Abstract

Aggregate domestic consumption spending is one of the prime drivers of economic progress that facilitates the process of industrialization, international trade, and innovation, but its effect on the environment remains underresearched. This paper proposes a novel framework to explain the impact of aggregate domestic consumption spending per capita (ADCSP) on carbon dioxide emissions (CO2e) in South Africa. Using the autoregressive distributed lag (ARDL) technique, the results indicated that the ADCSP determines CO2e in the short-run (SR) and long-run (LR). From ADCSP to carbon intensity (ADCSP-CI) estimations, it was observed that an increase (1%) in ADCSP increases CO2e in both the LR (0.31%) and SR (0.22%). Furthermore, the NARDL estimations showed that the LR effects of positive shocks in the ADCSP on CO2e are comparatively stronger than the SR effects. The paper offers important policy implications for academics, theorists, and policymakers.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Even though speedy economic growth in the past few decades has positively affected the social, technological, economic, urban, and industrial landscape of the emerging economies, it is also responsible for the increasing levels of greenhouse gases (GHGs) emissions and global temperature. Environmentalists tend to agree that human actions and activities (e.g., industrialization, production, and fossil-fuel consumption) are primary determinants of climate change and CO2e (Mikayilov et al. 2018). According to the National Research Council, Division on Earth and Life Studies, Board on Atmospheric Sciences and Climate (2010), climate change are also responsible for melting glaciers, rising sea-levels and global temperatures, weather abnormalities, and animal migrations. CO2e is frequently identified as the topmost pollutant in the developed and developing economies, which primarily originates from the combustion of fossil-fuel combustion for transportation, power plants, manufacturing, building energy systems, agriculture, and cement production (Kibert 2012). Recognizing that fossil-fuel consumption has been a prominent phenomenon affecting climate change in the advanced industrialized economies, both developed and developing nations are collaborating to address the environmental effects of increasing per capita emissions in the emerging economies, e.g., Africa, India and China (Yotova 2009).

Previous literature offers economic factors including, per capita income, population growth rate, foreign direct investments, trade openness, financial development, energy consumption, and globalization are main determinants of CO2e (Salahuddin et al. 2018; Sephton and Mann 2013; Sung et al. 2018; Yu et al. 2018). This paper, however, considers aggregate consumption as another unexplored determinant of CO2e for several reasons. Aggregate consumption is a critical component of the gross domestic product (GDP), and any changes in aggregate demand affect economic growth and development. More so, rising aggregate consumption triggers domestic and foreign industrial production. Due to rising consumer demand for industrial goods in the emerging economies, producers are often encouraged to use more energy and capital goods, which in turn, causes CO2e. South Africa, as an emerging economy, has shown impressive growth figures (on average) for real GDP (3.03%, on average) and consumption expenditures (3.64%, on average) during 1960–2017. Past studies reflect a significant rise in energy use (0.83%, on average) and CO2e (2.83%) during 1960–2014. Providing that total consumption has remained higher than the real GDP growth rate (on average), it appears irrational to undermine its potential implications for CO2e in South Africa.

The paper makes several contributions to previous theory and research in economics and the environment. As of this work, no published study has offered a theoretical or empirical framework on the possible association between ADCS (per capita) and CO2e. Second, the study proposes a new theoretical concept that explains how ADCS (per capita) causes CO2e. Third, the paper extends prior literature given that current models are derived from the national income identity and Environmental Kuznets Curve (EKC) hypothesis.

The paper is organized into the following parts. Section 2 presents a brief overview of social, economic, and environmental indicators. Section 3 critically examines related literature on the link between different economic indicators and CO2e. Section 4 focuses on the theoretical framework. Section 5 covers data sources, Materials and methods, and model specifications. Section 6 includes results and discussion. Section 7 presents the conclusion, followed by policy implication, limitations, and future research directions.

2 South Africa: A Social, Economic and Environmental Perspective

2.1 An Overview of Social and Economic Progress in South Africa

In 1994, South Africa’s transition from an unelected government to a democratic country was nothing less than extraordinary. This historic-political shift, by all means, signifies political, economic and social freedom for suppressed and deprived natives. Rodrik (2008) argues that the long-standing ethnic and income disparity would have eventually led to a ‘sham democracy’ if key political stakeholders underestimated the democratization, cycle of macroeconomic populism, and fair redistribution. Indeed, rapid socio-economic progress in the past two decades has facilitated public access to services, electricity, housing, health, and equal education opportunities. Approximately 90 and 84% of households have gained access to piped water and electricity, respectively. The policy of redistributive grants has successfully uplifted many above the poverty levels, while independent judiciary and improvements (infrastructure and technology) in the financial and banking systems have turned South Africa into regional financial capital (OECD Economic Surveys: South Africa 2017 2017). That said, the country appears to be struggling at many fronts despite stated accomplishments: declining economic growth rate due to supply-side constraints (i.e. electricity shortages and decreasing commodity prices); increasing unemployment levels, and stagnated GDP per capita (see Fig. 1).

Source: OECD Economic Surveys: South Africa 2017 (2017)

South Africa’s unemployment rate, GDP growth (2001–2016), and GDP per capita (2000–2015).

Figure 2 depicts that the household consumption spending plays a significant role in South Africa’s economic growth. In 2017, private consumption also reflected an increase, i.e. 2.2%. Due to dissipating drought effects and a robust exchange rate that exerted a low pressure on family’s financial plans, the moderation in the average price-levels allowed people to pay in real terms (African Development Bank 2019).

Source: The World Bank (2018)

South Africa’s GDP expenditures for the period 2014 (Q1)–2017 (Q4).

Figure 3, depicting the poverty, inequality and employment situation in South Africa, suggests that upper-middle-income economies (i.e. Namibia = 19.3%; Botswana = 28.7%) have greatly benefited from government’s poverty alleviation policies and efforts, but reported estimates for low-income economies like Malawi (70.7%) and Madagascar (50.7%) reflect unimpressive improvements in poverty (African Development Bank 2019).

Source: African Development Bank (2019)

Poverty statistics for South Africa by income groups (2000–2006, 2010–2015).

2.2 CO2e and Pollution: A South African Perspective

In South Africa, majority of people live in the urban areas, comprising of densely-populated small towns, and thus, it seems unfair to criticize either households or industries for the poor state of air quality and carbon emissions (Leiman et al. 2007). For long, South Africa has been struggling to reduce the detrimental effects of CO2e on human lives across different regions. Apart from air quality problems arising from mobile usage and industrial sources, the excessive utilization of fossil-fuels for lighting, heating, and cooking are also contributing to growing health problems in South Africa (Friedl et al. 2009; Henneman et al. 2016; Longhurst et al. 2015). From 2002 to 2013, the electricity consumption has increased from 50 to 78%, respectively (Lin and Sepulveda 2013). Despite the availability of electricity, solid-fuels are often consumed in some provinces as the primary source of energy for cooking and other economic activities (Matinga et al. 2014). This consumption trend has increased the risk of fire accidents and burn injuries (Kimemia et al. 2014).

In 2013, South Africa ranked among the top ten CO2-emitting countries globally by releasing 0.71 kg CO2/(2005US$GDP (PPP)) (Organisation for Economic Co-operation and Development 2015). Coal-fired power (CFP) stations are attributed as the primary sources of high emissions, while production of nearly 20% of its liquid fuels for transportation uses Sasol’s energy-intensive coal-to-liquid (CTL) process (Akhtar and Palagiano 2017). In 2010, coal was the largest contributor to GHG emanations, i.e. around 90% of the aggregate energy mix. During the 1990s, the GHG emanations increased by 1.1% each year but later peaked to around 3% each year during 2000–2008. Even though the global recession and economic slowdown (2009–2011) led to a decline in GHG emanations (see Fig. 4), per capita emanations are still higher than other middle-income economies in the world.

Source: OECD Environmental Performance Reviews: South Africa 2013 (2013)

Green house gas (GHG) emissions in South Africa during 1990–2010.

Figure 4 depicts the decoupled relationship of CO2e and economic growth. With energy sector leading as the prime source of CO2e, the transport sector reduced its emissions from 43 to (2000–2008) 23% in 2010, while the emanations in the industrial sector increased by 23%. Commercials and residential sectors had little share in overall CO2e (OECD Environmental Performance Reviews: South Africa 2013).

As shown in Fig. 5, although South Africa leads among the top-ten CO2-emitting emerging economies in Africa (45%), followed by Egypt (19%) and Algeria (14%), it remains the lowest CO2-emitter among other emerging economies in the BRICS i.e. China, Brazil, India, and Russia (see Fig. 6).

Source: The World Bank (2017)

CO2 emissions in top 10 African emerging economies.

Source: The World Bank (2017)

CO2 emissions in the BRICS economies.

3 Related Literature: Income, Energy, Trade, and CO2e Nexus

In the field of environmental and energy economics, previous research on the antecedents of environmental pollution represents three distinct strands of research: income-CO2e nexus, energy-CO2e nexus, and trade-CO2e nexus. The following part presents a brief overview of each strand in the present context.

3.1 Income Level and CO2e

As stated above, the first strand of research on the income-CO2e nexus comprises of empirical studies that examined the EKC hypothesis through various methods across different countries/regions. The EKC hypothesis posits that ecological pollution rises with the increasing national income during the early stages of economic development, reaches a certain threshold, and then decreases (Stern et al. 1996). Roca et al. (2001) further elaborates that pollution surges as per capita income expand, but higher income level tends to moderate the negative effects of pollution over time. Alexandre et al. (2017) view the EKC hypothesis as one of the most superior theories, in terms of asserting the need to maintain a balance between national income and sustainability of ecosystems. Even though many scholars have tested the EKC hypothesis over the past two decades, the results for different regions and countries are mixed. For instance, (Saboori et al. 2012) validated the EKC hypothesis for Malaysia, but argued that the inverted-U EKC curve provides but less information about the relationship dynamics that exists between income and pollution. (Panayotou 1993), however, identified the use of clean technologies, variations in the structure of output, and environmental awareness as the only factors predicting the gap between income and pollution. (Apergis et al. 2017), through non-linear approach, tested the EKC hypothesis in the United States but found support for the existence of the same in only ten states. These researchers found environmental regulations as an essential factor regulating the balance between pollution and growth. Recently, Jawad et al. (2017) have also found a non-linear rather than linear association income level and CO2e. Nevertheless, scholars have provided empirical support for the EKC hypothesis for China (Sunday et al. 2017); Pakistan (Rahman et al. 2019); Asian, African, and Latin American economies (Culas 2007); European economies (Zambrano-monserrate et al. 2018); India (Shahbaz et al. 2015); BRICS (Dong et al. 2017); eleven populous Asian economies (Rahman 2017); and France (Iwata et al. 2010).

Conversely, Pablo-romero and Jesús (2016) have attempted but failed to validate the EKC hypothesis for twenty-two Latin America and Caribbean economies. Arminen and Menegaki (2019) found the EKC hypothesis to be invalid for the group of high and upper-middle-income economies. As a possible explanation, these researchers argued that pollution and income levels in these economies have not yet reached the maximum threshold. Other researchers have also found no evidence of the validity of the EKC for different economies in Africa (Zoundi 2017); OECD and non-OECD (Özokcu and Özdemir 2017); India (Sinha and Rastogi 2017); and a sample of 152 selected economies (Alexandre et al. 2017).

3.2 Energy and CO2e

The second strand of literature focus on the energy-pollution nexus. Even though energy is often regarded as an engine of economic growth, researchers have used econometric techniques to establish that consumption and production of energy is the primary cause of negative environmental consequences and climate change in different regions and countries (Ur and Rashid 2017). Several other authors have also validated the detrimental environmental implications of energy for the OECD (Álvarez-Herránz et al. 2017); SAARC (Ur and Rashid 2017); Pakistan (Mirza and Kanwal 2017); (Ahmad et al. 2018) China; a panel of Asian economies (Ahmad et al. 2018); and a panel of world economies (Zaman and Moemen 2017). Beyond that, recent studies have shown that the integration of energy use in the EKC models is problematic and a source of possible spurious and biased results (Itkonen 2012; Jaforullah and King 2017). As an alternative, Arminen and Menegaki (2019) assert the use of fossil fuels consumption as explanatory variables (rather than energy consumption).

3.3 Trade and CO2e

The third strand of research comprises of empirical and conceptual studies on the impact of trade (export and imports) or trade openness on environmental pollution. Most studies in this study area have used the Pollution Haven Hypothesis (PHH) as a priori to examine the trade-pollution nexus. The PHH originated from the seminal work of Pethig (1976); however, Reinert et al. (2009) extended the same concept to propose that investment and trade liberalization cause pollution-intensive production in economies with weak environmental regulations. Over the years, several studies have been conducted using various econometric methods, but past empirical estimates show diverse and mixed results for a single country, regions, and panels. For instance, Sharif Hossain (2011) observed that trade openness has led to CO2e in the newly industrialized countries (NIC). The authors argued that the absence of energy conservation policies has encouraged NIC’s producers to consume excessive energy, especially fossil fuels, to produce cheap goods for exports. Al-mulali and Sheau-Ting (2014) also found a positive nexus between exports and CO2e for Western European countries, however, the authors were unable to provide a feasible explanation for the insignificant and negative association among exports and CO2e for some countries in the sample. More recently, Haug and Ucal (2019) investigated the asymmetrical connection among exports and CO2e for Turkey. The authors found that imports cause CO2e in the LR, even though the hypothesis for the inverse association between exports and CO2e was unsupported. In another study, Hasanov et al. (2018) found a positive nexus between exports, imports, and CO2e for oil-exporting economies. While Michieka et al. (2013) and Halicioglu (2011) found that exports contributed to CO2e in China and Turkey, respectively, but Jayanthakumaran et al. (2012) observed the opposite for China and India. Shahbaz et al. (2013) also reported the adverse effects of trade openness on CO2e in Indonesia.

Retrospectively, the review of previous empirical studies in the three distinct strands of research reflect the need to stretch the boundaries of traditional concepts for better understanding of empirical disparities.

4 Theoretical Framework

In an economic system, consumers and producers are integral economic agents that regulate the nexus between energy, income, trade, and CO2e. These two agents shape the success of an economic system in a manner that the producers utilize local and foreign resources (e.g., energy, material, raw materials) to fulfill the needs and demands of the consumers. Typically, consumers divide their income into savings and consumption, which is an integral part of the household’s total income and gross domestic product. In economic terms, the total national income or gross domestic product in an open economy can be expressed using the following Eq. (1).

where \(Y^{D}\), total value of domestically-produced goods or domestic total expenditures; \(C^{D}\), consumption spending on domestically produced goods; \(I^{D}\), investment spending on domestically produced goods; \(G^{D}\), government spending on domestically-produced goods; and \(X\), domestically-produced goods consumed in other countries. Consumers, investors, and governments spend money on the purchase of goods produced in both domestic and foreign markets. Thus, total spending on the purchase of goods (\(C\)) can be categorized into two parts; spending on purchase of domestically-produced goods (\(C^{D}\)) and foreign goods (\(C^{F}\)). In the same way, the total spending on capital goods (\(I\)) can be categorized into spending on the purchase of domestically-produced capital goods (\(I^{D}\)) and foreign-produced capital goods (\(I^{F}\)), while the total government’s expenses (\(G\)) can be categorised into spending on the domestically-produced goods (\(G^{D}\)) and foreign-produced goods (\(G^{F}\)). i.e.

By integrating Eqs. (2), (3) and (4) (\(C^{D}\),\(I^{D}\),\(G^{D}\)) into Eq. (1), the following Eq. (5) was obtained:

In Eq. (5), \(C - C^{F}\) represents the difference between total spending on the domestically and foreign-produced goods; \(I - I^{F}\) signifies the difference between total spending on domestically and foreign-produced goods by investor sector; \(G - G^{F}\) denotes the total spending on domestically and foreign-produced goods by government sector; and \(X^{D}\) represents domestic spending on the production of export goods. By rearranging the Eq. (5) for total spending on the purchase of goods and total spending on the purchase of imported goods, Eq. (6) was obtained.

where \(C + I + G + X\) signify aggregate spending on domestically-produced goods made by economic agents and \(C^{F} + I^{F} + G^{F}\) denotes aggregate spending on foreign-produced goods made by economic agents. By simplifying \(C + I + G + X = AC\) and \(C^{F} + I^{F} + G^{F} = AC^{F}\), Eq. (7) was obtained:

where \(AC\), aggregate spending on the consumption of goods; \(AC^{F}\), aggregate spending on the consumption of imported goods; and \(AC - AC^{F}\), aggregate domestic consumption spending (ADCS). In other words, the term ADCS is the difference between total spending on the consumption of goods as well as the total spending on the consumption of foreign-produced goods. The ADCS also includes the total spending on products produced in a country; and spending on energy goods and non-energy goods. In the present context, the spending on energy goods denotes money spent on the consumption of electricity, gas, coal, oil and other fossils fuels, while non-energy goods consist of both durable (e.g., vegetables and fruits) and non-durable items, e.g., automobiles, refrigerators, and air conditions.

As stated in the previous equation, the total domestic income is a function of total spending on domestically-produced goods produced in a country, and thus, any upsurge in the ADCSP causes an increase in the national income. The consumption of goods by economic agents increase the aggregate demand, which exerts pressure on the industries to produce more goods using different energy sources; consequently, increasing CO2e. The EKC hypothesis also explains the connection among per capita GDP and pollution by proposing that ecological disruption rises with a rise in the per capita income. In line with prior EKC literature (cf. Apergis 2016; Baek 2015; Bagliani et al. 2008; Dinda 2004; He and Richard 2010; Kearsley and Riddel 2010; Nasr et al. 2014; Sephton and Mann 2013), the nexus between per capita gross domestic production and CO2e can be written as Eq. (8);

where \(CO2\) refers to CO2e and \(Y^{D} /P\) denotes the income per capita. By dividing Eq. (7) by \(Y^{D} /P\), the following is obtained:

where \(\frac{AC}{P}\) represents the per capita aggregate spending on goods and \(\frac{{AC^{F} }}{P}\) indicates the per capita aggregate spending on imported goods. \(\frac{AC}{P} - \frac{{AC^{F} }}{P}\) is called aggregate domestic consumption spending (ADCS) per capita, described as the spending on domestically-produced goods per person. By combining Eqs. (8) and (9), the following equation depicts the positive relationship between ADCS and CO2e:

Sequentially stated, an upsurge in the ADCSP causes a rise in the industrial production and high demand for industrial products. The industrial sector, in response to this demand, increases total production and use more capital goods, natural gas, coal, and other fossil fuels that cause CO2e. Figure 7 explains the nexus between national income identity to the EKC hypothesis.

National income identity and CO2e

Given the relationship mentioned above, any change in the ADCSP is expected to predict a change in CO2e, as shown in the following Eq. (11).

where \(\Delta CO2\), change in CO2e; \({\raise0.7ex\hbox{${\Delta AC}$} \!\mathord{\left/ {\vphantom {{\Delta AC} {\Delta P}}}\right.\kern-0pt} \!\lower0.7ex\hbox{${\Delta P}$}}\), change in per capita aggregate spending and per capita; \({\raise0.7ex\hbox{${\Delta AC^{F} }$} \!\mathord{\left/ {\vphantom {{\Delta AC^{F} } {\Delta P}}}\right.\kern-0pt} \!\lower0.7ex\hbox{${\Delta P}$}}\), change in aggregate spending on imported goods; and \({\raise0.7ex\hbox{${\Delta AC}$} \!\mathord{\left/ {\vphantom {{\Delta AC} {\Delta P}}}\right.\kern-0pt} \!\lower0.7ex\hbox{${\Delta P}$}} - {\raise0.7ex\hbox{${\Delta AC^{F} }$} \!\mathord{\left/ {\vphantom {{\Delta AC^{F} } {\Delta P}}}\right.\kern-0pt} \!\lower0.7ex\hbox{${\Delta P}$}}\), change in the ADCS per capita. As presented in the mathematical form below, the changes in the ADCSP vis-a-viz CO2e termed as the aggregate domestic consumption spending per capita to carbon intensity (ADCSP-CI).

ADCSP-CI measures the changes in CO2e caused by changes in the ADCS per capita. The relationship between ADCSP and CO2e is depicted in Fig. 8.

The relationship between ADCS per capita and CO2e

In Fig. 8, \(CO2_{0}\) and \(ADCS_{0}\) represent the initial points of CO2e and ADCSP, respectively. As ADCSP increase from \(ADCS_{0}\) to \(ADCS_{1}\), CO2e also increases from \(CO2_{0}\) to \(CO2_{1}\), simultaneously. The curve arising from linking orange and blue points is described as the carbon intensity (CI)-ADCSP curve, representing the positive association between ADCSP and CO2e. The ADCSP-CI is represented by a CO2 line (a sloped line indicating variations in the CO2e (Y-axis) and the ADCSP (X-axis). The ADCSP-CI can be calculated given the availability of data on ADCSP and CO2e. The ADCSP-CI is not constant and varies with the level of ADCSP, i.e. higher the ADCSP, higher will be the ADCSP-CI. The ADCSP-CI delineates that higher ADCSP increases the aggregate demand, industrial production, energy ADCSP-CI consumption, economic growth; consequently, increasing CO2e. The ADCSP-CI enables the computation of proportionate increase/decrease of the cyclic relationship between ADCSP and CO2e.

Globally, economies experience positive/negative shocks in both SR and LR. Statistically, economic recessions (negative shock) cause a decrease in the total output, employment, consumption, industrial production, ADCS per capita, and savings. This decline in ADCS per capita also disrupts the production of goods and consumption of fossil-fuels, which mitigates CO2e. The SR policies to sustain rapid growth during initial phases of recession to increase domestic consumption and industrial production often result in excessive use of fossil-based energy sources, which generates CO2e. Instead, economies following the path of sustainable growth make incremental adjustments to boost the ADCSP, while simultaneously addressing employment and inflation problems.

5 Data Sources, Materials, and Methods

The data for this study were collected from the World Bank Database (1980–2014), comprising of CO2e (measured in kiloton (kt)), exports, and imports (measured in current US $ and population), and aggregate consumption (measured current US $ and population-annual total population). The ADCS per capita is equal to aggregate consumption plus exports minus imports and divided by the total population. The logarithmic form of all variables was used for data analysis. The ARDL technique was adopted to estimate the association between ADCSP and CO2e, while the NARDL method was adopted to assess the impact of shocks in ADCSP on CO2e. Pesaran et al. (2001) introduced the ARDL bound-testing method to assess cointegration between variables. This approach has gained wide acceptance due to its comparative advantages, robustness, and superior estimates over other econometric methods. For example, it is well-suited for small samples and data series with different orders, i.e. I(0), I(1) or both (Bildirici and Kayıkcı 2012; Dar and Asif 2017; Feridun 2010). As an extension of the ARDL approach, Shin et al. (2014) introduced the NARDL approach for economic factors with nonlinear characteristics, which can capture both the LR and SR asymmetrical links among different macroeconomic indicators (Karagöz et al. 2017; Mullineux 1990). In the same vein, the nexus between ADCSP and CO2e (along with other control variables) was tested using the ARDL equation given below:

where \(CO2\), carbon dioxide emissions; \({\text{ADCSP}}\), aggregate domestic consumption spending per capita; TO, trade openness; FFC, fossil-fuel consumption; \(\beta_{1}\) and \(\beta_{2}\), SR coefficients; \(\beta_{3}\) and \(\beta_{4}\), LR coefficients; and \(\upsilon_{t}\), error term. The error correction model of Eq. (13) can be written as:

where \(ECT\) denotes the error correction terms, the value which is obtained from the residuals of Eq. (13). \(\lambda\) shows the adjustment speed of the coefficient. Moreover, the impact of components (+ ve/− ve) of the ADCSP and CO2e are depicted in the long-run regression equation given below:

where \({\text{CO}}2\), carbon dioxide emissions (integrating of order one); \({\text{ADCSP}}_{{{\text{t}} - {\text{i}}}}^{\forall }\), aggregate domestic consumption spending per capita (integrating of order one); and \(\upgamma = (\upgamma_{1} ,\upgamma_{2} )\), a vector of LR unknown parameters. \({\text{ADCSP}}_{\text{t}}^{\forall } = {\text{ADCSP}}_{0}^{\forall } + {\text{ADCSP}}_{\text{t}}^{\forall + } + {\text{ADCSP}}_{\text{t}}^{\forall - }\), where \({\text{ADCSP}}_{\text{t}}^{\forall + }\) and \({\text{ADCSP}}_{\text{t}}^{\forall - }\), partial sum processes of variations (+ve/-ve) in the ADCSP. The partial sum of variation in \(ADCSP^{\forall }\) is depicted in the Eq. (16):

For the ARDL testing, Eq. (15) can be modified as:

where the symbol \(p\) denotes the lag order. Keeping in view the potential cointegration issues (misinterpretations of the estimated asymmetric coefficients) arising from estimating Eq. (17) (Lardic and Mignon 2008), the current study followed Shin et al. (2014) approach. That is, a limit was added to Eq. (17): \(\upgamma_{1} = - {\raise0.7ex\hbox{${\uppsi_{2} }$} \!\mathord{\left/ {\vphantom {{\uppsi_{2} } {\uppsi_{1} }}}\right.\kern-0pt} \!\lower0.7ex\hbox{${\uppsi_{1} }$}}\) and \(\upgamma_{2} = - {\raise0.7ex\hbox{${\uppsi_{3} }$} \!\mathord{\left/ {\vphantom {{\uppsi_{3} } {\uppsi_{1} }}}\right.\kern-0pt} \!\lower0.7ex\hbox{${\uppsi_{1} }$}}\). \(\varrho_{2}\) denotes the SR effect of ADCSP rise on the CO2e, while \(\varrho_{3}\) measure the short-run impact of ADCSP reduction on CO2e. So, in this step, the asymmetric SR impact of variations in variables on CO2e was measured along with asymmetric LR association. The error correction models (ECM) of the previous equation are depicted as:

The estimation of the ARDL and NARDL method involved the following procedures. Before proceeding to methodical steps, it must be noted that the ARDL method is applicable even if all the variables are the integration of order zero or one or have mixed results. In the first step, Augmented Dicky Fuller (ADF) and Phillips–Perron (PP) unit root, Zivot Andrews unit root test were carried out to check possible order of integrations. In the second step, Eqs. (13), (14), (17) and (18) were computed through the standard OLS procedure. In the third step, after estimating the ARDL and NARDL equations, bounds testing technique was used to test the presence of LR association among variables.

6 Results and Discussion

Table 1 displays the outputs of the unit-root tests. As seen, the ADF and PP tests for stationarity testing showed that all constructs were non-stationary at the level and stationary at first difference. Even though the results of the unit root tests offered support for using the ARDL and NARDL approach, these tests are unable to offer insight about the structural breaks in the series. Zivot and Andrews (1992) explain that non-stationarity in data series are often caused by structural changes in factors. Thus, it was critical to detect variations for unbiased results. Kim and Perron (2009) add that poor distribution size and low explanatory power of traditional unit-root tests often lead to biased and spurious results. Zivot and Andrews (1992) offer a unit-root test that incorporates a single unknown-structural break in the data series.

Table 2 depicts the output of Zivot–Andrew structure unit-root test with single break year. All the factors reflected non-stationarity at the level in the presence of structural breaks in 1990 (CO2e), 1991 (aggregate domestic consumption spending), 2004 (trade openness) and 2003 (fossil fuel consumptions). As seen below, CO2e, domestic aggregate consumption spending, trade openness, and fossil fuels consumption are stationary at the first difference, depicting that all the series have the same integration order (1). Of significance, it was interesting to observe that South Africa imposed several industrial, economics, trade, and energy policies to enhance its macroeconomic indicators over the sample period. For instance, the regional industrial policy implemented from 1990 to 1991 affected the aggregate industrial production, energy consumption, domestic consumption, and CO2e. Later in 2003–2004, the establishment of the International Trade Administration Commission (ITAC) also contributed to international trade, growth, and development. These trade policies and initiatives have significantly impacted the patterns of exports, imports, and fossil-fuel consumption. Furthermore, the structure break unit-root test indicated non-linearity in the data, and thus, apart from ARDL, the NARDL technique to analyze the linear and non-linear relationship among variables. After computing the integration order and identifying structural breaks, tests were conducted to select optimal lag order for further analysis. As per Table 3, the results supported the selection of lag order 3 as the maximum lag order.

Table 4 depicts the outputs of the ARDL testing. The results suggested that ADCSP had a significant and positive effect on CO2e—1% increase in ADCSP caused an increase in CO2e by 0.30% in the LR. This finding implies that an increase in the ADCSP exerted a pressure on the industrial sector to increase its spending on capital goods, fossil fuels, and infrastructure development in South Africa. A possible explanation for the high level of CO2e in South Africa resides in the changing consumption patterns from 1980 to 2014. The data on the surplus ADCSP from 1980 to 1997 reveals that the domestic aggregate consumption in South Africa was more than the aggregate spending on foreign goods, even though this trend reversed from 1998 to 2014. That said, South Africans not only spent a significant part of their income on the domestically-produced products (energy and non-energy) during 1998–2014 but also dedicated a sizeable portion of their income towards the purchase of foreign products (energy and non-energy). Additionally, the results presented a significant and positive nexus between ADCSP and CO2e in the SR—1% upsurge in the ADCSP led to a rise in CO2e by 0.23%. More so, the results also demonstrated that an upsurge in trade openness causes a rise in CO2e in both the SR and LR—1% increase in trade openness was followed by a rise in CO2e by 0.18% (LR) and 0.13% (SR). This finding suggested that the government has compromised environmental standards to boost economic growth in South Africa, a view consistent with previous findings for the West European countries (Al-mulali and Sheau-Ting 2014); oil-exporting countries (Hasanov et al. 2018); China (Michieka et al. 2013); and Turkey (Halicioglu 2011).

Next, the empirical estimates indicated that fossil fuel consumption contributes to CO2e in both the SR and LR—1% increase in fossil-fuel use increases in CO2e by 1.26% in the SR and 1.72% in the (LR). This finding suggests that excessive dependence of industrial sector on cheap fossil fuel plays a vital role in the increasing rate of CO2e, a view consistent with most recent studies for developing and developed economies (Arminen and Menegaki 2019) for; African economies (Mensah et al. 2019); emerging economies (Hanif et al. 2019); and Iran (Hanif et al. 2019). Apart from the previous tests, the co-integration between variables was examined through the F-statistic (lower and upper critical value). As seen in Table 4, the results of F-statistic (7.2) and the upper critical values—1% (5.58), 2.5% (4.79), 5% (4.16) and 10% (3.51) offered sufficient empirical evidence that the no co-integration hypothesis was rejected. This finding validated that ADCSP, TO, FFC and CO2e have an LR association. The negative and statistically significant error correction term reported in Table 4 further validated the LR nexus between variables.

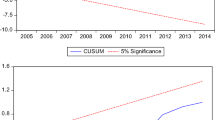

As per Table 4, the results of diagnostic tests confirmed that the estimated model was error-free. The plot of CUSUM test supported the stability of the model for the period 1980–2014 (see Fig. 9).

CUSUM plot for ARDL model

Table 5 demonstrates the results of the NARDL model. The SR estimates demonstrated positive and statistically significant values (elasticity coefficients) for the negative (0.393%) and positive (0.359%) shocks in the ADCSP—1% increase in the ADCS per capita led to an increase in CO2e by 0.59% and 0.393%, respectively. The LR estimates also showed positive values for the positive (0.395%) and negative (0.444%) shocks in the ADCSP—1% increase in the ADCS per capita led to an increase in CO2e by 0.395% and 0.444%, respectively. This finding implies that both positive and negative shocks to ADCSP generate CO2e. A possible explanation is that economic growth, employment rate, industrial production, and trade deficit improves during economic booms. With the increasing level of income, consumers are encouraged to spend more on energy and non-energy goods, subsequently increasing the aggregate demand. In response, firms utilize energy-based capital goods and fossil-fuels for production, which increases the level of CO2e. Simply stated, price competition and higher domestic consumption during economic booms encourage firms to produce more goods at lower prices and use fossil-fuels that intensifies CO2e.

On the contrary, the economic growth indicators stated-above reflect an adverse trend during economic downturns. In the initial stages, the decreasing income hurts consumers’ purchasing power and demand while encouraging producers to cut cost through the use of carbon-intensive energy sources (cheap and non-renewable). Government, in this situation, often introduce different policies for both consumers and producer to promote economic activities, e.g., bank rate reduction, tax holidays, relaxation in environmental regulation, and tax rebates. These policies and incentives increase aggregate consumption and industrial production, but also facilitate environmental pollution.

Table 5 displays the results of the NARDL bound test to confirm the co-integration among variables. The F-statistics (5.5820) supported the rejection of the no-cointegration hypothesis, offering support for LR association between variables. The coefficient of the error correction term also confirmed the LR nexus among ADCSP and CO2e. Moreover, the diagnostic tests demonstrated that the NARDL model is free from statistical problems: autocorrelation, heteroscedasticity, normality, and model specification error. As seen in Fig. 10, the plot of the CUSUM confirmed the stability of the model for the period 1980–2014. In Table 6, the outputs of the Granger-causality test validated the existence of a one-way causal relationship between positive and negative shocks to ADCSP and CO2e.

CUSUM plot for NARDL model

7 Conclusion and Policy Implications

This article has attempted to develop a novel concept to explain the impact of variations in the difference between aggregate consumption spending per person and aggregate spending on foreign goods per person causes an increase in CO2e. The present conceptual framework posits that higher ADCS per capita encourages the industrial sector to use more capital goods and fossil fuels in both the SR and LR, which in turn, increases CO2e. The paper proposes [and offer support for] the idea that shocks (+ve/-ve) in the ADCSP have a significant impact on CO2e in both the SR and LR, where the ADCSP-CI represents the swift response of variation in CO2e due to the corresponding variations in the ADCS per capita. The afore-mentioned framework was tested for South Africa using multiple data analysis techniques. First, the unit-root test (with and without structural breaks) indicated that all the variables had I(1)order of integration. Second, the ARDL model confirmed the LR relationship between ADCSP and CO2e. The ADCSP-CI showed that a 1% rise in the ADCSP increased CO2e by 0.31% and 0.22% in the LR and SR respectively, while the error correction term value for SR was found to be negative and significant at 1% level of significance. Third, the NARDL model outputs reflected that shocks (+ve/-ve) in the ADCSP have a positive and statistically significant impact on CO2e in both the SR and LR.

In terms of policy implications, although the paper empirically supports the idea that ADCSP harms the environmental quality, it discourages environmental policies that undermine the centricity of aggregate consumption for economic growth in South Africa. Instead, present findings assert the need for policymakers to allocate a significant portion of the budget towards research and development in clean and green technologies in South Africa. The application of green technology in the production process by the industrial sector to manufacture goods and products for domestic consumption is expected to yield economic and environmental benefits. Despite struggling to mitigate CO2e, South Africa has been promoting environmental policies and initiatives to combat climate change and global warming, for example, the introduction of a carbon tax to curb the rising levels of GHG emissions. In the budget of 2012–2013, the government introduced a 60% tax-free threshold on annual emissions for some strategic sectors (e.g., manufacturing, mining, and energy) to ensure its smooth transition into a low-carbon economy and sustain industry competitiveness, simultaneously. Even though South Africa stands as one of the first economies to sanction substantive climate change mitigation policies, the tax policy would exempt a significant quantity of CO2e until 2020 (Börzel and Hamann 2013). That said, South Africa has made noticeable progress in achieving its two strategic environmental goals: manage the inevitable effects of climate change by developing economic, social and environmental flexibility and emergency response capacity; play a leading role in the global efforts to reduce GHG emissions (IUCN World Commission on Environmental Law 2015).

Finally, some limitations of this study presented hereafter are expected to open multiple avenues for future research. First, although the study used ADCS per capita along with trade openness and fossil fuel consumption, researchers are encouraged to examine the same construct the unique relationship dynamics of energy and non-energy goods, separately. Second, future researchers can also examine the current conceptual model at the disaggregated level. Third, the empirical results for the proposed theoretical model represent South African perspective only. Perhaps, testing the present model for other developing economies, especially for the newly industrialized nations (NIN) and the BRICS economies is expected to explain the unique anomalies across different countries and regions. Fourth, researchers can also add greenhouse gases other than CO2 to enrich current findings. Fifth, current model combines all domestic components of expenditures; however, a separate study is needed to investigate the influence of domestic consumption on environmental quality vis-a-viz net exports. Sixth, the current model can be further developed using other exogenous factors, i.e. financial development, monetary policy, environmental regulations, research and development expenditures, and innovations in clean technologies. Lastly, researchers are encouraged to test the ADCS-CO2e nexus using the data on consumption-based CO2e for new insight.

References

African Development Bank (2019) Southern Africa Economic Outlook

Ahmad M, Khan Z, Ur Rahman Z, Khan S (2018) Does financial development asymmetrically affect CO2 emissions in China? An application of the nonlinear autoregressive distributed lag (NARDL) model. Carbon Manag 9(6):631–644. https://doi.org/10.1080/17583004.2018.1529998

Akhtar R, Palagiano C (2017) Climate change and air pollution: the impact on human health in developed and developing countries. Springer, Cham

Alexandre T, Cruz L, Barata E, García-sánchez I (2017) Economic growth and environmental impacts: an analysis based on a composite index of environmental damage. Ecol Ind 76(x):119–130. https://doi.org/10.1016/j.ecolind.2016.12.028

Al-mulali U, Sheau-Ting L (2014) Econometric analysis of trade, exports, imports, energy consumption and CO2 emission in six regions. Renew Sustain Energy Rev 33:484–498. https://doi.org/10.1016/J.RSER.2014.02.010

Álvarez-Herránz A, Balsalobre D, Cantos JM, Shahbaz M (2017) Energy innovations-GHG emissions nexus: fresh empirical evidence from OECD countries. Energy Policy 101:90–100. https://doi.org/10.1016/J.ENPOL.2016.11.030

Apergis N (2016) Environmental Kuznets curves: new evidence on both panel and country-level CO2 emissions. Energy Econ 54:263–271. https://doi.org/10.1016/j.eneco.2015.12.007

Apergis N, Christou C, Gupta R (2017) Are there environmental Kuznets curves for US state-level CO2 emissions? Renew Sustain Energy Rev 69(November 2016):551–558. https://doi.org/10.1016/j.rser.2016.11.219

Arminen H, Menegaki AN (2019) Corruption, climate and the energy-environment-growth nexus. Energy Econ 80:621–634. https://doi.org/10.1016/j.eneco.2019.02.009

Baek J (2015) Environmental Kuznets curve for CO2 emissions: the case of Arctic countries. Energy Econ 50:13–17. https://doi.org/10.1016/J.ENECO.2015.04.010

Bagliani M, Bravo G, Dalmazzone S (2008) A consumption-based approach to environmental Kuznets curves using the ecological footprint indicator. Ecol Econ 65(3):650–661. https://doi.org/10.1016/j.ecolecon.2008.01.010

Bildirici ME, Kayıkcı F (2012) Economic growth and electricity consumption in emerging countries of Europa: an ardl analysis. Econ Res 25(3):538–559. https://doi.org/10.1080/1331677X.2012.11517522

Börzel T, Hamann R (2013) Business and climate change governance: South Africa in comparative perspective. Palgrave Macmillan, UK. Retrieved from https://books.google.com.pk/books?id=e2WqmwEACAAJ

Culas RJ (2007) Deforestation and the environmental Kuznets curve: an institutional perspective. Ecol Econ 61(2–3):429–437. https://doi.org/10.1016/j.ecolecon.2006.03.014

Dar JA, Asif M (2017) Is financial development good for carbon mitigation in India? A regime shift-based cointegration analysis. Carbon Manag 8(5–6):435–443. https://doi.org/10.1080/17583004.2017.1396841

Dinda S (2004) Environmental Kuznets curve hypothesis: a survey. Ecol Econ 49(4):431–455. https://doi.org/10.1016/j.ecolecon.2004.02.011

Dong K, Sun R, Hochman G (2017) Do natural gas and renewable energy consumption lead to less CO2 emission? Empirical evidence from a panel of BRICS countries. Energy 141:1466–1478. https://doi.org/10.1016/J.ENERGY.2017.11.092

Feridun M (2010) Capital reversals and exchange market pressure: evidence from the autoregressive distributed lag (ARDL) bounds tests. Econ Res 23(4):11–21. https://doi.org/10.1080/1331677X.2010.11517430

Friedl AE, Holm DF, John J, Kornelius G, Pauw CJ, Oosthuizen RM, Van Niekerk A (2009) Air pollution in dense, low-income settlements in South Africa. Retrieved from https://www.semanticscholar.org/paper/AIR-POLLUTION-IN-DENSE-%2C-LOWINCOME-SETTLEMENTS-IN-Friedl-Holm/b3a930b2278eb9874f6b52ebadc2a0df1556515d

Halicioglu F (2011) A dynamic econometric study of income, energy and exports in Turkey. Energy 36(5):3348–3354. https://doi.org/10.1016/J.ENERGY.2011.03.031

Hanif I, Faraz Raza SM, Gago-de-Santos P, Abbas Q (2019) Fossil fuels, foreign direct investment, and economic growth have triggered CO2 emissions in emerging Asian economies: some empirical evidence. Energy 171:493–501. https://doi.org/10.1016/J.ENERGY.2019.01.011

Hasanov FJ, Liddle B, Mikayilov JI (2018) The impact of international trade on CO2 emissions in oil exporting countries: territory vs consumption emissions accounting. Energy Econ 74:343–350. https://doi.org/10.1016/J.ENECO.2018.06.004

Haug AA, Ucal M (2019) The role of trade and FDI for CO2 emissions in Turkey: nonlinear relationships. Energy Econ. https://doi.org/10.1016/J.ENECO.2019.04.006

He J, Richard P (2010) Environmental Kuznets curve for CO2 in Canada. Ecol Econ 69(5):1083–1093. https://doi.org/10.1016/j.ecolecon.2009.11.030

Henneman LRF, Rafaj P, Annegarn HJ, Klausbruckner C (2016) Assessing emissions levels and costs associated with climate and air pollution policies in South Africa. Energy Policy 89:160–170. https://doi.org/10.1016/J.ENPOL.2015.11.026

Itkonen JVA (2012) Problems estimating the carbon Kuznets curve. Energy 39(1):274–280. https://doi.org/10.1016/j.energy.2012.01.018

IUCN World Commission on Environmental Law (2015) Ethics and climate change: a study of national commitments. IUCN. Retrieved from https://books.google.com.pk/books?id=PLpFCgAAQBAJ

Iwata H, Okada K, Samreth S (2010) Empirical study on the environmental Kuznets curve for CO2 in France: the role of nuclear energy. Energy Policy 38(8):4057–4063. https://doi.org/10.1016/j.enpol.2010.03.031

Jaforullah M, King A (2017) The econometric consequences of an energy consumption variable in a model of CO2 emissions. Energy Econ 63:84–91. https://doi.org/10.1016/J.ENECO.2017.01.025

Jawad S, Shahzad H, Ravinesh R, Zakaria M (2017) Carbon emission, energy consumption, trade openness and financial development in Pakistan: a revisit. Renew Sustain Energy Rev 70(November 2016):185–192. https://doi.org/10.1016/j.rser.2016.11.042

Jayanthakumaran K, Verma R, Liu Y (2012) CO2 emissions, energy consumption, trade and income: a comparative analysis of China and India. Energy Policy 42:450–460. https://doi.org/10.1016/J.ENPOL.2011.12.010

Karagöz M, Zehir C, Bildirci M (2017) Istanbul as a global financial center. Retrieved from https://books.google.com.pk/books?id=mcI3DwAAQBAJ

Kearsley A, Riddel M (2010) A further inquiry into the pollution haven hypothesis and the environmental Kuznets curve. Ecol Econ 69(4):905–919. https://doi.org/10.1016/j.ecolecon.2009.11.014

Kibert CJ (2012) Sustainable construction: green building design and delivery. Wiley. Retrieved from https://books.google.com.pk/books?id=gSRHAAAAQBAJ

Kim D, Perron P (2009) Unit root tests allowing for a break in the trend function at an unknown time under both the null and alternative hypotheses. J Econ 148(1):1–13. https://doi.org/10.1016/j.jeconom.2008.08.019

Kimemia D, Vermaak C, Pachauri S, Rhodes B (2014) Burns, scalds, and poisonings from household energy use in South Africa: are the energy-poor at greater risk? Energy Sustain Dev 18:1–8. https://doi.org/10.1016/J.ESD.2013.11.011

Lardic S, Mignon V (2008) Oil prices and economic activity: an asymmetric cointegration approach. Energy Econ 30(3):847–855. https://doi.org/10.1016/J.ENECO.2006.10.010

Leiman A, Standish B, Boting A, van Zyl H (2007) Reducing the healthcare costs of urban air pollution: The South African experience. J Environ Manag 84(1):27–37. https://doi.org/10.1016/J.JENVMAN.2006.05.010

Lin JY, Sepulveda CP (2013) Annual World bank conference on development economics 2011: development challenges in a post-crisis World. Retrieved from https://books.google.com.pk/books?id=DXeAAQAAQBAJ

Longhurst JWS, Capilla C, Brebbia CA, Barnes J (2015) Air pollution XXIII. Retrieved from https://books.google.com.pk/books?id=ldKrCQAAQBAJ

Matinga MN, Clancy JS, Annegarn HJ (2014) Explaining the non-implementation of health-improving policies related to solid fuel-use in South Africa. Energy Policy 68:53–59. https://doi.org/10.1016/J.ENPOL.2013.10.040

Mensah IA, Sun M, Gao C, Omari-Sasu AY, Zhu D, Ampimah BC, Quarcoo A (2019) Analysis on the nexus of economic growth, fossil fuel energy consumption, CO2 emissions and oil price in Africa based on a PMG panel ARDL approach. J Clean Prod 228:161–174. https://doi.org/10.1016/J.JCLEPRO.2019.04.281

Michieka NM, Fletcher J, Burnett W (2013) An empirical analysis of the role of China’s exports on CO2 emissions. Appl Energy 104:258–267. https://doi.org/10.1016/J.APENERGY.2012.10.044

Mikayilov JI, Galeotti M, Hasanov FJ (2018) The impact of economic growth on CO2 emissions in Azerbaijan. J Clean Prod 197:1558–1572. https://doi.org/10.1016/J.JCLEPRO.2018.06.269

Mirza FM, Kanwal A (2017) Energy consumption, carbon emissions and economic growth in Pakistan: dynamic causality analysis. Renew Sustain Energy Rev 72:1233–1240. https://doi.org/10.1016/J.RSER.2016.10.081

Mullineux AW (1990) Business cycles and financial crises. Retrieved from https://books.google.com.pk/books?id=63k4QupUzhYC

Nasr AB, Gupta R, Sato JR (2014) Is there an environmental Kuznets curve for South Africa? A co-summability approach using a century of data. Working papers. Retrieved from https://ideas.repec.org/p/pre/wpaper/201466.html

National Research Council, Division on Earth and Life Studies, Board on Atmospheric Sciences and Climate, C. on M. for E. G. G. E (2010) Verifying greenhouse gas emissions: methods to support international climate agreements. National Academies Press. Retrieved from https://books.google.com.pk/books?id=5jJkAgAAQBAJ

OECD Economic Surveys: South Africa 2017 (2017) OECD. Retrieved from https://books.google.com.pk/books?id=cGxnDwAAQBAJ

OECD Environmental Performance Reviews: South Africa 2013 (2013) OECD Publishing. Retrieved from https://books.google.com.pk/books?id=KfcqAQAAQBAJ

Özokcu S, Özdemir Ö (2017) Economic growth, energy, and environmental Kuznets curve. Renew Sustain Energy Rev 72(November 2016):639–647. https://doi.org/10.1016/j.rser.2017.01.059

Pablo-romero MP, Jesús J De (2016) Economic growth and energy consumption: the energy-environmental Kuznets curve for Latin America and the Caribbean. Renew Sustain Energy Rev 60:1343–1350. https://doi.org/10.1016/j.rser.2016.03.029

Panayotou T (1993) Empirical tests and policy analysis of environmental degradation at different stages of economic development. ILO working papers. Retrieved from https://ideas.repec.org/p/ilo/ilowps/992927783402676.html

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econom 16(3):289–326. https://doi.org/10.1002/jae.616

Pethig R (1976) Pollution, welfare, and environmental policy in the theory of comparative advantage. J Environ Econ Manag 2(3):160–169. https://doi.org/10.1016/0095-0696(76)90031-0

Rahman MM (2017) Do population density, economic growth, energy use and exports adversely affect environmental quality in Asian populous countries? Renew Sustain Energy Rev 77(4):506–514. https://doi.org/10.1016/j.rser.2017.04.041

Rahman Z, Hongbo C, Ahmad M (2019) A new look at the remittances-FDI-energy-environment nexus in the case of selected Asian Nations. Singap Econ Rev. https://doi.org/10.1142/S0217590819500176

Reinert KA, Rajan RS, Glass AJ, Davis LS (2009) The Princeton encyclopedia of the world economy. Princeton University Press. Retrieved from https://books.google.com.pk/books?id=BnEDno1hTegC

Roca J, Padilla E, Farre M, Galletto V (2001) Economic growth and atmospheric pollution in Spain: discussing the environmental Kuznets curve hypothesis. Ecol Econ 39:85–99. https://doi.org/10.1016/S0921-8009(01)00195-1

Rodrik D (2008) Understanding South Africa’s economic puzzles*. Econ Transit 16(4):769–797. https://doi.org/10.1111/j.1468-0351.2008.00343.x

Saboori B, Sulaiman J, Mohd S (2012) Economic growth and CO 2 emissions in Malaysia: a cointegration analysis of the environmental Kuznets curve. Energy Policy 51:184–191. https://doi.org/10.1016/j.enpol.2012.08.065

Salahuddin M, Alam K, Ozturk I, Sohag K (2018) The effects of electricity consumption, economic growth, financial development and foreign direct investment on CO2emissions in Kuwait. Renew Sustain Energy Rev 81(June):2002–2010. https://doi.org/10.1016/j.rser.2017.06.009

Sephton P, Mann J (2013) Further evidence of an environmental Kuznets curve in Spain. Energy Econ 36:177–181. https://doi.org/10.1016/J.ENECO.2013.01.001

Shahbaz M, Hye QMA, Tiwari AK, Leitão NC (2013) Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renew Sustain Energy Rev 25:109–121. https://doi.org/10.1016/J.RSER.2013.04.009

Shahbaz M, Mallick H, Kumar M (2015) Does globalization impede environmental quality in India? Ecol Ind 52:379–393. https://doi.org/10.1016/j.ecolind.2014.12.025

Sharif Hossain M (2011) Panel estimation for CO2 emissions, energy consumption, economic growth, trade openness and urbanization of newly industrialized countries. Energy Policy 39(11):6991–6999. https://doi.org/10.1016/J.ENPOL.2011.07.042

Shin Y, Yu B, Greenwood-Nimmo M (2014) Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In: Sickles RC, Horrace WC (eds) Festschrift in honor of Peter Schmidt. Springer, New York, NY, pp 281–314. https://doi.org/10.1007/978-1-4899-8008-3_9

Sinha A, Rastogi SK (2017) Collaboration between central and state government and environmental quality: evidences from Indian cities. Atmos Pollut Res 8(2):285–296. https://doi.org/10.1016/j.apr.2016.09.007

Stern DI, Common MS, Barbier EB (1996) Economic growth and environmental degradation: the environmental Kuznets curve and sustainable development. World Dev 24(7):1151–1160. https://doi.org/10.1016/0305-750X(96)00032-0

Sunday J, Song D, Shu Y, Kamah M (2017) Decoupling CO2 emission and economic growth in China: is there consistency in estimation results in analyzing environmental Kuznets curve? J Clean Prod 166:1448–1461. https://doi.org/10.1016/j.jclepro.2017.08.117

Sung B, Song W-Y, Park S-D (2018) How foreign direct investment affects CO2 emission levels in the Chinese manufacturing industry: evidence from panel data. Econ Syst 42(2):320–331. https://doi.org/10.1016/J.ECOSYS.2017.06.002

The World Bank (2017) World development report 2018: learning to realize education’s promise. World Bank Publications. Retrieved from https://books.google.com.pk/books?id=uWM9DwAAQBAJ

The World Bank (2018) South Africa economic update, vol 1. https://doi.org/10.1596/25971

Ur M, Rashid M (2017) Energy consumption to environmental degradation, the growth appetite in SAARC nations. Renew Energy 111:284–294. https://doi.org/10.1016/j.renene.2017.03.100

Yotova A (2009) Climate change, human systems, and policy—volume I. Eolss Publishers. Retrieved from https://books.google.com.pk/books?id=-DO7CwAAQBAJ

Yu Y, Deng Y, Chen F (2018) Impact of population aging and industrial structure on CO2 emissions and emissions trend prediction in China. Atmos Pollut Res 9(3):446–454. https://doi.org/10.1016/J.APR.2017.11.008

Zaman K, Moemen MA (2017) Energy consumption, carbon dioxide emissions and economic development: evaluating alternative and plausible environmental hypothesis for sustainable growth. Renew Sustain Energy Rev 74(February):1119–1130. https://doi.org/10.1016/j.rser.2017.02.072

Zambrano-Monserrate MA, Carvajal-Lara C, Urgilés-Sanchez R, Ruano MA (2018) Deforestation as an indicator of environmental degradation: analysis of five European countries. Ecol Ind 90:1–8. https://doi.org/10.1016/j.ecolind.2018.02.049

Zivot E, Andrews DWK (1992) Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J Bus Econ Stat 10(3):251–270. https://doi.org/10.1080/07350015.1992.10509904

Zoundi Z (2017) CO2 emissions, renewable energy and the environmental Kuznets curve, a panel cointegration approach. Renew Sustain Energy Rev 72(2016):1067–1075. https://doi.org/10.1016/j.rser.2016.10.018

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Ahmad, M., Khattak, S.I. Is Aggregate Domestic Consumption Spending (ADCS) Per Capita Determining CO2 Emissions in South Africa? A New Perspective. Environ Resource Econ 75, 529–552 (2020). https://doi.org/10.1007/s10640-019-00398-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10640-019-00398-9