Abstract

In this chapter we present nonparametric methods and available quantlets for nonlinear modelling of univariate time series. A general nonlinear time series model for an univariate stochastic process Y t T t=1 is given by the heteroskedastic nonlinear autoregressive (NAR) process

where ξ t denotes an i.i.d. noise with zero mean and unit variance and ƒ(·) and σ(·) denote the conditional mean function and conditional standard deviation with lags i 1,... ,i m , respectively. In practice, the conditional functions ƒ(·) and σ(·) as well as the number of lags m and the lags itself i 1,... ,i m are unknown and have to be estimated.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

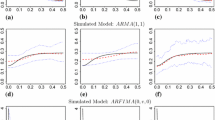

Unable to display preview. Download preview PDF.

Similar content being viewed by others

Bibliography

Auestad, B. and Tj0stheim, D. (1990). Identification of nonlinear time series: first order characterization and order determination’, Biometrika 77: 669-687.

Bera, A.K. and Jarque, CM. (1982). Model Specification Tests: a Simultaneous Approach, Journal of Econometrics, 20: 59-82.

Billingsley, P. (1968). Convergence of Probability Measures, New York: Wiley.

Brockwell, P.J. and Davis, R.A. (1991). Time Series: Theory and Methods, Springer, New York.

Doukhan, P. (1994). Mixing. Properties and Examples, Springer-Verlag, New York et al.

Fan, J. and Gijbels, I. (1995). ‘Data-driven bandwidth selection in local polynomial fitting: Variable bandwidth and spatial adaption’, Journal of the Royal Statistical Society B 57(2): 371-394.

Fan and Marron (1994). ‘Fast implementations of nonparametric curve estimators’, Journal of Computation and Graphical Statistics 3, 35 - 56.

Franke, J., Kreiss, J.-P., Mammen, E., and Neumann, M. H. (1998). ‘Properties of the nonparametric autoregressive bootstrap’, Discussion Paper 54/98, SFB 373, Humboldt University, Berlin.

Härdle, W. (1990). Applied Nonparametric Regression, Cambridge University Press: Cambridge

Härdle, W. and Tsybakov, A. (1997). ‘Local polynomial estimators of the volatility function in nonparametric autoregression’, Journal of Econometrics 81, 223-242.

Härdle, W. and Vieu, P. (1992). ‘Kernel regression smoothing of time series’, Journal of Time Series Analysis 13: 209-232.

Härdle, W., Klinke, S., and Müller, M. (2000), XploRe - The Statistical Computing Environment, Springer, New York.

Härdle, W., Lütkepohl, H., and Chen, R. (1997) ‘A review of nonparametric time series analysis’, International Statistical Review 65(1): 49-72.

Lu, Z. (1998). ‘On the geometric ergodicity of a non-linear autoregressive model with an autoregressive conditional heteroscedastic term’, Statistica Sinica 8: 1205-1217.

Robinson, P. M. (1983). ‘Non-parametric estimation for time series models’, Journal of Time Series Analysis 4: 185-208.

Silverman, B. (1986). Density estimation for Statistics and Data Analysis, Chapman and Hall, London.

Tjøstheim, D. (1994). ‘Nonlinear time-series - a selective review’, Scandinavian Journal of Statistics 21(2): 97-130.

Tjøstheim, D. and Auestad, B. (1994). ‘Nonparametric identification of nonlinear time-series - selecting significant lags’, Journal of the American Statistical Association 428: 1410-1419.

Tschernig, R. and Yang, L. (2000). ‘Nonparametric lag selection for time series’, Journal of Time Series Analysis , forthcoming.

Vieu, P. (1994). ‘Order choice in nonlinear autoregressive models’, Statistics 24: 1-22.

Yang, L., Härdle, W. and Nielsen, J.P. (1999). ‘Nonparametric autoregression with multiplicative volatility and additive mean’, Journal of Time Series Analysis 20: 579-604.

Yang, L. and Tschernig, R. (1999). ‘Multivariate bandwidth selection for local linear regression’, Journal of the Royal Statistical Society, Series B, 61, 793-815.

Yao, Q. and Tong, H. (1994). ‘On subset selection in non-parametric stochastic regression’, Statistica Sinica 4: 51-70.

Rights and permissions

Copyright information

© 2000 Springer-Verlag Berlin Heidelberg

About this chapter

Cite this chapter

Härdle, W., Tschernig, R. (2000). Flexible Time Series Analysis. In: XploRe® — Application Guide. Springer, Berlin, Heidelberg. https://doi.org/10.1007/978-3-642-57292-0_16

Download citation

DOI: https://doi.org/10.1007/978-3-642-57292-0_16

Publisher Name: Springer, Berlin, Heidelberg

Print ISBN: 978-3-540-67545-7

Online ISBN: 978-3-642-57292-0

eBook Packages: Springer Book Archive