Abstract

Although the correlation between the public and private market pricing of real estate has generated considerable research effort, the methods utilized in previous studies have failed to capture the dynamic nature of this correlation. This paper proposes a new statistical method to address this issue. This method, known as the dynamic conditional correlation GARCH model, enables us to study the dynamics of the correlation between the two markets over time and enrich our understanding of the public and private market pricing of real assets. We find that the correlation between NAV returns and REIT returns is dynamic for all REIT types and there is a strong degree of persistence in the series of correlation. Our Granger-causality tests show that price discovery generally takes place in the securitized public market. However, we also find significant variations across property types and individual firms within each type. Our results indicate that constructing an optimal portfolio requires firm level analysis of causality and correlation between REIT returns and NAV returns.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

One of the interesting puzzles in real estate is that publicly traded REITs often trade at values different than their underlying net asset value (NAV). Furthermore, the relationship between REITs and their NAV fluctuates through time. While REITs trade at a premium to their NAV in some periods, they trade at a discount to their NAV in some other periods. Understanding this REIT premium / discount has important implications for the study of the efficiency of the public versus private real estate markets.

The relative efficiency and performance of public and private real estate markets is also important for investors. If one market outperforms the other market or if prices in one market follow the prices in the other market, this will clearly impact the timing and magnitude of investments in the two property markets. Furthermore, financial decisions typically involve a trade-off between future risks and returns, and the major components of risk involve volatilities and correlations of assets in a portfolio. Thus, the construction of an optimal portfolio of two asset types, e.g., publicly versus privately traded real estate assets, requires an accurate estimate of volatilities and correlations between the returns of the two asset classes. A complicating factor here is that volatilities and second movements evolve over time in response to changes in the economy and arrival of new information. Volatilities and correlations measured from historical data will fail to capture changes in risk unless we utilize empirical methods that update estimates carefully and swiftly.

The objective of this study is to twofold. The first objective is to examine if there exists a unidirectional causality between REIT returns and NAV returns, with one market serving as a price discovery vehicle for the other market. Since different asset types could have different risk-return characteristics, our analysis differentiates among twelve REIT types based on their asset holdings: Multi-Family, Hotel, Industrial, Health Care, Manufactured Homes, Office, Self Storage, Shopping Center, Regional Mall, Other Retail, Specialty and Diversified.

The second objective of the paper is to investigate if the correlations of REIT and NAV returns are changing through time and whether or not the correlation between the two return series varies from one REIT type to another and across firms. For this, we utilize a new methodology that allows us a drastically richer investigation of the correlation of returns between the public and private real estate markets. The methodology we will be utilizing is known as the dynamic conditional correlation multivariate GARCH (Generalized Autoregressive Conditional Heteroskedasticity) method.Footnote 1 This econometric technique enables us to measure risks dynamically and test for the direction and magnitude of volatility spillovers between the two markets. It also enables us to resolve the heteroskedasticity problem, hence avoid biased cross-market correlation coefficients, by providing estimation of correlation coefficients based on standardized residuals.

We are able to conduct the causality and correlation analysis for each of the 146 firms in the sample.Footnote 2 Our Granger-causality tests in general confirm earlier empirical results that price discovery takes place in the securitized public market. However, our results also show that there are variations across firms and property types. We are able to identify the number of firms in each property sector for which the price discovery takes place in the public or the private market.

Our dynamic conditional correlation GARCH tests confirm our expectation that the correlation between NAV and REIT returns changes over time. We are able to identify the number of firms in each property sector for which the correlation is dynamic and find variations across property sectors. While more than half of the office REITs have dynamic correlation, for instance, only one-third of Industrial REITs display dynamic correlation. We also find a strong degree of persistence in the series of correlation. Industrial REITs have the highest persistence while Manufactured Homes have the lowest persistence in correlation.

The relationship between REIT returns and NAV returns has already been explored by a number of studies in the REIT literature.Footnote 3 However, as explained in detail in the methodology section of our paper, the methods utilized in these earlier studies suffer from a number of shortcomings in their attempts to capture the dynamic nature of the correlation between the public and private markets. This is clearly a serious constraint on the analysis since the correlation between the two markets is changing through time in response to developments in economic and market conditions. Furthermore, we offer the first analysis of causality and correlation for REIT price returns and NAV returns at the firm level. We find that there are significant variations not only across different property categories but also across individual firms in each category. For any given property category, it is possible that REIT returns lead NAV returns for some firms while NAV returns lead REIT returns for some other firms. Similarly, for any given property category, the correlation between the two returns can be dynamic for some firms but not for some other firms.

The analyses of the current study are crucial for optimal portfolio considerations. Our results demonstrate that any portfolio based on market or index returns data will yield suboptimal portfolio choices. Instead, our results show that firm-level data and a dynamic conditional correlation analysis of the returns are critical in identifying the optimal portfolio of firms within and across different property types.Footnote 4

We review the literature and offer a background on the REIT premium/puzzle in the next section. Empirical methodology is discussed in “Research Methodology”. “Empirical Results” discusses the results. “Summary and Discussion” offers some concluding remarks.

Literature Review and Background

The REIT premium / discount puzzle brings up an important and interesting question: which market, the securitized, indirect, public REIT market or the unsecuritized, direct, private market of the underlying properties discovers price more efficiently?

The evidence suggests that there exists Granger causality between the public and private real estate markets with the public market leading the private market in time. That is, the public market incorporates new information into price faster than the private market. This has been demonstrated for several countries, including US (Myer and Webb 1993), United Kingdom (Barkham and Geltner 1995) and Hong Kong (Newell and Chau 1996). Barkham and Geltner (1995) find that the transmission of information from the public to private markets is faster in the UK than in the US, and suggest that this may be due to greater homogeneity of properties and larger scale of securitization of properties in the UK. Chau et al. (2001) report that public market prices in Hong Kong lead private property prices by one quarter, which is in marked contrast to the lags of up to 2 years seen for the UK, Australian and US property markets. The authors attribute the difference to the structural and informational efficiency of the Hong Kong property markets compared with property markets in US, UK and Australia.

Benveniste et al. (2001) argue that the REIT premium / puzzle is due to the tradeoff between liquidity benefits of securitization and costs associated with setting up and running a REIT. They report a liquidity premium of 12–22% for REITs relative to NAV for the 1985–1992 time period. Clayton and MacKinnon (2001b), examining the short-run relationship between REIT prices and their NAV for 1992–2000, also find evidence of a significant liquidity premium in REIT prices relative to their NAV. Their results indicate that liquidity benefit of REITs is valued more in a down private market than in an up one. They also report that sentiment plays a significant role in REIT prices and the timing of REIT equity offerings.

Another difference between the public and private markets is that short selling is not available in private markets. Furthermore, purchase of real estate in private real estate markets requires significant amount of capital while purchase of REIT shares can be accomplished with a few dollars. Finally, private real estate markets are characterized by high transaction costs. In recent experimental studies, Haruvy and Noussair (2006) and Ikramov and Yavas (2008) provide evidence that enabling traders to short sell an asset has a significant impact on the price of the asset. Ikramov and Yavas (2008) also show that markets with high transaction costs have longer boom and bust periods, and asset prices deviate from fundamental values more in those markets where investments are bulky.

Subrahmanyam (2007) examines liquidity and order flow spillovers across NYSE stocks and REITs. The Granger-causality results indicate that stock market liquidity leads liquidity in REITs. Subrahmanyam argues that REITs serve as substitute investments for the stock market, which causes down-moves in the stock market to increase money flows to the REIT market. King (1966) suggests that 31% of the movements in REITs about their mean values could be attributed to general stock market movements.

The return comparison of publicly traded REITs versus privately held real estate was also the focus of Ling and Naranjo (2003). Ling and Naranjo (2003) argue that, due to infrequency of sales of the same property, NACREIF indices are based on periodic property appraisal, hence suffer from measurement problems. These measurement problems severely weaken the ability of the NACREIF index to capture risk-return characteristics of privately held commercial real estate. As an attempt to overcome these measurement problems, the authors utilize latent-variable statistical methods to estimate an alternative return index for privately held commercial real estate. They find that their alternative index is twice as volatile as the NACREIF total return index and often lead NACREIF returns, but it is less than half as volatile as the NAREIT equity index.

Two recent papers, Pagliari et al. (2005) and Riddiough et al. (2005), compare performance of REIT index with that of NCREIF index as the measure of privately held real estate. Both studies show that when they control for the major differences between the two indices, the performance of the two indices converges. Riddiough et al. (2005) use data from 1980–1998 period and finds that controlling for property-type mix, fees, leverage, partial year financial data and appraisal smoothing differences between the two indices narrows the performance gap between the two indices from four percentage points to 3.08 percentage points, in favor of publicly traded real estate. The performance gap turns statistically insignificant in Pagliari et al. (2005) in the more recent time period 1993–2001 once the authors control for property-type mix, leverage and appraisal smoothing differences between the two indices.

Tuluca et al. (2000) analyze the long-term relationships among five assets classes: T-bills, bonds, stocks, public and private real estate indices. They find that the price indices are non-stationary and cointegrated. Liow (2003) studies the relationship between real estate company stock prices and their net asset values from a mean reversion perspective. He applies cointegration test to both series and finds that they do not drift apart from each other, and are stable in the long term. Liow and Li (2006) investigate whether a long run contemporaneous cointegrating relation exists between real estate company stock prices and NAVs in eight Asian-Pacific real estate markets. They examine the long term behavior using three approaches: panel unit root test, heterogeneous panel cointegration and dynamic panel error-correction modeling. Their overall result is that long run net asset discounts persist in the individual Asian-Pacific real estate markets.

Huang and Zhong (2006) utilize the dynamic conditional correlation GARCH model to build a portfolio of seven asset classes—U.S. stocks, foreign stocks, U.S. bonds, foreign bonds, commodities, Treasury inflation-protected securities (TIPS), and U.S. REITs. They also utilize alternative correlation estimation methods, including the unconditional correlation, the rolling correlation, and the constant correlation. Their findings confirm our results. They find that the optimal portfolio based on the dynamic conditional correlation model outperforms the optimal portfolios based on the other methods (i.e., it produces portfolios with the smallest realized standard deviation given the target return). They also find that diversification benefits of the three asset classes change substantially over time.

Gentry et al. (2004) report that one can earn excess returns by buying REITs that trade at a discount to NAV, and shorting REITs that trade at a premium to NAV. They also argue that there is too much variation in the REIT premium/discount over time, and that it is unlikely that the REIT premiums and discounts reflect the investor sentiment hypothesis of Lee et al. (1991).

One possible explanation for the dynamic correlation between the public and private markets is the changes in real estate market capital flows. Clayton (2003) reports that there exists a correlation between real estate performance and debt capital flows, and the link between property returns and mortgage flows has changed through time. Part of the reason for the boom in REITs and real asset values in recent years, for instance, has been the flow of capital to real estate class of investments due to downturns in stock markets. Examples include the stock market decline during the mild recession of the 1990s and the technology stock decline of the early 2000s.

Unlike the earlier studies, we are able to conduct our analysis at the firm level. Our results confirm earlier results that price discovery generally takes place in the securitized public market. However, our results also show that there are significant variations among different property categories and among firms within each property category. We also find that the correlation between NAV and REIT returns is dynamic for many, but not all, firms in each property category. We again observe variations across different property categories and firms within each property category.

The REIT premium/discount puzzle is similar in many ways to the closed-end fund puzzle. Most closed-end funds hold publicly traded securities and the investors can trade either in the closed-end fund’s shares or directly in the underlying securities. Yet, closed-end fund share prices often differ from their NAV, sum of the values of the individual securities in the fund. There is an important difference between REITs and closed-end funds though; the NAV of a closed-end fund can be easily observed from the individual transaction prices of the securities held in the fund. REITs, on the other hand, own relatively illiquid assets.

As in the case of REIT premium/discount, the more challenging piece of the closed-end fund puzzle is the time-variation in the premium/discount. This led Lee et al. (1991) to a behavioral explanation which claims that closed-end fund discounts are the result of sentiment-based trading by individual investors. Their argument is based on the fact that closed-end funds are mainly held by individuals and are generally avoided by the more sophisticated institutional investors. However, this argument does not hold for REITs since REITs enjoy a high level of institutional ownership. A recent study by Cherkes et al. (2006) builds a theoretical model to offer a rational explanation for the questions of why closed-end funds generally trade at a discount to their NAV, and why investors are willing to buy a closed-end fund at a premium at its IPO, knowing that shortly after the IPO the fund will trade at a discount to its NAV. They argue that closed-end funds offer a means for investors to invest in illiquid securities, and the observed behavior in the market is a result of the trade-off between the liquidity benefits and management fees of closed-end funds.Footnote 5

In the next section, we discuss the methodology that we utilize to examine the relationship between the REIT returns and NAV returns. Our methodology allows us to investigate not only the price discovery in the two markets but also the time-variation in the correlation of the REIT and NAV return series.

Research Methodology

Given the objective of understanding the relationship between publicly traded REITs and their NAV, we have two goals in this paper. Our first goal is to examine if there exists a unidirectional causality between REIT returns and NAV returns, with one market serving as a price discovery vehicle for the other market. Our second goal is to investigate the correlation of REIT and NAV returns over time.

Price Discovery

In most of the previous empirical studies the lead lag relationship between the public market and the private market is examined by estimating granger causality regression where the returns in one market are explained by lagged, contemporaneous and lead returns in the other market (Chan 1992; Stoll and Whaley 1990). Lead-lag relationship between REIT and NAV returns are tested using the following Error Correlation Model (ECM):

where ΔNAV and ΔREIT are the return series of REITs and NAVs in period t, respectively, \( ECM_t = NAV_{t - p} - \beta REIT_{t - q} \) represents the long term relationship between NAV t-p and REIT t-p price series, γ NAV and γ REIT can be interpreted as the speed of adjustment factors, C 1 and C 2 are intercept terms, and ε NAV and ε REIT are white noise errors. The number of cointegration relations is determined by trace test and maximal eigenvalue statistics. In addition, the order of lag, for p and q, is predetermined from the cross correlation relationship between the two markets, and further supported by Akaike Information Criterion (AIC), Schwartz Bayesian Criterion (SBC), and likelihood ratio test. An F-test for the hypothesis a12 = 0 in Eq. (1) and for a21 = 0 in Eq. (2) is applied to test for the Granger causality. For example, if the null hypothesis a12 = 0 in Eq. (1) is rejected, we conclude that the NAV returns are Granger caused by REIT returns, i.e., REIT returns lead NAV returns.

If current NAV returns are significantly correlated with past REIT returns, we would conclude that the price discovery takes place in the REIT market, hence REIT returns lead NAVs. Similarly, if current NAV returns are significantly correlated with future REIT returns, then the price discovery takes place in the NAV market and NAV returns lead REIT returns. Unlike the previous studies on price discovery, we differentiate among different property types and among different firms within each property category, and test for price discovery for each property type and for each individual firm.

Clayton and MacKinnon (2001c) argue that discrepancies between REIT prices and their NAV are caused by “noise” or “information.” The noise theory suggests that when REIT investors become irrationally pessimistic about the securities, the stock market value of the REIT becomes lower than the value of the underlying properties. On the other hand, information based explanation suggests that the securitized market is “more informationally efficient” than the underlying real estate market; i.e., new information is first discovered in the securitized market and causes the share values to rise or fall, and the movements in REIT prices can be used to forecast the future performance of the property market. A test of this argument requires a methodology that would enable us to estimate dynamic trajectories of correlation behavior for the two return series, REITs and NAV.

The Dynamic Conditional Correlation (DCC) Multivariate GARCH Model

Financial time series returns mostly exhibit time varying volatilities with non normal distributions. This problem is referred to as the hetoroskedasticity problem. The strength of the DCC model over alternative models is that it resolves the heteroskedasticity problem by basing the estimation of correlation coefficients on standardized residuals.

Understanding the interaction between two time series returns requires estimating the current correlation. The challenge in estimating the current volatility is to figure out how it relates to the existing data on past returns. Correlation analysis will measure the degree of contagion in the time series data for REITs and their NAV. One way to estimate the correlation is to use all the data available. This will assign a constant correlation between the two return series throughout time. However, this estimation method has a serious shortcoming; it assigns equal weight to all observations, whereas the informational content of the earlier observations may be less important for the estimations than the information included in the more recent observations.

A common method to compute the sample correlation involves the use of moving window analyses, also called rolling correlation estimation (as an example, see Clayton and McKinnon 2001a). This method allows for correlations to change over time. Even though this method is simple to estimate and may capture the time-varying correlation, it has some serious weaknesses. First, it involves choosing an ad hoc window size for the estimation. Second, it weights all observations in the window equally, as in the case of constant correlation case, with the exception that it assigns zero weight for the observation not in the window. As pointed out above, assigning equal weights fails to capture the changing dynamics of correlation inside the window and it causes the correlation estimates to adjust slowly to new information. Failing to capture the changing volatility in returns in any given window will lead to biased correlation coefficient estimates. One implication of this problem, for instance, is that rolling correlation approach may have an upward bias during the high volatility periods in the market (see Forbes and Rigobon 2002).

To overcome the shortcomings of the rolling correlation estimation, we adapt DCC GARCH approach proposed by Engle (2002) to estimate time varying co-movements between REIT and NAV returns. The advantage of DCC is that it accounts for heteroskedasticity directly and is capable of estimating large time-varying covariance matrices for different assets or markets.Footnote 6 In addition, it calculates the current correlation between REIT and NAV return series. This can be instrumental in pinpointing an event coming into one market and estimating the magnitude of the impact of this event in both markets.

The procedure for estimating this model involves two-stage estimation and is relatively straightforward. The first stage entails estimating a univariate GARCH model using the residuals obtained from the error correction model shown in Eqs. (1) and (2). The second stage employs transformed residuals from the first stage estimation to obtain a conditional correlation estimator. This parameterization is shown to preserve the simple interpretation of the univariate GARCH model with an easy procedure to compute the correlation estimator. The standard errors for the first stage parameters are shown to be consistent while the standard errors for the correlation parameters can be modified in order to preserve consistency. DCC model allows us to analyze the correlation when there are multiple regime shifts in response to shocks and crises in the market.

The DCC multivariate GARCH model assumes that the adjusted residuals from the ECM or (VAR) for k assetsFootnote 7 are conditionally multivariate normal with zero mean and covariance matrix, H t ≡ D t R t D t , where D t is the k × k diagonal matrix of time varying standard deviations from the univariate GARCH models with \( \sqrt {h_{ii,t} } \) on the ith diagonal. The elements of D t are characterized by the GARCH(1,1) process:

where i, j = 1,2 represents REIT and NAV returns, a i represents the ARCH effect, or the short-run persistence of shocks to return i, b i represents the GARCH effect, or the contribution of shocks to return i to long-run persistence, and where the property a i + b i < 1 is maintained to ensure stationary. R t is the k × k matrix containing the conditional correlation of the standardized residuals, \( \varepsilon_t = \frac{{r_t }}{{D_t }} = \frac{{r_t }}{{\sqrt {h_{it} } }} \). For \( \rho_{ij,t} \) being the element of R t and i ≠ j, we have the conditional covariance of \( h_{ij,t} = \rho_{ij,t} \sqrt {h_{ii,t} } \sqrt {h_{jj,t} } \), where \( \rho_{ij,t} = \frac{{q_{ij,t} }}{{\sqrt {q_{ii,t} } \sqrt {q_{jj,t} } }} \) with q ij,t as the conditional covariance between the standardized residuals ε it and ε jt . The conditional covariance q ij,t is written as the following mean reverting process for DCC(1,1):

where \( \overline{{\rho_{ij} }} \)is the unconditional correlation between REIT and NAV returns. The parameters α and β are the DCC parameters that are estimated. These two parameters capture the effects of previous shocks and previous dynamic conditional correlations on current dynamic conditional correlations. If α and β are both equal to zero, then the constant correlation model is sufficient. Engle estimates the parameters from the below log-likelihood function:

First term is the volatility component, and the second term is the correlation component.

As stated earlier, the advantage of the DCC Multivariate GARCH model is that it preserves the simple interpretation of the univariate GARCH models while providing a consistent estimate of the correlation matrix (Kearney and Poti 2003).

Empirical Results

Data

The daily dataset in this research involves REIT prices and NAV values from February 2001 to September 2007. REIT prices and NAV values are obtained from SNL financial. SNL calculates the NAV of a REIT by appraising the real estate holdings of that REIT. The appraisal of an income property is often done by using the direct capitalization approach where aggregate Net Operating Income of the REIT is divided by a weighted average capitalization rate.Footnote 8 Since NAV values are based on estimation, not on frequently repeated transactions data, NAV estimates will vary from one analyst to another.Footnote 9 The use of appraisals in determining NAV values is also being criticized for appraisal smoothing, which refers to the argument that appraisal-based estimates smooth changes in NAV values, which in turn causes downward bias in estimates of return volatility. SNL estimates for NAV values depend on analysts valuation. They collect one to sixteen estimates for a particular building.

The data includes 12 different REIT types as classified according to the type of properties owned by these REITS: Diversified, Health Care, Hotel, Industrial, Manufactural Homes, Multifamily, Office, Regional Mall, Retail, Self Storage, Shopping Center, and Specialty. Total number of REITs is 146. For each REIT type we have a minimum of four and a maximum of twenty eight companies. Our observations for different REITs cover different time periods. For example, Capital Lease classified under Diversified has observations from 11/21/2005 to 9/7/2007, whereas Washington Real Estate Investment Trust classified under Diversified has observations from 1/2/2001 to 8/17/2007. As a result, our analysis cover differing time periods for different REITs depending on the availability of data. Table (1) provides the descriptive statistics of the data. Table 1 suggests that REIT returns are relatively more volatile than NAV returns. NAV returns have a larger value of kurtosis, hence indicating less normality for NAV returns than REIT returns. Figures (1) and (2) illustrate the data for a representative REIT within each property type, since it would be impractical to plot all 146 REITs. The representative REIT in each property category is the REIT with the longest time series observation in that category. Figure (1) plots the time series of the representative REITs in each property category and their corresponding NAVs. Figure (2) presents the log returns of the representative REITs, calculated as \( \log \left( {\frac{{P_{i,t} }}{{P_{i,t - 1} }}} \right) \) where P i,t is the price level i, i = {REIT price, NAV}, at time t. The time interval t in our data is uneven in that it varies from firm to firm and over time; some firms have daily data while others have weekly data, and some firms may not have observations for every day or week.

REIT and NAV series. Following graphs plot the time series of REIT stock prices and the corresponding NAVs for a sample REIT in each of the 12 REIT categories. The sample REIT within each REIT category is the REIT with the longest time series observations

Return Plot. Following graphs present the log returns of the data series for a sample REIT in each of the twelve REIT categories. The sample REITs are the same as those in Fig. 1

Price Discovery

The lead-lag relationship between the REIT and NAV returns is examined by estimating Eqs. (1) and (2). Based on the AIC, SBC criteria and the likelihood ratio test, we use N = 3 as the order of lags (N) to examine the price discovery in the public versus private markets for each of the twelve REIT types.

As shown in Table (2), we first utilize the Augemented Dicky-Fuller Test (ADF) to check for non-stationary properties of each NAV and REIT series. Johansen cointegraton procedure is then adopted to decide whether cointegration relations exist between each NAV and REIT price series. The number of cointegration relations is determined by a trace test and maximal eigenvalue statistics. Table (3) reports the average estimates of the error correction terms under ECM framework shown in Eq. (1) based on twelve types of non-stationary NAV and REIT price series. For Diversified properties, for example, the significant ratio for the coefficient γREIT is 3/4, suggesting that this coefficient is significant at 10% level for 3 out of the total 4 sample firms in the case of 2 correlation relations. We do not report the ECM estimates for non-cointegrated paired NAV and REIT price series in Table (3) since ECM will be simplified to pure VAR process of the first difference of the price series without error correction terms in this case.

Table (4) summarizes the granger causality results of Eqs. (1) and (2) for each REIT within twelve property categories. The F-statistics reported is the average of the F-statistics estimates for the sample firms in each property group. We also report the Significant Ratio for each property category; the ratio of the number of firms for which the corresponding causality is significant at 10% level to the total number of firms in that property category. For example, in the case of 2 cointegration relations, the significant ratio of 3/4 for Diversified properties implies that the overall Lag REIT returns lead NAV returns at 10% significance in 3 out of 4 sample firms. The number 4 is the total number of firms within Diversified categories with 2 cointegration relations within NAV and REIT price series. As stated earlier, this is the first study, to our knowledge, that examines the price discovery at the firm level.

Examining Table (4), we find that in most categories the lag values of REIT returns have a significant predictive power for the NAV returns. There are more firms whose REIT returns lead NAV returns, except for Industrial, Manufactured, and Retail categories where number of firms whose REIT returns lead NAV returns is the same as the number of firms whose NAV returns lead REIT returns. The results of Table (4) in general confirm earlier results that price discovery takes place in the securitized public market. However, our results also show that there are variations across different property types and across individual firms. The percentage of firms for which Lag REIT returns lead NAV returns varies from 35% (6/17) for Shopping Center and 40% (2/5) for Self-Storage to zero percent for Retail and 25% (2/8) for Regional Malls.

Correlation Over Time

We next test to see if the correlations of REIT and NAV returns are changing through time and whether or not the correlation between the two return series varies from one property type to another. For this, we utilize the dynamic conditional correlation multivariate GARCH method. The method estimates the DCC parameters and the time varying conditional correlations among the variables of interest. The correlation of the two time series will always vary as the window of estimation changes, but may indicate only small fluctuations. Therefore, we first need to check if the correlations are dynamic and not constant.

Table (5) displays the univariate GARCH (1,1) and DCC parameters where (c 1, a 1, b 1) are GARCH(1,1) parameters for NAV series, (c 2, a 2, b 2) are GARCH (1,1) parameters for REIT series, and (α, β) are the DCC parameters. We test for DCC (m,n) model where m = 1,2,3 and n = 1,2. Later, we only report the best of each model by looking at each model’s likelihoods. Significant α and/or β values in Table (5) indicate a strong dynamic correlation between REIT log returns and NAV log returns. Since we run the estimations firm by firm, we report the number of firms with a significant α and β in each property group. Table (5) shows that there is at least one firm within each property category with a dynamic correlation between NAV and REIT returns. For example, within the Diversified group, nine out of fourteen REITs confirm dynamic correlation. While twenty two of the twenty eight Office REITs confirm dynamic correlation, only two out of the six Industrial REITs display dynamic correlation. Furthermore, the sum of α and β coefficients being close to 1 suggests a strong degree of persistence for the series of correlation. Adding up α and β values for the twelve REIT types indicates that Office REITs have the highest degree of persistency between REIT and NAV returns, followed by Self-Storage and Shopping Center REITs.

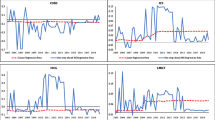

The correlation estimates are displayed for each of the twelve property types in Fig. 3. The representative REITs in Fig. 3 are the same as those in Figs. 1 and 2. As demonstrated for representative firms in Fig. 3, the correlation between REIT price returns and NAV returns is dynamic and displays changes over time.

As indicated earlier, the DCC GARCH approach enables us to estimate the current correlation between REIT and NAV return series. The estimates of the current correlation between the REIT and NAV return series can help us identify the impact of a particular current event or news release. As an example, consider the impact of the negative shock of September 11, 2001. Table 6 presents the correlation estimates for the twelve representative REITs for the four observation periods around September 11, 2001.Footnote 10 The correlation between REIT and NAV returns for the Health Care REIT (NHP; Nationwide Health Properties, Inc.), for instance, jumps from 9.5% on August 16th to –60.1% on October 1st. Similarly, we see significant jumps in the correlation for the Regional Mall REIT (CBL; CBL & Associates Properties) from–0.6% on August 23 rd to 14.3% on October 2nd. Some of the REITs (VNO; Vornado Realty Trust, ARE; Alexandria Real Estate Equities, Inc.), on the other hand, do not display changes in correlation before and after September 11th.Footnote 11 This result once again illustrates the need for property level analysis of the correlation returns and how they may react to a news release or a current event.

Two of our results raise important questions: Why is it that price discovery process displays variations across property types, and why do the direction of causality and correlation between REIT and NAV return series change over time? These are very relevant but difficult questions. First, it is worth indicating that our study is not the first study to point out the time-varying nature of the direction of casuality and correlation coefficients. Other examples in the literature include Chandrashekaran (1999) and Clayton and MacKinnon (2001c). Chandrashekaran (1999) computes correlation coefficients using monthly excess returns on a REIT index and the S&P 500 index and reports that the correlation was around 61% in 1975–1979, then increased to 79% in 1980–1984, and dropped to 48% in 1990–1996. Clayton and MacKinnon (2001c) compute correlation coefficients using quarterly returns on a NAREIT equity REIT index, the Russell 2000 index and the S&P 500 index and find that the correlation of the REIT index with each of the stock indices dropped significantly from the period 1979–1984 to the period 1992–1998.

Second, the answers to these questions are likely to vary across properties and through time. For instance, Case et al. (2008) highlight the importance of the relaxation in 1993 of a regulation known as “the five-or-fewer rule.”Footnote 12 Giambona et al. (2008) study five major property types (industrial properties, residential apartments, hotels, office buildings and retail shopping structures) and find that these property types represent five distinct lines of business with unique economic sensitivities. The authors argue that fundamental property characteristics affect capital structure across property types, which in turn could impact return correlations across property types. A recent study by Clayton et al. (2009) reports that investor sentiment played a pricing role in private commercial real estate market during the 1996–2007 period. Another possible explanatory factor could be differences across property types and over time in going-private activity in the industry. In addition to such time period and industry specific events, there could obviously be firm specific reasons as well. All this makes it very difficult to provide a unifying explanation for the observed differences in the direction of casuality and correlation coefficients across sectors and through time.

Summary and Discussion

The objective of this paper has been to investigate the relationship between REIT returns and NAV returns. For this purpose, we consider two issues. First, we study whether there exists a unidirectional causality between REIT returns and NAV returns, with one market serving as a price discovery vehicle for the other market. Then, we examine an important component of the risk analysis, the correlation between the REIT and NAV returns. Unlike the earlier studies in the literature, we differentiate among different property types and different firms within each property type, and examine if different firms and different property types exhibit varying price discovery patterns. Furthermore, we utilize a new estimation method that enables us to have more accurate estimates of the correlation between REIT and NAV return series over time. The data set allows us to conduct the causality and correlation analysis for each of the firms in the sample separately.

Our Granger-causality tests in general confirm earlier empirical results that price discovery takes place in the securitized public market. However, our results also show that there are variations among different firms and property types. We identify the firms in each property category for which the REIT (NAV) returns lead NAV (REIT) returns. Our dynamic conditional correlation GARCH tests confirm our expectation that the correlation between NAV and REIT returns changes over time. There is at least one firm within each property category with a dynamic correlation between NAV and REIT returns. Furthermore, we find persistence for the series of correlation and variations across property types and individual firms.

The methodology utilized in this study also enables us to estimate the current correlation between REIT and NAV return series. This, in turn, can help us identify the impact of a particular current event or news release on the correlation between the REIT and NAV return series.

By utilizing a firm level data, the current study highlights the importance of conducting the causality and correlation tests at the firm level. The results indicate that comparing the public and private markets at the index level, even after controlling for the property type, offers an incomplete picture. There are considerable variations across firms within each property type. For any given property category, REIT returns could be leading NAV returns for some firms while NAV returns could be leading REIT returns for some other firms. Similarly, for any given property category, the correlation between the two returns can be dynamic for some firms but not for some other firms. Clearly, these results have significant implications for constructing and updating an optimal portfolio of firms within and across different property types.

Notes

To our knowledge, this is the first study that examines the price discovery and correlation of REIT and NAV returns at the firm level

An application of the dynamic correlation multivariate GARC model to build an optimal portfolio can be found in Case et al. (2008) and Huang and Zhong (2006). Case et al. (2008) construct an optimal portfolio of RETis, stocks, bonds and cash while the portfolio of Huang and Zhong (2006) consists of seven asset classes—U.S. stocks, foreign stocks, U.S. bonds, foreign bonds, commodities, Treasury inflation-protected securities (TIPS), and U.S. REITs

Cherkes et al. (2006) also offer a nice review of the literature on this issue

Engle (2002) compares the DCC model with several other estimators, including moving average methods, and demonstrates the superiority of the DCC model. Two recent studies (Case et al. 2008; Huang and Zhong 2006) show that an optimal portfolio based on the DCC model would outperform an optimal portfolio based on alternative models

In our case, k is equal to 2 and includes REIT and NAV returns

The capitalization rate varies from location to location, across property types, and over time. The capitalization rate used in the NAV estimations reflects the property mix (apartment, office, industrial, etc.), geographic location, and growth prospects of the property holdings of the REIT

The reason for the discrepancy between two NAV estimates is due to noise in the calculations of capitalization rates and net operating income. Cap rates are often obtained from surveys of players in local markets and the net operating income needs to be estimated from the REIT’s financial statements

The four dates in the table are determined by the availability of data. The correlation analysis around September 11, 2001 could not be conducted for HLT (Hilton Hotel), NNN (Commercial Net Lease Reality, Inc.), and EPR (Entertainment Properties Trust) REITs because the NAV data for these firms is not available prior to September 11th

One possible explanation for the changes in the correlations around September 11, 2001 is that the attacks on that day prompted investors to re-estimate both REIT values and NAVs

The five-or-fewer rule refers to the restriction on REITs that the five largest shareholders cannot collectively own more than 50% of the company’s stock

References

Barkham, R., & Geltner, David G. (1995). Price discovery in American and British property markets. Real Estate Economics, 23, 21–44. doi:10.1111/1540-6229.00656.

Benveniste, L., Capozza, D., & Seguin, P. (2001). The value of liquidity. Real Estate Economics, 29(4), 633–660. doi:10.1111/1080-8620.00026.

Case, B., Yang, Y., & Yildirim, Y. (2008). Dynamic correlations among asset classes: REIT and stock returns, Working Paper.

Chan, K. (1992). A further analysis of the lead-lag relationship between the cash market and stock index futures market. Review of Financial Studies, 5, 123–152. doi:10.1093/rfs/5.1.123.

Chandrashekaran, V. (1999). Time-series properties and diversification benefits of REIT returns. Journal of Real Estate Research, 17, 91–112.

Chau, K. W., Macgregor, B. D., & Schwann, G. (2001). Price discovery in the Hong Kong real estate market. Journal of Property Research, 18(3), 187–216. doi:10.1080/09599910110060064.

Cherkes, M., Sagi, J., Stanton, R. (2006). A liquidity-based theory of closed-end funds. Working Paper.

Clayton, J. (2003). Capital flows and asset values: a review of the literature and exploratory investigation in a real estate context. University of Cincinnati, working paper.

Clayton, J., & MacKinnon, G. (2001a). Explaining the discount to NAV in REIT Pricing: noise or information? RERI Working Paper.

Clayton, J., & MacKinnon, G. (2001b). Liquidity, the private real estate cycle, investor sentiment and the premium or discount to net asset value in REIT Pricing. RERI Working Paper.

Clayton, J., & MacKinnon, G. (2001c). The time-varying nature of the link between REIT, real estate and financial asset returns. Journal of Real Estate Portfolio Management, 7(1), 43–54.

Clayton, J., Ling, D. C., & Naranjo, A. (2009). Commercial real estate valuation: fundamentals versus investor sentiment. Journal of Real Estate Finance and Economics, 38, 5–37. doi:10.1007/s11146-008-9130-6.

Engle, R. (2002). Dynamic conditional correlation—A simple class of Multivariate GARCH models. Journal of Business & Economic Statistics, 20, 339–350.

Engle, R., & Sheppard, K. (2001). Theoretical and empirical properties of dynamic conditional correlation multivariate GARCH. NBER Working Papers 8554.

Forbes, K., & Rigobon, R. (2002). No contagion, only interdependence: measuring stock market comovements. Journal of Finance, 57, 265–302. doi:10.1111/0022-1082.00494.

Gentry, W. M., Jones, C. M., & Mayer, C. J. (2004) REIT reversion: stock price adjustments to fundamental value. Columbia University Working Paper.

Giambona, E., Harding, J. P., & Sirmans, C. F. (2008). Explaining the variation in reit capital structure: the role of asset liquidation value. Real Estate Economics, 36, 111–137. doi:10.1111/j.1540-6229.2008.00209.x.

Haruvy, E., & Noussair, C. (2006). The effect of short selling on bubbles and crashes in experimental spot asset markets. Journal of Finance, 3, 1119–1157. doi:10.1111/j.1540-6261.2006.00868.x.

Huang, J-Z., & Zhong, Z. (2006). Time-variation in diversification benefits of commodity, REITs, and TIPS Working Paper, Penn State University.

Ikramov, N., & Yavas, A. (2008). What affects the efficiency of the real estate market: an experimental study. Working Paper.

Kearney, M. A., & Poti, V. (2003). DCC-GARCH modelling of market and firm-level correlation dynamics in the Dow Jones Eurotoxx50 index. Working Paper, Trinity College Dublin.

King, B. F. (1966). Market and industry factors in stock price behavior. Journal of Business, 39, 139–190. doi:10.1086/294847.

Lee, C. M. C., Shleifer, A., & Thaler, R. H. (1991). Investor sentiment and the closed-end fund puzzle. Journal of Finance, 46, 75–109. doi:10.2307/2328690.

Ling, D., & Ryngaert, M. (1997). Valuation uncertainty, institutional involvement, and the underpricing of IPOs: the case of REITs. Journal of Financial Economics, 43, 433–456. doi:10.1016/S0304-405X(96) 00891-4.

Ling, D., & Naranjo, A. (2003). The dynamics of REIT capital flows and returns. Real Estate Economics, 31, 405–434. doi:10.1111/1540-6229.00071.

Liow, K. H. (2003). Propery company stock price and net asset value: a mean reversion perspective. Journal of Real Estate Finance and Economics, 27(2), 235–255. doi:10.1023/A:1024780404907.

Liow, K. H., & Li, Y. (2006). Net asset value discounts for asian-pacific real estate companies: long-run relationships and short-term dynamics. Journal of Real Estate Finance and Economics, 33(4), 363–388. doi:10.1007/s11146-006-0338-z.

Myer, N., & Webb, J. (1993). Return properties of equity REITs, common stocks and commercial real estate: a comparison. Journal of Real Estate Research, 8, 87–106.

Newell, G., & Chau, K. W. (1996). Linkages between direct and indirect property performance in Hong Kong. Journal of Property Finance, 7(4), 9–30. doi:10.1108/09588689610152363.

Pagliari, J. L,. Jr, Scherer, K. A., & Monopoli, R. T. (2005). Public versus private real estate equities: a more refined, long-term comparison. Real Estate Economics, 33, 147–187. doi:10.1111/j.1080-8620.2005.00115.x.

Riddiough, T. J., Moriarty, M., & Yeatman, P. J. (2005). Privately versus publicly held asset investment performance. Real Estate Economics, 33, 121–146. doi:10.1111/j.1080-8620.2005.00114.x.

Stoll, H. R., & Whaley, R. E. (1990). The dynamics of stock index and stock index futures returns. Journal of Financial and Quantitative Analysis, 25(4), 441–468. doi:10.2307/2331010.

Subrahmanyam, A. (2007). Liquidity, return, and order-flow linkages between REITs and the stock market. Real Estate Economics, 35, 383–408. doi:10.1111/j.1540-6229.2007.00194.x.

Tuluca, W., Myer, F. C. N., & Webb, James R. (2000). Dynamics of private and public real estate markets. Journal of Real Estate Finance and Economics, 21(3), 279–296. doi:10.1023/A:1012055920332.

Author information

Authors and Affiliations

Corresponding author

Additional information

We are grateful to Dennis Capozza, Brad Case, Jim Clayton, Joseph Pagliari, Dogan Tirtiroglu, Editor and the anonymous referee for their helpful comments and Real Estate Research Institute (RERI) for their financial support.

Rights and permissions

About this article

Cite this article

Yavas, A., Yildirim, Y. Price Discovery in Real Estate Markets: A Dynamic Analysis. J Real Estate Finan Econ 42, 1–29 (2011). https://doi.org/10.1007/s11146-009-9172-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-009-9172-4