Abstract

-

This chapter gives an overview of Germany’s electric power system, its physical infrastructure, the regulatory environment, and the vision for smart grid development. The main topics presented were selected with the intention of providing examples of lessons learned and of sharing the German experience in the area of the main technological and regulatory challenges presented in the previous chapter.

-

The chapter contains a detailed description of the historical development and current design of German electricity markets with a special emphasis on market liberalization policies. It also focuses on the effects of aggressively expanding RES generation capacities in the context of such markets. The evidence presented here might be insightful for Chinese policy-makers given their will to promote the establishment of electricity markets and to increase RES generation capacities.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

FormalPara Chapter at a glance-

This chapter gives an overview of Germany’s electric power system, its physical infrastructure, the regulatory environment, and the vision for smart grid development. The main topics presented were selected with the intention of providing examples of lessons learned and of sharing the German experience in the area of the main technological and regulatory challenges presented in the previous chapter.

-

The chapter contains a detailed description of the historical development and current design of German electricity markets with a special emphasis on market liberalization policies. It also focuses on the effects of aggressively expanding RES generation capacities in the context of such markets. The evidence presented here might be insightful for Chinese policy-makers given their will to promote the establishment of electricity markets and to increase RES generation capacities.

4.1 Historical perspective

Reliability and affordability as the first policy goals

In the first decades of the electrification process, Germany’s electricity system developed rather independently from governmental regulation. Power generation units and electric power grids were built up in a decentralized manner and operated by a variety of local and regional companies. After World War I, 220-kV transmission grids were constructed to interconnect local and regional power grids. The trend towards a nationally integrated electric power grid contributed to increasing competition between companies from different regions which in turn resulted in a pronounced market consolidation.

The time of little government interference ended in 1935, when the German government issued the Energy Industry Act (EnWG). The main objective of this law was to pave the way for the effective and efficient development of a nationally integrated and reliable electricity grid. This goal was supposed to be achieved by incentivizing investments in generation units and in the grid infrastructure by formally assigning monopoly rights to predominant companies. Monopolistic structures were deemed more suitable to guarantee a reliable power grid and to operate the grid in a cost-efficient manner taking advantage of economies of scale.

As a result of regional monopoly rights, EnWG created an electricity system with a high degree of vertical integration and a low degree of competition. Electricity generation and transmission assets were owned and operated by integrated utilities, while electricity distribution and retail was in the hand of integrated municipal utilities. The municipal utilities were owned either by local governments or by the integrated utilities responsible for generation and transmission, which then combined all stages of the electricity supply chain into a single company. To protect consumers against the market power of the newly installed monopolies, EnWG obliged the companies to provide electricity to every end consumer; the Act also regulated construction and expansion of power plants in order to ensure system stability.

Sustainability as a more recent policy goal

One important shift in Germany’s electricity market regulation regime had its origin in the 1970 s, when environmental protection gained momentum as a new policy goal [1]. Due to high levels of local and regional air pollution caused by the combustion of fossil fuels for electricity generation, the German government issued the Federal Pollution Control Act (BIMSchG) in 1974. This law and its ordinances obliged power plants to install filter technology in order to reduce, for instance, sulfur dioxide (SO2) or nitrogen oxides (NOx) emissions. In the 1990 s, the German government further strengthened the role of environmental protection:

-

The 1991 Act on the Feed-In of Electricity from Renewable Sources into the Public Grid and its more prominent successor, the Renewable Energy Act (EEG) of 2000, had the objective to incentivize investments in renewable energies by guaranteeing investors financially attractive feed-in tariffs.

-

Another example of Germany’s regime shift to environmental protection is the Electricity Tax Act (StromStG) of 1999 which, amongst other objectives, had the aim of inducing consumers to consume less electricity by raising electricity prices.

Public acceptance – towards a fourth energy policy goal

The increasing importance of sustainability is generally supported by the German population. However, citizens are more frequently opposed to new energy infrastructures near residential areas if these infrastructures are related to visible, audible, or olfactory effects. In the light of Germany’s rather high population density, the build-up of distributed and renewable energy sources has of late entailed rising public opposition. An increasing number of citizens disapprove of investments in new wind farms, biomass power plants or transmission lines [2]. During the last few years, a certain number of energy projects – for instance new transmission lines or demonstration sites for carbon capture and storage – have failed to be realized owing to public opposition against them [3], [4]. As a consequence, public acceptance has recently gained prominence in the discussion as a fourth general energy policy goal in Germany, since it is only with a high level of public acceptance that the government and the companies are able to realize their investment plans [2]. Experiences in Germany reveal that three elements are important to ensure the support of the population for investments in energy infrastructure:

-

There has to be transparency on costs, benefits, and risks of new investments and technologies while the underlying motivations of the stakeholders involved in a project have to be communicated to the public.

-

The public has to be included in the entire planning process of new projects. Private citizens and other public stakeholders must be able to communicate their position and may also be allowed to invest financial funds of their own in the project.

-

Given that some conflicts cannot be solved unanimously, specific institutions or procedures for mediation and reconcialiation of interest are necessary to reduce number of court-cases [2].

A short summary of market liberalization tendencies since 1996

For a long time, Germany’s electric power system was characterized by a high degree of vertical integration and a low degree of competition. Today, the different stages in the supply chain are in a state of far-reaching unbundling, and competition has been established in the generation and retail sectors.

The market liberalization process on the European level began in 1996 with the First Electricity Directive [5], which was issued by the European Union (EU) and motivated by two main objectives [6]:

-

To open the electric power sector for third parties and to prevent discriminatory behavior towards generation companies by grid operators.

-

To allow end consumers to choose their retailer in an effort to increase the affordability of electricity through more competition. Thus, the protected supply areas (regional monopolies) of the incumbent retail companies were abandoned in favor of retail competition.

Based on this directive, the German government in 1998 revised EnWG and started to liberalize Germany’s electricity sector. After a short period of promising results with market entries of independent retail companies and decreasing retail prices, retail prices increased again. In addition, the market concentration did not decline significantly. Questions emerged regarding whether competition in generation and retail could be achieved as long as grid operators still had ownership in generation. Accordingly, the Second Electricity Directive issued by the European Union in 2003 contained a package of requirements to achieve legal unbundling. Legal unbundling can be described as an unbundling of accounts, operations, and information. It requires that transmission and distribution grid operators are independent from each other, as well as from generation and retail. In practice, legal unbundling requires a functional unbundling by guaranteeing independence in terms of legal form, organization/management and decision-making.

Based on the 2007 inquiry into the energy sector, the European Commission (EC) stated that, in spite of legal unbundling, the level of competition in the European energy market was still too low [7]. Major challenges were identified with respect to market concentration and vertical foreclosure.Footnote 1 This document criticized the fact that with legal unbundling, a utility might still be able to discriminate against competitors or even restrict access of new market actors to the infrastructure. In addition, the Commission Paper stated that a grid operator involved in competitive sectors might be able to cross-subsidize its activities in the market with the revenues generated from the monopoly part of its business [8]. Furthermore, the European Commission was concerned about insufficient incentives for network investments, especially across borders. Generally speaking, markets for electricity were organized on a national basis and there was only a weak relation between the various national markets, as shown by grid congestions at most borders. The Commission argued that incumbents might postpone investments into interconnector capacities in order to protect their own market against cheaper electricity imports. This behavior is known as strategic investment withholding by locally integrated utilities [9].

In 2009, the EU’s Third Electricity Directive introduced a compromise with three different options for unbundling on the transmission level. Basically, the aim of this rule was to separate the transmission grid from the other stages of the supply chain. The three options were:

-

Full ownership unbundling prohibits ownership of network and generation or retail assets by one and the same firm.

-

A model based on an Independent System Operator requires that an entity independent from the transmission grid owner takes over grid operation. With an independent system operator, network ownership can remain within an integrated company which also owns generation assets.

-

A model based on an Independent Transmission Operator (ITO) allows companies to retain both network ownership and management, but it puts strong limitations on cross involvement of employees in order to ensure network independence (please refer to [10] for further explanations on this model). In effect, the ITO model is similar to legal unbundling, though in a stronger form.

In Germany, the ITO model was applied. It had to be ensured that the transmission system was owned and operated by the ITO, which is legally independent from the commercial businesses of electricity generation and retail. Currently three out of the four transmission system operators (TSO) in Germany apply full ownership unbundling; the fourth is a genuine ITO. Distribution grids are currently subject to legal unbundling requiring administrative separation similar to the ITO model though in a less restrictive form. The objective is to ensure that no commercially sensitive information is exchanged between the power grid and other parts of the supply chain within one integrated company. Note that administrative unbundling is only applied for distribution system operators (DSO) with more than 100,000 customers. DSO with fewer customers do not have to unbundle and can remain an integrated part of a utility. This exception is known as the de-minimis rule.

4.2 Today’s power system and its most pressing challenges

4.2.1 Power generation

In 2013, Germany’s gross electricity generation amounted to roughly 634 TWh. Coal is currently Germany’s predominant primary energy source, accounting for more than 45 % of total electricity generation.Footnote 2 Nuclear power and gas are the second and third most important generation sources, accounting for approximately 15 % and 11 % of overall electricity generation respectively. Roughly 24 % of total electricity generation comes from RES, with wind accounting for 8.4 %, biomass for 6.7 %, solar for 4.7 %, hydro for 3.2 %, and household waste for 0.8 % [11].

During the last 20 years, overall electricity generation increased only slightly (see Fig. 4.1). However, the composition of the electricity mix has changed significantly owing to two specific governmental policies: the promotion of RES initiated in the 1990 s and the nuclear phase-out promulgated in 2002. As a consequence, there has been a steady decline in the proportion of electricity generated by means of nuclear power from 29.2 % in 1993 to 15.4 % in 2013, and coal, from 55.7 % in 1993 to 45.2 % in 2013, while the share of RES in the electricity mix has increased from 4.0 % in 1993 to 23.9 % in 2013 [11].

Electricity generation in Germany from 1993 to 2013 in TWh, data from [11]

The rise in the share of RES generation went along with a considerable shift of the importance of different RES generation sources. While hydro power was by far the most important RES generation source in 1993, it plays no more than a minor part in 2013. Wind, biomass, and solar power, virtually non-existent in 1993, are the most important RES generation sources in 2013 (see Fig. 4.2). Electricity generation from PV has seen large growth in recent years (from 4.4 TWh in 2008 to 30 TWh in 2013).

Composition of the RES generation mix from 1993 to 2013, data from [11]

A large part of Germany’s RES installations are distributed generation sources such as small rooftop PV installations, single wind turbines, or biomass plants. A look at PV installations, for example, reveals that more than 60 % of all installations feed in electricity in a decentralized manner at the level of low voltage grids [12]. The focus on distributed energy sources is reflected in a diverse ownership structure. More than 40 % of all RES installations in Germany are owned by private investors, with project developers and financial institutions following with 14 % and 13 % respectively [13]. Note that only roughly 12 % of RES installations are owned by power generation companies [13].

4.2.2 Power consumption

Germany’s electric power consumption amounted to about 528 TWh in 2013 [14]. The difference between gross electricity generation and consumption results from power plants’ own consumption, from electricity exports to other countries, and from line losses. Industry is the main consumer of electricity and is responsible for approximately 46 % of national electricity consumption (see Table 4.1). The residential sector follows with 26 % while the commercial and public sectors consume about 14 % and 10 % respectively. The transport and agricultural sectors play no more than minor roles with shares of roughly 2 % [14].

In comparison to China, the shares of residential and commercial loads are significantly higher in Germany. This results in a load curve with more pronounced peaks and valleys. The ancillary services necessary to cope with this pronounced load curve are mainly offered by gas-fired power plants in Germany. Neither total electricity consumption nor the relative importance of different types of consumers has changed significantly in recent years.

The increasing share of electricity generated from intermittent sources like wind and PV led to the question of how power consumption can adapt to fluctuating generation. The potential for load shifting, which is relatively easily accessible at reasonable costs, lies in Germany’s industrial sector with its large electricity consumers. Table 4.2 presents the maximum power which can be disconnected (neg.) or connected (pos.) for a short period of time in the residential, commercial, or industrial sectors according to different studies. The numbers have to been seen in relation to the German overall peak load of 80 GW.

4.2.3 Power logistics

Disparity between generation and consumption

Power generation and consumption are not equally distributed in Germany. The load centers are situated in western and southern Germany, both regions with strong industrial bases. Since the amount of electricity generated in nuclear and coal-fired power plants in these regions is generally not sufficient, they often have to import electricity from other parts of Germany or from neighboring countries. In contrast, Germany’s north and east, with their significant wind capacities, quite regularly generate more electricity than they consume. Thus, both regions frequently transfer electricity to southern and western Germany.

Grid infrastructure

Germany’s electric power grids can be classified into four different categories:

-

Extra high voltage grids (220-kV to 380-kV) form the German transmission grids. In addition to the transmission of electricity, they are responsible for the electricity feed-in of large generators such as nuclear and coal-fired power plants, or offshore wind farms. The transmission grid is mainly characterized by suspended above-surface cables with visible electricity pylons. There are currently approximately 35,000 km of transmission grids with 1,100 electricity transformers in Germany [19], [20].

-

High voltage grids (35-kV to 110-kV) are the highest voltage level of distribution grids. They act as a redistribution system at the regional level. Furthermore, high voltage grids provide electricity to large industrial consumers and are also employed to feed in electricity from smaller power plants, wind farms, and large PV parks. There are approximately 95,000 km of high voltage grids and 7,500 electricity transformers at this level [19] [20].

-

Medium voltage grids (10-kV to 30-kV) represent the subordinate level of distribution grids. They distribute electricity to the connected low voltage levels, provide electricity to connected bulk consumers, and feed in electricity from small PV parks or single wind turbines. The medium voltage level is characterized by underground cables; it is roughly 507,000 km in length and contains 560,000 local substations [19] [20].

-

Low voltage grids (230-V to 400-V) are typically also characterized by underground cables and distribute electricity from local substations to households and collect electricity from rooftop PV modules. It has an approximate length of 1,150,000 km [19].

An increasing amount of network congestion at times of peak generation is caused by small distributed rooftop PV installations on the low voltage level and rising feed-in from large wind farms at the high voltage level [21]. Due to the rapid build-up of RES generation capacities, grid capacities are not always sufficient to absorb RES-E. As a result, grid curtailment rates of solar and wind power have increased significantly within the last few years. In Schleswig-Holstein, a windy region in the north of Germany, 3.5 % of the total wind generation had to be curtailed in 2012 [22].

The curtailment of RES-E at times of peak generation can reduce the need for network investments. A recent study suggests that curtailing 30 % of PV peak production and 20 % of wind peak production could reduce infrastructure investments by 10 % between now and 2030 while a total of only 2 % of the annual electricity production from RES would be curtailed [23].

Through the transmission grid, Germany’s electric power system is well interconnected with those of neighboring countries (please refer to Fig. A.1 in the appendix for a snapshot of Germany’s transmission grids). All German TSO are members of the European Network of Transmission System Operators for Electricity (ENTSO-E), which was established in 2011 in order to

promote the completion and functioning of the internal market in electricity and cross-border trade and to ensure the optimal management, coordinated operation and sound technical evolution of the European electricity transmission network [24].

Supply security in Germany

In comparison with other European countries, Germany’s electric power system is characterized by a very high level of security of supply with, on average, only about 15 minutes of annual interruptions on the household level [25] [26].

The increasing feed-in of RES generation imposes challenges for the stability and reliability of Germany’s distribution grids. Three technical challenges for network stability caused by RES integration into distribution grids in Germany are presented in Table 4.3, together with the measures most frequently used to overcome them.

Investment needs in the grid infrastructure

Securing a high level of supply security in spite of the increasing share of electricity generated by variable RES requires significant investments in transmission and distribution grids. On the transmission grid level, it is estimated that roughly 3,600 km of 380-KV AC overhead lines will have to be installed between now and 2023 [23]. This represents a total investment of EUR 21 billion [28]. On the distribution grid level, the pressure is even higher: between 135,000 and 193,000 km will have to be added to the existing network by 2030. In addition, between 21,000 and 25,000 km of the existing distribution grid will have to be modernized in the same period of time. According to a recent study, these numbers add up to a total investment need of roughly EUR 42.5 billion on the distribution grid level [18].

4.3 Smart grid development in Germany

4.3.1 Motivation for smart grids in Germany

The rising importance of intermittent RES generation is the main smart grid driver in Germany. Today, the general opinion of most energy market experts in Germany is that building a smart grid, especially a smart distribution grid, is a cost-efficient way of ensuring security of supply in the presence of large-scale integration of intermittent RES [29], [30].

The challenge of fluctuating RES in extra high voltage grids

Germany’s transmission grids (380-kV/220-kV grid) have already achieved a high degree of smartness and are equipped with sophisticated real-time monitoring and control technologies. The increasing amount of wind power from large wind farms creates a need for more grid control. Sophisticated generation forecasts, for example, are needed to adequately react to the pools of fluctuating generators and maintain the 50 Hz grid frequency within its narrow tolerance range of ± 0.2 Hz.

The challenge of fluctuating RES in high voltage grids

The 110-kV high voltage grid also requires high availability and near-real-time monitoring and control. The main challenge within high voltage grids is to maintain voltage levels and loads within a technically viable band. In the event of overloads, for example arising from a high volume of RES-E, electricity has to be transferred to the higher voltage level. Bidirectional flows of electrical power are an additional challenge at the level of 110-kV high voltage grids. If overloads cannot be transferred to the higher voltage level, generation has to be curtailed or additional loads have to be activiated.

The challenge of fluctuating RES in medium voltage grids

Supply quality, specifically with regard to voltage maintenance, constitutes a major technical challenge in medium voltage grids due to the fluctuating and distributed generation from RES. The degree of utilization of ICT in medium voltage grids is limited. Continuous load measurement, for example, is used only for customers with consumption levels exceeding 100 MWh/a. As prescribed by the Electricity Network Access Ordinance (StromNZV), these customers’ average power consumption must be measured in periods of 15 minutes and this information delivered to the distribution grid operator which then uses the measurement data to compute a specific load profile. The measurement equipment is operated by the DSO or by the metering system operator. Like at the 110-kV level, wind and PV plants may result in inverted flows of electricity to the higher voltage level in order to avoid an overload of grid assets, especially in rural areas with a more limited infrastructure.

The challenge of fluctuating RES in low voltage grids

Today, ICT-based grid operation is very rarely installed at the level of low voltage grids, where rooftop PV represents a major challenge in terms of voltage maintenance and can cause a more rapid aging of grid assets. Grid operators currently handle these challenges by expanding the grid infrastructure with new cables or local substations. In the future, electric mobility may further increase the necessity for active control of low voltage grids. It should be noted that the control of assets in low voltage grids is especially difficult due to the large number and high heterogeneity of the connected assets (e. g. households, rooftop PV modules, local substations, electric vehicles). Thus, standardization of control interfaces is viewed as one of the key issues for assets being installed in low voltage grids [31].

4.3.2 Germany’s technological view of the smart grid

The development of smart grids in Germany

In Germany, smart grid technologies have been described, combined, tested, and implemented in a bottom-up process by research institutions, companies from the electric power sector, component suppliers, and ICT companies.

The primary driver for smart grid development was the integration of RES into the operational environments of grid operators. Their integration mainly relies on large monolithic supervisory control and data acquisition (SCADA) systems. Small amounts of renewables were controlled in parallel to the overall grid operations, often in so-called distributed energy management systems (DEMS). In terms of communications, the systems used existing communication infrastructure and heterogeneous proprietary data models and protocols. The need to integrate RES in daily grid operations led to a change in the paradigms on how to design and control RES. Aspects relating to the connection between different assets were the first to be focused upon – general packet radio service (GPRS), GSM, universal mobile telecommunications system (UMTS), and currently long term evolution (LTE) or IP-based open networks such as the internet have been used. After this initial focus on connectivity, more emphasis was put on the semantics and syntactical aspects of communication.

The government’s view on smart grids

As in China, different stakeholders in Germany have developed different views on smart grids. The primary goal of the German government, especially via the Federal Ministry for Economic Affairs and Energy (BMWi) and BNetzA, is to guide the debate and support convergence of the various stakeholders’ smart grid visions. BNetzA, in late 2011, published a position paper called Smart Grid and Smart Market [32] (see [33] for an English summary of this document).

The main objective of this document was to introduce a clear-cut criterion on how smart grids and so-called smart markets can be differentiated and to discuss the regulatory consequences. BNetzA points out that electricity volumes and related services have traditionally been traded on electricity markets independently from the available grid capacity.Footnote 3 In a power system based on smart grids, however, information on current grid status can be taken into account in market transactions. Markets allowing the trade of electricity volumes and related services based on available grid capacities are referred to as smart markets. Depending on the available grid capacity, smart markets can either operate without restriction – in case of sufficient grid capacity, or – in case of grid congestion – the grid operator has the right to intervene in the market to ensure grid stability and e. g. shut down power plants or cut off consumers [33]. One example for smart markets are regional energy market places.Footnote 4 Within a specific region, industrial, commercial, and domestic customers are given the option of trading electricity volumes and/or ancillary services in a market place. By trading ancillary services, power consumption schedules, and power generation (feed-in) schedules, market participants are exposed to price signals serving as an economic incentive to balance electricity supply and demand and thus stabilize the grid.

The position paper Smart Grid and Smart Market discusses relevant topics along six key concepts:

-

The first key concept, named Grid capacity and energy volumes as distinguishing criteria for grid and market, explains how grids and markets can be separated by identifying the main topics involved. All aspects relating to grid capacity (as measured in kW, MW, GW, etc.) refer to the grid whereas all topics relating to energy volumes (as measured in kWh, MWh, GWh, etc.) refer to the market.

-

The second key concept, Clarification of the discussion about the energy future through the terms of smart grid and smart market, follows-up on the first key concept. It clarifies that the term smart grid can be related to network issues while the term smart market can be related to energy volume issues.

-

The third key concept has the somewhat cumbersome title The energy future requires more responsibility on the market and more negotiated solutions. The grid should play a predominantly service role and should be separated from competitive activities as far as possible. It discusses the importance of new market actors in smart markets and underlines that competitive functions, especially those in smart markets, should not be attributed to grid operators. Grid operators are considered responsible only for the (smart) grid itself. Smart grids are seen as a platform for smart markets. Grid operators are consequently viewed as playing a supporting role for smart markets.

-

The fourth key concept, entitled Smart meters are part of, but not an absolute prerequisite for, the energy future, states that grids can be made smart without a widespread rollout of smart meters. The main argument is that it is sufficient to measure data on grid conditions in local substations or to install only some smart meters at potentially critical junctures in the grid.

-

The fifth key concept, named The smart grid is a part of an evolutionary, not a revolutionary, process, emphasizes that smart grids are not built from scratch but evolve in a gradual process. In the light of the heterogeneity of the various grid operators in Germany, BNetzA consequently stresses that a kind of uniform smart grid concept applicable to every grid operator does not exist and should not be promoted by means of regulation.

-

The sixth key concept is named If targets for the use of renewable energy are to be met it is essential that these producers, too, respond to market signals and grid exigencies. It underlines the importance of integrating RES more effectively in wholesale markets, potentially by redesigning the feed-in priority for RES.

Smart grids according to a recent study by the German Academy of Science and Engineering

In 2012, under the guidance of the German Academy of Science and Engineering (acatech), representatives of the electric power sector, equipment manufacturers sector, ICT sector, and from academia and research institutions developed a smart grid model for Germany: the Future Energy Grid (FEG) model [30]. The model complements the BNetzA view on smart grids by developing a conceptual and technological foundation for the separation of smart grids and smart markets. In particular, FEG can serve as a best practice example of how to develop and formulate a comprehensive smart grid vision. FEG is a systematic and comprehensive top-down approach that can be used to evaluate the current smartness of grids and to define a smart grid vision. It systematically addresses specific problems and challenges in Germany’s electric power system and introduces a model of system layers (see Fig. 4.3) and technology areas (see Fig. 4.4). The system layers represent different functions and requirements regarding the application of ICT in the power system. They were chosen in reference to a model adapted by the European Electricity Grid Initiative (see [34]).

Abstract smart grid system model regarding the application of ICT within three distinct layers, translated from [30]

Technology areas regarding ICT aspects of smart grid implementation in Germany, translated from [30]

In total, FEG comprises the following three system layers (see Fig. 4.3):

-

The innermost layer, referred to as the closed system layer, contains the critical infrastructure and power system equipment that serves as the backbone of the system and requires a high level of security and safety. Therefore, external access to the resources within this layer is restricted and may be limited to the grid operator or to an equivalent actor. Central (bulk) power generation, transmission and distribution grids, and the corresponding ICT-based control systems are components of this layer.

-

The outermost layer is referred to as the networked system layer. It contains heterogeneous power system components (distributed power generators, power storage units, consumers, marketplaces, meters, control applications, etc.) which are characterized by a high level of communication and information exchange. In contrast to the closed system layer, much of the value within this layer is created by interactions between the different participants on smart markets. As the exchange of sensitive power system information, e. g. real-time data on power generation and consumption, is of particular importance in this context, strict ICT and data security protocols have to be applied to ensure individual privacy rights are respected and overall power system security is guaranteed.

-

The ICT infrastructure layer enables communication within and between the two other layers. It contains the communication networks and associated components that provide ICT interface functionalities. In order to ensure that different components of each layer can communicate with each other, interoperability is a key factor. Interoperability is achieved with the help of standardization of system interfaces and communication protocols.

In the study Future Energy Grid, a smart grid vision based on the three system layers described above and nineteen technology areas is outlined (see Fig. 4.4, for a detailed description refer to appendix D).

4.4 The regulation of Germany’s electric power system

4.4.1 Policy setting and fundamental institutions

Policy setting

The Federal Government’s Energy concept for an environmentally friendly, reliable and affordable energy supply of September 2010 and The road to the energy of the future – safe, affordable and environmentally friendly (Key Elements of an energy policy concept) of June 2011 [35] contain guidelines and objectives relating to Germany’s future energy system. In particular, the trend towards more environmental protection is explicitly expressed by government plans to reduce CO2 emissions to 60 % of the 1990-level by 2020. It is planned to further reduce emissions to 20 % of the level of 1990 until 2050 [35].

These cuts in CO2 emissions are to be achieved by reduced energy use for transport and heating (see Fig. 4.5): e. g. energy consumption for room heating purposes should be reduced by 20 % between 2008 and 2020 and 80 % by 2050. For the power sector, the government’s objective is to generate 35 % of electricity with RES in 2020 and to increase the share to 80 % by 2050 [35] as shown in Fig. 4.5. At the same time, in the aftermath of the nuclear disaster in Fukushima, the German government decided to completely phase out nuclear power generation by 2022 [35].

Long-term targets for Germany’s energy sector (© Heinrich-Böll-Stiftung e. V. [36])

Many specific objectives with regard to the development of Germany’s power system are subordinated to the general goal of achieving more sustainability and the specific goal of increasing the importance of RES: for instance, the German government wants to expand transmission grids in the north-south direction, thus allowing a more effective transport of wind power from the north to the load centers in the south of the country. Other government goals such as improving energy efficiency and promoting energy storage technologies and electric vehicles are also related to the broad government plan of increasing the sustainability of Germany’s power system.

General governance structure

The governance structure of Germany’s energy system comprises several ministries and independent institutions. The ministries are responsible for enacting laws and ordinances that then have to be applied by independent institutions. This means that the ministry concerned can neither interfere in day-to-day business nor expand or restrict the competences of the institutions. Nonetheless, these institutions and the ministries cooperate closely.

Ministries responsible for Germany’s energy policy

There are currently two ministries at the core of the governance structure of the German electricity system:

-

The Federal Ministry for Economic Affairs and Energy (BMWi) has the main responsibility for formulating and implementing energy policy, including renewable energy, and is responsible for issues related to security of supply and competition policy.

-

The Federal Ministry for the Environment, Nature Conservation, Building and Nuclear Safety (BMUB) is responsible for those energy policy issues which are directly related to environmental protection, e. g. CO2 reduction, and energy efficiency in the building sector.

The market design of the electricity sector is a responsibility shared by BMWi and BMUB. Other relevant ministries in the context of energy and electricity sector policy and smart grids are:

-

The Federal Ministry of Transport and Digital Infrastructure (BMVI) takes responsibility for transportation and mobility issues as well as for the expansion of digital communication infrastructure, which is especially important as a backbone for smart grids.

-

The Federal Ministry of Labor, Social Affairs and Consumer Protection (BMAS) focuses on social issues related to energy.

Institutions responsible for Germany’s energy policy

The following three government authorities are of particular relevance with regard to the regulation of Germany’s electric power system:

-

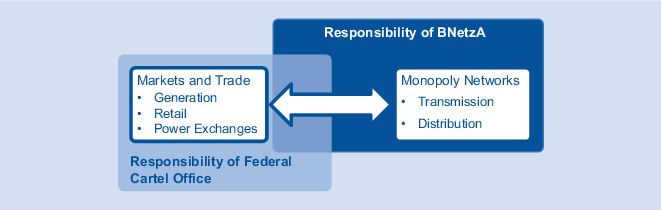

The Federal Network Agency for Electricity, Gas, Telecommunications, Post and Railway (BNetzA) is responsible for regulation of the networks which are natural monopolies, including the electricity grid (see Fig. 4.6). The existence and competences of BNetzA are laid down in laws such as EnWG and the Grid Expansion Acceleration Act for Transmission Networks (NABEG).Footnote 5 While BNetzA is in charge of national and interstate regulation it cooperates closely with regulatory counterparts on the level of the federal states. State regulators are responsible for DSO with less than 100,000 customers and BNetzA for all TSO and for DSO with more than 100,000 customers or with operations in more than one state.

Fig. 4.6

Responsibilities of BNetzA and of the Federal Cartel Office

-

The Federal Cartel Office is responsible for general competition matters (see Fig. 4.6). If competition problems are related to natural monopoly networks, the Federal Cartel Office can authorize BNetzA to handle the issue. The existence and competences of the Federal Cartel Office are laid down in the Act Against Restraints of Competition (GWB).

-

The Monopoly Commission advises on competition and monopoly issues. Its advice is non-binding and it does not have decision-making powers. Nonetheless, the Monopoly Commission plays a vital role in checking and evaluating the regulator’s work. The tasks of the Monopoly Commission are also laid down in GWB.

A brief history of BNetzA

The liberalization of European electricity markets began with the EU’s First Electricity Directive of 1996. A so-called negotiated Third Party Access (nTPA) was allowed as an option alongside regulated Third Party Access (rTPA). nTPA meant that access to the electricity networks, including network charges, had to be negotiated between network owners (grid operators) and network users (power companies). The directive did not explicitly prescribe a regulator and ultimately this approach failed to secure non-discriminatory network access and to deliver fair and reasonable network charges (cf. e. g. [37], [38] for an analysis and further literature).

The EU’s Second Electricity Directive of 2003 contained significant changes: rTPA became the only option making non-discriminatory network access conditions a requirement by law. The Directive also demanded the establishment of an electricity sector regulator and the creation of a regulatory framework for fair and reasonable network charges. In Germany, EnWG was amended to satisfy these demands, resulting in the establishment of BNetzA as a federal regulator for monopolistic networks and the development of incentive regulation (see Sect. 4.4.4 for more information on incentive regulation). The regulatory competences of BNetzA were based on the competences of its predecessor, which was the Regulatory Agency for Telecommunications and Post Services. Competences relating to electricity and gas were added, and the agency was renamed to BNetzA. Later on, the task of regulating the railway infrastructure was added as well.

The EU’s Third Electricity Directive of 2009 did not change the arrangements on rTPA or regulation. Instead, it strengthened the arrangements relating to unbundling rules. For the TSO, this led to the ITO approach while for DSO the unbundling rules stayed as they were in the Second Electricity Directive (see Sect. 4.1). BNetzA is also responsible for implementing the unbundling rules and monitoring compliance with them. Lastly, the Third Electricity Directive led to the creation of an Agency for the Cooperation of Energy Regulators (ACER). In a nutshell, ACER is responsible for cross-border issues and provides a platform for cooperation between various European regulators.

Main tasks and competences of BNetzA

The mission of BNetzA is to regulate the monopolistic part of the supply chain – the grid or network infrastructure by:

-

guaranteeing an affordable, consumer-friendly, efficient and environmentally friendly supply of electricity and gas,

-

ensuring an effective and undistorted competition in the supply of electricity and gas as well as securing a reliable operation of electricity and gas grids,

-

transposing and implement EU law in the field of grid-bound energy supply and

-

facilitating efficient approval processes to adapt the German high-voltage transmission grid to the needs of a rising share of renewable energy [39].

In this context, the two main tasks of the BNetzA are:

-

to secure non-discriminatory access to the network and

-

to regulate network charges.

This is reflected by the organizational structure of BNetzA (see Fig. 4.7). BNetzA consists of several departments. Two of them (Department 6 and Department N) focus on energy and network regulation. The decision process within BNetzA takes place within so-called ruling chambers. BNetzA has nine ruling chambers with decision-making powers, with five of these relating to electricity and gas:

BNetzA organization chart, adapted from [40]

-

network development and approval of individual network charges (ruling chamber 4 in Fig. 4.7),

-

access to electricity networks (ruling chamber 6 in Fig. 4.7),

-

access to gas networks (ruling chamber 7 in Fig. 4.7),

-

regulation of electricity networks (ruling chamber 8 in Fig. 4.7), and

-

regulation of gas networks (ruling chamber 9 in Fig. 4.7).

Note the focus on and restriction to networks as the core monopoly part of the supply chain. BNetzA is not responsible for the markets, where these are not related to the networks. Strictly speaking, BNetzA is not responsible for general competitive conditions, for example merger policy, which is one of the tasks of the Federal Cartel Office. In practice, however, the Federal Cartel Office and BNetzA cooperate closely. Moreover, BNetzA monitors market development in a so-called Monitoring Report, which is published on an annual basis.

Additional tasks of BNetzA

In addition to securing non-discriminatory access to the network and regulating network charges, further BNetzA tasks are:

-

ensuring consumer protection in retail issues (e. g. rules for switching the power retail company),

-

implementing and monitoring unbundling rules,

-

evaluating the network development plan (NDP),

-

approving network expansion plans and helping to accelerate licensing procedures for network expansion, as arranged by NABEG,

-

exchanging information with other European regulators, formally or informally, and cross-border issues (e. g. the interconnectors),

-

providing support for technical standards, and

-

providing data on power plants and electricity networks to the public.

Competences of BNetzA

It is of critical importance for the regulator to be powerful enough to impose sanctions on the grid operators. In Germany, this is regulated in § 29 to § 33 EnWG, which define the competences of BNetzA and the possible range of penalties it can impose:

-

§ 29 EnWG lists all discriminating behaviors of grid operators which can be penalized by BNetzA.

-

According to § 30 EnWG, BNetzA can force grid operators to stop any discriminating behavior against other market participants.

-

According to § 31 EnWG, information on discriminatory behavior of a grid operator can be provided to BNetzA by any legal or natural person.

-

§ 32 and § 33 EnWG specify how fines and compensation payments are to be settled in case of misconduct by a grid operator.

4.4.2 Market structure

Vertical and horizontal market structure

As described in Sect. 4.1, the stages in the supply chain of Germany’s electric power sector are in a state of far-reaching unbundling: transmission grids, for example, are owned and operated by fully unbundled companies that are independent from other parts of the supply chain. Distribution grid operators are legally unbundled from generation and retail companies so as to ensure that, within the same utility, no commercially sensitive information is exchanged between the power grid and other parts of the supply chain.

Competition in power generation has been increasing significantly in Germany since the EU’s First Electricity Directive. Before 1996, generation was monopolized by four major companies (RWE, E.ON, Vattenfall Europe, and EnBW). Meanwhile, these four companies together represent a market share of no more than roughly 44 % of total installed electricity generation capacities [41]. The decreasing market share of the former monopolists is also a result of the nuclear phase-out and the increasing share of distributed generation from RES. The growing importance of RES in particular has served as a key driver for competition in the generation sector. While investments into conventional power plants are a capital-intensive business, investments into RES have become profitable for small investors due to the guaranteed feed-in tariffs for renewables. As a result, there are currently some 300 smaller generation companies with capacities starting at 1 MW up to hundreds of MW.

The situation is similar in the retail sector. The market share of the four former monopolists has been continuously decreasing from 50 % in 2008 to 45 % in 2011 [19]. Most German retail companies have a regional focus with a high market share within their established service areas. Consumer switching rates to other retailers are still quite low due to the end consumers’ tendency to remain with the incumbent regional suppliers. In 2012, for example, only about 7.8 % of all households in Germany changed their electricity supplier [19].

The ownership structure on the transmission and distribution level is as follows: on the transmission level, four TSO own the infrastructure while roughly 900 DSO own parts of the distribution grid. Since electricity networks are a natural monopoly with network charges regulated by BNetzA, there is no competition for markets and customers between the different grid operators.

The emergence of new market actors

The unbundling process, the legally enforced trend towards more competition, as well as the migration towards smart grids and RES have contributed to the emergence of new market actors in Germany. Their growing importance can be considered as the most profound change in Germany’s electricity market structure during the last few years. A considerable number of new players have entered the supply chain of the electric power system: Figure 4.8 shows that the number of companies active in the German energy sector (including electricity, gas, heat, etc.) increased from 15,666 in 2006 to 48,292 in 2011 [42]. This represents an increase of more than 200 % within five years. Especially companies with less than nine employees, often innovative start-ups and energy service providers, have contributed to this increase. Their number increased from 14,545 in 2006 to 46,967 in 2013 [43].

Number of companies active in the German energy sector, data from [43]

Figure 4.9 presents an exemplary overview of established and new market actors in smart grids, as they are present or emerging in Germany, classified into the different smart grid supply chain areas Power Generation, Power Logistics, Power Trade and Retail, Power Consumption, and Information and Communication. In the following, some examples of new market actors depicted in Fig. 4.9 are described together with a brief explanation on their role in the smart grid development process:

Examples of established and new market actors in smart grids in Germany

4.4.2 Power Generation:

-

RES operators:

Traditionally, power plants in Germany were exclusively owned and operated by large utilities. Due to the financial support codified in EEG (see Sect. 4.4.3), a number of more than 1,500,000 RES plants, especially onshore wind, PV and biomass plants, has been installed so far. The largest part of these plants is operated by households as well as small and medium-sized companies: in 2013 for example, 6 % of all German households had their own RES generation units, especially small rooftop PV installations [44]. Companies in the manufacturing industry have also long since started to build their own RES generation units. By 2005, roughly 5 % of all German manufacturing companies owned RES. This number has more than tripled since, reaching roughly 18 % in 2012 [45].

-

New energy cooperatives:

In the tradition of cooperatives founded in Germany in the beginning of the 20th century to develop the first power supply systems, new energy cooperatives have emerged in recent years. These associations allow individual citizens or civil society to pool their financial resources and jointly invest in power system components otherwise exceeding the financial resources of their individual members. In Germany, 650 energy cooperatives with roughly 130,000 members invested more than one billion euros in power plants based on RES until 2012 [46].

4.4.2 Power Logistics:

-

Grid operations service providers:

This type of company specializes in offering services to operate smart grids for small-sized or municipally owned German DSO. The business model of grid operation service providers works out, since the small DSO often do not have the highly specialized personnel required for smart grid operation (i. e. with deep knowledge of ICT capabilities and with the required level of grid automation knowledge). A single grid operation service provider may operate the smart grids of several small DSO.

4.4.2 Power Trade & Retail:

-

VPP operators:

A virtual power plant is a network of decentralized, small to medium-scale power generating units such as biomass plants, combined heat and power (CHP) units, wind farms and solar parks. The interconnected units are partly operated through central control of the virtual power plant but nevertheless remain independent in their operation and ownership. Virtual power plants (VPP) deliver electricity products, such as balancing power, that can be traded on electricity market places. Product requirements, e. g. the minimum volume of the delivered power, are restrictive and usually cannot be met by single small scale power plants, like e. g. a single wind farm. VPP therefore bundle (aggregate) several small scale power plants and often even add other generation capacities and/or flexible loads, to fulfil the product requirements of the energy market places. Thus, the power generation of the units in the virtual power plant is bundled – or aggregated – and sold by a single trader on the energy exchange or other energy market places (e. g. market for balancing power). As a result, VPP can gradually take over the role of traditional power plants – selling their output in the wholesale markets. Today, in Germany, about 20 medium sized companies operate VPP.

-

Specialized marketplace operators:

These market actors operate market places e. g. for ancillary services or for electricity from well-defined sources. The concept of specialized market places has been piloted in several research projects of the German E-Energy program (see Sect. 4.4.6 for more information on the E-Energy program).

-

Power traders:

A person or entity that buys and sells energy goods and services in an organized electricity market (electricity or power exchange) or over-the-counter (OTC). Power traders offer dedicated electricity wholesale services to other market actors, e. g. industry companies or power retailers companies or larger end-users (like energy-intensive industry). Due to the complex nature of electricity markets, trading requires specialist knowledge and expertise, comparable to financial service providers. In Germany, power trading services are offered by some 50 companies [19].

-

Independent retailers:

Liberalization of the energy market in Europe led to the establishment of mostly medium-sized power retail companies that are independent from the established utilities. These companies offer their customers heterogeneous energy-based retail products, e. g. regional tariffs, time-of-use pricing or electricity with a low CO2-footprint. These products are widely accepted both by the population and by enterprises.

4.4.2 Power Consumption:

-

Smart appliance contractors:

Households as well as enterprises operate a growing multitude of power-consuming appliances like heating equipment, cooling devices or home electricity storage (so-called smart appliances). For these clients, smart appliance contractors offer individual services such as financing, installation, operation, maintenance, support and appliance replacement. Other contractors act as full-service providers and offer volume-based heating, cooling or load management services.

-

Prosumers:

The term prosumer is merged from the terms producer and consumer. Besides consuming power, these new market actors deliver surplus power to the grid, e. g. through small-scale rooftop PV or combined heat and power (CHP) plants.

-

Energy management service providers:

Energy management service providers deliver energy monitoring and controlling services to industry and large commercial companies. With their service portfolio they contribute to continuous improvement of energy procurement and use in smart grids.

-

Energy efficiency consultants:

These typically small-sized companies analyze the energy consumption of private households, enterprises, industry and municipalities in order to identify potentials for energy savings and energy efficiency improvements and consult the clients in efficient power usage. In a typical business model the advisory is paid for with a share of the savings generated from energy efficiency improvements. In Germany, a number of nearly 12,500 companies carried out more than 400,000 consulting projects in 2011 [47].

-

E-Vehicle infrastructure operators:

Electric vehicles need charging stations. These are built and/or operated by a growing number of infrastructure operators.

-

E-Vehicle service providers:

These new market actors are typically big-sized or mid-sized companies. E-Vehicle service providers operate pools of electric vehicles and rent them to companies and private consumers.

4.4.2 Information & Communication:

-

Metering system operators:

These companies install and operate electricity metering equipment. Metering system operators are an example for a new market role that has been created by the German government. Their role is described by EnWG (§ 21) and the Metering Access Ordinance (MessZV).

-

Metering service providers:

Metering service providers offer the service of reading out meter systems and delivering the gathered data to power retailers as a basis for billing. Their role is also described by EnWG (§ 21) and the Metering Access Ordinance.

-

Energy information service providers:

All market actors in smart grids require energy-related information to carry out their tasks and businesses, e. g. current or historical grid status data, metering data or weather data. Energy information service providers collect raw data from multiple sources, analyze and refine the data and then offer specialized information services to their customers. One example of an energy information service is wind and PV power generation forecasts, which are typically derived from a multitude of different weather data sources.

-

Energy system integrators:

Energy system integrators are established or new companies which develop ICT-based system solutions in all segments of the smart grid supply chain for their customers, e. g. solutions for advanced distribution system management and grid maintenance solutions for DSO, smart metering solutions for metering service providers or virtual power plant management solutions for VPP operators. The ICT sector in Europe has increasingly been participating in the development of smart grids and is involved in approximately 60 % of all related research projects [48]. The ICT-related smart grid concepts developed by energy system integrators contribute to the general understanding of smart grids among established and new market actors, public decision-makers, and the general public.

4.4.3 Market design and RES integration

General market design

German electricity wholesale markets bring together roughly 300 power generation companies, about 50 power trading companies, and approximately 1,110 power retail companies [19]. A high level of liquidity indicates that electricity wholesale markets are functioning well [19]. The German wholesale market is currently separated into two major energy-only markets (see Fig. 4.10):

Electricity wholesale markets in Germany

-

The European Energy Exchange (EEX) with two products: spot (short-term) and future (long-term) markets for electricity. In contrast to China, there is only one uniform wholesale price for electricity in Germany irrespective of the power source, production technology, or age of the power plant under consideration. The market price – for all generators – at any given time is determined by the marginal costs of the last power plant required to satisfy total electricity demand. This nationally integrated market leads to a situation in which, at any point in time, only those power plants with the lowest marginal costs of production are able to sell their electricity on the market.

-

The over-the-counter (OTC) market gives suppliers and buyers of electricity the opportunity to bilaterally trade electricity and to negotiate contracts and prices irrespective of standardized contracts or prices at the power exchange. Like the EEX, OTC contracts offer the possibility for spot and future trades. Products on both markets can be the same, e. g. short-term contracts with direct physical fulfillment can be either traded via the exchange or negotiated directly with another party on the OTC spot market.

Most of Germany’s electricity is traded bilaterally between generation and retail companies. In 2012 for example, 7,000 TWh of electricity were traded in OTC transactions, whereas only approximately 1,200 TWh were traded at the EEX [19].Footnote 6 The attractiveness of OTC trading results from the fact that OTC products can be designed more flexibly according to the specific needs of the parties involved. Nonetheless, EEX prices are very important because they serve as a reference value for OTC trading.

While generation and retail companies use the power exchange to trade electricity especially for short-term contracts (physical fulfillment), most of the trade at the power exchange is focused on the exchange of futures. Here electricity traders focus on financial exchanges. Traders expect to gain benefits through the arbitrage between different future periods. Retail companies have to pay the generators for the electricity produced and the grid operator for the transport of the electricity. The generation company needs to inform TSO in advance about the exact electricity volume that its facility will produce within a certain period of time and to which customer (e. g. power retail companies) the electricity needs to be transported.

Promotion and integration of RES

To subsidize the development of RES, a fixed feed-in tariff which is significantly above market prices is paid to RES owners. The EEG, which regulates the promotion of RES, was enacted in 2000 on the basis of the former Act on the Feed-In of Electricity from RES into the Public Grid, itself enacted in December 1990. The EEG regulates a feed-in system that comprises four key elements:

-

Fixed feed-in tariff: for each kWh produced and fed into the grid, a fixed price is paid which is higher than the wholesale market price for electricity.

-

Take-up obligation: grid operators must buy the electricity from RES at all times and pay the feed-in tariff independently from current market prices.

-

RES priority: RES has priority over non-RES in case of network congestion.

-

RES curtailment in last resort: in case of network congestion, conventional power supply needs to be curtailed as much as possible before RES can be curtailed as well.

Feed-in tariffs at a glance

The feed-in tariffs are usually paid for electricity stemming from hydro power, landfill gas, gas from purification plants, mine gas, biomass, biogas, geothermal power, onshore wind, offshore wind, small-sized rooftop PV installations, and large-scale PV parks. With regard to the specific design of the feed-in tariffs, three aspects must be considered:

-

First, feed-in tariffs differ depending on the power source under consideration.

-

Second, feed-in tariffs for installations using the same power source often depend on the installed capacity with higher feed-in tariffs applying to smaller installations.

-

Third, feed-in tariffs are paid for a period of 20 years and the feed-in tariff paid for each installation at the moment of its commissioning is guaranteed over the whole period.Footnote 7

Feed-in tariffs for new installations have been steadily adjusted downwards since the implementation of the EEG in 2000, reflecting technical progress and the declining costs of RES. However, feed-in tariffs for installations that went into service before the adjustments remain at their originally guaranteed level. To facilitate planning for RES investors, future reductions of the feed-in tariffs are already known today and recorded in specific reduction schemes that are part of governmental supplements to the EEG. Depending on the capacity and some other characteristics of the installations, the following ranges of feed-in tariffs for the power sources with the highest relevance were paid in 2012 [49]:

-

Hydro: 0.034 €/kWh–0.127 €/kWh

-

Onshore wind: 0.0893 €/kWh–0.0991 €/kWh

-

Offshore wind: 0.15 €/kWh–0.19 €/kWh

-

Biomass: 0.06 €/kWh–0.143 €/kWh

-

PV: 0.1794 €/kWh–0.2443 €/kWh

Financial burden caused by feed-in tariffs

Electricity generated by means of RES (RES-E) is traded on wholesale markets irrespectively of the feed-in tariffs. RES-E enters Germany’s wholesale markets in the following way:

-

Generators of RES-E receive the feed-in tariff from their respective distribution grid operator, who in turn gets an equivalent compensation from the transmission grid operator.

-

The transmission grid operator sells RES-E on a wholesale market, frequently receiving a price considerably lower than the governmentally fixed feed-in tariff.

-

To avoid financial burdens for transmission grid operators as a result of this practice, the difference between the fixed feed-in tariffs and the market prices for electricity is refunded in full to the transmission grid operator.

-

The financial capital for this compensation stems from the electricity consumers, who have to pay a surcharge for the promotion of RES on their electricity bill (renewable energy surcharge). The amount of the surcharge depends on the type of consumer (with high discounts for industrial consumers) but does not depend on the consumer’s geographic location.

The financial burden caused by this compensation has increased significantly in the course of the past years. In 2000, approximately one billion euros was necessary to cover the difference costs of RES feed-in tariffs.Footnote 8 This figure increased to approximately EUR 16 billion in 2012 and is projected to amount to roughly EUR 20 billion in 2014 [50]. Owing to the increasing share of RES in Germany’s electricity mix, the renewable energy surcharge rose from 0.0008 €/kWh in 2000 to 0.0528 €/kWh in 2013 [51]. Germany has made the experience that setting up a system with feed-in tariffs financed by means of a surcharge that does not vary in different regions redirects purchasing power from regions with high loads towards regions with high RES capacities. Berlin, with its more than 3 million inhabitants (roughly 4.1 % of Germany’s total population), received only 0.1 % of all RES connected payments, whereas Schleswig-Holstein, a federal state in Northern Germany with less than 3 million inhabitants (about 3.5 % of the population), received 7.0 % of all RES connected payments [51]. However, Berlin’s population did not pay less than the population in Schleswig-Holstein to finance the RES funds. This means that purchasing power was implicitly redirected from Berlin to Schleswig-Holstein owing to the RES financing mechanism.

The effects of RES on wholesale electricity prices

The price on the wholesale electricity market is determined by the marginal costs of the last power plant required to satisfy total electricity demand setting the price which is applied to all generators at that point in time. The power plants are ranked according to their marginal costs of electricity generation (merit order), with the plants with the lowest marginal costs necessary to meet demand dispatched first and the ones with the highest marginal costs brought online last.

TSO are mandated by law to prioritize the feed-in of RES before other conventional generation technologies. Once installed and connected to the grid, wind and PV installations can produce electricity with almost zero marginal costs, while costs of electricity generation from fossil fuel-fired power plants depends on the price of the combustibles used (fuel costs). Thus, electricity generated from RES enters the wholesale markets at the beginning of the merit order (at zero marginal costs) and is dispatched first. As a consequence, average wholesale prices decrease as the generation technologies with higher marginal costs are displaced by an increasing volume of RES-E. Thus, large-scale integration of RES-E suppresses wholesale electricity prices. This is known as the so-called merit order effect (see Fig. 4.11). With large amounts of RES-E traded on the wholesale markets (on windy and sunny days), wholesale prices are rather low. When high feed-in of RES-E corresponds to low demand on the consumption side (typically on Sundays), prices for electricity can even reach negative values. On these days, Germany sometimes exports electricity to foreign countries and has to remunerate these countries for absorbing the German electricity. There were negative spot market prices for almost 80 hours in 2013. Such negative prices occurred in ten of twelve months [52]. In conclusion, it can be said that the increasing share of RES leads to decreasing but much more volatile prices on the wholesale markets.

Effects of RES supply on the wholesale electricity prices

As wholesale market prices decrease, gas-fired power plants, which have high marginal costs, are dispatched less and less frequently making an economically viable operation difficult and deterring investors. However, with their flexibility and fast ramp times gas-fired power plants are considered a necessary part of a power system with a high share of variable RES. Due to these developments, discussions on a revision of the EEG and alternative support schemes and incentive mechanisms for investments in conventional power plants are currently taking place in Germany.

Electricity retail markets and prices

Electricity retail markets are based on bilateral standardized contracts without any interactions on marketplaces. They are less complex than wholesale markets. In both Germany and China, households and industrial consumers pay different retail prices. In contrast to China, German households have to pay significantly more than industrial consumers. In 2012, the price amounted to roughly 0.13 €/kWh for industrial consumers, whereas the price for household consumers amounted to approximately 0.26 €/kWh [53]. These privileges for industrial consumers were introduced to increase the competitiveness of Germany’s industry on world markets.

The retail price for electricity can be subdivided into three main categories:

-

Taxes (electricity tax and value-added-tax) and fees (mainly concessional duties and the renewable energy surcharge) currently make up approximately 50 % of the electricity price.

-

Costs of power generation and retail amount to approximately 30 % of the price. Between 1998 and 2000, these costs decreased from 0.1291 €/kWh to 0.0858 €/kWh as a result of the market liberalization of 1998, which created more market competition in all areas of the power sector supply chain. In the following years, the size of this price component increased slowly but steadily until 2009 and has remained rather stable since then [53].

-

Governmentally regulated network charges compensating grid operators for electricity transmission and distribution. Network charges make up roughly 20 % of the retail price paid by household consumers [3]

Figure 4.12 illustrates the development of electricity prices for private households and its composition in Germany since 2006. The electricity retail price has increased due to rising costs of power generation and retail as well as rising taxes and surcharges (fees), which increased from 0.0714 €/kWh in 2006 to 0.1163 €/kWh by 2012 [53]. The increase of the renewable energy surcharge from 0.008 €/kWh in 2006 to 0.0528 €/kWh in 2013 contributed to this development. In the same timeframe, the network charges decreased slightly.

Development of the electricity price for private households in Germany, adapted from [3]

4.4.4 Development of infrastructure and network regulation

Coordination of network expansion

In Germany, many different stakeholders are involved in grid expansion planning. Even if planning activity is mainly in the hands of TSO and BNetzA, other established power sector companies, third parties and the public can also influence network expansion planning. From a legal point of view, the expansion of the electric power grid is mainly regulated by EnWG, by the Energy Network Development Act (EnLAG), and by NABEG:

-

§ 12 EnWG states that transmission grid operators are responsible for elaborating and issuing a coordinated network expansion plan each year. This plan is supposed to describe which upgrades of the transmission grids will be necessary during the following ten years. The process of network expansion planning is monitored by BNetzA. It allows for public participation and is open to comments from various stakeholders.

-

EnLAG defines specific investment projects in single transmission lines with the intention of facilitating the integration of RES, improving the interconnection with neighboring countries, easing the connection of new power plants, and reducing network congestions.

-

NABEG further specifies procedures relating to the network expansion plan. Its main motivation is to accelerate the planning and approval procedures of network expansion.

Cost pass-through regulation until 2009

The costs of investments in the grid infrastructure are shared by all electricity consumers via network charges. Until 2009, investment into the grid infrastructure was regulated using a so-called cost pass-through regulation which was also applied in many European countries and the United States. Cost pass-through regulation adjusts permissible revenues according to the grid operator’s accounting and capital costs. The primary advantage of this system is that it lowers investment risks as practically all costs can be passed on to the end-user (via network charges), thus encouraging investment in the infrastructure. However, this regulation does not set incentives for efficient grid operation especially important in power systems with a limited need for grid expansion and upgrade.

Incentive-based regulation after 2009

Today, network charges in Germany are regulated using incentive-based regulation in the form of a so-called revenue cap. This solution relates to a model proposed by the former UK Treasury economist Stephen Littlechild in 1983. He criticized the lack of efficiency incentives of cost pass-through regulation and proposed the price-based regulation, which is known as RPI-X [54]. Apart from Germany, similar systems exist across Europe (e. g. the UK) and in some areas of the United States as well.

For Germany, the details of revenue cap regulation are defined in the Incentive Regulation Ordinance (ARegV). With price-based regulation, the future revenue cap is defined ex-ante for the coming regulation period (five years in Germany). Within the regulation period, the formula used to calculate the precise level of the revenue cap remains unchanged. Permissible revenues therefore follow a predetermined path during the regulation period. The revenue cap is mainly based on previous-year revenues minus the so-called RPI-X Factor. This factor consists of the retail price index (RPI) and an anticipated increase in productivity (the so-called X-Factor). The X-Factor is an important element of incentive-based regulation. It is determined individually for each grid operator. If a grid operator reaches a higher increase in productivity than anticipated by the regulator, additional cost savings need not be passed through to the consumer and thus remain as additional profit for the company. This mechanism therefore represents an incentive to improve efficiency. The disadvantage of incentive-based regulation is that cost-saving pressure may be at the expense of network investment. In Germany, with its large network investment requirements, a reform of the regulatory system to facilitate efficient investment is therefore currently being discussed.

Regulation of supply security

Network regulation relates not only to network charges but also to monitoring supply security. EnWG contains several paragraphs on this aspect. § 13 and § 14 EnWG assign responsibility for stable grid operation to transmission grid operators and distribution grid operators respectively. In urgent situations with a national relevance (for example situations of network congestions), grid operators must contact BNetzA without any delays (§ 13, section 6, EnWG). With regard to less urgent and more local situations, grid operators are obliged to issue a yearly report listing all supply interruptions within their respective grid area (§ 52 EnWG). This report must be submitted to BNetzA every year by the end of April via an internet-based process (see [55]).

The description of each supply interruption must include the time, duration, scope, and cause of the interruption. Grid operators are also obliged to describe the preventive measures taken to avoid such interruptions in the future. A document entitled Guidelines of BNetzA concerning reporting duties for supply interruptions in electric power grids according to § 52 EnWG (see [56]) specifies the information to be transmitted to the regulator.

4.4.5 Coordination of generation and consumption