Abstract

The global prices of raw materials used for steelmaking have been volatile over the past few decades. More recently, extreme weather events have exacerbated this situation, causing an imbalance between supply and demand for raw materials. This study examines the impact of natural disaster shocks on the prices of steelmaking raw materials. Using data on iron ore, which is used in the process of making crude steel, this study explores whether the occurrence of natural disasters causes price fluctuations in the iron ore market. The analysis focuses on contemporaneous and dynamic effects of disasters, considering the persistence of disaster shocks. It is expected that steel manufacturers are adversely affected by disaster shocks through the international trade of raw materials. Moreover, the negative impact of natural disasters may persist longer when affected areas or countries are severely damaged. Since intense natural hazards, such as prolonged floods and devastating storms, will become more likely under climate change, this study shows empirical evidence of risks associated with extreme weather events in steel production.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

Global steel production and consumption have been expanding considerably since the 2000s because of increasing demand and economic development in emerging countries. Notably, the unprecedented growth of the Chinese steel industry has been prominent, making the country a leading player as both a supplier and a consumer in the steel and related industries. As a result of the rapid expansion of the steel industry in recent decades, the global markets for steelmaking raw materials have become increasingly competitive and complex. To maintain sustainable production, it is critical for steel manufacturers to secure raw materials such as iron ore and coal. However, recently, extreme weather events have emerged as an additional concern in the steel industry, exacerbating the imbalance between supply and demand for steelmaking raw materials.

Given the increasing climate risks in the steel industry, this chapter examines the effect of natural disasters on the prices of steelmaking raw material. By focusing on iron ore, which is used in the production of crude steel, we investigate whether the prices of iron ore are affected by natural disasters in iron ore-producing countries. Iron ore is a key input for crude steel production and is traded globally. It is mined in approximately 50 countries, including Australia, Brazil, China, India, the United States, and Russia. The majority of iron ore is then exported to steel-producing countries, making iron ore the second most traded commodity worldwide (World Steel Association 2019a). Therefore, severe natural disasters in one country may have a widespread impact on the steel and raw material industries through global supply chains. Although anecdotal evidence shows that natural catastrophes have adversely affected the supply of raw materials by damaging mines and infrastructure, we are unaware of any studies that demonstrate the link between disaster shocks and the steel industry. In this context, it is necessary to focus on this important raw material to explore the climatic impact on steel production.

A number of studies have examined whether and to what extent extreme weather events affect the economy by analyzing data on weather conditions such as temperature and precipitation and natural disasters such as storms, floods, and droughts (see Dell et al. 2014; Heal and Park 2016). One strand of the literature has examined the impact of extreme weather and natural hazards on the economy at macro levels. Dell et al. (2009) use cross-sectional data on 134 countries to investigate the relationship between temperature and income. They show that an increase in temperature negatively affects GDP per capita. Their analysis using more detailed subnational data also finds a negative effect of temperature within countries. Noy (2009) analyzes the impact of natural disasters on the macroeconomy by focusing on a series of country characteristics. The author finds that natural disasters cause larger output losses in developing countries and smaller economies. In a study on temperature and aggregate outputs, Dell et al. (2012) demonstrate the causal effect of higher temperature on economic growth in poor countries. They estimate that a 1◦C rise in temperature leads to a decline in economic growth by approximately 1.3 percentage points.

Researchers have further focused on the multidimensional impact of extreme weather and natural disasters. A growing body of literature explores the complex mechanisms of climate impacts by analyzing channels through which climate affects the macroeconomy. Evidence of climate shocks is observed in diverse spheres, for instance, in agriculture, productivity, energy production, health and mortality, migration, and violent conflicts (Anttila-Hughes and Hsiang 2013; Chen et al. 2016a; Leiter et al. 2009; Marchiori et al. 2012; Maystadt and Ecker 2014; McDermott and Nilsen 2014). While the link between negative climate impacts and agricultural outcomes may be obvious and straightforward given the importance of weather conditions to agriculture, the findings of the existing literature suggest broad and heterogeneous effects of climate associated with various aspects of the economy. The study by Dell et al. (2012) mentioned above also investigates temperature shocks in both agricultural and industrial sectors, providing evidence of channels through which temperature conditions affect the aggregate economy. Hsiang (2010) estimates the impact of temperature and tropical cyclones in the Caribbean and Central America and reveals that climate shocks resulted in greater economic losses in nonagricultural production than in agricultural production. Using micro-level data, Leiter et al. (2009) find a negative impact of floods on productivity in European firms. Previous studies on climate and the economy suggest that the impact of natural disasters is rather diverse, observed not only in the agricultural sector but also in nonagricultural sectors.

In regard to the steel and iron ore industries, the negative impact of natural disasters may spread beyond the country of origin because a large volume of iron ore is traded in the international market. One strand of literature examines the climate-economy relationship with a particular focus on international trade. Jones and Olken (2010) examine the effects of temperature shocks on international trade. They estimate that a 1◦C rise in temperature is associated with a 2.0–5.7 percentage point decline in annual export growth in poor countries. Dallmann (2019) uses a series of bilateral trade data to investigate the effects of weather variations in exporting and importing countries. Analyses using the breakdown of export data show both positive and negative impacts of temperature and precipitation on exports at the sector and product levels.

In the context of the iron ore industry, researchers have analyzed factors that drive up iron ore prices and affect the global market in the wake of a shift in the pricing regime and China’s rise over the last two decades. In a qualitative analysis, Wilson (2012) reviews the iron ore market in the Asia–Pacific region and argues that the rapid growth of the Chinese steel industry led to the restructuring of the iron ore market. China’s domestic iron ore reserves are low grade and not suitable for steel production. Thus, procurement of iron ore depended on imports in response to the rapid development of steel production, which increased market prices. Sukagawa (2010) also emphasizes the Chinese economic boom and the increased demand for iron ore as main factors that drove an unprecedented price increase in the early 2000s. A quantitative study by Chen et al. (2016b) uses a quantile regression model to examine the factors that affect China’s import prices of iron ore. They find that production of crude steel in the previous period has a positive effect on current prices of imported iron ore, while the volume of iron ore imports in the previous period and domestic iron ore production have a negative effect. Wårell (2014) explores the impact of the pricing regime change in the iron ore market in China. Although they do not find clear evidence of the impact of the pricing regime, the results of their empirical analysis suggest that transportation costs and GDP growth are the driving forces that increase the import prices of iron ore.

This study contributes to the literature on the steel and related raw material markets. Research on the iron ore market has investigated aspects such as import volume (Tcha and Wright 1999), price volatility (Astier 2015; Chen et al. 2016b), market structure (Wårell 2014), and international market power (Zhu et al. 2019). While the rise of the Chinese steel industry is the main focus of many previous studies, this study analyzes the steel industry from a different perspective by examining the impact of natural hazards. To the best of our knowledge, this study is the first to empirically demonstrate the impact of natural disaster shocks in the iron ore market. The adverse economic consequences of severe natural disasters may become more pronounced; moreover, they are likely to accelerate further under climate change. This study aims to provide suggestive evidence of the risks associated with natural catastrophic events in the steel industry.

The remainder of this chapter proceeds as follows. Section 2 presents an overview of the global iron ore industry. We also discuss trends in iron ore prices and extreme weather events that may cause price fluctuations. Section 3 describes the estimation model and data used in the empirical analysis. Section 4 presents and discusses the results. Section 5 concludes.

2 Global Iron Ore Industry and Price Volatility

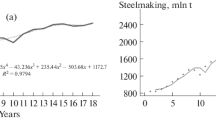

Iron ore, along with coking coal and recycled steel, is an important raw material used in steelmaking. Today, it is estimated that approximately 2 billion tonnes of iron ore are consumed annually to produce 1.7 billion tonnes of crude steel worldwide (World Steel Association 2019a). Figure 1 depicts trends in global iron ore production from 1998 to 2017. The industry has been steadily growing over the last two decades, with production doubling to 2.2 billion tonnes in 2017 from 906 million tonnes in 1998. The leading iron ore-producing countries include Australia, Brazil, China, India, the United States, and Russia, among which Australia and Brazil are the dominant exporters for steel producers worldwide. These two countries alone account for approximately 78% of total iron ore exports today (World Steel Association 2020).

In terms of imports, countries such as Japan, the Republic of Korea, Germany, the Netherlands, and China are the major iron ore importers, accounting for 86% of global total in 2017 (U.S. Geological Survey 2017). Notably, China has emerged as the largest importing country since the 2000s. The country depends on imports for procurement of iron ore while itself being one of the largest producers. The production of iron ore in China is estimated to be 360 million tonnes, following only Australia (883 million tonnes) and Brazil (425 million tonnes) in 2017 (U.S. Geological Survey 2017). Figure 2 shows China’s imports of iron ore by weight, together with the amount of crude steel production. As shown in Fig. 2, imports of iron ore have grown dramatically, in line with increasing trends in the country’s steel production during the same period. Iron ore imports into China increased from 70 million tonnes in 2000 to 1,075 million tonnes in 2017. China’s share of global iron ore imports also grew from 14 to 68% during this period (World Steel Association 2002, 2019b). Today, China is the largest consumer of the major iron ore exporters; for instance, the country accounted for 84% of Australia’s iron ore exports in 2017.

As described above, major steel-producing countries depend on imports of raw materials from foreign countries. Tanaka (2012) categorizes the mass-procurement systems for iron ore in the steel industry into three types: captive mines, long-term contracts, and spot trading. The captive mine approach dates back to the beginning of the twentieth century. It was first established and has been mainly practiced in the United States, where steel firms own captive mines domestically and internationally (mostly in Canada and South America). Long-term contracts between steel firms and iron ore suppliers have been adopted by Japanese steel firms since the 1950s. Other countries also began following this system, including the Republic of Korea and European nations, and now, procurement of iron ore by long-term contracts is most commonly used by large steel firms. Notably, from the 1980s, prices were set by the so-called benchmark system, where dominant steel firms and iron ore suppliers negotiated annual prices in the Asian and European markets. The yearly benchmark system was dissolved in 2010; instead, prices began to be negotiated quarterly based on spot market prices. The third system using spot markets was introduced as the pricing regime shifted during this period. Although the traditional practice based on long-term contracts is still predominant in the steel industry, the use of spot trading has been rapidly expanding in response to the increasing demand for steel products in China and other emerging countries.

Figure 3 shows trends in the monthly spot price of iron ore imported into China . The spot price of iron ore has been volatile throughout the period. Monthly prices rose steadily in the first half of 2008, with the highest price being USD 197.12 per dry metric ton unit (dmtu) in March. The market then witnessed a steep decline in the second half of 2008, and the iron ore price has continued to fluctuate in recent decades. After 2008, spot prices again increased to USD 187.18 per dmtu in February 2011, then the lowest price of USD 40.50 per dmtu was marked in December 2015. More recently, the average monthly spot price was USD 93.85 per dmtu in 2019. Within that year, the monthly spot price rose from USD 76.16 per dmtu in January to USD 120.24 per dmtu in July.

(Note The values are in nominal US dollars. Source World Bank [2020])

Trends in iron ore prices

In addition to the unprecedented growth in China’s steel production, natural disaster risks have posed a great concern that may trigger price volatility in steelmaking raw materials. For instance, Australia, one of the largest suppliers of steelmaking raw materials, has experienced extreme weather events in recent years. In November 2010, Australia received record-breaking precipitation in Queensland, the northeastern part of the country. The substantial rainfall and extensive floods in the following months caused widespread damage to the local economy, including coal production in this region (Nihon Keizai Shimbun 2011a). In the affected area, coal mines were inundated, and infrastructure was disrupted (Nihon Keizai Shimbun 2011b). As a result, coal production and shipping were forced into temporary reductions, leading to an increase in the global coal price. Along with the coal price, the price of iron ore reportedly rose during the 2010–2011 flood. Furthermore, iron ore suppliers and steel-producing firms face other climate risks because Australia is also prone to seasonal cyclones. In March 2019, the supply of iron ore was affected by a cyclone that struck in the western part of Australia. The temporary shutdown of a damaged port reportedly contributed to an increase in the iron ore price in spring 2019 (Nihon Keizai Shimbun 2019). More recently, a cyclone hit again in February 2020 and affected shipping of iron ore by destroying ports and railroads in western Australia (Nihon Keizai Shimbun 2020). Because iron ore is an internationally traded commodity, the steelmaking industry can be affected by natural disasters throughout the production process, including the shipping and trading of production inputs.

3 Empirical Analysis

3.1 Estimation Framework

Our empirical analysis aims to investigate the impact of natural disasters on steel production. To examine whether natural disasters affect the production of steel, this study analyzes data on iron ore, which is a key component of raw materials used in the steelmaking process. We use spot prices in China to represent global iron ore prices, with a monthly time series dataset from 2006 to 2019. As we estimate the causal effects of natural disasters on iron ore prices with time series data, this study applies the distributed lag model and incorporates lags for the disaster variables. We begin with the following specification to run the regression model:

where Price is the monthly price of iron ore imported to China, Disaster is the number of natural disasters that occurred in iron ore-exporting countries, Steel is the crude steel production in China, Transport is the shipping cost, and Rate is the exchange rate between the US dollar (USD) and Chinese yuan (CNY). In addition, δ denotes a set of time dummies to capture any external events and other seasonal components that may lead to omitted variable bias. Finally, ε is an error term.

The disaster variable in Eq. 1 includes lags indexed by j. With the distributed lag model, this study attempts to capture dynamic causal effects by using contemporaneous values of natural disasters and lagged values over previous months. When a disaster—for instance, a flood—hits, it is possible that its effects persist for more than one month. Natural disasters could directly cause damage to iron ore mines; moreover, iron ore production and exports may be affected by supply chain disruptions, severe damage to infrastructure, temporary loss of labor productivity, etc. The use of lags enables us to explore such underlying assumptions. For example, the estimated coefficient of the one-month lagged disaster variable indicates whether natural disasters in the previous month affect iron ore prices in the current month. Similarly, the coefficient of the six-month lagged variable estimates the impact of a natural disaster occurring six months ago, the coefficient of the 12-month lagged variable estimates the impact of a natural disaster occurring a year ago, and so forth. This study investigates both the immediate and dynamic effects of natural disasters on the prices of iron ore.

An advantage of using natural disasters in econometric models is that the occurrence of natural disasters itself can most likely be considered exogenous. In this study, we use OLS for the distributed lag regression by assuming that our disaster variable is exogenous. That is, the error term ε in Eq. 1 has a conditional mean of zero, given the present and past values of the disaster variable (Stock and Watson 2015). In other words, ε is uncorrelated with the disaster variables in the present and past periods. Note that it is not assumed that the disaster variables are strictly exogenous, where the error term is uncorrelated with the values of the regressor in all time periods, including past, present, and future. Strict exogeneity cannot hold when iron ore and steel producers can predict future disaster events by forecasting, for example, upcoming hurricanes and the possible flooding that follows. In that case, the error term that includes forecasts of natural disasters is correlated with future disaster occurrences, so strict exogeneity no longer holds.

3.2 Data Description

We construct a time series dataset using several different sources. Data on iron ore spot prices are taken from the World Bank. These are the cost and freight for iron ore imported to China (CFR China). To make the prices comparable, the dollar values for iron ore are adjusted to constant 2015 USD using the US GDP deflator. Although the data source provides long-term data on various commodities, monthly data on iron ore are available only after 2006. Overall, our dataset consists of 168 observations for a sample period from 2006 to 2019.

Data on natural disasters are obtained from the Emergency Events Database (EM-DAT) of the Centre for Research on the Epidemiology of Disasters at the University of Louvain (CRED and Guha-Sapir 2020). The EM-DAT is the most comprehensive disaster database, including more than 22,000 natural and technological disaster events worldwide. This database uses the following criteria for recording disasters: 10 or more people were reportedly killed; 100 or more people were reportedly affected; a state of emergency was declared; or international assistance was appealed for. Disaster events must satisfy at least one of these criteria to be included in the database. We construct a monthly dataset from the event-based disaster data from the EM-DAT.

As our dependent variable, the iron ore price represents the CFR to China. This study uses disaster events in the top 10 countries that export iron ore to China. These countries are chosen according to data on trade values in 2006. Data are obtained from UN Comtrade using Harmonized System (HS) classification codes. To identify iron ore exports, we use the four-digit code HS2601, labeled iron ores and concentrates, including roasted iron pyrites. Figure 4 presents the trade values and weights of iron ore for the 10 exporters included in the empirical analysis. Australia, India, and Brazil were the leading iron ore trading partners for China at the beginning of the sample period. This trend continues to this day, with a significant increase in value and weight. For instance, Australia’s iron ore exports to China exceeded USD 54,000 million or 690 million tonnes, in 2019. With these countries selected, natural disasters in our analysis include extreme temperatures, storms, floods, landslides, droughts, wildfires, earthquakes, and volcanic activity. The variable Disaster represents the total number of natural disasters, including all the abovementioned types, that occurred in a given month.

(Source United Nations [2020])

Top 10 iron ore-exporting countries (exports to China, 2006)

The following control variables are also included in the analysis. While focusing on natural disasters as the variables of interest in this study, we use these control variables to consider possible factors that may affect iron ore prices. These variables are all log-transformed in the regression models. For steel production, we use monthly crude steel production in China provided by the World Steel Association.Footnote 1 Data on the crude oil price are obtained from the World Bank. We use the average spot prices from Brent, Dubai, and West Texas Intermediate. The oil price is included to account for the transport costs of iron ore exports. Considering the effect of freight costs for shipping commodities, it is expected that changing oil (fuel) prices have impacts on the prices of iron ore. The values for this variable are converted into constant 2015 USD. Data on the exchange rate are taken from the IMF and represent the USD/CNY rate. We use this variable to account for Chinese economic conditions, which may impact iron ore exports.

Table 1 shows the descriptive statistics of the variables used in this study. The price of iron ore is shown in USD per dmtu. For the natural disaster variable, the number of events varies from one to 16 per month during the sample period in the 10 countries used in this study. On average, natural disasters occurred approximately 5.7 times per month. Table 1 also presents the variables for individual disaster types. In addition to natural disasters as a whole, this study further explores the specific effect of climate-related disasters in a later section. Our sample shows that floods are the most frequent natural disasters, in line with the global trends in the past two decades (Wallemacq and House 2018).

4 Results

4.1 Main Results

In the empirical analysis, we use Eq. 1 to estimate the contemporaneous and dynamic effects of natural disasters on iron ore prices. Our primary results are presented in Table 2. The estimation models with lag structures include up to a 6-month lag of the disaster variables. These lag variables estimate whether the impact of natural disasters persists during the post-disaster period. All specifications are estimated using heteroskedasticity- and autocorrelation-consistent (HAC) standard errors (Newey and West 1987). Following Stock and Watson (2015), we set the value of five as a rule of thumb for the truncation parameter based on the time period of our sample.

In column 1, we first estimate a static model without lags. The coefficient of the disaster variable is positive but insignificant, suggesting no immediate effect of natural disasters on iron ore prices. In columns 2–4, the results for the dynamic causal impact of natural disasters are presented. The estimation models are structured with one, three, or six lags. While the immediate impact remains insignificant, the lagged variables indicate that natural disasters affect iron ore prices in the post-disaster period. The coefficients of the disaster variables with a one-month lag (L.Disaster) in columns 2–4 are positive and statistically significant, suggesting that an additional disaster event in the previous month increases the price of iron ore in the present month by 1.1–1.3%. This dynamic effect is also observed when lagged variables are added in the models. In column 4, the lagged disaster variables are positively correlated with iron ore prices. The coefficients of the lagged variables indicate that a past disaster event is estimated to raise current iron ore prices by 1.1–1.6%. The findings show that the impact of natural disasters could persist for five months.

In columns 5–8, the models are estimated with additional control variables. The results are mostly consistent with regard to the disaster variables. Although the magnitude of the coefficients becomes slightly smaller than those in columns 1–4, the results suggest the robustness of the impact of natural disasters on iron ore prices. Steel production is positively related to iron ore prices. The coefficients of steel production are statistically significant, indicating that a 1% increase in China’s steel production is associated with a 1.1–1.3% increase in iron ore spot prices. We also find that the oil price is statistically correlated with iron ore prices. The findings imply that transport costs for export affect commodity prices, thus increasing input prices for steel production. On the other hand, we do not find a correlation between the exchange rate and iron ore prices. The results show that the coefficients are insignificant across alternative models. In the bottom rows of Table 2, the F statistics for the joint significance of time fixed effects are presented. The results are similar across alternative models in columns 1–4 and 5–8. The year dummies are jointly significant in all specifications, while the month dummies are jointly significant in the models with control variables.

4.2 Cumulative Effect of Natural Disasters

This section examines the cumulative effect of natural disasters on iron ore prices. The primary analysis in Sect. 4.1 suggests that more frequent natural disasters cause an increase in iron ore prices. By incorporating lags, we find a correlation between iron ore prices and natural disasters occurring a month prior, two months prior, and so forth. To understand the dynamic causal effects in more detail, this section analyzes whether and to what extent natural disaster events cumulatively affect the iron ore price in the present month. To estimate the cumulative dynamic effect, the distributed lag model in Eq. 1 is modified as follows:

where the coefficient θ1,j for the disaster variables is now the j-month cumulative dynamic multiplier (Stock and Watson 2015). The cumulative dynamic multipliers show the cumulative effect of natural disasters on iron ore prices over j months. For example, the one-month cumulative dynamic multiplier is denoted as θ1,1 and is equivalent to the sum of the zero-month dynamic effect β1,0 and the one-month dynamic effect β1,1 in Eq. 1. The coefficient θ1,L+1 therefore denotes the total sum of the dynamic multipliers, namely, β1,0 + β1,1 + β1,2 + … + β1,L.

The results for the cumulative dynamic effects are presented in Table 3. Similar to the main results, we find that the occurrence of natural disasters is associated with the price volatility of iron ore. The estimation model in column 1 includes disaster lags for six months and corresponds to the model in column 4 in Table 2. Here, the coefficient of the one-month lagged variable L.Disaster shows the cumulative effects of natural disasters over the past two months (the previous and present months), the coefficient of the two-month lagged variables L2.Disaster shows the cumulative effects over the past three months, and so forth. The coefficient of the six-month lagged disaster variable—i.e., the six-month cumulative dynamic multiplier—is positive and statistically significant at the 1% level. The findings suggest that the sum of the effect of natural disasters that occurred over six months induces an 8.2% increase in iron ore prices.

The following models in Table 3 explore alternative specifications and check the robustness of the estimation results. First, we reestimate the model by changing the value for the HAC truncation parameter to 10. The results are reported in column 2. The coefficients are quite similar to those in column 1, confirming that an alternative HAC truncation parameter does not alter the results. Second, we expand the model by adding the lags of disaster variables to examine whether the disaster impact persists for a longer period. In column 3, the results are similar and exhibit the cumulative dynamic effects of natural disasters on iron ore prices. For example, the coefficient of the three-month lagged variable is positive and statistically significant, indicating that the total effects of natural disasters over three months raise iron ore prices by 3.9%. Similarly, the cumulative effects of natural disasters cause an increase in iron ore prices by 7.1% in six months. We do not find the coefficients of lagged variables to be statistically significant after six months.

Figure 5 illustrates these estimated dynamic effects in more detail. Using the estimated result in column 3 in Table 3, Fig. 5a decomposes the cumulative effects and depicts the individual dynamic effect of natural disasters in each month, while Fig. 5b shows the cumulative dynamic effects for 12 months. In Fig. 5a, the dynamic effects appear to be positive for the first seven month lags and then become negative afterward. Given these positive and negative values, the cumulative dynamic effects increase over seven months, as shown in Fig. 5b. Although it remains positive, the estimated cumulative effects gradually decrease after reaching the peak, as the individual dynamic effects become negative during the eighth month.

(Note The solid lines represent the estimated effects, and the dashed lines represent the 90% confidence interval. The estimated model includes 12 lags of the disaster variable)

Dynamic effect of natural disasters on the iron ore price

In addition, we test the robustness of these results by estimating the models with control variables. The models in columns 4–6 show the corresponding results. Again, we find that past disaster events are statistically correlated with price volatility. The positive signs of the coefficients show that the occurrence of natural disasters over the past months cumulatively affects iron ore exports, thereby increasing prices. The findings suggest that the cumulative effects persist for six months after the onset of natural disasters.

Overall, the results in Sects. 4.1 and 4.2 show the dynamic causal effect of natural disasters on the prices of iron ore. By incorporating lagged variables, we find that a price increase is induced several months after natural disasters. The analysis also reveals the total impact of natural disasters in the post-disaster period by estimating the cumulative dynamic multipliers. These results imply that steel producers may suffer from the costs of natural disasters as a negative consequence of higher iron ore prices. This is indeed the case when steel firms cannot increase the prices of their final products to cushion price increases in raw materials (Astier 2015). The findings suggest that natural disasters lead to price fluctuations, causing a negative impact in the steel and iron ore industries.

4.3 Effect of Natural Disasters by Type

We further analyze the impact of natural disasters on iron ore prices by investigating the individual disaster types. Iron ore production and exports may be more sensitive to some natural hazards than others. Moreover, climate shocks such as frequent floods and intense tropical storms have been a great concern for steel producers in recent years. Therefore, this additional analysis explores possible heterogeneity in the effects of extreme weather events, with a focus on climate-related disasters. We run regressions using Eq. 2, which estimates the cumulative dynamic effects. The disaster variables now indicate the number of occurrences for a particular disaster type, that is, floods, storms, droughts, or extreme temperatures.

The estimation results are provided in Table 4. All specifications include six lags of the disaster variable and control variables. In column 1, the results show that floods have an impact on iron ore prices. The coefficients of all lagged variables except the first appear positive and statistically significant. As shown in the six-month lagged variable, the cumulative dynamic effects of floods drive up the current price of iron ore by 4.5%. In contrast, the results in column 2 show a negative correlation between storms and iron ore prices. We find dynamic and immediate impacts of storms that lower iron ore prices. The negative sign of the coefficients is not what we expected; nevertheless, the findings show that the market prices of traded commodities may be affected by natural disasters in exporting countries. In column 3, droughts appear to have a positive impact on iron ore prices. The results suggest that droughts tend to increase the prices of iron ore in the early months. In total, the coefficients of the six-month lagged variable indicate that an additional drought event is associated with a 5.8% increase in iron ore prices. Column 4 reports the results for extreme temperatures. We find that extreme temperatures do not immediately affect iron ore prices. The coefficients of the cumulative dynamic multipliers are positive and significant after the four-month lag. The findings suggest that in the long run, extreme temperatures induce a 9.7% increase in iron ore price over six months. The estimation results from individual natural disaster events show evidence of climate-induced price volatility that may affect the iron ore market.

5 Conclusions

This chapter examined the effect of natural disasters on the prices of iron ore, an important raw material used in steel production. The empirical investigation used spot prices of iron ore imported in China to examine whether price volatility is induced by natural disasters occurring in iron ore-exporting countries. Considering the persistent impact of natural disasters that may last after the onset, we estimated the dynamic effect of disasters by incorporating lagged variables in the analysis.

The main results showed that iron ore prices are significantly affected by the occurrence of natural disasters in exporting countries. The estimation results from the models with lag structure demonstrate that significant impacts persist in the post-disaster period, causing an increase in iron ore prices. We found that iron ore prices are estimated to increase by 1.1–1.6% by a disaster event in the previous months. These findings suggest that more frequent disasters may disturb the iron ore market by accelerating price fluctuations. The results were robust when the models included control variables. In addition to natural disasters, we found that steel production in China has a significant impact that drives iron ore prices. Transportation costs, measured by oil prices, also showed a positive association with iron ore prices.

Moreover, an additional analysis estimated the cumulative dynamic effect of natural disasters. The results were similar to the primary results that natural disasters were significantly related to iron ore prices over several months. The findings showed that natural disasters over six months raise iron ore prices by 8.2% in total. When we added more lags in the model, cumulative dynamic effects were also observed over six months, while a significant effect no longer appeared afterward.

This chapter illustrated the relationship between the steel industry and natural disasters, highlighting higher prices of one steelmaking raw material driven by the occurrence of natural disasters. Steel firms worldwide largely depend on imports of raw materials from several different countries. This study suggests that when iron ore exporters are hit by natural disasters, an economic consequence could appear in the prices of imported commodities. In other words, the negative impact may not be limited to a country hit by natural disasters but may further spread to steel producers through the global supply chain. For iron ore-exporting countries, higher export prices could be a disadvantage because they lower the relative costs of domestic iron ore in China and make the iron ore market more competitive (Astier 2015). Moreover, the findings of this study may have important implications for iron ore suppliers and policymakers regarding disaster risk reduction. To reduce the costs of current and future climate change, addressing disaster risks is important in the iron ore-exporting countries. This includes both pre- and post-disaster planning and operations, for example, investment in disaster-resilient facilities and infrastructure through the application of the Building Back Better (BBB) framework (UNISDR 2017). For steel-producing countries, higher raw material costs can also be problematic. In addition to the emerging influence of China’s economic growth, natural disasters may trigger price volatility, which causes steel production to be more unstable. Notably, steel firms must bear the higher costs of inputs if they cannot pass along these price increases to their customers in the form of higher steel product prices (Astier 2015). These potential consequences imply that steel firms should pay attention to natural disaster risks associated with procurement of raw materials. Furthermore, an increase in spot market prices may have a broader impact given that the quarterly negotiated prices of iron ore are influenced by spot market prices. In this regard, it is possible to assume that the pricing systems of the iron ore market may continue to transform depending on the economic and political conditions of the leading players in the steel and iron ore industries. Further expansion of spot trading can also be anticipated in raw material markets. Future research must focus on such complex and unique situations to further examine the effect of climate on the iron ore market.

Notes

- 1.

Available at https://www.worldsteel.org/.

References

Anttila-Hughes, J.K., and S.M. Hsiang. 2013. Destruction, disinvestment, and death: Economic and human losses following environmental disaster. SSRN. https://doi.org/10.2139/ssrn.2220501.

Astier, J. 2015. Evolution of iron ore prices. Mineral Economics 28: 3–9.

Chen, S., X. Chen, and J. Xu. 2016a. Impacts of climate change on agriculture: Evidence from China. Journal of Environmental Economics and Management 76: 105–124.

Chen, W., Y. Lei, and Y. Jiang. 2016b. Influencing factors analysis of China’s iron import price: Based on quantile regression model. Resources Policy 48: 68–76.

CRED, Guha-Sapir D. 2020. EM-DAT: The emergency events database. Université Catholique de Louvain (UCL), Brussels, Belgium. www.emdat.be. Accessed 17 March 2020.

Dallmann, I. 2019. Weather variations and international trade. Environmental and Resource Economics 72 (1): 155–206.

Dell, M., B.F. Jones, and B.A. Olken. 2009. Temperature and income: Reconciling new cross-sectional and panel estimates. American Economic Review 99 (2): 198–204.

Dell, M., B.F. Jones, and B.A. Olken. 2012. Temperature shocks and economic growth: Evidence from the last half century. American Economic Journal: Macroeconomics 4 (3): 66–95.

Dell, M., B.F. Jones, and B.A. Olken. 2014. What do we learn from the weather? The new climate–economy literature. Journal of Economic Literature 52 (3): 740–798.

Heal, G., and J. Park. 2016. Temperature stress and the direct impact of climate change: A review of an emerging literature. Review of Environmental Economics and Policy 10 (2): 347–362.

Hsiang, S.M. 2010. Temperatures and cyclones strongly associated with economic production in the Caribbean and Central America. Proceedings of the National Academy of Sciences 107 (35): 15367–15372.

Jones, B.F., and B.A. Olken. 2010. Climate shocks and exports. The American Economic Review 100 (2): 454–459.

Leiter, A.M., H. Oberhofer, and P.A. Raschky. 2009. Creative disasters? Flooding effects on capital, labour and productivity within European firms. Environmental and Resource Economics 43 (3): 333–350.

Marchiori, L., J.F. Maystadt, and I. Schumacher. 2012. The impact of weather anomalies on migration in sub-Saharan Africa. Journal of Environmental Economics and Management 63 (3): 355–374.

Maystadt, J.F., and O. Ecker. 2014. Extreme weather and civil war: Does drought fuel conflict in Somalia through livestock price shocks? American Journal of Agricultural Economics 96 (4): 1157–1182.

McDermott, G.R., and Ø.A. Nilsen. 2014. Electricity prices, river temperatures, and cooling water scarcity. Land Economics 90 (1): 131–148.

Newey, W.K., and K.D. West. 1987. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55 (3): 703–708.

Nihon Keizai Shimbun. 2011a. Gou kouzui, keizai wo appaku (Floods hit Australia’s economy). Nihon Keizai Shimbun 31 January 2011.

Nihon Keizai Shimbun. 2011b. Tekko, sekitan shokku futatabi (Steel industry affected by coal shock again). Nihon Keizai Shimbun 27 January 2011.

Nihon Keizai Shimbun. 2019. Tekko seki, 100 doru dai nose (Iron ore price rises above $100). Nihon Keizai Shimbun 25 May 2019.

Nihon Keizai Shimbun. 2020. Rio Tinto, tekkoseki shukkaryou 5% zou (Rio Tinto’s iron ore shipping increase by 5%). Nihon Keizai Shimbun 18 April 2020.

Noy, I. 2009. The macroeconomic consequences of disasters. Journal of Development Economics 88 (2): 221–231.

Stock, J.H., and M.W. Watson. 2015. Introduction to econometrics, Update, Global Edition, 3rd ed. England: Pearson Education.

Sukagawa, P. 2010. Is iron ore priced as a commodity? Past and Current Practice. Resources Policy 35 (1): 54–63.

Tanaka, A. 2012. Sengo nihon no shigen bijinesu: Genryo chotatsu shisutem to sogo shosha no hikaku keieishi (Postwar Japan’s mineral industry: A comparative history of its procurement system and sogo shosha). Nagoya: The University of Nagoya Press.

Tcha, M., and D. Wright. 1999. Determinants of China’s import demand for Australia’s iron ore. Resources Policy 25 (3): 143–149.

UNISDR. 2017. Build back better in recovery, rehabilitation and reconstruction. https://www.undrr.org/publication/words-action-guidelines-build-back-better-recovery-rehabilitation-and-reconstruction. Accessed 6 December 2020.

United Nations. 2020. UN Comtrade database. https://comtrade.un.org/data/. Accessed 9 October 2020.

US Geological Survey. 2017. 2017 Minerals Year Book. https://prd-wret.s3.us-west-2.amazonaws.com/assets/palladium/production/atoms/files/myb1-2017-feore.pdf. Accessed 31 October 2020.

Wallemacq, P., and R. House. 2018. UNISDR and CRED report: Economic Losses, Poverty & Disasters (1998–2017). Centre for Research on the Epidemiology of Disasters (CRED).

Wilson, J.D. 2012. Chinese resource security policies and the restructuring of the Asia-Pacific iron ore market. Resources Policy 37 (3): 331–339.

World Bank. 2020. World Bank commodity price data. https://www.worldbank.org/en/research/commodity-markets. Accessed 6 February 2020.

World Steel Association. 2002. World steel in figures 2002. https://www.worldsteel.org/en/dam/jcr:813fbac5-1c90-44f1-a758-c163d28047f5/World%2520Steel%2520in%2520Figures%25202002.pdf. Accessed 1 November 2020.

World Steel Association. 2008. Steel statistical yearbook 2008. https://www.worldsteel.org/en/dam/jcr:1044cace-dd58-4bf6-a59a-139249fd5170/Steel%2520statistical%2520yearbook%25202008.pdf. Accessed 31 October 2020.

World Steel Association. 2018. Steel statistical yearbook 2018. https://www.worldsteel.org/en/dam/jcr:e5a8eda5-4b46-4892-856b-00908b5ab492/SSY_2018.pdf. Accessed 31 October 2020.

World Steel Association. 2019a. Steel and raw materials. https://www.worldsteel.org/en/dam/jcr:16ad9bcd-dbf5-449f-b42c-b220952767bf/fact_raw%2520mat erials_2019.pdf. Accessed 30 October 2020.

World Steel Association. 2019b. World steel in figures 2019. https://www.worldsteel.org/en/dam/jcr:96d7a585-e6b2-4d63-b943-4cd9ab621a91/World%2520Steel%2520in%2520Figures%25202019.pdf. Accessed 1 November 2020.

World Steel Association. 2020. world steel in figures 2020. https://www.worldsteel.org/en/dam/jcr:f7982217-cfde-4fdc-8ba0-795ed807f513/World%2520Steel%2520in%2520Figures%25202020i.pdf. Accessed 1 November 2020.

Wårell, L. 2014. The effect of a change in pricing regime on iron ore prices. Resources Policy 41: 16–22.

Zhu, X., W. Zheng, H. Zhang, and Y. Guo. 2019. Time-varying international market power for the Chinese iron ore markets. Resources Policy 64: 101502.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Author(s), under exclusive license to Springer Nature Singapore Pte Ltd.

About this chapter

Cite this chapter

Tembata, K. (2021). Natural Disaster Shocks and Raw Material Prices in the Steel Industry. In: Ma, J., Yamamoto, M. (eds) Growth Mechanisms and Sustainability. Palgrave Macmillan, Singapore. https://doi.org/10.1007/978-981-16-2486-5_5

Download citation

DOI: https://doi.org/10.1007/978-981-16-2486-5_5

Published:

Publisher Name: Palgrave Macmillan, Singapore

Print ISBN: 978-981-16-2485-8

Online ISBN: 978-981-16-2486-5

eBook Packages: Economics and FinanceEconomics and Finance (R0)