Abstract

With concerns regarding global climate change increasing, recent studies on adapting to nonstationary climate change recommended a different planning strategy that could spread risks. Uncertainty in global climate change should be considered in any decision-making processes for flood mitigation strategies, especially in areas within a monsoon climate regime. This study applied a novel planning method called real option analysis (ROA) to an important water resources planning practice in Korea. The proposed method can easily be applied to other watersheds that are threatened by flood risk under climate change. ROA offers flexibility for decision-makers to reflect uncertainty at every stage during the project planning period. We successfully implemented ROA using a binomial tree model, including two real options—delay and abandon—to evaluate flood mitigation alternatives for the Yeongsan River Basin in Korea. The priority ranking of the four alternatives between the traditional discount cash flow (DCF) and ROA remained the same; however, two alternatives that were assessed as economically infeasible using DCF, were economically feasible using ROA. The binomial decision trees generated in this study are expected to be informative for decision-makers to conceptualize their adaptive planning procedure.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In response to increasing concerns regarding global climate change, many studies have been conducted since the mid-1970s. Research on climate change can be broadly categorized as either the assessment of its impact or the establishment of adaptation strategies. However, until the mid-2000s, most climate change studies were focused on impact assessment and rarely on the development of adaptation strategies. The establishment of adaptation strategies to cope with climate change is mainly hindered by “deep uncertainty”—a situation where the likelihood of an unknown event is also unknown. Lempert et al. (2000) warned that traditional decision-making methods might not be viable under deep uncertainty.

Research on climate change adaptation began to attract more interest after the decision analysis framework was introduced in the Intergovernmental Panel on Climate Change (IPCC) Third Assessment Report (IPCC 2001). Recent studies on adapting to nonstationary climate change recommended a different planning strategy that could spread risks. UKCIP (2003) suggested a decision-making process that provides decision-makers with multiple options in order to reduce potential risks induced by climate change uncertainty. Means et al. (2010) introduced five decision-making methods applicable to water resource planning under climate change: classic decision analysis, scenario planning, robust decision-making, real options, and portfolio planning.

In water resource planning, decisions have generally been made based on economic evaluation using the discounted cash flow (DCF) approach to carry forward the alternatives. The DCF process estimates the monetary value of a project using the concept of the time value of money. However, Trigeorgis (1996) pointed out that DCF may not be an appropriate approach under uncertainty because it tends to underestimate the option value attached to growing profitable lines of business (Myers 1977). Michailidis and Mattas (2007) also pointed out that another limitation of the DCF approach is that it depends on the assumption that future cash flows follow a constant pattern. More recently, Samis et al. (2011) discussed three shortcomings of the DCF approach: it does not consider (1) the randomness in cash flow variables, (2) the effects of contingent cash flow and flexibility, and (3) the dynamic variation of cash flow risk through time. Brugnach et al. (2008) stressed that flexibility should be considered in order to deal with uncertainty in water resource management. Under these circumstances, there is need for a new method to overcome the DCF’s limitations in addressing uncertainty.

The IPCC recently reported that there is a high possibility that past floods larger than those recorded since 1900 have occurred during the past five centuries in northern and central Europe, western Mediterranean region, and eastern Asia (Stocker et al. 2013). In addition, it is also expected that the increase in seasonal mean precipitation is pronounced in the East and South Asian summer monsoons while the change in other monsoon regions is subject to larger uncertainties. Because future increase in precipitation extremes related to monsoon seasons is very likely in South America, Africa, East Asia, South Asia, Southeast Asia, and Australia (Stocker et al. 2013), uncertainty in global climate change should be considered in any decision-making processes for flood mitigation strategies, especially in areas within monsoon climate regimes.

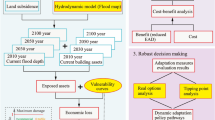

To consider climate change uncertainty in the decision-making process, we applied a novel planning method called real options analysis (ROA) to an important water resource planning practice. ROA spreads risks over “time” using “options.” The word “real” is derived from real assets to which the option pricing theory is often applied for the valuation of investment (Kim and Chung 2017). The concept of real options (RO) was introduced by Myers (1977), and proposed as an alternative to the DCF approach. This concept was initiated from the financial sector and later extended to various sectors such as electronics, agriculture, and engineering systems (Myers 1977; Kester 1984; Mason and Merton 1985; Trigeorgis and Mason 1987). Over the last decade, ROA began to get attention in water resources planning studies (Steinschneider and Brown 2012; Deng et al. 2013). Seo (2006) applied ROA to evaluate the economic feasibility of three irrigation systems in Texas to consider uncertainty in cotton yield. Michailidis and Mattas (2007) utilized ROA for an irrigation dam investment analysis using four options under uncertainty in water price. Kjaerland (2007) presented a valuation study of hydropower investment opportunities in Norway using the conceptual ROA framework of Dixit and Pindyck (1994). Recently, Steinschneider and Brown (2012) utilized ROA to hedge against the risk associated with operational forecasts and unexpected climate outcomes. Deng et al. (2013) developed an integrated framework to value investments in urban water management systems under uncertainty. These preceding studies demonstrated how ROA could improve DCF in the field of water resources systems such that ROA could become attractive to decision-makers who are faced with uncertainty. However, these studies focused mostly on uncertainty in price, but seldom on the uncertainties of rainfall and streamflow induced by global climate change.

Therefore, the objective of this study was to develop a new version of ROA as a decision-making framework that could be used for water resources planning by convenient use of global circulation model (GCM) projections to consider rainfall uncertainty in the future, and to evaluate the potential benefits from ROA by comparison to traditional economic analysis (DCF). To validate the applicability of the proposed ROA approach for local-scale analysis, an existing flood mitigation plan in Korea was tested.

2 Theoretical background

2.1 Discounted cash flow

The DCF approach is a valuation method used to estimate the attractiveness of an investment opportunity (Hussey and Hussey 1999). It uses future free cash flow projections and discounts them to arrive at a present value (PV) estimate, which is used to evaluate the potential for investment. The net present value (NPV) is an important term in DCF, and is defined as the difference between the present value of benefits (for example, flood damage reduced by a flood mitigation structure) and the present value of costs (for example, the installation and the operational costs of the flood mitigation structure) (Kim and Chung 2017). The evaluation of investment is often accompanied by a cost-benefit analysis (CBA). A key element of CBA is that it utilizes the DCF approach to calculate future costs and benefits to a present value (Buurman and Babovic 2016). The general procedure of DCF is given below (Kodukula and Papudesu 2006).

-

1.

Estimate the investment cost to launch the product today.

-

2.

Estimate the annual revenues and annual costs, and calculate the annual net cash flows for the expected project life cycle.

-

3.

Choose a discount rate for the entire project life that reflects the risks associated with the project.

-

4.

Calculate the PVs of each annual net cash flow by discounting the future values. (To do this, multiply the cash flow by the corresponding discount factor.)

-

5.

Add the PVs of all the annual net cash flows for the entire project life cycle.

-

6.

Calculate the project NPV by subtracting the investment cost from the sum of the PVs of the annual net cash flows.

2.2 Real options analysis

2.2.1 Overview

The ROA applies option valuation techniques to long-term investment decisions. A real option (RO) is the right, but not the obligation, to undertake certain project initiatives (Trigeorgis 1996). The ROA model that best depicts the decision problem being considered is then selected from several techniques, such as the Black-Scholes analytical approach (Lau et al. 2006), the binomial tree approach (Michailidis and Mattas 2007), the Monte Carlo simulation approach (Jeuland and Whittington 2013), or the decision tree approach (Borison and Hamm 2008). The selected ROA model is used to calculate the financial values of the individual combinations of the alternatives and options as a function of time with given monetary information such as price change (Kim and Chung 2017).

Unlike traditional economic analysis methods such as DCF, ROA is characterized by two main features: flexibility and uncertainty. The flexibility of ROA allows decision-makers to make changes to the project by providing options reflecting the value of each option at every step during the project. Seven types of options were categorized by Trigeorgis (1996): an option to defer (Tourinho 1979; McDonald and Siegel 1986; Paddock et al. 1988; Majd and Pindyck 1987), a time-to-build option, an option to alter the operating scale (Stulz 1982), an option to abandon (Myers and Majd 1990), an option to switch (Baldwin and Ruback 1986), a growth option, and a multiple interaction option. The options to defer and abandon are associated especially with the project lifetime, which could lead to positive values by consideration of additional information (Trigeorgis 1996).

Decision-making is difficult because of uncertainties in future scenarios, such as precipitation and water-demand projections. In terms of uncertainty, ROA quantifies the changes in the PVs over the project planning period. There can be a range of possible outcomes over the project lifetime owing to increasing uncertainty as a function of time. Thus, ROA accounts for this whole range of uncertainty using stochastic processes and calculates a “composite” option value for a project, considering only those outcomes that are favorable (Kodukula and Papudesu 2006).

The maximum value of all the options at each node is called the “expanded NPV (ENPV),” which is the addition of NPV and the “option premium” (Trigeorgis 1996). Therefore, the difference between ENPV and NPV at each node is the “option premium”. This difference indicates the value of using the options throughout the entire investment opportunity period (Kim and Chung 2017).

2.2.2 The binomial tree model procedure

The ROA often employs a decision tree strategy that can include uncertain but possible adaptation pathways. In this study, we employed the binomial tree model proposed by Cox et al. (1979) because of its ability to illustrate the probability of a given scenario. Both ROA with a binomial tree and Adaptation Pathways (AP) are recent approaches for dealing with uncertainty in policy making (Kim and Chung 2017). The adaptation pathways approach is used to assess current policies and management strategies and to determine when they no longer meet the clearly stated objectives (Buurman and Babovic 2016). The key element of AP is something called adaptation tipping points (Kwadijk et al. 2010). Therefore, in many cases where there can be multiple management strategies leading to similar outcomes, but with different cost and benefits, AP is preferred. In contrast, one of the premises of ROA is that flexibility has a value: a different pathway might be taken or a policymaker might adopt a strategy to wait until more information is available (Buurman and Babovic 2016). ROA used with the binomial tree focuses on the flexibility provided by managerial options for a single strategy. Thus, we used the binomial tree model in this study. Moreover, it can handle a wider variety of option types and its results are easier to explain than for other approaches.

Figure 1 shows the model configuration and the value propagation in a typical binomial tree, which requires three parameters, u (upward), d (downward), and p (risk-neutral probability), as described in Eq. (1) to (3).

where σ is the volatility represented by the standard deviation of the natural logarithm of the underlying free cash flow returns, δt is the time associated with each time step, and r is the risk-neutral interest rate.

Model configuration and value of the binomial tree. a Node. b Value (i = 0,1,2,…, N and j = 0,1,2,…,i)

In the model configuration of the binomial tree shown in Fig. 1a, each node represents a possible decision pathway at each discrete time. Figure 1b presents how the option value is calculated using the three predefined parameters, u, d, and p. Once u, d, and p are given, the option value V(i, j) at each node can be calculated. Because V(i + 1, j) = uV(i, j) and V(i + 1, j + 1) = dV(i, j) in Fig. 1, all the values of V(i, j) are automatically calculated with the initial value V(0,0) (= V(0)) using the forward-moving procedure. Alternatively, V(0), V(N,0), and V(N,N) are first specified, and then all other values of V(i,j) are calculated using the backward-moving procedure, where u and d are given in Eq. (4) and (5), respectively, while p is given in Eq. (3),

The biggest assumption of the risk-neutral approach is that the future option value remains unchanged regardless of future uncertainty. Therefore, to calculate the risk-neutral expectations, the underlying value needs to move backward through the binomial tree as described in Eq. (6).

Once the binomial tree is set up, ENPV at each node is then estimated as the maximum value of the applied options and NPV. The general procedure of ROA is given below.

-

1.

Estimate the parameters: upward (u), downward (d), and risk-neutral probability (p).

-

2.

Calculate the unit time value of the implementation at each node → NPV for all nodes and time steps.

-

3.

Create the option matrix for each alternative by calculating the option values moving backward from the maximum NPVs at the last stage.

-

4.

Compare the ENPVs of the alternatives.

-

5.

Calculate the option premium of each alternative (i.e., option premium = ENPV − NPV).

3 Case study

3.1 Existing feasibility study

To examine the effectiveness of ROA for the practice of water resources planning, and taking into account uncertainty in future climate change, we selected an existing study called “The Comprehensive Flood Mitigation Plan: Yeongsan River Basin (Ministry of Land, Infrastructure, and Transport, MLIT 2005)” to analyze using DCF. The Yeongsan River Basin is located in the southwestern part of South Korea (Fig. 2). The headwaters of the Yeongsan River flow 130 km and discharge into the Yellow Sea. Approximately two million people reside in the basin, within an area of 3460 km2. Owing to typhoon-related precipitation events in Korea, the flood mitigation plan is updated every 5 years as part of the comprehensive water resources management for the four major river basins in Korea. This includes the Yeongsan River Basin. MLIT (2005) suggested four alternatives to the flood mitigation plan based on past flood characteristics. Table 1 lists detailed flood mitigation plans for each alternative. The suitability of the alternatives was evaluated using the DCF approach. Alternatives 1 and 2 focus mainly on extension of the heights of existing dams (Jangsung, Naju, Damyang, and Gwangju) that were built for agricultural water supply. Alternative 3 updates dam operations to minimize environmental damage among the alternatives. Alternative 4 considers constructing six new washlands that could be deliberately flooded to prevent inundation of residential areas. It was assumed that all the measures in each alternative are implemented, delayed, or abandoned simultaneously.

Yeongsan River Basin

3.2 Application of the DCF approach

To carry out a traditional economic analysis using the DCF approach, the value of the benefit was calculated as changes in estimated damage cost between with and without the construction of each alternative plan. The overall process of the DCF approach is described below.

-

1.

The frequency analysis of the annual maximum of 24-h rainfall is driven by the Gumbel distribution using the probability weighted moments method over six rainfall stations.

-

2.

Hourly time series of the 24-h rainfall are generated based on second-quartile Huff distribution (Huff 1967) for 50, 100, and 200 years of return period.

-

3.

Runoff series are then simulated using HEC-HMS software, and water levels and inundated areas are calculated using HEC-1 software.

-

4.

Changes in the damage cost are calculated through five steps of the multi-dimensional flood damage analysis, which is widely used in economic feasibility studies for water resources in Korea. For details, refer to Kim et al. (2004).

Flood magnitudes at the outlet of the Yeongsan River Basin, as simulated by HEC-HMS, are presented in Table 2. Table 3 summarizes the results of the DCF approach indicating the values of the annual average cost and benefit of each alternative under a 200-year return period. The four alternatives have similar benefits even though they are different in their mitigation plans. Because they were proposed for the same purpose (i.e., to mitigate flood risk), their benefits can be estimated similarly. However, because their costs are different, the NPV of each alternative varies. According to the NPV value of each alternative, the best alternative was alternative 1, while alternatives 1 and 2 were economically feasible for the Yeongsan River Basin. However, alternatives 3 and 4 were not economically feasible because the annual costs were greater than the annual benefit.

3.3 Application of the ROA

Unlike with DCF, to consider uncertainty in climate change ROA utilized four global circulation model (GCM) data sets from IPCC AR4: Commonwealth Scientific and Industrial Research Organization (CSIRO), Centre National de Recherches Météorologiques (CNRM), Meteorological Institute of the University of Bonn (Institute of KMA and the Model and Data Group: CONS), and Hadley Centre for Climate Prediction and Research (Met Office United Kingdom: UKMO) (Table 4). Although up-to-date climate change information—IPCC AR5 GCM models with Representative Concentration Pathways (RCP) scenarios—have been used recently, we preferred to use the former data sets because they reflect a sufficient range of uncertainty in the future of climate change in Korea (Lee and Kim 2012). Representative scenarios were selected based on the ability to explain the range of uncertainty of all the climate change scenarios. The four GCM data sets were spatially downscaled using the cyclo-stationary empirical orthogonal function (CSEOF) and multi-linear regression analysis (Bae et al. 2007).

This study employed the backward-moving procedure described in Section 2.2 because it was relatively easier to estimate V max and V min than u and d as given parameter values for our specific case study. V max and V min were calculated based on GCM projections from 2016 to 2045 using the following procedure.

-

1.

Conduct the flood frequency analysis of annual maximum precipitation of each GCM.

-

2.

Transfer the T-year flood frequency calculated to the corresponding flood damage using a flood damage curve.

-

3.

Repeat (1) and (2) for all the GCMs tested. Choose the maximum and the minimum damage values over the GCMs tested for each T-year flood.

-

4.

Assign the maximum and the minimum values of the average annual damage as V max and V min, respectively, assuming the flood mitigation alternative can avoid this damage.

Thus, the range between the maximum and the minimum value of the flood frequency calculated among the GCM projections becomes the total range of rainfall uncertainty in the future. By considering only the maximum and minimum values, the values of u and d were easily calculated.

A decision tree was created based on the annual average benefit for a period of 30 years from 2016 to 2045 for each alternative. Two real options: abandon and delay, were considered in the ROA application. The basic assumption behind this approach is that the flood damage cost increases linearly as the flood frequency increases during a given rainfall intensity (i.e., if the same magnitude of flood occurs again, the damage cost is doubled). Because the updated frequency represents climate change during a period of 30 years and because floods are very low-frequency events, back-to-back floods were considered very rare events that are not likely to occur. Flood frequency was updated based on rainfall intensity driven by each GCM scenario.

3.3.1 Projection of exceedance probability of extreme rainfall

The exceedance probabilities of the extreme rainfalls (annual maximum of 24-h rainfall event under a 50-year, 100-year, and 200-year return period) were estimated using the GCM-driven rainfall series. We considered changes in the frequency of extreme rainfall rather than the amount of rainfall. Thus, the frequency was updated by the GCM-driven rainfall series given the same amount of extreme rainfall estimated by historic rainfall data. Table 5 lists the 12 estimated exceedance probabilities driven by the four GCMs, along with three emission scenarios (A1B, B1, and A2).

3.3.2 Reflection of uncertainty

The annual average benefit increases as much as the exceedance probability of extreme rainfall increases under the assumption that the alternative becomes more critical with higher exceedance probability of floods. For the range of uncertainty in 2045, the maximum and the minimum values of the exceedance probabilities driven by the GCM scenarios were selected in order to calculate the range of the future annual average benefits for 2045. Table 6 lists the present annual average benefit and the maximum and minimum values of the future annual average benefits for each alternative estimated by the climate scenarios. It was observed that the A2 emission scenario had the largest uncertainties across all the GCM models. The maximum and the minimum values of the annual average benefit were then used to calculate the binomial tree parameters that are time-discrete representations of the change in rainfall intensity over a time step.

3.3.3 Option value estimation

At each step, it was assumed that the value of the annual average benefit is calculated by the stochastic process (i.e., by moving up or down with two binomial tree parameters, u and d, respectively). The values of u and d were calculated using Eq. (4) and (5), respectively, where V max is the annual average benefit driven by A2, CONS for 2045, V min is the annual average benefit driven by A2, CSIRO for 2045, and V(0) is the present annual average benefit driven by historical data for 2016, and T = 30 (years). The option value at each node was then calculated backward from the expiration to the present.

The binomial tree of the annual average benefit was then formed from the present to the expiration year. The present value of the annual average benefit of each year was calculated with a 6% discount rate; then the present value of the annual cost was subtracted to obtain the NPV shown in Eq. (7). Next, the option matrix for each alternative, including the delay and abandon options, was created. These options provide an opportunity to adjust the flood mitigation plan by considering uncertainty in the conditions changed by the GCM scenarios. Delay option values were sequentially calculated backward from a zero value in 2045, and the value of each year was then estimated based on the risk-neutral approach, as given in Eq. (8). The abandon option value was assumed to be zero because benefit and cost are not estimable if the alternative plan never starts. The ENPV at each node was then estimated as the maximum value of the applied options and the NPV is given in Eq. (9).

where PV(i, j) is the present value at each node, C is the present value of the annual average cost, p is risk-neutral probability, r is risk-neutral discount rate, δt is discrete-time interval, D(i ,j) is delay option value at each node, and A(i, j) is the abandon option value, which is zero for all the nodes.

Last, the option premium of each alternative was calculated to determine the best alternative based on the ROA approach, and considering uncertainty.

4 Results

4.1 ENPV

The ENPV of each alternative was estimated by ROA with the binomial tree approach. The value of ENPV represents the quantitative value of each alternative, taking climate change uncertainties into account. Table 7 presents a comparison of the quantitative analysis; it shows the NPV and ENPV of each alternative estimated by the DCF and ROA approach, respectively. The quantitative values of alternatives 2, 3, and 4 were increased when ROA was used, and all four alternatives had positive values of ENPV while alternatives 3 and 4 had negative values of NPV. This is because the two real options, delay and abandon, provide flexibility across every stage during the planning period. Because the option premium reflects the potential value that comes from the options, all the alternatives were economically feasible, given that two options were considered throughout the planning period (i.e., the values of alternatives 2, 3, and 4 increased). Nonetheless, the order of priority among all the alternatives was not changed. The best plan was alternative 1, and there was no option premium with alternative 1. Thus, immediate implementation of alternative 1 would be the most beneficial choice.

4.2 Timing of the options

Along with the values of ENPV for the alternatives, ROA also provides the ideal timing of each option. Thus, the best option for each node can be selected based on the annual average benefit of each option estimated by the discrete-time model (as described in Eq. (7)–(9) in Section 3.3.3). Figure 3 demonstrates the evaluation of the options on each node for alternative 1. At the beginning node (1, 1), in 2016, ROA suggests invest (I) is the best option. This implies that the plan needs to be implemented immediately. If the plan cannot be implemented in 2016 for some reason, the best option is reevaluated based on the updated flood frequency. If flood frequency is expected to increase, u is directed to node (2,1), otherwise d is directed to node (2,2). At node (2,2), ROA suggests delay (D) is the best option if flood frequency is expected to decrease. Subsequently, the evaluation was extended to 2045, which is the last year of the planning period. Based on the execution framework generated by ROA, decision-makers could choose one option while taking their perception of changes in flood frequency into account. Note that once the plan is implemented or abandoned, the value of the alternative is no longer evaluated.

Evaluation of the options on each node for alternative 1 (unit is expressed in million dollars)

Figure 4a, d present the framework of ROA execution for alternatives 1 to 4, respectively. The initial of the option on each node represents the best option selected by ROA. Immediate implementation of the project was suggested only for alternative 1, and the delay option for the others. Because alternative 1 is the most attractive plan regardless of the option premium (as shown in Table 5), decision-makers do not need to consider other options for now (2016). Nonetheless, if the plan is not implemented in 2016, decision-makers need to consider the delay option, while taking uncertainties in climate change into consideration. In addition, the abandon option may be considered after 2029.

Symbolic execution of ROA: a Alternative 1. b Alternative 2. c Alternative 3. d Alternative 4

For alternative 2, the delay option was suggested until 2018. Then, implementation could be considered with the expectation of an increase in flood frequency. On the contrary, if a decrease in flood frequency is expected until 2028, decision-makers could also consider the abandon option. The timing for the abandon option was evaluated as being 1 year earlier than for Alternative 1.

For alternatives 3 and 4, the timing of the implementation was much more delayed than alternative 2. Because their NPV values were negative, early implementation of the plan was not suggested. The delay option was suggested until 2024 and 2023 for alternatives 3 and 4, respectively. Furthermore, the timing of the abandon option was moved up to 2025 and 2024, respectively. The timing of implementation was postponed for alternatives 3 and 4 because the present value of the annual average cost is far greater than the benefit. However, the overall values of alternatives 3 and 4 were evaluated as economically feasible by ROA, after taking delay and abandon options into consideration, as well as uncertainties in climate change.

5 Conclusions

ROA was successfully implemented for water resources planning study, taking into account uncertainty in global climate change in the decision-making process. The conventional method, such as DCF, has two main drawbacks in terms of climate change uncertainty. One is the assumption that future cash flow is predictable and fixable, and the other is that additional decisions are not available throughout the entire planning period. In this study, the binomial tree model was used to overcome these limitations by estimating potential uncertainties in the future using climate change scenarios, and by making additional decisions available during the entire planning period.

The priority ranking of the four alternatives between the traditional DCF and ROA remained the same; however, two alternatives that were assessed as economically infeasible using DCF turned out to be economically feasible using ROA. Although immediate implementation of the project was suggested only for alternative 1, flexible execution of the other two options—delay and abandon—resulted in the option premium. In particular, alternative 4 had the highest value of option premium because it also had the highest cost on the project. Therefore, ROA can provide decision-makers with flexible options for the project based on given uncertainties in the future, which are not considered by conventional methods. Evaluation of the project from various perspectives, such as environmental, socioeconomical, and scientific, would be available for each discrete-time step. It is important to note that these perspectives can vary a lot depending on differences in various factors such as climate regime, government preference, and level of development, around the world.

The applicability of the proposed method can be extended globally especially within a monsoon climate regime if adaptation strategies and climate change projection data sets for a watershed to be tested are prepared. Reliable economic analysis of the adaptation strategies is also required for the globally extended studies. At the global level, on the other hand, adaptation strategies should focus on how to allocate funds for the socio-infrastructure and flood mitigation plans in various regions of the world, as financial resources in many developing countries are insufficient for creating the infrastructure needed (Wang et al. 2014). Thus, as van der Pol et al. (2017) discussed, the global strategy for flood mitigation can be optimized if the global flood adaptation funds are properly allocated based on reliable economic analysis on flood mitigation plans of individual countries. Given that uncertainty under global climate change should be considered while making global strategies for flood mitigation, the ROA proposed in this study can be a powerful decision-making tool at both local and global levels.

The option matrix generated in this study could be informative for decision-makers to conceptualize their adaptive planning procedure. An alternative that was infeasible with DCF could become economically feasible if adequate options were implemented by considering given climate change pathways. This is because ROA is capable of adjusting investment timing as well as planning strategy using the options. In spite of these powerful advantages, ROA is resource-intensive and requires well-identified probabilities and economic data, which is often not feasible in practice (Kim and Chung 2017). In particular, it is very difficult to get reliable tools and data sets in developing countries. Therefore, global cooperation for incorporating worldwide data sets for climate change is required.

Recommendations on the global adaptation strategy for the flood mitigation are addressed in the following section:

-

Proper allocation of global funds and socio-infrastructures need to be established (especially for helping developing countries).

-

Economic analysis on flood mitigation plans in individual countries need to consider uncertainty in global climate change.

-

The global database on climate change should be updated frequently and should be made assessible worldwide.

-

Researchers should make efforts on both the reduction of climate change uncertainty and establishment of flexible adaptation strategy.

Although we considered a fixed value of p, the probability term in this approach, to address changing climate for the planning horizon, “changing probability over time” could be tested in a future study. Moreover, because the range of uncertainty depends on the climate change information to be used, the probabilities of increase and decrease of flood frequency can vary with the locations of application. If the flood frequency is not changed (remains the same), it may lead to less variability in option values. However, this does not mean that the advantage of ROA cancels out. ROA will return the optimal timing for each option based on ENPV at each node. Thus, it could also be analyzed to show how the range of uncertainty affects the option values, in a future study.

References

Bae DH, Jung IW, Lee BJ (2007) Outlook on variation of water resources in Korea under SRES A2 scenario. J Korean water Resour Assoc 40:921–930 (written in Korean)

Baldwin CY, Ruback R (1986) Inflation, uncertainty, and investment. J Finance 41:657–669

Borison A, Hamm G, Farrier S, Swier G (2008) Real options and urban water resource planning in Australia. WSAA Occas. Pap. 20, Water Serv Assoc of Aust, Melbourne, Australia

Brugnach M et al (2008) Toward a relational concept of uncertainty: about knowing too little, knowing too differently, and accepting not to know. Ecol Soc 13(2):30

Buurman J, Babovic V (2016) Adaptation pathways and real options analysis: an approach to deep uncertainty in climate change adaptation policies. Policy Soc 35(2):137–150

Cox JC, Ross SA, Rubinstein M (1979) Option pricing: a simplified approach. J Financ Econ 7(3):229–263

Deng Y et al (2013) Valuing flexibilities in the design of urban water management systems. Water Res 47(20):7162–7174

Dixit AK, Pindyck RS (1994) Investment under uncertainty. Princeton University Press, Princeton

Huff FA (1967) Time distribution of rainfall in heavy storms. Water Resour Res 3(4):1007–1019

Hussey J, Hussey R (1999) Discounted cash flow. In: Business accounting. Macmillan Education, UK, pp 265–273

Jeuland M, Whittington D (2013) Water resources planning under climate change: a “real options” application to investment planning in the Blue Nile environment-for-development. Discussion paper series no. dp-13-05-efd

IPCC (2001) Climate change 2001: The Scientific Basis, Third Assessment Report of the Intergovernmental Panel on Climate Change. Houghton JT et al (eds) Cambridge University Press, Cambridge, UK

Kester WC (1984) Today’s options for tomorrow’s growth. Harv Bus Rev 62:153–160

Kim YO, Chung ES (2017) Adaptation to climate change: decision-making. In: Kolokytha E et al (eds) Sustainable water resources planning and management under climate change. Springer, Singapore, pp 189–221

Kim TS et al. (2004) A study on improvement in economic analysis of flood management plan. Ministry Construction & Transportation (written in Korean)

Kjaerland F (2007) A real option analysis of investments in hydropower: the case of Norway. Energy Policy 35(11):5901–5908

Kodukula P, Papudesu C (2006) Project valuation using real options: a practitioner’s guide. J Ross Publishing, Florida

Kwadijk JC et al (2010) Using adaptation tipping points to prepare for climate change and sea level rise: a case study in the Netherlands. Wiley Interdiscip Rev Clim Chang 1:729–740

Lau KT, Fan H, Onof C (2006) The potential use of the Black-Scholes model in urban drainage risk management. Dissertation, Imperial College of Science, Technology and Medicine, London, UK

Lee JK, Kim YO (2012) Selecting climate change scenarios reflecting uncertainties. Atmosphere 22(2):149–161 (written in Korean with English abstract)

Lempert RJ et al (2000) The impacts of climate variability on near-term policy choices and the value of information. Clim Chang 45(1):129–161

Majd S, Pindyck RS (1987) Time to build, option value, and investment decisions. J Financ Econ 18:7–27

Mason SP, Merton RC (1985) The role of contingent claims analysis in corporate finance. In: Altman E, Subrahmanyam M (eds) Recent advance in corporate finance. Irwin, Homewood, pp 7–54

McDonald RL, Siegel DR (1986) The value of waiting to invest. Quarterly J Econ 101:707–727

Means E et al (2010) Decision support planning methods: incorporating climate change uncertainties into water planning. Water Utility Climate Alliance, San Francisco

Michailidis A, Mattas K (2007) Using real options theory to irrigation dam investment analysis: an application of binomial option pricing model. Water Resour Manag 21(10):1717–1733

MLIT (2005) The comprehensive flood mitigation plan: Yeongsan River Basin, Ministry of Land, Infrastructure and Transport (written in Korean)

Myers SC (1977) Determinants of corporate borrowing. J Financ Econ 5(2):147–175

Myers SC, Majd S (1990) Abandonment value and project life. Adv Futures Options Res 4:1–21

Paddock JL, Siegel DR, Smitha JL (1988) Option valuation of claims on real assets: the case of offshore petroleum leases. Quarterly J Econ 103:479–508

Samis M et al (2011) Using dynamic DCF and real option methods for economic analysis. Technical Reports NI43–101. Retrieved from http://inside.mines.edu/~gdavis/Papers/ValMin.pdf

Seo ST (2006) A real options approach to the investment analysis of irrigation systems. The Korean J Agric Econ 47(1):31–50 (written in Korean with English abstract)

Steinschneider S, Brown C (2012) Dynamic reservoir management with real-option risk hedging as a robust adaptation to nonstationary climate. Water Resour Res. doi:10.1029/2011WR011540

Stocker T et al (2013) Technical summary. In: Stocker T et al (eds) Climate change 2013: the physical science basis. Contribution of Working Group I to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge

Stulz R (1982) Options on the minimum or maximum of two risky assets: analysis and applications. J Financ Econ 10:161–185

Tourinho O (1979) The option value of reserves of natural resources. Working paper no. 94. University of California, Berkeley

Trigeorgis L (1996) Real options: managerial flexibility and strategy in resource allocation. The MIT Press, Cambridge

Trigeorgis L, Mason SP (1987) Valuing managerial flexibility. Midland Corporate Finance J 5(1):14–21

UKCIP (2003) Climate adaptation: risk, uncertainty and decision-making. United Kingdom Climate Impacts Programme, Oxford

van der Pol TD et al (2017) Economic analysis of adaptive strategies for flood risk management under climate change. Mitig Adapt Strateg Glob Change 22(2):267–285

Wang XJ et al (2014) Adaptation to climate change impacts on water demand. Mitig Adapt Strateg Glob Chang 22(4):595–608

Acknowledgements

This research was supported by a grant (14AWMP-B082564-01) from the Advanced Water Management Research Program funded by the Ministry of Land, Infrastructure, and Transport of Korea, a grant (11 Technology Innovation C05) from the Construction Technology Innovation Program funded by Ministry of Land, Infrastructure and Transport, and a grant (2014001310007) from the Climate Change Correspondence Program funded by the Korea Ministry of Environment. The authors are grateful to the editors and the anonymous reviewers for their insightful comments and helpful suggestions.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Ryu, Y., Kim, YO., Seo, S.B. et al. Application of real option analysis for planning under climate change uncertainty: a case study for evaluation of flood mitigation plans in Korea. Mitig Adapt Strateg Glob Change 23, 803–819 (2018). https://doi.org/10.1007/s11027-017-9760-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11027-017-9760-1