, and have fallen especially rapidly during recessions, which are shaded in the figure.

National monthly automobile fatalities over the business cycle. Notes: Recessions as determined by the National Bureau of Economic Research are denoted by shaded areas. Fatality and VMT data are from the Fatality Analysis Reporting System of the National Highway Traffic Safety Administration

A natural explanation is that those declines are simply a consequence of the decrease in vehicle miles travelled (VMT) that typically accompanies a recession. With a smaller labor force commuting to work, fewer goods being shipped along overland routes, and less overall economic activity, a decline in traffic facilities is no surprise. But the heavier line in the figure shows that the fatality rate (fatalities per VMT) has also decreased more sharply during recessions than during other parts of the business cycle.Footnote 1 This implies that factors other than declining VMT contribute to the reduction in fatalities that tends to occur when real economic activity contracts. The purpose of this paper is to document those factors with an eye toward informing public policies that could reduce fatalities during all parts of the business cycle.

Researchers have shown that cyclical fluctuations in economic conditions affect most major sources of accidental deaths, including motor vehicle accidents, and they have concluded that fatalities resulting from most of those sources decline approximately in proportion to the severity of cyclical contractions in economic activity (Ruhm 2000; Evans and Moore 2012).Footnote 2 Huff Stevens et al. (2011) found that overall death rates rose when unemployment fell, and argued that this relationship could be explained by labor shortages that resulted in elderly people receiving worse health care in nursing homes as the economy expanded. But, as noted by Peterman (2013), this line of research does not explain why the percentage decline in automobile fatalities during recessions has been so much greater than the percentage decline in VMT. In 2009, for example, VMT declined less than 1%, but fatalities declined fully 9%.

There are several leading hypotheses that have been proposed to explain the sharper decline in the automobile fatality rate during recessions, including:

-

motorists drive more safely because they are under less time pressure to get to various destinations (especially if they are unemployed and have a lower value of travel time than they have when they were working);

-

households try to save money by engaging in less discretionary or recreational driving, such as Sunday drives into the country on less-safe roads;

-

motorists become risk averse because of the economic strain during a recession and drive more carefully to avoid a financially devastating accidentFootnote 3;

-

recessions may cause a change in the mix or composition of drivers on the road that results in less risk and greater safety because the most dangerous drivers account for a smaller share of total VMT.

To the best of our knowledge, researchers have not tested those hypotheses empirically because the data on individual drivers’ VMT, socioeconomic and vehicle characteristics, and safety records during recessionary and non-recessionary periods that would be required to do so are not publicly available. Publicly available data on VMT are generally aggregated to at least the metropolitan area or state level and suffer from potentially serious measurement problems. For example, nationwide VMT statistics that are released by the federal government are not based on surveys of individual drivers’ VMT; instead, they are estimated from data on gasoline tax revenues to determine the amount of gasoline consumed which is then multiplied by an estimate of the average fuel efficiency of the nation’s vehicle fleet.Footnote 4

This paper avoids the problems associated with the publicly available data and instead analyzes motorists’ safety over the business cycle using a novel, disaggregated data set of drivers who allowed a private firm to use a new generation of information technologies, referred to as telematics, to remotely record their vehicles’ exact VMT from odometer readings and to store information about them and their safety records. The private firm supplied the data to State Farm Mutual Automobile Insurance Company (hereafter State Farm®) and State Farm provided the data to us. This unique data set enables us to identify heterogeneous adjustments in vehicle use to changes in local economic conditions across a large number of motorists and to assess how differences in their adjustments may affect overall road safety.

Capturing motorists’ heterogeneous responses turns out to be important because we find that changes in local unemployment do not affect the average VMT per driver across all drivers, but they do affect the composition of drivers on the road. In particular, we find that the drivers in our sample who are likely to pose the greatest risks to safety, as indicated by several observable characteristics such as the driver’s age and accident history, reduce their VMT in response to increasing unemployment. Thus, rational individual choices involving the risk of driving during a recession lead to safer drivers accounting for a larger share of VMT during periods when aggregate unemployment is high. This finding reconciles the two key safety-related phenomena observed during recessions: the large (and typically permanent) decline in aggregate automobile fatalities and the modest (and usually transient) decline in aggregate VMT, which we note may be spuriously correlated because the decline in aggregate VMT could be due to measurement error in the publicly available aggregate VMT data, reduced commercial driving activity, or other unobserved determinants of recessions that are correlated with driving. In contrast, we argue that our finding that increases in unemployment do not affect average VMT per driver is causal.

More importantly, the quantitative effect of the change in driver composition on automobile safety is economically significant: our estimates suggest that the change in the composition of VMT that results from an increase in the nationwide unemployment rate of one percentage point could save nearly 5000 lives nationwide per year or a reduction of 14% of the 34,000 deaths nationwide attributed to automobile accidents during our period of analysis. Thus, our finding identifies an economic benefit associated with a recession that should be noted in government spending programs that are guided by changes in the unemployment rate.

Our findings also illustrate the opportunity for policymakers to significantly reduce the aggregate costs of automobile accidents by implementing policies that induce the most dangerous drivers to curtail their VMT. However, we point out the difficulty of identifying specific policies that could target such a broad segment of the motoring public. At the same time, the significant technological advance in the automobile itself—such as the development of driverless or autonomous cars—suggests that prioritizing a push of the most dangerous drivers towards vehicles with greater autonomy could generate substantial social benefits as we transition to a fully autonomously driven fleet.

1 Data and empirical strategy

Previous analyses of automobile safety, such as Crandall et al. (1986) and Edlin and Karaca-Mandic (2006), have taken an aggregate approach to estimate the relationship between accident fatalities and VMT by including state-level controls for motorists’ socioeconomic characteristics (e.g., average age and income), riskiness (e.g., alcohol consumption), vehicle characteristics (e.g., average vehicle age), and the driving environment (e.g., the share of rural highways). Taking advantage of our novel data set, our disaggregated approach focuses on individual drivers to estimate the effect of changes in the macroeconomic environment on automobile fatalities, which could be transmitted through three channels:

-

individual drivers might respond to the economic changes by altering their behavior;

-

the composition of drivers or vehicles in use might respond to the economic changes;

-

the driving environment itself might be affected in ways that influence automobile safety (e.g., the public sector might increase spending on road maintenance as fiscal stimulus).

Our empirical analysis is based on data provided to us by State Farm (hereafter referred to as the “State Farm data”).Footnote 5 State Farm obtained a large, monthly sample of drivers in the state of Ohio containing exact odometer readings transmitted wirelessly (a non-zero figure was always reported) from August 2009, in the midst of the Great Recession, to September 2013, which was well into the economic recovery.Footnote 6 The number of distinct household observations in the sample steadily increased from 1907 in August 2009 to 9955 in May 2011 and then stabilized with very little attrition thereafter.Footnote 7 The sample also contains information about each driver’s county of residence, which is where their travel originates and tends to be concentrated, safety record based on accident claims during the sample period, socioeconomic characteristics, and vehicle characteristics. For each of the 88 counties in Ohio, we measured the fluctuations in economic activity and the effects of the recession by its unemployment rate.Footnote 8 We use the unemployment rate because it is easy to interpret and because other standard measures of economic activity, such as gross output, are not well measured at the county-month level. Using the size of the labor force residing in each county instead of the unemployment rate did not lead to any changes in our findings.Footnote 9

The sample is well-suited for our purposes because drivers’ average daily VMT and Ohio’s county unemployment rates exhibit considerable longitudinal and cross-sectional variation. Figure 2 shows that drivers’ average daily VMT over the period we examine ranges from a few miles to more than 100 miles and Fig. 3 shows that county unemployment rates range from less than 5% to more than 15%. Finally, we show in Fig. 4 that for our sample average daily VMT and the unemployment rate are negatively correlated (the measured correlation is -0.40), which provides a starting point for explaining why automobile fatalities are procyclical.

Distribution of daily VMT in Ohio, 2009–2013

Distribution of unemployment rates by county in Ohio, 2009–2013

Ohio average individual daily VMT and unemployment rate

We summarize the county, household, and vehicle characteristics in the sample that we use for our empirical analysis in Table 1. Although we do not observe any time-varying characteristics of individual drivers such as their employment status, we do observe monthly odometer readings from drivers’ vehicles that allow us to compute time-varying measures of their average daily VMT. The drivers included in our sample are generally State Farm policyholders who are also generally the heads of their respective households. The data set included information on one vehicle per household, which did not appear to be affected by seasonal or employment-related patterns that would lead to vehicle substitution among household members because less than 2% of the vehicles in the sample were idled in a given month.

The sample does suffer from potential biases because individual drivers self-select to subscribe to telematics services that allow their driving and accident information to be monitored in return for a discount from State Farm. Differences between the drivers in our sample and drivers who do not wish their driving to be monitored suggest that the Ohio drivers in our sample are safer compared with a random sample of Ohio drivers. This is confirmed to a certain extent in Table 1 because our sample, as compared with a random sample, tends to contain fewer younger drivers, with the average age of the household head nearly 60. The table also suggests our sample is likely to have safer drivers, as compared with a random sample, because it has a somewhat higher share of new cars and of trucks and SUVs.

To assess the potential bias on our findings, we obtained county-month level data from State Farm containing household and vehicle characteristics of all drivers in the (Ohio) population, and we used that data to construct sampling weights on each observed characteristic. But because we expect that unweighted regressions using our sample of disproportionately safe drivers, as we have hypothesized, should yield conservative estimates of the effect of the Great Recession on automobile safety, we initially report the results from those regressions. As a sensitivity check, we then re-estimate and report our main findings weighting by the age of drivers in the population in each county, which corrects for the most important potential source of sample bias.

Of course, drivers who select not to be in our sample may have unobserved characteristics that we cannot measure that contribute to their overall riskiness. Nonetheless, a weighted sample that somehow accurately represented those unobserved characteristics in the population would likely still be composed of a population of drivers who are less safe than the drivers in our unweighted sample, which again suggests that the unweighted sample yields conservative estimates of the effect of the Great Recession on automobile safety.

Another consideration regarding our sample—and generally any disaggregated sample of drivers’ behavior—is that although it consists of a large number of observations (291,834 driver-months, covering 15,228 drivers, and 17,766 vehicles, none of which was strictly used for commercial purposes), only a very small share of drivers ever experiences a fatal automobile accident. Thus our sample would have to be considerably larger than 300,000 driver-months to: (1) assess whether the change in fatalities during a business cycle can be explained by more than a change in VMT alone; and (2) identify the specific causal mechanism at work by jointly estimating how individual drivers’ employment status affects their VMT, and how any resulting change in their VMT affects their likelihood of being involved in a fatal automobile accident.

Accordingly, our empirical strategy proceeds as follows:

-

1.

We identify the causal effect of changes in the local economic environment over our sample period, as measured by the local unemployment rate, on the driving behavior of individual drivers, as measured by the variation in their monthly VMT. We first carry out this estimation at the aggregate (county) level, which appears to show that the primary channel through which increasing unemployment reduces fatalities is by reducing VMT. Estimating identical model specifications using disaggregated measures of average monthly VMT for individual drivers, however, reveals that rising local unemployment has no apparent effect on individual drivers’ VMT.

-

2.

In order to ascribe a causal interpretation to these estimates and address concerns about endogeneity bias, we replicate the disaggregate estimations using an instrumental variables approach that relies on plausibly exogenous spatial variation in economic conditions. The results reinforce our previous finding that the variation in local unemployment has no apparent effect on individual drivers’ VMT.

-

3.

We enrich our analysis by estimating heterogeneous effects of local economic conditions on VMT by individual driver and vehicle characteristics. We find that plausibly riskier drivers disproportionately reduce their driving in response to adverse economic conditions. Although we cannot separate the contribution of changes in drivers’ behavior and in their composition, both responses suggest that an important reason that highway safety improves during a recession is that a larger share of VMT is accounted for by safer drivers during periods of greater unemployment.

-

4.

Finally, we identify the effect of the local unemployment rate on the local automobile fatality rate (as measured by fatalities per VMT), and we find that rising unemployment within a county has a statistically and economically significant effect in reducing that county’s fatality rate.

Our analysis controls for a variety of factors related to the driving environment in order to explore the extent to which this effect is mediated solely through safer driving by some individuals (including switching to safer vehicles) or by changes in the representation of a greater share of less risky drivers on the road. Although we cannot control for all of the unobserved factors that characterize the driving environment, our results strongly suggest that the notable improvement in safety during the Great Recession has occurred largely because risky drivers’ share of total VMT has decreased.

2 Economic conditions and VMT

Based on aggregate statistics, it is widely believed that an economic downturn causes VMT to decline, which is central to understanding why automobile safety improves during recessions. We first investigate the relationship between economic conditions and aggregate VMT by constructing aggregate VMT in a given county as the simple average of the daily VMT of all the drivers in a given county in our sample. We then estimate a regression of aggregate county VMT on the county unemployment rate. We stress that those estimates should not be interpreted as causal, because as noted below they may suffer from endogeneity bias; nevertheless, they offer a useful comparison with other findings in the literature. In order to allow for multicollinearity across drivers within treatment groups, we estimate robust standard errors clustered at the county-month level in all regressions.

The estimation results presented in the first column of Table 2 indicate that recessions are associated with declines in VMT, and that this effect is statistically significant. As shown in the second column, the estimated coefficient increases somewhat when we control for county and year-month fixed effects, although its statistical significance declines from the 99% to the 90% level. Thus our use of the State Farm data to measure aggregated VMT and to estimate the relationship between it and unemployment yields results that are consistent with the conventional wisdom. This provides some reassurance about the accuracy of the VMT information obtained from the State Farm data and that it is not a potential source of bias that could affect our findings.

In order to take advantage of the unique panel of drivers that we observe, we re-estimate the two aggregate specifications at the driver level by computing each driver’s average daily VMT from the monthly odometer readings on his or her vehicle. As noted, we do not observe individuals’ employment status over time, but the specifications can shed light on whether unobserved driver characteristics are correlated with county level unemployment rates, which could bias the aggregate results. The estimates in the third column of Table 2 show that the effect of the county unemployment rate on individual VMT is considerably weaker as its estimated coefficient (-0.03) is barely non-zero but it is precisely estimated.

As shown in columns 4 and 5, the effect of local unemployment on individual drivers’ VMT clearly remains both statistically and economically insignificant when we include county, year-month, and individual driver fixed effects. Most important, the estimates from the disaggregated analysis differ statistically significantly from the estimates obtained using aggregate data. This result provides evidence that individual drivers’ responses to local economic conditions vary considerably, and casts serious doubt on the conventional wisdom that aggregate relationships between VMT and economic conditions identified in previous research can be interpreted as evidence that recessions reduce fatalities simply by reducing the level of automobile use. We suggest that our findings of a strong aggregate relationship between VMT and unemployment (in specification (1)) and virtually no disaggregate relationship between VMT and unemployment (in specification (3)) can be reconciled by the idea that the unobserved characteristics of drivers in county-months with lower unemployment lead them to drive more.Footnote 10

We address the issue of causality more carefully by using instrumental variables to verify that we have reliably identified the causal relationship between local economic conditions and VMT. Specifically, we use the unemployment rate in neighboring counties as an instrument for the unemployment rate in a given county and estimate the relationship between individual VMT of drivers in each county and that county’s unemployment rate using two-stage least squares.

Our identification strategy rests on the assumption that changes in economic conditions in surrounding counties are not related to unobserved determinants of changes in driving behavior in a given county. This is likely to be the case because according to the 2006 to 2010 American Community Surveys from the U.S. Census, nearly three quarters of Ohio workers were employed in the county where they resided, and according to the most recent National Household Travel Survey (NHTS) taken in 2009, roughly half of all vehicle trips were less than 5 miles.Footnote 11 At the same time, economic linkages are likely to make the economic conditions in neighboring counties a good predictor for the economic conditions in a given county. Because unemployment in a neighboring county might be correlated with unobserved determinants of cross-county trips for purposes other than commuting to work, however, we explore the robustness of our instrument by also examining more distant counties.

Figure 5 presents a map of Ohio that demarcates its 88 counties and their spatial relationships; note that the variation of county borders is likely to generate additional variation in unemployment rates between neighboring counties. Following the argument above, we constructed instruments for the unemployment rate of each county: (1) the unemployment rates of neighboring counties (for example, the unemployment rates of Ross, Pike, Adams, Brown, Clinton, and Fayette counties were used as instruments for the unemployment rate of Highland county); and (2) the unemployment rates of neighbors of neighboring counties (for example, the unemployment rates of Clermont, Warren, Greene, Madison, Pickaway, Hocking, Vinton, Jackson, and Scioto counties were used as instruments for the unemployment rate of Highland county). Our first instrument is likely to give a superior prediction of the unemployment rate of a given county, while the second instrument is more likely to provide plausibly exogenous variation in the unemployment rate of a given county.

County map of Ohio

We showed previously that Ohio county unemployment rates exhibited considerable variation.Footnote 12 The scatterplot in Fig. 6 indicates that a given Ohio county’s unemployment rate bears a strong positive relationship to its neighboring counties’ unemployment rates.

Relationship between a Ohio county’s and its neighbors’ unemployment rates

The persistence of unemployment suggests that lagged values of the instruments are also likely to be correlated with the county unemployment rates. We exploited this fact by specifying lagged values of neighboring county unemployment rates as additional instruments. Figure 7 in the appendix shows the strength of as many as six monthly lags and indicates that all of them have some explanatory power in a first-stage regression of county unemployment rates.Footnote 13 These additional instruments improve the strength of the first-stage regression and also crucially provide the means to conduct over-identification tests of our instruments’ validity.

Table 3 reports instrumental variables estimates of the relationship between VMT and county unemployment rates using six monthly lags for the neighboring and neighbors of neighboring county instruments. The specification in the first column obtains our previous finding based on OLS estimation that the county unemployment rate has a negative statistically significant effect on aggregate (county) VMT. The remaining specifications show that the county unemployment rate has a statistically insignificant effect on an individual driver’s VMT regardless of which of the two instruments we use and of whether we include the various fixed effects in the specification. Moreover, we cannot reject our exclusion restriction for any of the specifications as indicated by the p-values associated with the over-identification tests (Hansen 1982). Taken together, we interpret those results as strong evidence in support of our identification strategy. The estimated effects are also highly economically insignificant; for example, the fifth specification in Table 3 allows us to conclude with 95% confidence that a one percentage point increase in the unemployment rate causes drivers to decrease their daily VMT by no more than 0.09 miles.Footnote 14

However, this very small aggregate effect may mask heterogeneous and large effects for different subpopulations. We exploit our disaggregated data to identify heterogeneous effects of economic conditions on drivers’ VMT by including in our main regressions interactions of the unemployment rate with both driver and vehicle characteristics. We interacted those characteristics with the local unemployment rates instead of including those variables separately to capture the idea that changes in the unemployment rate are likely to affect the mix of drivers on the road by simultaneously affecting all motorists’ travel behavior. The driver’s characteristics indicated whether the driver had filed an accident claim at any time during the sample period, whether the driver is between the ages of 30 and 50 years old, whether the driver is over 60 years old, and whether the driver lives alone or with only one other person. The driver’s vehicle characteristics indicated whether it is at least five years old and whether it is an SUV or a truck. In all of these specifications, we specified the county unemployment rate by itself and its interaction with driver and vehicle characteristics, again using the neighboring unemployment rates as instruments for the county unemployment rate.Footnote 15

Empirical evidence obtained by other researchers suggests that in addition to a driver’s accident history these demographic categories could be important and distinct. Tefft (2012) provides evidence from 1995 to 2010 that mileage-based crash rates were highest for the youngest drivers, who are under-represented in the State Farm data, and decreased until age 60, after which they increased slightly. It is reasonable to characterize drivers in small (1 or 2 person households) as less likely to drive as safely as drivers in larger households, because automobile insurance companies consider married people to be safer drivers than their unmarried counterparts, as evidenced by the significant discounts on their automobile insurance rates that they offer. In addition, people in households with children tend to see themselves as role models in road safety for their children (Muir et al. 2010).

NHTSA (2013) provides evidence that drivers’ safety declines with the age of their vehicles. Recent safety improvements, in particular electronic stability control systems that make vehicles less likely to flip, are responsible for at least part of the drop in deaths associated with the latest model year vehicles.Footnote 16 Various other studies indicate that while drivers’ safety increases when they travel in vehicles in larger size classifications such as SUVs and trucks (for example, Jacobsen 2013), drivers of those vehicles tend to be safer than other drivers regardless of the vehicles they drive. Train and Winston (2007), for example, found that drivers in households with children are more likely to own SUVs and vans than are other drivers. A counterargument is that such drivers may engage in risky offsetting behavior by driving recklessly in their larger and safer vehicles (Peltzman 1975), but there are other factors that lead drivers to select those vehicles that apparently enable them to be classified by automobile insurance companies (including State Farm) as safer drivers when compared with drivers of other vehicle size classifications.Footnote 17

Two potential sources of endogeneity are present in the regressions. First, unobserved determinants of driving behavior could be correlated with local unemployment rates, but our instrumental variables should control for those unobservables following the earlier argument and empirical support for our instruments. Second, unobserved determinants of driving behavior could be correlated with drivers’ demographic characteristics, or with attributes of the vehicles they drive. This source of endogeneity, however, should not affect our causal interpretation that the coefficients simply capture heterogeneous effects of local unemployment on individual driving behavior. For example, if we find that drivers over the age of 60 decrease their VMT in response to local unemployment, it does not matter whether the reduction is attributable to age itself or attributable to an unobserved factor—like retirement—that is correlated with age. This would not undermine our central finding that different drivers respond differently to changes in local economic conditions.Footnote 18

The parameter estimates in the first column of Table 4 show that even after controlling for other factors, the county unemployment rate’s average effect on an individual driver’s VMT remains statistically insignificant.Footnote 19 But the statistically significant coefficient estimates on the various interaction terms show that drivers who experienced an accident during the sample period, who were over the age of 60, and who lived either by themselves or with only one other person did significantly reduce their VMT as the county unemployment rate increased. In contrast, drivers who were between the age of 30 and 50 increased their VMT as the county unemployment rate increased.

The parameter estimates in the second column indicate that, all else constant, the county unemployment rate’s effect on an individual driver’s VMT was statistically insignificant, but that drivers of vehicles that were at least five years old reduced their VMT as the county unemployment rate increased and that drivers of SUVs and light trucks increased their VMT as the county unemployment rate rose. Finally, as shown in the third column, any possible bias in the parameters of any of the socioeconomic characteristics does not appear to affect the estimates of the vehicle characteristics (and vice-versa), because the estimated parameters of both sets of characteristics change little when they were included in the same specification.

Because unemployment and driver behavior in Ohio are quite seasonal, we included year-month dummies in all regressions of interest. It is possible that those seasonal effects could influence different drivers differently. For example, drivers over the age of 60 may have different seasonal driving patterns than younger drivers (e.g., they may drive less when it is dark, and therefore drive less during the winter than other groups drive). We took two approaches to explore those possible patterns in our data. First, we interacted monthly dummy variables with a given demographic characteristic, but we did not find any changes in the results.Footnote 20 Second, we estimated all of the coefficients separately for months with inclement weather, including all the winter and some spring months (December–May), and for other months. However, we were unable to obtain statistically significant differences between the two seasonal models, which we acknowledge may be due to a lack of statistical power.

As we summarize in the following chart, the general thrust of our estimation results is that economic fluctuations, as indicated by changes in the unemployment rate, affect the VMT of individual drivers, as characterized by various characteristics, differentially.

Characteristic | High risk or low risk? | Impact of recession on VMT |

|---|---|---|

Accident claim filed | High | Negative |

Age 30–50 | Low | Positive |

Age 60+ | High | Negative |

Lives in 1–2 person household | High | Negative |

Car 5+ years old | High | Negative |

SUV or truck | Low | Positive |

Moreover, it appears that these heterogeneous effects cause riskier drivers to reduce their VMT, while at the same time causing safer drivers to increase their VMT. It is reasonable to interpret the estimated change in the overall mix of drivers as conservative, because it is likely that safer drivers are already overrepresented in the State Farm data.

Why, compared with other drivers, do riskier drivers appear to reduce their VMT during a recession even if their employment situation remains unchanged? One possibility is that a correlation between less safe drivers and risk aversion is reinforced by economic downturns. For example, Dohmen et al. (2011) conducted a study of attitudes toward risk in different domains of life and found that older people were much less willing than younger people to take risks when driving, which could lead to them taking fewer risky trips, such as driving in bad weather, late at night, on less-safe roads, or after they had been drinking. Individuals in our sample who were previously involved in an accident may have also developed some new aversion to driving and may thus have taken fewer risky trips during the recession. The financial stress caused by a recession may even result in drivers who were not initially risk averse to take fewer risky trips. Cotti and Tefft (2011) found that alcohol-related accidents declined during 2007–2008 and Frank (2012) reported that accidents and VMT declined between 2005 and 2010 during the times of day (generally late at night) that are considered to be the most dangerous times to drive. Both changes in driving behavior could reflect less risk taking by older drivers, drivers living in small households, and other drivers whose characteristics were associated with more risky behavior during normal economic conditions.Footnote 21

At the same time, the recession could also induce some people to offset a potential loss in income by increasing their work effort, which could include taking jobs that involve longer commutes to work by automobile, taking an additional job that requires more on-the-job driving, and so on. Those responses could explain why we find that drivers of prime working ages and drivers of utility vehicles like SUVs and trucks increased their VMT.Footnote 22 This behavior implies that the decline in VMT that is generally observed during recessions is likely to be primarily explained by a decrease in commercial and on-the-clock driving, including for-hire trucking, other delivery services, and certain business-related driving during the workday. Indeed, data provided to us by the Traffic Monitoring Section of the Ohio Department of Transportation indicated that as of 2013, vehicle-miles-traveled by trucks on the Ohio state system of roads, including interstates, U.S. Routes, and state routes, had declined notably during the recession and continued to do so even thereafter (roughly 10% during our sample period).

3 Implications for automobile safety

The final step in our analysis is to link the change in different drivers’ VMT to potential improvements in automobile safety. As noted, we lack the statistical power to analyze individual drivers’ fatalities, so we analyze the determinants of total monthly automobile fatalities in each of Ohio’s 88 counties.Footnote 23 For each county in each month, we compute the average daily VMT of drivers in the State Farm sample, and we obtain the number of motor vehicle occupant fatalities from the National Highway Traffic Safety Administration’s Fatality Analysis Reporting System (FARS) database.

We include monthly fixed effects to capture statewide trends such as changes in gasoline prices and alcohol consumption.Footnote 24 In addition, effective August 31, 2012, a new Ohio law prohibited persons who were less than 18 years of age from texting and from using an electronic wireless communications device in any manner while driving. Abouk and Adams (2013) found that texting bans had an initial effect that reduced accident fatalities but that this effect could not be sustained. In any case, our monthly fixed effects capture the introduction of this ban. It is possible that monthly fixed effects may not capture a trend like traffic congestion if congestion affects traffic fatalities and changes significantly across counties over time. However, Ohio does not have many highly-congested urban areas and the six that are included in the Texas Transportation Institute’s Urban Mobility Report, Dayton, Cincinnati, Cleveland, Toledo, Akron, and Columbus, experienced little change in congestion delays during our sample period.

We also specify county fixed effects, which capture the effect of variation in police enforcement of maximum speed limits and other traffic laws, differences in roadway topography and conditions, and other influences that vary geographically, on highway fatalities.Footnote 25

The first column of parameter estimates in Table 5 shows that VMT and the county unemployment rate on their own do not affect fatalities, but their interaction does have a statistically significant (at the 90% level) negative effect on vehicle fatalities. Based on our previous estimation results, we hypothesize that increases in the unemployment rate reduce automobile fatalities by increasing the share of total VMT accounted for by safer drivers. While this specification cannot capture any effect of the changing composition of drivers, we can capture that effect by estimating the determinants of fatality rates. Because we found that unemployment does not significantly affect the VMT of the average driver in our sample, any reduction in the average county fatality rate due to unemployment must be attributable to a reduction in the average fatality rate of all drivers. Such a reduction could occur only if there was a change in the composition of VMT for the drivers in our sample, or if some motorists drove more safely as unemployment rose.

The second column of Table 5 presents the results of OLS estimates showing that an increase in the county unemployment rate does appear to reduce the average county fatality rate. The magnitude of the effect of unemployment on the fatality rate is potentially underestimated because a decline in VMT due to increasing unemployment, which we reported in our OLS estimates in Table 2, columns 1 and 2, would by itself mechanically increase the fatality rate. In column 3, we address this potential bias by re-estimating the model using six lags of the unemployment rate in neighboring counties as instruments for the local unemployment rate.Footnote 26 As expected, the resulting estimates show that the effect of the county unemployment rate on the fatality rate increases—in fact, nearly doubles—and that this effect is statistically significant. The average daily fatality rate in our sample is 0.03; thus, our estimated coefficient implies that a one percentage point increase in unemployment reduces the fatality rate by roughly 16%.Footnote 27

Of course, other influences on the driving environment within counties may vary over time and thus help to explain why observed automobile fatalities declined during our sample period. In the fourth and fifth columns of Table 5, we present estimates that include per-capita transfers from the state of Ohio to each county, including both intergovernmental transfers from the state to counties and direct capital spending by state government within each county. Those variables control for financial conditions that may be correlated with the driving environment that motorists encounter in different counties, and that affect highway safety. We also include a measure of cold weather conditions—the number of days with minimum temperatures less than or equal to 32 degrees Fahrenheit—which may adversely affect highway safety.Footnote 28

The parameter estimates reported in columns (4) and (5) indicate that the capital transfers, which are primarily used to improve transportation and infrastructure, reduce fatalities per VMT, and their effect has some statistical reliability. However, the intergovernmental transfer and weather measures are statistically insignificant, perhaps because they vary insufficiently across Ohio counties to allow us to identify their effects. In any case, the effect of the unemployment rate is only slightly reduced by including those variables, and remains statistically significant. As a further robustness check, we control for any time-varying effects on fatalities that may differ between urban and rural counties, which could include changes in commercial driving and congestion, by specifying separate, fully flexible time trends for those county classifications.Footnote 29 The traffic fatality rate in 2012 on Ohio’s non-interstate rural roads was 2.15 per 100 million miles of travel compared with a traffic fatality rate of 0.63 on all its other roads (TRIP 2014). The estimates presented in the fifth column show that including those time trends increases the regression’s overall goodness of fit, but again has no effect on the estimated parameter for the county unemployment rate, which increases the confidence we have in the validity of our instrumental variables.

Based on the specification in the last column of Table 5, a one percentage point increase in unemployment reduces the fatality rate 14% on average.Footnote 30 Instrumental variables estimate local average treatment effects; thus, extrapolation of this estimate to the entire United States should be done with caution. That said, it is plausible to use our estimate to simulate the safer driver composition of VMT that results from a one percentage point increase in unemployment throughout the country, which implies that we could reduce the roughly 34,000 annual fatalities by as many as 4800 lives per year.Footnote 31 Extrapolating our results to estimate the effects of more dramatic economic shocks, such as the 4 to 8 percentage point increases in unemployment experienced by some parts of the country during the Great Recession, would be inappropriate and quite likely to be misleading.Footnote 32

In addition to the benefits from fewer fatal accidents, changing the mix of VMT to reflect a larger share of safer drivers would reduce injuries in non-fatal accidents, vehicle and other property damage, and congestion. Accounting for the reductions in all of those social costs by assuming plausible values for life and limb, time spent in congested traffic, and the cost of repairs yields an estimate of total annual benefits in the tens of billions of dollars with some favorable distributional effects.Footnote 33

Taking a broader perspective, our estimate may be conservative if a national recession reduces average VMT even if an increase in local unemployment does not. Thus, a recession may have a direct (linear) effect and a compositional effect that reduces VMT, and it is possible that both effects may be mediated through macroeconomic variables other than the unemployment rate.

Finally, we previously hypothesized that our estimate of benefits may be conservative because the share of risky drivers in our sample is likely to be less than the share of risky drivers in the population. To test this possibility, we estimated weighted regressions based on weights we constructed from data provided by State Farm on the household characteristics of drivers in Ohio’s population. Specifically, we re-estimated the specification in Table 5 weighting the regression based on the age of drivers in Ohio’s driving population, the most important potential source of sampling bias, and we found that the effect of a one percentage point increase in unemployment increased the reduction in the fatality rate to 22%, on average, which confirms that our estimates based on the unweighted regressions are conservative.Footnote 34

We did not estimate a weighted regression that simultaneously accounted for all the variables that may reflect sampling bias, including household and vehicle characteristics, because that estimation requires us to observe the joint distribution of all those characteristics in the population to accurately construct the sampling weights, which we were unable to do. In any case, reweighting our initial regression to reflect the fact that our sample of drivers is safer than the drivers in the population would likely show that we are underestimating the effect of unemployment on fatality rates.

4 Qualifications and policy implications

We have addressed the long-standing puzzle in automobile safety of why fatalities per vehicle-mile decline during recessions by showing that a downturn in the economy causes the mix of drivers’ VMT to change so that the share of riskier drivers’ VMT decreases while the share of safer drivers’ VMT increases. This combination results in a large reduction in automobile fatalities. It is also possible that this result arises partly because riskier drivers actually drive more safely—rather than simply driving less—during recessions. To the extent that this contributes to the result we observe, however, it reinforces our argument that a key to improving highway safety is to reduce the safety differential between drivers with varying degrees of riskiness.

We were able to perform our empirical analysis by obtaining a unique, disaggregated sample of Ohio drivers. The sample’s main drawback is that middle-aged (and thus arguably safer) drivers are over-represented, while younger and arguably more dangerous drivers are under-represented. Nonetheless, we were still able to observe sufficient heterogeneity among drivers to document our explanation of the automobile safety puzzle and to show that aggregate data, which continues to be used to analyze highway safety, is potentially misleading because it obscures differences among drivers and their responses to varying conditions that affect vehicle use and road safety. Indeed, the extent of aggregation bias may be even greater in a representative sample of Ohio drivers because such a sample would include a greater share of younger drivers and would capture more heterogeneity than was captured in our sample. In addition, our sensitivity tests using regressions that were weighted to more accurately reflect the characteristics of drivers in the population indicated that our findings based on the unweighted regressions were conservative.

While we control for the effects of many aspects of the driving environment, our findings certainly do not rule out other possible explanations of the safety puzzle. We hope to have motivated other scholars to build on our work and findings by assembling and analyzing a more extensive and representative disaggregated sample of drivers and their behavior.Footnote 35

Because we have documented an instance of a natural economic force that impels riskier drivers to drive less while not discouraging safer drivers, it should give us hope that we could suggest a public policy that has the same effect. However, our characterization of riskier drivers applies to an amorphous group that includes drivers with a broad range of socioeconomic characteristics; thus, it is difficult to apply our findings to develop a new well-targeted public policy that could affect those drivers’ behavior and produce a substantial improvement in highway safety.

Turning to conventional policies, Morris (2011) points out that from 1995 to 2009 annual traffic fatalities declined considerably less in the United States than in other high-income countries and that officials in those countries attribute their improvement in highway safety to more stringent regulations and penalties for driving offenses such as speeding, drunk driving, and drug use, and to more aggressive and extensive police enforcement of traffic safety laws. Although those measures might reduce motorists’ fatalities in the United States, it is not clear that they would do so by disproportionately reducing the most dangerous drivers’ VMT.

In fact, an ongoing challenge to policymakers has been to improve automobile safety efficiently by designing and implementing VMT taxes that reflect the riskiness of different drivers (Winston 2013). Economists have pointed out that policies that have been proposed to help finance highway infrastructure expenditures, such as raising the gasoline tax for motorists or introducing a fee for each mile driven, could improve highway safety by reducing VMT (Parry and Small 2005; Edlin and Karaca-Mandic 2006; and Langer et al. 2016). Anderson and Auffhammer (2014) have recently proposed a mileage tax that increases with vehicle weight to account for the fact that heavier vehicles increase the likelihood that multi-vehicle accidents will result in fatalities. However, our analysis suggests that those pricing policies do not fully satisfy the challenge facing policymakers because they do not take account of the different risks posed by different drivers and thus are not focused on reducing the most dangerous drivers’ VMT.

Finally, automobile insurance companies have a strong interest in reducing accidents and they offer discounts to drivers who drive safely; but, to the best of our knowledge, they have not implemented a detailed VMT-based policy for rates that encourages the most dangerous drivers to drive less.

Fortunately, it appears that recent technological advances in the automobile itself may be able to accomplish what public policies cannot by effectively recreating in expansionary periods the safer pool of drivers who are found on the road during recessions. Specifically, exciting developments in autonomous automobile technologies are currently being tested in actual driving environments throughout the nation and the world. The transition to their eventual adoption on the nation’s roads is increasingly likely to happen in the near future.

Driverless cars are operated by computers that obtain information from an array of sensors on the surrounding road conditions, including the location, speed, and trajectories of other cars. The onboard computers gather and process information many times faster than the human mind can do so. By gathering and reacting immediately to real-time information and by eliminating concerns about risky human behavior, such as distracted and impaired driving, the technology has the potential to prevent collisions and greatly reduce highway fatalities, injuries, vehicle damage, and costly insurance. Additional benefits include significantly reducing delays and improving travel time reliability by creating smoother traffic flows and by routing—and when necessary rerouting—drivers who have programmed their destinations.

Driverless cars could affect the mix of VMT in two ways. First, during the transition from human drivers to driverless cars, policymakers could allow the most dangerous drivers, who ordinarily might have their driver’s licenses suspended or even revoked following a serious driving violation or who have reached an age where their ability to operate a vehicle safely has been seriously impaired, to continue to have access to an automobile provided it is driverless or at the very least has more autonomy than current vehicles. This would expedite the transition to driverless cars and help educate the public and build trust in the new technology (Reimer 2014). At the same time, it would immediately improve the safety of the most dangerous drivers on the road by giving them legal and safe access to automobile travel when they might otherwise drive illegally and—given their driving records or physical condition—dangerously.

Second, with the transition to driverless cars eventually complete, the risk among drivers would be eliminated. To be sure, automobile accidents, even fatal ones, might still occur. But that would pose a technological instead of a human problem, which our society has historically found much easier to solve.

Notes

In a simple time series regression of the change in the fatality rate on a time trend and a recession dummy with seasonal controls, the coefficient on the recession dummy is negative and statistically significant at the 99% level.

Ruhm (2013) finds that although total mortality from all causes has shifted over time from being strongly procyclical to being essentially unrelated to macroeconomic conditions, deaths due to transportation accidents continue to be procyclical. Stewart and Cutler (2014) characterize driving as a behavioral risk factor. But in contrast to other risk factors such as obesity and drug overdoses, motorists’ safer driving and safer vehicles have led to health improvements over the time period from 1960 to 2010.

As a related point, Coates (2008) conducted experiments and found that people became more risk averse as economic volatility became greater. This may occur during a recession.

The government also collects VMT data from the Highway Performance Monitoring System (HPMS) and from Traffic Volume Trends (TVT) data. HPMS data count vehicles on a highway under the assumption that those vehicles traverse a certain length of highway. So, if 10,000 cars are counted per day on a midpoint of a segment of road that is 10 miles long, the daily VMT on that segment is estimated as 100,000. Those data suffer from a number of problems including (1) they are aggregated across drivers, so the best that can be done is to distinguish between cars and large trucks; (2) the vehicle counts are recorded at a single point and assumed to remain constant over the entire road segment, ignoring the entry and exit of other vehicles; (3) daily and seasonal variation in traffic counts is unaccounted for; and (4) the traffic counts are infrequently updated. The final problem causes the HPMS data to be especially inaccurate during unstable economic periods like recessions when VMT could decrease significantly. The TVT data are VMT estimates that are derived from a network of about 4000 permanent traffic counting stations that do not move and that operate continuously. Unfortunately, the locations were explicitly determined by their convenience to the state Departments of Transportation instead of by a more representative sampling strategy.

We are grateful to Jeff Myers of State Farm for his valuable assistance with and explanation of the data. We stress that no personal identifiable information was utilized in our analysis and that the interpretations and recommendations in this paper do not necessarily reflect those of State Farm.

Although the National Bureau of Economic Research determined that the Great Recession officially ended in the United States in June 2009, Ohio was one of the slowest states in the nation to recover and its economy was undoubtedly still in a recession when our sample began.

Less than 2% of households left the sample on average in each month. This attrition was not statistically significantly correlated with observed socioeconomic or vehicle characteristics.

Monthly data on county unemployment were obtained from the U.S. Department of Labor, Bureau of Labor Statistics.

We considered allowing the county unemployment rate to vary by age classifications, but such data were not available, perhaps because employment in certain age classifications may have been too sparse in lightly populated counties.

Formally, we can express the difference in the coefficients on VMT from the aggregate and disaggregate regressions as \( \left({\beta}^A-{\beta}^D\right)=\frac{1}{u_{ct}}\left(\frac{1}{n_{ct}}{\displaystyle \sum_{ct}}{\lambda}_i+\left(\frac{1}{n_{ct}}{\displaystyle \sum_{ct}}{\epsilon}_{ict}^D-{\epsilon}_{ct}^A\right)\right), \) where u ct is the unemployment rate in county c in month t, n ct is the number of drivers in the sample in county c in month t, λ i is the driver i fixed effect, and ϵ D ict and ϵ A ct . refer to error terms from the disaggregate and aggregate regressions respectively. The large difference in the estimated coefficients from the aggregate and disaggregate regressions is not particularly surprising given several terms contribute to this difference, including individual driver heterogeneity, differences in the number of drivers across counties, and the potential bias in the estimated aggregate error.

The NHTS is available at http://nhts.ornl.gov.

The wide distribution of unemployment rates in neighboring counties during any single month is also similar to the wide distribution of county unemployment rates, ranging from below 5% to more than 15%.

Our findings did not change when we used fewer lags.

Given that we obtained very similar results with both sets of instruments, which are constructed using different spatial information, it is likely that our empirical strategy and specification avoid potential spatial autocorrelation of the error terms.

We obtained similar results when we used the unemployment rates of the neighbors of neighboring counties as instruments.

As a rough attempt to control for the type of people who drive new cars, Andrea Fuller and Christina Rogers, “Safety Gear Helps Reduce U.S. Traffic Deaths,” Wall Street Journal, December 19, 2014 report that new models from 2013 had a noticeably lower fatality rate than comparable brand-new cars had five years earlier.

Since 2009, total U.S. vehicle traffic and pedestrian deaths have been declining and pedestrian deaths as a share of total vehicle-related deaths have been increasing. This could indicate that some offsetting behavior has been occurring or it may indicate that recent safety improvements protect vehicle occupants more than they protect pedestrians or that growing urbanization has increased pedestrian traffic.

Although we do not invoke an exogeneity assumption about the effect of socioeconomic characteristics on utilization, it is worth noting that a long line of empirical research on consumers’ utilization of durable goods (for example, Dubin and McFadden 1984) has argued that it is reasonable to treat socioeconomic characteristics, such as drivers’ ages and household size, as exogenous influences on VMT, and that Winston et al. (2006) did not find that VMT had an independent effect on the probability of a driver being involved in an accident. It is possible that unobserved variables that influence VMT are correlated with a driver’s age and household size, but our primary interest in estimating the VMT regression is to explore whether the effect of unemployment on driving is different for different groups of people. As noted, the drivers in the State Farm data may not be representative of the population of drivers in Ohio, but our central goal is to document the selected effects of unemployment on those drivers’ VMT. Finally, Mannering and Winston (1985) showed that although, in theory, VMT is jointly determined with vehicle type choice (i.e., make, model, and vintage), and thus with vehicle characteristics, Mannering (1983) has argued that vehicle characteristics could be treated as exogenous in VMT equations if VMT were being analyzed over a short time period as we do here.

Our basic findings did not change for any of the specifications in the table when we specified VMT in logarithms to control for the possibility that different demographic groups had substantially different VMT baselines.

Indeed, less than 10% of the variation in daily VMT interacted with the driver characteristics in Table 4 across months in our sample, which substantially limited the scope for different seasonal driving patterns across demographic groups to explain our findings.

Bhatti et al. (2008) reported that individuals in France were less likely to drive while they were sleepy soon after they retired from the workforce. The changes in driving behavior may also reflect less risk taking by the youngest drivers, who are generally included among the most risky drivers. However, as noted, the State Farm data tended to include very few of those drivers, so we could not identify how they adjusted their VMT in response to the recession.

Note we are suggesting that those drivers increased their VMT on vehicles that were used for work-trips and non-work trips, not on vehicles that were used for commercial purposes only.

Although our data from State Farm include individual drivers’ claims related to predominantly non-fatal accidents, we found that even those claims were too infrequent to analyze empirically.

We obtained average monthly gasoline prices from GasBuddy.com that varied by county, but when we included them in the model they had a statistically insignificant effect on fatalities and had no effect on the other parameter estimates. This is not surprising given that we include the year-month fixed effects.

DeAngelo and Hansen (2014) found that budget cuts in Oregon that resulted in large layoffs of roadway troopers were associated with a significant increase in traffic fatalities and The National Economic Council (2014) concluded that poor road conditions were associated with a large share of traffic fatalities.

The instrumental variable parameter estimates presented in this column and in the other columns of the table were statistically indistinguishable from those that were obtained when we used the unemployment rate in neighbors of neighboring counties as an instrument.

We obtain this figure by multiplying a hypothetical one percentage point increase in the unemployment rate by the coefficient capturing its effect on the fatality rate and expressing it as a percentage of the average fatality rate in the sample (i.e., \( \frac{-0.49\times 1\%}{0.03}\approx 16\% \).)

Annual county level financial data (expressed in 2013 dollars) are from the Ohio Legislative Service Commission. The majority of capital spending is allocated to transportation and infrastructure, while the majority of subsidies are allocated to Revenue Distribution, Justice and Corrections, and Education and Health and Human Services and some is also allocated to local governments for infrastructure. Monthly weather data are from the National Climatic Data Center of the National Oceanographic and Atmospheric Administration. We used readings from local weather stations in 76 Ohio counties. For the 12 counties without fully operational stations, we used data from the neighboring county with the longest shared border. We also explored using a precipitation measure of weather, but a number of weather stations did not report that information.

Urban counties are defined as those in which more than 50% of the population lives in an urban setting as defined by the 2010 U.S. Census.

As before, this figure is obtained by multiplying a hypothetical one percentage point increase in the unemployment rate by the coefficient capturing its effect on the fatality rate and expressing it as a percentage of the average fatality rate in the sample, so \( \frac{-0.43\%}{0.03}\approx -14\% \). The decline in Ohio’s unemployment rate during 2009 to 2012 was associated with a modest increase in its fatality rate, but that association does not hold any other effects constant, such as alcohol consumption, which would affect the fatality rate.

Ohio’s 2012 fatality rate per 100,000 people of 9.73 is reasonably close to the average fatality rate of all states and the District of Columbia of 10.69 (Sivak 2014). Thus our extrapolation based on Ohio drivers’ behavior and safety environment should not be a poor prediction of the likely nationwide improvement in automobile safety. Because we have tried to hold commercial driving constant in this specification, which generally declines when unemployment increases thereby reducing fatal accidents, we have probably overestimated the precise number of lives that would be saved. However, our estimate of annual lives saved in the thousands is of the right order of magnitude.

Although we observe within county variation of unemployment of as much as 4 to 8 percentage points during our sample period, it is important to note that we can use only the component of that observed variation that is induced by changes in our instruments, the neighboring counties’ unemployment rate and the neighbors of neighboring counties’ unemployment rate, to identify the effects of unemployment on driving behavior. Because the amount of variation in our instruments is not equivalent to the amount of variation in a county’s unemployment rate, instead their variation is roughly three-quarters of the amount of variation in a county’s unemployment rate (see, for example, Fig. 6), and because the largest of the first stage coefficients for our instruments is roughly 0.66, we caution readers not to extrapolate the impact of a change in unemployment that exceeds 2 percentage points. This caution is especially warranted because the effect of unemployment on fatalities may be non-linear, with the first percentage point drop in unemployment, for example, inducing a decrease in driving by the most dangerous drivers and subsequent percentage point decreases in unemployment not having nearly the same effect on the composition of VMT and fatalities. We tried to estimate non-linear effects in a more flexible specification, but we were unable to obtain statistically precise coefficient estimates. We suspect that this may be due to insufficient statistical power; hence, we maintain that the non-linear relationship between unemployment and traffic fatalities is a valid topic of interest that merits further research.

Per capita pedestrian death rates from automobile accidents are greater in lower income census tracts than in higher income census tracts. Data provided to us by Governing magazine, published in Washington, D.C., shows that this difference has widened as the U.S. economy has come out of the recession and unemployment has decreased. Changing the mix of VMT to reflect a larger share of safer drivers would reduce the difference in pedestrian death rates across census tracts with different levels of income.

We constructed driving age sampling weights for the regressions using the following procedure. We obtained year-month-county level data on the number of drivers in eight distinct age bins (under 25, 25–34, 35–44,…, 65–74, over 75) from State Farm. We used these data to estimate the age distribution of the population of drivers in each year, month, and county. We then weighted each observation in our data set by the relative probability that it was sampled (where that weight is given by: \( Weight=\frac{ \Pr \left( in\ Pop.\right)}{ \Pr \left( in\ Sample\right)} \)) and re-estimated the regressions by weighted least squares. We also constructed household size and vehicle type sampling weights by an analogous procedure using data from State Farm on the household size and vehicle type distributions of the population of drivers in each year, month, and county. We again found that our weighted regressions tended to yield estimates of the effect of unemployment on the fatality rate that were greater than the estimates obtained by the unweighted regressions.

Using a disaggregate data set to link VMT to the business cycle is also important to get a more precise understanding of how much VMT will increase as the economy completes its recovery. For example, recent aggregate estimates of VMT released by the Federal Highway Administration indicate that as of June 2015, Americans’ driving has hit an all-time high, fueling calls for greater investment in highways that must bear growing volumes of traffic. At the same time, some observers have claimed that younger people (specifically, Millennials) are driving less than previous generations in their age group drove, which has implications for forecasts of VMT growth and estimates of funds for future highway spending. In addition, the financial success of any public-private highway partnerships will be affected by the accuracy of traffic growth estimates.

References

Abouk, R., & Adams, S. (2013). Texting bans and fatal accidents on roadways: Do they work? Or do drivers just react to announcements of bans? American Economic Journal: Applied Economics, 5, 179–199.

Anderson, M. L., & Auffhammer, M. (2014). Pounds that kill: The external costs of vehicle weight. Review of Economic Studies, 81, 535–571.

Bhatti, J. A., Constant, A., Salmi, L. R., Chiron, M., Lafont, S., Zins, M., & Lagarde, E. (2008). Impact of retirement on risky driving behavior and attitudes toward road safety among a large cohort of French drivers. Scandinavian Journal of Work, Environment & Health, 34, 307–315.

Coates, J. M. (2008). Endogenous steroids and financial risk taking on a London trading floor. Proceedings of the National Academy of Sciences, 105, 6167–6172.

Cotti, C., & Tefft, N. (2011). Decomposing the relationship between macroeconomic conditions and fatal car crashes during the Great Recession: Alcohol and non-alcohol-related accidents. The B.E. Journal of Economic Analysis & Policy, 11, 1–22.

Crandall, R. W., Gruenspecht, H. K., Keeler, T. E., & Lave, L. B. (1986). Regulating the automobile. Washington, DC: Brookings Institution.

DeAngelo, G., & Hansen, B. (2014). Life and death in the fast lane: Police enforcement and traffic fatalities. American Economic Journal: Economic Policy, 6, 231–257.

Dohmen, T., Falk, A., Huffman, D., Sunde, U., Schupp, J., & Wagner, G. G. (2011). Individual risk attitudes: Measurement, determinants, and behavioral consequences. Journal of the European Economic Association, 9, 522–550.

Dubin, J. A., & McFadden, D. L. (1984). An econometric analysis of residential electric appliance holdings and consumption. Econometrica, 52, 345–362.

Edlin, A. S., & Karaca-Mandic, P. (2006). The accident externality from driving. Journal of Political Economy, 114, 931–955.

Evans, W. N., & Moore, T. J. (2012). Liquidity, economic activity, and mortality. Review of Economics and Statistics, 94, 400–418.

Frank, P. (2012). Hour-of-the-week crash trends between the years 2005–2010 for the Chicago, Illinois region. Chicago Metropolitan Agency for Planning Working Paper.

Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica, 50, 1029–1054.

Huff Stevens, A., Miller, D. L., Page, M. E., & Filipski, M. (2011). The best of times, the worst of times: Understanding pro-cyclical mortality. NBER working paper 17657.

Jacobsen, M. R. (2013). Fuel economy and safety: The influences of vehicle class and driver behavior. American Economic Journal: Applied Economics, 5, 1–26.

Langer, A., Maheshri, V., & Winston, C. (2016). From gallons to miles: A short-run disaggregate analysis of automobile travel and taxation policies. University of Arizona working paper.

Mannering, F. L. (1983). An econometric analysis of vehicle use in multivehicle households. Transportation Research A, 17A, 183–189.

Mannering, F., & Winston, C. (1985). A dynamic empirical analysis of household vehicle ownership and utilization. Rand Journal of Economics, 16, 215–236.

Morris, J. R. (2011). Achieving traffic safety goals in the United States: Lessons from other nations. Transportation Research News 272: New TRB Special Report, 30–33.

Muir, C., Devlin, A., Oxley, J., Kopinathan, C., Charlton, J., & Koppel, S. (2010). Parents as role models in road safety. Monash University Accident Research Centre, Report No. 302.

National Economic Council. (2014). An economic analysis of transportation infrastructure investment. Washington, DC: The White House.

National Highway Traffic Safety Administration. (2013). How vehicle age and model year relate to driver injury severity in fatal crashes. Washington, DC: Traffic Safety Facts, NHTSA, U.S. Department of Transportation.

Parry, I. W. H., & Small, K. A. (2005). Does Britain or the United States have the right gasoline tax? American Economic Review, 95, 1276–1289.

Peltzman, S. (1975). The effects of automobile safety regulations. Journal of Political Economy, 83, 677–726.

Peterman, D. R. (2013). Federal traffic safety programs: An overview. Washington, DC: Congressional Research Service Report for Congress.

Reimer, B. (2014). Driver assistance systems and the transition to automated vehicles: A path to increase older adult safety and mobility? Public Policy and Aging Report, 24, 27–31.

Ruhm, C. J. (2000). Are recessions good for your health? Quarterly Journal of Economics, 115, 617–650.

Ruhm, C. J. (2013). Recessions, healthy no more? NBER working paper 19287.

Sivak, M. (2014). Road safety in the individual U.S. States: Current status and recent changes. University of Michigan Transportation Research Institute report no. UMTRI-2014–20.

Stewart, S. T., & Cutler, D. M. (2014). The contribution of behavior change and public health to improved U.S. population health. NBER Working Paper 20631.

Tefft, B. C. (2012). Motor vehicle crashes, injuries, and deaths in relation to driver age: United States, 1995–2010. Washington, DC: AAA Foundation for Traffic Safety.

Train, K. E., & Winston, C. (2007). Vehicle choice behavior and the declining market share of U.S. automakers. International Economic Review, 48, 1469–1496.

TRIP. (2014). Rural connections: Challenges and opportunities in America’s heartland. Washington, DC, www.tripnet.org.

Winston, C. (2013). On the performance of the U.S. transportation system: Caution ahead. Journal of Economic Literature, 51, 773–824.

Winston, C., & Mannering, F. (2014). Implementing technology to improve public highway performance: A leapfrog technology from the private sector is going to be necessary. Economics of Transportation, 3, 158–165.

Winston, C., Maheshri, V., & Mannering, F. (2006). An exploration of the offset hypothesis using disaggregate data: The case of airbags and antilock brakes. Journal of Rick and Uncertainty, 32, 83–99.

Acknowledgments

We received valuable comments from Robert Crandall, Parry Frank, Ted Gayer, Amanda Kowalski, Ashley Langer, Fred Mannering, Robert Noland, Don Pickrell, Chad Shirley, Kenneth Small, Jia Yan, a referee, and the editor and financial support and useful suggestions from the AAA Foundation.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Strength of instruments. Note: Each bar corresponds to a single first stage regression with year-month fixed effects, county fixed effects and the corresponding number of lagged instruments. For each regression, we report the estimated coefficient on the most lagged instrument and its 95% confidence interval

Rights and permissions

About this article

Cite this article

Maheshri, V., Winston, C. Did the Great Recession keep bad drivers off the road?. J Risk Uncertain 52, 255–280 (2016). https://doi.org/10.1007/s11166-016-9239-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11166-016-9239-6