Abstract

Objective

To create and validate a micro-costing methodology that surgeons and hospital administrators can use to evaluate the cost of implementing innovative surgical technologies.

Methods

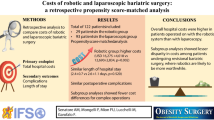

Our analysis is broken down into several elements of fixed and variable costs which are used to effectively and easily calculate the cost of surgical operations. As an example of application, we use data from 86 robot assisted gastric bypass operations made in our hospital. To validate our methodology, we discuss the cost reporting approaches used in 16 surgical publications with respect to 7 predefined criteria.

Results

Four formulas are created which allow users to import data from their health system or particular situation and derive the total cost. We have established that the robotic surgical system represents 97.53 % of our operating room’s medical device costs which amounts to $4320.11. With a mean surgery time of 303 min, personnel cost per operation amounts to $1244.73, whereas reusable instruments and disposable costs are, respectively, $1539.69 and $3629.55 per case. The literature survey demonstrates that the cost of surgery is rarely reported or emphasized, and authors who do cover this concept do so with variable methodologies which make their findings difficult to interpret.

Conclusion

Using a micro-costing methodology, it is possible to identify the cost of any new surgical procedure/technology using formulas that can be adapted to a variety of operations and healthcare systems. We hope that this paper will provide guidance for decision makers and a means for surgeons to harmonise cost reporting in the literature.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Until recently, the expense or cost of a new surgical procedure or technology in the developed countries was a secondary consideration to all parties involved: patients who were well covered by state or private insurance, hospitals, with healthy profit margins and surgeons, who were concerned with improving patient care (or marketing their services) “cost be damned”.

Recent global financial constraints have forced a shift in thinking on the part first of payers and regulatory agencies, second on the part of hospitals who are feeling pressure on their bottom line and finally, by “trickledown”, on the part of surgeons. Patients in most western countries, as of yet, have not had to face the cost issues of healthcare—though this is changing as well.

Perhaps because it was not historically needed (or required), the economics of new procedures and surgical technologies is seldom addressed in the surgical literature. When it is addressed it is usually incomplete, flawed and often biassed [5].

With no consistent metrics to measure costs comparative analysis becomes impossible [5]. This leads to complications in the decision-making process for both hospitals and physicians, especially regarding new innovative technologies.

To be fair, the economics of surgical intervention are extremely complex and not straightforward. Hospitals are complex economic environments that deal with a multitude of vendors, different levels of staff, administration and policy, etc. In most systems, there is no simple way to determine the “cost” of something.

More socialized systems have global budget funding, and granular details of expenditures are often poorly documented. Other systems, based on billing for services, have a multitude of customers and use complex cost-shifting strategies to maintain an operating profit. Still, one can create economic models that take into account the cost elements that any business would have. These can then be expressed as formulas that can use institution-specific data to calculate costs relevant to individual situations.

Health economic methodologies have continually gained importance since the introduction of Health economics as a discipline by Kenneth Arrow in 1963 [3]. Among these methods, Health Technology Assessment (HTA) is used to study and analyse the medical, social, ethical and economic aspects of adopting medical devices.

For our study, we are interested in the economic evaluation part which essentially makes reference to the cost-benefit, cost-utility, cost-effectiveness, budget impact and cost of illness techniques. It is interesting to point out that the common point between these five techniques is the cost part, the focus of our paper.

The cost analysis can be done following two approaches: macro-costing (or top-down) or micro-costing (bottom-up). The traditionally used top-down approach produces results more easily than its counter-part, but at the cost of being less precise [24]. It is with precision in mind that we chose to develop our method around a bottom-up approach.

Aim of the study

We present an attempt to develop a reproducible economic methodology that surgeons and hospital administrators can use to evaluate the cost of using innovative surgical technologies. Our analysis will provide guidance for decision makers and a mean for surgeons of harmonising cost reporting in the literature.

Method

Economic methodologies

From an economic standpoint, the distinction between cost and charge is essential for an analysis to have any utility. The cost is the price paid by the producer (hospital) for resources consumed during the production process (surgery). Charge is the price paid by the consumer (patient) needed for the institution to break even and to be solvent [17].

Furthermore, a distinction must be made between fixed versus variable and direct versus indirect costs. A cost is considered fixed if it does not vary according to the level of activity, and variable if it does [14]. A direct cost reflects the price of resources that are directly attributable to the project, whereas indirect costs are not directly attributable to the completion of the studied activity and have to be estimated using an allocation formula [1].

We follow a micro-costing approach for direct costs separated into two categories: fixed and variable. Our choice is meant to provide hospitals with detailed information on when, where, how and if they can optimize surgery cost [28].

The elements taken into account in each category include medical devices and personnel as fixed costs, whereas the variable costs encompass re-usable instruments and disposables. Note that if the personnel’s salaries were based on hourly remunerations, the personnel cost would then be considered as variable [28].

In the next subsections, we establish several formulas to calculate the cost of a surgical operating room with respect to these elements.

Fixed costs: medical devices

In today’s technology leveraged surgical practice, the initial purchase price of surgical equipment needed to perform the procedure is only part of the financial investment required. Most advanced technologies need some type of routine maintenance or upkeep which is usually covered by “maintenance/service contracts” with the company or third-party vendors.

For mechanical and software based technologies, accounting principles dictate a “life expectancy” for the device. This is based on the average replacement cycle for the technology based on mechanical failure and obsolescence. It is an indication that allows projected amortization of the purchase price and maintenance cost.

The investment cost of a new surgical technology is thus dependent on several parameters. Consider an operating room equipped with m medical devices (anaesthetic machine, monitors, endoscopy video column, etc.), we can calculate the Technology Cost (TC) per operation using the following equation [26]:

where P i , M i , E i and N i are, respectively, medical device i’s: purchase price, maintenance fee per year, life expectancy expressed in years, mean number of operations per year for which the device has been used.

The discount rate r, fixed at 2.5 % for France, reflects the time value of money. In other words, money that is available today is worth more than the same amount of money available in the future since it could be earning interest.

Fixed costs: personnel

The term “robotic” or “robot-assisted” leads the imagination to a semi-automatic operation partially conducted by a robot. In reality, a robot-assisted surgery requires as many personnel as a laparoscopic operation and results, in most cases, in an increase in operative times [16, 18]. These longer surgical operations translate into an increase in surgery cost with respect to the personnel cost which can be determined using Eq. 2. The per minute personnel cost (PC) of a number p of personnel present during surgical operations is expressed as

where W i , L i , Ewd i and t i are, respectively, personnel i’s: annual loaded salary, weekly paid working hours, effective working days per year; as in (working days—paid leave), mean time spent in surgery operations, expressed in minutes.

Variable costs: re-usable instruments

Hospitals today are faced with many management choices that affect operating costs. The choice of reusable versus disposable operating room supplies used to be clear-cut: re-usable supplies were less expensive but disposable supplies were more convenient. Today, with patient safety concerns, increasing regulations, labour costs and increasing disposable costs, this simplified view no longer holds. Both reprocessing expenses and disposable costs must be taken into account when evaluating the cost of a procedure.

Equation 3 can be used to identify the instrument cost (IC) per operation during which n re-usable instruments were needed. It takes into account the sterilisation cost for an instrument with respect to the fact that once the instrument has used up its last life then it would not require sterilisation.

where P i , E i and S i are, respectively, instrument i’s: purchase price, maximum number of uses allowed, sterilisation cost.

The additional cost (S i ) reflects the resources needed to sterilise instrument i as in labour (based on technician/nurse’s time), rinsing, disinfection, packaging and steam autoclaving [42].

Variable costs: disposables

Depending on the procedure, number of complications and other factors, various consumables (anaesthetic agent, implants, units of blood, etc.) will add to the operation cost. Integrating this element into our equation is an easy task. The challenge, however, lies in the time-consuming process of collecting such detailed data.

Hospitals that successfully manage to identify all disposables used during surgical operations need only to multiply the number of units used by their purchase price to obtain the disposable cost (DC). Mathematically, for a number d of disposables:

where N i and P i are, respectively, disposable i’s: number of units used, purchase price

Case study

For our analysis, we use the example of robot-aided laparoscopy because it is a current “hot topic” for patients and surgeons, and hospitals are feeling a great deal of pressure to make the multi-million dollar investment in this innovative technology.

Robotic surgery and its history

Advances in robotic surgery started in 1985 with the introduction of “Puma 200” during a stereotactic brain surgery [24]. Further development in the following years saw the introduction of “PROBOT” [11], “ROBODOC” [10], “AESOP” [35], “ZEUS” [34] and finally, the da Vinci® Surgical System in 2000 [4].

The distribution of the da Vinci® Surgical Systems was approved by the US Food and Drug Administration (FDA) in 2001 [21]. Today, they are being used in various specialities among which: Head&Neck, Colorectal, General Surgery, Gynaecology, Cardiac, Thoracic and Urology.

The latest of the series, da Vinci® SI, is composed of four elements [22]: Surgeon console, patient-side cart, surgical instruments and a 3D HD vision system.

The console allows the surgeon to operate while being seated, viewing a high-definition 3D image of the surgical field. His hand movements are transmitted from the master controls situated at the console to the 4 robotic arms that are part of the patient-side cart.

The vision system is equipped with a high-definition 3D endoscope and image processing equipment that provide the entire operating room (OR) team with a view of the operating field on a large monitor. Through this system, we can observe the surgical instruments’ movements among which many follow a design with seven degrees of motion.

Cost of robot-assisted surgery

We seek to validate our estimation model by applying our formulas to 86 Gastric Bypass operations performed between 02/01/2012 and 17/12/2012 at Strasbourg’s University Hospital. All the analyses have been made using the free open source statistical environment R [33], with which we created an automated user friendly micro-costing analysis code.

Details over instrument costs and operative times were provided by the Image-Guided Minimally Invasive Surgical Institute of Strasbourg (IHU Strasbourg), whereas personnel and medical devices’ costs were retrieved from Strasbourg’s University Hospital.

The chosen room for the analysis is equipped with several medical devices that are common to 528 operations made during 2012. For the IHU’s da Vinci® Si System, we amortize the purchase (1.8 M) and maintenance (135 k) costs over 147 operations during which the robot was used, all procedures taken into account.

We consider 86 typical gastric bypass operations that start off with a coelioscopic phase to prepare the patient, followed by a robot-assisted phase to perform the jejunojejunal (JJ) and/or gastrojejunal (GJ) anastomosis and a second coelioscopic phase to finish the operation. The mean operating room occupation time was determined to be 303 min.

For illustration purpose, we provide details on what is included in each element:

-

Medical Devices: Robotic system, endoscopy column, operating table, surgical lights, surgical pendant, syringe pumps, ceiling supply unit, anaesthetic machine, electrosurgical unit, monitors

-

Personnel: Surgeon, interns, circulator, scrub, anaesthetist doctor, anaesthetist nurse

-

Re-usables: Bowel grasper, 5-mm needle driver, monopolar curved scissors, fenestrated bipolar forceps

-

Disposables: Drapes, tip covers, canula seals, needles, antiseptic, electric bistoury, urine collector, endoGIA stapler/recharges, gloves, syringe, etc.

Due to lack of data, we had to base our analysis on several assumptions. We list those in an attempt to minimize their impact on our methodology:

-

Past their life expectancy, medical devices have a null value

-

Medical devices’ maintenance fees are fixed

-

Hospitals should consider investing in a new surgical robot when volumes exceed 400 robot-assisted operations per yearFootnote 1

Most of our results are based on European prices (taxes included) to which we apply an exchange rate of 1€ = 1.3345$.

Table 1 presents the total cost per operation for the 86 robot-assisted Gastric Bypass with regard to each element of the fixed, variable costs.

The amortized value of the medical devices amounts to a total of $4320.11, inclusive of taxes, per operation. Considering that the da Vinci® Si System was only used in a total of 147 operations, its amortization value amounts to $4213.32 which represents 97.52 % of all Medical Devices’ cost.

By determining the mean duration each personnel spends in the operating room, we are able to integrate the total payroll costs data provided by our hospital into Eq. 2. With a mean occupation time of 303 min, we determine a per minute personnel cost of $4.11.

The cost of re-usable instruments, tax excluded, sums up to $1458.56. However, we must take into account that we did not perform fully robot-assisted operations, and it is thus likely that some robotic instruments were not needed or were replaced by traditional laparoscopic instruments.

While the disposables’ cost accounts for 34 % of the total cost per operation, we have little control over it. This value can vary greatly from one procedure type to another especially if implants are needed or if complications occur. However, we can try to manage it by limiting wastefulness and preferring basic over new high-technology disposable instruments with the same functionality.

Discussion

Literature review

Worldwide, cost is rapidly becoming one of the most important metrics in surgical care. As medical costs consume increasing proportions of national economies, the dramatic, undeniable and almost totally technology leveraged, improvements in surgical care are earning critical scrutiny if not criticism for their costliness. “Is it worth it?” is a question that surgeons and hospital directors never had to answer in the past but now have to respond to routinely.

Robotic surgery has occasioned a great deal of excitement on the part of surgeons (attracted by its ergonomics and marketability) and patients, who are attracted by its futuristic implications of superiority over traditional surgery. However, from an economic standpoint, robotic laparoscopy definitely deserves an extensive cost-effectiveness analysis as it requires a massive financial investment and, to date, has shown little if any clinical benefit over traditional laparoscopic or even open surgical approaches.

To backup the usefulness of our methodology, we assessed the cost approaches used in the surgical literature for robotic surgery through a Pubmed search using the Mesh terms (“Surgery, Computer-Assisted”[Mesh] OR “Robotics”[Mesh]) AND “Costs and Cost Analysis”[Mesh] for Prostatectomy, Cystectomy, Hysterectomy, Gastric bypass and Fundoplication. We manually selected the 19 most relevant articlesFootnote 2 to our study, which we analysed with respect to the following criteria:

-

Cost, not charge, data are used

-

Operating room costs can be calculated separately from hospital admission and exams

-

Medical devices’ (Robot included) cost and maintenance are taken into account

-

Personnel cost is identified

-

Re-usable instruments’ costs are calculated (with sterilisation)

-

Disposables’ costs are reported (with anaesthetic agent)

Six papers [19, 31, 32, 39–41] did not meet the first two criteria, making the operating room cost analysis, separately from the hospitals’, impossible. For an economist, the segmentation of costs is essential for analysing the cost-effectiveness of decisions or policies. Considering that policies affecting the operating room also indirectly affect the rest of the hospital, decision makers should have the correct tools to reallocate resources from one segment to another depending on the desired direct and indirect effects.

Out of the 13 remaining articles, the robot’s purchase and maintenance costs were only accounted for in seven [6, 9, 15, 25–27, 37]. Published articles that do not take these costs into account [8, 12, 13, 23, 30, 36], even if the robot was a donation, introduce a significant bias in the surgical literature. Conclusions on cost-effectiveness ratios, or comparative analysis, either become more favourable towards adopting the new technology or lack in evidence for any reliable decision.

None of the articles took into account medical devices that are shared among different specialities (monitors, surgical pendant, etc.). Sarlos et al. [36], and Huben et al. [23] did not consider the cost of any medical device, whether shared or not. The introduction of new technologies render other ones obsolete, and the changes that are thus incurred affect both shared and procedure-specific devices. If we are to identify these changes, our cost analysis must cover the entire operating room without making exceptions.

Three articles [15, 26, 37] demonstrated an intriguing variability in calculating personnel cost. While Smith et al. [37] took into account OR personnel and excluded surgeon fee, Lee et al. [26] only took the latter into account. El nakadi et al. [15] preferred to include only the OR nurse cost. Two articles [9, 23] did not take into consideration the personnel cost at all. While all other direct expenses are determined as a per operation expense, the personnel cost defines the cost per minute of the operating room. This element is essential if surgeons wish to identify the cost of an additional minute of operation.

Further variability is observable in the study by Dennis et al. [13] which, even though only considered the cost of the anaesthesia machine in the medical devices’ category, was the only article to fully integrate the cost of re-usable instruments and disposables with the sterilisation and anaesthetic agent costs taken into account. It was also the only article to provide the cost of the entire OR personnel.

Costi et al. [9] took into account the cost of medical devices, re-usable and disposable instruments only incompletely, whereas Bolenz et al. [6] took partial consideration of each criterion.

The current peer reviewed literature is clearly weak regarding robotic surgery outcomes, particularly in the cost-effectiveness field. When cost is reported in the surgical literature it is frequently done in a haphazard and non-rigorous way. Due to missing information on what is included in each calculation, we were neither able to compare results nor use weighted scoring methods, for the weight of each cost vary from one procedure to another. Nonetheless, our survey clearly indicates the need for a harmonised analysis method.

Generalizing results

The French National Authority for Health (HAS) provides recommendations on how medico-economic evaluations should be conducted. In their 2011 guide on the methodology choice [20], the HAS explicitly recommends the use of micro-costing analysis for innovative technologies, specifically those for which a reimbursement price has not been determined.

Hospitals that wish to acquire such new surgical technologies must base their decision on plausible estimations of both benefits and costs. Depending on the point of view from which they conduct their analysis, the method and information they extract are very likely to be different. Charge data should be used when conducting an analysis from a patient’s point of view, and the information we thus extract will reflect the patient’s, or payer’s, behaviour. When using cost data, the conclusions will serve as guidance for the hospital and surgeons.

We positioned ourselves from the hospital’s point of view. Our formulas provide a mean for estimating the cost per operation by taking into account all changes that would affect the operating room, with regard to the predicted number of operations and surgery time.

In our example, the amount of resources necessary to acquire a da Vinci® Si Surgical System ranges from $1.0 M to $2.3 M, with a yearly maintenance cost of around $100 K to $170 K (Intuitive Surgical Investor Presentation Q1 2013).

Published studies focused on robot-assisted surgery either choose to amortize the purchasing price over 5 years [7, 15, 29, 37] or 7 years [6, 19, 27, 38]. The choice mainly seems to depend on the hospital’s policy for medical devices’ amortization with no consensus over the life expectancy of the surgical system.

The importance of determining the life expectancy of surgical systems and surgical instruments should be emphasized. Tools that are used beyond their life expectancy tend to give the impression that their investment is more profitable. However, from an economic standpoint, this situation does not necessarily represent a smart move.

Past their life expectancy, machines tend to require additional maintenance and encounter failures more often. The impact of the former in terms of cost is straightforward. The latter directly influences the probability of complications for the patient during surgical operations and, in turn, increases the risk of lawsuit, financial loss and harming the surgeon’s or their hospital’s reputation. The incremental economic benefit is thus exponentially decreasing with each use beyond the device’s life expectancy.

To justify the choice of investing in a new technology, hospitals ought to present reasonable arguments that are adapted to their situation. This can be done through both break-even and budget impact analyses. It is more convenient, for example, for business institutions to acquire technologies with low fixed costs for, in case of low activity, the losses would be limited. However, for high volumes of activity, it is more advantageous for a company to invest in technologies with low variable costs to increase the return on investment in the long term.

In other words, hospitals that estimate their activity to be higher than the level needed to reach the break-even point should focus primarily on controlling their variable costs. If the activity is estimated to be lower, then decreasing the fixed costs should be the primary concern.

We present a few illustrative figures using Eq. 1 using the da Vinci® Surgical System. We base our calculations on an optimistic assumption of 400 robot-assisted operations and a 7 years life expectancy which allows us to identify the lowest possible amortization values of the purchase and maintenance expenses, per operation, of the surgical system.

Following our assumption and according to Table 2, hospitals would have to charge their patients $558.78 to $1164.21 per operation to cover the initial purchase and maintenance costs, i.e. reach the break-even point, of the da Vinci® Surgical System alone.

For a fixed purchase price, we are able to calculate the investment’s amortization for, respectively, 100, 200 and 300 operations per year (Example Table 3).

As Table 3 indicates, the cost per operation is highly sensible to the volume of the hospital’s activity. To add, the incremental effect on amortization tends to decrease as the volume of activity becomes higher. Investing in technologies with a high fixed cost is thus equivalent to taking higher risks.

To illustrate, consider a fixed reimbursement amount of $1676.34 per operation based on an estimation of 200 operations per year (Table 3). Hospitals that end up with 125 operations, for example, would make a total yearly net loss of (200 − 125)*1676.34 = 125723.25$ from the robot investment alone. With that mindset, hospitals with small activity will be unable to invest in expensive, but potentially breakthrough, technologies unless they are risk-loving. If so, they will have a clear incentive to increase surgical volume and control costs instead of emphasizing quality.

A system where Hospitals prioritize quantity over quality is unsustainable and will eventually lead to a degradation of the healthcare system. As Arrow [3] points out, the special characteristics of the medical-care market emphasize the role of trust between physicians and patients. Charges, which are borne by the consumer/payer, that fail to be correctly justified will eventually lead to a negative impact on hospital-patient or hospital-insurance company relationship.

As with the medical devices, re-usable instruments also have a life expectancy. More precisely, they have a maximum number of uses beyond which the overall risk is higher for patients, surgeons and hospitals.

In the case of Intuitive Surgical, the da Vinci® Surgical System is programmed to block the installation of its instruments after a specific number of uses pre-determined by the manufacturer. The most basic instruments are limited to a maximum of 10 uses (EndoWrist® Instrument & Accessory Catalogue, January 2013). After installing the instrument for the 10th time onto the robot’s arm, the system will refuse any further installations even if the instrument is still technically reusable.

The manufacturer has made a positive contribution towards protecting their patients by limiting the use of surgical instruments. Laparoscopic instruments that were used until they break, frequently during surgical operations and causing complications, are now replaced more often.

However, one might question whether the lower probability of complications is worth the added cost per use, and whether the current limit of 10 uses for some robotic instruments, 20 for others, is justified. To be able to provide an answer, an analysis of the complications’ cost should be made along with a calculation of the probability of having laparoscopic surgical instruments break and cause complications. We should then seek to compare the product of these two values with the difference in the cost per use of the laparoscopic instrument and its robotic alternative. Due to the lack of data, we are currently unable to conduct such a study.

In their 2013 catalogue, Intuitive Surgical provides an EndoWrist® Instrument Application Matrix with recommendations on which instruments to use for five surgical specialities and the associated procedures (Table 4): Urology (1, 2, 3), Gynaecology (4, 5, 6), Cardiothoracic (7, 8, 9), General (10, 11, 12) and Paediatric (13, 14).

Based on experts’ reviews of this list, we make the assumption that when a surgeon is faced with a choice between two instruments that fill the same role, he would choose the cheapest one. We also assume that instruments designated as supplementary are not mandatory, and thus can be omitted from the calculation. This allows us to identify the minimum instrument cost per procedure as recommended by Intuitive Surgical (Table 4).

Other things being equal, the cardiac revascularization procedures are ranked as the most expensive with a total instruments cost per operation of $3890.67. This high value is explained by the high number of recommended instruments among which the Endowrist® stabilizer that costs $1276.81 per use.

The low anterior resections are, by far, the least expensive procedures with an instrument cost of $964.02. However, we should note that the price of disposable accessories, which can prove very high, needed for some re-usable instruments are not considered in this section.

Out of the 42 EndoWrist® Instruments, 8 require additional investment in the form of disposable accessories. For example, the Harmonic ACE® Curved Shears 8 mm costs $1755.62 can be used 20 times ($87.78 per use) but requires a disposable insert that costs $686.28 per unit which sums up to $774.06 per use. The same applies to the Endowrist® Stabilizer ($1276.81 per use) which requires the Clearfield® ($497.95 per unit) and CardioVac® ($446.88 per unit) disposable tubings.

Limits of the methodology

Operations occurring in a traditional hospital operating room are considered to be the most costly activities of the healthcare system. This is due to the extensive facility modifications required for a sterile environment, the large ancillary labour force needed to conduct high risk interventions in a safe and effective manner, and increasingly, the high cost of the enabling technology needed for the procedure. All these elements can be distilled into an institution-specific per minute or per operation cost for using the operating room—and any supplementary technology would be added on to this baseline “overhead”.

Traditionally, a micro-costing methodology would include both direct and indirect costs. We chose not to include the indirect element in this particular case study because it requires an extensive knowledge of the hospital’s activity and organisation. As such, indirect costs are hard for surgeons to obtain unless the hospital collaborates. Note however, that when comparing the cost of two surgical techniques, the overhead cost will often be the same if the same calculation method is used and can thus be left out in a comparative analysis study.

By necessity, much of our formulas are based on assumptions that were made based either on actual data from robotic centres including our own, or as provided by Intuitive Surgical or on literature review and expert opinion. Still, any data based on opinion may be flawed and corrupt to some extent.

Due to data unavailability, the sterilisation cost was determined through a literature survey. In our search, Apelgre et al. [2] were the only authors to address this issue in detail. By considering the time and resources needed for cleaning, sterilisation and packaging of reusable instruments, they determined a total cost of ($0.80) per instrument per case.

We have deliberately forgone the opportunity cost, which requires an extensive investigation of the benefits provided by the studied technology and its alternatives, for this analysis goes beyond the purpose of our current objective.

Even though we do not address the issue of benefits in this article, we would like to point out the necessity of covering that part of the analysis. Focusing solely on cost could pose a threat to the development of innovation, especially in the early stages of adoption, as it could lead to simple “cost-cutting” without regard to the potential long-term benefits of the technology. Therefore, any discussion of costs implies the need to consider an analysis of the “benefits” or the “return on investment”.

Nevertheless, the analyst will face several challenges when analysing the benefits of an innovative surgical technology as some are hard to discern, especially when capturing the financial benefit of intangible factors.

In spite of these weaknesses in our study, we feel that compared to the variable approaches used in most of the cost peer-reviewed literature, our approach has a sound economic foundation and is supported by the real-life examples we used.

Conclusion

In the past, “surgeons love it and patients want it…” was all that was required to drive a new technology into hospital practice; today however, costs must be justified by the economics of improved patient outcomes. To do so, one must begin with a precise measurement of the procedure’s cost.

We present the components of a surgical cost analysis and seek to validate our formulas with the example of da Vinci robot-assisted laparoscopic surgery. Using micro-costing methodologies, we show that it is possible to identify the cost of any new surgical procedure/technology using formulas that can be adapted to a variety of operations and healthcare systems.

The presentation of our methodology in a formulaic format is intended to make it applicable to different healthcare systems by allowing them to adjust input variables according to their real-life data and to skip elements of the calculation if they don’t apply. It is intended to provide a concise way of harmonising the literature regarding surgery costs as to improve the possibilities of comparative analysis.

We hope this paper and the formulas we develop will provide a new, consistent format for the evaluation of the cost of new surgical technologies like robotics and be of help to institutions and physicians who are considering investing in new technology-enabled surgical procedures.

In future work, we will be extending our methodology to the “benefit” half of the equation. Recognizing that even if a technology is more costly to use, it can be worth it if there is sufficient patient and social benefits.

Notes

Based on an expert's feedback and supported by Intuitive Surgical's recommendations.

We excluded articles that only analyse the cost of complications and those for which we did not have access to.

References

AACE R International (2013) Recommended practice no. 10s-90: cost engineering terminology, 38, 54

Apelgren KN, Blank ML, Slomski CA, Hadjis NS (1994) Reusable instruments are more cost-effective than disposable instruments for laparoscopic cholecystectomy. Surg Endosc 8:32–34

Arrow KJ (2004) Uncertainty and the welfare economics of medical care. 1963. Bull World Health Organ 82:141–149

Autschbach R, Onnasch JF, Falk V, Walther T, Krüger M, Schilling LO, Mohr FW (2000) The leipzig experience with robotic valve surgery. J Card Surg 15:82–87. doi:10.1111/j.1540-8191.2000.tb00447.x1

Bailey JG, Hayden JA, Davis PJB, Liu RY, Haardt D, Ellsmere J (2013) Robotic versus laparoscopic Roux-en-Y gastric bypass (RYGB) in obese adults ages 18 to 65 years: a systematic review and economic analysis. Surg Endosc 28:414–426. doi:10.1007/s00464-013-3217-8

Bolenz C, Gupta A, Hotze T, Ho R, Cadeddu JA, Roehrborn CG, Lotan Y (2010) Cost comparison of robotic, laparoscopic, and open radical prostatectomy for prostate cancer. Eur Urol 57:453–458. doi:10.1016/j.eururo.2009.11.008

Breitenstein S, Nocito A, Puhan M, Held U, Weber M, Clavien P-A (2008) Robotic-assisted versus laparoscopic cholecystectomy. Ann Surg 247:987–993. doi:10.1097/SLA.0b013e318172501f

Broome JTPS (2012) Expense of robotic thyroidectomy: a cost analysis at a single institution. Arch Surg 147:1102–1106. doi:10.1001/archsurg.2012.1870

Costi R, Himpens J, Bruyns J, Cadière GB (2003) Robotic fundoplication: from theoretic advantages to real problems. J Am Coll Surg 197:500–507. doi:10.1016/S1072-7515(03)00479-4

Cowley G (1992) Introducing ‘Robodoc’. Newsweek 120:86

Davies BL, Hibberd RD, Ng WS, Timoney AG, Wickham JE (1991) The development of a surgeon robot for prostatectomies. Proc Inst Mech Eng H 205:35–38

Delaney CP, Senagore AJ, Fazio VW (2003) Comparison of robotically performed and traditional laparoscopic colorectal surgery. Dis Colon Rectum 46:1633–1639

Dennis T, de Mendonça C, Phalippou J, Collinet P, Boulanger L, Weingertner F, Leblanc E, Narducci F (2012) Study of surplus cost of robotic assistance for radical hysterectomy, versus laparotomy and standard laparoscopy. Gynécol Obstét Fertil 40:77–83

Drummond MF, Sculpher MJ, Torrance GW, O’Brien BJ, Stoddart GL (2005) Methods for the economic evaluation of health care programmes, 3rd edn. Oxford University Press, USA

El Nakadi I, Mélot C, Closset J, De Moor V, Bétroune K, Feron P, Lingier P, Gelin M (2006) Evaluation of da Vinci Nissen fundoplication clinical results and cost minimization. World J Surg 30:1050–1054. doi:10.1007/s00268-005-7950-6

Ficarra V, Novara G, Artibani W, Cestari A, Galfano A, Graefen M, Guazzoni G, Guillonneau B, Menon M, Montorsi F, Patel V, Rassweiler J, Van Poppel H (2009) Retropubic, laparoscopic, and robot-assisted radical prostatectomy: a systematic review and cumulative analysis of comparative studies. Eur Urol 55:1037–1063. doi:10.1016/j.eururo.2009.01.036

Finkler SA (1982) The distinction between cost and charges. Ann Intern Med 96:102–109

Fourman MM, Saber AA (2012) Robotic bariatric surgery: a systematic review. Surg Obes Relat Dis 8:483–488. doi:10.1016/j.soard.2012.02.012

Hagen ME, Pugin F, Chassot G, Huber O, Buchs N, Iranmanesh P, Morel P (2012) Reducing cost of surgery by avoiding complications: the model of robotic Roux-en-Y gastric bypass. Obes Surg 22:52–61. doi:10.1007/s11695-011-0422-1

Haute Autorité de Santé (2011), Choix méthodologiques pour l’évaluation économique à la has.

http://www.accessdata.fda.gv/scripts/cdrh/cfdcs/cfpmn/pmn.cfm?ID=2016. Accessed 31 May 2013

http://www.intuitivesurgical.cm/prducts/davinci_surgical_system/. Accessed 31 May 2013

Hubens G, Balliu L, Ruppert M, Gypen B, Tu T, Vaneerdeweg W (2007) Roux-en-Y gastric bypass procedure performed with the da Vinci robot system: is it worth it? Surg Endosc 22:1690–1696. doi:10.1007/s00464-007-9698-6

Kwoh YS, Hou J, Jonckheere EA, Hayati S (1988) A robot with improved absolute positioning accuracy for CT guided stereotactic brain surgery. IEEE Trans Biomed Eng 35:153–160

Lau S, Vaknin Z, Ramana-Kumar AV, Halliday D, Franco EL, Gotlieb WH (2012) Outcomes and cost comparisons after introducing a robotics program for endometrial cancer surgery. Obstet Gynecol 119:717–724. doi:10.1097/AOG.0b013e31824c0956

Lee R, Ng CK, Shariat SF, Borkina A, Guimento R, Brumit KF, Scherr DS (2011) The economics of robotic cystectomy: cost comparison of open versus robotic cystectomy. BJU Int 108:1886–1892. doi:10.1111/j.1464-410X.2011.10114.x

Lotan Y, Cadeddu JA, Gettman MT (2004) The new economics of radical prostatectomy: cost comparison of open, laparoscopic, and robot-assisted technique. J Urol 172:1431–1435. doi:10.1097/01.ju.0000139714.09832.47

Macario A (2010) What does one minute of operating room time cost? J Clin Anesth 22:233–236. doi:10.1016/j.jclinane.2010.02.003

Morgan JA, Thornton BA, Peacock JC, Hollingsworth KW, Smith CR, Oz MC, Argenziano M (2005) Does robotic technology make minimally invasive cardiac surgery too expensive? A hospital cost analysis of robotic and conventional techniques. J Card Surg 20:246–251

Morino M, Pellegrino L, Giaccone C, Garrone C, Rebecchi F (2006) Randomized clinical trial of robot-assisted versus laparoscopic Nissen fundoplication. Br J Surg 93:553–558. doi:10.1002/bjs.5325

Park CW, Lam ECF, Walsh TM, Karimoto M, Ma AT, Koo M, Hammill C, Murayama K, Lorenzo CSF, Bueno R (2011) Robotic-assisted Roux-en-Y gastric bypass performed in a community hospital setting: the future of bariatric surgery? Surg Endosc 25:3312–3321. doi:10.1007/s00464-011-1714-1

Pasic RP, Rizzo JA, Fang H, Ross S, Moore M, Gunnarsson C (2010) Comparing robot-assisted with conventional laparoscopic hysterectomy: impact on cost and clinical outcomes. J Minimally Invasive Gynecol 17:730–738. doi:10.1016/j.jmig.2010.06.009

R Development Core Team (2011) R: a language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0

Reichenspurner H, Damiano RJ, Mack M, Boehm DH, Gulbins H, Detter C, Meiser B, Ellgass R, Reichart B (1999) Use of the voice-controlled and computer-assisted surgical system ZEUS for endoscopic coronary artery bypass grafting. J Thorac Cardiovasc Surg 118:11–16

Sackier JM, Wang Y (1994) Robotically assisted laparoscopic surgery. From concept to development. Surg Endosc 8:63–66

Sarlos D, Kots L, Stevanovic N, Schaer G (2010) Robotic hysterectomy versus conventional laparoscopic hysterectomy: Outcome and cost analyses of a matched case–control study. Eur J Obstet Gynecol Reprod Biol 150:92–96. doi:10.1016/j.ejogrb.2010.02.012

Smith A, Kurpad R, Lal A, Nielsen M, Wallen EM, Pruthi RS (2010) Cost analysis of robotic versus open radical cystectomy for bladder cancer. J Urol 183:505–509. doi:10.1016/j.juro.2009.09.081

Van Dam P, Hauspy J, Verkinderen L, Trinh XB, van Dam P-J, Van Looy L, Dirix L (2011) Are costs of robot-assisted surgery warranted for gynecological procedures? Obstet Gynecol Int 2011:1–6. doi:10.1155/2011/973830

Venkat P, Chen L-M, Young-Lin N, Kiet TK, Young G, Amatori D, Dasverma B, Yu X, Kapp DS, Chan JK (2012) An economic analysis of robotic versus laparoscopic surgery for endometrial cancer: costs, charges and reimbursements to hospitals and professionals. Gynecol Oncol 125:237–240. doi:10.1016/j.ygyno.2011.11.036

Wright JDAC (2013) Robotically assisted vs laparoscopic hysterectomy among women with benign gynecologic disease. JAMA 309:689–698. doi:10.1001/jama.2013.186

Wright KN, Jonsdottir GM, Jorgensen S, Shah N, Einarsson JI (2012) Costs and outcomes of abdominal, vaginal, laparoscopic and robotic hysterectomies. JSLS 16:519–524. doi:10.4293/108680812X13462882736736

Yung E, Gagner M, Pomp A, Dakin G, Milone L, Strain G (2010) Cost comparison of reusable and single-use ultrasonic shears for laparoscopic bariatric surgery. Obes Surg 20:512–518. doi:10.1007/s11695-008-9723-4

Disclosure

Imad Ismail, Sandrine Wolff, Agnes Gronfier, Didier Mutter, Lee L. Swantröm have no conflicts of interest or financial ties to disclose.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Demonstration: medical devices

Objective:

-

TCi = Cost per operation of medical device i’s purchase and maintenance costs.

Let

-

P i = purchase price

-

M i = maintenance fee per year

-

E i = life expectancy expressed in years

-

N i = mean number of operations per year for which medical device has been used

-

r = discount rate

By summing the Purchase cost and Maintenance cost per operation:

Demonstration: medical devices

Objective:

-

PCi = Personnel i’s cost per operation

Let

-

W i = Annual loaded salary

-

L i = Weekly paid working hours

-

t i = Mean time spent in operations, expressed in minutes

$${\text{Monthly}}\;{\text{loaded}}\;{\text{salary}}\,{ = }\,{\frac{{W_{i} }}{ 1 2}}$$$${\text{Weekly}}\;{\text{paid}}\;{\text{working}}\;{\text{minutes}}\, = \,{L_{i} \times 6 0}$$$${\text{Effective}}\;{\text{working}}\;{\text{days}}\;{\text{per}}\;{\text{month}}\, = \,{\frac{{{\text{Effective}}\;{\text{working}}\;{\text{days}}\;{\text{per}}\;{\text{year}}}}{ 1 2} = \frac{{\left( {{\text{working}}\;{\text{days}}\;{\text{per}}\;{\text{year}} - {\text{Paid}}\;{\text{leave}}} \right)}}{ 1 2}}$$$${\text{Effective working weeks per month }} = \,{\frac{{{\text{Effective}}\;{\text{working}}\;{\text{days}}\;{\text{per}}\;{\text{month}}}}{ 5} = \frac{{\left( {{\text{Working}}\;{\text{days}}\;{\text{per}}\;{\text{year}} - {\text{Paid}}\;{\text{leave}}} \right)}}{{\left( { 1 2\times 5} \right)}}}$$$$\begin{aligned} {\text{Effective}}\;{\text{working}}\;{\text{minutes}}\;{\text{per}}\;{\text{month}} \\ & \quad {\text{ = Weekly}}\;{\text{paid}}\;{\text{working}}\;{\text{minutes}} \times {\text{effective}}\;{\text{working}}\;{\text{weeks}}\;{\text{per}}\;{\text{month}} \\ & \quad = \left( {L_{i} \times 6 0} \right) \times \frac{{\left( {{\text{working}}\;{\text{days}}\;{\text{per}}\;{\text{year}} - {\text{Paid}}\;{\text{leave}}} \right)}}{ 6 0} \\ & \quad = L_{i} \times \left( {{\text{Effective}}\;{\text{working}}\;{\text{days}}\;{\text{per}}\;{\text{year}}} \right) \\ \end{aligned}$$

Cost per minute of personnel i × Minutes personnel i spent in operation j:

Rights and permissions

About this article

Cite this article

Ismail, I., Wolff, S., Gronfier, A. et al. A cost evaluation methodology for surgical technologies. Surg Endosc 29, 2423–2432 (2015). https://doi.org/10.1007/s00464-014-3929-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00464-014-3929-4