Abstract

China is in a phase of rapid urbanization and economic development; in addition, the country’s carbon dioxide (CO2) emissions are increasing. Using a multivariate vector error correction model, this paper investigates the relationship between urbanization, income growth and CO2 emissions in China. The empirical evidence shows that the three variables are cointegrated, indicating a long-term relationship among urbanization, income growth and CO2 emissions. Moreover, a Granger causality test reveals that urbanization is the reason for income growth in China. There is also evidence that both urbanization and income growth lead to CO2 emissions. Hence, authorities should pay more attention to mitigating the negative effects on the environment when developing and implementing policies that promote urbanization and income growth. However, CO2 emissions do not cause changes in income and urbanization in China. Therefore, China should enforce stricter policies for reducing CO2 emissions.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Many countries in the developing world—and particularly the larger emerging countries—have experienced rapid-paced urbanization over the past three decades (Wang et al. 2016). China is no exception (Zhu 2016). Implementing important strategic initiatives such as the household registration system reformation resulted in China’s urban population rising to 749.16 million in 2014, 3.34 times larger than it was in 1978. Simultaneously, the urbanization rate rose from 17.92 to 54.77%, an increase of 36.85% (NBS 2015a). In 2011, this process culminated in the urban population surpassing the rural population for the first time in China (NBS 2015a).

Together with urbanization, China’s economy has developed, and per capita income has increased (Han et al. 2011; Liu et al. 2015). In 2009, China became the world’s second largest economy (World Bank 2009). Over the 1978–2014 period, per capita income reached 3.314 thousand CNY (Chinese Yuan) at constant 1978 prices, increasing by a factor of 18.36 (NBS 2015a). Moreover, over the same time span, urban and rural residents’ per capita income reached 2.465 thousand CNY and 0.849 thousand CNY, increasing by multiples of 39.07 and 6.74, respectively (NBS 2015a).

Another phenomenon tracking the growth of urbanization and income is China’s increasing trend of carbon dioxide (CO2) emissions (Wang et al. 2012; Zhang and Da 2013). According to the IPCC, CO2 emissions (the primary greenhouse gas) accounted for 76.7% of total greenhouse gas emissions in 2004 (IPCC 2007). Moreover, developing countries began producing 50% of the world’s CO2 emissions in 2003. China’s total CO2 emissions ranked first in the world in 2006 for the first time and grew to 9680 million tons by 2014, 5.63 times its emissions in 1978 (GCP 2015). Additionally, China’s per capita CO2 emissions, which had been 1.5 tons in 1978, rose to 7.1 tons by 2014 (GCP 2015).

In fact, as Fig. 1 shows, we see that urbanization, income and CO2 emissions have similar increasing trends when we put them into the same framework over the 1981–2014 period. In fact, China’s urbanization, income and CO2 emissions grew at average rates of 3.08, 8.05 and 4.95%, respectively, during this period. Higher urbanization growth rates are found in 1982, 1984 and 1996. The biggest growth rates for income are found in 1982, 1984 and 2007. Moreover, the highest CO2 emissions growth rates are found in 1984, 2004 and 2006. Based on the above information, it is likely that there is a real linkage among these three variables. However, few studies in the previous literature have investigated these three variables together.

Urbanization, income and CO2 emissions in China, 1981–2014. Notes: CE, UR and PI represent per capita CO2 emissions in metric tons, urbanization rate as a percentage and per capita income in Chinese Yuan. Data source: The urbanization rate is taken from China Statistical Yearbook 2015 by the National Bureau of Statistics of the People’s Republic of China (NBS 2015a). Per capita income data are collected from New China in 65 Years (NBS 2015b) and China Statistical Yearbook 2015 (NBS 2015a) by the National Bureau of Statistics of the People’s Republic of China. Per capita CO2 emissions data are from the Global Carbon Atlas published by the Global Carbon Project (GCP 2015)

Most studies of the relationship between two of the three variables employ the Environmental Kuznets Curve (EKC) hypothesis, which presents a single assumption for a causal relationship (Chen et al. 2016). Thus, studies of income and CO2 emissions typically consider income as the cause and CO2 emissions as the result (Ozturk and Acaravci 2013; Govindaraju and Tang 2013; Nasir and Rehman 2011; Jalil and Mahmud 2009). Similarly, studies also consider that CO2 emissions result from urbanization (Wang et al. 2015; Zhu et al. 2012; Martínez-Zarzoso and Maruotti 2011). These studies lack the feedback mechanism from CO2 emissions to income or to urbanization. In this context, the VEC model holds out the promise of providing a coherent and credible approach to data description, forecasting, structural inference and policy analysis (Stock and Watson 2001). Moreover, its simple framework provides a systematic method of demonstrating rich dynamic relationships over multiple time series (Zhang 2016). Therefore, the model has been widely applied in studies of relationships with different variables and has gained acceptance among scholars. This paper will use the vector error correction (VEC) model to investigate the relationships between urbanization, income and CO2 emissions in one framework, which can thus overcome the drawback of a single assumption and objectively detect the mutual relationships among the three variables.

The remainder of this paper is organized as follows: Section 2 presents a review of the relevant literature. Section 3 introduces the study’s methodology and data sources. Section 4 discusses the empirical results, and conclusions and policy implications are presented in Sect. 5.

2 Literature review

Most prior studies focus on the relationship between two of the three variables, i.e., economic growth, urbanization or CO2 emissions.

2.1 The causal relationship between urbanization and economic growth

Many studies that focus on the relationship between urbanization and economic growth suggest that urbanization will promote economic growth because urban economic activities are intensified when a large labor force shifts from agricultural areas to urban-based industrial areas. Hossain (2011) draws this conclusion in nine newly industrialized countries. Kasman and Duman (2015) indicate that urbanization is the cause of economic growth in both EU member and candidate countries. Furthermore, many studies have been focused on China in this regard and showed the same result that urban development brings economic growth (Han et al. 2011; Cheng 2013; Liu 2009). However, Ghosh and Kanjilal (2014) and Pradhan et al. (2014) draw the opposite conclusion that economic growth contributes to urbanization in India and the G20 countries. Moreover, Dogan and Turkekul (2016) show bidirectional causality between the two variables in the USA. In other words, although urbanization promotes economic growth, economic growth also leads to urbanization in the USA. Hossain (2012) find no causal relationship between economic growth and urbanization in Japan. Solarin and Shahbaz (2013) and Salim and Shafiei (2014) draw the same conclusion in Angola and in Organization for Economic Cooperation and Development (OECD) countries.

2.2 The causal relationship between economic growth and CO2 emissions

More attention has gradually been focused on studies of the causal relationship between economic growth and CO2 emissions. First, using Granger causality, some studies conclude that economic growth can lead to increased CO2 emissions because industrial development always leads to higher demands on energy use, giving rise to more environmental pollution. Solarin (2014) finds that economic development significantly contributes to CO2 emissions in Malaysia. Most importantly for our study, Chang (2010) and Jalil and Mahmud (2009) draw the same conclusion in China. Second, a few studies find that CO2 emissions contribute to economic growth but not vice versa (Ang 2008; Mehrara et al. 2011; Menyah and Wolde-Rufael 2010; Pao and Tsai 2010). For example, Ang (2008) shows that the promotion of economic output in Malaysia is attributable to the environmental pollution generated by deforestation. Third, many studies in China, Turkey and India, among other countries, find a bidirectional relationship between economic growth and CO2 emissions (Long et al. 2015; Ghosh 2010; Halicioglu 2009; Wang 2011). However, other studies demonstrate that there is no causal relationship between the two variables in China, the USA and Turkey (Soytas and Sari 2006, 2009; Soytas et al. 2007). Richmond and Kaufmann (2006) show the same result in a study of 36 developed and developing countries. Moreover, Dinda and Coondoo (2006) investigate the causality relationship between economic growth and CO2 emissions in 88 countries and show that there is unidirectional relationship from economic growth to CO2 emissions in Central American countries, unidirectional relationship from CO2 emissions to economic growth in European countries and bidirectional causality between the two variables in African countries.

2.3 The causal relationship between urbanization and CO2 emissions

The relationship between urbanization and CO2 emissions can be summarized in the following three conclusions. First, higher urbanization is the Granger cause of larger CO2 emissions because urbanization greatly changes the population’s settlement and consumptive patterns. In the meantime, the urban industrial production process becomes intensified. What urbanization can bring about is a rapid rise in energy use and severe environmental problems. Wang et al. (2016) and Li et al. (2016) find that urbanization development indeed contributes to higher CO2 emissions in Southeast Asian Nations and the BRICS countries, respectively. Kasman and Duman (2015) indicate that urbanization is the cause of increasing CO2 emissions in EU member and candidate countries. Al-mulali et al. (2012) agree in their study of the following seven world regions: East Asia and the Pacific, Eastern Europe and Central Asia, Latin America and the Caribbean, the Middle East and Northern Africa, Southern Asia, sub-Saharan Africa and Western Europe. In addition, Al-mulali et al. (2012) emphasize that there is a positive correlation between urbanization and CO2 emissions in 84% of these countries. Zhang and Lin (2012) argue that urbanization is positively related to carbon emissions in China. However, in a study of nine emerging industrialized countries, Hossain (2011) draws the opposite conclusion, i.e., that urbanization development cannot “Granger-cause” CO2 emissions. Third, studies have shown bidirectional causality between urbanization and CO2 emissions. Al-mulali et al. (2013) investigate countries in the Middle East and North Africa and show that urbanization development and CO2 emissions reinforce one another. Dogan and Turkekul (2016) also show bidirectional causal relationships between the two variables in the USA. However, Hossain (2012) concludes that there are no causal relationships between urbanization and CO2 emissions in Japan.

Although there are many studies of two of the three variables, no consistent results are obtained. These different conclusions in the previous literature regarding the relationships among these variables may result from different explanatory variable selections, subject/country selections, data time spans, and empirical econometric model specifications (Zhang 2016; Chen et al. 2016; Payne 2010; Hondroyiannis et al. 2002; Masih and Masih 1996).

As the largest developing country in the world, China is facing the conflicting goals of economic development and severe emissions reduction. Therefore, it is key that China uncovers the actual relationship among urbanization, income growth and CO2 emissions. However, to the best of our knowledge, we have not found studies on the relationships between urbanization, income and CO2 emissions together. We have found only two studies that resemble ours. Zhang et al. (2014) find significant relationships from urbanization and economic growth to CO2 emission intensity in China. In addition, Liu et al. (2016) also show that both urbanization and economic growth are the cause of CO2 emissions in China but not vice versa. These studies focus on the macro perspective and mainly use macro-economic indicators such as gross domestic product (GDP), which may be driven by industrial development, investment changes and income changes. Thus, its link to urbanization and CO2 emissions may be more indirect, while our study focuses on the matter from the perspective of citizens and uses a relatively microeconomic indicator: citizens’ income. The relationship between income, urbanization and CO2 emissions is strong. Urbanization may lead to an increase in both income and changes in household consumption structure and to an increase in electric appliances purchasing and use, in particular, and then may lead to higher CO2 emissions. In the meantime, income growth may attract more people to the cities, resulting in growing urbanization. Nonetheless, no study has yet addressed the relationship among the three variables. This study fills this gap.

3 Methodology and data sources

3.1 Methodology

To investigate the relationships among CO2 emissions, income growth and urbanization in China, the following function is proposed (Woodridge 2008; Zhao and Wang 2015):

where \(\ln {\text{CE}}_{t}\) represents CO2 emissions, \(\ln {\text{PI}}_{t}\) is income and \(\ln {\text{UR}}_{t}\) represents urbanization. \(\alpha_{1}\) and \(\alpha_{2}\) are the long-term elasticities of CO2 emissions with respect to income and urbanization, respectively. In the above equation, CO2 emissions are the dependent variable, the other two variables are the independent variables. However, any of the variables might become the dependent variable. Therefore, we utilize the Eviews 8.0 software to construct a VEC model that can objectively detect the dynamic causal relationships among urbanization, income and CO2 emissions. The VEC model is the vector autoregressive (VAR) model with cointegrated restrictions established by several non-stationary series. Thus, the VEC model helps explain and predict the long-term and short-term equilibrium relationships among these non-stationary time series. In this investigation, the VEC form can be expressed as follows:

where \(\Delta\) represents the first difference, t represents the time, \(p - 1\) is the lag lengths in the VEC system, the coefficient matrix \(\beta\) is the impact of independence variable’s short-term changes on the dependent variable, \({\text{ECT}}\) is the error correction term, γ is the extent of adjustment when variables depart from the long-term equilibrium relationship, and \(\varepsilon\) is the error term.

Before building the VEC model, whether the data are stable or integrated in order 1 must be investigated. There are many methods to examine whether a time series is stable. The default test type is augmented Dickey–Fuller (ADF), which is one of the most widely used and accepted unit root test methods (Block et al. 2012). The regression Eq. (3) of the ADF unit root test is shown as follows.

where \(\Delta\) represents the first difference, \(\alpha ,\omega \;{\text{and}}\;b\) denote the coefficients, d represents deterministic exogenous variables, p is the lag difference term, e is the white noise process, and t represents time.

The unit root test has three optional equation types, including \({\text{DT}}0\), \({\text{DT}}1\) and \({\text{DT}}2\) with respect to none, constant and trend types. However, many studies have not clearly introduced how to determine the test equation type. The data-generating process (DGP) recognition (Table 1) will show its merits, but the discussion about DGP is almost nonexistent, except for Hamilton (1994).

If the variables meet the condition of same integrated order, the cointegration test will be performed in this study. According to Engle and Granger (1987) and Granger (1998), cointegration refers to the linear combination of two or more non-stationary time series that may become stationary and indicates that there are long-term equilibrium cointegrating relationships among these unstable variables. Johansen and Juselius (1990) propose the cointegration test based on regression coefficients, which is appropriate to investigate the cointegrating relationships among multiple variables (Asafu-Adjaye 2000; Block et al. 2012). The long-term cointegrating relationships are examined when the statistics for the trace and maximum eigenvalue tests are larger than critical values at the 5% level. Furthermore, the cointegrating VEC model can be built for the Granger causality test, the impulse response and the variance decomposition analysis.

The Granger causality test is based on the cointegrating VEC model. The cointegrating relationship indicates the existence of causality among variables. Nevertheless, the interactive directions between variables are not accurately given by the cointegrating relationship where the Granger causality test shows its merits. Granger causality refers to the prediction contribution one variable makes for another. The null hypothesis is that one variable is not the Granger cause for another, which will be excluded when it passes the significance level at 5%; at that point, the prediction contribution can be confirmed from one variable to another.

To examine the short-term dynamic relationships among variables, Koop et al. (1996) propose generalized variance decomposition. Furthermore, Pesaran and Shin (1998) propose the generalized impulse response method. The impulse response function (IRF) aims to find the future response of each variable to one standard deviation innovation by the other variables in the system. The generalized variance decomposition analysis is used to show the percentage of variation in the forecast error for each variable that can be attributed to other variables’ innovations over various time periods.

3.2 Data sources

This study aims to examine the relationship between urbanization, income and CO2 emissions in China from 1981 to 2014. Our research period begins after 1978, which is the year that marked the beginning of reform and opening up. In particular, in October 1980, China put forward the urbanization development policy to “strictly control large cities, rationally develop medium-sized cities and small cities, and actively develop small towns.” Under this urbanization policy, China’s urbanization rate first reached approximately 20% in 1981. Therefore, our data series are selected beginning in 1981. Moreover, our research data are relatively new compared to the data from other studies. Some studies include data from the 1950s or 1960s. However, at that time, population movements were restricted in China. Individual income was also limited under the planned economy. Thus, this study does not include those periods. This study spans the 1981–2014 period and is thus more in line with our market-oriented features.

Specifically, the empirical analysis utilizes annual time-series data from 1981 to 2014 in China, including the urbanization rate (UR) as a percentage, per capita income (PI) in CNY and per capita CO2 emissions (CE) in metric tons. Urbanization is the proportion of the urban population to the total population. Urbanization data are collected from China Statistical Yearbook 2015 by the National Bureau of Statistics of the People’s Republic of China (NBS 2015a). Per capita income data from 1981 to 2013 can be collected from New China in 65 Years by the National Bureau of Statistics of the People’s Republic of China (NBS 2015b); however, it does not have income data for 2014. We find these data from the China Statistical Yearbook 2015 by the National Bureau of Statistics of the People’s Republic of China (NBS 2015a). Moreover, the income data are calculated at constant 1978 prices. In fact, all the data should be collected from the National Bureau of Statistics of the People’s Republic of China. However, we only find the data for urbanization and income from this source. CO2 emissions data cannot be found there. Although there are data regarding fossil fuel consumption, it is not sufficiently comprehensive to account for CO2 emissions. The Global Carbon Project is an authoritative institution concentrating on the study of greenhouse gases, particularly CO2 emissions from the combustion of fossil fuels, cement production and land-use changes over multiple decades. Moreover, to our knowledge, the Global Carbon Project has more current data regarding CO2 emissions than other institutions. Therefore, the per capita CO2 emissions data are taken from the Global Carbon Atlas published by the Global Carbon Project (GCP 2015). To eliminate heteroskedasticity and linearize the data trend, the data of three time series are converted to natural logarithms in this study, respectively, represented by ln UR, ln PI and ln CE.

4 Empirical results

4.1 Unit root test

This paper adopts the ADF test to determine whether the time-series data are stationary. The unit root test lag length is determined by the Schwarz information criterion (SIC). The DGP is mainly examined using the mean value of difference series. If the mean of difference series is nonzero, the corresponding set DT2 will be used in the unit root test. Conversely, if the mean of the difference sequence is zero, the corresponding set DT1 will be determined. Furthermore, the test will select the set of DT0 if the constant term is zero.

Table 2 presents the mean values of ln CE, ln PI and ln UR at their first differences, which are nonzero. The option containing the constant and time trend will be selected. Next, the ADF unit root test results in Table 3 suggest that the level series among the above three time series all accept the unit root hypothesis but reject it at their first difference. Therefore, ln CE, ln PI and ln UR are all integrated of order 1.

4.2 Johansen cointegration test

According to the ADF unit root test results, ln CE, ln PI and ln UR are integrated of order 1; thus, they meet the Johansen cointegration test condition. To determine the cointegration test lag intervals, the optimal lag order \(p\) of vector autoregressive (VAR) model should be determined by the LR test statistic (LR), the final prediction error (FPE), the Akaike information criterion (AIC), the Schwarz information criterion (SC) and the Hannan-Quinn information criterion (HQ). Based on the lag of first difference, the Johansen cointegration test lag interval is \(p - 1\). Table 4 shows that both the trace statistic and maximum eigenvalue statistic are significant at the 5% level, which indicates 1 cointegrating relationship among urbanization, income and CO2 emissions. The cointegrating relationship denotes the existence of Granger causality among the three variables. However, the VEC model must be estimated because it can distinguish between long-term and short-term Granger causality (Arvin et al. 2015).

4.3 VEC-based Granger causality test

Based on the cointegration test type, the number of cointegration relationships and the lag order of cointegration, we can further establish the VEC (1) model of urbanization, income and CO2 emissions. Chen (2012) notes that if the VEC model contains M variables and C cointegrating relationships, the characteristic polynomial will have M–C roots and will be limited to unit roots. Two roots are limited to 1 on the unit circle because the VEC model contains 1 cointegrating relationship; other reciprocal roots remain inside the unit circle as depicted in Fig. 2. Consequently, the VEC (1) model is stable, and we can further perform the Granger causality test, the impulse response function and the variance decomposition analysis to investigate the interactive relationships among urbanization, income growth and CO2 emissions.

Inverse roots of the AR characteristic polynomial for the VEC model

Both long-term cointegrating relationships and the short-term relationships among CO2 emissions, income and urbanization can be provided by the VEC model. The long-term equilibrium relationship is detected by the error correction term (\({\text{ECT}}_{{_{t - 1} }}\)), which means that the dependent variable tends to close to its long-term equilibrium state in response to changes in the other variables.

As depicted in Table 5, the \({\text{ECT}}_{{_{t - 1} }}\) is not significant when we set \(\Delta \ln {\text{UR}}\) and \(\Delta \ln {\text{PI}}\) as dependent variables. The results represent that there is no long-term causality from income and from CO2 emissions to urbanization, and neither is there from urbanization and CO2 emissions to income. However, when \(\Delta \ln {\text{CE}}\) becomes a dependent variable, the \({\text{ECT}}_{t - 1}\) is significant at the 1% level, indicating that there is long-term causality from urbanization and income to CO2 emissions. The long-term causality can be represented as:

The equation can be expressed as the following:

The above long-term cointegrating relationship shows that urbanization and income growth play a positive role in promoting CO2 emissions. The long-term elasticities of CO2 emissions with respect to urbanization and income are 0.94 and 0.24, respectively. CO2 emissions will increase 0.24% when income improves 1%, and CO2 emissions will increase 0.94% when urbanization increases 1%.

Although the long-term relationship among urbanization, income and CO2 emissions has been detected, short-term causality must also be examined. Therefore, the Granger causality test must be performed. Granger causality indicates that one variable has significant influences on the future values of other variables (Block et al. 2012); each variable may be dependent or independent, and we can obtain the clear direction of causality.

Urbanization, income and CO2 emissions are never islands unto themselves. As listed in Table 5, urbanization is the Granger cause of income growth \(\left[ {{\text{UR}} \to {\text{PI}}} \right]\) because it can pass the significance level test when \(\Delta \ln {\text{PI}}\) is the dependent variable. Likewise, the Granger causality test also reveals that both \(\Delta \ln {\text{UR}}\) and \(\Delta \ln {\text{PI}}\) reject the null hypothesis at the 1% level when \(\Delta \ln {\text{CE}}\) is the dependent variable, which is strong evidence of unidirectional Granger causality running from urbanization to CO2 emissions \(\left[ {{\text{UR}} \to {\text{CE}}} \right]\) and from income growth to CO2 emissions \(\left[ {{\text{PI}} \to {\text{CE}}} \right]\). The urbanization process accompanies economic growth in China, which can offer many relatively high-paying employment opportunities and raises per capita income to higher levels. However, the growth also results in rapidly increasing CO2 emissions because income growth, improvements in standards of living and lifestyle changes directly result in higher demands on various energy sources and products, particularly those fossil fuel products producing substantial amounts of CO2 emissions. Additionally, CO2 emissions cannot cause income growth, which suggests that income will not be reduced if we control CO2 emissions in China. Two related studies support our findings. Liu et al. (2016) show that, in China, there are unidirectional relationships running from economic growth to land urbanization, from land urbanization to CO2 emissions, and from economic growth to CO2 emissions. Zhang et al. (2014) indicate that there are significant unidirectional relationships running from both urbanization and economic growth to carbon emission intensity. In these two studies, both urbanization and economic growth are the Granger cause of CO2 emissions in China, supporting the results in our study. However, the first study draws the conclusion that economic growth can cause land urbanization changes in China, but not vice versa, which results because economic growth—and particularly the economic development of tertiary industries—has stimulated demand for residential land, commerce, entertainment, transportation and land for other urban construction, such that land urbanization has been improved.

4.4 Impulse response analysis

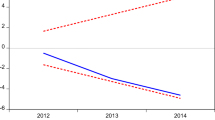

Our previous results offer a brief description of the statistical significance of historical changes. However, the results do not indicate how a variable responds to shocks in other variables during different phases. Hence, we deploy generalized impulse response functions to uncover this information. The generalized impulse response functions is utilized to trace out the effect of a shock in one variable on the current and future value changes in other variables (Arvin et al. 2015). Moreover, this method provides more robust results than the orthogonality method because the results are invariant to the ordering of the variables in the VEC system (Block et al. 2012; Papapetrou 2000). As shown in Fig. 3a, when a standard deviation innovation is attached to urbanization in China, CO2 emissions respond to it in two directions. In the first period, urbanization development has a positive effect on CO2 emissions. By contrast, from the second to the sixth period, the positive response turns into a constant negative response that drops to the minimum −0.018 in the third period. Moreover, the response of CO2 emissions to urbanization is positive from the seventh to the twelfth period and threatens to increase and stay near 0.025.

Generalized impulse responses to one SD innovation

As Fig. 3b shows, CO2 emissions always remain positive when a standard deviation innovation is attached to income. The impact continues multiplying in the first period, reaching a maximum of 0.319. After the sixth period, it continues to decrease but stays above the zero line.

Figure 3c shows that when one standard deviation innovation is attached to urbanization in China, income always remains positive; the maximum is 0.01 in the first period and decreases afterward. The figure remains stable at 0.005 in the fifth and sixth periods. However, the positive impact begins to rise again in the seventh period, reaching 0.008 in the twelfth.

4.5 Variance decomposition

The variance decomposition results are shown in Figs. 4, 5 and 6, which reports the contribution rate of each variable innovation to the movement of the dependent variable.

Generalized variance decomposition of \(\ln {\text{CE}}\)

Generalized variance decomposition of \(\ln {\text{PI}}\)

Generalized variance decomposition of \(\ln {\text{UR}}\)

As Fig. 4 shows, CO2 emission innovations account for a gradually smaller contribution rate to explain the variation in the forecast error. In the first six periods, the rate of contribution drops rapidly and subsequently levels out. The contribution of income changes to the variation in the forecast error for CO2 emissions continues to increase and remains at 46.50%, beginning in the eleventh phase. The contribution rate of urbanization changes soars from the outset, hitting its peak of 43.72% in the fourth period, only to subsequently decline and become steady near 34.00% at the end. We can draw the conclusion that income and urbanization changes have a relatively higher contribution rate to explain the variation in the forecast error for CO2 emissions.

Figure 5 presents the variance decomposition of income. The contribution of income innovation to its own variation in the forecast error gradually lessens and remains stable at 87.80% after the eighth phase. By contrast, urbanization changes make a gradually larger contribution in the first eight periods, achieving a maximum at 9.51% before falling to approximately 9.00%. The contribution rate of CO2 emissions changes with the variation in the forecast error for income; it decreases slowly throughout the periods and steadies at 3.28% through the twelfth period.

Finally, Fig. 6 reports the variance decomposition of urbanization. In the first three stages, the contribution rate of urbanization innovation to itself has a gradually decreasing trend with a minimum of 71.11%. In the fourth period, it begins to rise and then remains at 76.00%. The contribution rate of CO2 emissions changes to the variation in the forecast error for urbanization continues to decrease over the first three periods and recovers to increase in the fourth period; however, the contribution rate decreases again in the seventh phase and reaches 0.56% in the twelfth phase. As for income innovation, it contributes to the variation in the forecast error for urbanization in the first three periods, reaching a maximum of 28.24%. In the fourth period, it begins to decrease and remains at 23.00% from the ninth phase on.

5 Conclusions and policy implications

This study attempts to empirically examine the causal relationship between urbanization, income and CO2 emissions in China using time-series data over the 1981–2014 period. Before testing the causal relationship among variables within a VEC system, a cointegration analysis is conducted. The results show that there is a long-term equilibrium relationship among urbanization, income and CO2 emissions.

One of our key results involves the relationship between urbanization and income growth, as we reveal a unidirectional causality from urbanization to income growth in China. Furthermore, the generalized impulse response functions and variance decomposition confirm the results of the Granger causality tests. These results suggest that the Chinese government should continue to push forward with urbanization and encourage rural residents to move into urban areas because urbanization will offer them higher-paying jobs. The increased income can help people to improve their living standards.

Two other key results have some important policy implications. Unidirectional causality is examined from urbanization to CO2 emissions and from income to CO2 emissions, indicating that both urbanization and income growth can lead to increased CO2 emissions in China. Furthermore, the results are confirmed by generalized impulse response functions and variance decomposition. The impulse responses show that shocks in urbanization and income have significant positive effects on CO2 emissions. Moreover, the variance decomposition results show that income growth gradually takes over changes in urbanization as the largest contributor of CO2 emissions. In general, urbanization can increase people’s income, which may lead to changes in their lifestyles, such as the use of cars and electrical appliances. All those will result in increased CO2 emissions and lead to extreme weather and respiratory diseases. However, the results suggest that CO2 emissions cannot cause income growth, which means that income will not be reduced if we control CO2 emissions in China. The Chinese government can directly reduce CO2 emissions by developing and implementing stricter policies, such as carbon taxation and carbon emissions trading. Under such environmental regulation polices, those enterprises who emit CO2 would pay for their polluting behaviors. Environmental cost payments encourage enterprises to apply clean technologies or improve energy efficiency. Simultaneously, enterprises should become more socially responsible by cultivating a corporate culture of environmental protection and establishing environmental funds. For individuals, it is necessary to establish the consumption concept of environmental protection, which means that improving the energy consumption structure and increasing green consumption should be taken into account. In other words, individuals can change their lifestyles by buying more energy-efficient vehicles or taking public transportation.

By implementing this set of policies, we predict that urbanization and income can continue to rise, while CO2 emissions are reduced. There may be less extreme weather. Moreover, with improved air quality, the rates of asthma and other lung-related ailments will decrease.

References

Al-mulali U, Sab CNBC, Fereidouni HG (2012) Exploring the bi-directional long run relationship between urbanization, energy consumption, and carbon dioxide emission. Energy 46:156–167

Al-mulali U, Fereidouni HG, Lee JYM, Sab CNBC (2013) Exploring the relationship between urbanization, energy consumption, and CO2 emission in MENA countries. Renew Sustain Energy Rev 23(4):107–112

Ang JB (2008) Economic development, pollutant emissions and energy consumption in Malaysia. J Policy Mod 30(2):271–278

Arvin MB, Pradhan RP, Norman NR (2015) Transportation intensity, urbanization, economic growth, and CO2 emissions in the G-20 countries. Util Policy 35:50–66

Asafu-Adjaye J (2000) The relationship between energy consumption, energy prices and economic growth: time series evidence from Asian developing countries. Energy Econ 22:615–625

Block H, Rafiq S, Salim R (2012) Coal consumption, CO2 emission and economic growth in China: empirical evidence and policy responses. Energy Econ 34:518–528

Chang CC (2010) A multivariate causality test of carbon dioxide emissions, energy consumption and economic growth in China. Appl Energy 87(11):3533–3537

Chen DT (2012) Applied econometrics: advanced lecture notes on Eviews. Peking University Press, Beijing

Chen PY, Chen ST, Hsu CC, Chen CC (2016) Modeling the global relationships among economic growth, energy consumption and CO2 emissions. Renew Sustain Energy Rev 65:420–431

Cheng C (2013) Dynamic quantitative analysis on Chinese urbanization and growth of service sector. In: LISS 2012: proceedings of 2nd international conference on logistics, informatics and service science, pp 663–670

Dinda S, Coondoo D (2006) Income and emission: a panel-data Based cointegration analysis. Ecol Econ 57:167–181

Dogan E, Turkekul B (2016) CO2 emissions, real output, energy consumption, trade, urbanization and financial development: testing the EKC hypothesis for the USA. Environ Sci Pollut Res 23:1203–1213

Engle RF, Granger CWJ (1987) Cointegration and error correction: representation, estimation and testing. Econometrica 55:251–276

GCP (Global Carbon Project) (2015) Global carbon atlas 2015. http://www.globalcarbonatlas.org/?q=en/emissions. Accessed 14 July 2016

Ghosh S (2010) Examining carbon emissions economic growth nexus for India: a multivariate cointegration approach. Energy Policy 38(6):3008–3014

Ghosh S, Kanjilal K (2014) Long-term equilibrium relationship between urbanization, energy consumption and economic activity: empirical evidence from India. Energy 66:324–331

Govindaraju VGRC, Tang CF (2013) The dynamic links between CO2 emissions, economic growth and coal consumption in China and India. Appl Energy 104:310–318

Granger CWJ (1998) Some recent developments in a concept of causality. J Econom 39:71–83

Halicioglu F (2009) An econometric study of CO2 emissions, energy consumption, income and foreign trade in Turkey. Energy Policy 37(3):1156–1164

Hamilton JD (1994) Time series analysis. Princeton University Press, New Jersey

Han X, Wu PL, Dong WL (2011) An analysis on interaction mechanism of urbanization and industrial structure evolution in Shandong, China. Econ Manag 11:1291–1300

Hondroyiannis G, Lolos S, Papapetrou E (2002) Energy consumption and economic growth: assessing the evidence from Greece. Energy Econ 24:319–336

Hossain MS (2011) Panel estimation for CO2 emissions, energy consumption, economic growth, trade openness and urbanization of newly industrialized countries. Energy Policy 39(11):6991–6999

Hossain S (2012) An econometric analysis for CO2 emissions, energy consumption, economic growth, foreign trade and urbanization of Japan. Low Carbon Econ 3:92–105

IPCC (Intergovernmental Panel on Climate Change) (2007) Climate Change 2007: the physical science basis. Cambridge Press, New York

Jalil A, Mahmud SF (2009) Environment Kuznets curve for CO2 emissions: a cointegration analysis for China. Energy Policy 37(12):5167–5172

Johansen BS, Juselius K (1990) Maximum likelihood estimation and inference on cointegration with applications to the demand for money. Oxf Bull Econ Stat 52(2):169–210

Kasman A, Duman YS (2015) CO2 emissions, economic growth, energy consumption, trade and urbanization in new EU member and candidate countries: a panel data analysis. Econ Mod 44:97–103

Koop G, Pesaran MH, Potters SM (1996) Impulse response analysis in nonlinear multivariate models. J Econom 74:119–147

Li L, Wang Y, Kubota J, Han R, Zhu X, Lu G (2016) Does urbanization lead to more carbon emission? Evidence from a panel of BRICS countries. Appl Energy 168:375–380

Liu Y (2009) Exploring the relationship between urbanization and energy consumption in China using ARDL (auto regressive distributed lag) and FDM (factor decomposition model). Energy 34(11):1846–1854

Liu TY, Su CW, Jiang XZ (2015) Is economic growth improving urbanization? A cross-regional study of China. Urban Stud 52(10):1883–1898

Liu YS, Yan B, Zhou Y (2016) Urbanization, economic growth, and carbon dioxide emissions in China: a panel cointegration and causality analysis. J Geogr Sci 26(2):131–152

Long X, Naminse EY, Du J, Zhuang J (2015) Nonrenewable energy, renewable energy, carbon dioxide emissions and economic growth in China from 1952 to 2012. Renew Sustain Energy Rev 52:680–688

Martínez-Zarzoso I, Maruotti A (2011) The impact of urbanization on CO2 emissions: evidence from developing countries. Ecol Econ 70:1344–1353

Masih A, Masih R (1996) Energy consumption, real income and temporal causality: results from a multi-country study based on cointegration and error-correction modeling techniques. Energy Econ 18:165–183

Mehrara M, Sharzei G, Mohaghegh M (2011) The relationship between health expenditure and environmental quality in developing countries. J Health Adm 14(46):79

Menyah K, Wolde-Rufael Y (2010) Energy consumption, pollutant emissions and economic growth in South Africa. Energy Econ 32(6):1374–1382

Nasir M, Rehman FU (2011) Environmental Kuznets curve for carbon emissions in Pakistan: an empirical investigation. Energy Policy 39:1857–1864

NBS (National Bureau of Statistics of the People’s Republic of China) (2015a) China statistical yearbook 2015. China Statistics Press, Beijing

NBS (National Bureau of Statistics of the People’s Republic of China) (2015b) New China in 65 years. China Statistics Press, Beijing

Ozturk I, Acaravci A (2013) The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ 36:262–267

Pao HT, Tsai CM (2010) CO2 emissions, energy consumption and economic growth in BRIC countries. Energy Policy 38(12):7850–7860

Papapetrou E (2000) Oil price shocks, stock market, economic activity and employment in Greece. Energy Econ 23:511–532

Payne J (2010) A survey of the electricity consumption-growth literature. Appl Energy 87:723–731

Pesaran MH, Shin Y (1998) Generalized impulse response analysis in linear multivariate models. Econ Lett 58(1):17–29

Pradhan RP, Arvin MB, Norman NR, Bele SK (2014) Economic growth and the development of telecommunications infrastructure in the G-20 countries: a Panel-VAR Approach. Telecommun Policy 38(7):634–649

Richmond AK, Kaufmann RK (2006) Is there a turning point in the relationship between income and energy use and/or carbon emissions? Ecol Econ 56:176–189

Salim RA, Shafiei A (2014) Urbanization and renewable and non-renewable energy consumption in OECD countries: an empirical analysis. Econ Mod 38:581–591

Solarin SA (2014) Tourist arrivals and macroeconomic determinants of CO2 emissions in Malaysia. Anatolia 25:228–241

Solarin SA, Shahbaz M (2013) Trivariate causality between economic growth, urbanization and electricity consumption in Angola: cointegration and causality analysis. Energy Policy 60:876–884

Soytas U, Sari R (2006) Can China contribute more to the fight against global warming? J Policy Mod 28:837–846

Soytas U, Sari R (2009) Energy consumption, economic growth and carbon emissions: challenges faced by an EU candidate member. Ecol Econ 68:1667–1675

Soytas U, Sari R, Ewing BT (2007) Energy consumption, income, and carbon emissions in the United States. Ecol Econ 62:482–489

Stock JH, Watson MW (2001) Vector autoregressions. J Econ Perspect 15(4):101–115

Wang ZM (2011) A reexamination of urbanization and urban-rural income gap in China. Econ Geogr 8:1289–1293

Wang ZH, Zhang B, Yin JH (2012) Determinants of the increased CO2 emission and adaption strategy in Chinese energy-intensive industry. Nat Hazards 62:17–30

Wang Y, Zhang X, Kubota J et al (2015) A semi-parametric panel data analysis on the urbanization-carbon emissions nexus for OECD countries. Renew Sustain Energy Rev 48:704–709

Wang Y, Chen LL, Kubota J (2016) The relationship between urbanization, energy use and carbon emissions: evidence from a panel of Association of Southeast Asian Nations (ASEAN) countries. J Clean Prod 112(2):1368–1374

Woodridge JM (2008) Introductory econometrics: a modern approach. South-Western College Pub Press, Cincinnati

World Bank (2009) Data bank: China. http://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=CN. Accessed 27 Nov 2016

Zhang H (2016) Exploring the impact of environmental regulation on economic growth, energy use, and CO2 emissions nexus in China. Nat Hazards 84:213–231

Zhang YJ, Da YB (2013) Decomposing the changes of energy-related carbon emissions in China: evidence from the PDA approach. Nat Hazards 69:1109–1122

Zhang CG, Lin Y (2012) Panel estimation for urbanization, energy consumption and CO2 emissions: a regional analysis in China. Energy Policy 49:488–498

Zhang YJ, Liu Z, Zhang H (2014) The impact of economic growth, industrial structure and urbanization on carbon emission intensity in China. Nat Hazards 73:579–595

Zhao Y, Wang SJ (2015) The relationship between urbanization, economic growth and energy consumption in China: an econometric perspective analysis. Sustainability 7:5609–5627

Zhu JM (2016) Making urbanisation compact and equal: integrating rural villages into urban communities in Kunshan, China. Urban Stud. doi:10.1177/0042098016643455

Zhu HM, You WH, Zeng ZF (2012) Urbanization and CO2 emissions: a semi-parametric panel data analysis. Econ Lett 117:848–850

Acknowledgements

This research was financially supported by the Natural Sciences Foundation of China (NSFC) (71203203), the MOE project of Humanities and Social Sciences (12YJCZH057), the Beijing Higher Education Young Elite Teacher Project (YETP0667), the Fundamental Research Funds for the Central Universities (2652015149 and 2652016134) and the Project from the Strategic Research Center of Oil and Gas Resources of MLR of China (Grant No. 1A15YQKYQ0112).

Author information

Authors and Affiliations

Corresponding author

Additional information

Xiangrong Ma and Jianping Ge have contributed equally to this study and shared first authorship.

Rights and permissions

About this article

Cite this article

Ma, X., Ge, J. & Wang, W. The relationship between urbanization, income growth and carbon dioxide emissions and the policy implications for China: a cointegrated vector error correction (VEC) analysis. Nat Hazards 87, 1017–1033 (2017). https://doi.org/10.1007/s11069-017-2807-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11069-017-2807-5