Abstract

Using annual data from Italian banks, we study the link between non-interest revenues and profitability. We find that income diversification increases risk-adjusted returns. Our results provide econometric evidence consistent with current studies on EU banks, but do not support findings on the U.S. experience. In our view, the differences depend primarily on the relative importance of local banks: we find that the relation is stronger at large banks. In addition, we find that there are limits to diversification gains as banks get larger. Small banks can make gains from increasing non-interest income, but only when they have very little non-interest income share to start with. The source of non-interest income is less important than its level.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In this paper we examine diversification in banking. In the past two decades, both academic and applied research paid attention to this issue. To assess to what extent it may enhance bank profitability and/or reduce bank risks, a substantial number of scientific works deal with loan portfolio diversification (industrial, sectoral, geographic, etc.), but a growing body of literature investigates the relation between the diversification of revenue sources and the bank’s risk–return trade-off. Our paper contributes to this latter stream of research through an empirical analysis concerning the experience of the Italian banking system over the 1993–2003 period.

Since the early 1990s, in Italy the banking industry has moved from interest toward non-interest income. Although it is undisputed that this shift represents a relevant step toward higher profits, there are some doubts regarding the effects of such a process on overall bank performance. Thus, the basic question that we address in this paper is the following: has this shift positively affected risk-adjusted bank profitability, or, in contrast, is the strong increase in non-interest income associated with a troublesome growth of profit instability?

The results of our empirical analysis suggest a positive answer to that question: that for Italian banks, the shift toward activities that generate non-interest income has proved to be beneficial. This result contrasts with U.S. studies, which tend to find that no general improvement in financial performance is associated with increases in non-interest income. In addition, our findings suggest that diversification gains associated with non-interest income diminish with bank size; that small banks with very little non-interest income share make financial performance gains from increasing non-interest income; and that measured performance gains appear to be associated with non-interest income in general, rather than with the specific business lines that generate that income. Thus, our findings are of interest when comparing the relative risk and performance of European and U.S. banks, and, in this respect, they help fill a gap in the literature on bank performance and diversification.

The remainder of the paper is organized as follows. In Section 2 we look briefly at the aforementioned literature. In Section 3 we document the main trends in the income structure at Italian banks. In Section 4 we describe the variables, data, and the empirical model that we use. Section 5 presents and discusses the results of the estimations. Section 6 concludes.

Review of the Literature on Bank Performance and Diversification

From a theoretical standpoint, the decision to diversify income sources is desirable for both efficiency and risk management. The joint production of a wide range of financial services should increase a bank’s efficiency, thanks to economies of scope (Klein and Saidenberg 1997). Thus, generally speaking, diversification across new types of services should enhance profitability.

When researchers consider risk, it is generally believed that diversification of income sources—that is, the shift from interest to non-interest income—should reduce total risk. Here, the idea is simple: since activities that generate non-interest income are thought of as uncorrelated, or, at least, imperfectly correlated, with those that produce interest income, diversification should stabilize operating income and give rise to a more stable stream of profits.

Studies on banking have also offered arguments against this conventional wisdom. DeYoung and Roland (2001) suggest three main reasons why non-interest income may increase the volatility of bank earnings:

-

1.

A bank is more likely to lose clients with whom it engages in a fee-based relationship rather than a loan-based relationship. In spite of the greater sensitivity to movements in interest rates and economic downturns, “revenue from a bank’s traditional lending activities is likely to be relatively stable over time, because switching costs and information costs make it costly for either borrowers or lenders to walk away from a lending relationship” (DeYoung and Roland 2001, p. 56).

-

2.

Moving from interest to non-interest income can require heavy fixed investments in technology and human resources. As a consequence, an increase in operating leverage and earnings volatility.

-

3.

Many fee-based activities can be performed holding little or no regulatory capital and this suggests a higher degree of financial leverage and, as a consequence, earnings volatility.

Empirical research has examined the issue of diversification benefits from several standpoints and through different methodological approaches. In spite of what economic theory postulates, namely, a positive relation between diversification and profitability, it has produced evidence that is by no means clear cut. An exhaustive survey of the literature on bank product mix and bank risk goes beyond the purpose of this paper (for such a survey see, for instance, DeYoung and Roland 2001). Here, we are interested only reviewing the most recent papers and comparing the findings for the U.S. and the EU. In fact, most of the studies that we review deal with U.S. banks (DeYoung and Roland 2001; Stiroh 2004a, b; DeYoung and Rice 2004a; Stiroh and Rumble 2006), but to the best of our knowledge, only a few papers focus on the experience of European banks (European Central Bank 2000; Smith et al. 2003) and none of them uses econometric methods.

DeYoung and Roland (2001), in a paper that uses data from 472 U.S. commercial banks over the period 1988–1995, find that as the average bank tilts its product mix toward fee-based activities and away from traditional lending activities, the bank’s revenue volatility, its degree of operating and financial leverage, and the level of its earnings all increase. These three results imply both increased earnings volatility and a possible risk premium.

Stiroh (2004b), considering U.S. banking data between 1984 and 2001, finds that in the aggregate, industry-wide level, the correlation between net interest income growth and non-interest income growth increased in the 1990s; moreover, that non-interest income is much more volatile than net interest income, Further, that the lowering of operating revenue volatility, which occurred in the 1990s, can be traced directly to the declining volatility of net interest income. Finally, Stiroh finds that at the bank level, risk-adjusted returns are negatively associated with non-interest income shares.

Stiroh (2004a) looks at American community banks, i.e., small banks that do not belong to any banking group, and examines the link between income diversification and risk–return performance for the 1984–2000 time period. He performs a regression analysis and shows that, broadly speaking, the increase in fee-based revenues caused a worsening in the risk–return trade-off. However, he points out that there are significant differences between small- and medium-sized community banks, and that the smaller banks are able to reach higher levels of competitiveness when they shift from interest based activities toward fee-based ones.

DeYoung and Rice (2004a), using data for U.S. commercial banks between 1989 and 2001, find that marginal increases in non-interest income were associated with higher profits, more variable profits, and on net, a worsening of risk–return trade off.

Stiroh and Rumble (2006), in a study on U.S. financial holding companies for the 1997–2002 period, find that there is no link between diversification and performance, but that there is a large negative relation between non-interest share and performance.

The European Central Bank (2000) examines the experience of EU countries, which, in a survey conducted across the EU countries for the period 1989–1998, stresses, among several other points, that the composition of non-interest income is highly heterogeneous; that in recent years, this component of operating income has been the most dynamic one; that non-interest income has played a major role in the growth of banks’ profitability; that in many EU countries, there is apparently an inverse cross-sectional correlation between interest and non-interest income; and that for the period examined, net interest income has registered greater volatility in Europe than in the U.S., while non-interest income has shown a lower volatility (measured by the coefficient of variation) in Europe than in the U.S.

Smith et al. (2003) analyze the variability of interest and non-interest income and their correlation, for the banking systems of the 15 EU countries during the 1994–1998 period. For each country, Smith et al. (2003) consider commercial, savings, cooperative, and mortgage banks on the one hand and large and small banks on the other, and study the correlation of income sources. They find that in the majority of the cases, the increased reliance on activities that generate non-interest income has stabilized profits.

Main Trends in Changes in the Income Structure at Italian Banks

Since early 1990s, the Italian banking industry has undergone profound changes, spurred not only by the external environment—financial markets integration, the European Economic and Monetary Union, technological advances and so forth—but also by country-specific regulatory and legislative innovations. These changes have fostered a reshaping of bank ownership structure, higher concentration, and increased competition. Of the state-owned banks, which in early 1990s comprised approximately 70% of the banking industry, almost all have been privatized. Further, thanks to the significant number of mergers and acquisitions (M&As) that took place between 1993 and 2003, 530 operations involving majority interests and approximately 60% of the total Italian banking assets, the number of banks has drastically fallen, decreasing from more than a thousand in 1993 to less than 800 in 2003. Also, the average size of banks has increased: the ten largest banks have doubled their share in total bank assets.

Changes in the regulatory framework have also had an important impact on the functioning of the market. After the liberalization that allowed banks to open new branches, expansion that was strongly regulated until 1990, by 2003 the overall number of branches doubled to more than 30,000. Thanks to the growth of investment in information and communication technology (ICT), technological advance was also relevant. The number of ATMs grew from 25,500 in 1993 to approximately 37,000 in 2003, and the number of point of sale terminals (POS) increased from 275,000 to approximately 900,000.

Important changes also occurred in the banks’ business lines through the enhancement of some traditional retail banking segments such as consumer credit and mortgage loans. At the same time, banks developed new services in the area of payment services, insurance and social security, and asset management (Italian Banking Association 2003).

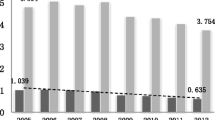

All these changes had a substantial impact on the structure of bank income and composition of bank revenues. Figure 1 depicts this evolution. The non-interest component of operating income increased from approximately 23% in the early 1990s to around 45% in the early 2000s.

Net interest income and net non-interest income as percentage of net operating revenue (1993–2003)

Table 1 displays the year-by-year dynamics of the main items in the industry income statement for the period 1993–2003. As a percentage of total assets, net interest income fell from 3% in 1993 to 1.8% in 2003, but non-interest income grew from around 1% to 1.4%, and operating costs went down from 2.5% to 1.95%. Further, in a context of declining provisions owing to the improvement in the credit quality, return on equity (ROE) jumped from 2.8% in 1993–1994 on average, to 7% at the end of the decade (and 11% in 2000).

Variables, Data, and the Empirical Model

For the empirical analysis we use data from balance sheets of individual Italian banks. In this section, as first point, we define the key variables in the analysis, then we describe our database and the empirical model that we apply.

Measures of Diversification and Performance

We base our empirical analysis on a set of variables that includes an index of diversification, measures of risk-adjusted return, and several control variables.

First of all, we consider the following variables: NET (net interest income), which we measure as interest receivable minus interest payable; NII (net non-interest income), measured as commissions receivable minus commissions payable plus net profits (losses) on trading activities plus other net non-interest income. We note that here, and in the remainder of the paper, we refer to interest and non-interest income as entirely separate components of the bank operating income, although we are aware of the fact that the line between them is becoming increasingly blurred.

We take their respective shares in net operating income (NET + NII):

and use them to compute a Herfindahl–Hirschman Index of income specialization (NETs2 + NIIs2). In contrast, following Stiroh and Rumble (2006), we define our measure of income diversification as:

By construction, under the constraint that NET and NII have to assume positive values, such an index varies from 0.0 to 0.5. It is equal to zero when diversification reaches its minimum, i.e., when net operating income stems entirely either from net interest income or from non-interest income, and equal to 0.5 when there is complete diversification.

Next, as profitability measures we consider Return On Equity (ROE) and Return On Assets (ROA). To adjust these measures for risk (volatility), we compute their standard deviation over the entire sample period. We define our indicators of bank performance as the ratio between the annual return and its standard deviation. Following Stiroh (2004b), we call these indexes Sharpe ratios (or risk-adjusted returns, SHROE and SHROA). In formulas, we have:

where SHROE i,t and SHROA i,t indicate risk-adjusted returns, respectively, in terms of ROE and ROA, for the bank i in the year t.

Data

We use annual data taken from the balance sheets of individual Italian banks submitted to the Bank of Italy and collected by the Italian Banking Association over the period 1993–2003.Footnote 1 We construct our sample on the basis of two criteria: the sample banks must have reported all the data necessary to construct the dependent and independent variables for 1993 to 2003; and NET and NII must always be non-negative.

The first criterion meets the need of avoiding the econometric problems that arise from incomplete panels with non randomly missing data (Baltagi 2005). In fact, the remarkable number of M&A deals in Italy during the 1990s that we noted in Section 3 has produced several de novo bank entries and bank exits.

The second criterion ensures that our diversification measure (DIV) is bounded between zero and 0.5.

As a result of this selection procedure, we obtain a balanced panel consisting of 85 banks. We provide a complete list of these banks in the Appendix. In terms of size, five banks are “very large”, six are “large”, 19 are “medium,” and the remaining 55 as “small and very small” (of which 46 belong to a multibank holding company in 2003). For the geographical scope of their activities, we classify six banks as “national”, ten as “intra-regional”, 17 as “regional”, 49 are “provincial/intra-provincial”, and the remaining three as “not defined”. These banks represent almost 60% of the Italian banking system, as measured by total assets.

Due to the shortage of observations, we choose not to truncate the data. Given our choice of criteria, if we truncated the performance measures at the 1st and 99th percentiles, we would drop more than ten banks from the total of 85, which, in terms of the total bank assets, would mean a drop in the representativeness of our sample to below 50%. By not truncating our data, we follow the same approach followed by Acharya et al. (2002) in dealing with Italian banks’ data. However, we apply the procedure suggested by Tukey (1977) to check for the presence of outliers in our performance measures. The application of such a procedure does not detect the presence of far outliers.Footnote 2

The Empirical Model

We use the following empirical specification:

where Y is a measure of risk-adjusted returns, k is a constant, α is a time fixed effect, and λ is a bank fixed effect.

As in Stiroh and Rumble (2006) and in Stiroh (2004a), we note that the estimates of \(\hat \beta _1 \) and \(\hat \beta _2 \) are of particular importance. \(\hat \beta _1 \) represents the impact of income diversification between interest and non-interest income; positive values of \(\hat \beta _1 \) indicate that income diversification improved risk-adjusted returns. \(\hat \beta _2 \) denotes the effect on risk-adjusted returns due to variations in the share of non-interest income on net operating income holding the effects of diversification (DIV) constant; positive values of \(\hat \beta _2 \) show that increases in non-interest income share are associated with higher risk-adjusted returns. Stiroh and Rumble (2006) point out that due to the dependence of DIV on NIIs, \(\hat \beta _1 \) and \(\hat \beta _2 \) may be interpreted in another manner as well. Calculating the first derivative of risk-adjusted returns with respect to NIIs we obtain:

A positive (negative) value of Eq. 7 means that an increase in the share of non-interest income produces an increase (decrease) in the risk-adjusted return.

It is clear that \(\hat \beta _1 \) and \(\hat \beta _2 \) may be interpreted, respectively, as the indirect and the direct effect on risk-adjusted returns associated with a variation in NIIs; the sum of both these effects is the net effect. As noted by Stiroh and Rumble (2006), the indirect effect depends both on the sign of \(\hat \beta _1 \) and on the level of NIIs; the effect of the increase in NIIs on DIV will depend on the initial level of NIIs itself. In particular, if the initial value of NIIs is lower than 50%, any further increase generates a rise in DIV; but if its initial value is equal or greater than 50%, any further increase will imply a lowering of DIV.

However, the dependence of DIV on NIIs can generate econometric problems. In fact, in our sample period, the predominant presence in the sample of banks with an initial level of NIIs below 50% causes collinearity between DIV and NIIs. If this collinearity is high, then \(\hat \beta _1 \) and \(\hat \beta _2 \) are still unbiased, but we have overestimated their variance and covariance. We apply Wald’s procedure to test for the joint statistical significance of \(\hat \beta _1 \) and \(\hat \beta _2 \) and, furthermore, in Eq. 6 we use DIV and NIIs separately.

In Eq. 6 we use the following control variables:

-

ASSETS, which is the natural log of bank assets deflated with the GDP deflator. We use this control variable only in the equation for SHROE, since SHROA is inversely correlated with the level of bank assets. As in other empirical studies on this subject (Stiroh 2004a, b; Stiroh and Rumble 2006, DeYoung and Rice 2004a), we use this control variable because it captures the effects of bank size. In particular, large-sized banks are able to invest a lot of money in ICT, so they can build up know-how and technologies for high-quality risk-management. Furthermore, a larger size allows the bank to operate more business lines and with a wider range of customers. On the other hand, small-sized banks could benefit both from a greater operating flexibility, i.e., being capable of adapting their strategies very quickly to the changing economic environment, and from lower fixed operating costs. In Eq. 6 ASSETS also takes the quadratic form, to capture a possible non linear link between risk-adjusted returns and size. The hypothesis we want to test is that as bank size grows, scale and scope economies tend to more than offset the higher costs that result from the more rigid organizational structure and growing operating complexity. However, beyond a certain threshold, scale diseconomies could appear, with a consequent worsening of the risk-adjusted returns. In sum, with such a specification we want to test if there is an inverted U-shaped relation between size and risk-adjusted returns.

-

GROWTH, which is the growth rate of real bank assets, i.e., bank assets deflated with the GDP deflator. This variable is our proxy for the bank managers’ preference for risk taking. In fact, risk-loving bank managers usually prefer fast growth to more stable profits (Stiroh 2004a). GROWTH could be also interpreted as a control variable for growth-by-acquisition.

-

EQUITY, which is the ratio between equity and bank assets and represents the degree of financial leverage. We use this variable only in the equation for SHROA, since SHROE is inversely correlated with the capital endowment. This variable is our proxy for the bank managers’ risk aversion. In fact, a high degree of capitalization signals a high risk aversion, and vice versa (Stiroh 2004a).

-

LOAN, which is the ratio between total loans and bank assets. As in DeYoung and Rice (2004a) and Stiroh (2004a), we include this variable to control for the effects on risk-adjusted returns of the composition of banks’ asset portfolio. In so doing we check if the lending strategy affects risk-adjusted returns and in which direction. The sign of the relation between lending strategy and risk-adjusted return is positive if loans are more profitable than other earning assets.

-

BAD, which is a standard index of loan risk equal to the share of non-performing loans in total loans (DeYoung and Rice 2004a). We expect that worse loan quality is going to lower the risk-adjusted returns.

-

HOLDING, which is a dummy variable equal to one if the bank belongs to a multibank holding company, zero otherwise. As in DeYoung and Rice (2004a) and Stiroh (2004b), this variable checks for the influence of the bank organizational model on its risk-adjusted returns. We expect to find a negative relation between holding company organizational model and risk-adjusted returns. In fact, according to 2003 data, 85% of bank branches belong to a holding group. Clearly, this kind of organizational model is widespread among Italian banks because, in our view, bank owners achieve benefits from diversification. This result implies that one single bank that belongs to a holding company does not necessarily adopt a diversification strategy in all the aspects of its business, because the optimal combination of activities that maximize the risk-adjusted returns is achieved at a group level.

-

REGION, which is a dummy variable equal to one if the bank operates its branches in only one of the 20 regions that exist in Italy, and equal to zero otherwise. The relation between geographic markets diversification/focus and risk-adjusted returns can be either positive or negative. In fact, the gains from geographic diversification in terms of returns could be overcompensated by the costs of monitoring.

In Table 2 we report summary statistics and definitions of all the variables described above and used in the regressions.

Regression Results

Table 3 displays the regression results for Eq. 6. Among the explanatory variables and for SHROE and SHROA, respectively, Models (I) and (IV) include both DIV and NNIs. In both cases DIV has a coefficient with a positive but nonsignificant sign, and the coefficient on NIIs is positive and significant. Stiroh (2004a) gets exactly the same result in terms of the significance of the coefficients: jointly taken, the coefficients on the diversification index and on the non-interest income share are never statistically significant.

However, a Wald test shows that \(\hat \beta _1 \) and \(\hat \beta _2 \) are jointly statistically significant, indicating the presence of a high degree of collinearity between DIV and NIIs. To confirm this result we estimate Eq. 6 by excluding from the independent variables DIV (Models (II) and (V) for SHROE and SHROA, respectively) and NIIs (Models (III) and (VI)) alternatively. If considered separately, we find that \(\hat \beta _1 \) and \(\hat \beta _2 \) are positive and statistically significant.

When we check for the value of the first derivative of risk-adjusted return for NIIs, we verify that in both models it is positive and highly significant. An increase of NIIs, whose mean value in our sample is under 50%, and, as consequence, of DIV produces an increase in the risk-adjusted return.

A positive influence of NIIs and DIV on SHROE and SHROA is inconsistent with studies on the U.S. experience, such as those by Stiroh and Rumble (2006) and Stiroh (2004a), but is consistent with Smith et al. (2003), who deal with the European experience.Footnote 3 Thus, our study appears to confirm the remarkable structural and regulatory differences between the European and U.S. markets. The differences, which DeYoung and Rice noted in their 2004 study, can explain the different relation between income diversification and risk-adjusted returns.

In our interpretation, one of the most important differentiating structural factors between U.S. and EU banking industries is bank size. According to data reported in Jones and Critchfield (2005), as of 2003, in the U.S., small banks held 14% of total bank assets; in the European Union the corresponding market share is 4.1% (European Central Bank 2005). On this point, Jones and Critchfield (2005) underline that “in the absence of a new shock to the industry, the U.S. banking industry is likely to retain a structure characterized by several thousand very small to medium-size community bank organizations, a less-numerous group of midsize regional organizations, and a handful of extremely large multinational banking organizations. [...] the U.S. banking industry is not likely to resemble the banking industries in countries such as Germany, which have only a handful of universal banks” (Jones and Critchfield 2005, p. 48). For example, in our data, the mean bank size is about 2.6 times as big as the bank size observed by Stiroh and Rumble (2006).

But how can bank size influence the relation between income diversification and risk-adjusted bank profits? Economies of scale and being capable of investing more intensively in ICT mean that larger banks are better placed to manage the operating leverage associated with fee-based transactions (DeYoung and Roland 2001). The use of new technologies, such as online services, enables banks to sell additional products at very low—or even no—marginal costs. These benefits can compensate for the disadvantages that arise from the growth of fixed costs linked to investments in ICT. Stiroh (2004a) also notes the importance of dimension for U.S. banks. He shows that income diversification affects banks’ risk-adjusted performance negatively in the case of community banks (banks with assets below $300 million that do not belong to multibank groups) and positively in the case of other kinds of banks.

To check how the share of non-interest income interacts with bank size, in Eq. 6 with SHROE as dependent variable, we add two more regressors, the product between ASSETS and NIIs and the product between ASSETS squared and NIIs. In Table 4, Model (I), we see that the first derivative of risk-adjusted returns with respect to NIIs, evaluated at the mean value of NIIs and ASSETS, is positive and significant, showing that the increase of the non-interest income share has a positive influence on SHROE.

To investigate the size and direction of the results away from the means of the data, on the basis of Model (I) in Table 4, we construct a matrix of the estimates of the first derivative of risk-adjusted returns for NIIs evaluated at different values of the average non-interest income share and bank assets (on the basis of a percentile rank). In Table 5, we show that at the 25th, 50th, and 75th percentiles of non-interest income share, the derivative increases as ASSETS increases. This finding confirms that the relation between risk-adjusted returns and non-interest income is stronger at large banks.

Moreover, in Table 5 we see that the first derivative of risk-adjusted returns is not significant for banks at the 25th percentile of ASSETS and 75th percentile of NIIs. This result suggests that small banks can make gains from increasing non-interest income only when they have a low level of NIIs to start with.

In Models (II) and (III) of Table 4, we perform an additional test that addresses the bank size issue. In this test we re-estimate Model (I) for two subsamples: the smaller and the larger half of banks. We rank our sample of 85 banks on the basis of their average size and divide it into two groups obtaining 42 small banks and 43 large banks. In these two separate regressions, the first derivative, which we evaluate at the mean value of NNIs and ASSETS, turns out to be positive and significant only for larger banks (Model III), while it is positive but not statistically significant for smaller banks (Model II). However, for larger banks (Model III), we find that the DIV coefficient is not significant. This result suggests that there are limits to diversification gains as banks get larger.

There are two other possible explanations that might explain the systematic differences found in studies that compare European and U.S. banks. The first is the longevity of fee-based relationships: although the switching costs associated with fee-based relationships are lower than those of lending relationships, customer behavior suggests that clients change their reference bank rarely (European Commission 2006). The second is the diffusion of credit scoring methods: the use of these risk-analysis methods, mostly by larger banks, combined with the possibility of using information contained in data-sharing credit registers, can reduce the switching costs in transaction-based lending both for borrowers and lenders.

Stiroh (2004b) argues that an aspect that could limit the benefits of income diversification is the cross-selling of banking products. However, on the basis of the European Commission (2006) data, the number of products purchased together from the same bank by a consumer or SME in Italy is very small (for consumer and SMEs, 2 and about 2.5, respectively).

Clearly, the degree of cross-selling in Italy, and more generally in Europe, is so small that it is improbable that it can produce a positive correlation between interest and non-interest income.

The unavailability of reliable data on the longevity of fee-based relationships, on the diffusion of credit scoring methods, and on the incidence of cross-selling does not allow us to perform an empirical investigation on the impact of these three factors.

Control Variables

For our control variables, we calculate the first derivative of SHROE with respect to ASSETS, on the basis of Model (I), Table 4, and find a negative-sloped linear relation in bank size that intersects the x-axis at a level of ASSETS equal to about 10.5. This finding suggests that the relation between SHROE and bank size is an inverted U-shape: as bank size increases, risk-adjusted returns increase too, but this effect tends to die off. Beyond the size threshold, equal to 10.5 (nearly 59% of the data are under this level), it reverses sign.

In our view, this outcome happens because up to a certain size level, banks are able to exploit scale and scope economies and more efficient risk-management techniques. After a given threshold, the difficulties that arise from the greater complexity of a larger organizational structure and the rigidity of the cost structure lead to a worsening of the risk-adjusted returns. This outcome could be due to the differences in the cost structure related to the two kinds of bank businesses (DeYoung and Rice 2004b). The costs of the inputs needed to increase lending activity are mainly variable (the interest rate paid on additional funding), while the costs to increase activities that generate non-interest income are mainly fixed (e.g., investment in human capital).

The coefficient associated with LOAN is positive and statistically significant for all the specifications considered. This result indicates that, ceteris paribus, for Italian banks an increase in the lending activity will lead to greater risk-adjusted returns. Thus, our findings differ from Stiroh’s (2004a) and Stiroh and Rumble’s (2006). These authors interpret their finding of a negative coefficient as an indication that lending is a risky activity. However, we note that in their econometric specification they do not consider the loan quality, which in our opinion, once taken into account, can make the difference. On the other hand, in DeYoung and Rice (2004a), the coefficient on the ratio between loans and bank assets comes out positive but statistically not significant.

The BAD control variable has a negative impact on risk-adjusted returns. This result is in line with the DeYoung and Rice (2004a) findings.

REGION enters all the equations with a significant and positive sign. Thus, ceteris paribus, banks with a restricted spatial presence would exhibit a higher increase in their risk-adjusted profits. Considering that banks with a high geographic concentration (dispersion) are those with a smaller (larger) size, the variable REGION is going to only partially offset the positive effect of ASSETS. Morgan and Samolyk (2003) find the same evidence. Acharya et al. (2002) find that geographic diversification produces an improvement in the risk–return trade-off only for moderate-risk banks, while for the high risk banks the effect is negative.

To evaluate the interaction of REGION with income diversification, we divide our sample in two subsamples: in the first subsample (Table 4, Model (IV)) we include the banks with a presence in only one Italian region (REGION=1). In the second subsample we consider the remaining banks (Table 4, Model (V)). In both Models (IV) and (V) the first derivative of SHROE with respect to NIIs is positive and significant. However, we find that the DIV coefficient in Model (V) becomes negative, signalling that a wider geographic presence can produce income diversification losses. A possible explanation of such an outcome may be attributable to the higher and more volatile operating costs associated with a widespread network of branches. Moreover, geographic focus could enable banks to gain higher benefits in terms of clients’ monitoring.

Another explanation of this result is the diminishing importance of geographic diversification that is due to the diffusion of credit derivatives and securitization. This diffusion allows banks to optimize the active management of credits with low operating costs (see, e.g., Winton 1999). However, we stress that during the period 1993–2003, 60% of all banks with geographic focus belonged to holding companies. This figure shows that the geographic diversification obtains at the group level (Klein and Saidenberg 1997, show that bank holding companies do get benefits from geographic diversification).

Robustness Tests

One drawback of the DIV measure of diversification is the fact that it can change even when the underlying product mix does not change; for example, if a bank reduces its loan interest rates but increases its loan origination fees, leaving total income unchanged. To test the robustness of our regression results to the change of the income diversification measure, we construct a new measure that takes into account three separate components of non-interest income. This measure is equal to:

where NCOMMs is the share of net commissions income (i.e., the yield from a wide variety of banking services ranging from provision of guarantees to securities and payment transactions, from bonds and account administration to saving management services, from investment banking to distribution of third parties’ products) over net operating income; NTRADs is the share of net trading income, which is derived from equities, bonds, foreign exchange, and derivatives trading, over net operating income; and OTHERs is the share of other non-interest income, which is derived from participations, financial leasing, and merchant banking, over net operating income.

We run a new set of regressions on the basis of the following model:

Table 6 displays the regression results for Eq. 9. The impact of the measure of income diversification based on the non-interest income components (DIVC) is positive and statistically significant. The first derivative of risk-adjusted returns with respect to NIIs for an increase of one of its three components (NTRADs, NCOMMs, and OTHERs, respectively) is positive and statistically significant. Thus, income diversification obtained through a change of the bank product mix has a positive influence on risk-adjusted returns. Moreover, the differences between the coefficients of the three components of NIIs, considered as pairs, are not statistically significant. This result suggests that the source of non-interest income is less important than the level of NIIs. Broadly speaking, the diversification gains seem to be associated with non-interest income in general, not with the specific business lines that generate that income.

We successfully test the robustness of our results in several other ways. We apply to Eq. 6 a model with time fixed effects, but with bank random effects. Furthermore, we redefine the dependent variables of Eq. 1, taking into account as profit measures, and hence as Sharpe ratios, the return on equity and assets before tax. Finally, we estimate Eq. 6 by using a data sample whose bank performance measures are truncated at the 1st and 99th percentiles. We do not find relevant differences either in the signs or in the statistical significance of the estimated coefficients.Footnote 4

Conclusions

Although the shift toward non-interest revenues is undisputedly recognized as one of the important factors behind the recovery of Italian banks’ profitability, whether the increase in return has been obtained at the expense of higher profit volatility is still an open question.

In this paper, we try to answer that question through an empirical analysis for which we use data from a sample of Italian banks for the period 1993–2003. We run panel regressions of a set of risk-adjusted return measures on an income diversification measure that we derive from a Herfindahl–Hirschman Index of specialization.

On the basis of our regression results, we conclude that for our balanced sample of Italian banks during the 1993–2003 timeframe, the relation between income diversification and risk-adjusted returns has been positive, that is, the increase in non-interest income has been associated with an increase in profits per unit of risk. We also find an inverted U-shaped relation between profits per unit of risk and bank size.

Our results also suggest that small banks with very small non-interest income shares experience financial performance gains from increasing non-interest income. Further that measured performance gains are associated with non-interest income in general and not with the specific business lines that generate that income.

Our findings confirm the earlier findings of Smith et al. (2003), namely, that the different impact of the increase in non-interest income share on European and U.S. banks. In our interpretation, this outcome is due to the existing structural and regulatory differences. One of the main structural economic factors that can positively affect the relation between income diversification and income stability is bank size. In our view, economies of scale and the capability of investing more intensively in ICT allow larger banks to manage the operating leverage associated with fee-based transactions (see DeYoung and Roland 2001) much better than small-sized banks. The use of new technologies, such as online services, enables banks to sell additional products and services, entailing limited or no operating marginal costs. These benefits can more than compensate the disadvantages from higher fixed costs linked to investment in ICT.

We find an empirical confirmation of this interpretation: the relation between risk-adjusted return and non-interest income is stronger at large banks. Thus, the findings in U.S. studies, that financial performance is either neutral or negative with respect to increases in non-interest income, may simply reflect the fact that most U.S. banks are relatively small. Further study is thus warranted.

Alternatively, it may be the case that the typical Italian bank was ITC-deficient at the start of our sample period (relative to the typical U.S. bank), and that the increase in non-interest income during our sample period was simultaneously accompanied by increased investment in ITC necessary for these new products and production processes. Thus, the improvement in financial performance associated with non-interest income could be at least partly caused by improved overall productive efficiency. This explanation would be consistent with research on the drivers of Italian bank mergers (Focarelli et al. 2002), and suggests that these banks merged in order to “modernize”, i.e., increase both fee-based income and ITC investment.

Other possible explanations that we do not test here, due to lack of data, are the longevity of fee-based relationships (switching costs associated with fee-based relationship are lower than that of lending relationship, but the observation of customer behavior tells us that clients rarely change their reference bank; see European Commission 2006); the diffusion of credit scoring methods (the use of these risk-analysis methods, most of all in larger banks, combined with the possibility of using information contained in data sharing credit registers, can reduce the switching costs in transaction-based lending both for borrowers and lenders); the degree of cross-selling of banking products (the low number of products purchased together from the same bank by a consumer or an SME in Italy and Europe in general, signal that the correlation between interest and non-interest income should be small or negative). The role of these last three factors could be the subject of future research.

Notes

In the U.S., the increase in non-interest income started in the early 1980s and took around 20 years to level off. In Italy, the process started much later, so it is possible that we are using data that refer to a transition phase. However, the period we examine is long enough to include two macroeconomic recessions (1993 and 2001) and the explosion of the financial markets bubble (2000).

A data point is considered a far outlier if its value is less than the first quartile of distribution minus three times the difference between the first and third quartiles (interquartile range, or IQR) or is greater than the third quartile plus three times the IQR. In order to save space, we do not report the results of such a procedure.

Testing exactly the same fixed effect specifications used in Stiroh and Rumble (2006, Table 8) we find a positive coefficient for NIIs. For the sake of brevity, we do not report the regression outcome.

The results of these robustness tests are available in a longer working paper version of this study upon request.

References

Acharya VV, Hasan I, Saunders A (2002) The effects of focus and diversification on bank risk and return: evidence from individual bank loan portfolios. Discussion paper no. 3252, Centre for Economic Policy Research, March

Baltagi BH (2005) Econometric analysis of panel data. Wiley, Chichester

DeYoung R, Rice T (2004a) Non-interest income and financial performance at U.S. commercial banks. Financ Rev 39(1):101–127 (February)

DeYoung R, Rice T (2004b) How do banks make money? The fallacies of fee income. Federal reserve bank of Chicago. Econ Perspect 4Q:34–51 (November)

DeYoung R, Roland KP (2001) Product mix and earnings volatility at commercial banks: evidence from a degree of leverage model. J Financ Intermed 10(1):54–84 (January)

European Central Bank (2000) EU banks’ income structure, Mimeo, April

European Central Bank (2005) EU banking sector stability, Mimeo, October

European Commission (2006) Interim Report II, Current accounts and related services, Sector inquiry under article 17 regulation 1/2003 on retail banking, Mimeo, July

Focarelli D, Panetta F, Salleo C (2002) Why do bank merge? J Money, Credit Bank 34(4):1047–1066 (November)

Italian Banking Association (2003) Italian Banks, a ten years revolution, Mimeo, October

Jones KD, Critchfield TS (2005) Consolidation in the U.S. Banking industry: is the long, strange trip about to end? FDIC Bank Rev 17(n. 4):31–61 (February)

Klein PG, Saidenberg MR (1997) Diversification, organization, and efficiency: evidence from bank holding companies.” Working Papers 97–27, Wharton School Center for Financial Institutions, University of Pennsylvania, February

Morgan DP, Samolyk K (2003) Geographic diversification in banking and its implications for bank portfolio choice and performance. Working Paper, Federal Reserve Bank of New York, February

Smith R, Staikouras C, Wood G (2003) Non-interest income and total income stability. Working Paper 198, Bank of England, August

Stiroh KJ (2004a) Do community banks benefit from diversification? J Financ Serv Res 25(2–3):135–160 (April)

Stiroh KJ (2004b) Diversification in banking: is non-interest income the answer? J Money, Credit Bank 36(5):853–882 (October)

Stiroh KJ, Rumble A (2006) The dark side of diversification: the case of U.S. financial holding companies. J Bank Financ 30(8):2131–2161 (August)

Tukey JW (1977) Exploratory data analysis. Addison-Wesley, Massachusetts

Winton A (1999) Don’t put all eggs in one basket? Diversification and specialization in lending. Working Paper, University of Minnesota, Finance Department, September

Acknowledgment

We are indebted to Riccardo Brogi, Konstantinos Drakos, Marcello Messori, Pier Carlo Padoan, Gianfranco Torriero, and two anonymous referees for their helpful comments. The usual disclaimer applies. We would like to thank Marialuisa Giachetti for her help in the data set acquisition. The opinions expressed in the paper are those of the authors and in no way involve the responsibility of the Italian Banking Association.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Chiorazzo, V., Milani, C. & Salvini, F. Income Diversification and Bank Performance: Evidence from Italian Banks. J Finan Serv Res 33, 181–203 (2008). https://doi.org/10.1007/s10693-008-0029-4

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10693-008-0029-4