Abstract

We investigate whether Real Estate Investment Trust (REIT) managers actively manipulate performance measures in spite of the strict regulation under the REIT regime. We provide empirical evidence that is consistent with this hypothesis. Specifically, manipulation strategies may rely on the opportunistic use of leverage. However, manipulation does not appear to be uniform across REIT sectors and seems to become more common as the level of competition in the underlying property sector increases. We employ a set of commonly used traditional performance measures and a recently developed manipulation-proof measure (MPPM, Goetzmann et al., Rev Finan Stud 20(5):1503–1546, 2007) to evaluate the performance of 147 REITs from seven different property sectors over the period 1991–2009. Our findings suggest that the existing REIT regulation may fail to mitigate a substantial agency conflict and that investors can benefit from evaluating return information carefully in order to avoid potentially manipulative funds.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

To what extent do U.S. REIT managers manipulate risk-adjusted performance measures to enhance evaluation outcomes? Brown et al. (1996) argue that managerial compensation and reputation often depend upon performance evaluation outcomes using measures such as Jensen’s alpha (Jensen 1967), the Sharpe (Sharpe 1966, 1994) and information ratios or the Stutzer index (Stutzer 2000). A priori, REIT managers have the same incentive to manipulate performance measures as fund managers from other asset classes. However, REITs operate in a regulated environment that may limit manipulation opportunities. For instance, a common manipulation strategy relies on financial derivatives (Goetzmann et al. 2007). Yet, U.S. REITs are required to generate a minimum proportion of income from real estate, reducing the scope for managers to utilise this strategy.

Other manipulation strategies exploit informational asymmetries between managers and uninformed investors (Goetzmann et al. 2007). Research suggests that REITs are a transparent investment vehicle due to their strict regulation (Demsetz and Lehn 1985; Hardin and Hill 2008; Smith and Watts 1992), limiting the emergence of many information asymmetries. However, regulation on the corporate level may not fully address the informational deficiencies of real estate as an asset class, such as low levels of market transparency (Georgiev et al. 2003) or high levels of private information required for accurate asset pricing (Han 2006). Downs and Güner (1999) document that these characteristics induce significant information asymmetries in public REIT markets. Further, REIT insiders appear to exploit information asymmetries when the opportunity arises (Damodaran and Liu 1993). Such opportunistic managerial behaviour can create the basis for the manipulation of REIT performance measures.

Identifying manipulation using traditional performance metrics is difficult, as these are the same measures that may be manipulated. In order to avoid this bias, we assess manipulation in U.S. REITs by comparing performance evaluation outcomes under a manipulation-proof measure (MPPM) developed by Goetzmann et al. (2007) with evaluation outcomes under a set of traditional performance measures, namely the Sharpe ratio, Jensen’s alpha, the information ratio and the Stutzer index. We test for manipulation using formal hypothesis tests based on the difference between the evidence for out- or underperformance of a REIT over a benchmark index under the traditional measures and the MPPM.

We present evidence that, in line with findings in the traditional equities sector and in spite of the strict REIT regulation, risk-adjusted performance measures in the REIT sector may indeed be manipulated. As a result, investors may be able to benefit from assessing performance information carefully in order to avoid funds where management engages in manipulative practices.

Evidence consistent with manipulation has increased since the inclusion of REITs in broader stock market indices. Managers may now find their performance being monitored and assessed more closely. We provide evidence that the changes in short-term leverage appear to be correlated with performance manipulation—a manipulation strategy that is not limited by the current REIT regulation. We present results suggesting that the extent of performance manipulation is positively correlated with the degree of competition that prevails in a property sector. In contrast to what is often implicitly assumed in studies of performance manipulation, managerial incentives for manipulation do not seem to be exogenous. We present support for this hypothesis while controlling for a REIT’s position in the growth cycle as well as analyst coverage and the quality of corporate governance. Our evidence suggests that analyst coverage and the quality of corporate governance fail to alleviate the agency conflicts that can cause performance manipulation.

Evidence for performance manipulation in the REIT sector has significant consequences for investors and managers. First, evidence for manipulation suggests that the REIT regulation is inefficient in mitigating a substantial agency conflict. Diversified ownership requirements in the REIT sector imply that equity-holders are less able to rely on take-overs for the replacement of incompetent or indeed manipulative management. Instead, their primary defense against mismanagement is price-protection (Feng et al. 2007). Therefore, REIT managers who fail to convince investors that they do not manipulate performance may incur higher cost of equity. Conversely, REIT managers can actively commit to being evaluated under the manipulation-proof measure, for instance through incorporating this evaluation in performance-based executive compensation agreements. Such a commitment may support corporate governance and sharpen their competitive advantage.

Research Hypotheses

Evidence for Manipulation

Performance measures represent an important fund selection criterion for investors, have an indirect influence on manager reputation and often directly impact remuneration (Brown et al. 1996). Real estate fund managers are typically evaluated and remunerated based on performance (Cannon and Vogt 1995) and thus, a priori, have the same incentive to exhibit superior performance as fund managers from other asset classes. The characteristics of real estate as an asset class give rise to significant information asymmetries in public REIT markets (Downs and Güner 1999) that are, on occasion, exploited by REIT insiders (Damodaran and Liu 1993). On this basis, we expect to find evidence for similarly opportunistic behaviour by REIT insiders in relation to performance manipulation.

H1: U.S. REIT managers manipulate traditional performance measures.

Manipulation Strategies

Manipulation in the U.S. REIT industry requires that managers have at least one viable manipulation strategy at their disposal. Goetzmann et al. (2007) distinguish between static and dynamic manipulation, each relying on different strategies. Static manipulation targets the distribution function governing the returns that feed into performance measures. Specifically, static manipulation violates the assumption of normally distributed returns that underlies many traditional performance measures, such as the Sharpe ratio, the information ratio, and Jensen’s alpha. Lhabitant (2000) and Spurgin (2001) show how managers can employ derivatives strategies characterised by asymmetric payoffs to enhance traditional performance measures that fail to recognise the effects of skewed distributions.

Research into the use of derivatives in REITs is sparse, with the notable exception of Horng and Wei (1999). Their results suggest that derivatives play a minor role in the REIT sector. First, the authors argue that the income requirement of the REIT legislation significantly limits the use of derivatives for speculative purposes. Consistently, their results suggest that investments in derivatives by REITs mostly involve interest rate instruments to hedge financing costs and asset value fluctuations, not investments for speculative purposes. It seems therefore unlikely that U.S. REIT managers employ derivatives-based strategies of performance manipulation.

Dynamic manipulation of performance measures involves varying portfolio holdings depending on past performance, defying the assumption of independently and identically distributed returns that underlies many traditional measures (Goetzmann et al. 2007). The authors show that given any performance history within the evaluation period, the overall performance measure is maximised by holding in the future a portfolio that maximises the performance measure calculated over the remainder of the evaluation period. This strategy relies on increasing market exposure through the opportunistic use of leverage.

The U.S. REIT regime does not restrict the amount of leverage employed by REITs, either explicitly or implicitly (Lehman and Roth 2010). While the REIT regime implicitly places significant restrictions on the use of derivatives, the lack of regulatory control over leverage choices provides REIT managers with the scope to use leverage for performance enhancement. The opportunistic use of leverage in order to manipulate performance evaluations resonates with aspects of REIT behaviour previously established in empirical research. Alcock et al. (2012) identify an opportunistic pattern in REIT financing choices. In contrast to traditional real estate companies, REITs appear to employ leverage to actively secure cheaper funds as well as to signal firm quality. The REIT regulation appears to free up scope in the capital structure to pursue such more opportunistic objectives. The interpretation of REIT financing behaviour as opportunistic lends support to the view that REIT managers may employ leverage in order to enhance performance measures also.

H2: U.S. REIT managers manipulate traditional performance measures through the opportunistic use of leverage.

Manipulation and Competition

Arguably, REIT property sectors can be characterised by varying degrees of competition, depending on the number of funds active in a sector. We hypothesise that higher levels of competition may increase a fund manager’s propensity to exhibit superior performance through manipulation. The incentives for manipulation may not be exogenous, but a function of the competitive pressure in a property sector.

Research traditionally suggests an inverse relationship between competition and agency conflicts. Hart (1983) argues that if investors cannot observe managerial effort, potential for moral hazard may exist. For instance, managers may attribute underperformance to factors beyond their control, such as input prices. Hart (1983) postulates further that competition helps align managerial incentives because investors can observe a group of similar, competing firms in order to benchmark managerial effort. However, this model relies on the investor’s ability to observe information that is relevant for benchmarking managerial effort from a group of comparable competitors. This may not be possible for investors trying to monitor real estate fund managers. Real estate assets are heterogenous and thus substantially less comparable (Georgiev et al. 2003), limiting the observability of the information that is relevant for the meaningful monitoring of managers.

Our hypothesis implies that there is more potential for genuine outperformance in a sector with fewer competitors. Research often suggests otherwise and postulates a positive relationship between competition and firm efficiency (Alchian 1950; Stigler 1958). In this context, efficiency generally relates to the management of production inputs relative to the value created. However, successful real estate investment may be more closely related to the ability to obtain price-sensitive private information about assets in a market characterised by low transparency and heterogenous assets. While the input-output relationship determining the efficiency of industrial firms can be regarded as a continuum, there is arguably only a fixed amount of price-sensitive information available about a real estate asset.

If, consistent with theory, firms become more efficient with fiercer competition, they become better at obtaining this information, and the ability of an individual firm to be the only competitor in possession of a significant amount of private information diminishes. Therefore, the sources for genuine outperformance in terms of superior insight or forecasting skills become increasingly thinly spread as competition edges up. At the same time, the pressure on fund managers to compete for sector-specific investor capital intensifies with competition, increasing the temptation for managers to improve performance through manipulation. Differences in observed manipulation across sectors may suggest that the incentive for manipulation is not exogenous but determined by the competitive pressure prevailing in a sector. Specifically, we expect a positive relationship between manipulation and competition. Two testable hypotheses result from this discussion.

H3: The evidence for manipulation is not uniform across U.S. REIT property type sectors.

H4: The extent of manipulation employed by a U.S. REIT manager is a positive function of the level of competition in the REIT property sector.

Data and Methodology

Return and Benchmark Data

We analyse the monthly total return data of all U.S. publicly traded REITs contained in the SNL database over the period December 1990–2009. The final sample after exclusion of funds with no data consists of 147 REITs and a total of 21,955 firm-month observations, covering 23 diversified, 15 hotel, 7 industrial, 20 office, 27 other (healthcare, self storage and specialty), 20 residential and 35 retail REITs. Data on sector classification is provided by SNL Financial and is based on the percentage of total assets invested in a particular sector. We employ the S&P 500 index as the proxy for the market benchmark, obtained from Datastream, and the 1-month treasury bill as proxy for the risk-free rate, obtained from Kenneth French’s website, consistent with Dimson et al. (2002).

Roll (1977, 1978) argues that the choice of market proxy matters for performance evaluation. For robustness, we replicate our analysis on the basis of the MSCI world stock market index. Data on the MSCI is obtained from Datastream. Dimson et al. (2002) note that typically two types of proxies for the risk-free rate are available, short-term treasury bills or government bonds with maturities from ten to thirty years. Among the two, the short-term rate is a closer proxy for a truly risk-free asset. However, a long-term proxy may be appropriate if the cash flows of the project extend many years into the future, as is usually the case in real estate. In order to further test our results for robustness, we also employ data on the 10-year U.S. government bond obtained from Datastream.

Methodology

Hypothesis 1: Evidence for Manipulation

In order to examine the empirical evidence for manipulation in the U.S. REIT industry, we assess the consistence of out- or underperformance of REITs relative to the market benchmark. Consistence relates to the evaluation outcomes achieved under the different risk-adjusted performance measures. If REITs statistically significantly outperform the market benchmark under the traditional performance measures as well as the MPPM, we interpret this as evidence for no manipulation. Conversely, if the evaluation outcomes are inconsistent, in other words if REITs outperform under the traditional measures but underperform under the MPPM, we conclude that REIT managers manipulate traditional performance measures.

For each performance measure, we test the null hypothesis that the median performance evaluation outcome across all REITs is equal to the performance evaluation outcome of the market benchmark against the alternative hypothesis of inequality. We employ non-parametric binomial sign tests (Friedman 1937; Wilcoxon 1945) to accommodate for potential non-normality and asymmetry of the sample performance measures. However, this test has lower power than the parametric counterparts (Siegel 1956). Any rejection of the Null hypothesis is therefore conservative; it is more difficult to find evidence for significant outperformance of REITs over the market proxy. At the same time, it is just as difficult to prove significant underperformance under the MPPM, which is the prerequisite for establishing evidence of manipulation in REITs. Any evidence for divergence between performance evaluations under the traditional measures and the MPPM is therefore also conservative.

We calculate all performance measures based on return data, rather than relying on performance measures reported by the funds, in order to mitigate any potential selection bias induced by funds that choose to report only certain performance measures. For each REIT we calculate Jensen’s alpha (Jensen 1967), the Sharpe ratio (Sharpe 1966; 1994), the information ratio, and the Stutzer index (Stutzer 2000). We include the information ratio, similar in concept and form to the Sharpe ratio, since it offers an alternative perspective on the value added through active management. However, just like the Sharpe ratio and the Jensen measure, the information ratio implicitly relies on the assumption of normally distributed returns as it uses a symmetric risk measure. The Stutzer index is robust to non-normal return data. The underlying definition of risk as the likelihood of underperforming a benchmark does not make any assumptions about the distribution of the return data.

We include the Jensen measure in our analysis as it is one of the most widely used performance measures in practice (Goetzmann et al. 2007). This measure is characterised by strong conceptual links to the CAPM. However, some authors question the appropriateness of the single-index CAPM in explaining REIT performance and adopt a multi-factor approach, as discussed for instance in Clayton and MacKinnon (2003). In the context of our study, REIT managers may misrepresent fund performance relative to a certain, commonly employed market benchmark. Manipulation-induced outperformance might then be reduced or not apparent at all when evaluating funds against alternative benchmarks. Therefore, we also estimate an alternative alpha from a four-factor model including the size, value and momentum effects (Carhart 1997; Fama and French 1992).

We compare performance evaluation outcomes from the traditional measures with those from the MPPM. Goetzmann et al. (2007) define the MPPM as the certainty equivalent of the average excess return of a risky portfolio over the risk-free rate. In order to be insensitive to static manipulation, the MPPM is a concave function of returns. In order to be insensitive to dynamic manipulation, the MPPM is time separable and has a strong independence property. This property originates from utility theory and makes the MPPM insensitive to returns that are not independently and identically distributed. We calculate the MPPM, \(\hat \Theta\), as:

where ρ represents the chosen parameter of constant relative risk aversion. Consider the following numerical example (Goetzmann et al. 2007): A fund generates monthly returns of −10%, 5%, 17% and −2%. For ρ = 2, the MPPM equals 6.6%. This measure represents a certainty equivalent. Therefore, a risk-free asset would have to earn a constant monthly rate of return of c. 1.6% to achieve the same MPPM and make investors indifferent between the two options.

The intuition behind ρ is to link the average excess return in the MPPM to a notion of risk. As an increasing function of returns, the MPPM is similar in concept to traditional performance measures. For instance, the Sharpe ratio relates the average excess return to a notion of risk or the ‘price’ of the excess return, represented by the variability of the excess return. The MPPM also relates the average excess return to a notion of risk, by expressing this excess return as a certainty equivalent, assuming constant relative risk aversion measured by the parameter ρ. Alternatively, the parameter ρ can be viewed as a link of the MPPM to a benchmark portfolio earning a log-normal return \(\tilde{r}_b\). The value of ρ is selected in line with the fundamental valuation relationship in the mean-variance framework (Bailey 2005):

Goetzmann et al. (2007) observe historical values of ρ for common market proxy portfolios between 2 and 4, and choose a value of 3. The Morningstar Risk-Adjusted Return Measure, similar in concept and structure to the MPPM, adopts a value of 2 (Morningstar 2002). Given this uncertainty surrounding the correct parametrisation, we employ ρ values of 2, 3 and 4.

We initially conduct our analysis for the full study period that covers a variety of market conditions, implicitly assuming that our results do not suffer from period bias. However, the study period covers several important events in the REIT history. As a result, we also consider a number of sub-periods. We evaluate fund performance over the periods prior to and following the inclusion of REITs in broad stock market indices in 2001, the periods prior to and following the onset of the recent global financial crisis in 2008, as well as the period between these potential structural breaks, i.e. 2002–2008. For robustness, we also evaluate performance over these sub-periods using the alternative proxies for the the risk-free rate (10-year U.S. government bond instead of 1-month T-bill) and the market (MSCI instead of S&P 500). The corresponding results are included in Tables 9 and 10, respectively.

Hypothesis 2: Manipulation Through the Opportunistic Use of Leverage

We run the following panel regression for each performance measure:

where \(\Delta PM^{n}_{it}\) is the annual change in the measure n observed for fund i at the end of year t, α is a constant, and β 1 to β 3 as well as β 4 to β 6 are the coefficients associated with quarterly changes in long- and short-term leverage, respectively. Long-term leverage (LLT) is measured as the ratio of long-term debt over the book value of assets, and short-term leverage (LST) is the ratio of debt with maturities less than one year over the book value of assets. LLT12 and LST12 for instance relate to the change in long-term and short-term leverage from the first to the second quarter of year t. The matrix OCV it summarises the control variables included in the analysis. We control for the annual changes in the other performance measures observed for fund i to capture a variety of aspects of performance. We also control for the effects of merger and acquisition activity on the performance and financial structure of a firm by forming an indicator variable M&A that takes the value one if a firm was part of a merger or acquisition in a given year as well as a set of corresponding interaction terms with the leverage variables. Data about M&A activity including the identity of the buyer firm and the target firm as well as the date of completion of the transaction is obtained from SNL. The vector γ contains the parameters associated with the control variables. The ϵ it are i.i.d. normal residuals. We use heteroskedasticity- and autocorrelation-robust clustered standard errors (Hoechle 2007; Petersen 2009), and employ Hausman tests to choose between fixed or random panel effects.

Goetzmann et al. (2007) argue that many traditional performance measures can be gamed via leverage. We therefore expect that changes in quarterly leverage throughout the year are positively related to performance evaluation outcomes over the entire year under these traditional measures. Conversely, we expect leverage to be negatively related to the corresponding variation in the MPPM. The MPPM should identify leverage as a source of performance that does not directly translate into investor utility and penalise its misuse accordingly. However, our study design assumes that the evaluation period observed by a manager is based on calendar years, and that all manipulative adjustments to leverage are captured in the quarterly reports. Any evidence in favour of our hypothesis is therefore likely to underestimate the strength of the true relationships.

Hypothesis 3: Uniformity of Manipulation Across REIT Property Sectors

In order to examine the uniformity of potential manipulation across REIT property sectors, performance measures for individual REITs are grouped according to sector focus. The analysis of the third hypothesis follows the methodology we employ to investigate the first hypothesis. We test whether the median performance evaluation outcome across the REITs in a given property sector is statistically significantly different from the corresponding market benchmark value. We employ non-parametric binomial sign tests. A non-parametric method is especially warranted here given the small sample size in some of the sectors.

Hypothesis 4: Manipulation as a Function of Competition

In order to test our last hypothesis, we first rank funds by their annual performance evaluation outcomes under the Jensen measure and the MPPM, and obtain the annual differences in ranks as a proxy for the degree of manipulation a fund employs.Footnote 1 We then run a panel regression:

where α is a constant, and ΔRANK it is the difference in ranks for fund i in year t. If a fund manipulates the Jensen measure, it will rank higher under that measure than under the MPPM. Assuming the MPPM is effective, the magnitude of the difference in ranks under the two measures will reflect the extent of manipulation.

The main variable of interest, WOBS, proxies for the level of competition in a sector, measured by the weighted number of funds active in a sector in year t. We weight the number of funds by their share of the total number of observations in a sector in year t. This adjustment allows us to control for cases when, in year t, a sector comprises of two funds, one of which has very few observations compared to the competitor. We expect a positive sign on WOBS. We implicitly argue that a sector with fewer participants has lower competition. However, an alternative interpretation is that a smaller number of participants is a sign of lower supply of sector-specfic assets, thereby intensifying the sector-level competition. This possibility implies that evidence to reject the null in favour of a positive relationship between our measure of competition and the extent of manipulation is conservative.

We include the following control variables. AGE is the cumulative number of monthly return observations up to time t as a proxy for a fund’s age, since a fund’s position in the growth cycle may impact on its propensity to manipulate. NAN is the average annual number of analyst forecasts for a REIT obtained from the I/B/E/S database, on the basis that coverage can improve transparency (Chui et al. 2003; Devos et al. 2007; Downs and Güner 1999). GIN is a control variable capturing corporate governance using the G-Index (Bauer et al. 2010; Campbell et al. 2011; Gompers et al. 2003), obtained from Riskmetrics, as the quality of corporate oversight has the potential to restrict a fund manager’s scope for manipulation. We further control for aspects of annual absolute (the value of a fund’s Jensen and MPPM measures, JEN and MPPM) and relative performance (a fund’s rank under the the Jensen measure, RJEN). Standard errors are clustered by firm to be robust to heteroskedasticity and autocorrelation.

Descriptive Statistics

Table 1 shows the descriptive statistics of the monthly total returns for the different REIT sectors, REITs overall and the benchmarks over the full study period. The REIT sample consists of 21,955 firm-month observations. REITs overall have a mean monthly total return of 1.20%, as compared to 0.80% for the S&P 500. Simple χ 2 tests detect that REITs on average exhibit significantly higher variation in monthly total returns (11.13%) than the S&P 500 (4.29%). Simple t-tests (for unequal variances) suggest that on average, REIT returns seem in line with the market.

Retail and office REITs have the highest average total return (1.37% and 1.31% respectively) while hotel REITs have the lowest return (0.71%). Conversely, hotel REITs exhibit the highest standard deviation of returns (14.31%) as compared to retail and office REITs (12.66% and 11.16% respectively). Diversified REITs exhibit the lowest levels of standard deviation (9.08%), at below average return levels (1.07%). The contrast between the sectors suggests a link between REIT performance and the nature of the underlying operation as suggested in Mueller and Anikeeff (2001). The values of skewness and kurtosis suggest non-normal return distributions. Given the limitations of many traditional performance measures in relation to the underlying distribution of returns (Goetzmann et al. 2004), this finding reinforces the importance of including a performance measure in our analysis that accounts for non-normality, such as the Stutzer index. On average, REITs have a CAPM β of 0.8686, consistent with anecdotal evidence that real estate securities display lower sensitivity to market returns than the average financial asset. Among the specialised REIT sectors, discarding the combined category of other REITs, retail, office and residential REITs are the largest sectors by the number of funds and observations, suggesting higher levels of competition.

Figure 1 shows a histogram of the distribution of firm-month observations in our sample. The median number of firm-month observations is 180 with a standard deviation of 65. Under 15% of the firms have five years or less of consecutive firm-month observations for total returns. Approximately 25% of the firms in the sample have return data for the entire study period. The majority of REITs in the sample have broadly between 60 and 220 firm-month observations for total return data.

The graph shows a histogram of the firms in the final sample. The horizontal axis shows the number of firm-month observations in the final sample comprising 147 REITs over the period 1991 to 2009 and a total of 21,955 firm-month observations. The vertical axis shows the percentage of a certain firm-month observation range of the total sample in steps of 12 months

Performance measures can be utilised to establish relative fund rankings (Chen and Knez 1996; Eling 2008; Eling and Schuhmacher 2007; Sharpe 1966). Brown et al. (2010) use ranking correlations to test the ability of the MPPM to detect manipulation and confirm that the MPPM evaluates performance more accurately than other measures. The intuition behind this approach is as follows. Consider total fund performance as the sum of the performance generated through skill and potentially another component that stems from manipulation. The MPPM is designed to strip out the manipulation element and assess performance solely based on the genuine element. In the absence (presence) of manipulation, the traditional measures and the MPPM produce the same (different) relative fund rankings, and the ranking correlation between traditional performance measures and the MPPM should be high (low) (Brown et al. 2010).

The ranking correlations between the performance measures for individual REITs are shown in Table 2 and illustrated in Figs. 2 and 3. The lowest correlations are observed between the Jensen measure and the MPPM, suggesting that the Jensen measure may be subject to manipulation. In relative terms, the differences in ranks for individual funds will be greatest when comparing the Jensen ranking with the MPPM ranking, especially for performance measures calculated using the 10-year government bond. On the other hand, the ranking correlation between the Stutzer index and the MPPM is high, suggesting that the Stutzer index may not be gamed. However, if fund managers perform equally well based on skill, the correlation between traditional performance measures and the MPPM should be determined by the differences in manipulation only. If fund managers manipulate to similar extents, ranking correlations may not be able to unveil manipulation. This is why we employ explicit hypothesis tests to establish statistically robust evidence of manipulation.

Results

Evidence for Manipulation in the REIT Sector

Table 3 shows the performance evaluation results of U.S. REITs over the full study period. When considering the 1-month T-bill and the S&P 500 as benchmark proxies, REITs show a significantly positive Jensen’s alpha, suggesting positive value added for investors through active REIT management. The information ratio also suggests outperformance. When we evaluate REIT performance on the basis of the alternative alpha determined in a broader four-factor model, the evidence for outperformance remains significant, but, as expected, the magnitude of outperformance is reduced in comparison to the original Jensen’s alpha. We interpret this finding as evidence suggesting that REIT managers may focus on delivering superior performance relative to the single-index market benchmark.

However, these traditional performance measures may, at least partially, be influenced by manipulation. REITs appear to significantly underperform the market under the MPPM, and increasingly so for higher values of ρ. The discrepancy between evaluation outcomes using the traditional measures and the MPPM is consistent with the hypothesis that REITs employ strategies of manipulation. This result is in principle in line with studies of manipulation in the REIT sector that focus on accounting measures, such as funds from operations (Graham and Knight 2000; Zhu 2006; Zhu et al. 2010).

Our result implies that the REIT regulation seems inefficient in preventing a significant agency conflict that leaves managers room to manipulate performance measures. The characteristics of real estate as an asset class appear to generate sufficient private information that can be exploited by REIT managers to game performance evaluation outcomes. Our findings imply that investors need to evaluate fund return data carefully to identify funds where management may engage in manipulative practices to misrepresent fund performance. Investors may be able to improve their basis for making investment decisions by evaluating funds under the MPPM. This performance measure appears to be able to add substantial information about fund performance beyond that contained in many other common performance measures.

Panel (b) of Table 3 shows the results of our performance evaluation using the 10-year government bond as the alternative proxy for the risk-free rate. The resulting findings appear to be largely robust to using this alternative proxy. However, we now find additional evidence consistent with manipulation of the Sharpe ratio and the Stutzer index that is not apparent when using the 1-month T-bill. This new finding suggests that the short-term interest rate may be of significance in manipulation strategies, a result to which we return when examining the relationship between manipulation and the use of leverage. Panels (c) and (d) of Table 3 show the performance evaluation results for the MSCI world index as the alternative market proxy. The evidence we present consistent with manipulation is largely equivalent to the original evidence using the S&P 500, suggesting that our findings are robust to the choice of market proxy.

In the period prior to the inclusion of REITs in the broader stock market indices in 2001, the evidence we find consistent with manipulation is closely aligned with the evidence for the full study period (Panel (a) of Table 4). From 2002 onwards, the magnitude of out- and underperformance of REITs relative to the market proxy under the traditional measures and the MPPM (especially for ρ values of 3 and 4) seems more pronounced (Panel (b)). The extent of potential manipulation may have increased as REITs are evaluated in more direct comparison to the general stock market. Evidence consistent with manipulation appears to be stronger in the period after the onset of the global financial crisis from 2008 onwards as compared to the period before 2008 (Panels (c) and (d)). Lastly, evidence consistent with manipulation seems slightly weaker in the intermediate period 2002–2008 (Panel (e)). Anecdotal evidence suggests that these were unusually strong years for REITs, so that outperformance in this period seems genuine.

Manipulation Through the Use of Leverage

Table 5 shows the results from the panel regressions of annual changes in fund performance measures on quarterly changes in leverage and the control variables. Changes in short-term leverage from the second to the third quarter appear to be positively related to the change in a fund’s information ratio over the entire year. Our evidence seems consistent with REIT managers engaging in dynamic manipulation of the information ratio. A fund manager may monitor fund performance from the start of the evaluation period at the beginning of year t until a point when she judges that the fund has shown poor performance to date, say, the end of the second quarter of year t. Our findings are consistent with the manager adjusting short-term leverage in the third quarter, improving the evaluation outcome for the year.

Short-term debt is priced at a rate more closely aligned with the short-term T-bills, reflecting our comment on the significance of the short-term interest in manipulation strategies. In Table 6 we replicate the leverage analysis using performance measures that are calculated on the basis of excess returns over the 10-year government bond. In this case, the Sharpe ratio also responds positively to changes in short-term leverage, supporting the evidence consistent with a link between manipulation and the use of leverage. This finding reflects that it may become more difficult to identify manipulation strategies if these involve the use of interest rates closely aligned with those employed to calculate the performance measures to be analysed.

Our result further suggests that improvements in performance evaluation outcomes are primarily related to change in short-term leverage. This finding seems intuitive. Managers who seek to manipulate performance may be more willing to temporarily accept sub-optimal levels of short-term debt as these positions are naturally reversed more quickly and economically than debt holdings with longer maturities.

We find that evaluation outcomes under the MPPM are negatively related to changes in long-term leverage from the second to the third quarter of the year. This finding is in line with expectations that the MPPM, unlike the traditional measures, controls for the effect of leverage as a source of performance that does not directly translate into investor utility. The negative sign of the coefficient is consistent with the MPPM correctly identifying manipulation strategies based on leverage and penalising the funds concerned by assigning a lower evaluation value. As intuition would suggest, the magnitude of the effect increases with the risk aversion parameter ρ.

Our findings may also provide some insight into REIT capital structure choices. The absence of corporate taxation and the strict income distribution rules in the REIT sector call into question the applicability of many common corporate leverage theories. Howe and Shilling (1988) assert that in the absence of tax benefits, REITs cannot compete for debt and will favour equity. Similarly, Shilling (1994) argues that REIT value is maximised for equity-only financing. It has long puzzled researchers why REITs still use debt, and in some cases substantially higher leverage ratios than unregulated real estate companies. The consideration of endogeneity and simultaneity between leverage and maturity choices (Alcock et al. 2012) provides more detailed insight into the question and helps identify an opportunistic pattern in REIT financing decisions. Their findings suggest that the regulatory setting and tax-exempt status of REITs provides sufficient flexibility in the capital structure to exploit the benefits of more offensive capital structure strategies. Our findings from the present study suggest that, in line with this opportunistic approach to financing choices, REITs might employ leverage in order to deliberately enhance performance and modify the established, income-orientied characteristics of REIT investments.

Not all traditional performance measures show positive relationships with changes in leverage. This finding is in principle consistent with fund managers concentrating manipulation efforts on the most common performance measures that arguably have the strongest impact on remuneration and reputation. Similarly, performance evaluation outcomes are not significantly related to changes in leverage over all quarters of the year. This finding may suggest that fund managers wait until sufficient evidence for unsatisfactory performance has accumulated before adjusting leverage to enhance performance evaluation outcomes. Alternatively, the cost of adjusting leverage to remedy underperformance may on occasion be too high. Lastly, the selective nature of manipulative adjustments to capital structure may reflect that certain periods of the year are more relevant for performance evaluation than others.

Table 5 shows that the Sharpe and Jensen measures also appear to be negatively related to changes in leverage in some quarters of the year. Assume a fund’s performance is evaluated over the twelve months to June each year. Also assume that a fund manager has taken on a sub-optimal level of leverage throughout the second half of the evaluation period after observing poor fund performance during the first half. If fund performance is evaluated at the end of June, the sub-optimal leverage position is likely to be corrected in the third quarter of the year, when the excess leverage is no longer required to enhance performance.

Our implicit assumption about the timing of evaluation and reporting practice may lead us to observe an apparent inverse relationship between annual changes in fund performance and quarterly changes in leverage. This assumption also implies that any evidence we find for significant relationships between annual fund performance and quarterly leverage possibly understates the true strength of the relationship.

Uniformity of Manipulation Across REIT Property Type Sectors

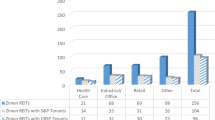

Table 7 reports the results of the hypothesis tests for out- or underperformance of REIT sectors relative to the market. Most sectors seem to outperform under the Jensen measure. Hotel and industrial REITs perform in line with the market. The relative homogeneity of evaluation results under the Jensen measure is in line with Goetzmann et al. (2007) who argue that outperformance is easier to achieve under the Jensen measure since the null hypothesis is that alpha is equal to zero. However, under the Sharpe ratio a fund must first make up the difference between zero excess return and the excess return of the market. However, the homogeneity in the Jensen-based assessment appears to contradict our earlier argument that the degree of manipulation of the Jensen measure differs significantly across funds. However, here we aim to relate differences in evaluation outcomes to property sectors. Discrepancies in evaluation outcomes across funds can arise for a variety of reasons, including property sector focus, but also manager skill. The evidence for a lack of outperformance in the industrial sector is inconsistent with the Mueller and Anikeeff (2001) evidence. However, they focus their analysis on the coefficient of variation, a measure of risk-adjusted performance we do not consider in this study.

Under the Sharpe ratio, most sectors perform in line with the market, while hotel REITs significantly underperform. The evidence for a lack of outperformance in hotel REITs under the Jensen and Sharpe measures is consistent with previous evidence (Kim et al. 2002). Mueller and Anikeeff (2001) argue that hotel leases have the strongest link to the underlying business, and therefore both income and long-term returns have higher volatility, detracting from risk-adjusted performance. As compared to the Jensen measure, the magnitude of outperformance of REIT sectors over the market benchmark is significantly reduced, consistent with the view that performance is managed relative to a particularly popular benchmark model. Managerial efforts, especially if apparent strong performance is actually induced by manipulation, do not seem to pertain to the same degree in the less common four-factor benchmark model.

The results of the information ratio and the Stutzer index are consistent with the Jensen and Sharpe measures, respectively. The similarity between the evaluation results under the information ratio and the Jensen measure reflects the similarity in their evaluation objectives. Jensen’s Alpha measures the excess return earned that is not due to a fund’s sensitivity to variation in the return on the market benchmark, and is therefore a measure of active management. The form of the information ratio is more alike to the Sharpe ratio, but its objective is the evaluation of a fund’s active return: the excess return earned by deliberately tilting the fund portfolio away from the benchmark relative to the variability of that excess return.

The similarity between the evaluation results under the Sharpe ratio and the Stutzer index is somewhat surprising but may reflect that the Stutzer index mainly aims to account for observed investor skewness preference. However, the values of kurtosis in our sample diverge more heavily from those implied in the normal distribution than the values of skewness. The Stutzer index aims to produce a relative ranking of funds with non-normal returns without penalising positive skewness. If non-normality is relatively more due to excess kurtosis rather than excess skewness, the differences in evaluation results produced under the Stutzer index and the Sharpe ratio may be less apparent.

Under the MPPM, diversified, industrial, other and residential REITs do not outperform the market. Hotel, office and retail REITs significantly underperform. The hotel REIT result is consistent with the evaluation under the traditional measures. However, our results suggest performance manipulation in office and retail REITs. These sectors appear to perform as strongly as the market benchmark under the traditional measures but underperform under the MPPM. Residential REITs outperform under some of the traditional measures but fail to do so under all variants of the MPPM.

Overall, our results suggest that, consistent with our hypothesis, not all REIT sectors show evidence of performance manipulation. There appear to be significant differences in the extent to which manipulative practices are employed to in the different REIT property sectors to enhance performance evaluation outcomes.

Manipulation and Competition

Table 8 shows the results from a regression of the difference in ranking under the Jensen measure relative to the ranking under the MPPM on the number of funds in a sector, weighted by their share of the total number of observations in the sector and a set of control variables. As we hypothesise, the weighted number of funds in a sector is significantly related to the difference in ranking of a fund under the Jensen measure and the MPPM. Consistent with our expectations, the coefficient also carries a positive sign. The higher the weighted number of funds in a sector, i.e. the higher the competition, the greater the difference in ranking for a fund under the Jensen measure and the MPPM.

The greater the competition in a sector, the more the average non-manipulative fund will improve in the ranking under the MPPM from where it was ranked under the Jensen measure. Assume that not all funds manipulate performance, at least not to the same degree. Then the average fund will improve in the ranking under the MPPM. Under the Jensen measure, the average fund was outranked by those competitors that successfully manipulate performance. Under the MPPM, those funds that previously ranked higher are identified as manipulative, and are penalised relative to the average fund.

Our findings are robust to controlling for fund age and the strength of corporate governance. The lack of association between the G-index and manipulation is consistent with the evidence presented in Bauer et al. (2010) that there is no significant link between the strength of corporate governance in REITs and REIT value or performance. Consider the effect of corporate governance as ensuring that fund performance actually creates value for investors. Our dependent variable is the difference in ranking of a fund under the Jensen measure and the MPPM, which can be interpreted as the difference between performance and actual value added for investors. If there is no significant relationship between corporate governance and REIT performance, this means that corporate governance cannot explain the differential between performance and value for investors either.

The insignificance of analyst coverage in our regression is consistent with Downs and Güner (1999) who present evidence that the informational deficiencies of real estate as the underlying asset class induce significant information asymmetries in the public REIT markets that are not mitigated or alleviated by analyst following.

Conclusion

Risk-adjusted performance measures represent important fund selection criteria for investors. However, the possibility for manipulation of traditional performance measures detracts from their reliability. Investors may be led to trust that the strict REIT regulation prevents the agency conflicts underlying the manipulation of performance measures. In this study, we present some empirical evidence to the contrary. Our evidence seems to suggest that REIT managers may in fact manipulate some widely used performance measures. At the same time, we do not attempt to provide a fully exhaustive explanation of every difference between evaluation outcomes established using traditional performance measures and the MPPM, and acknowledge that there may be other reasons for divergence apart from manipulation. Examples could include the commonly reported serial correlation of direct real estate return distributions, which may affect some traditional performance measures.

We provide empirical evidence consistent with the hypothesis that REIT managers may opportunistically employ leverage in order to game performance measures. Our results suggest that the agency conflicts underlying performance manipulation cannot be fully mitigated by the REIT regulation so long as leverage is not strictly controlled. Of course, the manipulation of traditional risk-adjusted performance measures is difficult to detect. Our evidence suggests that investors can gain important information by analysing REIT returns carefully using the MPPM measure.

We find that the extent of manipulation appears to be positively related to the level of competition in a property sector. Our results support the view that incentives for performance manipulation are not exogenous but a function of the prevailing competitive pressures. As a result, investors are able to utilise information about sector competition to assess the likelihood of a fund engaging in manipulative practices. Investors can then selectively monitor those funds that seem at risk of manipulating performance measures in an efficient and targeted manner. We further provide evidence that investors cannot rely on analyst following or corporate governance to discipline managers and suppress the manipulation of performance evaluations.

Given increased investor need for price-protection in the REIT industry against the backdrop of diversified ownership requirements, REITs that manipulate performance may incur higher cost of equity. However, managers can commit to evaluations under the MPPM, e.g. via executive compensation, and thus improve corporate governance.

Appendix

Notes

References

Alchian, A. A. (1950). Uncertainty, evolution and economic theory. Journal of Political Economy, 58(3), 211–221.

Alcock, J. T., Steiner, E., & Tan, K. J. K. (2012). Joint leverage and maturity choices in real estate firms: The role of reit status. Working Paper.

Bailey, R. E. (2005). The economics of financial markets. Cambridge University Press.

Bauer, R., Eichholtz, P., & Kok, N. (2010). Corporate governance and performane: The reit effect. Real Estate Economics, 31(1), 1–29.

Brown, K. C., Harlow, W. V., & Starks, L. T. (1996). Of tournaments and temptations: An analysis of managerial incentives in the mutual fund industry. Journal of Finance, 51(1), 85–110.

Brown, S., Kang, M., In, F., & Lee, G. (2010). Resisting the manipulation of performance measures: An empirical analysis of the manipulation-proof performance measure. Working Paper.

Campbell, R., Ghosh, C., Petrova, M. T., & Sirmans, C. F. (2011). Corporate governance and performance in the market for corporate control: The case of REITs. The Journal of Real Estate Finance and Economics, 42(4), 451–480.

Cannon, S. E., & Vogt, S. C. (1995). Reits and their management: An analysis of organizational structure, performance and management compensation. Journal of Real Estate Research, 10(3), 297–318.

Carhart, M. M. (1997). On persistence in mutual fund performance. Journal of Finance, 52(1), 57–82.

Chen, Z., & Knez, P. (1996). Portfolio performance mesurement: Theory and evidence. Review of Financial Studies, 9, 551–556.

Chui, A. C. W., Titman, S., & Wei, K. C. J. (2003). The cross-section of expected reit returns. Real Estate Economics, 31(3), 451–479.

Clayton, J., & MacKinnon, G. (2003). The relative importance of stock, bond and real estate factors in explaining reit returns. Journal of Real Estate Finance and Economics, 27, 39–60. doi:10.1023/A:1023607412927.

Damodaran, A., & Liu, C. (1993). Insider trading as a signal of private information. Review of Financial Studies, 6, 79–119.

Daniel, K., & Titman, S. (2011). Testing factor-model explanations of market anomalies. Working Paper.

Demsetz, H., & Lehn, K. (1985). The structure of corporate ownership: Causes and consequences. Journal of Political Economy, 93, 1155–1177.

Devos, H., Ong, S., & Spieler, A. (2007). Analyst activity and firm value: Evidence from the reit sector. Journal of Real Estate Finance and Economics, 35(3), 333–356.

Dimson, E., Marsh, P. R., & Staunton, M. (2002). Triumph of the optimists, 101 years of global investment returns. Princeton University Press.

Downs, D. H., & Güner, Z. N. (1999). Is the information deficiency in real estate evident in public market trading? Real Estate Economics, 27(3), 517–541.

Eling, M. (2008). Does the measure matter in the mutual fund industry? Financial Analysts Journal, 64(3), 54–66.

Eling, M., & Schuhmacher, F. (2007). Does the choice of performance measure influence the evaluation of hedge funds? Journal of Banking and Finance, 31(9), 2632–2647. doi:10.1016/j.jbankfin.2006.09.015

Fama, E., & French, K. (1992). The cross-section of expected stock returns. Journal of Finance, 48, 427–465.

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33, 3–56.

Fama, E. F., & MacBeth, J. D. (1973). Risk, return, and equilibrium: Empirical tests. Journal of Political Economy, 81(3), 607–636. http://www.journals.uchicago.edu/doi/abs/10.1086/260061.

Feng, Z., Ghosh, C., & Sirmans, C. (2007). On the capital structure of real estate investment trusts (reits). Journal of Real Estate Finance and Economics, 34, 81–105.

Fisher, R. A. (1915). Frequency distribution of the values of the correlation coefficient in samples from an indefinitely large population. Biometrika, 10(4), 507–521.

Fisher, R. A. (1921). On the probable error of a coefficient of correlation deduced from a small sample. Metron, 1, 3–32.

Friedman, M. (1937). The use of ranks to avoid the assumption of normality implicit in the analysis of variance. Journal of the American Statistical Association, 32(200), 675–701.

Georgiev, G., Gupta, B., & Kunkel, T. (2003). Benefits of real estate investment. Journal of Portfolio Management, 29, 28–33.

Goetzmann, W., Ingersoll, J., Spiegel, M., & Welch, I. (2004). Sharpening sharpe ratios. Yale ICF Working Paper No 02-08, Yale School of Management.

Goetzmann, W., Ingersoll, J., Spiegel, M., & Welch, I. (2007). Portfolio performance manipulation and maipulation-proof performance measures. Review of Financial Studies, 20(5), 1503–1546.

Gompers, P., Ishii, J., & Metrick, A. (2003). Corporate governance and equity prices. Quarterly Journal of Economics, 118(1), 107–155. http://www.mitpressjournals.org/doi/abs/10.1162/00335530360535162.

Graham, C. M., & Knight, J. R. (2000). Cash flows vs. earnings in the valuation of equity reits. Journal of Real Estate Portfolio Management, 6(1), 17–25.

Han, B. (2006). Inside ownership and firm value: Evidence from real estate investment trusts. Journal of Real Estate Finance and Economics, 32, 471–493.

Hardin, W., & Hill, M. D. (2008). Reit dividend determinants: Excess dividends and capital markets. Real Estate Economics, 36(2), 349–369.

Hart, O. D. (1983). The market mechanism as an incentive scheme. The Bell Journal of Economics, 14(2), 366–382.

Hoechle, D. (2007). Robust standard errors for panel regressions with crosssectional dependence. Stata Journal, 7(3), 281–312(32).

Horng, Y. S., & Wei, P. (1999). An empirical study of derivatives use in the reit industry. Real Estate Economics, 27(3), 561–586.

Howe, J., & Shilling, J. (1988). Capital structure theory and reit security offerings. Journal of Finance, 43, 983–993.

Jensen, M. C. (1967). The performance of mutual funds in the period 1945–1964. Journal of Finance, 23(2), 389–416.

Kim, H., Mattila, A. S., & Gu, Z. (2002). Performance of hotel real estate investment trusts: A comparative analysis of Jensen indices. International Journal of Hospitality Management, 21(1), 85–97.

Lehman, R., & Roth, H. (2010). Global real estate investment trust report 2010—against all odds. Ernst & Young LLP.

Levene, H. (1960). Robust tests for equality of variances. In S. G. Ghurye, W. Hoeffding, W. G. Madow, H. B. Mann. & I. Olkin (Eds.), Contributions to probability and statistics (pp. 278–292). Stanford University Press, Palo Alto, CA.

Lhabitant, F. (2000). Derivatives in portfolio management: Why beating the market is easy. Working Paper, EDHEC, Lille/Nice.

Morningstar (2002). The new morningstar rating methodology. Morningstar Inc.

Mueller, G. R., & Anikeeff, M. A. (2001). Real estate ownership and operating businesses: Does combining them make sense for REITs? Journal of Real Estate Portfolio Management, 7(1), 55–65.

Petersen, M. (2009). Estimating standard errors in finance panel data sets: Comparing approaches. Review of Financial Studies, 22(1), 435–480. http://rfs.oxfordjournals.org/cgi/reprint/hhn053v1.

Roll, R. (1977). A critique of the asset pricing theory’s tests part i: On past and potential testability of the theory. Journal of Financial Economics, 4(2), 129–176.

Roll, R. (1978). Ambiguity when performance is measured by the securities market line. Journal of Finance, 33(4), 1051–1069.

Sharpe, W. F. (1966). Mutual fund performance. Journal of Business, 39(1), 119–138.

Sharpe, W. F. (1994). The sharpe ratio. Journal of Portfolio Management, 21(1), 49–58.

Shilling, J. D. (1994). Taxes and the capital structure of partnerships, reits, and other related entities. Working Paper, University of Wisconsin.

Siegel, S. (1956). Nonparametric statistics for the behavioral sciences. McGrawHill.

Smith, C., & Watts, R. (1992). The investment opportunity set and corporate financing, dividend and compensation policies. Journal of Financial Economics, 32, 263–292.

Spurgin, R. (2001). How to game your sharpe ratio. The Journal of Alternative Investments, 4, 38–46.

Stigler, G. J. (1958). The economies of scale. Journal of Law and Economics, 1, 54–71.

Stutzer, M. (2000). A portfolio performance index. Financial Analysts Journal, 56(3), 52–61.

Wilcoxon, F. (1945). Individual comparisons by ranking methods. Biometrics Bulletin, 1(6), 80–83.

Zhu, H. (2006). Management of performance measures other than earnings: Evidence from the reit industry. Working Paper.

Zhu, Y. W., Ong, S. E, & Yeo, W. Y. (2010). Do reits manipulate their financial results around seasoned equity offerings? evidence from us equity reits. Journal of Real Estate Finance and Economics, 40, 412–445.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Alcock, J., Glascock, J. & Steiner, E. Manipulation in U.S. REIT Investment Performance Evaluation: Empirical Evidence. J Real Estate Finan Econ 47, 434–465 (2013). https://doi.org/10.1007/s11146-012-9378-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-012-9378-8