Abstract

This study is one among the few attempts to link aggregate fluctuations with productivity and technical efficiency using the data of the Indian industrial sector. In doing so, this study uses firm-level data from the CMIE Prowess and macroeconomic indicators of Indian economy from various government databases. We estimate productivity and technical efficiency using the standard econometric approach. Further, a structural vector error correction (SVEC) model is employed to understand the importance of technological shocks in explaining the aggregate fluctuations. The result without ambiguity indicates that the percentage of variance explained by aggregate demand shocks is larger at lower lag and decreasing. However, the share of technology shock shows an increasing trend over the period of time. Therefore, the aggregate demand shock and the technology shock have conflicting impact as far as aggregate output fluctuations are concerned. The results are similar when we substitute TFP with TE. The findings in general indicate the transitory nature of aggregate demand shocks compared to technology shocks.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

JEL Classification

1 Introduction

Identification of the sources of fluctuations in aggregate output is very important both from modelling and policy perspective. These fluctuations can be due to demand and supply shocks. Some of the theoretical models like real business cycle (RBC) models attribute random variations in technology as the main source of business cycle and emphasizes the role of aggregate supply shocks, whereas the new Keynesian models give prominence to aggregate demand shocks propagated through price stickiness and imperfect competition. The effectiveness of any policy is conditional on the nature of shocks to aggregate output (Lucas 1977). The demand stabilisation policies will be effective if the demand shocks explain most of the variations in business cycles as predicted by Keynesian models, but it becomes counterproductive if technological shocks are important. Therefore, it is important to empirically examine the importance of different shocks on aggregate fluctuations.

Economic reforms initiated in the early 1990s and the increased international integration of Indian economy brought a high growth rate. A move away from regulated and closed economy to a market-determined and more integrated one does have implications for business cycle facts. Indian economy has also grown from an agrarian economy to a service-oriented and industrial economy over the period of time. The stylised facts of Indian business cycles are very different from pre-reform period as documented by Ghate et al. (2013). In the post-reform period, output becomes less volatile and it is strongly correlated with investment. Imports become pro-cyclical, and exports and exchange rates are counter-cyclical in the post-reform period compared to acyclical nature of these variables in the pre-reform period. In this regard, examining the business cycle facts and its driving forces are very much relevant from an emerging economy perspective.

There are significant advancements in the methods and tools used to understand business cycles and its driving forces following the works of Kydland and Prescott (1982) and Long and Plosser (1983). Particularly, the dynamic stochastic general equilibrium models become an inevitable tool for analysing business cycles’ facts. There are some attempts to examine the driving forces using vector autoregressive (VAR) models developed by Sims (1980). Later, the structural VAR models developed by Blanchard and Quah (1988) and its extensions were used to understand business cycle fluctuation with minimum required assumptions. In few other studies, structural VAR models are often used. Following this strand of the literature, this study attempts to investigate the main source of macroeconomic fluctuations in India and relate with the total factor productivity (TFP) and technical efficiency.

2 Technological Shocks as a Source of Business Cycles

The idea that technological innovations propagate growth and business cycles dates back to Schumpeter (2010). According to Schumpeter, business cycle happens mainly due to fluctuations in technological innovations and emphasised cyclical nature of economic growth. He distinguished four phases of economic fluctuations: prosperity, recession, depression and recovery. He characterised the cyclical fluctuation into different categories depending on the length of the waves: short-term 3–5 year Kitchin cycles, medium-run Juglar cycles and long-run Kondratieff cycles (Schumpeter 1939). In all these cycles, innovations play a crucial role. The spurt of innovations at particular periods of time known as “neighbourhoods of equilibrium” leads to cycles in the aggregate growth.

The Schumpeterian idea of stochastic technological innovations as the main propagation mechanism came into focus again with the work of Kydland and Prescott (1982) and Long and Plosser (1983) on real balance cycle (RBC).Footnote 1 The RBC models were built on frictionless neoclassical framework with optimising agents. They argued that the technological shocks often defined as random variations around the productivity cause aggregate output to fluctuate around the long-term trend. Thus, the real business cycle attributes substantial amount of aggregate fluctuations to technological shocks. Following the work of Kydland and Prescott (1982), many studies have emphasised this fact.Footnote 2 The RBC models popularised dynamic stochastic general equilibrium (DSGE) models which incorporate the preferences and optimising behaviour of producers and other economic agents. These models were later extended to incorporate other features including but not limited to the new Keynesian assumptions.

Apart from DSGE approach, empirical studies have also used structural VAR models to test the predictions of standard RBC models. For example, Shapiro and Watson (1988) used a structural vector autoregressive model (SVAR) to capture the share of demand and technology shocks. They find that one-third of the output variations can be explained by technological shocks. Similarly, Cochrane (1994) examined the importance of transitory (demand shocks) and permanent shocks (technology or productivity shocks) in explaining short-run dynamics of business cycles. They have used weak exogeneity of the variable in a co-integrated system to identify the permanent and transitory components. They find that substantial amount of variations in GNP growth, and stock returns are explained by transitory shocks. It was Blanchard and Quah (1988) who developed a comprehensive approach to decompose demand and supply shocks using a two-variable structural system. They considered supply shocks to have permanent effect while demand shocks are assumed to be transitory in nature. Their approach was generalised to incorporate more variables and allowing for co-integration.

Following Blanchard and Quah (1988) approach, Gali (1999) tried to examine the explanatory power of technology shocks in explaining business cycle fluctuations as predicted by real business cycle models. He employed two SVAR models (i) a bivariate model with labour productivity and labour hours (ii) a five-variable model with labour productivity, labour hours, real money balances, real interest rates and the inflation rate. More specifically, using the five-variable SVAR, the paper identified permanent shocks (technology shocks and labour supply shocks) and transitory shocks interpreted as demand shocks. They refute the predictions of RBC models and show that the technological shocks are unrelated to business cycles. Moreover, the results indicate that the technology shock induces a negative co-movement between productivity and employment.Footnote 3 Another important issue is related to the measurement of technological innovations. Previous studies have used many proxies for technological innovations including an aggregate measure of total factor productivity (TFP). These measures are often constructed using aggregate data. These measures often ignore the heterogeneous nature of technological innovations.Footnote 4 An index constructed using firm-level TFP would be a better measure of technological innovations, and this study tries to construct the TFP using firm-level data.

There are few studies in Indian context, and most of them focus on extracting business cycles and try to analyse the co-movements of various aggregates variables (see for e.g., Dua and Banerji 2012; Chitre 1982). Some of the recent studies attempted to analyse the features of business cycles using DSGE framework. For instance, Bhattacharya et al. (2013) examined how terms of trade affect business cycles. Similarly, Ghate et al. (2016) examined the role of fiscal policy in the business cycles of emerging markets. In another study, Banerjee and Basu (2017) developed a small open economy new Keynesian DSGE model for India to understand the importance of two technology shocks, Hicks-neutral total factor productivity (TFP) shock and investment-specific technology (IST) shock for an emerging market economy like India. The results indicated that output correlates positively with TFP but negatively with IST and are important factors in explaining aggregate fluctuation in India. Similarly, the importance of IST has increased after the post-reform period.

In this context, this study tries to examine the role of aggregate fluctuations in a SVECM framework. We also try to construct the productivity measure using highly disaggregated data at the firm level. There are very few studies in Indian context that tries to examine the nature of aggregate fluctuations using measures constructed with microlevel data.

3 Data and Methods

Data for this paper is derived from both at firm-level and macrolevel. The firm-level data is collected from the Prowess database of the Centre for Monitoring Indian Economy (CMIE), and macroeconomic data is collected from various government databases of macroeconomic indicators. The macroeconomic indicators include quarterly data on log of real GDP (LRY) and real money supply (LRM) constructed as the difference between the log of M3 and log of consumer price index. From the firm-level data on inputs and output, we compute total factor productivity (TFP) and technical efficiency (TE) and assume to be the proxies of technological innovations at firm level. Since quarterly data on GDP was available from 1996 Q2, the sample period is chosen as 1996 Q2 to 2017 Q2.

The first part of the method employed in this paper is to calculate TFP and TE. Here, we use a stochastic frontier production function to estimate the technical efficiency, which can be expressed as follows:

where \( Y_{it} \) is the output of the ith firm (i = 1, …, N) in period t = 1, …, T; \( f\left( {X_{it} ,t;\beta } \right) \) represents the production technology; \( X_{it} \) is a (1 × K) vector of inputs and other factors influencing production associated with the ith firm in period t; β is a (K × 1) vector of unknown parameters to be estimated; \( v_{it} \) is a vector of random errors that are assumed to be \( {\text{iid}}\;N\left( {0,\sigma^{2}_{v} } \right) \); and uit is a vector of independently distributed and non-negative random disturbances that are associated with output-oriented technical inefficiency. Specifically, uit measures the extent to which actual production falls short of maximum attainable output. If the firm is efficient, the actual output is equal to potential output. Thus, \( Y_{it} - Y_{it}^{*} = u_{it} \), where, uit = inefficiency. The technical efficiency of a producer at a certain point in time can be expressed as the ratio of actual output to the maximum potential output, and the technical efficiency can be calculated as.

The error term representing technical inefficiency is specified as: uit = exp (−η (t − T)ui). Under this specification, inefficiencies in periods prior to T depend on the parameter η. As t tends to T, uit approaches uΤ. Inefficiency prior to period T is the product of the terminal year’s inefficiency and exp (−η (t − T)). If η is positive, then exp (−η (t − T)) = exp (η (t − T)), and it is always greater than 1 and increases with the distance of period t from the last period T. The positive value of η indicates inefficiencies fall overtime, whereas negative value of η indicates inefficiencies increase overtime.

The above model can be estimated by the maximum likelihood estimates (MLE). Restricting μ = 0 in the model, it reduces the model to the traditional half-normal distribution. If μ is not restricted, then μ follows truncated normal distribution. If η = 0, then technical efficiency is time-invariant, i.e., firms never improve their efficiency. The value of \( \gamma = \sigma^{ 2}_{u} /\sigma^{ 2} \;\left( {{\text{where}}\;\sigma^{ 2} = \sigma^{ 2}_{u} + \sigma^{ 2}_{v} } \right) \) will lie between 0 and 1. If uit equals zero (which indicates full technical efficiency), then γ equals zero, and deviations from the frontier are entirely due to noise vit. If γ equals one, all deviations from the frontier are due to technical inefficiency.

Besides the above rationality, the following Cobb-Douglas specification of functional form is employed to specify the parameters of the model to estimate the efficiency since it is widely used one in efficiency studies. The functional form in the present case is:

where Q = output; C = capital; L = labour; M = material; and E = energy

The parameters of the stochastic frontier model, defined in Eq. (3), are estimated using Coelli (1996) method. The total factor productivity is also estimated using the ACF production function,Footnote 5 which is widely used in recent estimates of TFP. For estimating TFP and TE, we used data drawn from the CMIE. In this study, gross output at constant prices is used as a measure of real output. Prowess reports gross output data in value terms (Rs. lakh). Nominal values of gross output are deflated by the wholesale price indices for industrial goods. Wages and salaries of employees are considered for the labour input. Unlike other factors of production, capital is used beyond a single accounting period, and measuring capital stock input is rather problematic. For capital stock, we have followed perpetual inventory method (PIM) as followed in Goldar et al. (2004) and many other studies on Indian manufacturing sector. Once, both TFP and TE are calculated at firm level for each year, they are converted to quarterly TFP and TE based on NIC-2008 classifications of two-digit industrial classifications.

The second part of the empirical analysis is to employ structural vector error correction (SVEC) model to understand the importance of technological shocks in explaining the aggregate fluctuations. We have considered a three-variable VEC model expressed as:

where \( X_{t} \) is a vector of K variables, \( B\varepsilon_{t} = u_{t} \) and \( \varepsilon_{t} \sim N\left( {0,I_{K} } \right) \)

Following Lütkepohl (2005), equation above can be decomposed into permanent and transitory components using a multivariate Beveridge–Nelson representation as:

where \( \Xi = \beta_{ \bot } \left( {\alpha_{ \bot }^{\prime} \left( {I_{K} - \mathop \sum \nolimits_{i = 1}^{p - 1} \varGamma_{i} } \right)\beta_{ \bot } } \right)^{ - 1} \alpha_{ \bot }^{\prime} \) and \( \Xi \) has a reduced rank equal to \( K - r \). Thus, first term in the right-hand side (RHS) of the equation is integrated of order one, and the middle term is stationary and \( \Xi_{j}^{*} \) converges to zero as \( j \to \infty \). The third term in the equation has all the initial values. Since \( \Xi \) is a reduced rank matrix, we have r shocks that are transitory and \( k^{*} = K - r \) common trends in the system. Replacing \( u_{t} \) with \( B\varepsilon_{t} \) we can recover the orthogonalised short-run impulse response using \( \Xi_{j}^{*} B \) as in the case of structural VAR, and the long-run effect of the structural shocks is given by \( \Xi B \). Hence, the elements in B matrix can be interpreted as contemporaneous effects of the structural innovations. The long-run impact matrix \( \Xi B \) can have at most r columns of zeros. Thus, as mentioned earlier, there are r shocks with transitory effects and \( k^{*} \) shocks with permanent effects.

4 Results and Discussions

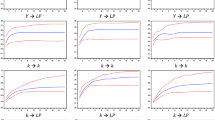

The measures of plots of the technical efficacy and total factor productivity are shown in Figs. 1 and 2. The figures show an increasing both technical efficacy and total factor productivity which started increasing since 2002 and a slight decline after 2014. The minimum value of total factor productivity for the sample period is 2.68 and maximum is 3.30, it is 0.58 and 0.61 for technical efficiency. Before estimating the structural system, the variable under consideration was examined for its time-series properties. The results of unit root test are given in Table 1.

Measures of total factor productivity (1996 Q2–2014 Q2)

Measures of technical efficiency (1996 Q2–2014 Q2)

Standard unit root tests such as augmented Dicky–Fuller (ADF) and Phillips–Perron (PP) are used to test the stationary properties of the variables. The tests indicate that all the variables under consideration are integrated of order one. As all the variable are I(1), we have proceeded to test co-integration before estimating the structural VECM.

We have considered two different specifications for the Johansen test of co-integration. The first model includes a vector of three variables \( X_{t} = \left\{ {{\text{LRY}}_{t} ,{\text{LRM}}_{t} ,{\text{TFP}}_{t} } \right\} \). The TFP is then substituted by the alternative measure TE. The results of the co-integration test are given in Table 2. The results indicate one co-integrating relation among these variables for both specifications.Footnote 6 This implies that we can decompose the structural system into two permanent and one transitory components by appropriately restricting the long-run impact matrix and short-run contemporaneous relationship.

Two shocks with permanent effect and one with transitory effect are identified. The long-run impact matrix is a reduced rank matrix since there is one co-integrating vector as suggested by Johansen test. Accordingly, we have restricted the first column of the long-run matrix to zero. Thus, in the presence of co-integration, we need only two more additional restrictions. The first two elements in the last row can be restricted to zero assuming constant returns to scale.

One more restriction is required for the identification of structural innovations. This can be obtained by assuming that the real money shock has no contemporaneous impact on productivity. Thus, the B matrix can be written as

The structural system is exactly identified with these restrictions. The variance decomposition is recovered with these restrictions which are given in Tables 3 and 4.Footnote 7

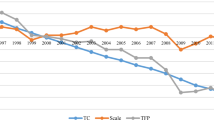

The results of variance decompositions of real output due to technology shocks with TFP are given in Table 3. The results clearly indicate that the percentage of variance explained by aggregate demand shocks is larger at lower lag and decreasing over the period. There was 40% at lag one and decreased to 18% by lag 36. However, the share of technology shock shows an increasing trend over the period of time. The share of technology shock was just 13% at first lag abut increased to 26%. The results are similar when we substitute TPF with TE. However, the share of TE is very negligible till the lag 24 (below 10%). But, it starts increasing after lag 30. The results in general indicate the transitory nature of aggregate demand shocks compared to technology shocks. The technology shocks explain the forecast error variance of real output at longer lags.

5 Conclusion

This study is one of the rarest attempts to empirically establish a relationship between microdata and macrodata for the Indian economy in general and industrial data and macroeconomics data for the Indian economy in particular. For the Indian economy, there are many studies that have looked at the estimation of TFP and TE and their determinants. Similarly, studies have identified business cycle co-movements, movements in GDP and other macroeconomic indicators. This study, however, links the aggregate fluctuations with TFP and TE for the Indian economy. In doing so, we gather firm-level data from the CMIE Prowess and macroeconomic indicators of Indian economy. The results clearly indicate that the percentage of variance explained by aggregate demand shocks is larger at lower lag and decreasing. However, the share of technology shock shows an increasing trend over the period of time. Therefore, the aggregate demand shock and the technology shock are inversely related in this case. The results are similar when we substitute TPF with TE. The results in general indicate the transitory nature of aggregate demand shocks compared to technology shocks.

Notes

- 1.

- 2.

- 3.

Similarly, Basu et al. (2006) constructed a measure of aggregate technology change and argued that sticky-price models fit the data well compared to RBC models. Some studies stressed other important shocks that affect aggregate fluctuations like “fundamental disturbance to the functioning of financial sector” (Justiniano et al. 2010), investment-specific technology shocks (Greenwood et al. 1997; Fisher 2006) and news shocks (Beaudry and Portier 2006).

- 4.

Many studies have highlighted the importance of idiosyncratic firm-level shocks to aggregate fluctuations (Gabaix 2011)

- 5.

For detail methodology, please see Ackerberg et al. (2015).

- 6.

VECM was estimated with two lags as suggested by AIC information critera.

- 7.

Only the results of variance decomposition of output due to output, TFP/TE and real money supply are represented in the tables. The results of other variables are available upon request.

References

Acemoglu, D., Carvalho, V. M., Ozdaglar, A., & Tahbaz-Salehi, A. (2012). The network origins of aggregate fluctuations. Econometrica, 80(5), 1977–2016.

Ackerberg, D. A., Caves, K., & Frazer, G. (2015). Identification properties of recent production function estimators. Econometrica, 83(6), 2411–2451.

Aghion, P., & Jaravel, X. (2015). Knowledge spillovers, innovation and growth. The Economic Journal, 125(583), 533–573.

Akcigit, U., & Kerr, W. R. (2018). Growth through heterogeneous innovations. Journal of Political Economy, 126(4), 1374–1443.

Banerjee, S., & Basu, P. (2017). Technology shocks and business cycles in India. Macroeconomic Dynamics, pp. 1–36.

Basu, S., Fernald, J. G., & Kimball, M. S. (2006). Are technology improvements contractionary? American Economic Review, 96(5), 1418–1448.

Beaudry, P., & Portier, F. (2006). Stock prices, news, and economic fluctuations. American Economic Review, 96(4), 1293–1307.

Bhattacharya, R., Patnaik, M. I., & Pundit, M. (2013). Emerging economy business cycles: Financial integration and terms of trade shocks (No. 13–119). International Monetary Fund.

Blanchard, O. J., & Quah, D. (1988). The dynamic effects of aggregate demand and supply disturbances.

Chitre, V. S. (1982). Growth cycles in the Indian economy. Pune: Gokhale Institute of Politics and Economics.

Cochrane, J. H. (1994). Permanent and transitory components of GNP and stock prices. The Quarterly Journal of Economics, 109(1), 241–265.

Coelli, T. J. (1996). A guide to FRONTIER version 4.1: A computer program for stochastic frontier production and cost function estimation (Vol. 7, pp. 1–33). CEPA Working papers.

Cooley, T. F., & Prescott, E. C. (1995). Economic growth and business cycles. Frontiers of business cycle research, Vol. 1.

Dua, P., & Banerji, A. (2012). Business and growth rate cycles in India (No. 210).

Fisher, J. D. (2006). The dynamic effects of neutral and investment-specific technology shocks. Journal of Political Economy, 114(3), 413–451.

Gabaix, X. (2011). The granular origins of aggregate fluctuations. Econometrica, 79(3), 733–772.

Gali, J. (1999). Technology, employment, and the business cycle: Do technology shocks explain aggregate fluctuations? American Economic Review, 89(1), 249–271.

Ghate, C., Gopalakrishnan, P., & Tarafdar, S. (2016). Fiscal policy in an emerging market business cycle model. The Journal of Economic Asymmetries, 14, 52–77.

Ghate, C., Pandey, R., & Patnaik, I. (2013). Has India emerged? Business cycle stylized facts from a transitioning economy. Structural Change and Economic Dynamics, 24, 157–172.

Goldar, B., Renganathan, V. S., & Banga, R. (2004). Ownership and efficiency in engineering firms: 1990-91 to 1999-2000. Economic and Political Weekly, pp. 441–447.

Greenwood, J., & Smith, B. D. (1997). Financial markets in development, and the development of financial markets. Journal of Economic dynamics and control, 21(1), 145–181.

Justiniano, A., Primiceri, G. E., & Tambalotti, A. (2010). Investment shocks and business cycles. Journal of Monetary Economics, 57(2), 132–145.

King, R. G., & Rebelo, S. T. (1999). Resuscitating real business cycles. Handbook of Macroeconomics, 1, 927–1007.

Kydland, F. E., & Prescott, E. C. (1982). Time to build and aggregate fluctuations. Econometrica: Journal of the Econometric Society, pp. 1345–1370.

Long, J. B., Jr., & Plosser, C. I. (1983). Real business cycles. Journal of Political Economy, 91(1), 39–69.

Lucas, R. (1977). Understanding business cycles. In Carnegie-Rochester conference series on public policy (Vol. 5, No. 1, pp. 7–29). Elsevier.

Lütkepohl, H. (2005). New introduction to multiple time series analysis. Springer Science & Business Media.

Schumpeter, J. A. (1939). A theoretical, historical and statistical analysis of the Capitalist process. In Business cycles. New York, Toronto, London: McGraw-Hill.

Schumpeter, J. A. (2010). Capitalism, socialism and democracy. Routledge.

Shapiro, M. D., & Watson, M. W. (1988). Sources of business cycle fluctuations. NBER Macroeconomics Annual, 3, 111–148.

Sims, C. A. (1980). Macroeconomics and reality. Econometrica: Journal of the Econometric Society, pp. 1–48.

Acknowledgements

This is a modified and updated version of our earlier paper presented during the “Silver Jubilee Seminar of Madras School of Economics” jointly organised by Forum of Global Knowledge Sharing (Knowledge Forum) during August 11, 2018. We would like to thank the participants of the seminar for constructive comments and suggestions during the presentation. Usual disclaimer applies.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2020 Springer Nature Singapore Pte Ltd.

About this chapter

Cite this chapter

Paul, S., Sahu, S.K., Jacob, T.I. (2020). Aggregate Fluctuations and Technological Shocks: The Indian Case. In: Siddharthan, N., Narayanan, K. (eds) FDI, Technology and Innovation. Springer, Singapore. https://doi.org/10.1007/978-981-15-3611-3_11

Download citation

DOI: https://doi.org/10.1007/978-981-15-3611-3_11

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-15-3610-6

Online ISBN: 978-981-15-3611-3

eBook Packages: Economics and FinanceEconomics and Finance (R0)