Abstract

In this paper, we show that it may be optimal for individuals to educate more and retire earlier when life expectancy increases. This result reconciles the findings of Hazan (Econometrica 77:1829–1863, 2009) with theory. Further, the paper contributes to a better understanding of the conflicting empirical findings on the causal effect on income per capita from increased life expectancy.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

The theoretical literature on individuals’ education decisions, initiated by the seminal work of Ben-Porath (1967), shares the conclusion that increasing life expectancy induces more schooling. The intuitive reasoning goes as follows: A longer (expected) working life, where the benefits from education are reaped, induces individuals to invest more in their human capital. This Ben-Porath mechanism implies that optimal schooling time increases if and only if lifetime working hours increase.

The consensus in the theoretical literature on schooling and life expectancy is, however, not reflected in the empirical counterpart. Accordingly, whether life expectancy has a positive effect on schooling and thereby on income per capita is highly debated.Footnote 1 A recent contribution in this debate is Hazan (2009). He shows that expected lifetime working hours declined in a period of increasing life expectancy because individuals decreased their lifetime labor supply. This leads him to conclude that the Ben-Porath mechanism was not a causal factor of the observed rise in education over the last centuries.Footnote 2

We argue that the description of the incentives behind the Ben-Porath mechanism, which is that individuals choose schooling time only with the purpose of maximizing the present value of lifetime earnings, delivers a knife-edge result relying crucially on an assumption of access to perfect financial markets. By relaxing this assumption, we show that individuals’ optimal response to increased life expectancy may be to increase schooling time and, at the same time, decrease future working hours where the schooling investments pay off in terms of a higher hourly wage rate.

The purpose of the present paper is therefore to reconcile the empirical findings in Hazan (2009) with theory and thereby, more generally, to help explain the gap between the existing theory and the various empirical findings. We do this by using a simple three period life-cycle model in which we examine the effects of an increased probability of survival on the schooling, saving, and retirement decisions of an individual. The model is based on two assumptions about financial markets, which serve to capture realistic features of the incentive structure of the individual schooling choice.

First, our model carries the notion that more schooling time comes with the cost of less consumption during youth. Thus, in our model, a young individual is unable to smooth consumption, via the financial markets, between his schooling period and the rest of his life. By excluding borrowing as a way to finance consumption during the schooling period, our model implies that choices on schooling and the consumption path are interdependent, i.e., the separation theorem does not hold (see Kodde and Ritzen 1985). In the growth literature, this credit market imperfection approach is employed by Galor and Zeira (1993) and Galor and Moav (2004) to study the implications of income distribution on economic growth. In the present paper, the exclusion of borrowing during schooling highlights an important part of the incentive structure during youth: Spending more time in school implies a lower standard of living.Footnote 3

Second, saving behavior and thereby the consumption profile of an individual is affected by mortality risk due to absence of annuity markets. This is along the lines of Kalemli-Ozcan and Weil (2010) who also examine the affect of mortality risk on the retirement decision. Under the assumption of no annuity markets, they show that increased life expectancy, comprising less uncertainty about the age at death, may induce individuals to choose a lower retirement age. We also find this negative relationship between life expectancy and the retirement age, which is driven by a steeper consumption profile and thereby leisure profile (provided that consumption and leisure are compliments). In contrast to Kalemli-Ozcan and Weil (2010), where the consumption profile is only determined by life-cycle savings, individuals in our model also make their consumption profile steeper by spending more time in school during youth. This is due to credit market imperfections, which implies that more schooling entails a lower level of consumption in youth and a higher level of consumption in the future due to higher future earnings. We provide and explain the condition to be fulfilled for this to be optimal when individuals, at the same time, retire earlier and thereby reaping the benefits from education for a shorter period.

Cervellati and Sunde (2010) is closely related to the present paper. They show that the data do not reject that changes in mortality rates increased the benefits (increased lifetime working hours) relative to the opportunity cost (delayed entry in the labor market) of schooling. This leads to the conclusion that the empirical evidence cannot exclude life expectancy as a causal factor to the observed increase in schooling for cohorts born after 1870. We depart from their analysis by studying, theoretically, how both education and retirement decisions are affected by increased life expectancy.

The paper proceeds as follows: Section 2 describes the model and provides the main result. Section 3 discusses the perspectives of the result regarding the divided empirical literature. Section 4 offers some concluding remarks. All proofs are provided in the “Appendix.”

2 The model

Consider an individual who lives at most for three periods. In the first period, the individual is endowed with one unit of time and one unit of human capital. The unit time endowment is divided between schooling time, e, and labor supply 1 − e. When working, the individual receives a wage of w > 0.Footnote 4 Income in the first period, \(w\left[ 1-e \right]\), is used solely for first period consumption, c 1:

Equation 1 shows that individuals hold zero wealth at the end of the first period by assumption. However, choosing to hold zero wealth may be the likely outcome of optimizing behavior. First, negative wealth may be excluded by credit markets imperfections implying that individuals hold nonnegative wealth throughout life.Footnote 5 Second, when e > 0, the income in the second period is higher than the income in the first period. If individuals desire to smooth consumption, they would borrow rather than save in the first period. Alternatively, suppose that individuals live with their parents in the first period. This would imply that the opportunity cost of education becomes forgone leisure. This approach, which is used by, e.g., Glomm and Ravikumar (1992) and Zhang and Zhang (2005), would generate the same results as those presented in the present paper.

Individuals survive with certainty into the second period where they supply h units of efficient labor inelastically.Footnote 6 The wage income is divided between consumption, c 2, and savings, s > 0:

An individual’s schooling time, e, increases the level of human capital:

where h ′(e) > 0, h ″(e) < 0, and h(0) = 1.

Survival becomes uncertain at the end of the second period where \(\phi \in \left( 0,1\right) \) denotes the probability of surviving into the third period. Contingent on survival, individuals divide the unit time endowment between leisure, l, and working time, 1 − l. To facilitate the interpretation, we denote 1 − l as the retirement age. Labor market income in the third period, \(wh\left[ 1-l\right] \), together with savings with accrued interest, Rs, is used for third period consumption, c 3:Footnote 7

Since annuity markets are absent, the return to savings is unaffected by the survival probability, ϕ, i.e., individuals are not compensated with a higher interest rate when facing a lower probability of surviving (and vice versa). The absence of annuity markets implies that accidental bequests are generated by individuals dying at the end of the second period of life. Following Kalemli-Ozcan and Weil (2010), we abstract from intergenerational aspects in the form of accidental bequests.Footnote 8

The expected lifetime utility is represented by:

where ψ is an inverse measure of the taste for acquiring knowledge from education, β > 0 is a time discount factor, and θ > 0 is the (relative) taste for leisure in the third period. Standard assumptions are made about the utility functions: \(u^{\prime }\left( c_{i}\right) >0\) and \( u^{\prime \prime }\left( c_{i}\right) <0\), for i = 1,2,3 together with \( v^{\prime }\left( l\right) >0\) and \(v^{\prime \prime }\left( l\right) <0\).

The problem for each individual consists of maximizing Eq. 5 subject to Eqs. 1–4. Restricting attention to an interior solution, the first-order necessary conditions for e,s, and l are, respectively:

Combining the two first-order conditions in Eqs. 6 and 7 yields:

Equation 9 shows that the allocation of consumption matters for the schooling choice of credit constrained individuals, i.e., Fisher’s separation theorem does not apply. The sum of the two terms on the left-hand side is the marginal utility benefit of schooling. These terms reveal that lifetime uncertainty affects the education choice only from its effect on marginal utility of second period consumption, \(u^{\prime }\left( c_{2}\right) \), via Eq. 7. A rise in the probability of surviving into the third period, ϕ, induces individuals to increase the propensity to save, which tends to decrease second period consumption. In order to spread out the implied decline in consumption before the third period, individuals increase the time spent on schooling in the first period of life. Consequently, an individual may respond to an increase in life expectancy by increasing schooling time and at the same time (due to life-cycle effects of mortality) to decrease future working hours where the benefits from schooling are reaped.

If individuals, on the contrary, would have been able to smooth consumption between the first and second period, then Eq. 9 would change to:Footnote 9

In this case, the separation theorem applies and schooling is decided only with the objective of maximizing present value lifetime income. As a consequence, earlier exit from the labor market (\(\left[ 1-l\right] \) decreases) is associated with less schooling time (h e increases). Based on this conventional theoretical result, Hazan (2009) concludes that increased longevity did not induce more schooling via the Ben-Porath mechanism since he observes a decrease in lifetime working hours over the studied period. However, as we show below, the effect from the Ben-Porath mechanism may be dominated by a life-cycle effect on schooling. This indicates that the empirical finding in Hazan (2009) may, in addition to general equilibrium effects, be driven by first-order effects due to changed life-cycle behavior.

We now turn to comparative statics to show the result formally and get a better understanding of the forces behind it. To fix ideas and intuition, we start out by assuming that each individual takes the retirement age as exogenously given to show the effect on schooling from changes in life expectancy and the retirement age. Subsequently, we keep schooling time constant to focus on how the retirement choice is affected by the increase in life expectancy. Finally, we combine the results and show the overall finding.

The effect on schooling time from an increase in life expectancy is provided in the following proposition:

Proposition 1

Holding the retirement age fixed, an exogenous rise in the survival probability, ϕ, unambiguously increases schooling time, e.

Consistent with the data used in Hazan (2009), an increase in life expectancy (ϕ) implies a rectangularization of the survival curve. A rise in ϕ makes individuals attach more weight to the third period of life, and they are therefore more inclined to save. This entails more time devoted to schooling in the first period because schooling is the only instrument by which individuals can smooth consumption between the first and second period, i.e., the only way that the transfer of more resources to the third period of life can be smoothed between the first and the second period of life.

The next piece of the overall result is the relation between schooling and the retirement age. Consider an exogenous fall in the retirement age:

Proposition 2

An exogenous fall in the retirement age, 1 − l, has a nonnegative effect on schooling time, e, if the following condition holds:

where \(\sigma _{i}\equiv -\frac{u^{\prime \prime }\left( c_{i}\right) c_{i}}{u^{\prime }\left( c_{i}\right) }\) for i = 2,3.

Proposition 2 states that the relation between schooling and lifetime labor supply is in general ambiguous. This ambiguity originates from the two counteracting effects that a lower retirement age has on schooling time. On the one hand, the implied decline in lifetime working hours tends to decrease schooling time due to the standard Ben-Porath mechanism (a substitution effect). On the other hand, the schooling decision also comprises a life-cycle choice in our model. At impact, a lower labor supply decreases income in the third period (an income effect). To smooth consumption between the third and second period, individuals will increase savings. However, to smooth consumption between the first period and the rest of life, individuals must increase schooling. If condition in Eq. 11 is satisfied, the latter effect dominates the former and individuals find it optimal to spend more time in school even when the number of future working hours shrinks. If σ 2 = σ 3 = σ, the condition in Eq. 11 boils down to 1 < σ, implying that the life-cycle effect dominates the Ben-Porath mechanism.Footnote 10

The final piece of the overall result is how the retirement age is affected by life expectancy. Holding schooling time fixed gives rise to the following proposition:

Proposition 3

Holding schooling time, e , fixed, an exogenous rise in the survival probability, ϕ , unambiguously lowers the age of retirement, 1 − l.

The result stated in Proposition 3 is intuitive after noticing that the absence of annuity markets makes individuals save as if they were to live to the (constant) maximum attainable age regardless of the probability of surviving into the third period. Consequently, a higher survival probability makes individuals increase their saving propensity, which permits a lower retirement age. This effect was first shown in Kalemli-Ozcan and Weil (2010). Compared to their ambiguous result, we find an unambiguous negative effect on the retirement age from increased survival. This is simply because increased survival probability, in our model, automatically implies a lower uncertainty about reaching the constant maximum attainable age.Footnote 11

This result, together with Propositions 1 and 2, enables us to conclude that a rise in ϕ may reduce lifetime working hours and at the same time increase schooling time.

To illustrate our result, with all the variables being endogenously determined (schooling, saving, and retirement), we apply the functional forms \(u\left( c_{i}\right) =\ln \left( c_{i}\right) \) and \(v\left( l\right) =\ln \left( l\right) \) and obtain the following solutions for schooling time and leisure, respectively:

where \(\mu \equiv \frac{h^{\prime }\left( e\right) }{h}e>0\) is the constant elasticity of human capital with respect to schooling time. Equations 12 and 13 lead to the following proposition:

Proposition 4

When \(u\left( c_{i}\right) =\ln \left( c_{i}\right) \) and \(v\left( l\right) =\ln \left( l\right) \) and the elasticity of human capital with respect to schooling time is constant, an exogenous rise in the survival probability, ϕ, has a positive effect on schooling time, e, and at the same time a negative effect on the retirement age, 1 − l.

Proposition 4 provides an example from which we obtain the negative relation between schooling time and lifetime labor supply. Besides the advantage of an analytical solution, the logarithmic case is a convenient benchmark showing that our result does not rely on any favoring of income or substitution effects. It is worth mentioning that the effect on schooling does not depend on how responsive earnings are to schooling time, captured by μ, except for the assumptions made on the function \(h\left( e\right) \).

We now study the robustness of the result. To do this, we generate numerical results using the following functional forms: \(u\left( c_{i}\right) =\frac{ c_{i}^{1-\sigma }}{1-\sigma }\), \(v\left( l\right) =\frac{l^{1-\gamma }}{ 1-\gamma }\), and \(h\left( e\right) =1+Ae^{\mu }.\) The parameters of the model are set as follows:Footnote 12

By considering the length of the each period as 25 years, our benchmark value of education corresponds to an average years of education for men born in 1850 of approximately 9 years, as reported in Table 1, and a retirement age of roughly 62 years which squares well with Hazan (2009).

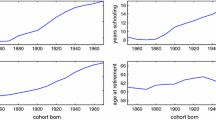

The value of ϕ = 0.7 is chosen to match the probability of surviving to age 50 conditional on reaching age 20 for American men born in 1840 as reported in Hazan (2009). Figure 1 shows that an increase in the survival rate from 0.7 to 0.95 results in a little less than 1 year of additional education, using σ = 0.8. This is a relatively modest effect, comparing with Table 1 showing that average years of schooling for men in 1980 was 15.5 years. However, one should keep in mind that the model only explains the incentive effects on schooling from increased life expectancy which leaves room for several other important explanations for the rise in education.Footnote 13 Moreover, Fig. 1 reveals that our result is robust to changes in σ. Intuitively, a higher level of σ means that individuals are less willing to substitute consumption across periods which results in a lower level of education for all survival rates.

The effect of life expectancy on schooling and retirement. Notes: Years of schooling is calculated as 25 ·e and retirement age as 50 + 25 · (1 – l). The parameters σ and ϕ are defined in the text

To sum up, our model shows that the effect of life expectancy on life-cycle behavior and the choice of schooling can only be studied separately under the assumption of perfect market for student loans. Otherwise, the schooling and saving decisions are interdependent choices since they are both instruments to alter the allocation of consumption over the life cycle.

Our result may help to get a better understanding on how human capital and thereby the size of the effective labor force is affected by increasing life expectancy.Footnote 14 In particular, the quality of an individual’s labor supply may increase along with a decrease in the quantity supplied throughout life. Based on this theory, it is not clear in what way one should expect an exogenous increase in life expectancy to affect economic performance through the effect on human capital. In the next section, we discuss the implications of our result for the empirical analyses on the causal effect of increasing life expectancy on income.

3 Life expectancy and income

As argued above, rising life expectancy may have an ambiguous effect on an individual’s lifetime supply of human capital, even when we abstract from general equilibrium and aggregation effects caused by a changed population structure.Footnote 15 Below we argue that our result may help explain the mixed findings in the empirical literature by analyzing whether cross-country variation in life expectancy can explain variation in income per capita.

Most empirical studies testing the causal effect running from life expectancy to income presume that increasing life expectancy tends to increase human capital accumulation via the Ben-Porath mechanism (see for instance Lorentzen et al. 2008; Jayachandran and Lleras-Muney 2009; Aghion et al. 2010). However, the empirical finding in Hazan (2009) suggests that there might be no such relation at all. In order to link this finding to the general discussion of whether life expectancy can explain cross-country variation in income per capita, we now examine the supply side of an economy. Suppose that economy i has the following production function:

where 0 < α < 1, \(y_{i}\equiv \frac{Y_{i}}{N_{i}}\) denotes the income per capita and \(\ \tilde{h}_{i}=h_{i}n_{i}\) is the supply of human capital per capita given by the product of the representative individual’s human capital, h i , and the number of hours supplied, n i . The size of the total population is given by N i . Suppose further, along the lines of Acemoglu and Johnson (2007), that the following relations hold:

where X i denotes life expectancy. Inserting Eqs. 15–17 into Eq. 14 yields:

In terms of the specification in Eq. 1, the Ben-Porath mechanism suggests that ε > 0 if and only if v > 0. In that case, the theoretical reasoning for life expectancy to have a negative impact on income per capita will rely on decreasing returns to scale, i.e., a Malthusian effect (assuming λ > 0). On the other hand, our model shows that optimal behavior may entail a situation where ε > 0 and at the same time v < 0, demonstrating counteracting forces on human capital induced by higher life expectancy. Therefore, the net effect from life expectancy to income per capita may be negative not only because of decreasing returns to scale but also because individuals respond by decreasing their lifetime labor supply. More generally, our analysis indicates that the Ben-Porath mechanism may overstate the net effect on human capital caused by gains in life expectancy depending on financial market imperfections and at which ages the mortality rate declines.

A related argument is found in Boucekinne et al. (2002). In their model, increasing life expectancy causes the effective workforce to shrink in the long run since it is comprised of relatively older vintages of workers who are relatively less educated and therefore have a lower productivity. Yet, their result relies on the standard Ben-Porath mechanism, implying that an increase in life expectancy increases both lifetime working hours (the retirement age) and schooling time. As we have shown, this positive relation relies on perfect financial markets. Therefore, our result implies that the tendency of a workforce comprising an increasing share of old and more obsolete workers, due to higher life expectancy, may by circumvent by incentive effects, i.e., individuals choose more education and earlier retirement.

Finally, in relation to the empirical discussion of whether life expectancy has positive effect on income—with Acemoglu and Johnson (2007) in the one corner and Lorentzen et al. (2008) in the other—it is worthwhile noticing that Cervellati and Sunde (2011) have demonstrated that the effect may depend on the stage of development of the economy. In this way, the authors unify the two corners in the literature: those who reject and those who support the health income view. In particular, they argue that in an early stage of development, the Malthusian stage, an increase in life expectancy exerts a positive effect on population size as stated in Eq. 17, whereas in a later stage of development, life expectancy and population size are negatively related via changing fertility behavior (implying that λ < 0). The authors support this argument empirically.

4 Concluding remarks

Life expectancy may have important indirect effects on schooling via its effect on life-cycle behavior. This paper has shown that a higher propensity to save, induced by an increase in life expectancy, can induce earlier retirement and more schooling. This result provides a theoretical foundation for the finding in Hazan (2009) and more generally shows opposing effects on schooling and thereby human capital and income, when life expectancy increases.

Notes

See the discussion below, where the recent results in the field are discussed and related to our finding.

This is not equivalent to exclude life expectancy to have a causal effect on education; the impact is just not working through an increase in the expected lifetime working hours. We thank Moshe Hazan for pointing this out.

By assuming that individuals cannot borrow during youth does not exclude the possibility of positive savings to smooth consumption across periods. However, in the schooling period, we regard this as a theoretical curiosity, since higher earnings later in life and a desire to smooth consumption will pull in the direction of borrowing rather than saving.

For evidence of credit constraints hampering education, see Flug et al. (1998). Furthermore, the assumption of no annuity markets implies that individuals cannot die in debt. This is true since a lender will always prefer a safe return in the capital market instead of lending money to a mortal individual unless he is compensated for the mortality risk, i.e., if annuity markets exist.

We make these assumptions to focus on the effect on the retirement choice. Considering uncertain survival to the second period would not change our result. Introducing a choice between labor and leisure in the second period would only blur our main result. In fact, a constant labor at supply at the intensive margin is consistent with the empirical finding in Hazan (2009). As he notes, expected lifetime labor supply mainly declined from later entry and earlier exit of the labor market, whereas the intensive margin remained relatively constant.

Equation 4 shows that we assume no depreciation of human capital from the second to the third period of life. Introducing depreciation into the model does not change the results.

Because the following relation would apply: \(u^{\prime }\left( c_{1}\right) =\beta Ru^{\prime }\left( c_{2}\right) .\)

We thank an anonymous referee for pointing this out.

Including accidental bequests would make the effect on the retirement age from an increase in the survival rate ambiguous (see, e.g., Hansen and Lønstrup 2010).

For example, the increasing demand for educated labor caused by technological progress (Galor and Weil 2000)

Actually, in our model, lifetime labor supply shrinks both because of earlier retirement and later entry into the labor market. We focus here how changed mortality rates affect the retirement decision whereas the effect on the entry decision is analyzed in more detail in Sheshinski (2009) and Cervellati and Sunde (2010).

References

Abel AB (1985) Precautionary saving and accidental bequests. Am Econ Rev 75(4):777–791

Acemoglu D, Johnson S (2007) Disease and development: the effect of life expectancy on economic growth. J Polit Econ 115(6):925–985

Aghion P, Howitt P, Murtin F (2010) The relationship between health and growth: when lucas meets Nelson–Phelps. Working paper 15813. NBER

Ben-Porath Y (1967) The production of human capital and the life cycle of earnings. J Polit Econ 75(4):352–365

Boucekinne R, de la Croix D, Licandro O (2002) Vintage human capital, demographic trends, and endogenous growth. J Econ Theory 104(2):340–375

Bouzahzah M, De la Croix D, Docquier F (2002) Policy reforms and growth in computable OLG economies. J Econ Dyn Control 26(12):2093–2113

Cervellati M, Sunde U (2010) Longevity and lifetime labor supply: evidence and implications revisited. Mimeo

Cervellati M, Sunde U (2011) Life expectancy and economic growth: the role of the demographic transition. J Econ Growth 16(2):99–133.

Flug K, Spilimbergo A, Wachtenheim E (1998) Investment in education: do economic volatility and credit constraints matter? J Dev Econ 55(2):465–481

Galor O, Zeira J (1993) Income distribution and macroeconomics. Rev Econ Stud 60(1):35–52

Galor O, Weil DN (2000) Population, technology, and growth: from malthusian stagnation to the demographic transition and beyond. Am Econ Rev 90(4):806–828

Galor O, Moav O (2004) From physical to human capital accumulation: inequality and the process of development. Rev Econ Stud 71(4):1001–1026

Glomm G, Ravikumar B (1992) Public versus private investment in human capital: endogenous growth and income inequality. J Polit Econ 100(4):818–834

Hansen C, Lønstrup L (2010) Aging, imperfect annuity markets and retirement. Mimeo

Hazan M (2009) Longevity and lifetime labor supply: evidence and implications. Econometrica 77(6):1829–1863

Hazan M, Zoabi H (2006) Does longevity cause growth? A theoretical critique. J Econ Growth 11(4):363–376

Heijdra BJ, Mierau JO, Reijnders LSM (2010) The tragedy of annuitization. Working paper 3141. CESifo, Munich

Jayachandran S, Lleras-Muney A (2009) Life expectancy and human capital investments: evidence from maternal mortality declines. Q J Econ 124(1):349–397

Kalemli-Ozcan S (2008) The uncertain lifetime and the timing of human capital investment. J Popul Econ 21(3):557–572

Kalemli-Ozcan S, Weil DN (2010) Mortality change, the uncertainty effect, and retirement. J Econ Growth 15(1):65–91

Kodde DA, Ritzen JMM (1985) The demand for education under capital market imperfections. Eur Econ Rev 28(3):347–362

Lorentzen P, McMillan J, Wacziarg R (2008) Death and development. J Econ Growth 13(2): 81–124

Ludwig A, Vogel E (2010) Mortality, fertility, education and capital accumulation in a simple OLG economy. J Popul Econ 23(2):703–735

Sheshinski E (2009) Uncertain longevity and investment in education. Working paper 2784. CESifo, Munich

Tang KK, Zhang J (2007) Health, education, and life cycle savings in the development process. Econ Inq 45(3):615–630

Zhang J, Zhang J (2005) The effect of life expectancy on fertility, saving, schooling and economic growth: theory and evidence. Scand J Econ 107(1):45–66

Zhang J, Zhang J (2009) Longevity, retirement, and capital accumulation with an application to mandatory retirement. Macroecon Dynam 13(3):327–348

Zhang J, Zhang J, Lee R (2003) Rising longevity, education, savings, and growth. J Dev Econ 70(1):83–101

Acknowledgements

We thank Oded Galor, Per Svejstrup Hansen, Moshe Hazan, Jens Iversen, Peter Sandholt Jensen, and seminar participants at Brown University, University of Southern Denmark and 2nd LEPAS Workshop on the Economics of Ageing for useful comments and suggestions. We are also grateful to two anonymous referees whose comments greatly improved the paper.

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Junsen Zhang

Appendix

Appendix

The first-order conditions 6–8 are here repeated for convenience:

To prove the propositions, we need the following second-order derivatives:

Proof of Proposition 1

It is to be shown that \(\frac{\partial e}{\partial \phi }>0\).

Under the assumption of an exogenous retirement age, the first-order conditions reduces to Eqs. 19 and 20. By taking the total differential of these and solving the subsequent system of equations for \(\frac{\partial e}{\partial \phi }\), we obtain:

where H is the Hessian matrix. For the problem to have a unique solution, \( \left\vert H\right\vert >0\) which is now first proven. The determinant of Hessian matrix is given by:

Inserting Eqs. 22, 23, 30 and assume, without loss of generality, that w = β = 1 yields:

given the assumption on h(e) and u(c i ) for i = 1,2,3.

Thus, \({\rm sign}\frac{\partial e}{\partial \phi }=\left\vert \begin{array}{cc} U_{ss} -U_{s\phi } \\ U_{es} -U_{e\phi } \end{array} \right\vert \). Inserting the expressions in Eqs. 22–25 yields:

which completes the proof.□

Proof of Proposition 2

It is to be shown that \(\frac{\partial e}{\partial l}\geq 0\) if Eq. 11 holds.

The proof parallels that of Proposition 1. Thus:

In the proof of Proposition 1, it is shown that \(\left\vert H\right\vert >0\). Thus, \({\rm sign}\frac{\partial e}{\partial l}=\left\vert \begin{array}{cc} U_{ss} -U_{sl} \\ U_{es} -U_{el} \end{array} \right\vert \). Inserting Eqs. 22, 23, 27, and 28 yields:

because \(\beta ^{3}\phi wh^{\prime }(e)u^{\prime \prime }(c_{2})<0\ \) we conclude that \(\frac{\partial e}{\partial l}>0\) if the following condition holds:

which is the condition in Eq. 11 where \(\sigma _{3}\equiv -c_{3}\frac{ u^{\prime \prime }(c_{3})}{u^{\prime }(c_{3})}\) is the coefficient of relative risk aversion. This completes the proof.□

Proof of Proposition 3

It is to be shown that \(\frac{\partial l}{\partial \phi }>0.\)

The proof parallels those of Proposition 1 and 2. Thus:

Then determinant of the Hessian matrix is given by:

By using Eqs. 22, 26, and 31, this yields:

with the assumed increasing and concave functions h(e),u(l), and u(c i ), i = 1,2,3.

Thus, \({\rm sign}\frac{\partial l}{\partial \phi }=\left\vert \begin{array}{cc} U_{ss} -U_{s\phi } \\ U_{ls} -U_{l\phi } \end{array} \right\vert \). Inserting Eqs. 22, 24, 26, and 29 and obtain:

which completes the proof.□

Proof of Proposition 4

Rights and permissions

About this article

Cite this article

Hansen, C.W., Lønstrup, L. Can higher life expectancy induce more schooling and earlier retirement?. J Popul Econ 25, 1249–1264 (2012). https://doi.org/10.1007/s00148-011-0397-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00148-011-0397-1