Abstract

Blockchain has enormous capabilities to transform the traditional business models in countless ways. Banks in India are building collaborative blockchain ecosystems to create an innovative business model and disrupt the traditional one to create further competitive advantages. The purpose of this study is to examine the relationship between blockchain capabilities (BCC), competitive advantages (CA) and organizational performance (OP). Further, to evaluate the mediating role of CA on the relationship between BCC and OP. In this context, scientific research model consisting of a hypothesis has been developed from the existing literature. The proposed model was tested using statistical data collected from Blockchain specialists, blockchain product marketing managers, experts of future and emergent technology and VP/AVP/Chief Manager/Branch head of banks/ financial Analyst/divisional Managers who are involved in planning and deployment of practical blockchain in banking/financial sector. Data was analyzed and tested through AMOS 22.0 and process macro using a sample of 289 responses. Our empirical result indicated that there is a significant positive relationship between BCC, CA and OP. Furthermore, relationship of BCC and OP partially mediated CA. This paper presents originality and contributes towards the body of knowledge on this subject to understand the relationship and mediation role of CA on the relationship between BCC and OP in Indian banking sector.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

The Banking Sector has always been the first mover in regularly exploring, innovating and upgrading technologies to enhance customer experience, eliminate resource intensive processes of their operations. Today, banking industry is exploring the applications of blockchain technology and as a result, it could prove to be the potential game-changer in financial world. Blockchain technology has a great potential to provide secure, collaborative framework and capabilities to address the issues related such as operational risk and administrative costs as it can be made transparent and immutable. Besides enhancing operational efficiency, blockchain technology has the capability to embrace new revenue opportunities and new strategic positioning for future growth.

Blockchain was originally developed as a technical platform for digital cryptocurrency, now Blockchain technology is being posited as the next frontier in banking sector. Blockchain is a distributed ledger held collaboratively that enables decentralized exchange of trusted data through consensus mechanisms and strong data encryption technology without the need for a central authority. Blockchain components like cryptographic hash functions, distributed ledger and different type of consensus algorithm when combined creates a powerful new form of data exchanging, sharing and transferring and capable of eliminating all intermediaries/third party and expensive reconciliation processes. The traceability and ensured immutability of digital transactions recorded in a blockchain helps save resources. The ability to execute smart contracts based on pre-determined conditions and data requirements ensure that the end-to-end traceability process is authentic and effective.

Blockchain provides banks with a platform to reform their organization and service offering required to fit into digitally savvy agile modern society. It also allows tracking of assets/transactions without the need of a centralized trusted authority and creates a secure, tamperproof, transparent, reliable and immutable record of ownership. It also has abilities to solve some of`` the pressing problems like transfer/payment settlement, cross-border payments, insuring deposits & loans, KYC processes and trade finance. According to Accenture, Blockchain technology has a potential to reduce the infrastructure costs of world’s largest investment banks between $8 to $12 billion a year by 2025 (Accenture, 2017). Thus, renovation in existing financial business models to accommodate or replace centralized model with blockchain technology, not only offers an infinite number of applications that may enhance financial offering but also maintains the fundamental existence of banking (Rajnak & Puschmann, 2020).

As IBEF (2021), “The robust Indian banking system consists of 12 PSB (public sector banks), 22 PVS (private sector banks), 44 FB (foreign banks), 43 RRB (regional rural banks), 1484 UCB (urban cooperative banks) and 96,000 RCB (rural cooperative banks) in addition to CCI (cooperative credit institutions)”. Indian banking industry is the backbone of the world’s fastest growing major economy and it has 7.7% contribution in India’s GDP (Singh & Malik, 2018). “Indian Banks' Blockchain Infrastructure Co Pvt Ltd (IBBIC)” is a coalition of India’s fifteen banks which includes ten private sector, four public sector and one foreign bank coming together to form a new entity named to solve a major issues of traditional banking like processing of GST invoices, Letters of Credit (LCs), trade financing and e-way bills (Rebello, 2021). The 15 banks which are the part of this new company are— “RBL Bank, ICICI Bank, HDFC Bank, Kotak Mahindra Bank, Axis Bank, IndusInd Bank, Yes Bank, South Indian Bank, Federal Bank, IDFC First Bank, SBI, Bank of Baroda, Indian Bank, Canara Bank and Standard Chartered” (). To achieve the potential blockchain benefits, collaborative efforts are required among banks to create the necessary network to establish global payments. Blockchain technology is still in its nascent experimental and testing stages of development in India but most of the banks are investigating the use of blockchain opportunities independently.

A bank gains competitive advantage when it performs the activities at a lower cost leveraging disruptive technology platforms for speed, security, immutability, traceability and transparency. With blockchain technology, banks can address industry-wide problems and bottlenecks. A significant question to ponder is if the 15 banks have access to the same platform, then how can blockchain contribute to competitive advantage in banking sector? Once blockchain platforms would be implemented industry-wide the cost and pricing structures will change drastically and there might be more efficient equilibrium. At that point, competitive advantage would not stem from the implementation of blockchain platform using decentralized database rather the differentiator would be with regards to better and faster service experience to customers. For organizations operating in an ever-connected market, absence of blockchain technology may lead to competitive disadvantage over the long term, thus, constantly innovating solutions and choosing the right use cases will be quintessential in order to stay competitive. It is more than likely that Indian banks will utilize the capabilities of blockchain to gain a competitive advantage through modified business model and lead to organizational performance. A lot of success stories were published by academia and blockchain vendors which highlights the capabilities of blockchain enhancing competitive advantage and organizational performance (Vega, 2021; 7 bits technologies (2021); Silva, 2019; McCauley, 2019; Oracle Netsuite, 2019; Ma, 2000). However, the relationship of blockchain capabilities, competitive advantage and organizational performance has not been examined empirically. This study aims to address this research gap.

The study aims to investigate empirically and accumulate scientific knowledge about the relationship of blockchain capabilities, competitive advantage and organizational performance. We used blockchain capabilities as an investigation tool for the study. The following research questions have been investigated in our study.

-

RQ1. Do blockchain capabilities have a relationship with competitive advantage and organizational performance in Indian Banking sector?

-

RQ2. Does competitive advantage play an essential mediating role in the relation between blockchain capabilities and organizational performance?

To address the above questions, we developed a conceptual model to analyze the relationship of blockchain capabilities, competitive advantage and organizational performance. Data was analyzed and tested using structural equation modeling (SEM) techniques on AMOS 22.0, SPSS 26.0 and Hayes’ SPSS process macro to carry out the mediation effect on total of 289 usable responses.

Remaining part of the paper is organized as follows- Sects. 2 and 3 largely focused on literature review, conceptual model and hypotheses development, Sect. 4 discusses research methods, Sects. 5 and 6 presents the data analysis and results, discussion and implications followed by conclusion, limitations and future scope of research.

2 Literature review

2.1 Blockchain capabilities (BCC)

Blockchain has evolved and emerged as transformative technologies which changed the market paradigms (Gumsheimer et al., 2016; Schuetz & Venkatesh, 2020). Blockchain was first conceptualized by Satoshi Nakamoto (2008) in a white paper, since then substantial amount of research has been conducted. The existing literature primarily focus on three aspects of blockchain – characteristic of blockchain (Chang et al, 2020; Feng et al., 2018; Garg et al., 2021), application of blockchain (Maiti et.al., 2021; Garg et.al., 2021; Queiroz & Wamba, 2019), and challenges of blockchain (Harwik & Caton, 2020; Drescher, 2017; Iansiti & Lakhani, 2017) as depicted in Table 1. Interestingly, a set of studies focus on strategic impact of blockchain on the existing business models (Maiti et.al., 2021; Rajnak & Puschmann, 2020; Kshetri, 2018). Though Blockchain is still in embryonic stage but its commercial and industrial application has been validated across industries worldwide namely healthcare and financial sector (Maiti et.al., 2021; Chang et. al, 2020; Grech & Camilleri, 2017; Grewe & Bosch, 2016). In simple words, blockchain is a digital, decentralized, immutable and distributed ledger that record transactions in near real time. As a result, blockchain may develop as a resource capability of a business to streamline its processes, reduce costs, reduce operational risk with tamper-proof, transparent and robust security systems (Akins et al., 2014).

Developing blockchain as a capability may offer several advantages to an organization – (1) Improves efficiency due to fast response to every transaction, (2) Faster transactions based on automated record keeping, (3) Save transaction time and operational cost, (4) Quick settlements and payment without third party involvement, (5) Enhance third party trust with the use of cryptography, and (6) Real time information leads to transparency at both sides (Gupta & Gupta, 2018; Underwood, 2016). Therefore, it is crucial for organizations like banks to develop capabilities that build trust among people and flourish operational excellence (Casino et al., 2019a, 2019b; Kant, 2020; Pilkington, 2016).

Banking sector is the backbone of any economy as it functions with large amount of confidential ledger and balances of many centralized authorities of a country (Libert et al., 2016; Mu et al., 2019). Arguably, deep-rooted complex centralized business models of banking industry particularly in India restricts the rising possibilities of blockchain technology (Pilkington, 2016; Rajnak & Puschmann, 2020). Blockchains provide significant innovation to financial markets which increases efficiency and operational performance with regard to digital payments and settlement (Beck et al., 2016; English & Nezhadian, 2017; Gao et al., 2018; Lundqvist et al., 2017; Min et al., 2016; Papadopoulos, 2015; Yamada et al., 2016). It can facilitate banks to make direct international payments economical and efficient (Guo & Liang, 2016; Isaksen, 2018). Notably, Hassani et al. (2018) highlights that blockchain may create sweet and sour relationship in banking sector that brings opportunities as well as threats. Nonetheless, blockchain is highlighted as an intangible resource to an organization by few researchers (Hitt, 2001; Berney, 1991) in early years and consequently Garg et al. (2021) proposed an instrument to measure blockchain capabilities (BCC) recently. The instrument consists of 26 items categorized into five constructs: “Quality customer services”, “reduced cost”, “efficiency and security”, “secure remittances” and “regulatory compliances”. The list of these sub-constructs, along with their definition and supporting literature, are provided in Table 2.

Thus, with a constant evolution of blockchain from 1.0 to 4.0 (Swan, 2015), banking sector has many reasons to look forward to BCC as a source of creating and sustaining competitive advantage (Grech & Camilleri, 2017).

2.2 Competitive advantage (CA)

Competitive advantage (CA) is achieved by an organization when it outperforms its competitors with a certain set of resources, attributes and strategies (Kant, 2021; Wang, 2014). Resources cover possession of every asset, process, information, skills, methods, knowledge and function that builds an organization (Barney, 1991). Attributes includes basic characteristics like flexibility, innovation, technological advancements etc. to enhance the organizational competency to assess and reconfigure threats into opportunities with timely response to rivals (Barney, 2001). Putting all together, resources and attributes builds organizational capabilities. The organizational capabilities such as blockchain accumulate internal as well as external resources in such a manner that sustains ‘competitiveness’ (Teece, 2007; Weerawardena & Mavondo, 2011) and therefore it acts as a strategic move of an organization to negate threats by its own abilities (Teece & Pisano, 1994). As suggested by Pasquale (2015), blockchain capabilities has huge potential to resolve a variety of threats and function as strategic resource to gain superior performance by sustaining competitive advantage (Kant & Agrawal, 2020).

Owning to strategic advantage there exists a clear consensus in available literature that CA can be attained by three generic strategies namely—cost leadership, differentiation and focus as mentioned by Porter (1980). In a cost leadership strategy, the objective is to become the lowest-cost producer of banking products or services whereas under differentiation strategy, a unique distinctive characteristic in banking products or services from the competitors is created as differentiator and finally in a focus strategy, the bank offerings may focus on a narrow target market segment (Porter, 1980). Interestingly, Cater and Pucko (2005) highlighted that organizations may opt for two parallel strategies at one time instead of one strategy, for example lower price and differentiation in offering may be used simultaneously to fetch better results. Such strategic choices may support banking sector to gain their CA. Further, Arifin and Frmanzah (2015) claimed that successful technology adoption may significantly contribute to CA. While Barney (2001) mentioned that CA of an organization must have few qualities such as value, rarity, non-substitutability etc. To add, Ionescu and Dumitru (2015) argued that organizations need to constantly update their CA by displaying their capacity to change in dynamic business environment. Given the current circumstances, several research studies indicate that due to distinctive features and many advantages of blockchain, it may emerge as potential strategic resource to sustain CA (Kant, 2020; Kant & Agrawal, 2020). Therefore, it would be interesting to validate Blockchain Capabilities as competitive advantage in banking sector. Based on the prior literature, Koufteros (1995), Zhang (1997) and Li et al. (2006) defines the five sub-constructs of “competitive advantage”, “Price/Cost”, “Quality”, “Delivery Dependability”, “Product Innovation” and “Time to Market”. The list of these sub-constructs, along with their definition and supporting literature, are provided in Table 3.

2.3 Organizational performance (OP)

Extant of literature is rich with many definitions of organizational performance (OP) mainly in three dimensions -managerial performance (Mishra & Mohanty, 2014; Nanni et.al, 1992; Eccles, 1991), leadership characteristics (Gabriela, 2020) and organizational effectiveness (Hult et.al., 2008; Venkatraman & Ramanujam, 1986; Ginsberg & Venkatraman, 1985). Traditionally, managerial performance illustrates financial performance of an organization, therefore it is “the narrowest conception of business performance” (Richter et al., 2017, pp.95–96). But with an ever-changing dynamic, OP has evolved as concept that encompasses several other aspects like market reputation, achievement of goals, survival and relationship with competitors representing organizational effectiveness (Richter et al., 2017; Hult et.al., 2008). Interestingly, Gabriela (2020) highlighted leadership characteristics attributing to OP and further established relationship between the two. Notwithstanding, organizational performance is defined as an overall performance of a business measured by tangible and intangible goal accomplishment. Tangible goals are quantifiable targets drawn from market performance and financial performance of an organization resulting in its higher economic value. Few studies have attempted to measure financial performance of an organization using financial returns such as return on investment, return on equity, return on sales etc. (Mishra & Mohanty, 2014; Nanni et al., 1992) and market performance using market-related criteria such as increase in market share, overall competitive position in the marketplace, and so on (Flynn et al, 2010; Stock et al, 2000). Regardless of various definitions and conceptual development on this topic, every organization is careful of their performance and intends to retain its existing market position in most optimal manner. Therefore, in its crystallized form OP primarily reflect how the organization creates value and disseminates that value to its own customers to meet its objective.

3 Conceptual model and hypotheses development

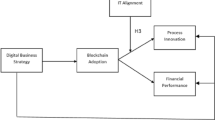

Blockchain has a potential to transform the traditional business models in countless ways. Banks in India are developing collaborative blockchain ecosystems to create an innovative business model and disrupt the traditional one. The conceptual model for this study was built from the synthesis of published research articles, blockchain client success stories and subsequent discussions with experts who are responsible for deploying practical blockchain (7 bits technologies (2021); Silva, 2019; McCauley, 2019; Oracle Netsuite, 2019; Ma, 2000). The conceptual model illustrated in Fig. 1 sheds light on the BCC as source of CA to enhance OP. The model presents (see Fig. 1) the direct relationship of BCC with OP. Second, the model depicts the mediating effect of CA in explaining the relationship between BCC and OP.

Conceptual model and research hypotheses

As part of research, a small preliminary study was conducted to understand the exact nature, dimensions, relationships and items of BCC, CA and OP, we identified experts from the banks and IT Industries as well as academia who were involved in the development and deployment process of practical blockchain in banking sector across India. We invited a focus group consisting of four business specialists from banks, two blockchain experts, two IT professionals and two professors. Based on comprehensive study and synthesis of literature, coupled with analysis of focus group discussion, we defined the dimensions of BCC, CA and OP (see Fig. 1). BCC is conceptualized as a five-dimensional construct namely: “quality customer services”, “reduced cost”, “efficiency and security”, “secure remittances” and “regulatory compliances” (Garg et al., 2021). CA of the banks is evaluated as a five-dimensional construct which are: “price/cost”, “quality”, “delivery dependability”, “product innovation” and “time to market” while OP of the bank will be evaluated through “financial performance” and “market performance” (Koufteros, 1995; Li et al, 2006). Using literature support, the expected relationships among BCC, CA and OP are discussed and hypotheses relating these variables are developed. Subsequently during our pilot study phase, the dimensions and items of BCC, CA and OP were verified and validated using confirmatory factor analysis. According to Churchill (1979), “….it is very important to identify theoretical relationships between any newly proposed construct and other conceptually related, but distinct concepts…”. In the next following section, using literature support we will determine the expected relationship among the BCC, CA and OP for further hypotheses formulation of the study.

The literature on the impact of BCC and OP is recent, most of the literature on BCC in the banking sector focuses on the use of methods and concepts and there is little research on blockchain capabilities and its impact on organizational performance which is mostly inconclusive in literature. Original IT Capabilities with added enhancements can be used as a proxy for measuring the impact of blockchain capabilities on organizational performance in banking sector. The relationship between IT capabilities and organizational performance is widely taken by number of researchers such as Bhardwaj et al. (2000), Braojos et al (2019), Cheng et al. (2020), Gil-Padilla (2008) and Rehman et al (2020). According to Murray et al. (2021), blockchain technology directly reduced the transaction cost and directly mitigated the agency cost that stem from contracting with agents inside the firm. A number of available researches reflect a strong link between business capabilities and financial performance, (profits, returns, etc.) indicators such an approach is evident in the studies of Fahy et al. (2000), Tsai and Shih (2004), and Vorhies and Morgan (2003). With BCC, companies can save a substantial cost by eliminating the several third-party intermediaries (7 bits technologies, 2021). According to McKinsey, blockchain technology is expected to reduce banks operational costs by USD 13.5–15 billion annually and cost of risk by USD 1.1–1.6 billion annually. Furthermore, transaction efficiency improvement ensures a smoother flow of overall trade financing channels, which greatly increase the income of the overall trade chain.

Hypothesis 1

There is a significant relationship of blockchain capabilities on organizational performance in Indian banking sector.

Resource base view (RBV) of a firm was initially introduced by Barney (1991) as unique resources where company must be competitive in the world of competition. These strategic resources must consist of characteristics of being valuable, rare, imperfectly imitable and strategically irreplaceable (Barney & Arikan, 2001; Guimarães, et al., 2017). Blockchain offers itself with tremendous potential as a significant intangible resource for the organizations applying it strategically—with the underpinnings provided by the arguments of Hitt et al., (2001a, 2001b) highlighting that the contributions of intangible resources are significantly greater than tangible resources, and by Barney (1991) positing that intangible and internal resources are more useful than tangible and external resources – for attaining and sustaining competitive advantage. According to Harrington (2019) “……Over the last few decades the cost of data has gone way down, and now with blockchains we have a technology platform that allows us to very easily share and operate on that shared data. The competitive advantage shifts from having the data to how you use the data….” (McCauley, 2019). The banks develop blockchain products for its own use that can lead to competitive advantages. With blockchain technology & banking software solutions, many financial institutions have been in a position to improve their operations and become more competitive in the banking industry. According to Alara Basul (2021), it is important to reimagine the role of technology within the banking and financial sector and it’s imperative for businesses to understand how to utilize new platforms and understand the impacts of new regulations in order to stay competitive and compliant in a crowded market.

Hypothesis 2

There is a significant relationship of blockchain capabilities on competitive advantage in Indian banking sector.

Firms attain CA by offering better services and create customer value to attain differentiation benefits are likely to have increased market share and profitability (Barney, 1991; Prahalad & Hamel, 1997). CA refers to capability that allows organization to produce goods or services when compared to its competitors in term of lower prices, higher quality, higher dependability and shorter delivery time. These capabilities will, in turn, enhance the organization’s overall performance c(Mentzer et al., 2000). An organization can charge premium prices by offering high-quality products and consequently increase its profit margin on sales and ROI. An organization having optimal time to market and rapidly innovate captures a dominant share of the market and sales volume (Li et al, 2006). Therefore, a positive relationship between competitive advantage and organizational performance can be proposed. CA can contribute to superior economic performance, customer loyalty and satisfaction and interpersonal effectiveness. Brands with higher consumer loyalty face less competitive switching in their target segments thereby increasing sales and profitability (Moran, 1981). Competitive advantage involves from the creation of superior competencies that are leveraged to create customer value and achieve cost and/or differentiation advantages, resulting in market share and profitability performance (Barney, 1991; Coyne, 1986; Day & Wensley, 1988; Prahalad & Hamel, 1997).

Hypothesis 3

There is a significant relationship of competitive advantage on organizational performance in Indian banking sector.

There are very few studies who are mainly confined on how Blockchain capability can generate more profit and sales revenue by achieving CA (Pradipto et al, 2019; Sheel & Nath, 2019; 7 bits technology (2021); Silva, 2019) but considering this mediating role of CA we do not gather empirical evidence from the exiting literature which adequately demonstrates that blockchain capabilities may improve organizational performance through CA. Accordingly, it was finally hypothesized that:

Hypothesis 4

Competitive advantage has a mediating role on the relationship between blockchain capabilities and organizational performance in Indian banking sector.

A conceptual model shown in Fig. 1 was used to illustrate that BCC have a positive relationship with OP both directly and indirectly through CA.

4 Research methods

4.1 Item generation

The study was designed to investigate the relationship between blockchain capabilities (BCC), competitive advantage (CA) and organizational performance (OP). Therefore, conceptual research model covers three areas: BCC, CA and OP. Instruments to measure BCC, CA and OP were adapted from previous studies with minor modifications.

BCC dimensions (“Quality customer products/services”, “Reduced cost”, “Efficiency and security”, “Secure remittances”, “Regulatory compliance”) are measured using 26-item scale adapted from Garg et al. (2021). CA dimensions (“Price/Cost”, “Quality”, “Delivery Dependability”, “Product Innovation” and “Time to Market”) are measured with 16—items adapted from (Koufteros, 1995; Li et al., 2006) and OP dimensions (“financial performance” and “Market performance”) are measured with 6 items adapted from (Koufteros et al., 1997; Li et al, 2006). The dimensions and items used for study were adapted from the previously published studies and were found to be empirically reliable and valid. Therefore, there was no need to test the instrument again during the pilot study. Still, it should be revalidated with subject matter experts to ensure the relevancy of questions with respect to BCC, CA and OP in the banking sector. Hence, 26 items of BCC, 16 items for CA and 6 items of OP were subjected to a second-order CFA to examine the well-fitting measurement model.

4.2 Instrument development and data collection

To examine the relationship between BCC, CA and OP in the Indian banking sector, the authors developed a closed ended initial draft questionnaire based on discussion and reflection of reviews of associated literature (Garg et al., 2021; Koufteros, 1995; Li et al., 2006). To receive the inputs on accuracy and modifications on the draft questionnaire, we invited seven knowledgeable individuals (i.e. five academicians, 1 blockchain specialist and 1 head of bank) for review. The experts were asked to assess the questionnaire for its comprehensibility and appropriateness of the items. Based on the comments and feedback received from experts, the wording of questions was modified slightly as per context of this study (but not the content and meaning). As a result, 4 questions were modified, and version 1 of the questionnaire was developed for pilot testing first. Post the experts review, initial small pilot tests were conducted where head of 10 banks and 11 blockchain specialist were asked to complete the survey questions – to avoid repetition, ambiguous phrasing, grammatical errors and sequencing, to draw respondents’ sense. Based on the comments and feedback of the experts, the questionnaire was refined during pilot stage which experts opined are inappropriate with respect to banking sector. Another pilot study was conducted after the changes have been made in the questionnaire. Head of 50 banks and blockchain specialists were invited complete the questionnaire and made a very few adjustments.

The questionnaire was refined multiple times based on the feedback received during preceding pilot studies, and final version of questionnaire was developed which contained 48 items (questions) under 4 broad categories. Part one consisted of questions related to demographic profile of respondents, questions under the second category related to BCC, Part three consisted of questions related to CA and part four was mainly concerned to OP. A five-point Likert scale was used to measure respondents' agreement with various statements. Items of BCC, CA and OP were examined on a 5-point Likert scale on a continuum from strongly disagree (1) to strongly agree (5). Details of scale items along with sources of these construct are indicated in the Appendix A.

4.3 Data gathering

The respondent of the present study were actual business users who were using or implementing blockchain enabled application in banking sector. Around 63 banks (21 Private Sector Banks, 12 public sector banks, 30 foreign banks), fintechs, blockchain startups and IT companies were contacted telephonically to ascertain whether or not they are engaged in using/implementing/planning and deployment of blockchain in banking/financial sector institution so that the right person can be contacted to ensure homogeneity of the samples. Following organization's response Blockchain experts and consultants, blockchain product marketing managers, experts of future and emergent technology, and VP/AVP/Chief Manager/Branch head of banks were contacted to take up the survey.

Questionnaires were sent to the select individuals and their responses were collected through mailers sent to individuals and administering the questionnaire through Google forms. For this study, questionnaires were sent to 600 respondents. Initially 165 respondents responded (about 27.5%), the follow up mail was sent to respondents for improvement of response rate. The follow mail repeated the purpose of study, elaborated the questionnaires and also assured the respondents that they will remain unidentified and only the data will be utilized. After the first follow up, 155 more respondents replied taking the response rate to 53.33%. Out of 320 responses, we found that 21 questionnaires have missing or incomplete answers and no engage response. The analysis of data also found that 20 respondents had left certain questions unanswered. These respondents were contacted telephonically and explained about the research purpose. 10 respondents responded. While trying to evaluate non response bias, follow-up calls were made to respondents who were selected from the sample of non-responders (N = 20; around 4% of the non-respondents) to find out why they didn't take part in the overview. The reason for not completing the survey by respondents was that they didn't have time to complete the survey. Therefore 31 questionnaires were excluded during the analysis process and 289 valid samples were used for final analysis. Data collection activities were carried out from June – Nov 2021.

4.4 Demographic profile

Table 4 summarizes the details of the demographic profiles of respondents. There were a total of 289 respondents who participated in survey with approximately 59 female and 230 male respondents. In context to the age, 49.83% of respondents were between the age of 25–35, 41.52% of respondents were between the age of 35–50 and the remaining 8.65% respondents were above age of 51. The survey revealed that 26.30% of the respondents were VP/AVP/DVP/Chief Manager/Branch head of banks/financial Analyst/divisional Managers, 49% respondents were Blockchain specialist/consultants, 13.84% respondents were blockchain marketing/product managers.

4.5 Data analysis

The second order construct was established for the study to confirm that conceptual model used in the study loads into numbers of dimensions/sub-constructs (see Fig. 1). All three Construct variables (BCC, CA and OP) are multidimensional second-order constructs. All second-order constructs were explained by its first-order constructs. First-order constructs were measured using reflective measured items. Hence SEM was suitable for the study. SPSS 24.0 was used for analyzing the descriptive statistics and SEM in AMOS 22.0 was further used to examine and test the proposed hypothesis.

5 Data analysis and results

Structural equation modeling (SEM) is multivariate statistical technique which involves two models namely ‘measurement model’ and ‘structural equation model’ (Blunch, 2008). The measurement model measures the relationships between constructs (latent variables) and respective measuring items (observed variables) whereas structural model describes interrelationships among latent constructs involved in the study (Hair et al., 2010; Gefen et al, 2000). Confirmatory factor analysis is a part of measurement model which test the relationships between construct and its observed variables whereas structural model verifies the relationship among constructs (Wright, 1918, 1920, 1923).

5.1 Evaluation of first-order measurement model

In this study, the theory posits that the BCC construct consists of five underlying sub-constructs, CA construct consists of five underlying constructs, OP constructs consists of 2 underlying sub-constructs wherein each sub-construct is measured by certain items.

According to Fornell and Larcker (1981), before testing the significance of the relationships among constructs, it is necessary to ensure the validity and reliability of measurement model. The measurement model must have a significant level of validity and reliability. The validation procedure for measurement model was carried out through confirmatory factor analysis (CFA). Reliability estimates “the stability and the consistency of the measuring instrument whereas validity refers the accuracy of an instrument….” (Sekaran & Bougie, 2010).

The construct reliability can be determined by using Cronbach alpha and composite reliability. The internal reliability of a construct is said to be achieved when the Cronbach’s Alpha value is 0.7 or higher (Nunnally & Beinstein, 1994). Composite reliability is a measure of internal consistency, unlike Cronbach's Alpha, it is more concern on individual reliability referring to different outer loadings of the indicator variables (Hair et al., 2010). The cut off for composite reliability score between 0.6 and 0.7 is a good indicator of construct reliability (Henseler & Sarstedt, 2013).

A confirmatory factor analysis (CFA) using AMOS 22.0 was used to compute the factor loading for every measuring items and correlation between constructs. The result of first-order measurement model using CFA is shown in Table 5. Using factor loading, we computed the average variance extracted (AVE) and composite reliability (CR). AVE determine the convergent validity of the construct whereas CR reflects the extend of reliability of the construct. Two items were deleted because of low factor loading because it was less than the threshold value 0.5 (see Appendix A, items marked with * deleted from the final measurement). The cronbach’s alpha of all first order measuring items value ranged from 0.701 to 0.918, composite reliability were ranged from 0.715 to 0.919 (more than 0.5 threshold). Further, the AVE value was ranged from 0.561 to 0.736 (more than 0.5 threshold). The reliability and convergent validity were established. From Table 6, we can see that discriminate validity of the first order reflective construct validity was assessed by two criteria: the Fornell–Larcker criteria and the Heterotrait-Monotrait (HTMT) criteria. As per Fornell-Larcker criteria, the results show that square root of AVE is greater than the correlation between other latent constructs. Moreover, the HTMT criteria confirmed that all HTMT values are lower than the threshold of 0.90 (Hair et al., 2017) concluding the discriminant validity of the constructs.

Finally, we tested the model for Common Method Bias (Podsakoffet al., 2003) using Herman’s single factor test. In this test, EFA is conducted on all the items in which all the items are loaded onto one common factor and if the total variance for a single factor is less than 50%, it suggests that CMB does not affect the data. In our study factors, 22.27% of the variance is contributed by first factor which clearly indicates that there is no effect of common method bias on validity of research. From the results showed in Tables 5 and 6, we can conclude that first-order measurement model showed adequate reliability, convergent and discriminant validity.

5.2 Evaluation of the second-order measurement model

Second-order models are potentially applicable when (a) the lower-order factors are substantially correlated with each other, and (b) there is a higher-order factor that is hypothesized to account for the relationship among the lower order factors. The second-order BCC general factor that accounts for the commonality among lower order factors representing each of the five domains: QCS (“Quality customer products/services”), RC (“Reduced cost”), ES (“Efficiency and security”), SR (“Secure remittances”), RC (“Regulatory compliance”). Similarly, CA represented by 5 domains namely PC (“Price/cost”), QL (“Quality”), DD (“Delivery dependability”), PI (“Product innovation”), TM (“Time to market”) and finally OP is represented by 2 domains: FP (“financial performance”) and MP (“Market performance”). The reliability and validity of the second-order model can be assessed like first-order model.

According to Fornell and Larcker (1981), if AVE is less than 0.5, but composite reliability is higher than 0.7, the convergent validity of the construct is still adequate. In our analysis, the construct BCC and CA has an AVE is less than 0.5 but composite reliability is higher than 0.7, we can state that convergent validity is established. The results in Table 7 confirmed the high reliability and validity of second-order measurement in terms of convergent and discriminant validity. Therefore, we concluded that the second-order measurement model is internally consistent and reliable as suggested by Fornell and Larcker (1981).

We tested the discriminant validity for the second-order measurement model. Table 8 shows that the entire diagonal values square root of each construct's AVE) exceed the squared inter-construct correlations. Therefore, we conclude that the first-order construct can be explained by the second-order construct.

After the validity and reliability test of measurement model, the reported indices for the current study on the first-order measurement model and the second-order measurement model are shown in Table 9. CFA results indicated that the resulting measurement model (first-order and second-order) with all constructs have acceptable goodness-of fit indices showed as: CFI was 0.952/0.941; GFI was 0.842/0.825; NFI was 0.852/0.837; TLI was 0.946/0.938 and RMSEA was 0.037/0.040 (see Table 9). According to Geffen (2000), GFI and NFI score of measurement model could not fall within the recommended criteria but it was closer to threshold value, thus representing an acceptable model fit. We can conclude that all study constructs are well retained for the satisfactory loadings and acceptable model fit so we can proceed for estimating structural model using SEM.

5.3 Estimation of structural model

Figure 2 depicts the structural model which is almost a replica of our proposed conceptual model shown in Fig. 1.

Structural model

There are three constructs in the model: blockchain capabilities (BCC), Competitive Advantage (CA) and organizational performance (OP). BCC is regarded as independent variables whereas CA and OP are regarded as dependent variables. Table 10 displays the Fitness indices of full structural model. The score of X2/DF was 1.467 which is below 3 as per recommended value, CFI was 0.941, GFI was 0.825, NFI was 0.837, and TLI was 0.938 and RMSEA was 0.040. According to Geffen (2000), GFI and NFI score of measurement model could not fall within the recommended criteria but it was closer to threshold value, thus representing an acceptable model fit. Considering all the fitness indices into account and statistical significance of the structural model it can be concluded that model is fit for the structure. This will enable us to examine the hypothesis described in our model.

As reported in Table 11, finding revealed that there is a significant and positive relationship between BCC and OP, shows that hypotheses 1 is supported (β = 0.133; p < 0.05). Findings also indicates that there is a significant and positive relationship between BCC and CA (β = 0.239; p < 0.001) thus supported H2. Results also shows that there is a significant and positive relationship between CA and OP (β = 0.257; p < 0.05), hence H3 is supported for the study. All relationships are consistent and significant as p-value is less than 0.05 and in the anticipated direction.

5.4 Estimation of mediation effect

To investigate the mediated relationship of CA between BCC and OP, we used SPSS Process Macro written by Hayes & Little (2018). For our hypotheses related to hypothesis 4, we applied model 4 to conduct a simple mediation analysis. Table 12 provides the result of mediation analysis dependent variable (OP) and independent variable (BCC) via mediating effect of CA. As we can observe in Table 12, a significant direct effect of BCC on OP (effect = 0.2056; t = 3.3205; p < 0.1) and indirect significant effect of BCC on OP via CA (effect = 0.0546; 95%CI [0.0139, 0.2751]). Therefore, based on 95% confidence interval, our analysis reveals that CA partially mediating the relationship between BCC and OP.

6 Discussion and implications

Blockchain technologies have the potential to disrupt current ways of working for the banking and allied sectors. Banks where blockchain is adopted in an agile manner at an early stage stand to benefit the most from the ones who are late adopters. Therefore, it is advisable to the leadership to initiate groundwork on the technology adoption and the change driven mindset to drive early success.

The objective of this research is to explore the unknown and unlock new possibilities on the relationship between BCC, CA and OP. Empirically, findings of the research have established that Blockchain capabilities leads to a sustainable competitive advantage for the banking sector and results in better organizational performance which is consistent with (7 bits technologies, 2021; Silva, 2019; McCauley, 2019, Oracle Netsuite, 2019, Ma, 2000) postulations. The quintessential findings of our study are that CA has a partial mediation role between BCC and OP.

The current study indicates that banks have multiple opportunities to redefine their business models and integrate blockchain-enabled business processes to gain further competitive advantage. Early adopters of blockchain technology may gain a larger market share and absence of blockchain technology will be a competitive disadvantage in the long term. In order to stay competitive, banks must have to constantly innovate and choose the right use cases e.g. Anti-money laundering (AML), Know your consumer (KYC), Clearing & settlement, trade financing, cross country payments, Identity Management, Data Management & Data Protection in Indian Banking Sector.

The real benefits of blockchain would come when banks in India will partner with other competitive banks, Technology partners, Fintech and regulators which, in turn, bring benefits to consumers and the financial system. The results of this study lead to several important implications.

6.1 Theoretical implications

The present study contributes to the blockchain capabilities literature in numerous ways. The first theoretical contribution of the empirical research is to reinforce the finding of self-developed blockchain capabilities scale Garg et al. (2021) by testing instrument in context to Indian banking sector. The second contribution is to build the conceptual model and confirm the relationship among BCC, CA and OP. However, to our knowledge, no study has investigated the relationship empirically in context to Indian banking sector. Furthermore, the present study contributes to the body of knowledge and paves way for future research on block chain capabilities in context to Indian banking sector.

6.2 Managerial implications

Findings of the study shed light on the positive relationship between BCC, CA and OP. The findings are valuable for banks who are facing several roadblocks in their journey to adapt blockchain technology due to not fully realizing the potential benefits in terms of speeding up and simplifying cross-border payments, trade financing, improving online identity management and in loyalty and rewards. The findings of this study are also valuable for those banks that have already adopted or piloted blockchain technology but are still looking for further improvement areas where enhanced adoption of smart technologies can improve the business model to unlock sustainable gains, efficiency gains, savings and long-term competitive advantage.

Our paper offers two main implications for managers. First, it proposes blockchain initiatives that enable banks to a new business model which will offer better security, traceability, savings and long-term competitive advantage. Second, for effective management of the block chain-related projects, managers must have clarity about why blockchain is important, what would be business implications of blockchain, where it is important, how blockchain provides transformative benefits. In addition, the managers should be clear about their requirement and open to continuous new learning and upskilling their knowledge.

6.3 Conclusion, limitations and future scope of research

Very few studies have attempted to empirically validate the relationship between BCC, CA and OP in the Indian banking sector. This study presents the empirical evidence regarding the direct relationship between BCC and OP partially mediated by CA.

This study has some limitations and opportunities for future research.

-

This study provides empirical evidence from the sample that consists of respondents from the representatives of the Banks, fintech and IT companies which are operating in India. This may affect the results and may not be the basis for a generalization and limit to generalization in other industries also.

-

The maturity of blockchain technology is still in its nascent stage of development and adoption in India and therefore new dimensions and research items can be developed for studying the blockchain capabilities in the banking sector.

However, these limitations have paved the way for future research. To generalize the finding of this study, the research model can be extending to other countries.

References

Accenture(2017), Blockchain Technology Could Reduce Investment Banks’ Infrastructure Costs by 30 Percent, According to Accenture Report, https://newsroom.accenture.com/news/blockchain-technology-could-reduce-investment-banks-infrastructure-costs-by-30-percent-according-to-accenture-report.htm#:~:text=17%2C%202017%20%E2%80%93%20Blockchain%20technology%20could,is%20part%20of%20Aon%20Hewitt

Accenture (2018). Building the future-ready bank. Accessed on 16th June 2019- https://www.accenture.com/gb-en/_acnmedia/PDF-78/Accenture-Banking-Technology-Vision-2018.pdf.

Akins, B. W., Chapman, J. L., & Gordon, J. M. (2014). A whole new world: Income tax considerations of the Bitcoin economy. Pitt Tax Review, 12, 25.

Alara basul (2021). The future of competitive advantage in banking and payments, https://www.bobsguide.com/articles/the-future-of-competitive-advantage-in-banking-and-payments/.

Alm, J., Lindblad, J., Meddeb, J., Nord, P., Söderberg, K., & Wall, J. (2019). Toward a framework for assessing meaningful differences between blockchain platforms. https://odr.chalmers.se/server/api/core/bitstreams/69c25640-a748-432e-aba4-fac4ac664c47/content.

Arifin, Z., & Frmanzah,. (2015). The effect of dynamic capability to technology adoption and its determinant factors for improving firm’s performance; toward a conceptual model. Procedia-Social and Behavioral Sciences, 207, 786–796.

Ashish, M. Shaji, (2020). Significance of Blockchain in Banking Sector, https://enterslice.com/learning/significance-of-blockchain-in-banking-sector/.

Axios (2018). Corporate America’s blockchain and bitcoin fever is over. (Accessed January 2019) https://www.axios.com/corporate-america-blockchain-bitcoin-fervor-overfb13bc5c-81fd-4c12-8a7b-07ad107817ca.html.

Banks Editorial Team (2018). How Blockchain Benefits Banks. (Accessed on 5th Nov, 2021)- https://www.banks.com/articles/cryptocurrency/blockchain-benefits banks/.

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management Science, 17(1), 99–120.

Barney, J. B., & Arikan, A. M. (2001). The resource-based view: origins and implications. The Blackwell Handbook of Strategic Management. https://doi.org/10.1177/014920639101700107

Beck, T., Chen, T., Lin, C., & Song, F. M. (2016). Financial innovation: The bright and the dark sides. Journal of Banking & Finance, 72, 28–51.

Bits technologies (2021). How can blockchain help you gain a competitive advantage, https://www.sevenbits.in/post/how-can-blockchain-help-you-gain-a-competitive-advantage.

Blunch, N. J. (2008). Classical test theory. In C. A. Thousand Oaks (Ed.), Introduction to Structural Equation Modeling Using SPSS and AMOS (pp. 36–41). Sage.

Braojos, J., Benitez, J., & Llorens, J. (2019). How do social commerce-IT capabilities influence firm performance? Theory and empirical evidence. Information & Management, 56(2), 155–171.

Casino, F., Dasaklis, T. K., & Patsakis, C. (2019b). A systematic literature review of blockchain-based applications: Current status, classification and open issues. Telematics and Informatics, 36, 55–81.

Casino, F., Kanakaris, V., Dasaklis, T. K., Moschuris, S., & Rachaniotis, N. P. (2019a). Modeling food supply chain traceability based on blockchain technology. Ifac-Papersonline, 52(13), 2728–2733.

Cater, T., & Pucko, D. (2005). How competitive advantage influences firm performance: The case of Slovenian firms. Economic and Business Review for Central and South-Eastern Europe, 7(2), 119.

Chang, V., Baudier, P., Zhang, H., Xu, Q., Zhang, J., & Arami, M. (2020). How Blockchain can impact financial services–The overview, challenges and recommendations from expert interviewees. Technological Forecasting and Social Change, 158, 120166.

Chege, S. M., Wang, D., & Suntu, S. L. (2020). Impact of information technology innovation on firm performance in Kenya. Information Technology for Development, 26(2), 316–345.

Churchill, G. A., Jr. (1979). A paradigm for developing better measures of marketing constructs. Journal of Marketing Research, 16(1), 64–73.

Clark, K. B., & Fujimoto, T. (1991). Heavyweight product managers. McKinsey Quarterly, 1, 42–60.

Consultancy.uk (2016). The benefits and use cases for blockchain technology in banking. (Accessed on 2nd June 2019)- https://www.consultancy.uk/news/12801/the-benefits-and-use-cases-for-blockchain-technology-in-banking.

Coyne, K. P. (1986). Sustainable competitive advantage—What it is, what it isn’t. Business Horizons, 29(1), 54–61.

Coyne, J. G., & McMickle, P. L. (2017). Can blockchains serve an accounting purpose? Journal of Emerging Technologies in Accounting, 14(2), 101–111.

Davidson, S., De Filippi, P., & Potts, J. (2016). Economics of blockchain. Available at SSRN 2744751.

Day, G. S., & Wensley, R. (1988). Assessing advantage: A framework for diagnosing competitive superiority. Journal of Marketing, 52(2), 1–20.

Drescher, D. (2017). Planning the Blockchain. Blockchain Basics (pp. 57–62). Berkeley, CA: A press.

Dwivedi, Y. K., Wastell, D., Laumer, S., Henriksen, H. Z., Myers, M. D., Bunker, D., & Srivastava, S. C. (2015). Research on information systems failures and successes: Status update and future directions. Information Systems Frontiers, 17(1), 143–157.

Eccles, R. G. (1991). The performance measurement manifesto. Harvard Business Review, 69(1), 131–137.

English, S. M., & Nezhadian, E. (2017, April). Conditions of full disclosure: The blockchain remuneration model. In 2017 IEEE European Symposium on Security and Privacy Workshops (EuroS&PW) (pp. 64–67). IEEE.

Fahy, J. (2000). The resource-based view of the firm: some stumbling-blocks on the road to understanding sustainable competitive advantage. Journal of European Industrial Training., 24, 94–104.

Feng, L., Zhang, H., Chen, Y., & Lou, L. (2018). Scalable dynamic multi-agent practical byzantine fault-tolerant consensus in permissioned blockchain. Applied Sciences, 8(10), 1919.

Flynn, B. B., Huo, B., & Zhao, X. (2010). The impact of supply chain integration on performance: A contingency and configuration approach. Journal of Operations Management, 28(1), 58–71.

Forester (2018). The blockchain revolution will have to wait a little longer. (Accessed December 2018) https://go.forrester.com/blogs/predictions-2018-the-blockchainrevolution-will-have-to-wait-a-little-longer/.

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50.

Gao, F., Zhu, L., Shen, M., Sharif, K., Wan, Z., & Ren, K. (2018). A blockchain-based privacy-preserving payment mechanism for vehicle-to-grid networks. IEEE Network, 32(6), 184–192.

Garg, P., Gupta, B., Chauhan, A. K., Sivarajah, U., Gupta, S., & Modgil, S. (2021). Measuring the perceived benefits of implementing blockchain technology in the banking sector. Technological Forecasting and Social Change, 163, 120407.

Gefen, D., Straub, D., & Boudreau, M. C. (2000). Structural equation modeling and regression: Guidelines for research practice. Communications of the Association for Information Systems, 4(1), 7.

Gil-Padilla, A. M., & Espino-Rodríguez, T. F. (2008). Strategic value and resources and capabilities of the information systems area and their impact on organizational performance in the hotel sector. Tourism Review, 63, 21–47.

Ginsberg, A., & Venkatraman, N. (1985). Contingency perspectives of organizational strategy: A critical review of the empirical research. Academy of Management Review, 10(3), 421–434.

Glaser, F., & Bezzenberger, L. (2015). Beyond cryptocurrencies-a taxonomy of decentralized consensus systems. In 23rd European conference on information systems (ECIS), Münster, Germany.

Gray, J. L., & Harvey, T. W. (1992). Quality value banking: Effective management systems that increase earnings, lower costs, and provide competitive customer service. Wiley.

Grech, A., & Camilleri, A. F. (2017). Blockchain in education. Publications Office of the European Union.

Grewe, I., Bosch, R. (2016). Can the financial services industry master cryptofinance? BearingPoint Institute.

Guimarães, J. C. F. D., Severo, E. A., & Vasconcelos, C. R. M. D. (2017). Sustainable competitive advantage: A survey of companies in Southern Brazil. BBR. Brazilian Business Review, 14, 352–367.

Gumsheimer T, Felden F, Schmid C (2016) Recasting IT for the digital age, BCG perspectives, The Boston Consulting Group.

Guo, Ye., & Liang, C. (2016). Blockchain application and outlook in the banking industry. Financial Innovation, 2(1), 1–12.

Gupta, V. (2017). The promise of blockchain is a world without middlemen. Harvard Business Review Digital Articles, 6, 2–5.

Gupta, A., & Gupta, S. (2018). Blockchain technology application in Indian Banking Sector. Delhi Business Review, 19(2), 75–84.

Hair, J. F., Jr., Matthews, L. M., Matthews, R. L., & Sarstedt, M. (2017). PLS-SEM or CB-SEM: Updated guidelines on which method to use. International Journal of Multivariate Data Analysis, 1(2), 107–123.

Hair, Jr, J. F. (2010), Multivariate Data Analysis Joseph F. Hair Jr. William C. Black Barry J. Babin Rolph E. Anderson Seventh Edition.

Hall, R. (1993). A framework linking intangible resources and capabiliites to sustainable competitive advantage. Strategic Management Journal, 14(8), 607–618.

Handfield, R. B., & Pannesi, R. T. (1995). Antecedents of leadtime competitiveness in make-to-order manufacturing firms. The International Journal of Production Research, 33(2), 511–537.

Harigunani, P. (2017). Blockchain for Banks: benefits and Implications. Accessed on 15th July 2021- https://www.ciol.com/8-benefits-blockchain-banks-future-implications/.

Harrington, K. (2019). Distributed autonomous learning framework. Disruptive Technologies in Information Sciences, 11013, 110130M.

Harwick, C., & Caton, J. (2022). What’s holding back blockchain finance? On the possibility of decentralized autonomous finance. The Quarterly Review of Economics and Finance, 84, 420–429.

Hassani, H., Huang, X., & Silva, E. (2018). Banking with blockchain-ed big data. Journal of Management Analytics, 5(4), 256–275.

Hawlitschek, F., Notheisen, B., & Teubner, T. (2018). The limits of trust-free systems: A literature review on blockchain technology and trust in the sharing economy. Electronic Commerce Research and Applications, 29, 50–63.

Henseler, J., & Sarstedt, M. (2013). Goodness-of-fit indices for partial least squares path modeling. Computational Statistics, 28(2), 565–580.

Hitt, M. A., Bierman, L., Shimizu, K., & Kochhar, R. (2001a). Direct and moderating effects of human capital on strategy and performance in professional service firms: A resource-based perspective. Academy of Management Journal, 44(1), 13–28.

Hitt, M. A., Ireland, R. D., Camp, S. M., & Sexton, D. L. (2001b). Strategic entrepreneurship: Entrepreneurial strategies for wealth creation. Strategic Management Journal, 22(6/7), 479–492.

Hooper Matthew. (2018). Top five blockchain benefits transforming your industry, https://www.ibm.com/blogs/blockchain/2018/02/top-five-blockchain-benefits-transforming-your-industry/.

Hughes, L., Dwivedi, Y. K., Misra, S. K., Rana, N. P., Raghavan, V., & Akella, V. (2019). Blockchain research, practice and policy: Applications, benefits, limitations, emerging research themes and research agenda. International Journal of Information Management, 49, 114–129.

Hult, G. T. M., Ketchen, D. J., Griffith, D. A., Chabowski, B. R., Hamman, M. K., Dykes, B. J., & Cavusgil, S. T. (2008). An assessment of the measurement of performance in international business research. Journal of International Business Studies, 39(6), 1064–1080.

IBEF(2021), “Indian Banking Industry Analysis”, https://www.ibef.org/industry/banking-presentation.

Iansiti, M., & Lakhani, K. R. (2017). The truth about blockchain. Harvard Business Review, 95(1), 118–127.

Ionescu, A., & Dumitru, N. R. (2015). The role of innovation in creating the company’s competitive advantage. Ecoforum Journal, 4(1), 14.

Isaksen, M. (2018). Blockchain: The Future of Cross Border Payments (Master's thesis, University of Stavanger, Norway).

Iyer, S. (2016). The benefits of blockchain across industries. (Accessed on 2nd July 2019)- https://blogs.oracle.com/profit/the-benefits-of-blockchain-across-industries.

Jaikrishnan, G. (2021a). IBBIC way for block: Paving chain adoption by Indian banks, https://www.grantthornton.in/insights/blogs/ibbic-paving-way-for-blockchain-adoption-by-indian-banks/.

Kant, N. (2020). Blockchain: a resource of competitive advantage in open and distance learning system. Blockchain technology applications in education (pp. 127–152). Hershey: IGI Global.

Kant, N., & Agrawal, N. (2020). Developing a measure of climate strategy proactivity displayed to attain competitive advantage. Competitiveness Review—an International Business Journal, 31, 832–862.

Kessler, E. H., & Chakrabarti, A. K. (1996). Innovation speed: A conceptual model of context, antecedents, and outcomes. Academy of Management Review, 21(4), 1143–1191.

Kloppmann, M. (2017). Digital process automation and blockchain in financial services. (Accessed on 1st Feb, 2019)- https://www.ibm.com/blogs/blockchain/2017/08/digital-process-automation-blockchain-financial-services/.

Koufteros, X. A. (1995). Time-based competition: developing a nomological network of constructs and instrument development. The University of Toledo.

Krause E.G., Velamuri V.K., .Burghardt T., Nack D., Schmidt M. and Treder T.M. (2018). Blockchain technology and the financial services market. (Accessed on 11th Nov, 2021)- https://www.infosys.com/consulting/insights/Documents/blockchain-technology.pdf.

Kshetri, N. (2018). 1 Blockchain’s roles in meeting key supply chain management objectives. International Journal of Information Management, 39, 80–89.

Levine, M. (2017). Cargo blockchains and Deutsche bank. Retrieved from https://www.bloomberg.com/view/articles/2017-03-06/cargo-blockchains-and-deutsche-bank.

Li, S., Ragu-Nathan, B., Ragu-Nathan, T. S., & Rao, S. S. (2006). The impact of supply chain management practices on competitive advantage and organizational performance. Omega, 34(2), 107–124.

Libert, B., Beck, M., Wind, J. (2016) How blockchain technology will disrupt fnancial services frms. http://knowledge.wharton.upenn.edu/article/blockchain-technology-will-disrupt-fnancial-services/firms.

Liebenau, J.M., Elaluf-Calderwood, S.M., Bonina, C.M. (2014). Modularity and network integration: emergent business models in banking. In: HICSS 2014 proceedings. http://ieeexplore.ieee.org/document/6758750.

Limechain.tech, blockchain in Banking. https://limechain.tech/blockchain-use-cases/banking/.

Lundqvist, T., De Blanche, A., & Andersson, H. R. H. (2017). Thing-to-thing electricity micro payments using blockchain technology. In 2017 Global Internet of Things Summit (GIoTS) (pp. 1–6). IEEE.

Ma, H. (2000). Competitive advantage and firm performance. Competitiveness Review: An International Business Journal.

Maiti, M., Kotliarov, I., & Lipatnikov, V. (2021). A future triple entry accounting framework using blockchain technology. Blockchain Research and Applications, 2, 100037.

Matteson, A. (2017). Benefits and use cases for blockchain in banking. (Accessed on 2nd June 2021)- https://www.datasciencecentral.com/profiles/blogs/the-benefits-and-use-cases-for-blockchain-technology-in-banking.

McCauley, A. (2019), Can blockchains give you competitive advantage?, https://www.forbes.com/sites/alisonmccauley/2019/12/11/can-blockchains-give-you-competitive-advantage/?sh=3a0a866629f0.

Min, X., Li, Q., Liu, L., & Cui, L. (2016, August). A permissioned blockchain framework for supporting instant transaction and dynamic block size. In 2016 IEEE Trustcom/BigDataSE/ISPA (pp. 90–96). IEEE.

Mishra, S., & Mohanty, P. (2014). Corporate governance as a value driver for firm performance: Evidence from India. Corporate Governance, 14, 265–280.

Moran, W. T. (1981). Research on discrete consumption markets can guide resource shifts, help increase profitability. Marketing News, 14(23), 4.

Mu, W., Bian, Y., & Zhao, J. L. (2019). The role of online leadership in open collaborative innovation: Evidence from blockchain open source projects. Industrial Management & Data Systems.

Murray, A., Kuban, S., Josefy, M., & Anderson, J. (2021). Contracting in the smart era: The implications of blockchain and decentralized autonomous organizations for contracting and corporate governance. Academy of Management Perspectives, 35(4), 622–641.

Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review, 21260. https://bitcoin.org/bitcoin.pdf.

Nanni, A. J., Dixon, R., & Vollmann, T. E. (1992). Integrated performance measurement: Management accounting to support the new manufacturing realities. Journal of Management Accounting Research, 4, 1–19.

Nelito (2018). Blockchain technology in banking and finance. (Accessed on 3rd May 2021)- https://www.nelito.com/blog/blockchain-technology-in-banking-and-finance.html.

Oracle Netsuite. (2019). What blockchain technology can do for your business, According to experts, https://www.netsuite.com/portal/resource/articles/business-strategy/blockchain-technology.shtml.

Oza H. (2018). The importance of blockchain in the banking sector. Accessed on 5th May 2021-https://www.hyperlinkinfosystem.com/blog/the-importance-of-blockchain-in-the-banking-sector.

Papadopoulos, G. (2015). Blockchain and digital payments: an institutionalist analysis of Cryptocurrencies. Handbook of digital currency (pp. 153–172). Academic Press.

Pasquale, F. (2015). The Black Box Society: The Secret Algorithms That Control Money and Information. Harvard University Press.

Pilkington, M. (2016). Blockchain technology: Principles and applications. Edward Elgar Publishing.

Porter, M. E. (1980). Industry structure and competitive strategy: Keys to profitability. Financial Analysts Journal, 36(4), 30–41.

Pradipto, Y. D., Barlian, E., Suprapto, A. T., Buana, Y., Bawono, A., Garnaditya, D., & Pangaribuan, C. H. (2019). The role of blockchain technology as a mediator between knowledge management and sustainable competitive advantage. In SU-AFBE 2018: Proceedings of the 1st Sampoerna University-AFBE International Conference, SU-AFBE 2018, 6–7 December 2018, Jakarta Indonesia (p. 319). European Alliance for Innovation.

Prahalad, C. K., & Hamel, G. (1997). The core competence of the corporation. Strategische Unternehmungsplanung/Strategische Unternehmungsführung (pp. 969–987). Physica.

Queiroz, M. M., & Wamba, S. F. (2019). Blockchain adoption challenges in supply chain: An empirical investigation of the main drivers in India and the USA. International Journal of Information Management, 46, 70–82.

Rajnak, V., & Puschmann, T. (2020). The impact of blockchain on business models in anking. Information Systems and e-Business Management, 19, 1–53.

Rebello, J. & Jaikrishnan. (2021b), 15 banks to start new trade finance system using blockchain technology, https://economictimes.indiatimes.com/industry/banking/finance/banking/15-banks-to-start-new-trade-finance-system-using-blockchain-tech/articleshow/83545043.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst.

Rehman, N., Razaq, S., Farooq, A., Zohaib, N. M., & Nazri, M. (2020). Information technology and firm performance: Mediation role of absorptive capacity and corporate entrepreneurship in manufacturing SMEs. Technology Analysis & Strategic Management, 32(9), 1049–1065.

Research Report (2018). A blockchain guide to the benefits, frameworks, initiatives, & more for the public sector. (Accessed on 23rd April 2021)- https://www.comptia.org/resources/harnessing-the-blockchain-revolution-comptia-s-practical-guide-for-the-public-sector.

Richter, N. F., Schmidt, R., Ladwig, T. J., & Wulhorst, F. (2017). A critical perspective on the measurement of performance in the empirical multinationality and performance literature. Critical Perspectives on International Business, 13, 94–118.

Rondeau, P. J., Vonderembse, M. A., & Ragu-Nathan, T. S. (2000). Exploring work system practices for time-based manufacturers: Their impact on competitive capabilities. Journal of Operations Management, 18(5), 509–529.

Schuetz, S., & Venkatesh, V. (2020). Blockchain, adoption, and financial inclusion in India: Research opportunities. International Journal of Information Management, 52, 101936.

Seebacher, S., & Schüritz, R. (2017). Blockchain technology as an enabler of service systems: A structured literature review. In International Conference on Exploring Services Science (pp. 12–23). Springer, Cham.

Sekaran, U., & Bougie, R. (2010). Research methods for business: a skill building approach (5th ed.). John Wiley and Sons.

Selgin, G. (2015). Synthetic commodity money. Journal of Financial Stability, 17, 92–99. https://doi.org/10.1016/j.jfs.2014.07.002

Sheel, A., & Nath, V. (2019). Effect of blockchain technology adoption on supply chain adaptability, agility, alignment and performance. Management Research Review, 42(12), 1353–1374.

Silva, E. (2019). How can blockchain help your business gain a competitive advantage? Springer.

Singh, D., & Malik, G. (2018). Technical efficiency and its determinants: a panel data analysis of indian public and private sector banks. Asian Journal of Accounting Perspectives, 11(1), 48–71.

Stalk, G., (1988). Time the next source of competitive advantage. Harvard Business Review, 66, 41–51.

Staples, M., Chen, S., Falamaki, S., Ponomarev, A., Rimba, P., Tran, A. B., & Zhu, J. (2017). Risks and opportunities for systems using blockchain and smart contracts Data61. CSIRO.

Stock, A. M., Robinson, V. L., & Goudreau, P. N. (2000). Two-component signal transduction. Annual Review of Biochemistry, 69(1), 183–215.

Swan, M. (2015). Blockchain: Blueprint for a new economy. O’Reilly Media Inc.

Swanitiinitiative. (2018). Improving Public Service Delivery through Blockchain Technology. (Accessed on 1st April 2019)-http://www.swaniti.com/wp-content/uploads/2018/02/Blockchain-Paper_Swaniti-Initiative-1.pdf.

Tapscott, D., & Tapscott, A. (2017). How blockchain will change organizations. MIT Sloan Management Review, 58(2), 10.

Tecsynt Solutions (2018a). 4 key advantages of using blockchain in banking. (Accessed on 9th April 2019)- http://newagebankingsummit.com/europe/ 4-key-advantages-of-using-blockchain-in-banking/.

Tecsynt Solutions (2018b). Blockchain technology for banks: trends and perspectives. (Accessed on 2nd Feb 2021)-https://hackernoon.com/blockchain-technology-forbanks-trends-and-perspectives-895a854e1344.

Teece, D. J. (2007). Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strategic Management Journal, 28(13), 1319–1350.

Teece, D. J., & Pisano, G. (1994). The dynamic capabilities of firms: An introduction. Industrial and Corporate Change, 3(3), 537–556.

Trade finance (2018). Blockchain Technology in Trade Finance Infographic. (Accessed on 3rd May 2019)- https://tradeix.com/blockchain-technology-trade-finance/.

Tsai, M. T., & Shih, C. M. (2004). The impact of marketing knowledge among managers on marketing capabilities and business performance. International Journal of Management, 21(4), 524.

Umalkar M., Macneil A. and Light D. (2016). What every CEO should know about blockchain. (Accessed on 15th April 2019)-file:///C:/Users/pgarg/Downloads/Accenutre-Outlook-Blockchain-POV.pdf.

Underwood, S. (2016). Blockchain beyond bitcoin. Communications of the ACM, 59(11), 15–17.

Universal payments (2017). Unlocking the real benefits of blockchain through its “Sweet Spot”. (Accessed on 12th Nov, 2021)- https://www.aciworldwide.com/-/media/files/collateral/trends/unlocking-benefits-of-blockchain-tl-us.pdf.

Vega, M. (2021). How blockchain is transforming the banking industry, https://www.hexacta.com/blockchain-in-banking-transforming-the industry/#:~:text=Using%20Blockchain%20in%20the%20banking,a%20wide%20array%20of%20clients.

Venkatraman, N., & Ramanujam, V. (1986). Measurement of business performance in strategy research: A comparison of approaches. Academy of Management Review, 11(4), 801–814.

Vorhies, D. W., & Morgan, N. A. (2003). A configuration theory assessment of marketing organization fit with business strategy and its relationship with marketing performance. Journal of Marketing, 67(1), 100–115.

Wang, H. L. (2014). Theories for competitive advantage. Springer.

Weerawardena, J., & Mavondo, F. T. (2011). Capabilities, innovation and competitive advantage. Industrial Marketing Management, 40(8), 1220–1223.

Wood, R., Bandura, A., & Bailey, T. (1990). Mechanisms governing organizational performance in complex decision-making environments. Organizational Behavior and Human Decision Processes, 46(2), 181–201.

Wright, S. (1918). On the nature of size factors. Genetics, 3(4), 367.

Wright, S. (1920). The relative importance of heredity and environment in determining the piebald pattern of guinea-pigs. Proceedings of the National Academy of Sciences of the United States of America, 6(6), 320.

Wright, S. (1923). The theory of path coefficients a reply to Niles’s criticism. Genetics, 8(3), 239.

Yamada, Y., Nakajima, T., & Sakamoto, M. (2016). Blockchain-LI: a study on implementing activity-based micro-pricing using cryptocurrency technologies. In Proceedings of the 14th International Conference on Advances in Mobile Computing and Multi Media (pp. 203–207).

Ying, W., Jia, S., & Du, W. (2018). Digital enablement of blockchain: Evidence from HNA group. International Journal of Information Management, 39, 1–4.

Yoo, S. (2017). Blockchain based financial case analysis and its implications. Asia Pacific Journal of Innovation and Entrepreneurship.

Yu, T., Lin, Z., & Tang, Q. (2018). Blockchain: The introduction and its application in financial accounting. Journal of Corporate Accounting & Finance, 29(4), 37–47.

Zhang, J. (1997). The nature of external representations in problem solving. Cognitive Science, 21(2), 179–217.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix A

1.1 Required- Part-A

Name of the Respondent |

Organization |

Department |

Designation |

Gender |

Age range |

Email ID |

Measurement

Measures of the blockchain capabilities (BCC) |

Blockchain is a distributed ledger technology has the capabilities to offer quality customer products/services, enhance efficiency and security, reduce operational cost and regulatory compliance secure remittances. With regards to blockchain capabilities, based on your experience on block chain implementation in banking sector, please indicate the number that accurately reflects capabilities of blockchain in context to banking sector. All items are measured on 5 points whereas 1 = "strongly disagree” and 5 = "strongly agree". |

2.1 Quality customer products/services (BCC/QCS)

Do you think that blockchain implementation enhances transparency in banking system (BCC/QCS1)?

Do you think that blockchain implementation enhances trust in banking system (BCC/QCS2)?

Do you think that blockchain implementation enhances data accuracy in banking system (BCC/QCS3)?

Do you think that blockchain implementation mitigates the risk in banking system (BCC/QCS4)?

*Do you think that blockchain implementation automates actions and transactions between parties in banking system (BCC/QCS5)?

2.2 Reduced cost(BCC/RC)

Do you think that blockchain implementation decreases transaction cost in banking system (BCC/RC1)?

Do you think that blockchain implementation eliminates intermediaries in banking system (BCC/RC2)?

Do you think that blockchain implementation lessen administrative cost in banking system (BCC/RC3)?

Do you think that blockchain implementation lessen operational cost in banking system (BCC/RC4)?

2.3 Efficiency and security (BCC/ES)

Do you think that blockchain implementation ensures tracking real time business transactions in banking system (BCC/ES1)?

Do you think that blockchain implementation enhances speed of transaction in banking system (BCC/ES2)?

Do you think that blockchain implementation enhances efficiency in banking system (BCC/ES3)?

Do you think that blockchain implementation enhances security in banking system (BCC/ES4)?

Do you think that blockchain implementation enhances the integrity of the system in banking system (BCC/ES5)?

2.4 Secure remittances (BCC/SR)

Do you think that blockchain implementation enables an immutable audit trail in banking system (BCC/SR1)?

Do you think that blockchain implementation enables a fast and secure payment process in banking system (BCC/SR2)?

Do you think that blockchain implementation enhances system resilience in banking system (BCC/SR3)?

Do you think that blockchain implementation enhances robustness in banking system (BCC/SR4)?

Do you think that blockchain implementation enhances the traceability of transactions in banking system (BCC/SR5).

Do you think that blockchain implementation enhances the control on data in banking system (BCC/SR6)?

2.5 Regulatory compliance (BCC/RCo)

Do you think that blockchain implementation ensures to streamline of the business process in banking system (BCC/RCo1)?

Do you think that blockchain implementation ensures the immutable business rules in banking system (BCC/RCo2)?