Abstract

Africa is at cross-roads. On the one hand, there are opportunities. The continent possess significant renewable energy potential. The International Renewable Energy Agency estimates that modern renewable energy potential amounts to 310 gigawatts (GW). This could provide half of the continent’s total electricity generation capacity. On the other hand, there are challenges, skepticism and cautions about energy transition induced -stranded assets and debates on alternative sources of revenues beyond oil. Whilst these dynamics have received attention in the energy transition literature, there is dearth of studies on energy governance and how it can help drive the transition. Therefore, based on a desktop review, the paper seeks to examine the renewable governance systems in West Africa, and the European Union (EU). The paper shows that whilst West Africa has renewable energy potential and some level of national energy governance structures, private sector investment is limited. Lack of transparency, power sector financial challenges, overdependence on donor funding and high interest rate may account for this. Though regional and sub-regional initiatives have been implemented to overcome some of these challenges, there is more room for improvement. Indeed, unlike the EU, most of the sub-regional and regional targets appear not to be mandatory and there are limited economic instruments to attract the private sector.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction and background

Africa struggles to meet the hydra-headed challenges of energy access, affordability and reliability despite improvements in North Africa and South Africa. The story is not different in most parts of Sub-Saharan Africa where several of the people are plagued with energy poverty with low amount of energy services which hinders economic activities on the continent (Quitzow et al. 2016b). Africa has an abundance of energy resources both renewable (Quitzow et al. 2016a; IRENA 2013) and non-renewable (Carmody 2011; Ovadia 2016; Yates 2012). More so, there is ongoing oil and gas exploration and productions despite the drop-in oil prices across the globe. In addition, at the regional level, issues such as climate change and sustainable development have become relevant. In recognition of this, most African countries have signed on to a number of international conventions and protocols. Prominent among these are the Sustainable Development Goals (SDGs), the Paris Agreement (PA), the Africa Union (AU)’s Agenda 2063, Africa Clean Energy Corridor and the Economic Community of West African States (ECOWAS) Policies on Renewable Energy (RE). The Sustainable Energy Fund for Africa managed by the African Development Bank (AfDB) has been investing in new and RE sources as well.

In recognition of these opportunities and challenges, it is important to strategize to turn these RE potentials into generation, strengthen research and advocacy and deal with energy-related governance issues sustainably. Through this strategy, a balance between economic development and the protection of the climate would be established. Indeed, in recent times, the world has begun to embrace technologies of RE due to its cost-effectiveness and environmental friendliness. Clearly, the world is transitioning into a post-carbon world, making the panoramas of Africa to use carbon resources less promising (Graham & Ovadia 2019). At the same period, RE continues to gain traction across the globe with RE technologies increasing their presence in developing and emerging economies (REN212017). Nonetheless, meeting the current and future energy demand and supply on the continent is a major challenge to African countries especially those in Sub-Saharan Africa such as West Africa (Quitzow et al. 2016b). It is the least electrified in Africa.

RE has become the remedy for several failures of hydrocarbon energy or fossil fuel since it has been hailed as a more effective means for advancing economic, social and environmentally viable development agenda in both developed and developing countries (REN21 2017). It has been argued that investment in energy proficient technologies and RE technologies has the potential of increasing the employment rate by 20% by 2050, also enhancing economic growth and reductions in greenhouse emissions. But, policy provisions are needed to accomplish these transitional challenges (Rickerson 2012, p. 1).

Africa’s renewable potential is astronomical and needs to be tapped. In essence, several developing countries are heavily endowed with RE resources due to their geographical makeup or nature which is yet to be tapped (Rickerson 2012). One of the surest ways to tap into these RE potentials is through legal and institutional framework, policies and governance structure. In recent times, the United Nations Environment Programme (UNEP) has had series of conservation on freshwater (McCaffrey and Weber 2005) and RE policy (Ottinger and Bradbook 2007). It is against this background that this paper seeks to examine the renewable governance system in West Africa (WA), and the European Union (EU). It does so by comparing them, pointing to the successes and challenges that WA faces in its drive toward increasing investments in RE.

The paper is based on an analysis of secondary data. The sources of data are reports from various stakeholders such as government, civil society organizations amongst others. In addition, books, journals, reports, and online news outlets were consulted. The paper is organized as follows. "The Paris agreement (PA) and sustainable development goals (SDGs)" section looks at the Paris Agreement, SDGs amongst others. "Attracting Investment" section assesses the RE potential and invesment attraction in WA. "Renewable Energy Targets" section reviews the governance structure of RE in WA by comparing with the EU. "Governance systems" section points to governance gaps in WA by comparing with EU and Asia and "Conclusion and recommendations" section is the conclusion and recommendations.

The Paris Agreement (PA) and sustainable development goals (SDGs)

UNFCCC Paris Agreement, Article 2

-

1.

This Agreement, in enhancing the implementation of the Convention, including its objective, aims to strengthen the global response to the threat of climate change, in the context of sustainable development and efforts to eradicate poverty, including by:

-

(a)

Holding the increase in the global average temperature to well below 2.0 °C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5 °C above pre-industrial levels, recognizing that this would significantly reduce the risks and impacts of climate change.

-

(b)

Increasing the ability to adapt to the adverse impacts of climate change and foster climate resilience and low greenhouse gas emission development, in a manner that does not threaten food production; and

-

(c)

Making finance flows consistent with a pathway toward low greenhouse gas emissions and climate-resilient development.

-

2.

This Agreement will be implemented to reflect equity and the principle of common but differentiated responsibilities and respective capabilities, in the light of different national circumstances (UNFCCC 2015).

The Paris Agreement (PA) of the United Nations Framework Convention on Climate Change (UNFCCC) was signed on 12th December 2015. It deals with greenhouse-gas-emissions alleviation, adaptation and finance. The PA build upon several rich and multifarious institutional frameworks, producers and regulations which evolved over twenty-five years (1990–2015) to comprise of what is known as the UN climate regime. The fundamentals of this regime consist of the 1992 United Nations Framework Conventions on Climate Change (UNFCCC) and the Kyoto Protocol of 1997. In order to realize these two regimes, the signatories and participant created an ostentatious institutional infrastructure, and approved over 500 policy decision on numerous issues such as the creation of thorough reporting processes, promoting gender-balance initiatives and capacity building in developing countries. These meetings and negotiations ultimately produced the PA, which was the third treaty implemented under climate change from the annual sessions of the Conference of Parties (COP) with the goal of addressing the challenges of climate change across the globe (Klein et al. 2017). Klein et al. (2017) points out that several of the PA principal concepts and distinct provisions have their foundation on earlier meetings and agreement from earlier treaties.

The PA is based on conventions which brought together all nations on the same platform to combat climate change (UNFCCC 2015). The predominant aim of the PA is to fortify the international response to the dangers of global warming or climate change. The PA seeks to keep the global temperature rise below 2.0 °C which is above pre-industrial level within this century and to follow ways to limit the temperature increase (UNFCCC 2015). This agreement is made up of 29 articles. It has 189 members who have signed to it. The PA deals with greenhouse gas emission reductions from a bottom-up approach. This is done in a way where all signatory states propose mitigation measures through their various Nationally Determined Contributions (NDCs) (Stua 2017, p. 2). Nonetheless, PA is as strong as the sum of all the states actions as a result of the flexibility mechanisms built in its Article 6. These measures can only be applicable if an adequate number of state officials are willing to use these mechanisms either on the giving or receiving side (Stua 2017, p. 2).

The SDGs is a collection of 17 goals set in 2015 by the UN General Assembly with the aim of achieving them globally by 2030 (United Nations Sustainable Development Goals 2015). The SDGs 13 deals with addressing climate change and its implications. This goal is essentially linked to the other 16 goals with the agenda of attaining them by 2030. To achieve this goal, the members of the UN adopted the Paris Agreement (PA) in 2015 to limit the global temperature rise to below 2 °C. This decision was taken due to the impact that climate change was having on countries across the world.

Progress of goal 13 in 2019

-

Increasing greenhouse gas emissions are driving climate change. In 2017, greenhouse gas concentrations reached new highs, with globally averaged mole fractions of CO2 at 405.5 parts per million (ppm), up from 400.1 ppm in 2015, and at 146% of pre-industrial levels. Moving toward 2030 emission objectives compatible with the 2 °C and 1.5 °C pathways requires passing a peak emission as soon as possible, followed by rapid reductions.

-

As indicated under Sustainable Development Goal 1 during the period 1998–2017, direct global economic losses from disasters were estimated at almost US $3 trillion. Climate-related and geophysical disasters claimed an estimated 1.3 million lives.

-

As of April 2019, 185 parties had ratified the Paris Agreement. Parties to the Paris Agreement are expected to prepare, communicate and maintain successive nationally determined contributions, and 183 parties had communicated their first nationally determined contributions to the secretariat of the United Nations Framework Convention on Climate Change, while 1 party had communicated its second. Under the Agreement, all parties are required to submit new nationally determined contributions, containing revised and much more ambitious targets, by 2020.

-

Global climate finance flows increased by 17% in the period 2015–2016 compared with the period 2013–2014.

-

As of 20 May 2019, 28 countries had accessed Green Climate Fund grant financing for the formulation of national adaptation plans and other adaptation planning processes, with a value of US $75 million. Of these, 67% were for least developed countries, small island developing States and the African States. Proposals from an additional seven countries, with a value of US $17 million, are in the final stage of approval. In total, 75 countries are seeking support from the Green Climate Fund for national adaptation plans and other adaptation planning processes, with a combined value of $191 million (United Nations Economic and Social Council 2019, pp. 18–19).

On the African continent, investments in the energy sector has been noted as a priority by stakeholders, regional organizations and international non-governmental organizations. In this regard, several initiatives have been put in place with the aim of supporting the continent to achieve sustainable development and energy access for all. Examples of such initiatives include the Africa-EU Energy Partnership (AEEP), the Sustainable Energy for All (SE4ALL), the Vienna Energy, the Third International Conference on Financing for Development and many more (Quitzow et al. 2016a). In addition to the aforementioned initiatives, stakeholders mapped existing investment and regional efforts to assess strength and weaknesses and learn lessons for the effective implementation of the PA. This position was welcomed by several stakeholders leading the "mapping of existing initiative and programs". This mapping initiative is was proposed by the African Union Commission (AUC), the African Development Bank, amongst others and supported by AEEP (Quitzow et al. 2016a).

Recent studies have looked at the energy production-energy consumption-climate change relationship and discussed how to minimise energy-related emissions. This paper seeks to build upon these studies by assessing the governance framework required for the energy transition in West Africa.

Attracting Investments

Many studies have looked at assessing the potentials of RE in enhancing development in the energy sector of sub-Saharan Africa (SSA) (Hafner et al. 2019). A report published in 2015, recommends a strategy for Africa's energy transitions by focusing on RE. The report proposed 14 actions to help accelerating Africa's RE uptake by adopting investor friendly polices, legal and institutional framework to foster investment, innovative measures to attract investments and the promotion of off-grid renewable solution in order to increase access and reduce the abject poverty on the continent (IRENA 2015).

It has been estimated that the investment needed to achieve universal access by 2030 as suggested by the SDG-7 will be at an additional US $9–30 billion per year from 2010–2020 (PBL Netherlands Environmental Assessment Agency 2017). The PBL Netherlands Environmental Assessment Agency’s report mentions the important role of decentralized electrification such as mini-grid and stand-alone systems. This report further shows that RE generation will increasingly become competitive though fossil fuel will remain relevant in the future of electricity production in SSA (PBL Netherlands Environmental Assessment Agency 2017).

Renewable Energy Targets

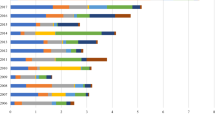

In 2013, the International Renewable Energy Agency (IRENA) performed its first assessment of the prospects for RE in the countries of the Economic Community of West African States (ECOWAS). This assessment, presented in the 2013 report of West African Power Pool: Planning and Prospects for Renewable Energy, came on the heels of two major regional policy developments—the formal adoption of the 2011/12 West African Power Pool (WAPP) Master Plan, and the ECOWAS Renewable Energy Policy (EREP), which aims to increase the share of RE in the region’s overall electricity generation mix to 23% in 2020 and 31% in 2030 (ECREEE 2013).

Regional EREP target scenario

The Regional EREP Target Scenario imposes a region-wide minimum target on the Reference Scenario in line with EREP targets. The EREP aims to increase the share of grid-connected RE in the region’s overall electricity mix (defined as the share of RE capacity as a percentage of peak load) to 35% in 2020 and 48% in 2030, which include 25% and 29% of medium-sized/large hydropower, respectively (ECREEE 2013). Figure 1 shows the RE Targets of West African Countries.

Source Author’s creation

RE targets of West African countries.

In a study by RES4Africa (2020), it was revealed that between 2009 and 2018, Africa accounted for only 2% of additional RE capacity despite the existence of individual country targets. Even so, North and South Africa accounted for 50%. The causes of this low investment can be grouped into economic and non-economic factors.

Among the economic factors that accounted for this low RE is the issue of perceived high risks environment. In addition, over dependence on Foreign Direct Investments (FDI) is another factor. Whilst FDI accounts for 6% of new RE capacity globally, it accounts for 50% in Africa (RES4Africa 2020). Whilst FDIs contribute significantly to national development, it is important to mobilize domestic sources of funding to complement these sources. Another challenge with FDI is that, it is not evenly distributed.Footnote 1 South Africa, Morocco and Egypt accounted for about 60% of the FDI flows in Africa’s RE sector over the past decade. In addition, minimal transmission infrastructure and low trading among countries affected RE investments. In West Africa where electricity trade is relatively advanced, less than 10% of electricity is traded (Cambridge University 2017, IEA 2018). Moreover, according to the World Bank (2016), the weighted average tariff in SSA is US$0.08 per kWh, with significant variations across the region. The financial gap due to under-pricing accounts for US$0.10 per kWh billed, leading to losses equivalent to 0.4% of the annual GDP. In addition to this, less than 25% of the final energy consumed in Africa goes to productive sectors (World Bank 2020). This leads to subsidized and often unpaid electricity supplied to the residential sector.

The non-economic factors include the desire to set targets with little action and funding plan. Enerdata (2020) reports that more than 8 African countries had RE targets for 2020. Despite these targets, the inclusion of non-hydro sources of RE in the energy mix has been a challenge. In Ghana for instance, despite a 10% non-hydro RE target, set in the Strategic National Energy Plan in 2006, the current level is about 2% (Ackah and Asomani 2015). Factors such as instability, poor macroeconomic conditions, minimal transparency and opaque regulatory conditions have all contributed to low investments. It has been estimated that Africa requires an average annual investment of US$70 billion from 2015 to 2030 to help in carbon-dioxide emissions reductions of up to 310 megatons per annum (IRENA 2015). These investments would require both economic and governance reforms.

Governance systems

There are four levels of governance systems concerning RE policies. These are the global RE conventions, the continental AU level ones, the sub-regional policy directives and the national targets and systems. For instance, at the sub-regional level, the ECOWAS Renewable Energy Policy stipulates that member countries shall increase the share of RE penetration including medium and large hydro to 35% by 2020 and 48% by 2030 in their energy mix. At the regional level, the AU’s Agenda 2063 calls on Africa to harness all its energy resources to ensure modern, efficient, reliable, cost-effective, renewable and environmentally friendly energy to all African households, businesses, industries and institutions, through building the national and regional energy pools and grids and energy projects.

Globally, issues such as climate change, and sustainable development have become relevant to energy sector development. In recognition of this, most West African countries have signed on to a number of international conventions and protocols. Prominent among these are the Sustainable Development Goals (SDGs), the Paris Agreement, the Africa Union (AU)’s Agenda 2063 ECOWAS White Paper on Energy Access and the ECOWAS Policies on RE. The challenge however is that countries that practice some form of democracy often govern with their manifestoes. Since most of these manifestoes, especially in West African countries, are not empirically tested, some of the promises on RE are often not linked to the national, continental or sub-regional policies. To address this challenge, a number of initiatives have been implemented at the continental or sub-regional level. One such governance structure is the Africa Renewable Energy Initiative (AREI), which is an inclusive, transformative, Africa-owned and Africa-led effort to accelerate and scale up the harnessing of the continent’s huge RE potential. Under the mandate of the African Union and endorsed by the Committee of African Heads of State and Government on Climate Change (CAHOSCC), the AREI aims achieving at least 10 GW of new and additional RE generation capacity by 2020, and at least 300 GW by 2030. The goal of the Africa Renewable Energy Initiative is to ensure universal access to clean and affordable energy to ensure sustainable development, enhanced wellbeing and fast track the rate of economic development. The AREI has two phases. In phase one, (2017–2020), activities carried out include situational analysis, assessments and other strategies for full implementation. In phase two, there will be full roll out.

In order to finance the AREI, plans are advanced to secure direct funding, through both international and African domestic means.

On the sub-regional level, the Ouagadougou Declaration, adopted at the ECOWAS Conference for Peace and Security on 12 November 2007 in Burkina Faso, articulated the need to establish a regional centre to promote RE and energy efficiency. At the 61st Session of ECOWAS Council of Ministers, held in 2008, a legal backing was given for the establishment of the ECOWAS Regional Centre for Renewable Energy and Energy Efficiency (ECREEE). It deploys a number of initiatives to achieve their mandate of universal access to energy by 2030. These commitment at the regional and sub-regional level on the African continent could be a good avenue to discipline members states who fail to fulfill their pledges.

Whilst these governance arrangements have chalked some successes, there are some challenges. First, the implementation of these initiatives are often donor dependent. This implies the selection of targets and implementation instruments may be externally driven and not based on local conditions. Indeed, Pineau (2008) has pointed out the lack of regional and local ownership in most of these initiatives. On the other hand, it is important to point out that, donor agencies have over the years served as reliable source of finance for Africa energy deficiencies. An example is the the Sustainable Energy Fund for Africa (SEFA) which is a special donor fund under the management of the African Development Bank. It provides a catalytic source of funds to facilitates private sector investments in RE and energy efficiency on the African continent. The SEFA offers technical support and concessional finance instruments to remove market barriers, build a more robust pipeline of projects and improve the risk-return profile of individual investments. The goal of SEFA is to help with the universal access to cheap, dependable, viable, and up-to-date energy services for all in Africa, in conjunction with the Energy for Africa and Sustainable Development Goal 7 (AfDB.org 2020). Additionally, such donor support or external support provided Africa with the needed skills and expertize in the energy sector. Many of these external supports have all the experience and skill in the energy sector especially in RE. It is therefore important for African leaders and authorities to collaborate with these donors to harness their skills and experiences in RE in order to attain RE sustainability and the PA goals.

Second, whilst the private sector has been looked at as a possible partner for implementation of some of these initiatives, some power distribution off takers in the sub-region are often not financially stable. Nonetheless, Okonjo-Iweala (2020) has argued that the private sector is driving Africa’s shift toward RE while state-owned enterprises (SOE) are lagging behind. It is important for African government to support reforms in the SOE in this regard.

Third, interest rates across the sub-region are very high which may discourage debt financing. Fourth, unlike the EU, most of the regional targets are not binding. Further, Karaki (2017) points out the lack of transparency and accountability in energy contracting in the sub-region and cites the West Africa Power Pool Project as an example. Eberhard et al (2011) posit that conflicts, and instability can affect the implementation of such regional initiatives. According to Chambers et al. (2012), unconfirmed reports suggest that while some delays and contract amendments may have arisen from genuine (albeit severe) underestimation of original costs and a lack of capacity among constructing agents, there were likely illicit agreements between those responsible for authorizing some of the work under the West Africa Power Pool Project and those contracted.

The European Union (EU) has put a policy directive together that creates binding obligations to all of its members with the aim of reaching the EU target of consuming 20% of its energy from of renewables by 2020. In the current climate and energy framework, the EU has committed itself to increasing its renewables share to 20% by 2020. This European target was then translated into binding national targets. To achieve this, both policy and economic instruments have been used and developed. For instance, the EU ETS and in particular had first two phases (2005–2007 and 2008–2012). As of 2013, the EU ETS abolished national target setting in favour of an EU-wide target that directly applies to the operators of installations covered by the system. Indeed, in the US for instance, 29 US states have successfully adopted Renewable Portfolio Standards (RPS) state laws that require local utilities to supply a certain percentage of the electricity they distribute from renewable sources. Some West African countries use feed-in tariff which are at times poorly designed and make RE uncompetitive.

Additionally, part of the reason African states have not been able to institute mandatory climate and energy target for its member states are, first of all, its historically negligible carbon emission. Secondly, most of them lack leadership to implement and enforce these energy targets (Okonjo-Iweala 2020). Nonetheless countries like Morocco has built the world’s largest resolute solar facility to help facilitate their goal of 52% RE mix by the end of 2030 (ibid). South Africa enacted the Carbon Act in June 2019, which places specific tariffs on greenhouse gases from fuel combustion and industrial emissions. It is projected that by 2035 the South African carbon tax may reduce their carbon emissions by 33% (Ntombela et al. 2019).

Conclusion and recommendations

Four things have been identified as key drivers in RE investments. These are the RE potential, investments to turn these potential into electricity, institutions, structures and regulations to safeguard these investments and conserve the potential and the regional harmonization of RE policies. For countries in West Africa, the RE potential is not in doubt. In addition, a number of institutions are regulating and promoting investments in RE. The missing link has been inadequate sustained investments in the sector. These have been due to weak and non-solvent power distributors in some countries, limited contract transparency and accountability, lack of regulations on off-grid RE systems, high interest rate, and at times, politicization of these investments. In order to address these challenges, regional and sub-regional initiatives have been implemented. The challenge though is the non-binding nature of some of the regional targets, and the excessive donor dependence for the implementation of these initiatives. Addressing these challenges would require bottom–up sub-regional policies, establishment of regionally funded RE investment vehicles, establishment of regional RE investment judicial processes, and the creation of incentives to attract the private sector and encourage countries to comply.

References

Ackah I, Asomani M (2015) Empirical analysis of renewable energy demand in Ghana with autometrics. Int J Energy Econ Policy 5(3):754–758

AfDB.org (2020) Sustainable energy fund for Africa. https://www.afdb.org/en/topics-and-sectors/initiatives-partnerships/sustainable-energy-fund-for-africa. Accessed 20 Aug 2020

Carmody P (2011) The new scramble for Africa. Polity Press, Cambridge

Chambers V, Foresti M, Harris D (2012) Final report: political economy of regionalism in West Africa scoping study and prioritisation. Overseas Development Institute, London

Eberhard A, Rosnes O, Shkaratan M, Vennemo H (2011) Africa’s power infrastructure: investment, integration, efficiency. The World Bank, Washington, D. C.

ECREEE (2013) ECOWAS Renewable Energy Policy (EREP) ECOWAS Centre for Renewable Energy and Energy Efficiency. http://www.ecreee.org/sites/default/files/documents/ecowas_renewable_energy_policy.pdf

Enerdata. Database. Accessed 18 Feb 2020

Graham E, Ovadia JS (2019) Oil exploration and production in Sub-Saharan Africa, 1990-present: trends and developments. Extr Ind Soc 6(2):593–609. https://doi.org/10.1016/j.exis.2019.02.001

Hafner M, Tagliapietra S, Falchetta G, Occhiali G (2019) Renewables for energy access and sustainable development in East Africa. Springer, Berlin. https://doi.org/10.1007/978-3-030-11735-1

IEA (2018) Total final consumption (TFC) by sector.https://www.iea.org/data-and-statistics?country=WEOAFRICA&fuel=Energy%2520consumption&indicator=Total%2520final%2520consumption%2520(TFC)%2520by%2520sector

IRENA (2013) Africa_renewable_future.pdf. https://www.irena.org/DocumentDownloads/Publications/Africa_renewable_future.pdf

IRENA (2015) Africa 2030: roadmap for a renewable energy future. https://irena.org/publications/2015/Oct/Africa-2030-Roadmap-for-a-Renewable-Energy-Future

Karaki K (2017) ECOWAS energy: from national interests to regional markets and energy access. ECDPM policy brief

Klein DR, Carazo MP, Doelle M, Bulmer J, Higham A (eds) (2017) The Paris Agreement on climate change: analysis and commentary. Oxford University Press, Oxford

McCaffrey SC, Weber GS (Eds.) (2005) Guidebook for policy and legislative development on conservation and sustainable use of freshwater resources. Nairobi, Kenya: United Nations Environment Programme, Environmental Law Branch. Division of Environmental Law and Conventions, United Nations Environment Programme. https://wedocs.unep.org/bitstream/handle/20.500.11822/8781/-Guidebook%2520for%2520Policy%2520and%2520Legislative%2520Development%2520on%2520Conservation%2520and%2520Sustainable%2520Use%2520of%2520Freshwater%2520Resources-2005496.pdf?sequence=2&%3BisAllowed=

Ntombela SM, Bohlmann HR, Kalaba MW (2019) Greening the South Africa’s economy could benefit the food sector: evidence from a carbon tax policy assessment. Environ Resource Econ 74(2):891–910. https://doi.org/10.1007/s10640-019-00352-9

Okonjo-Iweala N (2020) Africa can play a leading role in the fight against climate change. https://www.brookings.edu/research/africa-can-play-a-leading-role-in-the-fight-against-climate-change/. Accessed 20 Aug 2020

Ottinger R, Bradbook AJ (2007) UNEP handbook for drafting laws on energy efficiency and renewable energy resources. United Nations Environment Programme. https://www.ecolex.org/details/literature/unep-handbook-for-drafting-laws-on-energy-efficiency-and-renewable-energy-resources-mon-079714/

Ovadia JS (2016) The petro-developmental state in Africa: making oil work in Angola Nigeria and the Gulf of Guinea. Hurst & Company Ltd, London

PBL Netherlands Environmental Assessment Agency (2017) Towards universal electricity access in Sub-Saharan Africa | PBL Netherlands Environmental Assessment Agency. https://www.pbl.nl/en/publications/towards-universal-electricity-access-in-sub-saharan-africa

Pineau PO (2008) Electricity sector integration in West Africa. Energy Policy 36(1):210–223

Quitzow R, Röhrkasten S, Berchner M, Bayer B, Borbonus S, Gotchev B, Lingstädt S, Matschoss P, Peuckert J (2016a) Mapping of Energy Initiatives and Programs in Africa (p. 60). European Union Energy Initiative Partnership Dialogue Facility (EUEI PDF). https://www.euei-pdf.org/sites/default/files/field_publication_file/mapping_of_initiatives_final_report_may_2016.pdf

Quitzow R, Röhrkasten S, Jacobs D, Bayer B, Jamea EM, Waweru Y, Matschoss P (2016b) The Future of Africa’s Energy Supply (p. 80). Institute for Advanced Sustainability Studies (IASS). https://www.iass-potsdam.de/sites/default/files/files/study_march_2016_the_future_of_africas_energy_supply.pdf

REN21 (2017) Renewables 2017: global status report. https://apps.uqo.ca/LoginSigparb/LoginPourRessources.aspx?url=http://www.deslibris.ca/ID/10091341

RES4Africa (2020) Renew Africa Initiative: Advancing European Commitment to Africa’s Clean Energy Access At Scale. https://www.res4africa.org/wpcontent/uploads/2020/02/renewAfrica_PresentationCard.pdf

Rickerson W (2012) Feed-in tariffs and a policy instrument for promoting renewable energies and green economies in developing countries. United Nations Environment Programme. https://wedocs.unep.org/handle/20.500.11822/8102

Stua M (2017) From the Paris Agreement to a low-carbon bretton woods. Springer, Berlin. https://doi.org/10.1007/978-3-319-54699-5

Teske S (2019) Achieving the Paris climate agreement goals: global and regional 100% Renewable energy scenarios with non-energy GHG pathways for +1.5 °C and +2 °C. Springer, Berlin. https://doi.org/10.1007/978-3-030-05843-2

UNFCCC (2015) The Paris Agreement: UNFCCC. https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement

United Nations Economic and Social Council (2019) Special edition: progress towards the Sustainable development goals. https://sustainabledevelopment.un.org/sdg13

United Nations Sustainable Development Goals (2015) About the sustainable development goals. United Nations Sustainable Development. https://www.un.org/sustainabledevelopment/sustainable-development-goals/

World Bank (2016) Financial Viability of electricity sectors in Sub-Saharan Africa-Quasi-Fiscal deficits and hidden costs

World Bank (2020) Worldwide governance indicators. https://databank.worldbank.org/source/worldwide-governance-indicators

Yates DA (2012) The scramble for African Oil: oppression, corruption and war for control of Africa’s natural resources. Pluto Press, London

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Ackah, I., Graham, E. Meeting the targets of the Paris Agreement: an analysis of renewable energy (RE) governance systems in West Africa (WA). Clean Techn Environ Policy 23, 501–507 (2021). https://doi.org/10.1007/s10098-020-01960-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10098-020-01960-6