Abstract

This article examines the impact of detailed tourism expenditure on the long-run economic growth by employing autoregressive distributed lag approach and Hatemi causality test to investigate causality for 2005:I to 2012:1 in Turkey. New data set tourism detailed expenditure—is employed that has not previously been used for the causality of tourism expenditure on economic growth. The results of the bounds test show that there is a sustainable long-run relationship between each of the tourism expenditure and economic growth. The results of the causality test, on the other hand, show that there is bidirectional causality between university graduate tourists’ expenditure and economic growth and a causal flow from high school tourism expenditure to GDP growth which is verified growth-led tourism hypothesis. Results reveal that university and post graduate degree with tourists’ expenditure is more successful on explaining the long-run relationship between tourism expenditure and economic growth in Turkey. This result implies a policy that, although Turkey need to focus more on tourism development for all level of education to reach higher real income levels; policy makers should concentrate on attracting the attention of university graduate tourist to gain more from tourism industry.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

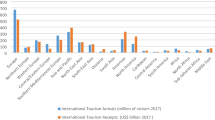

From 1990 to 2012, the countries of the southern and eastern Mediterranean: Algeria, Egypt, Israel, Jordan, Lebanon, Libya, Morocco, Syria, Tunisia and Turkey—illustrated the highest growth rates of inbound world tourism. The economic performance of tourism in southern and eastern Mediterranean countries was surprising given region risks such as natural disasters and the politic and economic uncertainties. Although, there were various crises (political, financial and economic) in the world such as 2008, no major impact is observed on this tourism growth (Lanquar 2013).

Despite the slowdown in the tourism potential of the Arab spring in early 2011, the tourism sector in countries such as Algeria, Israel and Turkey continued the progress (See Table 1).

Turkey has the highest share in this group of countries with 31.7 million international visitors. With this share, Turkey is the 6th top destination in the world after three other Mediterranean countries (France, Spain and Italy). At 2011, Turkey ranks 12th in the world in terms of International tourism, receipts.

Turkey ranks first in receipts (US$ 20.8 billion) arrivals (31.7 million) in southern and eastern Mediterranean countries (See Tables 1 and 2).

Tourism industry development has been the center of attention of study in recent times. A general agreement has appeared that it not only raises foreign exchange reserve, but also creates employment opportunities, encourages the growth of the tourism industry and by virtue of this, triggers overall economic growth (Lee and Chang 2008). In other words, tourists provide a significant part of the necessary financing for especially developing countries which are traditionally dependent upon primary products in exports.

Balaguer and Cantavella-Jorda (2002) theorized the tourism-led growth (TLG) hypothesis, which postulates that the economic growth of countries can be generated not only by increasing the amount of physical and human capital, but also by expanding tourism exports. There are also the cultural and environmental outcomes of tourism, and these costs may be considered as externalities. Of course, whether or not the development of tourism will encourage the economy will depend on whether the benefits outweigh the negative externalities from tourism. In other words, the development of tourism does not always bring about economic growth. Despite the belief in tourism-led economic development, It is possible that the increase in tourism may or may not lead the economic growth (Po and Huang 2008).

Hazari and Ng (1993) suggest that tourism can decrease economic welfare and have a negative effect on economic growth under monopolistic power. Over the past few decades, empirical studies on the relationship between tourism development and economic growth has been extensively research for different country/countries in different years and employing different methods, but the direction of its causality remains as yet an unsolved puzzle.

In the literature, we discern three main hypothesis for the causal relationship between tourism development and real GDP growth. The first hypothesis states that tourism is a major driver of economic growth, and this view is referred to as the TLG hypothesis. The second view is that economic growth contributes to the growth, which is referred to as the growth-led tourism hypothesis. The last view argues that both tourism and economic growth Granger-cause each other (Kumar 2014).

Although tourism has become a crucial export sector in the Turkey, responsible for the generation of jobs as well as income, very few studies investigate the relationship between tourism expenditure and economic growth in Turkey and the empirical relationship between tourism expenditure and economic growth is still ambiguous as seen in Table 3. The present study, as a contribution to the literature, differs from the previous studies in several respects.

First, the most of the previous studies used either Johansen or Engle-Granger procedures for investigating the relationship between tourism expenditure and economic growth. In this paper, recently developed autoregressive distributed lag (ARDL) approach to co integration was utilized.

Second, because of some limitations of Toda-Yamamoto causality procedureFootnote 1 which was used for determining the causal relationships between tourism expenditure and economic growth by some previous studies, this study utilizes recently developed causality test by Hatemi (2012) for examining the causal relationships between tourism expenditure and economic growth.

Third, since unstable co integration parameters will cause invalid empirical implications, this article also involves stability analysis of Brown et al. (1975) in order to verify the stability of co integration parameters.

Fourth, in order to solve the problems of data size and a power property, ADF-WS unit root test is employed. Fifth, selecting true lag order is so important. Selecting a higher order lag length than true one cause an increase in the mean square forecast errors of the VAR and that under fitting the lag length often generates auto correlated errors. Hatemi-J Criteria (HJC) is employed to pick true lag order which is not sensitive to the way the variables are ordered in the model.

Sixth, to the best of our knowledge, there is no study which focuses on tourist’s expenditure in the line with educational level on economic growth. Tourism expenditure impact on economic growth has been investigated very often. However, in this study, the characteristics of tourist spending are addressed. In this context, the expenditures of tourists by level of education affect on economic growth are important. Nowadays cultural tourism is chosen instead of marine tourism. So how is this situation impact on economic growth? This study is a pioneering work in this context. Hence, this paper aims to fulfill this gap and contribute to the empirical literature.

The rest of the paper is organized as follows: The next section describes the data, methodology and the results from empirical analysis. Section 3 presents conclusion and policy implications of the paper.

2 Data, methodology and results

We have estimated our models using quarterly data for Turkey covering the period from 2003:I to 2012:1. While tourism expenditure with educational level data is obtained from Turkish Statistical Institute (TurkStat), real GDP data is attained from International Financial Statistics (IFS) database. The features of the tourism expenditure series are further highlighted in Table (4), which shows descriptive statistics for each series.

The data in the Table 4 shows that university graduate tourist’ expenditure is the largest component of tourism expenditure; while, only literate group’ is the smallest in Turkey.

In unit root analysis, to have good size and power properties, Augmented Dickey-Fuller test (ADF-WS) is employed. Leybourne et al. (2005) have also recently explained that weighted symmetric ADF-WS has good size and power properties when it is compared with the other unit root tests. Therefore, it needs much shorter sample sizes than conventional unit root tests to attain the same statistical power. To overcome the low power problems associated with conventional unit root tests, especially in small samples, we therefore choose the ADF-WS test of Park and Fuller (1995).

According to the results, while some of the variables are I(0) such as secondary graduate and university graduate, the other variables are I(1) (See Table 5). Since the unit root test results showed that the considered variables have different integration orders, it is decided to employ the ARDL approach (i.e., the bounds testing approach) to co integration developed by Pesaran et al. (2001). The ARDL representation which should be estimated for the bounds testing approach is as follows:

where \(Y\) is real income and \(T\) is the indicator of tourism development \(\Delta \) is the difference operator, \(p\) is the lag length, and \(u\) is serially uncorrelated error term. All variables are in natural logarithms which makes the parameters elasticity.

There are two stages that the ARDL procedure has. In the first one, the null hypothesis of no-co integration is tested against the alternative hypothesis of co integration. This process is based on the F-statistic. Since the asymptotic distribution of this F-statistic is non-standard irrespective of whether the variables are I(0) or I(1), Pesaran et al. (2001) have generated two sets of critical values. One set assumes that all variables are I(0) and other set assumes that all variables are I(1). This provides a bound covering all possible classifications of the variables. If the calculated F-statistics lies above the upper level of the bound, the null hypothesis is rejected, supporting co integration relationship in the long-run. If the calculated F-statistic lies below the lower level of the bound, the null hypothesis cannot be rejected, indicating lack of co integration.

Once the long-run relationship is supported, the error-correction model (ECM) from the equations above is estimated as the second stage of the ARDL procedure. The ECM models are as follows:

where \(\uppsi \) is the error-correction parameter and EC is the residual obtained from the equation.

The bounds testing approach to co integration requires carrying out the F test on the selected ARDL models including appropriate lag lengths. In this stage, it is imposed maximum two lags on the level of variables and then employed Schwarz Bayesian Criterion (SBC) to select the optimum lag numbers.

The F-statistics for co integration analysis based on the selected ARDL models are reported in Table 6 for each level. Calculated F-statistics show that, except only literate and primary graduate, represent co integration relationship among variables in consideration. Moreover, significant negative error-correction parameters also confirm the existence of co integration relationship for those samples.

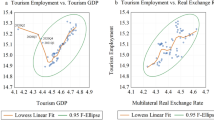

Table 7 shows the long-run co integration vector for each educational level. Accordingly, estimated coefficients indicate that all tourism expenditure with educational level has positive impacts on economic growth for Turkey with statistical significance at 1 % level.

By focusing on the magnitude of statistically significant educational level coefficients, it is realized that university and post graduate degree with tourist are more successful on explaining the relationship between tourism expenditure and economic growth in Turkey. This result implies a policy that Turkey should invest in tourism to attract the attention of university graduate tourist in order to advantage more from tourism. Since the ARDL method needs the assumptions of the OLS are presented, Table 8 exhibits the results for diagnostic checking.

It is demonstrated that none of the estimated models (at least 1 % significance level) have serial correlation, heteroscedasticity, non-normality and functional form. As well as the diagnostics tests, stability of the co integration parameters was proved by the CUSUM and CUSUMSQ. These tests for parameter stability based on the recursive regression residuals were developed by Brown et al. (1975). According to the results, all of the models have stable parameters over the time.

Causality between tourism expenditure and economic growth was investigated by employing a recently developed causality analysis by Hatemi (2012). According to this method, the modified Wald (MWALD) statistic is employed which tests the null hypothesis of non-Granger causality. Hatemi-J utilizes bootstrapping simulation technique to manage the possibility of autoregressive conditional heteroscedasticity (ARCH) effects.

The bootstrap critical values are generated for 1, 5 and 10 % levels of significance. Two of the most successful criteria according to the simulation results presented in the literature are Schwarz Bayesian information criterion (1978) and the Hannan–Quinn information criterion (1979). On the other hand, the earlier studies illustrated that each of these two different criteria can perform better than the other depending on the properties of the true VAR model. Hatemi-J Criteria is employed to pick true lag order which was suggested by Hatemi (2003). The following information criterion is used to select the optimal lag order \((p)\):

where \(\big | {\mathop {\Omega }\limits ^{\cap }{}_j}\big |\) is the determinant of the estimated variance–covariance matrix of the error terms in the VAR model based on lag order j, n is the number of equations in the VAR model and \(T\) is the number of observations.

where \(t\)=1,2,...,\(T\), the constants \(y_{1,0}\) and \(\hbox {y}_{2,0}\) are the initial values, and the variables \(\varepsilon _{1i}\) and \(\varepsilon _{2i}\) signify white noise disturbance terms. Positive and negative shocks are defined as the following:

\(\varepsilon _{1i}^{ + } = \max (\varepsilon _{1i} ,0),\varepsilon _{2i}^{ + } = \max (\varepsilon _{2i} ,0),\varepsilon _{1i}^{ - } = \min (\varepsilon _{1i} ,0)\) and \(\varepsilon _{2i}^- =\min (\varepsilon _{2i} ,0)\) respectively. Therefore, one can express \(\varepsilon _{1i} =\varepsilon _{1i}^+ +\varepsilon _{1i}^- \) and \(\varepsilon _{2i} =\varepsilon _{2i}^+ +\varepsilon _{2i}^- \) It follows that

As a final point, the positive and negative shocks of each variable can be defined in a cumulative form as \(y_{1t}^+ =\sum _{i=1}^t {\varepsilon _{1i}^+ }, y_{1t}^- =\sum _{i=1}^t {\varepsilon _{1i}^- }, y_{2t}^+ =\sum _{i=1}^t {\varepsilon _{2i}^+ }\) and \(y_{2t}^- =\sum _{i=1}^t {\varepsilon _{2i}^- }\) . In the following, the case of testing for causal relationship between positive cumulative shocks is checked. Assuming that \(y_t^+ =(y_{1t}^+ ,y_{2t}^+ )\), the test for causality can be implemented by using the following vector autoregressive model of order \(p\), VAR \((p)\):

The null hypothesis that \(k\)th element of \(y_t^+ \) does not Granger-cause the \(\omega \) th element of \(y_t^+\) is tested after selecting the optimal lag order. That is, the following hypothesis is tested:

\(\mathbf{H}_\mathbf{0}\) the row \(\omega \), column \(k\) element in \(A_{r}\) equals zero for \(r\)= 1 ,..., p. In order to define a Wald test in a compact form, we make use of the following denotations:

The null hypothesis of non-Granger causality,

\(\mathbf{H}_\mathbf{0}\) \(\hbox {C}\beta = 0\), is tested by the following test method:

where \(\otimes =\) the Kronecker product, \(Y=ap\times n(1+n(p+d)\), \(V_U =\) the estimated variance-covariance matrix of residuals, when the null hypothesis of non-Granger causality is not imposed, \(\varphi =vec\hbox { }(F),\) where vec represents the column-stacking operator. Kronecker product, and \(Y\) is a \(p\times n(1 + np)\) indicator matrix with elements ones for restricted parameters and zeros for the rest of the parameters. \(V_{U}\) is the variance–covariance matrix of the unrestricted VAR model estimated as \(\hbox {V}_{U}=\frac{\xi ^{\prime }_U \xi _U }{T-q}\), where \(q\) is the number of parameters in each equation of the VAR model. When the assumption of normality is fulfilled, the Wald test statistic above has an asymptotic \(x^{2}\) distribution with the number of degrees of freedom equal to the number of restrictions to be tested (in this case equal to \(p\)). The Table 9 reveals that there is bi-causality between university graduate tourists’ expenditure and economic growth. That is, TLG hypothesis and growth-led tourism hypothesis are present for Turkey in terms of university graduate tourists. On the other hand, there is a causal relationship from high school graduate tourists’ expenditure to GDP growth which is verified growth-led tourism hypothesis. For secondary and post-graduate degree tourists’ expenditure, the findings provide the absence of causality between tourism expenditure and reel GDP which means the validity of the neutrality hypothesis.

3 Conclusion

Recently developed ARDL approach and Hatemi (2012) causality tests are employed to study linkages between tourism expenditure and economic growth in literate, Primary Graduate, Secondary Graduate, High School Graduate, University Graduate and Post-Graduate as classified by TURKSTAT in Turkey for 2003:I to 2012:1.

To co integration was employed for this purpose. In addition, the study employs recently developed causality test by Hatemi (2012) for investigating the causal relationships between tourism expenditure in line with educational level and economic growth. Calculated F-statistics show that, except only literate and primary graduate, represent co integration relationship among variables. Furthermore, significant negative error-correction parameters also confirm the existence of co integration relationship for those samples. According to causal relationships, there is bi-causality between university graduate tourists’ expenditure and economic growth. That is, TLG hypothesis and growth-led tourism hypothesis are valid for Turkey in terms of university graduate tourists. On the other hand, there is a causal relationship from high school tourism expenditure to GDP growth which is verified growth-led tourism hypothesis. For secondary and post-graduate degree tourists’ expenditure, the findings provide the absence of causality between tourism expenditure and reel GDP which means the validity of the neutrality hypothesis.

Results reveal that university and post graduate degree with tourists’ expenditure is more successful on explaining the long-run relationship between tourism expenditure and economic growth in Turkey. This result implies a policy that, although policy makers need to concentrate more on tourism expenditure for all level of education to reach higher real income levels; Turkey should concentrate on attracting the attention of university graduate tourist to gain more from tourism.

Notes

Asymmetric causal effects stemming from asymmetric information phenomenon and absence of no separation between the causal impacts of positive or negative shocks are some of the most important factors that determine causality among variables. Since Toda-Yamamoto procedure does not take this asymmetric structure into account, this paper uses causality test developed by Hatemi (2012) which is good at dealing with this problem.

References

Arslanturk, Y., Balcilar, M., Ozdemir, Z.A.: Time-varying linkages between tourism receipts and economic growth in a small open economy. Econ. Model. 28(2011), 664–671 (2011)

Aslan, A.: Türkiye’de Ekonomik Büyüme ve Turizm İlişkisi Üzerine Ekonometrik Analiz. Erciyes Üniversitesi SBE Dergisi 24, 1–11 (2008)

Balaguer, L., Cantavella-Jorda, M.: Tourism as a long-run economic growth factor: the Spanish case. Appl. Econ. 34, 877–884 (2002)

Brown, R.L., Durbin, J., Evans, J.M.: Techniques for testing the constancy of regression relationships over time. J. Roy. Stat. Soc. 37, 149–163 (1975)

Chien-Chiang, Lee, Chun-Ping, Chang: Tourism development and economic growth: a closer look at panels. Tour. Manag. 29, 180–192 (2008)

Demiroz, D.M., Ongan, S.: The contribution of tourism to the long run Turkish economic growth. Ekonomický Časopis 9, 880–894 (2005)

Gunduz, L., Hatemi, J.A.: Is the tourism-led growth hypothesis valid for Turkey? Appl. Econ. Lett. 12, 499–504 (2005)

Halicioglu, F.: An econometric analysis of the aggregate outbound tourism demand of Turkey. Tour. Econ. 16(1), 83–97 (2010). March 2010 (15)

Hannan, E.J., Quinn, B.G.: The determination of the order of an autoregression. J. Roy. Stat. Soc. 41, 190–195 (1979)

Hatemi, J.A.: A new method to choose optimal lag order in stable and unstable VAR models. Appl. Econ. Lett. 10, 135–137 (2003)

Hatemi, J.A.: Asymmetric causality tests with an application. Empirical Economics (2012). doi:10.1007/s00181-011-0484-x

Hazari, B.R., Ng, A.: An analysis of tourists’ consumption of non-traded goods and services on the welfare of the domestic consumers. Int. Rev. Econ. Financ. 2, 43–58 (1993)

Husein, Jamal, Kara, S.Murat: Research note: re-examining the tourism-led growth hypothesis for Turkey. Tour. Econ. 17(4), 917–924 (2011)

Katircioglu, S.T.: Revising the tourism-led-growth hypothesis for Turkey using the bounds test and Johansen approach for cointegration. Tour. Manag. 30, 17–20 (2009)

Kumar, R.R.: Exploring the nexus between tourism, remittances and growth in Kenya. Qual. Quant. 48(3), 1573–1588 (2014)

Lanquar, R.: Tourism in the Mediterranean: scenarios up to 2030. MEDPRO Report No. 1 (2013)

Leybourne, S.J., Kim, T., Newbold, P.: Examination of some more powerful modifications of the Dickey–Fuller test. J. Time Ser. Anal. 26, 355–369 (2005)

Ozturk, I., Acaravci, A.: On the causality between tourism growth and economic growth: empirical evidence from Turkey. Transylv. Rev. Adm. Sci. 25E(2009), 73–81 (2009)

Park, H.J., Fuller, W.A.: Alternative estimators and unit root tests for the autoregressive process. J. Time Ser. Anal. 16, 415–429 (1995)

Pesaran, M.H., Shin, Y., Smith, R.J.: Bounds testing approaches to the analysis of level relationships. J. Appl. Econ. 16, 289–326 (2001)

Schwarz, G.: Estimating the dimension of a model. Ann. Stat. 6, 461–464 (1978)

Wan-Chen, Po, Bwo-Nung, Huang: Tourism development and economic growth—a nonlinear approach. Phys. A 387(2008), 5535–5542 (2008)

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Aslan, A. The sustainability of tourism income on economic growth: does education matter?. Qual Quant 49, 2097–2106 (2015). https://doi.org/10.1007/s11135-014-0095-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11135-014-0095-7