Abstract

We use a bivariate Vector Error Correction model to assess the transmission of price signals from selected international food markets to developing countries. We introduce a Generalized Conditional Autoregressive Heteroscedasticity (GARCH) effect for the model’s innovations in order to assess volatility spillover between the world and domestic food markets of Ethiopia, India and Malawi. Our results point out that short-run adjustment to world price changes is incomplete in Ethiopia and Malawi, while volatility spillovers are significant only during periods of extreme world market volatility. The problem in these countries is one of extreme volatility due to domestic, rather than world market shocks. In India, the analysis supports relatively rapid adjustment and dampened volatility spillovers which are by large determined by domestic policies.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

10.1 Introduction

Between 2007 and 2008, the world experienced a dramatic swing in commodity prices. Agricultural commodity prices also increased substantially with the FAO food price index rising by 63% between January 2007 and June 2008, as compared with an annual increase rate of 9% in 2006. During the same period, the international prices of traditional staple foods such as maize and rice increased by 74 and 166%, respectively, reaching their highest level in nearly 30 years. After its peak in June 2008, the food price surge decelerated and in the autumn, international food prices decreased sharply as expectations for an economic recession set in. Between June 2008 and January 2009, with the demand for commodities weakening due to the global economic slowdown in conjunction with improved food crop supply, the FAO food index decreased by 33%.

The sudden and unexpected rise in world food prices strengthened the attention of policy makers to agriculture and fuelled the debate about the future reliability of world markets as a source for food. The possibility for further spells of volatility in food prices has instigated renewed efforts in designing and proposing price stabilising mechanisms at both the national and international levels. There is widespread recognition that beyond market fundamentals, a new set of forces drive food prices. These forces emerge from linkages between the agricultural and the energy markets, the role of financial and currency markets, together with the wider macroeconomy, which together, render agricultural markets much more vulnerable to shocks. During the 2007–2008 period, the concurrence of so many drivers, in conjunction with crop production decreases around the world, gave rise not only to an unprecedented price surge, but also to significant volatility. Indeed, there is the perception that volatility for many of the major internationally traded food commodities has been steadily increasing over the past decade, becoming more and more persistent and a permanent feature of the food markets.

The recent price surge in the food markets and the perceptions on increased volatility have renewed interest in analysing the interactions of food markets. This chapter focuses on assessing the persistence of food price volatility, as well as examining the mean and volatility spillover between world food markets and the domestic markets of developing countries. Spillover in the mean denotes the transmission of price changes from the world to domestic prices and vice versa (in terms of levels), while volatility spillover reflects the co-movement of the price variances in these markets. A better understanding of the price mean and variance relationships between the world market and the markets of developing countries can assist policy formulation. Increases in food price volatility have important negative implications for economic welfare in developing countries where agricultural commodities form the basis for household income and food consumption.

Commodity prices, both at the world and the domestic markets, tend to be non-stationary processes that are integrated of order one. Often, their first differences tend to be leptokurtic. Non-stationarity implies that shocks to the series are permanent, rendering the mean dependent on time. However, in the first differences, shocks have a transitory impact resulting in volatility clustering. This suggests that the conditional variance of the first differences may be also time variant. Consequently, we model price transmission, or mean spillover, within a Vector Error Correction (VEC) framework. This allows us to reveal the dynamics of adjustment of prices to their long-run equilibrium path. The analysis of volatility spillover is based on the application of multivariate Generalised Autoregressive Heteroscedasticity (GARCH) on the innovations of the VEC model. GARCH models were introduced by Engle (1982) and generalised by Bollerslev (1986) and take into account that variances vary over time. Although there are many applications of vector autoregressions and GARCH models in the finance literature (see, for example, De Goeij and Marquering, 2004; Hassan and Malik, 2007; Qiao et al., 2008; Alizadeh et al., 2008), such analyses are uncommon in agricultural economics.

We study food markets in three different developing countries, namely wheat in Ethiopia, rice in India and maize in Malawi. In Ethiopia, wheat is a major staple food mainly consumed in urban areas. In 2003–2005, wheat and wheat products accounted for 16% of the total dietary energy supply while the country’s self-sufficiency ratio of wheat and wheat products was 76%. India is a major producer and exporter of rice. It is fully self-sufficient in rice which is the main staple food throughout the country. Rice accounted for 30% of the total dietary energy supply in 2003–2005. In Malawi, maize is the main staple food produced and consumed throughout the country. Maize and maize products accounted for 52% of the total dietary energy supply in 2003–2005. On average in 2004–2008, per capita annual consumption of maize was 127 kg. The self-sufficiency ratio of maize was 97%.

The chapter is organised as follows. The next section discusses the modelling framework. Section 10.3 presents the empirical results and Section 10.4 discusses policy implications and concludes.

10.2 The Model

Given prices for a commodity in two spatially separated markets p 1t and p 2t , the Law of One Price and the Enke–Samuelson–Takayama–Judge model (Enke, 1951; Samuelson, 1952; Takayama and Judge, 1971) postulate that at all points of time, allowing for transfer costs m, for transporting the commodity from one market to another, the relationship between the prices is as follows:

If a relationship between two prices, such as Eq. (10.1), holds, the markets can be said to be integrated. However, this extreme case may be unlikely to occur, especially in the short run. At the other end of the spectrum, if the joint distribution of two prices were found to be completely independent, then one might feel comfortable saying that there is no market integration and no price transmission. In general, spatial arbitrage is expected to ensure that prices of a commodity will differ by an amount that is at most equal to the transfer costs with the relationship between the prices being identified as the following inequality:

Fackler and Goodwin (2002) refer to the above relationship as the spatial arbitrage condition and postulate that it identifies a weak form of the Law of One Price, the strong form being represented by equality in Eq. (10.1). They also emphasise that relationship in Eq. (10.2) represents an equilibrium condition. Observed prices may diverge from relationship in Eq. (10.1), but spatial arbitrage will cause the difference between the two prices to move towards the transfer cost. The condition encompasses price relationships that lie between the two extreme cases of the strong form of the Law of One Price and the absence of market integration. Depending on market characteristics, or the distortions to which markets are subject, the two price series may behave in a plethora of ways, having quite complex relationships with prices adjusting less than completely, or slowly rather than instantaneously and according to various dynamic structures or being related in a non-linear manner.

Within this context, complete price transmission between two spatially separated markets is defined as a situation where changes in one price are completely and instantaneously transmitted to the other price, as postulated by the Law of One Price presented by relationship in Eq. (10.1). In this case, spatially separated markets are integrated. In addition, this definition implies that if price changes are not passed-through instantaneously, but after some time, price transmission is incomplete in the short run, but complete in the long run, as implied by the spatial arbitrage condition. The distinction between short-run and long-run price transmission is important and the speed by which prices adjust to their long-run relationship is essential in understanding the extent to which markets are integrated in the short-run. Changes in the price at one market may need some time to be transmitted to other markets for various reasons, such as policies, the number of stages in marketing and the corresponding contractual arrangements between economic agents, storage and inventory holding, delays caused in transportation or processing, or “price-levelling” practices.

The spatial arbitrage condition implies that market integration lends itself to a cointegration interpretation with its presence being evaluated by means of non-cointegration tests. Cointegration can be thought of as the empirical counterpart of the theoretical notion of a long-run equilibrium relationship. If two prices in spatially separated markets p 1t and p 2t , contain stochastic trends and are integrated of the same order, say I(d), the prices are said to be cointegrated if

where u t is stationary and β is the cointegrating parameter. Evidence for cointegration reflects that prices are jointly determined. The concept of cointegration has an important implication, purported by the Granger Representation Theorem (Engle and Granger, 1987). According to this theorem, if two trending, say I(1), variables are cointegrated, their relationship may be validly described by a Vector Error Correction (VEC) model, and vice versa. In the case that prices from two spatially separated markets are cointegrated, the VEC model representation is as follows:

where \(\left. {{{\textbf{v}}_t}} \right|{\Omega _{t - 1}}\sim N\left( {0,{{\textbf{H}}_t}} \right)\) are normally distributed disturbances conditional on past information with zero mean and a variance-covariance matrix denoted by H t , while the operator Δ denotes that the I(1) variables have been differenced in order to achieve stationarity. \({{\boldsymbol{\Pi }}_{}}{{\textbf{p}}_{t - 1}}\) states the long-run relationship while the matrix Π can be decomposed in \({{\boldsymbol{\Pi }}_{}} = \alpha \beta '\) as follows:

The inclusion of the levels of the prices alongside their differenced terms is central to the concept of the VEC model. Parameters contained in matrices Γ, measure the short-run effects, while β is the cointegrating parameter that characterises the long-run equilibrium relationship between the two prices. The levels of the variables enter the VEC model combined as the single entity \(({p_{1t - 1}} - \beta {p_{2t - 1}})\) which reflects the errors or any divergence from this equilibrium, and correspond to the lagged error term of Eq. (10.3). The vector \({\left( {{\alpha _1}{\textrm{ }}{\alpha _2}} \right)^\prime }\) contains parameters, commonly called “error correction coefficients”, which measure the extent of corrections of the errors that the market initiates by adjusting the prices towards restoring the long-run equilibrium relationship. The speed with which the market returns to its equilibrium depends on the proximity of α i to unity. Within this context, short-run adjustments are directed by, and consistent with, the long-run equilibrium relationship, allowing the researcher to assess the speed of adjustment that shapes the relationship between the two prices.

The model also allows testing for causality in the Granger sense, providing evidence on which direction price transmission is occurring, as well as the decomposition of the forecast error variance in parts that are due to international and domestic shocks respectively. The cointegration-VECM framework takes into account that prices are stochastic processes which have time dependent means, and replicates their systematic behaviour being essentially a description of the conditional process of realising the data.

While the VEC model provides the conditional expected means of the variables, in order to examine for higher moment relationships which reflect volatility spillovers, the VEC model’s errors v t are specified as a bivariate GARCH model (Bollersev, 1986). We employ the BEKK parametrisation by Engle and Kroner (1995) which incorporates quadratic forms in such a way so that the covariantce matrix is positive semi-definite, a requirement that is necessary for the estimated variances to be non-negative.

The BEKK parameterisation is given by

where H t+1 is the conditional variance matrix, C is a 2 × 2 lower triangular matrix with three parameters and B and A are 2 × 2 matrices of parameters restricted to be diagonal. In this parsimonious specification the conditional variances are a function of the lagged variances and error terms. Expanding Eq. (10.6) gives the variance–covariance equations:

where \(b_{12}^2 = b_{11}^2b_{22}^2\) and \(a_{12}^2 = a_{11}^2a_{22}^2\).

The \(b_{ii}^2\)s measure the extent to which current levels of conditional variances are related to past conditional variances. The \(a_{ii}^2\)s assess the correlations between conditional variances and past squared errors reflecting the impact of shocks on volatility. This specification retains the intuition and interpretation of the univariate GARCH model with the variances and the covariance h t+1 being determined by “old” news, or past behaviour as reflected by the lagged h t , as well as by “fresh” news, reflected by the lagged errors ν t .

10.3 Empirical Results

10.3.1 Data and Preliminary Analysis

We use logarithmic transformations of monthly domestic prices measured in US$ per tonne from January 2000 to December 2009. We apply the VEC–BEKK model to investigate spillover between the world market and the wheat market in Ethiopia, the rice market in India and the maize market in Malawi. The data on domestic prices is collected from the FAO Global Information and Early Warning System. Data on the corresponding international market prices is collected from the IMF International Financial Statistics.

The order of integration of the price series is assessed by the Augmented Dickey Fuller (ADF) test (Dickey and Fuller, 1979) and the Zρ test by Phillips and Perron (1988). All series were found to be non-stationary and integrated of order 1 (Table 10.1).

Table 10.2 presents a range of descriptive statistics for the differenced prices Δp t . The sample moments for all differenced prices indicate non-normal distributions. Zero excess kurtosis is rejected for all series suggesting leptokurtic distributions with heavy tails. In general, the statistics indicate that the differenced prices exhibit time varying variance and volatility clustering with large changes being likely to be followed by further large changes.

The Jacque–Bera test is used to test the hypothesis that the differenced prices are normally distributed. In all cases, the probability values are smaller than 0.01, rejecting the null hypothesis. We also calculated the sample autocorrelation functions, which provided evidence for autocorrelation at least for the first and the second lag.

10.3.2 Empirical Results

10.3.2.1 VEC models: Price Transmission or Mean Spillover

For each of the food markets, we test for cointegration between the domestic and world prices using the Full Information Maximum Likelihood method developed by Johansen (1995). This test is based on the rank of matrix Π in Eq. (10.4) and is the most commonly encountered in the price transmission literature. A rank equal to zero indicates non-cointegration. In our bivariate case, a rank of one would suggest cointegration between the domestic and world prices. For n + 1 variables, Johansen derived the distribution of two test statistics for the null of at most n cointegrating vectors referred to as the Trace and the Eigenvalue tests.

Table 10.3 presents the results of the non-cointegration tests for the food markets under consideration. In all cases, there is strong evidence that the domestic prices and the world prices are cointegrated, with the Johansen test rejecting the null hypothesis of no cointegration, but failing to reject the null hypothesis of one cointegrating vector. These results suggest that the domestic markets of these commodities are well-integrated with the world markets in the long run.

We formulate VEC models in order to assess the dynamics and the speed of adjustment and we also perform forecast error variance decomposition. The estimated VEC models are presented in Table 10.4. For the Ethiopian wheat market the estimated VEC model suggests that the adjustment process of the domestic price to the world price is significantly slow. On average, over the 2000–2009 period, about 0.06% of the divergence of the domestic price from its notional long-run equilibrium with the world price is corrected each month. In addition, the short-run dynamics indicate that changes in the world market price are not transmitted to the Ethiopian wheat market in the short-run. The non-significant error correction coefficient in the world price VEC model suggests that the world price is weakly exogenous, identifying a causal relationship, in the Granger sense, which runs from the world to the Ethiopian market, as expected for a small player in the wheat market as Ethiopia.

High transaction costs and trade policies can result in discontinuities in trade which, within a time series modelling framework, give rise to slow speed of convergence to a long-run relationship. Such a slow adjustment to the world market prices suggests that the wheat market in Ethiopia may be characterised by high price volatility due to inadequate buffer capacity and a limited possibility to adjust domestic adverse shocks through trade. Indeed, 12 months ahead forecast variance decompositions, estimated by means of the VEC model, suggest that, on average, it is domestic shocks that give rise to volatility.Footnote 1 The estimates indicate that shocks in the domestic wheat market explain about 65% of the domestic price variability. On the other hand, slow adjustment indicates that world price surges may take some time to pass through to the domestic market, although there is the possibility of asymmetric response where increases in the world price are rapidly and more fully transmitted than decreases.

The statistical significance of both error correction coefficients in the Indian-world rice market VEC model suggests that both prices are endogenous, with the world price or rice influencing the Indian market price and vice versa. This is not surprising, given the importance of India in the world rice market. The results indicate that both the Indian and the world prices adjust to their long-run equilibrium relatively rapidly, correcting about 16% of the divergence each month.Footnote 2

Maize is an important staple food in Malawi. The estimated VEC model suggests that the world maize price is the long-run driver of the price of maize in Malawi. The domestic maize price adjusts to changes in the world maize price quite slowly. About 11% of divergences from the long-run path are corrected during the period of 1 month. As in the case of Ethiopia, the slow transmission of changes in the world price to the Malawian maize market may lead to increased volatility. The 12 months ahead forecast variance decomposition suggests that, on average during the 2000–2009 period, domestic shocks explained about 85% of the maize price variance with the remainder being due to international shocks.

10.3.2.2 BEKK: Conditional Variances or Volatility Spillover

The estimation of the BEKK parameterisation of the multivariate GARCH is carried out by maximising the conditional non-linear log-likelihood function following Engle and Kroner (1995). The numerical maximisation method used was the Berndt, Hall, Hall and Hausman algorithm. The Schwartz–Bayes criterion was used to choose the appropriate lag length. The estimated parameters are shown in Table 10.5.

The estimated parameters capture the volatility spillovers between the domestic food markets under consideration and the world market. They quantify the effects of own lagged innovations (ARCH effects), as well as those of the lagged variances (GARCH effects) and thus reveal the persistence of volatility. On the whole, the parameters are significant indicating the presence of strong ARCH and GARCH effects. For the wheat and maize prices, the estimated GARCH parameters are considerably larger than the corresponding ARCH coefficients (ranging from 0.61 to 0.85, as compared with the lagged innovation parameter estimates of 0.06–0.11). This indicates that the variances of these prices are more influenced by their own lagged values, rather than by “fresh news” which are reflected by the lagged innovations. However, for the conditional variances of the Indian and the world rice prices past shocks also appear to be relatively important.

In all markets volatility, as reflected by the conditional variances, can be persistent. Higher levels of conditional volatility in the past are associated with higher conditional volatility in the current period. On the whole persistence as measured by sum of the ARCH and GARCH coefficients, \(b_{ij}^2 + a_{ij}^2\) which is for all cases close to unity, is high. In all covariance equations the estimated parameters of the cross past innovations \(v_{1t - 1}^2\) \(v_{2t - 1}^2\) are positive, suggesting that if shocks in the domestic and world markets have the same sign will affect the covariance in a positive manner reflecting the possibility for some indirect volatility spillover between the domestic and the world markets under consideration.

Rather than focusing on the parameters themselves, we discuss the time plots of the estimated conditional variances and covariances over the period 2000–2009. We also calculate the conditional correlation as follows:

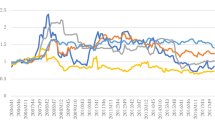

Panels 10.1, 10.2 and 10.3 present the conditional variances, covariances and correlations for the markets examined in Ethiopia, India and Malawi, respectively.

Ethiopian and world wheat prices: conditional variances and correlations

Indian and world rice prices: conditional variances and correlations

Malawian and world maize prices: conditional variances and correlations

The plots show that the conditional variances of the wheat and maize price pairs are not constant over time. For the wheat price pair volatilities tend to cluster during the 2008 price surge. The world maize price conditional variance also becomes significantly more volatile during the surge period. The maize price in Malawi is, during the whole period 2000–2009, extremely volatile. These findings are in line with the result of the previous section and the estimated VEC models. Very slow adjustment to world market prices points out a partly insulated market with limited buffer capacity to contain domestic shocks. The rice price pair variances appear to be relatively stable over the 2000–2007 period, with the exception of a high volatility incidence in the Indian market, while both series exhibit volatility clustering during the recent food price spike.

In general, the conditional variances of the world wheat and maize prices appear to follow a weak positive trend, suggesting that volatility in these markets has been increasing during the 2000–2009 period. We regressed both conditional variances on a time trend to corroborate this observation. In both regressions, the estimated time trend parameter was statistically significant, albeit small. The variances of the domestic food prices do not show to follow a trend, however, they tend to cluster during the 2007–2008 period following, to differing degrees, the world price volatilities.

The conditional covariances of Ethiopian wheat and world prices are not constant over the period under examination and also tend to cluster over time in line with the conditional variances. For the wheat price pair, the covariance assumes negative values suggesting opposite shocks in the innovations in the two markets. Even during the recent price shock, the covariance suggests that the volatility spillover was limited, although wheat prices surged above import parity, as fuel subsidies and restrictions on the foreign exchange market created a shortage of foreign currency, preventing private traders from importing grain (Minot, 2010). Perhaps the large negative value of the covariance in 2009 indicates a significant reduction in spillover, as Ethiopian wheat prices remained at high levels, in spite of the reduction in the world market price. The conditional correlations follow a similar pattern, being in general very low. It appears that, although world price changes are transmitted into the Ethiopian wheat market in terms of levels (or mean), there is limited volatility spillover, with domestic price volatility being persistent and mainly due to domestic shocks.

Both the world and the Indian rice markets appear to be characterised by very low volatility up to the year 2007. Indeed, since the mid-1980s, prices have been low and quite stable (Dawe, 2002). The world rice market is quite thin, with only about 7% of world production being traded, while all major producers manage their domestic markets mainly through trade policy measures. The Indian government intervenes in the rice market through procurement, stocking and distribution policies (Gulati and Dutta, 2010). The conditional variance of the Indian market prices exhibits sharp spikes in 2002–2003, due to climatic conditions during that harvest period, and in 2008 during the food price surge.

The conditional covariance of the Indian and world rice prices assumes positive values for most of the 2000–2009 period and also exhibits sharp increases during 2002–2003 and 2008, indicating volatility spillovers. In general, the covariances tend to assume values which are higher (lower) in times of high (low) volatility. This is also observed by the conditional correlation coefficient which assumes high values during the extreme volatility episodes, suggesting spillovers. Although our findings indicate significant volatility persistence and spillover, the volatility in the Indian market is significantly lower, as compared with that in the world market during the recent price episode, as government intervention in India stabilises the domestic price level. Indeed, during the 2008 price surge, the imposition of a ban in rice exports resulted in less domestic price volatility. As other major rice exporting countries followed suit by restricting exports due to food security fears, the world price of rice increased sharply and became more volatile.

The conditional covariance of maize prices in Malawi and the world market assumes positive values for most of the period under examination. The maize market in Malawi is characterised by a dual marketing structure where the government operates along the private sector through parastatal marketing boards and food security programmes and intervenes in the market. Both parastatals, the Agricultural Development and Marketing Corporation (ADMARC) and the Food Reserve Agency, respectively maintain a strong presence in the market.

In addition to unfavourable climatic conditions, which generate wide shocks, discrete and largely unexpected policy responses increase volatility. For example, during the food price surge of 2008, based on estimates of surplus production in May 2008, the government requested that the ADMARC accumulate stocks by initiating purchases in the domestic market. Within an environment of upward trending world maize prices, ADMARC progressively increased its price in order to outbid private traders and secure the requested quantities. Competition for maize between traders and the board was likely to have led to the domestic price increasing and remaining to high levels even after the world maize price decrease in the autumn of 2008 (Rapsomanikis, 2009). Such shocks have probably given rise to conditional covariances and correlations that change abruptly from positive to negative values. Again, irrespective of the signs, the conditional correlations are low, indicating insignificant volatility spillover from the world market, with the domestic maize price volatility being extreme, persistent and determined by domestic shocks.

10.4 Conclusions and Policy Implications

The effects of food price shocks on developing countries receive considerable emphasis whenever there are major international commodity price booms or slumps, such as the sustained price increases during the mid-1970s and the more recent price surge in 2008. Our main empirical findings can be summarised as follows. In the small developing countries examined, world price changes are partly transmitted to domestic markets. Although domestic markets are integrated with the world market in the long-run, the adjustment of food prices in these countries is exceptionally slow, suggesting that in the short-run such markets can be considered insulated. Volatility spillover is also quite limited. In general, domestic price volatility is persistent and mainly due to domestic shocks, rather than world market shocks, although some spillover takes place during extreme volatility episodes.

The analysis of the Indian rice market is of particular interest. India’s market power in the world market results in a bi-directional causal effect. Changes in the price of rice in one market will affect the other. The results suggest that volatility is characterised by the same relationship. Nevertheless, price stabilisation policies in India, and more specifically the imposition of export restrictions during the recent price surge, dampen domestic market volatility, while increase volatility in the world market, if same measures are implemented by other major exporters.

Our estimates also tend to underline the point that the major policy focus for reducing extreme price volatility in insulated developing countries, such as Malawi, should be domestic policies leading to reductions in domestic shocks. Price volatility contributes significantly towards the vulnerability to poverty and inhibits development. It results in significant income risks which blunt the adoption of technologies necessary for agricultural production efficiency, as producers may decide to apply less productive technologies in exchange for greater stability. Self-insurance strategies, such as crop diversification, hinder efficiency gains from specialisation in production.

On the one hand, policies that aim to increase integration with the world market through investment on transport infrastructure and interventions in the marketing and movement of commodities are necessary. On the other hand, such measures will also enhance the volatility spillover during episodes of extreme volatility in the world market. Governments may intervene in providing commodity price insurance as self-insurance strategies, such as crop and income diversification and consumption smoothing, may be inadequate in reducing uncertainty. For food importers, it is possible to obtain a reduction both in the average level and variability of food security costs through futures hedging on relative to a simple import strategy (Dana et al., 2006). Market-based derivative instruments that provide insurance for internationally traded commodities consist of an important policy option (Larson et al., 2004). Market-based weather insurance that covers yields’ risks has also been suggested (Skees et al., 2001).

Completely banning food exports was a common reaction to the food price surge across the developing world. Although, in general, export bans can lower domestic food prices and dampen volatility, there are also a number of negative consequences. First, export bans imply a tax on producers and lower the incentive to respond to the world price rise by increasing supply. In the long term, export restrictions may discourage investment in agriculture and thus can have negative implications for food security. Second, in the short term, export restrictions can harm traditional trading partners. For example, during the height of the food price surge in 2008, the National Cereals and Produce Board, the state marketing board of Kenya, was not able to import sufficient quantities of maize mainly due to export bans implemented by a number of countries in the region.

Concerted implementation of export restrictions by major exporters renders the world market unreliable as a source of food. Government control over exports and imports and food reserve management to defend pre-determined prices characterises the rice sectors of most Asian rice producing countries. During the 2008 price surge, bans in rice export triggered substantial instability in the market, especially because governments announced the export bans without clarifying their duration. More predictable and less discretionary policies would convey clearer information and render panic and hoarding less likely, resulting in less uncertainty.

Notes

- 1.

Forecast error variance decomposition for the domestic price yields the contribution of the variance of international prices to the domestic prices and the part of the variance that is purely attributable to shocks in the domestic price.

- 2.

The bi-directional Granger causality between the Indian and world prices does not allow meaningful forecast error variance decomposition.

References

Alizadeh A.H., Nomikos N.K., Pouliasis P.K. (2008). A Markov regime switching approach for hedging energy commodities. Journal of Banking and Finance, 32, 1970–1983.

Bollerslev T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31, 307–328.

Dana J., Gilbert C.L., Shim E. (2006). Hedging grain price risk in the SADC: case studies of Malawi and Zambia. Food Policy, 31, 357–371.

Dawe D. (2002). The changing structure of the world rice market, 1950–2000. Food Policy, 27, 355–370.

De Goeij P., Marquering W. (2004). Modelling the conditional covariance between stock and bond returns: a multivariate GARCH approach. Journal of Financial Econometrics, 2, 531–564.

Dickey D., Fuller W. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74, 427–431.

Engle R.F. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation. Econometrica, 50, 987–1008.

Engle R.F., Granger C.W.J. (1987). Cointegration and error correction: representation, estimation and testing. Econometrica, 55, 251–276.

Engle R.F., Kroner K.F. (1995). Multivariate simultaneous generalized ARCH. Econometric Theory, 11, 122–150.

Enke S. (1951). Equilibrium among spatially separated markets: solution by electrical analogue. Econometrica, 19, 40–47.

Fackler P.L., Goodwin B.K. (2002). Spatial price analysis. In B.L. Gardner and G.C. Rausser, (Eds.). Handbook of agricultural economics. Amsterdam: Elsevier Science, 971–1024.

Gulati A., Dutta M. (2010). Rice policies in India in the context of the global rice spike. In D. Dawe (Ed). The rice crisis: markets, policies and food security. London: FAO and Earthscan, 273–295.

Hassan S.A., Malik F. (2007). Multivariate GARCH modelling of sector volatility transmission. The Quarterly Review of Economics and Finance, 47, 470–480.

Johansen S. (1988). Statistical analysis of cointegration vectors. Journal of Economic Dynamics and Control, 12, 31–254.

Johansen S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models. Econometrica, 59, 551–1580.

Johansen S. (1995). Likelihood-based inference in cointegrated vector-autoregressions. Advanced texts in econometrics. Oxford: Oxford University Press.

Larson D.F., Anderson F., Jock R., Varangis P. (2004). Policies on managing risk in agricultural markets. World Bank Research Observer, 19, 199–230.

Minot N. (2010). Transmission of food price changes from world markets to Africa. Summary “Price Transmission and Welfare Impact in Sub-Saharan Africa” project, April.

Phillips P.C.B., Perron P. (1988). Testing for a unit root in time series regression. Biometrica, 75, 335–346.

Qiao Z., Chiang T.C., Wong W.K. (2008). Long-run equilibrium, short-term adjustment and spillover effects across Chinese segmented stock markets and the Hong Kong stock market. Journal of International Financial Markets, Institutions and Money, 18, 425–437.

Rapsomanikis G. (2009) Policies for the effective management of food price swings. FAO Commodity and Trade Policy Technical Paper No. 12.

Samuelson P.A. (1952). Spatial price equilibrium and linear programming. American Economic Review, 42, 560–580.

Skees J., Gober S., Varangis P., Lester R., Kalavakonda V. (2001). Developing rainfall based index insurance in Morocco. Policy Research Working Paper 2577. Washington, DC: World Bank.

Takayama T., Judge G.G. (1971). Spatial and temporal price allocation models. Amsterdam: North Holland.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Additional information

Disclaimer: The views expressed in this chapter are those of the authors and do not necessarily reflect the views of the Food and Agriculture Organization of the United Nations.

Rights and permissions

Copyright information

© 2011 Springer Science+Business Media, LLC

About this chapter

Cite this chapter

Rapsomanikis, G., Mugera, H. (2011). Price Transmission and Volatility Spillovers in Food Markets of Developing Countries. In: Piot-Lepetit, I., M'Barek, R. (eds) Methods to Analyse Agricultural Commodity Price Volatility. Springer, New York, NY. https://doi.org/10.1007/978-1-4419-7634-5_10

Download citation

DOI: https://doi.org/10.1007/978-1-4419-7634-5_10

Published:

Publisher Name: Springer, New York, NY

Print ISBN: 978-1-4419-7633-8

Online ISBN: 978-1-4419-7634-5

eBook Packages: Business and EconomicsEconomics and Finance (R0)