Abstract

The power generation mix of the Association of Southeast Asian Nations (ASEAN) is dominated by fossil fuels, which accounted for almost 80% in 2017 and are expected to account for 82% in 2050 if the region does not transition to cleaner energy systems. Solar and wind power is the most abundant energy resource but contributes negligibly to the power mix. Scalable electricity production from wind and solar energy faces tremendous challenges due to system integration practices in ASEAN. Investors in solar or wind farms face high risks from electricity curtailment if surplus electricity is not used. Technologies for battery storage (lithium-ion batteries) have been developed to handle surplus electricity production from wind and solar energy but they remain costly. Hydrogen produced from electrolysis using surplus electricity, however, has numerous advantages that complement battery storage, as hydrogen can be stored as liquid gas, which is suitable for many uses and easy to transport. Employing the policy scenario analysis of the energy outlook modelling results, this paper examines the potential scalability of renewable hydrogen production from curtailed electricity in scenarios of high share of variable renewable energy in the power generation mix. The study intensively reviewed potential cost reduction of hydrogen production around the world and its implications for changing the energy landscape. The study found many social and environmental benefits as hydrogen can help increase the share of renewables in decarbonising emissions in ASEAN.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

JEL Codes

1 Introduction

The economic, social, and political dynamics of the Association of Southeast Asian Nations (ASEAN) have made it one of the fastest-growing regions. However, Southeast Asia faces great challenges in matching its energy demand with sustainable energy supply as the region transitions to a lower-carbon economy. The transition requires development and deployment of green energy sources. Growing energy demand can be met by energy supply produced by renewables and other clean energy alternatives such as hydrogen and by clean technologies. Whilst Organisation for Economic Co-operation and Development (OECD) countries have quickly reduced greenhouse gas emissions in response to the commitments of the Paris Climate Conference or the 21st Conference of the Parties (COP21), developing Asia has some way to go to balance economic growth and affordable and available energy. Much of the future energy mix of emerging ASEAN countries will rely on fossil fuel to power economic development. However, they can follow a renewable energy path to economic growth, social well-being, and environmental sustainability.

Increasing the share of renewables is hindered by the trade-off between political issues, energy affordability, and affordable technologies. Although countries have rich wind and solar resources, production of scalable electricity is greatly encumbered by system integration practices. Investors in solar or wind farms will face high risks from electricity curtailment when they produce too much electricity and grid cannot absorb it. In this case, the curtailed electricity poses risks to solar or wind projects’ revenue if there is no technology to utilise or store the surplus electricity. Many countries have recently developed technologies for battery storage (lithium-ion batteries) for surplus electricity produced from wind and solar energy, but battery storage remains costly. Hydrogen produced from electrolysis using surplus electricity, however, has numerous advantages that complement battery storage, as hydrogen can be stored as liquid gas, which is suitable for many uses and easy to transport.

In the past 10 years, renewable energy proponents have rarely mentioned hydrogen although it is frequently used in the ammonia, petrochemical, and oil refining industries. The use of hydrogen has been accelerating, however, as it is versatile and can be produced from many energy sources. Hydrogen fuels have untapped potential as clean energy. About 120 million tonnesFootnote 1 of hydrogen are produced globally, of which two-thirds are pure hydrogen and one-third mixed with other gases (IEA 2020). Hydrogen can be produced from either fossil fuels or from renewables. About 95% of hydrogen is produced from coal and gas without carbon capture, sequestration, and storage (CCS) (‘grey’ hydrogen), with only small amounts produced with CCS (‘blue’ hydrogen). About 5% of total hydrogen production uses renewables (‘green’ hydrogen [H2]). Reducing greenhouse gas emissions is high on the global agenda under COP 21 and the upcoming COP26, which will require leaders to pursue alternative fuel pathways, shifting from fossil fuel–based to clean energy systems. Although its share remains small in global energy consumption, hydrogen fuel represents positive growth potential as world leaders start to see the great benefit and promise of its use to abate climate change. Hydrogen fuel enjoys political support in many advanced countries, including Germany, the Netherlands, and several other OECD countries. In many ASEAN countries, hydrogen as an alternative fuel is not yet on the policy agenda. The ASEAN Plan of Action for Energy Cooperation (APAEC) Phase 2, however, will include policy measures to encourage emerging and alternative technologies such as hydrogen and energy storage.

The potential use of hydrogen in transport, power generation, and industry has been proven by projects around the world. Renewable hydrogen has attracted leaders’ attention as an option to increase the share of renewables in electrical grids amidst the falling cost of renewable electricity from wind and solar energy. The International Renewable Energy Agency (IRENA 2018) predicted that the cost of electrolysers, the devices used to produce hydrogen from water, will halve from US$840 now to US$420 per kilowatt by 2040. Renewable hydrogen production could be the cheapest energy option in the foreseeable future. The cost-competitiveness of producing renewable H2 is key for the wide adoption of hydrogen. Renewable H2 production costs dropped drastically from US$10–US$15/kilogram (kg) in 2010 to US$4–US$6/kg in 2020 (Hydrogen Council 2020). Costs are expected to decrease to US$2.00–US$2.50/kg of H2 in 2030, which is competitive with hydrogen production using natural gas through steam methane reforming with CCS.

Hydrogen is a clean energy carrier and can be stored and transported for use in hydrogen-run vehicles, synthetic fuels, upgrading of oil and/or biomass, ammonia and/or fertilizer production, metal refining, heating, and other end uses. Developing hydrogen, therefore, is an ideal pathway to sustainable clean energy systems and can help scale renewables such as solar and wind energy. Adopting renewable hydrogen would bring more renewables into the energy mix and could be a game changer in the transition from fossil dependence to a cleaner energy system. Hydrogen could help integrate the current electricity system with wind and solar energy. Solar and wind penetration of the electrical grid is hindered by the high intermittency of electricity from wind and solar energy, and many grid operators around the world are, therefore, hesitant to include a large share of it. For ASEAN Member States (AMS) that can afford to invest more in renewable energy, an important concern is the need for electricity storage and smart grids to support higher renewable energy penetration levels. Smart grid technologies already significantly contribute to electricity grids in some OECD countries. However, these technologies are continually being refined and are vulnerable to potential technical and nontechnical risks. Renewable energy growth is constrained by weak infrastructure development and the slow deployment of technology, including the capacity to assess and predict the availability of renewable energy sources in many developing countries. Hydrogen can provide an unlimited supply of electricity from wind and solar energy. How it works is simple. On-site electrolysers convert electricity excess from wind and solar energy into hydrogen, which can be stored for a longer time and used to produce electricity, industrial heat, vehicle fuel cells, and fertilizers such as ammonia, and to power petrochemical processes.

2 The Study’s Objectives and Structure

The study investigates the potential of renewable hydrogen as a clean energy source for ASEAN’s energy mix, which will need huge investment in hydrogen energy–related industries. The paper aims to do the following:

-

(i)

Use energy modelling scenarios to explore policy options of increasing the share of renewables, particularly wind and solar energy, in the power mix, and explore the possibility of electricity curtailment resulting from the high share of renewables that can be converted to hydrogen production.

-

(ii)

Estimate the potential emission abatement resulting from the introduction of hydrogen produced using curtailed renewable electricity.

-

(iii)

Review scalable renewable electricity from wind and solar energy from a cost reduction perspective, considering global experience.

-

(iv)

Review technologies and cost perspectives of hydrogen produced using curtailed electricity.

-

(v)

Review a hydrogen policy and road map that can be applied to ASEAN.

Hydrogen adoption and development could be highly beneficial for ASEAN. Renewable hydrogen will enable the deployment of variable renewable energy (VRE) and will be a game changer by breaking the barrier of integrated traditional power systems, which cannot absorb a high share wind and solar energy. The paper highlights how public awareness and participation in promoting hydrogen use, especially willingness to pay and public financing of renewable hydrogen production, will promote investment. Section 8.2 reviews the literature. Section 8.3 explains the methodological approaches. Section 8.4 discusses the study’s results. Section 8.5 draws conclusions and recommends policy.

3 Literature Review

3.1 Hydrogen Adoption and Development

The Economic Research Institute for ASEAN and East Asia’s research on hydrogen energy since 2017 has identified the significant potential of hydrogen energy supply and demand in East Asia. By 2040, the cost of hydrogen will decrease by more than 50% if it is adopted in all sectors. The target price of US$2.00–US$2.50/kg of H2 in 2040 is competitive with the price of gasoline. The cost of supplying hydrogen is about 3–5 times higher than that of gas, mainly due to limited investment in hydrogen supply chains and the lack of a strategy to widely adopt hydrogen usage. The wide adoption and usage of hydrogen will need time to ensure cost-competitiveness and safety, especially for automobiles. The large-scale hydrogen-based energy transition from ‘grey’ and ‘blue’ to ‘green’ hydrogen will happen concurrently with a global shift to renewables. ‘Green’ hydrogen can face current system integration challenges that have blocked increasing the share of wind and solar energy.

Hydrogen uptake will happen in several ways. The European Union’s ambition to make Europe the first climate-neutral continent by 2050 includes a large role for hydrogen fuel. Many OECD hydrogen projects will come online by 2023, including electrolysers and pipelines to distribute hydrogen to end users. Since hydrogen is a clean energy carrier, it has the best prospect of accelerating hydrogen storage in island countries such as Indonesia, Malaysia, the Philippines, Brunei, Australia, and New Zealand. In East Asia, China is one of the biggest potential producers and consumers of hydrogen energy. China has recently accelerated hydrogen investment support to local industries, where about $2 billion is expected to be invested in the next few years. China plans to put in place 300 hydrogen fuelling stations in 2025 and scale up to 1000 by 2030 to support the deployment of 50,000 to 1 million fuel cell electric cars from 2025 to 2030 (Hydrogen Council 2019). Japan is promoting the global adoption of hydrogen for vehicles, power plants, and other potential uses. Japan had planned to provide the 2020 Olympics with fuel cell shuttle buses.

In the United States (US), more than 10 million tonnes of hydrogen are produced annually to meet demand mainly in oil refining and in ammonia production for fertilizer. About 95% of hydrogen produced in the US comes from natural gas feedstock (DOE 2020c). The US has about 1600 miles of hydrogen pipeline, more than 26,000 hydrogen fuel cell forklifts in use, more than 30 hydrogen fuel cell buses, and more than 40 public stations supporting more than 7500 fuel cell cars. California alone has about 40 hydrogen stations for passenger cars; other states with such stations include Connecticut, Hawaii, Massachusetts, Michigan, and South Carolina. On 23 January 2020, the US Department of Energy announced up to US$64 million in funding to advance innovations that will support transformational research and development (R&D), and innovative hydrogen concepts that will encourage market expansion and increase the scale of hydrogen production, storage, transport, and use.

In ASEAN, Brunei Darussalam leads in the hydrogen supply chain and has supplied liquefied hydrogen from Muara port to Japan since late 2019. However, the liquefied hydrogen process consumes a great deal of energy to cool gaseous hydrogen into liquid hydrogen at temperatures of –253 °C and lower. The hydrogen supply chain demonstration project, in cooperation with Japan’s government, explored an alternative way of shipping hydrogen using a new technology called liquid organic hydrogen carrier. If the technology is economically viable, it will pave the way for market access worldwide and overcome hydrogen supply chain barriers.

The use of hydrogen is expanding in transport and gaining momentum. For example, India is starting to call for foreign investment in fuel cell vehicles and hydrogen transport infrastructure development in some pilot cities. In Japan, the Tokyo metropolitan government will increase the number of hydrogen buses to 100 in 2020, and in Malaysia, the Sarawak government will soon start to operate hydrogen buses. Singapore is working closely with Japanese companies to explore developing hydrogen fuel to decarbonise emissions.

Japan is pioneering the renewable hydrogen economy, in which producing hydrogen through electrolysis of renewable electricity from wind, solar, and nuclear energy could be a game changer in decarbonising emissions. Japan is the first country in East Asia to adopt a basic hydrogen strategy to make sure that hydrogen production will reach cost parity with gasoline fuel and power generation in the long term. A 2019 Fuji Keizai market survey of potential hydrogen demand in Japan indicated that hydrogen demand will increase 56-fold by 2030, needing investment estimated at more than JPY400 billion. Although Japan’s government and businesses are making efforts to kick-start hydrogen adoption and usage, realising a hydrogen society will largely depend on whether the cost of hydrogen production is competitive and whether society is willing to pay. The Republic of Korea has set a bold target for hydrogen use: 10% of total energy consumption by 2030 and 30% by 2040 to power selected cities and towns.

In many ASEAN countries, hydrogen is not yet on the policy agenda as an alternative fuel. However, APAEC, which is under preparation for endorsement at the ASEAN Ministers on Energy Meeting in November 2020, will include policy measures to promote emerging and alternative technologies such as hydrogen and energy storage. APAEC will help AMS increase their adoption of hydrogen to enlarge the share of hydrogen in the energy mix.

3.2 Selected Pathways of Hydrogen Production Processes

Hydrogen emits zero emissions when used in combustion for heat and energy. If pure hydrogen (H2) combusts by reacting with oxygen (O2), it will form water (H2O) and release energy that can be used as heat, in thermodynamics, and for thermal efficiency. Hydrogen is the most abundant chemical substance in the universe, but it is rarely found in pure form (H2) because it is lighter than air and rises into the atmosphere. Hydrogen is found as part of compounds such as water and biomass and in fossil fuels such as coal, gas, and oil (DOE 2020a). Several ongoing researches use two processes to extract hydrogen fuel: steam methane reforming, mainly applied to extract hydrogen from fossil fuels, and electrolysis of water, applied to extract hydrogen from water using electricity.

Steam methane reforming extracts hydrogen from methane using high-temperature steam (700–1000 °C). The product of steam methane reforming is hydrogen, carbon monoxide, and small amount of carbon dioxide (DOE 2020b). Most hydrogen is produced through this process, which is the most mature technology. Given how cheap natural gas is in the US and other parts of the world, hydrogen is one pathway to transition to a cleaner economy if steam methane reforming can be augmented with CCS. Technically, the chemical reaction process can be written as follows.

Steam methane reforming reaction (heat must be supplied through an endothermic process):

Applying water–gas shift reaction produces more hydrogen:

At this stage, carbon dioxide and other impurities are removed from the gas stream, so the final product is pure hydrogen.

Instead of steam methane reforming, partial oxidation can be applied to methane gas to produce hydrogen. However, the partial oxidation reaction produces less hydrogen fuel than does steam methane reforming. Technically, partial oxidation is an exothermic process, producing carbon monoxide and hydrogen and giving off heat:

Applying a water–gas shift reaction produces more hydrogen:

Electrolysis can produce hydrogen by splitting water into hydrogen and oxygen in an electrolyser, which consists of an anode and a cathode. Electrolysers may have slightly different functions depending on the electrolyte material used for electrolysis.

The polymer electrolyte membrane (PEM) electrolyser is an electrochemical device to convert electricity and water into hydrogen and oxygen. The PEM electrolyte is solid plastic. The haft reaction that takes place on the anode side forms oxygen, protons, and electrons:

The electrons flow through the external circuit and the hydrogen ions move across the PEM to the cathode, in which hydrogen ions combine with electrons from the external circuit to form hydrogen gases:

PEM electrical efficiency is about 80% in terms of hydrogen produced per unit of electricity used to drive the reaction. PEM efficiency is expected to reach 86% before 2030.

Another method is alkaline water electrolysis, which takes place in an alkaline electrolyser with alkaline water (pH > 7) with an electrolyte solution of potassium hydroxide (KOH) or sodium hydroxide (NaOH). In the alkaline electrolyser, the two electrodes are separated. Hydroxide ions (OH−) are transported through the electrolyte from cathode to anode, with hydrogen generated on the cathode side. This method has been commercially available for many years, and the new method of using solid alkaline exchange membrane is promising as it is working in a laboratory environment.

4 Methodology and Scenario Assumptions

Hydrogen is used mainly to produce petrochemicals and ammonia. The potential of hydrogen, however, clearly remains untapped in ASEAN countries because it is a clean energy carrier that can be produced from various sources using fossil fuel and renewable energy. To build a hydrogen society, the cost of producing hydrogen must be competitive with that of conventional fuels, such as gas, for transport and power generation.

Renewable or ‘green’ hydrogen must be produced using renewable electricity from wind, solar, hydropower, and geothermal energy. Excess electricity from nuclear power, however, could be used to produce hydrogen as nuclear power plants provide base-load power and cannot be easily ramped up and down. During low demand, electricity from nuclear energy and VRE could be used to produce hydrogen. To produce renewable hydrogen using VRE, it is important to know the predicted available curtailed electricity resulting from power system integration challenges due to higher share of renewables.

Two components determine the cost to produce ‘green’ hydrogen: electricity cost from renewables and the cost of electrolysis. If these costs could be reduced significantly to allow the cost of hydrogen production to be competitive with that of natural gas, then hydrogen adoption and usage could be accelerated. This study reviews the falling cost of VRE and electrolysis to see how their current and future cost could allow competitive hydrogen production cost. High VRE penetration of the electrical grid is the biggest challenge for the grid operator as electricity from VRE is variable and intermittent. Upgrading the grid system with the Internet of Things to create a smart grid could allow more penetration by VRE; otherwise, VRE electricity would be greatly curtailed due to a weak power grid system. This study calculates potential renewable hydrogen production and potential emission abatement under various scenarios assuming the following:

-

(i)

Under current grid system integration, curtailment is likely to be 20–30% if the VRE share in the power mix exceeds more than 10%. Given the large potential of hydropower, geothermal, wind, and solar energy, increasing the share of renewables is technically possible using hydrogen storage. The study assumes the following scenarios: replacement by renewables of total combined fossil fuel generation (coal, oil, and gas) by 10, 20, and 30% by 2050, or Scenario1 = 10%, Scenario2 = 20%, and Scenario3 = 30%.

-

(ii)

In Scenario1, Scenario2, and Scenario3, renewable hydrogen producing using curtailed electricity is calculated based on assumptions of curtailed electricity generated from renewables at the rate of 20–30% of total generation from renewables. Potential renewable hydrogen produced using curtailed electricity in Scenario1, Scenario2, and Scenario3 is expressed as Scenario1 H2, Scenario2 H2, and Sceario3 H2.

-

(iii)

The formulas to calculate potential renewable hydrogen production in the renewable scenarios are as follow:

Scenario1H2 (Mt-H2) = [Scenario1 (TWh) X (Percentage of curtailed electricity)/48 (TWh)

Scenario2H2 (Mt-H2) = [Scenario2 (TWh) X (Percentage of curtailed electricity)/48 (TWh)

Scenario3H2 (Mt-H2) = [Scenario3 (TWh) X (Percentage of curtailed electricity)/48 (TWh)

Mt-H2 stands for million tonnes of hydrogen; TWh is terawatt-hour; percentage of curtailed electricity is 20–30% of total generation from renewables. The study also applies the conversion factor of 48 kilowatt-hours (kWh) of electricity needed to produce 1 kg H2 (ISES 2020).

-

(iv)

The potential emission abatement is the difference between (a) the business as usual (BAU) scenario and (b) the alternative policy scenario (APS) and other high-renewable-share scenarios such as Senario1, Scenario2, and Scenario3.

To estimate potential hydrogen produced using curtailed electricity, the power generation mix for the BAU and APS is estimated using ASEAN countries’ energy models by applying the Long-range Energy Alternative Planning System (LEAP) software, an accounting system to project energy balance tables based on final energy consumption and energy input and/or output in the transformation sector. Final energy consumption is forecast using energy demand equations by energy and sector and future macroeconomic assumptions.

In the modelling work applying LEAP, the baseline of 10 AMS was 2017, the real energy data available in 2017, which are the latest that the study employed. Projected demand growth is based on government policies, population, economic growth, and other key variables, such as energy prices used by the International Energy Agency energy demand model (IEA 2017). BAU is in line with current energy policy in the baseline information, which is used to predict future energy demand growth. However, APS differs from BAU in policy changes and targets, with a greater share of renewables, including possible nuclear uptake based on an alternative policy for energy sources and more efficient power generation and energy in final energy consumption.

For electricity generation, experts from 10 AMS specified assumptions based on their national power development plans and used the assumptions to predict ASEAN’s power generation mix. For renewable hydrogen production, the study applies a conversion factor of 48 kWh of electricity needed to produce 1 kg of hydrogen (ISES 2020).

5 Results and Discussion

The potential of renewable hydrogen produced using curtailed electricity in Scenario1, Scenario2, and Scenario3 is quantified according to a renewable curtailment rate of 20–30% for the high share of renewables in 2050. Emission abatement—the difference between (i) BAU and (ii) APS, Scenario1, Scenario2, and Scenario3—is calculated. The higher share of renewables under Scenario1, Scenario2, and Scenario3 could only happen if hydrogen is developed as energy storage by utilising curtailed renewable electricity. The study discusses hydrogen as an enabler of higher shares of renewables, the need to reduce the cost of renewable hydrogen production by reducing the cost of electrolysis and renewables, and the need to develop a hydrogen road map for ASEAN to guide industry and key investors in renewable hydrogen development. The road map will help create a large-scale ASEAN hydrogen society.

5.1 Potential Renewable Hydrogen from Curtailed Electricity

ASEAN’s power generation is dominated by fossil fuel (coal, oil, and gas), the share of which in the power mix was 79% (equivalent to 1041 TWh) in 2017 and is predicted to be 82% (2826 TWh) and 72% (2087 TWh) in 2050 for BAU and APS, respectively (Fig. 8.1). The share of combined fossil fuel (coal, oil, and gas) in the power generation mix is expected to reduce drastically from 82% in BAU to 65, 58, and 51% in Scenario1, Scenario2, and Scenario3, respectively, in 2050 (Fig. 8.2). The share of combined renewables is expected to increase from 18% in BAU to 35, 42, and 49% in Scenario1, Scenario2, and Scenario3, respectively, in 2050. The higher share of renewables in the power generation mix is desirable to decarbonise emissions in ASEAN’s future energy system. However, the high share of renewables can only happen with bold policy actions to develop and deploy renewable hydrogen to support the power integration system, which has a higher penetration of renewables. Utilizing unused electricity and/or curtailed renewable electricity to produce hydrogen could be ideal to tap the maximum potential pf renewables.

ASEAN’s power generation mix in business as usual and alternative policy scenario by source

Share of combined fossil fuels (coal, oil and gas) versus renewables under various scenarios. APS = alternative policy scenario, BAU = business as usual.

Scenario1, Scenario2, and Scenario3 assume the replacement of combined fossil fuel (coal, oil, and gas) power generation in 2050 with 10, 20, and 30% of power generation from renewables. Renewable power generation amounts in 2050 are 1016, 1224, and 1433 TWh for Scenario1, Scenario2, and Scenario3, respectively (Table 8.1).

In Scenario1, Scenario2, and Scenario3, the shares of renewables in the power mix will be 35%, 42%, and 49%, respectively, in 2050. Because of higher shares of renewables in the power mix, renewable energy generation will be highly curtailed. The curtailed electricity rate could vary from 20 to 30%, depending on the power grid infrastructure in AMS. Based on this curtailed electricity, with varying shares of renewables in Scenario1, Scenario2, and Scneario3, hydrogen production scenarios are created—Scenario1H2, Scenario2H2, and Scenario3H2. Potential renewable hydrogen from curtailed electricity in scenarios in AMS range from 4.23 to 8.96 million tonnes hydrogen (Table 8.2).

The higher share of renewables under various scenarios such as APS, Scenario1, Scenario2, and Scenario3 will see a large reduction in carbon dioxide emissions (CO2), which could resu lt in decarbonising emissions and contribute to COP commitments. Potential emission abatement ranges from −340 million tonnes carbon (Mt-C) in APS to −648 Mt-C, −710 Mt-C, and −774 Mt-C in Scenario1, Scenario2, and Scenario3, respectively (Table 8.3). Emissions were cut by 28% from BAU to APS, 53% from BAU to Scenario1, 58% from BAU to Scenario2, and 64% from BAU to Scenario3.

5.2 Hydrogen, an Enabler to Scale up Variable Renewable Energy

In ASEAN, power generation is dominated by coal, gas, and hydropower. Intermittent renewables from solar and wind energy contributed a negligible amount (14.47 TWh) or about 1.4% in 2017. However, the most optimistic prediction is that ASEAN will increase the share of wind and solar energy in the power generation mix to about 12.3% by 2050 (calculated from Fig. 8.1). The inclusion of the share of hydro (17.6%) and geothermal (2.2%) energy in the power generation mix contributed to the overall renewable share of 21.2% in 2017. However, future abundant resources are wind and solar energy, the current share of which is negligible. Grid operators had many misperceptions of VRE such as wind and solar energy, although its production cost has drastically dropped in recent years; solar photovoltaic farms’ levelized cost of electricity (LCOE) dropped from US$0.378/kWh in 2010 to US$0.043/kWh in 2020 in some places. Similarly, all LCOE cost trends for wind energy and concentrated solar power dropped drastically in 2010–2020 and will continue to drop in 2021 (Fig. 8.3), but their share in the power generation mix remains small. Misperceptions stemmed from the concern that VRE production is variable and intermittent, and that its higher share in the grid will add costs as it will require backup capacity from conventional gas power plants (NREL 2020).

Falling costs of renewables. CSP = concentrated solar power, kWh = kilowatt-hour, LCOE = levelized cost of electricity, PV = photovoltaic.

Technically, VRE power production output varies within a few seconds depending on wind or sunshine. However, the risk of variable energy output can be minimised if the power system is largely integrated within the country and within the region. The aggregation of output from solar and wind energy from different locations has a smoothing effect on net variability (NREL 2020). However, the ASEAN power grid is progressing slowly and the integrated ASEAN power market might be far off because of several reasons, such as regulatory and technical harmonisation issues within ASEAN power grids and utilities.

Scalable electricity production from wind and solar energy faces tremendous challenges from the current practice of system integration in ASEAN. Investors in solar or wind farms will confront high risks from electricity curtailment if surplus electricity is not used. Many countries have advanced research and technologies for battery storage (lithium-ion batteries) for surplus electricity produced from wind and solar energy, but advanced battery storage remains costly. Produced from electrolysis using surplus electricity, hydrogen has many advantages as it can be stored as liquid gas, which is suitable for numerous uses and easy to transport. Many ASEAN countries could produce wind, solar, hydropower, or geothermal electricity. Their resources, however, are far from demand centres and developing the resources would require large investments in undersea transmission cables. A solution would be to turn renewables into easily shipped hydrogen.

Hydrogen is a potential game changer for decarbonising emissions, especially in sectors where they hard to abate, such as cement and steel. Scalable resources from wind and solar energy and other renewables can be fully developed by widely adopting the hydrogen solution. The more electricity produced from wind and solar energy, the higher the penetration by renewables of the grid; at the same time, surplus electricity during low demand hours can be used to produce hydrogen. The more power generated from wind and solar energy and other renewables, the greater the possibility to increase the efficiency of electrolysis to produce hydrogen. On-site hydrogen production from wind and solar farms will solve the issue of curtailed wind and solar electricity. To increase the efficiency of electrolysis and allow further penetration by renewables of grids, a hybrid energy system including hydropower, geothermal, or nuclear plants, for example, would be the perfect energy choice. Since hydrogen is a clean energy carrier and can be stored and transported for use in, amongst others, hydrogen vehicles, synthetic fuels, upgrading of oil and/or biomass, ammonia and/or fertilizer production, metal refining, heating, and other end uses, hydrogen development is an ideal pathway to a sustainable clean energy system and enables scalable VRE such as solar and wind energy.

5.3 Need to Reduce Renewable Hydrogen Production Cost

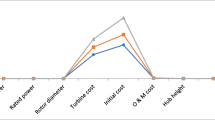

Cost-competitiveness of producing renewable hydrogen is key for the wide adoption of hydrogen uses. The upfront costs of renewable hydrogen such as electrolysers, transport infrastructure, and storage, and the varying costs of electricity tariffs are key factors contributing to the high production cost of renewable hydrogen (Fig. 8.4). ‘Green’ hydrogen production costs dropped drastically from US$10–US$15/kg of H2 in 2010 to US$4–US$6/kg of H2 in 2020, with varying assumptions of lower and higher upfront costs of electrolysers with 20 megawatts and producing capacity of 4,000 normal cubic metres per hour (IRENA 2019a; Hydrogen Council 2020). The costs are expected to reduce to US$2.00–US$2.60/kg of H2 in 2030, which is competitive with steam methane reforming with CCS.

Hydrogen production cost trends with upfront cost of electrolysers. CCS = carbon capture, sequestration, and storage, SMF = steam methane reforming. H2 = hydrogen

Considering the electricity tariffs of up to US$0.10/kWh with varying load factors of 10–50%, the cost of producing hydrogen ranged from US$0.90–US$5.50/kg of H2 to US$4.20–US$8.90/kg of H2 (Fig. 8.4), meaning that electricity tariff is the major cost of producing hydrogen using electrolysis. At zero electricity tariff or when VRE is expected to be curtailed, the cost of producing hydrogen can be as low as US$0.90/kg of H2 at an electrolyser’s load factor of 50%, and US$5.50/kg of H2 at an electrolyser’s load factor of 10%. The International Renewable Energy Agency’s target of cost-competitiveness of producing renewable hydrogen is US$2.00–US$2.50/kg of H2 (IRENA 2019b). In this case, an electricity tariff of US$0.03/kWh with an electrolyser’s load factor of 30% is the most practical given all the constraints.

The solar photovoltaic farm and onshore wind already cost US$0.02–US$0.03/kWh in some locations (IRENA 2019b). Even the target cost of US$2.00–2.50/kg of H2 to produce ‘green’ hydrogen, however, would not be competitive with low-cost natural gas at US$5 per gigajoule (GJ)Footnote 2 (US$0.018/kWh), but would be with natural gas, which costs US$10–US$16/GJ (US$0.036–US$0.057/kWh).

Technically, if renewable hydrogen production uses only curtailed electricity from renewables, the operating load factor of electrolysis, which contributes the most to the cost of producing hydrogen, will likely be low at 10% or less. Based on Hydrogen Council (2020), the electrolyser will need to run at a load factor of at least 30% or more to lower the cost of producing hydrogen to US$2.00–2.50/kg of H2, which is competitive with the natural gas grid price (Fig. 8.5).

Hydrogen production cost with varying electricity cost and electrolysis load factors

Electrolysis facilities must have a load factor above 30% to ensure the cost-competitiveness of producing renewable hydrogen, and other capital expenditures such as the electrolyser’s upfront cost must be reduced by 50% from US$840 today to US$420 per kilowatt by 2040. As wind and solar energy is expected to increase its share in the power generation mix, expected curtailed electricity from renewables will be higher by 10–30%. By 2030, the share of VRE curtailment will be 10–30% in Sweden, which provides the most incentives for renewable hydrogen (IRENA 2019b). In 2020, Chile, Australia, and Saudi Arabia have achieved the target cost of US$2.50/kg to produce ‘green’ hydrogen because of cheap access to electricity from wind and solar energy. The cost is expected to drop further to US$1.90/kg in 2025 and to US$1.20/kg in 2030, which is highly competitive with the cost of ‘grey’ hydrogen production.

Effective policies and incentives to develop and adopt hydrogen can promote economies of scale and cost-competitiveness in producing hydrogen, encouraging investors to manufacture electrolysers; improve their efficiency, operation, and maintenance; and use low-cost renewable power such as hydrogen to enable scaling VRE penetration of the power grid. ‘Green’ hydrogen production cost could decline even faster and go even lower than US$2/kg of H2 if governments, business, and stakeholders join hands to adopt the wider use of ‘green’ hydrogen and increase investment and R&D in hydrogen fuels. Australia, Chile, and Saudi Arabia have achieved cost-competitiveness in wind and solar energy generation.

The energy transition will largely depend on the clean use of fossil fuel leading to a clean energy future. Although hydrogen is a clean fuel, the way it is produced matters. Almost 95% of hydrogen production is from natural gas with or without CCS. The gasification of coal can be used as feedstock for producing hydrogen, but it emits roughly four times more CO2/kg of H2 produced than natural gas feedstock does. The production cost of low-carbon or blue hydrogen depends on feedstock cost and suitable geographical CCS storage. IRENA (2019a) estimated that ‘blue’ hydrogen production in China and Austria with current CCS infrastructure could realise a production cost of about US$2.10/kg of H2 for a cost of coal of about US$60 per ton. In the US, where natural gas is below US$3 per million British thermal units and has large-scale CO2 storage such as depleted gas fields and suitable rock formations, ‘blue’ hydrogen cost could drop below US$1.50/kg in some locations. If the carbon cost of about US$50 per ton of CO2 is considered, low-carbon hydrogen could reach parity with ‘grey’ hydrogen. ‘Blue’ hydrogen cost in the US and the Middle East could drop further to about US$1.20/kg in 2025 if economies of scale prevail.

World leaders need to provide a clear policy to develop and adopt hydrogen. The right policy will enable economies of scale for producing hydrogen cost-competitively, inducing investors to explore electrolyser manufacturing; improve electrolyser efficiency, operation, and maintenance; and use low-cost renewable power. With the full participation of governments, business, and stakeholders, hydrogen can become the fuel that enables scaling up renewable energy penetration in all sectors, decarbonising global emissions.

5.4 Need for Renewable Hydrogen Development Policies in ASEAN

Until 2020, ASEAN did not have a hydrogen road map. APAEC, however, mentions alternative technologies and clean fuels such as hydrogen and energy storage. APAEC will help AMS increase the share of hydrogen in the energy mix. An ASEAN hydrogen road map is needed to guide national road maps. Based on the analysis of the drastic drop in the cost of VRE and electrolysers, opportunities to introduce ‘green’ hydrogen produced using curtailed electricity will be plentiful. The hydrogen road map should include hydrogen development and penetration in transport, power generation, and industry. To guide investment, hydrogen penetration policies and targets must be set up. This study, however, can only suggest policies to develop, adopt, and use hydrogen. The study adopts Australia’s hydrogen road map, especially its key polices (Bruce et al. 2018), and tailors them to ASEAN’s energy landscape (Table 8.4).

ASEAN needs a comprehensive hydrogen road map that includes a policy framework supporting hydrogen production, storage, and transport, and hydrogen utilisation in power generation, transport, heat production, industrial feedstock, and import and export. In developing the hydrogen road map, governments should consult industry, financial, and banking stakeholders and cultivate people’s willingness to support a hydrogen society.

6 Conclusion and Policy Implications

ASEAN’s energy transition will largely depend on increasing the share of renewables and clean fuels such as hydrogen and the clean use of fossil fuel to create a clean energy future. Fossil fuel (coal, oil, and gas) accounted for almost 80% of ASEAN’s energy mix in 2017, a share that is expected to rise to 82% in BAU. Transitioning from a fossil fuel–based energy system to a clean energy system requires drastic policy changes to encourage embracing renewables and clean fuels whilst accelerating the use of clean technologies in employing fossil fuel (coal, oil, and natural gas). The study uses energy modelling scenarios to explore policy options to abate emissions in ASEAN by giving wind and solar energy a high share of the energy mix, and using electricity curtailment to promote renewable hydrogen production. The study reviews the potential cost reduction of renewables and hydrogen around the world and hydrogen road maps that might help ASEAN create its own strategy. Hydrogen will be an enabler, allowing wind and solar resources to be used to their maximum potential, without concern for electricity curtailment. ‘Green’ hydrogen will be important in increasing the share of renewables in the power generation mix by breaking the traditional barriers of power system integration, which cannot absorb a high share or intermittent electricity from solar and wind energy. Hydrogen enables increasing the share of other renewables such as geothermal, hydropower, and biomass energy. In the US, Japan, the Republic of Korea, and other OECD countries, renewable hydrogen will play a big role in using nuclear power–based load during low demand hours to produce ‘green’ hydrogen.

Hydrogen is not yet on the policy agenda in many ASEAN countries as an alternative fuel, but APAEC includes policy measures to utilise emerging and alternative technologies such as hydrogen and energy storage. APAEC will help AMS adopt the use of hydrogen. Hydrogen production in AMS is mainly used in the refining, fertilizer, and petrochemical industries. However, the energy landscape will see hydrogen fuels used more in many sectors as clean fuels and as an enabler of increasing renewables in the energy mix.

The findings suggest that ASEAN has high potential to produce renewable hydrogen using curtailed electricity. The higher share of renewables under various policy scenarios will see a large reduction in CO2 emissions, which could lead to decarbonising emissions and contribute to abating global climate change. The potential emission abatement ranges from −340 Mt-C in APS to −648 Mt-C, −710 Mt-C, and −774 Mt-C in Scenario1, Scenario2, and Scenario3, respectively. Emissions will be cut by 28% from BAU to APS, 53% from BAU to Scenario1, 58% from BAU to Scenario2, and 64% from BAU to Scenario3. The study found that OECD countries are accelerating toward the hydrogen society, which will have a big impact on the world’s energy landscape. ASEAN needs to catch up.

Hydrogen development is ideal for bringing sustainable clean energy to ASEAN and the rest of the world. Major policy reforms are needed to ensure that clean fuels such as hydrogen and renewables and clean technologies will gradually replace traditional fuels and technologies. The study’s findings have policy implications for hydrogen adoption:

-

(i)

ASEAN leaders must strongly commit to promoting a hydrogen society. ASEAN Ministers on Energy Meetings, facilitated by the ASEAN Secretariat, are an excellent platform for drafting a clear and actionable hydrogen development road map.

-

(ii)

ASEAN energy leaders must develop a clear strategy to promote hydrogen use in transport; power generation; and other sectors where emissions are hard to abate, such as the iron and steel industries. Singapore, Malaysia, Thailand, Indonesia, and the Philippines could take the lead by investing in R&D on hydrogen produced from renewables and non-renewables and by setting investment targets adapted from OECD countries. Investment in industries that can adopt hydrogen energy has strong potential, but to realise it ASEAN must accelerate its plans and strategies to embrace hydrogen use.

-

(iii)

Leaders in ASEAN and around the world must provide a clear investment policy to develop and adopt hydrogen as a fuel. The policy must enable economies of scale in cost-competitive production of hydrogen to induce investors to consider electrolyser manufacturing; improvements in electrolyser efficiency, operation, and maintenance; and the use of low-cost renewable power. With the full participation of governments, business, and stakeholders, hydrogen can become the fuel that enables scaling up renewable energy penetration in all sectors, decarbonising global emissions.

-

(iv)

Governments must engage the public, build its awareness of the many benefits of a hydrogen society, and ensure that the public is willing to pay for them. The success of introducing hydrogen on a large scale needs the participation of all stakeholders, including governments and public and private companies. Financing mechanisms such as banks must create favourable conditions to finance facilities such as electrolysers. Governments must provide financial incentives to invest in developing hydrogen.

-

(v)

Improving the electricity governance system in ASEAN developing countries will help reduce the cost of managing energy systems, allow the uptake of clean energy technology investment, and upgrade the grid system to bring in more renewables. The energy sector must be reformed; rules and procedures must allow more advanced and competitive technologies to enter the market. Electricity reform will attract foreign investment to modernise electricity infrastructure, including by making power systems more efficient and phasing out inefficient power generation and technologies.

-

(vi)

Unbundling of ownership in the electricity market, non-discriminatory third-party access to transmission and distribution networks, and the gradual removal of subsidies for fossil fuel–based power generation are key to ensure market competition. Other policies to attract foreign investment include tax holidays; reduction of market barriers and regulatory burdens; and plans to reduce the upfront cost investment, such as a rebate payment system through government subsidies and government guarantees that investment will be feasible and low risk.

Notes

- 1.

Tonne = metric ton. 1 metric ton = 1000 kg.

- 2.

Conversion factor: US$0.01/kWh = US$2.80/GJ.

References

Bruce S, Temminghoff M, Hayward J, Schmidt E, Munnings C, Palfreyman D, Hartley P (2018) National hydrogen roadmap. Commonwealth Scientific and Industrial Research Organisation, Canberra

European Union (EU) (2020) EU action: 2050 long-term strategy. https://ec.europa.eu/clima/policies/strategies/2050 (Accessed 27 Apr 2020)

Hydrogen Council (2019) Hydrogen for policy makers. https://hydrogencouncil.com/en/hydrogen-for-policymakers/ (Accessed 16 July 2020)

Hydrogen Council (2020) Path to hydrogen competitiveness: a cost perspective. https://hydrogencouncil.com/wp-content/uploads/2020/01/Path-to-Hydrogen-Competitiveness_Full-Study-1.pdf (Accessed 10 June 2020)

IEA (2020) Global energy prospects and their implications for energy security and sustainable development. https://www.oecd.org/parliamentarians/meetings/gpn-meeting-february-2020/Faith-Birol-Global-energy-prospects.pdf (Accessed 28 Apr 2020)

International Energy Agency (IEA) (2017) Capital cost of utility-scale battery storage systems in the new policies Scenario, 2017–2040. Paris. https://www.iea.org/data-and-statistics/charts/capital-cost-of-utility-scale-battery-storage-systems-in-the-new-policies-scenario-2017-2040 (Accessed 11 June 2020)

International Renewable Energy Agency (IRENA) (2018) Hydrogen from renewable power: technology outlook for the energy transition. Abu Dhabi

International Solar Energy Society (ISES) (2020) Renewable transformation challenge: hydrogen production from renewables. https://www.renewableenergyfocus.com/view/3157/hydrogen-production-from-renewables/. (Accessed 27 Sept 2020)

IRENA (2019a) Innovation landscape brief: renewable power-to-hydrogen. Abu Dhabi

IRENA (2019b) Hydrogen: a renewable energy perspective. Abu Dhabis

IRENA (2020) How falling costs make renewables a cost-effective investment. https://www.irena.org/newsroom/articles/2020/Jun/How-Falling-Costs-Make-Renewables-a-Cost-effective-Investment. (Accessed 20 June 2020)

Kimura S, Phoumin H (2019) Energy outlook and saving potential in the East Asia. Economic Research Institute for ASEAN and East Asia, Jakarta

McKenna J (2020) Europe’s New love affair with hydrogen. https://spectra.mhi.com/europes-new-love-affair-with-hydrogen?gclid=EAIaIQobChMI-NS1xoaI6QIVlg4rCh1qMAPqEAAYASAAEgJf6vD_BwE (Accessed 27 Apr 2020)

National Renewable Energy Laboratory (NREL) (2020) Wind and solar on the power grid: myths and misperceptions. https://www.nrel.gov/docs/fy15osti/63045.pdf. (Accessed 1 July 2020)

Phoumin H (2015) Enabling clean coal technologies in emerging Asia, working paper for the 2015 Pacific energy summit. National Bureau of Asia Research, Washington, DC, USA

United States (US) Department of Energy (DOE) (2014) DOE hydrogen and fuel cells program record. https://www.hydrogen.energy.gov/pdfs/18003_current_status_hydrogen_delivery_dispensing_costs.pdf. (Accessed 14 July 2020)

United States Environmental Protection Agency (2016) GHG equivalencies calculator—calculations and references. https://www.epa.gov/energy/ghg-equivalencies-calculator-calculations-and-references. (Accessed 16 Nov 2016)

US DOE (2020a) Hydrogen production and distribution. Altern Fuel Data. https://afdc.energy.gov/fuels/hydrogen_production.html. (Accessed 26 June 2020)

US DOE (2020b) Hydrogen production: natural gas reforming. https://www.energy.gov/eere/fuelcells/hydrogen-production-natural-gas-reforming. (Accessed 26 June 2020)

US DOE (2020c) Hydrogen and fuel cell technologies. https://www.energy.gov/eere/fuelcells/hydrogen-and-fuel-cell-technologies-office. (Accessed 16 July 2020)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Author(s), under exclusive license to Springer Nature Singapore Pte Ltd.

About this chapter

Cite this chapter

Phoumin, H., Kimura, F., Arima, J. (2021). Potential Green Hydrogen from Curtailed Electricity in ASEAN: The Scenarios and Policy Implications. In: Phoumin, H., Taghizadeh-Hesary, F., Kimura, F., Arima, J. (eds) Energy Sustainability and Climate Change in ASEAN. Economics, Law, and Institutions in Asia Pacific. Springer, Singapore. https://doi.org/10.1007/978-981-16-2000-3_8

Download citation

DOI: https://doi.org/10.1007/978-981-16-2000-3_8

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-16-1999-1

Online ISBN: 978-981-16-2000-3

eBook Packages: Economics and FinanceEconomics and Finance (R0)