Abstract

Static and discrete time pricing operators for two price economies are reviewed and then generalized to the continuous time setting of an underlying Hunt process. The continuous time operators define nonlinear partial integro–differential equations that are solved numerically for the three valuations of bid, ask and expectation. The operators employ concave distortions by inducing a probability into the infinitesimal generator of a Hunt process. This probability is then distorted. Two nonlinear operators based on different approaches to truncating small jumps are developed and termed \(QV\) for quadratic variation and \(NL\) for normalized Lévy. Examples illustrate the resulting valuations. A sample book of derivatives on a single underlier is employed to display the gap between the bid and ask values for the book and the sum of comparable values for the components of the book.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In classical economic theory the law of one price prevails and market participants trade freely in both directions at the same price. Furthermore, these prices are determined by market clearing equating aggregate demand to supply or excess demand to zero. Recently, Madan (2012) presents an equilibrium model in which both the law of one price and market clearing simultaneously fail. The law of one price is replaced by a two price economy and market participants continue to trade freely with the market but the terms of trade now depend on the trade direction. The starting of this paper is the equilibrium pricing rule that prevails in such a two price economy.

The failure of market clearing occurs on account of a gap between the events that can occur and the events that can be contracted. The latter is a much smaller set of events. As a result unexpected events can cause endowments to disappear, making the clearing of precommitted demands impossible. In such situations markets must be supported by a financial system that approves trades by participants and covers any subsequent losses.

All market participants are modeled as selling their endowments to the financial system for a conservative valuation. They then spend the proceeds of this sale to meet their demands by purchasing from the financial system at an inflated valuation. The financial system in turn sets the spread between its conservative purchase price and its inflated sale price with a view to making trades acceptable.

The financial system is not an optimizing agent but passively sets the terms at which market participants may trade. The financial system may be viewed as the Walrasian auctioneer operating in a world in which market clearing is not attainable. Therefore, instead of determining the market clearing price, the auctioneer, now subject to potential losses, determines the two prices of a two price economy with a view to making such loss exposures acceptable.

The purpose of this paper is to develop the continuous time theory for such two price economies. The two prices may be termed bid and ask prices for some precision and brevity but they should not be confused with the literature relating bid-ask spreads to transactions costs, the modeling of illiquidity, the effects of asymmetric information or other frictions involved in modeling the financial industry (see Freixas and Rochet 2008). There is a large literature both empirical and theoretical studying bid ask spreads by focusing on the costs, incentives, objectives and constraints of liquidity providers seen as rational agents operating as market makers in exchange traded securities. We cite in this regard (Allen and Gale 2007; Ahimud et al. 2006) and the references therein. Modeling the optimal behavior of rational agents introduces interesting game theoretic considerations into the analysis. In contrast the approach taken here is to model passively the Walrasian auctioneer with a limited interest in attempting to clear markets. The model is then simpler and though tractable, sufficient complexities remain.

The two prices of a two price economy are determined in a non market-clearing equilibrium with a view to making loss exposures acceptable. Acceptability is itself defined as a positive expectation under a family of test measures or scenarios. As a result the bid price is the infimum of test valuations and the ask price is the supremum of such valuations. On the space of random variables, the bid price functional is then a concave functional while the ask price functional is convex. Economically packaged risks are more attractive as they embody potential diversification benefits while the linearity of arbitrage pricing disappears given the absence of the law of one price.

Given that the bid and ask price functionals are respectively concave and convex their dynamic counterparts are of necessity examples of nonlinear expectation operators. Nonlinear expectation operators are a fast developing field of mathematical analysis (see Peng 2004; Rosazza Gianin 2006). These connections were noted in Madan et al. (2013), and Madan and Schoutens (2012b) by relating to Cohen and Elliott (2010). Cohen and Elliott (2010) develop nonlinear expectations as solutions to backward stochastic difference equations in the context of a finite state discrete time Markov chain. Nonlinear expectation operators provide us with dynamically consistent nonlinear pricing rules as discussed in Jobert and Rogers (2008) and Bion-Nadal (2009).

Encouraged by the work of Peng (2006) in developing nonlinear \(\mathcal{G }\)-expectations (see section 3 of Peng 2006) we propose here a continuous time nonlinear \(\mathcal{G }\)-expectation operator for the continuous time modeling of two price economies. In contrast to Peng (2006) we simultaneously model both a linear expectation operator and two nonlinear operators for the bid and the ask. The linear expectation operator serves the purpose of a traditional risk neutral valuation operator except that all trades occur at the nonlinear prices. However, we maintain some of the advantages of a linear operator by preserving linearity on comonotone risks.

From a financial and risk management perspective the contribution of this paper is to provide operational algorithms for the computation of risk sensitive bid and ask prices as functionals on the space of random variables. The Basel system has sought such procedures for years building ad-hoc approaches in the interim. Further as argued in Madan (2012) for two price economies marking to market must be interpreted as marking to two price markets with assets marked to bid and liabilities marked to ask. It is then insufficient to just have available linear risk neutral valuation operators, one needs the nonlinear two price operators to mark the books. Additionally capital reserves reflect the asset shaves and liability add ons built into the bid and ask functionals relative to the expectation functional. In this regard all three operators, the nonlinear bid and ask and the linear expectation are employed. The present paper delivers all three with the property that under the linear expectation the bid price is a submartingale while the ask price is a super martingale.

The outline of the rest of the paper is as follows. Section 2 summarizes the two price economy and its bid and ask price functionals in a static one period context. The discrete time dynamic construction with its links to nonlinear expectations for finite state Markov chains is summarized in Sect. 3. Section 4 introduces the continuous time bid and ask price functionals as nonlinear \(\mathcal{G }\)-expectations in the context of a Hunt (1966) process. Illustrative valuations are conducted in Sect. 5. Section 6 applies these methods to the valuation of a derivatives book on a single underlier. Section 7 illustrates calibration procedures. Section 8 concludes.

2 The one period two price economy

Much has been written on modeling the mathematical representation of consumers, producers, firms, financial institutions, financial intermediaries and other market participants. They are all generally seen as optimizing agents with various approaches taken to represent their objectives and constraints. For consumers for example there is the use of expected utility, or a dual choice theory, Choquet expected utility and more recent formulations of Behaviorial Finance. The econophysics literature models agents as automatons following prespecified decision rules. For firms and other agents there is in addition the modeling of production technologies along with the difficult question of risk attitudes when market incompleteness leads to insufficient price information as some risks are not priced.

But what about the Walrasian auctioneer or the market itself? Technically in the Arrow Debreu theory the market is modeled as a non-optimizing agent that merely seeks to set prices with a view to ensuring market clearing. Once this is done, equilibrium is attained and we have a competitive economy in equilibrium. The two price economy focuses attention on the Walrasian auctioneer or the market itself as another agent with whom all must trade. This implicit agent, however, by virtue of being the counterparty for all trades, is too powerful and does not optimize. This auctioneer or more generally the market merely defines passively the terms of trade for all participants, remaining interested in market clearing.

The difference between classical economic theory and the theory of a two price economy is that market clearing though an objective for the market seen as a passive agent is in fact unattainable. Were clearing possible with positive excess supplies for all items in all states, the law of one price would return. Recognizing that markets cannot always clear, the interest shifts to making excess supplies acceptable, though not necessarily nonnegative. The market tries to get excess supplies to belong to some small prespecified cone containing the nonnegative random variables. This is done with a view to minimizing loss exposures. The size of this cone serves as a financial primitive in defining the two price economy. The larger the size of this cone the greater is the set of approved trading opportunities and the larger is the size of the real economy. On the contrary when this cone contracts, the real economy shrinks, the market approves of fewer transactions and economic activity is reduced.

Consider now an economy trading state contingent claims on a classical probability space \((\Omega ,\mathcal{F },P)\). In addition to endowments, preferences, technology and firm objectives we now have to define the set of acceptable aggregate excess supplies. This set is by construction a convex cone of random variables \(\mathcal{A }\) containing the nonnegative random variables. Artzner et al. (1999) show that all such sets are defined by a convex set of probability measures \( \mathcal{M }\) with the defining condition being

The set of probability measures \(\mathcal{M }\) has been called the set of test measures or scenarios that test for and approve the acceptability of a random variable. In fact the Federal Reserve Board now requires major banks with more than 50 billion in assets to conduct such stress tests annually (FRB Press Release, November 22 2011) with a view to ascertaining capital adequacy.

In a two price economy the market targets the acceptability of excess supplies \(\left( X\in \mathcal{A }\right) \) defined in this way for some set of test or scenario measures \(\mathcal{M }\). The market’s interest lies in keeping \(\mathcal{A }\) small and therefore \(\mathcal{M }\) is large. However in trading with economic agents, all of whom must trade with the market, the market is more lenient and is willing to define a larger set of acceptability, \(\mathcal{B },\) with a related much smaller set of test measures \(\mathcal{N }\). Indeed it is possible that even with this generous definition of acceptability offered to individual market participants the aggregate excess supply may nonetheless enter the required smaller set \( \mathcal{A }\). By way of contrast with classical economic theory as opposed to the two price economy one notes that classically \(\mathcal{B }\) is a very generous half space with \(\mathcal N= \left\{ Q\right\} \) for the risk neutral measure \(Q\) and \(\mathcal{A }\) is the cone of nonnegative random variables with \(\mathcal{M }\) being the set of all probability measures.

When the market offers individual market participants the cone \(\mathcal{B }\) of acceptability it is shown in Madan (2012) and easily observed that the price system offered by the market is now a two price system with bid price \( b(X)\) and ask price \(a(X)\) defined by

Equations (1) and (2) define the price system offered in equilibrium to all market participants by the market as the counterparty for all trades.

We note at this point that by construction the bid pricing functional will be a concave functional on the space of random variables while the ask price functional will be a convex functional. They are then both nonlinear pricing operators and it is these properties that will later take us to nonlinear expectation operators. Furthermore, one only needs to learn how to construct the bid pricing functional as the ask price is always the negative of the bid price of \(-X\).

The next step in the operational development of two price economies comes in the construction of the set of approving probability measures. The realization here is not to give up completely on classical theory and its selection of a risk neutral equilibrium pricing operator, but to ensure that the cone of a two price economy is strictly contained in the classical half space. We therefore begin by selecting a classical risk neutral equilibrium pricing measure \(Q^{*}\) as an element of \(\mathcal{N }\). Next we consider the possibility of defining acceptability of a random variable \(X\) completely in terms of the probability law of \(X\) under \(Q^{*}\). Acceptability must then be defined with just the distribution function \( F_{X}(x)\) of \(X\) under \(Q^{*}\) as an input or the definition of acceptability is law invariant in the sense of Kusuoka (2001).

Such a definition based only on the probability law may be objectionable from the perspective of human agents who may wish to consider how the random variable enters the portfolio of risks being held. However, we are modeling here the market or Walrasian auctioneer with the single minded interest of eventual clearing suitably modified for two price economies. There is no portfolio to refer to or preferences to formulate. With these qualifying remarks we proceed to define acceptability just in terms of the risk neutral distribution function.

The next item to be addressed is the preservation of some linearity in the pricing functionals. They are nonlinear by construction but we may ask for linearity for some set of risks. In this regard we note that two random variables \(X,Y\) are said to be comonotone if

Comonotone variables always move together in the same direction, or one is in fact an increasing function of the other. Preserving linearity for comonotone variables is a useful reduction in the complexity of the pricing operator and we can ask that

for \(X,Y\) comonotone.

Assuming both law invariance and linearity for comonotone risks yields by Kusuoka (2001) a representation for all such functionals as a distorted expectation. More specifically there must then exist a concave distribution function \(\Psi (u)\) for \(0\le u\le 1,\) with \(\Psi (0)=0,\) \(\Psi (1)=1\) such that for all \(X\) we have

Such distorted expectations were proposed as models for bid prices in Cherny and Madan (2010). A distorted expectation is an expectation under a change of measure via

with the measure change \(\Psi ^{\prime }(F_{X}(x))\) depending on \(X\) and hence the nonlinearity. With a view to reweighting losses and discounting gains whereby \(\Psi ^{\prime }\) tends to infinity and zero as \(u\) tends to zero or unity, Cherny and Madan (2009) proposed the distortion termed minmaxvar and defined by

The computations conducted in this paper employ this distortion.

It is critical to note that when there is no distortion being applied and \( \Psi ^{\prime }(u)=1\) we recover the expectation and the bid equals the ask. With a distortion the reweighting upwards of losses and downwards of gains forces the bid price to fall below the expectation. Similar considerations force the ask price to be above the expectation.

One may relate to any such distortion \(\Psi \) a Choquet capacity \(c(A)\) (Choquet 1954) defined via

for every \(A\in \mathcal{F }\). It is shown in the appendix that \(c\) defined this way is a Choquet capacity. One may also define a Choquet capacity \(\nu \) on \(\mathbb R \) by

The distorted expectation (3) for the bid price is the Choquet type integral

Given the wide use of Choquet capacities in numerous contexts, it is noteworthy to observe that the bid pricing functional proposed under law invariance and linearity under comonotonicity is a Choquet integral.

Cherny and Madan (2009) show that the set of measures supporting acceptability consists of all distribution functions on the unit interval dominated pointwise above by the distortion. The connection with Choquet capacities provides an alternative demonstration of the set of supporting measures \(\mathcal{N }\).

Applications of the static model for bid and ask prices have been made in a number of papers. Madan (2009) employs the static bid price to define capital requirements and monitor leverage. Madan (2010) determines option hedges for complex claims written on many underliers with a view to minimizing the ask price of the unhedged risk. Eberlein and Madan (2012) use these methods to determine capital requirements for the major US banks at the end of 2008 along with determining the value of the limited liability option to put losses back into the economy. Carr et al. (2011) advocate capital requirements as the difference of ask and bid prices. Eberlein et al. (2012) relate this capital requirement to risk weighted assets as defined in the Basel accords. Cherny and Madan (2010) also estimate stress levels of distortions from market bid and ask price quotes of put and call options. Madan and Schoutens (2011a) study clientele effects on optimal debt in the absence of tax advantages to debt via an application of two price economy accounting. Madan and Schoutens (2011b) apply the static two price theory to the valuation of contingent capital notes. Madan (2011) models risk weighted assets with these methods for pricing contingent capital notes. Madan and Schoutens (2012a) study the equilibrium of two price economies trading structured notes. Eberlein et al. (2012) show how valuing liabilities at ask prices mitigates the level of profits associated with debt valuation adjustments (DVA).

3 The discrete time two price economy

Consider now a discrete time economy with the uncertainty evolution described by a finite state Markov chain. For computational purposes and model calibrations one may employ Markov chain approximations to more general processes as described in Mijatović and Pistorius (2013). Following Cohen and Elliott (2010) we may view the Markov chain \( (X_{t},t=1,\ldots ,T)\) as taking values in the unit vectors of N-dimensional space \(\mathbb R ^{N},\) i.e.

with \(e_{i}=(0,0,\ldots ,0,1,0,\ldots ,0)^{\prime }\in \) \(\mathbb R ^{N}\). The price of a stock \(S_{t}\) for example could then be modeled as,

where the \(x_{i }^{\prime }s\) are the \(N\) possible values for the logarithm of the stock price at each time step. The chain is described by \(T\) transition probability matrices that could be time dependent.

Let \(\left( \Omega ,\mathcal{F },\left\{ \mathcal{F }_{t}\right\} _{0\le t\le T},Q^{*}\right) \) be the filtered probability space generated by some risk neutral process \(X\). Let \(C\) be a terminal cash flow known at time \(T\). The set of all terminal cash flows to be valued may be taken to be a subset \(\mathcal{C },\) \(\ \mathcal{C }\subset L^{2}\left( \mathcal{F } _{T}\right) \). Anticipating the nonlinearity of bid and ask pricing operators we follow Cohen and Elliott (2010) in first defining a system of dynamically consistent nonlinear expectation operators. An alternatively approach axiomatizes time consistency for a dynamic and adapted family of risk measures that are then related to BSDE’s. We refer the reader to Bion-Nadal (2009), Bielecki et al. (2011) and Rosazza Gianin and Sgarra (2012) for an analysis of the associated dynamic risk measures.

A nonlinear, dynamically consistent system of conditional expectations is a set of operators

satisfying the following four properties.

-

1.

For any \(C,C^{\prime }\in \mathcal{C }\)

$$\begin{aligned} \mathcal{E }\left( C|\mathcal{F }_{t}\right) \ge \mathcal{E }\left( C^{\prime }|\mathcal{F }_{t}\right) Q^{*}-a.s. \end{aligned}$$whenever \(C\ge C^{\prime }\) \(\ \ \ Q^{*}-a.s\). with equality iff \( C=C^{\prime }\) \(\ \ \ Q^{*}-a.s\).

-

2.

\(\mathcal{E }\left( C|\mathcal{F }_{t}\right) =C\) \(Q^{*}-a.s\). for any \(\mathcal{F }_{t}\)-measurable \(C\).

-

3.

\(\mathcal{E }\left( \mathcal{E }\left( C|\mathcal{F }_{t}\right) | \mathcal{F }_{s}\right) =\mathcal{E }\left( C|\mathcal{F }_{s}\right) \) \( Q^{*}-a.s\). for any \(s\le t\).

-

4.

For any \(A\in \mathcal{F }_{t},\) \(\ \ \mathbf 1 _{A}\mathcal{E }\left( C| \mathcal{F }_{t}\right) =\mathcal{E }\left( \mathbf 1 _{A}C|\mathcal{F } _{t}\right) \) \(\ \ \ Q^{*}-a.s\).

The dynamically consistent system of bid and ask prices will be respectively concave and convex systems of nonlinear expectation operators. Furthermore they are dynamically translation invariant in the sense that for any \(C\in \mathcal{C }\) and any \(q\in \mathcal{F }_{t}\)

The construction of such dynamically translation invariant nonlinear expectations on a finite state Markov chain is linked to the solution of backward stochastic difference equations by Theorem 5.1 of Cohen and Elliott (2010). We denote a nonlinear expectation by \(\mathcal{E }\) while a classical linear expectation is denoted by \(E\). To describe these equations and their solution for a finite state Markov chain we introduce the martingale difference process

A backward stochastic difference equation \((BSDE)\) for our purposes is defined by a real-valued driver \(F\left( \omega ,u,Y_{u},Z_{u}\right) \) where \(Y\) is a real-valued stochastic process adapted to the Markov chain, \( Z \) is an \(\mathbb R ^{N}\)-valued stochastic process, and \(F\) is a progressively measurable map

which is essentially bounded. A \(BSDE\) based on \(M\) with driver \(F\) and terminal value \(C\) is an equation of the form

where \(C\) is an essentially bounded \(\mathcal{F }_{T}\)-measurable random variable, with \(Y\) and \(Z\) the unknowns. In difference form we may write

and taking \(\mathcal{F }_{t}\)-conditional linear expectations we see that

and so we solve for \(Y_{t}\) backwards by evaluating the conditional expectation of \(Y_{t+1}\) and adding the penalty given by the driver. By Theorem 5.1 of Cohen and Elliott (2010) for the construction of a nonlinear dynamically consistent and translation invariant conditional expectation the driver is independent of \(Y_{t}\) and is itself the nonlinear expectation of the zero mean one step ahead risk or

We define \(Z_{t}^{^{\prime }}\) by

For computing bid prices, denoted \(Y_{t}^{b},\) the driver is

while for ask prices \(Y_{t}^{a},\) the driver is

The functions \(b,a\) are one step ahead distorted expectations. The use of distortions at each time step yields locally law invariant time consistent expectations. For time consistency coupled with a global law invariance we refer the reader to Kupper and Schachermayer (2009).

We may observe from this construction, recalling that bid prices lie below expectations while ask prices are above them, that the bid price process satisfies

whereas for the ask price process we have

Hence dynamically consistent bid prices are submartingales while ask prices are supermartingales. This property is preserved in the continuous time formulation.

It is useful to note that as constants may be extracted freely from distorted expectations the distorted expectation may always be viewed as applied to a centered variable. The bid price for a variable with zero expectation is then negative while the ask is positive. One may then view dynamic bid and ask price sequences as respectively, subtracting or adding, a risk charge from the one step ahead expectation. The magnitude of this charge depends on the probability law of the centered variable.

Numerous papers have applied these discrete time dynamically consistent bid and ask price sequences. For example Madan et al. (2013) price a variety of structured products in a context where transition probabilities are estimated to meet marginal densities extracted from option prices. The procedure for extracting transition probabilities follows Davis and Hobson (2007). Madan and Schoutens (2012b) investigate the effect of the discrete tenor on such pricing sequences. Madan (2010) implements dynamic hedging modified to minimize capital requirements defined as the difference between dynamically consistent ask and bid price sequences as advocated in Carr et al. (2011). Madan et al. (2011) apply these methods to the pricing of insurance loss liabilities, the determination of capital minimizing reinsurance attachment points and the financial hedging of securitized insurance loss exposures.

4 Continuous time modeling of bid and ask price functionals

The static and discrete time models for two price economies, as useful as they are in a variety of contexts, fall short of providing valuations for claims delivered at arbitrary time points in the future. It is like an option pricing theory constrained to maturities being an integer multiple of some tenor. The objective here is to extend the theory of two price economies to continuous time. This leads us naturally to dynamically consistent nonlinear pricing in continuous time. Fortunately much progress has already been made here in the construction of \(\mathcal{G }\)-expectations by Peng (2006). Our task reduces to describing the \(\mathcal{G }\) in our application of \(\mathcal{G }\)-expectation.

We proceed in subsections, first introducing the context in which we work by reviewing the construction of expectations that are to be lifted to \( \mathcal{G }\)-expectations. Next we present the general approach of \(\mathcal{G }\)-expectations that we will follow. A presentation of two particular nonlinear \(\mathcal{G }\)-operators ensues. The operators are related to the distortions employed in the static and discrete time cases. The next subsection includes some results on simplifying valuations for monotone classes of functions. The final subsection studies the Doob–Meyer decomposition of the bid price under the linear expectation operator and shows that bid prices are submartingales.

4.1 The underlying uncertainty and expectation operator

The underlying uncertainty is given by a pure jump Lévy process \( (X_{t},0\le t\le T)\). More generally one could take an underlying (Hunt 1966) process. The applications made use of such a process by allowing the parameters of the jump compensator to depend mildly on the current level of the process. However, for the theoretical discussion such a dependence is not necessary. The pure jump Lévy process is specified by the drift term \(\alpha \) and the Lévy measure \(k(y)dy\) defined for \(y\ne 0\). An example that we shall work with is the variance gamma process (Madan and Seneta 1990; Madan et al. 1998) for which the Lévy density is given in CGMY format (Carr et al. 2002) by

In general the Lévy measure is not a finite measure but satisfies

We shall work with processes satisfying the stronger condition

In such cases the infinitesimal generator \(\mathcal{L }\) of the process is given by

Now let \(u(x,t)\) be the time zero financial value when \(X(0)=x,\) of a claim paying \(\phi (X_{t})\) at time \(t\). The function \(u(x,t)\) for a constant interest rate of \(r,\) is the solution of the partial integro–differential equation

subject to the boundary condition \(u(x,0)=\phi (x)\).

More formally

with \(X_{t}\) the driving Lévy process. The linear expectation equation (8) is what we shall generalize to a nonlinear partial integro–differential equation that will yield the bid and ask pricing functionals of our two price economy in continuous time.

4.2 The \(\mathcal{G }\)-expectation approach

The infinitesimal generator \(\mathcal{L }\) of equation (7) is a linear operator on \(u\). (Peng 2006) created \(\mathcal{G }\)-expectations defined as nonlinear expectations that are unique viscosity solutions to nonlinear equations of the form

for the boundary condition \(u(x,0)=\phi (x)\). The result is

where \(\mathcal{E }\) is a dynamically consistent nonlinear expectation operator.

The operator \(\mathcal{G }\) is now a nonlinear operator. For the definition of \(\mathcal{G }\)-Brownian motion the specific operator \(\mathcal{G }\) is given by

where \(a^{+}=\max (a,0)\) and \(a^{-}=\max (-a,0)\) and one solves the equation

The way to get nonlinear bid and ask price functionals described in the following section is to replace the linear operator \(\mathcal{L }\) by a suitable nonlinear operator \(\mathcal{G }\) and then to solve

for \(u(x,0)=\phi (x)\). The solution of this equation is a financial bid price

4.3 \(\mathcal{G }\)-expectations using distortions

Concave distortions are applied to distribution functions of random variables exaggerating their low states and discounting their high states. The role of the Lévy measure in the expression for \(\mathcal{L }(u)\) is not unlike that of a probability as it is the limit of probabilities. However, the Lévy measure does not integrate to unity whereas distortions operate on the unit interval. Our first suggestion is to rewrite the integral expression in \(\mathcal{L }(u)\) with the objective of forcing a probability measure into view. We may equivalently write for the integral in (7) the expression

where we now write

thus recovering (7). The function \(g(y)\) is positive, integrates to unity and thus is a probability density. In the altered expression (11) \(g(y)\) is employed to compute the expectation of the variable which is random in \(y\) for a given \(x,t\) and defined by

We may equivalently define the distribution function

and then write the integral (11) as

Now we consider the distorted expectation

which agrees with the integral

where \(P^{g}\) indicates that we evaluate probability under the quadratic variation scaled density \(g(y)\).

We define

and solve (10) for the nonlinear bid price. The ask price is the negative of the bid for the negative cash flow.

We note that scaling by quadratic variation is a way of ignoring or truncating the small moves. Another way to ignore these jumps given that the function being evaluated is of order \(O(y^{2})\) is to consider the integral

where we effectively truncate a small neighbourhood of zero. We may now rewrite and force the probability \(h(y)\) as

where we now define the density

The random variable in \(y\) for fixed \(x,t\) is now

and the relevant nonlinear operator denoted \(\mathcal{G }_{NL}\) for normalized Lévy is

We have thus defined two nonlinear partial integro–differential operators the solutions of which yield nonlinear bid prices for claims written on the terminal value of the Lévy process. These are the \(QV\) and \(NL\) approaches which ignore small jumps and induce a probability to distort. In our applications the nonlinear partial integro–differential equations are solved numerically for the value of contracts.

4.4 Valuing monotone and comonotone classes

This subsection considers monotone and a particular class of comonotone functions.

4.4.1 Monotone functions

For monotone claims like call and put options the value functions are monotone in the jump size \(y\). For an increasing claim the distorted expectation may be simplified by working with just the distribution function \(G(v)\) given by

where \(g(y)\) is as defined in (12).

Restricting attention to the finite variation case the integral part of Eq. (7) can be simplified to

We may now distort to

For decreasing claims like put options we wish to distort

and the distorted expectation writes

In both cases these expectations are conducted under an altered Lévy measure given by

for call options and

for put options.

When valuing options by Markov chain approximations one may easily adjust transition rates by Eqs. (13) and (14) to construct bid and ask prices for calls and puts to calibrate directly to bid and ask quotes. Section 7 of the paper illustrates such a calibration procedure.

4.4.2 A comonotone class of functions

Nonlinear valuations based on concave distortions are additive for comonotone classes of functions. An interesting comonotone class of functions is the set of even functions that are completely monotone on the right. This class has extreme points given by functions of the form

as all functions in the class may be expressed by Bernstein’s theorem as

for some finite measure \(\mu \). Hence the \(QV\) and \(NL\) nonlinear valuations of the double exponentials with parameter \(a\) enable one to evaluate

4.5 Bid prices as submartingales under the original linear expectation

Consider, in the case of zero rates and quadratic variation scaling, the bid price at time \(t\) for the claim paying \(\phi (X_{T})\) at time \(T\) when the original Lévy process is at \(X_{t}\). This bid price is given by

where the function \(u(x,t)\) solves

for the boundary condition \(u(x,0)=\phi (x)\). We observe in the appendix that for all functions \(u(.,t)\) we have the inequality

We now develop the Doob-Meyer decomposition of \(b_{t}\) under the original expectation operator as

The domination (15) then establishes the submartingale property for the bid price under the original linear expectation. The proof of (16) follows on showing that

In both Eqs. (16) and (17) \(M_{t}\) denotes a martingale. We note some similarity of Eq. (17) with Proposition 2.1 in Kunita (1997). The result (17) is established in the Appendix.

From the demonstration of Eq. (15) in the appendix one observes that the risk charge on a risk with distribution function \(F_{x,t}(v)\) is given by

and is strongly influenced by the concavity of the distortion.

5 Some illustrative valuations

For numerical computations the underlying uncertainy may easily be taken to be more general than that of a Lévy process and one may entertain Hunt processes (Hunt 1966). In the applications presented in the following, the underlying uncertainty is given by a pure jump Hunt process with space dependent jump compensators for the logarithm of the stock price at \(x\). Let the arrival rate for a jump of size \(y\in \mathbb R \backslash \{0\},\) when the log stock price is \(x,\) be \(k(x,y)\). The function \(k(x,y)\) is taken from the class of variance gamma \((VG)\) Lévy measures (6) and we then have

For a specification of the dependence of the \(VG\) parameters on the space variable the \(VG\) model is reparameterized with parameters \(a,v,q\) where \(a\) is the ratio of positive to negative variation, \(v\) is the level of finite variation in the symmetric process with exponential decay at \((G+M)/2\) and \( q \) is the quadratic variation of the symmetric process. Such a reparameterization allows us to model via \(a,\) mean reversion or momentum depending on how the rate of positive variation moves with the level of the stock. The behavior of \(v\) specifies peakedness of densities. Peakedness is greater at lower levels of \(v\). The parameter \(q\) captures the behavior of volatility or quadratic variation.

The mapping from the parameters \(a,\) \(v,\) \(q\) to \(C,\) \(G,\) \(M\) is given by

The reverse map is

For the stock price ratio \(S/S_{0}\) below 0.75 or above 1.25 the parameters are assumed to be constant. For the ratios of 0.75, 1.0 and 1.25 we specify the value of the three parameters and interpolate linearly in the interval \([0.75,1.25]\). The computations presented are for the parameterization

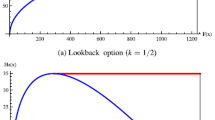

For this parameterization of a Hunt process we present in Figs. 1 and 2 the bid, ask and expectation for a \(0.9,1.1\) half year and one year strangle for a stock priced at unity for both the \(QV\) and \(NL\) pricing models where for \(NL\), \(\varepsilon =0.001\). The distortion employed is minmaxvar at the stress level 0.1.

QVCDF strangle at 6 months and 1 year

NLG strangle at 6 months and 1 year

We further report in Fig. 3 the bid and ask prices and the common expectation for a Lévy model with \(a,\) \(v,\) \(q\) specification \( 0.3,0.2,0.02\).

The two ways of truncating small jumps are observed to be comparable and the next section considers the valuation of a derivatives book for just the \(QV\) specification.

Comparison of QVCDF and NLG pricing on a 1 year 0.9, 1.1 strangle at minmaxvar stress 0.1 for a, v, q at 0.3, 0.2, 0.02

We also present in Fig. 4 the \(QV\) bid, ask and expected values for the basis functions \(\exp (-a|x|),\) of the comonotone class considered earlier, for \(a=1\) and 2.

Nonlinear valuations of extreme points of the class of even, completely monotone functions

6 Valuing a derivatives book

Consider a book of derivatives on a single underlier with cash flows \(\phi \left( x_{i},t_{j}\right) \) at future dates \(t_{j}\) for \(j=1,\ldots ,N\) that may be interpolated to build payout functions \(\phi (x,t_{j})\) and extrapolated as constant at the value at the nearest neighbour, out of the range of specified points. The nonlinear value of a derivatives book cannot be determined as the sum of the nonlinear values of each item as nonlinear values are not additive. In implementation we shall use an interpolated grid specification but in general we consider the nonlinear valuation \(u(x,t)\) for

To determine this valuation we define

and set

We then solve in the interval \(0<s\le t_{N}-t_{N-1}\)

and define the solution \(v^{N}(x,t_{N}-t_{N-1})\). We then define

and solve in the interval \(0<s\le t_{N-1}-t_{N-2}\) the function

to define \(v^{N-1}(x,t_{N-1}-t_{N-2})\). We then define

until we have computed \(v^{1}(x,t_{1})\) that is the value of the book. We then define

By way of an example we take four cash flows at the four maturities, 1, 3, 6 and 12 months to meet target greek positions. The targeted greeks are

The cash flows accessed to meet these target greeks are displayed in Fig. 5 for the four maturities. The cash flows are from positions in \(21\) strikes for out of the money options at each maturity. The strikes range from \(80\) to \(120\) in steps of \(2\) dollars. The positions are determined to match the target greeks.

Cash flows accessed at four maturities

For these cash flows we compute the expectation, as well as the bid and ask prices for the four maturities taken together and the sum of the bid and ask prices for the four maturities taken separately. The result is displayed in Fig. 6.

Bid, ask, expectation and the sum of four separate bid and ask prices for each of four maturities

We see clearly the effect of nonlinear pricing on the bid and the ask with the gap between the ask and bid of the sum and the sum of the bid and ask prices.

7 Illustrative calibration

For monotone payoffs like put and call options one may price under an altered Lévy measure as shown in Sect. 4.4.1. Equations (13) and (14). One may then approximate a Hunt process by a finite state Markov chain on non-uniform grid and tilt the transition rates by Eqs. (13) and (14) where for a local \(VG\) evolution we have explicitly that

and

For data on SPX options for April 20 2009, the parameter estimates for \( a,v,q \) in the Hunt specification were

The stress parameter was \(20\) basis points. Figures 7 and 8 present the graphs for the fit to Bid and Ask prices.

Graph of the Hunt process fit with VG a, v, q parameterization to SPX bid prices for April 20 2009

Graph of the Hunt process fit with VG a, v, q parameterization to SPX Ask prices for April 20 2009

8 Conclusion

The static and discrete time models for bid and ask prices as nonlinear operators prevailing as the equilibrium market valuation operators of two price economies are reviewed and then generalized to the continuous time setting of an underlying Hunt process. The resulting pricing operators are nonlinear partial integro–differential operators that may be numerically solved for the three valuations of bid, ask and expectation. The operators involve concave distortions that were used in the static and discrete time cases by inducing a probability into the infinitesimal generator of the Hunt process that is then distorted. Two nonlinear operators based on different approaches to ignore small jumps are developed and termed \(QV\) and \(NL\) for quadratic variation and normalized Lévy. Numerous examples of sample solutions illustrate the valuation applications that result, including the valuation of a sample book of derivatives on a single underlier.

References

Ahimud, Y., Mendelson, H., Pedersen, L.: Liquidity and Asset Pricing. Boston: Now Publishers Inc. (2006)

Allen, F., Gale, D.: Understanding Financial Crisis. Oxford: Oxford University Press (2007)

Artzner, P., Delbaen, F., Eber, M., Heath, D.: Coherent measures of risk. Math Financ 9, 203–228 (1999)

Bielecki, T., Cialenco, I., Zhang, Z.: Dynamic Coherent Acceptability Indices and their Applications to Finance. arXiv:1010.4339v2[q-fin.RM] (2011)

Bion-Nadal, J.: Bid-ask dynamic pricing in financial markets with transactions costs and liquidity risk. J Math Econ 45, 738–750 (2009)

Carr, P., Geman, H., Madan, D.B., Yor, M.: The fine structure of asset returns: an empirical investigation. J Bus 75, 305–332 (2002)

Carr, P., Madan, D.B.: Markets, profits, capital, leverage and returns. J Risk 14, 95–122 (2011)

Cherny, A., Madan, D.: New measures for performance evaluation. Rev Financ Stud 22, 2571–2606 (2009)

Cherny, A., Madan, D.B.: Markets as a counterparty: an introduction to conic finance. Int J Theor Appl Financ 13, 1149–1177 (2010)

Choquet, G.: Theory of capacities. Annales de l’Institut Fourier 5, 131–295 (1954)

Cohen, S., Elliott, R.J.: A general theory of finite state backward stochastic difference equations. Stoch Process Appl 120(4), 442–466 (2010)

Davis, M.H.A., Hobson, D.G.: The range of traded option prices. Math Financ 17, 1–14 (2007)

Eberlein, E., Madan, D.B.: Unlimited liabilities, reserve capital requirements and the taxpayer put option. Quant Financ 12, 709–724 (2012)

Eberlein, E., Gehrig, T., Madan, D.B.: Accounting to acceptability: with applications to the pricing of one’s own credit risk. J Risk 15(1), 91–120 (2012)

Freixas, X., Rochet, J.-C.: The Microeconomics of Banking, 2nd edn. Boston: MIT Press (2008)

Hunt, G.: Martingales et Processus de Markov. Paris: Dunod (1966)

Jobert, A., Rogers, L.C.G.: Pricing operators and dynamic convex risk measures. Math Financ 18, 1–22 (2008)

Kunita, H.: Infinitesimal generators of nonhomogeneous convolution semigroups on lie groups. Osaka J Math 34, 233–264 (1997)

Kupper, M., Schachermayer, W.: Representation results for law invariant time consistent functions. Math Financ Econ 2, 189–210 (2009)

Kusuoka, S.: On law invariant coherent risk measures. Adv Math Econ 3, 83–95 (2001)

Madan, D.: Capital requirements, acceptable risks and profits. Quant Financ 7, 767–773 (2009)

Madan, D.B.: Joint risk neutral laws and hedging. Trans Inst Ind Eng 43, 840–850 (2010)

Madan, D.B.: On pricing contingent capital notes. In: Kijima, M., Muromachi, Y., Nakaoka, H. (eds.) Recent Advances in Financial Engineering 2011: Proceedings of the KIER-TMU International Workshop on Financial Engineering. Singapore: World Scientific (2011)

Madan, D.B.: A two price theory of financial equilibrium with risk management implications. Ann Financ 8(4), 489–505 (2012)

Madan, D.B., Schoutens, W.: Conic finance and the corporate balance sheet. Int J Theor Appl Financ 14, 587–610 (2011a)

Madan, D.B., Schoutens, W.: Conic coconuts: the pricing of contingent capital notes using conic finance. Math Financ Econ 4, 87–106 (2011b)

Madan, D.B., Schoutens, W.: Structured products equilibria in conic two price markets. Math Financ Econ 6, 37–57 (2012a)

Madan, D.B., Schoutens, W.: Tenor specific pricing. Int J Theor Appl Financ 15, 6 (2012b). doi: 10.1142/S0219024912500434

Madan, D., Seneta, E.: The variance gamma (V.G.) model for share market returns. J Bus 63, 511–524 (1990)

Madan, D., Carr, P., Chang, E.: The variance gamma process and option pricing. Eur Financ Rev 2, 79–105 (1998)

Madan, D.B., Wang, S., Heckman, P.: A Theory of Risk for Two Price Market Equilibria (2011). www.casact.org/liquidity/LRP9.1.pdf

Madan, D.B., Pistorius, M., Schoutens, W.: The valuation of structured products using Markov Chain models. Quant Financ 13(1), 125–136 (2013)

Mijatović, A., Pistorius, M.: Continuously monitored Barrier options under Markov processes. Math Financ 23(1), 1–38 (2013)

Peng, S.: Dynamically Consistent Nonlinear Evaluations and Expectations. Preprint No. 2004–1, Institute of Mathematics, Shandong University (2004). http://arxiv.org/abs/math/0501415

Peng, S.: G-Expectation, G-Brownian Motion and Related Stochastic Calculus of Itô Type (2006). arXiv:math/0601035v2 [math.PR]

Rosazza Gianin, E.: Risk measures via g-expectations. Insur Math Econ 39, 19–34 (2006)

Rosazza Gianin, E., Sgarra, C.: Acceptability Indexes Via G-Expectations: An Application to Liquidity Risk. SSRN.2027787 (2012)

Acknowledgments

Dilip Madan and Marc Yor acknowledge the support from the Humboldt foundation as Research Award Winners.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Proof that \(c(A),\) (5) is a Choquet capacity.

To show that \(c\) is a capacity we must show that

Defining

we must show that

Equivalently we have

Now

Proof that \(\mathcal{G }_{QV}(u(.,t))\le \mathcal{L }(u(.,t))\)

The operator \(\mathcal{G }_{QV}(u(.,t))\) evaluates the distorted expectation of a random variable \(Y_{x,t}\) with distribution function \(F_{x,t}(v)\) that may be written as

On the other hand the operator \(\mathcal{L }\) evaluates the expectation that may be written as

The results follows on noting that \(\Psi (u)\ge u\).

Proof of Eq. (17)

We begin by writing

where \((t_{n})\) is a sequence of subdivisions of \([0,t],\) with mesh going to zero and

For \(B\) we note that if \(u_{t}^{\prime }\) is jointly continuous

It remains to consider \(A\).

where the notation \(M\) with a superscript denotes a martingale. The second term converges to

and so the first converges to a limit we call \(M_{t}\). We wish to show that \( M_{t}\) is a martingale, but this follows from the tower property

Then for \(s<t\)

Hence the result.

Rights and permissions

About this article

Cite this article

Eberlein, E., Madan, D., Pistorius, M. et al. Two price economies in continuous time. Ann Finance 10, 71–100 (2014). https://doi.org/10.1007/s10436-013-0228-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10436-013-0228-3