Abstract

Companies operating on the OTC markets are a special collection of enterprises. In many countries of the European Union, different OTC markets operate, which differ among themselves in terms of number of listed companies, industry specificity of listed companies, level of capitalization of shares, etc. It is worth noting, however, that among the OTC markets operating in the so-called “new” EU countries the Polish NewConnect market stands out, which ranks higher in different rankings than many OTC markets in the so-called “old” EU countries. Taking into account the specificity of companies listed on the Polish market, empirical research was conducted on the use of ICTs by these companies. The developed case study of the Polish OTC market indicates that companies are quite used to ICTs, although the level of ICTs investments is not at the highest level. Enterprises expect measurable business benefits from the implementation of ICTs, but they understand that implementation processes are accompanied by a number of threats. The case study pointed out that the implementation of ICTs in enterprises provides the foundation for their functioning in a global economy in network structures, increasing their relationship with stakeholders and allowing access to resources.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

FormalPara The key points of the chapter are the following ones:-

1.

to specify the influence of ICTs on the contemporary enterprises;

-

2.

to identify the main attributes of the OTC markets’ enterprises in the context of ICTs and risk management;

-

3.

to understand the role and significance of enterprises of the OTC markets in the development of branches and sectors in the European Union countries;

-

4.

to identify the differences between the OTC markets in the “old” and “new” countries in the European Union;

-

5.

to specify the scope and complexity of ICTs’ implementation in enterprises listed on the Polish OCT market—as a case study.

1 Introduction

Information and Communication Technologies (ICTs) are a development platform for many companies today . They, generally, enable them to acquire resources and develop a business relationship network with other entities. ICTs, supporting knowledge management processes and innovative processes, can contribute to improving the enterprises’s competitiveness. The scale and scope of ICTs implementation is subject to the age and size of the business and the industry in which it operates. These factors influence the level of investment in ICTs as well as the level of needs and requirements of the enterprises themselves.

The main objective of this chapter is to identify the basic differences between chosen European OTC markets and specify the scope and complexity of ICTs’ implementation in enterprises listed in the Polish OCT market—as a case study and a source of potential best practices for other OTC markets in the EU. The case study aims to show whether ICTs implementation in companies gives the basis for the functioning of these enterprises in global economic conditions in network structures, enhancing their relationship with internal and external stakeholders and allowing access to external resources.

2 ICTs in Contemporary Enterprises

Nowadays Information and Communication Technologies play a key role in designing and improving the performance of businesses in various industries and sectors. ICTs can be defined as “all kinds of computer technologies (hardware and software), communication technologies, data management technologies and the relationships between these technologies that support business processes in the enterprise” (Turek 2010: 35). ICTs are becoming not only the resource (an element of technical infrastructure) but, above all, a specific “gateway key” to the global economy. In situations when market success depends not only on the structure and value of resources, but rather the flexibility in the action (mainly operational) and the relational capital, the basic determinant of the potential of the enterprise is the ability to use opportunities that appear in the environment (Wereda and Woźniak 2015: 66 et seq.; Bratnicka-Myśliwiec 2016: 40 et seq.). One of the basic ways of using the environment of an enterprise is to implement and develop certain ICTs. It is worth remembering that different types of businesses use different technologies. The basic criteria that differentiate the scale and scope of ICT implementation in enterprises are (own study on a base of Nowicki 2010: 45 et seq.):

-

size (determined by number of employees or annual turnover),

-

the core business sector as well as the level of maturity of the industry (measured, inter alia, by the level of enterprise trust and stakeholder value),

-

age and maturity of the company,

-

the internal potential of employees and the financial capacity of enterprises,

-

ICTs’ efficiency in the core business of the company,

-

technological opportunities for co-operants and co-operators,

-

the level of technological maturity of local societies and the overall level of ICT development on a global scale.

At this point it should be noted that the above criteria permeate all layers of the company’s environment: internal, closer external (market/competitive) and further external (general). This approach reflects the essence of holistic thinking and action (Fig. 1) (see e.g. in Woźniak and Zaskórski 2015: 115 et seq.; Sage and Rouse 2009: 1 et seq.). The choice of certain ICTs for specific companies, taking into account the different criteria, is most appropriate and desirable. It minimizes the risk of mismatching these technologies both to the specificity of the enterprise (as an internally integrated entity) and its relationship with the various classes of external stakeholders (based on Kaplan and Norton 2011: 13 et seq.; Orzechowski 2008: 92–99). This mismatch can be a source of different types of costs and thus may cause (especially in the long run) the need for corrective action, which may adversely affect, for example, liquidity. Risks are not only financially sound, but they can also affect the organization and execution of processes within an enterprise, e.g. in terms of ongoing communication with other entities, data collection, or analytical and decision making processes (see e.g. Borodzicz 2005: 15 et seq.; Wereda and Woźniak 2015: 66 et seq.).

Holistic approach to the implementation of the ICTs in the enterprise (own elaboration)

ICTs, spanning virtually the entire organizational system of a company, determine its efficiency, effectiveness, productivity and performance, e.g. in a human resources dimension (Rummler and Brache 2000). ICT accompanies enterprises from the stage of their design, through systematic development and ending with redesign (e.g. process reengineering) or liquidation (Sage 2009: 923 et seq.). In fact, in today’s businesses there are no processes that would not even be implicit in the implementation and development of ICTs in a given enterprise (Gonciarski 2012). Today, ICTs should create conditions for the integration (internal and external) of enterprises (Bakonyi 2017: 112 et seq.; Bratianu 2013: 109 et seq.). Incorrect implementation (not corresponding to the current needs, capabilities and requirements of the company and its external stakeholders ) of ICTs becomes the basis for the formation of formal and organizational barriers to the organization as well as the gradual alienation of the company from the dynamics of the environment (Fig. 2).

ICTs in the life cycle of the enterprise (own elaboration)

One of the basic assumptions for implementing ICTs in modern enterprises is to allow access to various resources, mainly intangible resources/assets (Hammer 2001, 2012; Sirkin et al. 2008: 85 et seq.; Surma 2008: 108 et seq.; Suszyński 2013: 175–181; Perechuda 2015: 15–18; Hadad 2017: 205 et seq.). The Internet is a specific platform for the flow of this resource class, which creates an environment for the creation of virtual structures and the free exchange of data, information and knowledge between enterprises (and not only) on a global scale (Chomiak-Orsa 2016: 48 et seq.; Sobińska 2016: 88 et seq.; Ziółkowska 2015: 231 et seq.). In this way, network organizations with high growth dynamics/changes in the global environment will be created, enabling the flexibility (see Matheson and Matheson 1998) of the network organization to grow and the use of economies of scale (through access to new resources and markets) in their individual development (Wiersema 2002). There is, among others, positive and generally strong synergy effect. Noteworthy here is the currently significant development of the sharing economy (see e.g. Nowicka 2017: 71 et seq.). ICT can also be followed by rapid internationalization of businesses, which generally positively influences their market value (see e.g. Surma 2008: 111 et seq.; Ciesielska 2008: 47 et seq.), and the value for customers (see Doligalski 2013: 55 et seq.; Gonciarski 2012: 23–25).

The implementation of ICT in modern enterprises improves, inter alia, the processes of (Zaskórski 2012: 201 et seq., 2015: 183 et seq.; Dziembek 2010: 38–44; Chomiak-Orsa 2016: 48 et seq.; Dohn et al. 2014: 4 et seq.; Pindelski and Mrówka 2014: 19 et seq.; Januszewski 2008a: 17 et seq., 2008b: 7 et seq.; Silver 2014: 11 et seq.; Lipińska 2012: 96–99):

-

data acquisition and collection,

-

data processing (e.g. aggregation, exploration, transaction, visualization),

-

forecasting, reasoning and creating knowledge,

-

enterprise information integration,

-

sharing data and information.

Today, large-scale deployments are being made in enterprise databases, as well as data and knowledge warehouses, Data Mining, and Cloud Computing (Kołodziejczyk 2015: 81 et seq.; Sobińska 2015: 93 et seq.). Integrated Management Information Systems (e.g. CRM, MRP I/II, ERP) play an important role in the improvement of enterprises (Zaskórski 2015: 187 et seq.; Adamczewski 2015: 12 et seq.). DEM class systems enable dynamic redesign of the enterprise, including towards the process structures. In the development of modern businesses, social media, mobile technologies and the Internet of things are becoming increasingly important. A separate class of information and communication technologies are tools and systems supporting design processes (e.g. CASE and CAx) and project management (Zaskórski 2015: 212–219).

ICTs, as a catalyst for management and business processes, determine the ability of a company to adapt to changes in a broadly understood environment (see Osbert-Pociecha 2011; Skrzypek 2015: 239–240; Adamczewski 2016: 62). Different types of enterprises respond differently to the implementation of ICT, and the development of these technologies is different in different organizational environments. It is worth emphasizing, however, that ICTs should be implemented on the basis of a thorough analysis of the internal and external environment, rather than merely opinions and financial possibilities (on a base of Stępniak 2010: 26 et seq.; Żeliński 2017: 7 et seq.).

3 Attributes of Enterprises on the OTC Markets: In the Context of ICTs and Risk Management

In order to specify the attributes of companies listed on alternative markets, the determinants of the functioning of these markets should first be identified. Alternative economic turnover is an Over The Counter (OTC) market which is organized by an investment firm or a company running regulated market (NewConnect 2015: 9 et seq.). In Poland, NewConnect is an example of this market, in Luxembourg it is EuroMTF, AIM and SFM in Great Britain, and Entry Standard in Germany. A list of examples of OTC markets in Europe is provided in Table 1.

On the OTC markets securities and money market instruments are traded. This system provides a concentration of supply and demand in a way that makes it possible to conclude transactions between its participants. Currently on alternative markets, in addition to FX transactions, it also trades futures for stock indices, raw materials, stocks, CFDs and other financial instruments. Alternative markets offer investors an interesting opportunity to allocate capital in a variety of innovative industries. Companies listed on alternative markets offer investors a potentially high return on their investments while at the same time increasing the risk of investment. Investors are unsure as to how the market in which companies operate will change , and whether the external effectiveness of the company’s operations (i.e., the extent to which the external stakeholders are involved) will be at the expected level (NewConnect 2015). Moreover, it is important to link the role of relationships with stakeholders in the organization to the confidence-building process between the various groups, since the level of trust decreases year by year due to the ongoing but fortunately declining economic crisis and the problems that enterprises or public entities need to be tackled with daily in a turbulent environment (Wereda 2013: 248–249; Wereda 2014: 125–126).

Companies listed on alternative markets are primarily characterized by (own preparation based on NewConnect 2015: 9 et seq.):

-

small or medium size; these are mainly start-ups or young companies, seeking effective ways to build their value on the market; however, there may be companies that already have a well-established market position but do not want to enter the main market for various reasons;

-

high growth potential and flexibility/agility as they operate in innovative industries and sectors that reflect market niches such as advanced technology, ecology, specialist services, or financial operations;

-

a desire to quickly raise capital for development , including for the improvement of the abovementioned technologies—that is basic activity, but also auxiliary activities, related to business relationship (B2B), client relationship (B2C) and state and local administration (B2A); the need to raise capital derives from a high level of capital intensity of processes (e.g. created innovations ), as well as high unpredictability of markets (competitors’ actions and customer purchasing behaviour) and the period of implementation of processes/innovations (the period of work on a particular solution/process is determined by capital).

-

difficulties in obtaining financing for development , mainly because the markets in which these companies operate are underdeveloped and the demand for products/services may not be high enough; there may also be a relatively low level of social trust (and therefore difficult to finance in the form of loans or credits offered by banks) to such activities, or the cost of capital offered by banks is too high for these companies.

Attributes of OTC-listed companies may suggest a relatively high level of risk in their business. In addition, the level of risk is also influenced by the environment (Kicia 2011: 57 et seq.). One of the basic measures in the field of risk management in enterprises is to reduce the negative impact of risk and risk avoidance (see e.g. ISO 31000:2009). This is a “traditional” approach. Based on a modern approach to risk management (inter alia in the operating activities of enterprises), the risk is controlled to create the so-called opportunity factors (Kasiewicz and Rogowski 2006: 34). The specificity of business operations in OTC markets involves interacting with external stakeholders , such as acquiring resources, streamlining information flows, or establishing new and lasting relationships—to gradually reduce uncertainty and risk in the environment.

One of the solutions designed to create this type of opportunity is the implementation of ICT. ICT is, on the one hand, a carrier of threats, but at the same time it increases the level of security of business activity in different countries. The main benefits of implementing ICT in OTC-listed companies are as follows (on a base of Zaskórski 2012; Wrycza 2010; Shapiro and Varian 2007; Larose 2006; Januszewski 2008a, b):

-

support for planning and forecasting processes—in case of instability of the environment (internal and external) and weak market position, companies can try to better understand the environment in which they operate and can anticipate changes , ahead of competitors in the innovation process (companies alone or in clusters) can create new market niches where they will dominate,

-

streamlining financial management processes and increase financial transparency, which may increase the confidence of the firm on the part of individual investors and other companies (strengthening of B2B market ties);

-

increasing the efficiency of capital allocation (e.g. by means of multi-dimensional analysis of investment profitability),

-

streamlining innovation activities, e.g. through support for manufacturing processes, R&D, analytical processes and decision making, etc.,

-

enabling businesses to enter into network structures (including virtual ones), e.g. in the form of industry clusters, enabling businesses to have access to rare resources strategically important for their development , as well as to help them enter new markets—participation in networking structures can thus also increase the credibility of the company on the market and give rise to a boost to brand value,

-

increasing scale and scope—OTC companies are typically small to medium sized, and their scale of operation is limited, e.g. to the metropolitan area, geographic region, or territorial unit or area; ICTs provide the basis for global action—the location criterion does not limit business development ,

-

increasing the efficiency of distribution channels and the promotion of products and services (including innovation) offered, thus enabling entry into new market segments and increasing liquidity both in the short and the long term.

ICTs are the basis for active shaping of the business conditions of companies listed on the OTC markets by creating and using opportunities (both inside and outside). ICT, by streamlining the analytical and decision processes, determines the condition of financial, marketing or manufacturing situation, enabling its systematic and structured development in an unstable environment. It is worth stressing here that the risk avoidance or neutralization alone cannot positively influence the competitiveness of enterprises (Kicia 2011: 66), including those listed on the OTC markets. Passive business activity on dynamic and uncertain markets is definitely not enough to succeed. It is therefore imperative to take active actions that are geared to the changing (by the possibility) of certain elements of the environment of the company, as well as the risk appetite (see e.g. Gai and Vause 2005: 6 et seq.; Danielsson et al. 2009: 3 et seq.; González-Hermosillo 2008: 6 et seq.). Conservative actions in OTC market companies will not give expected high returns to investors, and thus raising capital for development will be difficult. One of the basic solutions in this area is the relatively fast internationalization of OTC business activities with the use of ICT. The deployment and development of ICTs can increase the level of widely understood economic security (including market, financial, or social) of enterprises (see Woźniak 2013: 22 et seq.).

4 Role and Significance of Enterprises of the OTC Markets in the Development of Branches and Sectors in the European Union Countries

OTC markets play an important role in the development of individual European Union countries. Their impact on the economic development of individual countries or regions is multifaceted. It penetrates, among others, the social, financial, technological & technical, and the market development layers of these national economies by stimulating (or limiting) the activities of both individual businesses and entire societies (Fig. 3). As mentioned above, OTC markets are concentrated in small size businesses, high financial needs and weak market position, but with high potential for short-term growth (NewConnect 2015). Therefore, these companies are able to (and appropriately finance) create certain, expected values for the environment and positively influence that environment.

The potential influence of OTC markets’ enterprises on the development of branches and sectors in the EU countries—with the use of ICTs (own elaboration)

The main “tool” for developing enterprises in the OTC markets and their (positive) impact on the environment is innovation (usually a product). Assuming that companies in the OTC markets are internationalizing (or are aiming for) their activities, innovation can be spread globally, contributing directly to improving the lives of societies in different countries, or indirectly by supporting businesses that offer the goods for society. Innovation contributes to the technical and technological progress of national economies, or even to the global economy (if a case for breakthrough innovation is considered) (Niklewicz-Pijaczyńska 2013: 335 et seq.). Another example of the impact on technical and technological progress in EU countries is the creation and diffusion of know-how in OTC-listed companies. Creation of knowledge enhances the value of the enterprise itself, but it can also positively influence other companies and entire industries/sectors of national economies, e.g. by participating in clusters and other industry associations (Jankowska 2015: 54 et seq.; Pietrzykowski 2016: 161 et seq.). There are processes of knowledge transfer and mutual improvement between companies.

Technologically advanced and highly specialized clusters, such as IT, ecology, civil engineering, finance, etc., can be a strategic area for the development of national economies, determining the direction of change , e.g. in structure, time and scope of foreign direct investment, and thus inflow of capital to a given country. This is particularly true for new EU member states. OTC business activities can indirectly and in the long term determine the development of individual industries and sectors, but this depends on the efficiency and effectiveness of the financing of their business by external parties. It is also worth remembering that in the case of less developed and young OTC markets, the impact of companies listed on these markets on industries and sectors of national economies may be weak or even negligible.

OTC business activities are related to the creation of material and financial values for external stakeholders . The dynamic development of this business class may result in an accelerated flow of financial resources in the industry and clusters. Investing in business relationships, such as subcontractors, increasing financial liquidity of enterprises results in increasing the level and scope of their investments in own development with the use of external entities. This enables them to develop new specialized industries (outsourcing or offshoring services) that support existing industries such as IT, space technology, finance, bio-systems, etc. (on a base of Pauka 2010. In addition, the development of the scope and scale of business financing in OTC markets may reflect increased social trust for small and niche but innovative companies as well as developing capital markets in individual EU countries (see Pauka 2010). However, one must keep in mind that each of these markets develops at its own rate, has a different history and is dedicated to slightly different types of companies (on a base of NewConnect 2015; Feder-Sempach 2010).

In conclusion, companies listed on OTC markets may (generally indirectly) determine the level of development of specific industries and sectors in individual EU countries. This effect may be noticeable in the long run, especially in the underdeveloped OTC markets. It is important, however, that these companies, in particular due to their market, financial, technological and social potential, with the expected level of external financing, are able to change the structure and functioning of the industries and sectors in which they operate. However, these changes require time, as well as changes in the attitude of the public, including individual and institutional investors, to support this class of enterprises. OTC markets can be seen today as one of the pillars of supporting the competitiveness of national companies that are also geared towards global business.

5 Polish vs. Other European OTC Markets

The selection of OTC markets in Europe was made on the basis of the available data contained in NewConnect (2015).

In Europe, in the OTC market dominates the London AIM, which has both the largest number of listed companies (Fig. 4) and capitalization (Fig. 5). It is worth adding, however, that this market functions much longer than its European counterparts—it was created in 1995.Footnote 1 According to data for 2014Footnote 2 in terms of the number of listed companies on the OTC market behind the London market are the following: Warsaw NewConnect, NYSE Euronext (Alternext) (established by stock exchanges in the Netherlands, Portugal, France and Great Britain), German Entry Standard, Luxembourg market EuroMTF, the NASDAQ OMX (First North) market (set up by stock exchanges in Sweden, Denmark, Finland and Iceland), the Turkish Borsa market in Istanbul, the Slovakian market, the Italian AIM market, and the Norwegian Oslo Axess market. The following markets are in the following locations: Spanish, Irish, Hungarian, Austrian, Cypriot and Greek (NewConnect 2015: 10).

Number of companies listed on chosen European OTC markets—state at the end of the year 2014. (Author’s own figure based on data from NewConnect 2015: 10)

Capitalization of shares for chosen European OTC markets—state at the end of the year 2014. (Author’s own figure based on data from NewConnect 2015: 10)

Taking into account the capitalization criterion, the London AIM market ranks first in Europe at the end of 2014. The Irish, German, NYSE Euronext (Alternext), Turkish, NASDAQ OMX (First North), Austrian, Italian, Polish, Norwegian and Spanish markets followed. The smallest shares capitalization of the analyzed markets is found in the markets of Cyprus, Luxembourg and Slovakia (Fig. 5) (NewConnect 2015: 10).

The analyzed markets (including data at the end of 2014) can be divided into four main groups (Fig. 8) (own preparation based on NewConnect 2015: 10):

-

1.

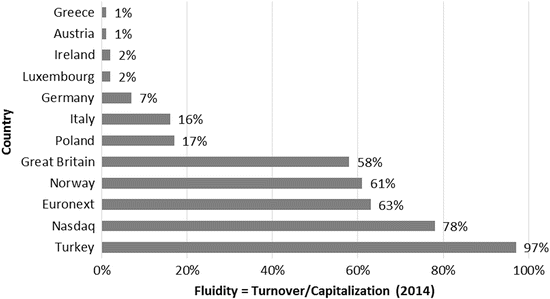

having a high level of capitalization of shares and, at the same time, a relatively large number of listed companies—this market includes Great Britain and German markets; These are the most developed markets with a relatively long history and reputation; It is also worth noting that these markets are also characterized by relatively high shares turnover (for the London market it amounts to 53,170 million EUR and for the German market 2373 million EUR) and relatively high liquidityFootnote 3 (for the London market the liquidity was 58%, while for the German market it was much less—just 7%) (Figs. 6 and 7);

Fig. 6

Shares turnover for chosen European OTC markets—state at the end of the year 2014. (Author’s own figure based on data from NewConnect 2015: 11)

Fig. 7

Fluidity for chosen European OTC markets—state at the end of the year 2014. (Author’s own figure based on data from NewConnect 2015: 11)

-

2.

with a high level of capitalization of shares and at the same time relatively small number of listed companies—this group includes the Irish market, which is characterized by high value of listed companies, but small in size, which may result from restrictions on entering the market or insufficient willingness of enterprises to enter it; The market is also characterized by a relatively high shares turnover (EUR 1047 million), while low liquidity (2%) (Figs. 6 and 7);

-

3.

with low capitalization of shares and relatively large number of listed companies—Polish, NYSE Euronext (Alternext), Luxembourg, NASDAQ OMX (First North) and Turkish; These markets are mainly concentrated in companies with relatively low market value, although companies are willing to enter these markets, mainly because of their reputation and the potential for potential value growth; They are also not markets with a long history and a well-established position on the capital markets; Among these markets, two fractions are distinguished: (1) very high liquidity markets and at the same time very high turnover—Turkish, NYSE Euronext (Alternext) and NASDAQ OMX, as well as (2) medium liquidity and shares turnover values—these are the Polish and Luxembourg markets (Figs. 6 and 7);

-

4.

with low capitalization of shares and at the same time relatively small number of listed companies—it is in fact the largest group, with the following markets: Italian, Slovak, Norwegian, Spanish, Austrian, Greek and Cypriot; These are, for the most part, young markets that are just beginning to develop; As a consequence, companies are not keen to enter these markets, mainly because of the risk (e.g. market) and the absence of potential benefits from participating in these markets; It is also worth mentioning that these are markets established in countries with relatively small populations in Europe, which may also result in the population of micro, small and medium-sized enterprises potentially entering these markets. Among these markets one can distinguish two fractions: (1) markets with relatively high or medium liquidity and at the same time relatively high or medium level of shares turnover—these are Norwegian, Italian and Austrian markets, and (2) very low liquidity and very low shares turnover values—these are markets: Greek, Spanish, Slovak and Cypriot (Figs. 6 and 7).

Summary of the number of companies listed on the chosen European OTC markets and capitalization of shares for these markets—state at the end of the year 2014. (Author’s own figure based on data from NewConnect 2015: 10)

By setting the criteria for the number of listed companies and shares capitalization at the end of 2014, it can be seen that (Fig. 8):

-

the London market is well above the other European markets, both in terms of the number of listed companies (the number of listed companies on the London market is over two and a half times the number of listed companies on the second Polish market) and capitalization (almost twice the London market capitalization exceeds capitalization of shares on the second Irish market);

-

the Polish market, despite the relatively low capitalization is characterized by exceptionally high number of listed companies, which may prove very attractive for micro, small and medium enterprises (also those of low market value). This situation also arises from the profile of this market—it is dedicated mainly to micro-companies on a European scale; Moreover, the nature of the NewConnect market is related to the specificity of the Polish economy, where micro-enterprises dominate (NewConnect 2015: 10);

-

the existence of three specific clusters in a group with relatively low capitalization of the stock market: (1) a relatively large number of listed companies (NYSE Euronext, Luxembourg, NASDAQ OMX), (2) the medium number of listed companies (markets: Turkish, Italian, Slovak), and (3) a small number of listed companies (Norwegian, Spanish, Austrian, Greek and Cypriot markets).

From 2007 to 2014, the number of listed companies was clearly dominated by the London AIM (Fig. 9). However, it can be noted that since 2007 the number of listed companies on this market has steadily decreased. In 2014, the first increase since 2007 was observed (from 1087 companies in 2013 to 1104 in 2014) (NewConnect 2015: 10). Among the other markets (operating in the so-called “old” EU countries) two basic fractions can be distinguished (Fig. 10) (NewConnect 2015: 10):

-

1.

markets with relatively large number of listed companies—Luxembourg, NYSE Euronext, NASDAQ OMX and German; It can be observed here that the German, NYSE Euronext and NASDAQ OMX markets experienced a rising trend (in some generalizations), while the Luxembourg market from 2012 marked a sharp decline in the number of listed companies; It is also worth mentioning that all four markets in this faction were characterized by a downward trend or a stagnation in the number of IPOs;

-

2.

markets with a relatively small number of listed companies—these are Spanish, Greek, Italian, Austrian and Irish markets; In this segment, the upward trend in the number of listed companies occurred only in the Italian and Spanish markets, while in the Greek, Irish and Austrian markets there was a downward trend; As regards the number of IPOs, the Italian market has been systematically growing and the Spanish market has been stagnating; On the Irish and Austrian markets, the number of IPOs has been at a very low level in recent years (there are only one or two new entrants in the market).

Number of companies listed on the chosen European OTC markets (operating in the “old” EU countries) in the years 2007–2014. (Author’s own figure based on data from NewConnect 2015: 10)

Number of companies listed on the chosen European OTC markets (operating in the “old” EU countries) without Great Britain in the years 2007–2014. (Author’s own figure based on data from NewConnect 2015: 10)

Among the OTC markets operating in the years 2007–2014 in the “new” EU countries, the distinctive position of the Polish market in terms of number of listed companies can be noted (Fig. 11). The other three markets (Slovakia, Hungary and Cyprus) were significantly less listed during the period considered. It is also worth noting that the dynamics of growth of the number of companies on the Polish market was the highest, and the number of IPOs in 2007–2014 was at a relatively high level, reaching in 2011 a maximum of 172 debuting companies. Outside the Polish market, only the Cypriot market was able to observe an upward trend in the number of listed companies. On the other hand, there were no significant changes in the number of listed companies in the Slovak and Hungarian markets (NewConnect 2015: 10).

Number of companies listed on the chosen European OTC markets (operating in the “new” EU countries) in the years 2007–2014. (Author’s own figure based on data from NewConnect 2015: 10)

Comparing the Polish NewConnect market to the leading markets in the so-called “old” European Union countries, it can be seen that in the years 2007–2014 it was the Polish market which was characterized by the highest dynamics of growth of the number of listed companies and was the only one with a strong upward trend in the number of companies listed (Fig. 12). It is also worth noting that in the case of the number of IPOs, the Polish market in the period under consideration also distinguished itself, ahead of such markets as Germany, Luxembourg, NYSE Euronext and NASDAQ OMX. On the other hand, in terms of IPO value, the Polish market was not as good in each analyzed period taking the sixth place (i.e. the last one in the selected markets) (NewConnect 2015: 10).

Polish vs. leading OTC markets from “old” EU countries in the framework of the criterion of number of listed companies in the years 2007–2014. (Author’s own figure based on data from NewConnect 2015: 10)

In summary, it is important to note that the OTC markets in the “old” EU countries perform better than the markets in the “new” EU Member States—except for the NewConnect market, which is low in the IPO only. Among the “old” EU countries are the leading markets in Great Britain, Germany and Luxembourg, as well as markets NYSE Euronext and NASDAQ OMX. They are attractive to investors and companies themselves as they have been operating for many years, have a strong reputation and guarantee a return on their investment. This is reflected in both the capitalization of companies, shares turnover values and liquidity. The less developed markets among the “old” EU countries are the Italian, Austrian, Greek and Spanish markets. These markets have similar results to markets in the “new” EU (excluding the Polish market), i.e. the Slovak, Hungarian and Cypriot markets. It is worth remembering that these are young markets which are only in the early stages of development and whose origins were in the years of the recent financial crisis (or soon after).

6 ICTs in the Enterprises on Polish NewConnect Market

6.1 Research Methodology

The specificity of the Polish market, as well as the availability of data and the proximity of businesses, have made NewConnect the chosen market for empirical research and a case study. The case study aims to indicate to what extent and to what scale companies listed on the Polish OTC market use ICTs and what benefits they expect after implementation and what threat they perceive in these processes.

The specification of the research methodology is presented in Table 2.

6.2 Characteristics of the Research Sample

The age distribution of the studied companies is not normal—it is right-angled. There is a predominance of companies below the middle age, i.e. 14.5 years of operation on the market. Most of young companies (up to 10 years old) operate in the following industries: trade, information technology, financial services, as well as advice and training. One company operating in the eco-energy sector can also be identified here. Older businesses are involved in the media, recycling, industrial processing, and building & construction. The greatest variation in the age of enterprises occurs in the sectors of: building & construction, computer science, as well as advice and training.

Most of small businesses (10–49 employees) operate in the fields of computer science, trade, financial services, and building & construction. Most of medium-sized companies (50–249 employees) operate in the following industries: industrial processing, and trade. On the other hand, a large company (the only one that went to the research trial) is in the recycling business. In general, most of the surveyed companies operate in the sectors of trade, computer science, industrial processing, building & construction, and financial services (Table 3).

Among small enterprises, “young” entities dominate (4–9 years of activity on the market) and some “older” (10–15 years of activity on the market). In this business class, there are the few “old” companies (over 25 years of activity on the market). Midsize companies are dominated by older companies (between 10 and 24 years old). There are relatively few “young” enterprises here (4–9 years of activity on the market). In the large enterprise class, only one entity is classified as “old” (over 25 years) (Table 4).

The “young” companies (from 4 to 9 years on the market) are principally engaged in computer science (five indications) and trade (four indications). In addition, companies in this age group are involved in financial services (three indications), building & construction (two indications) and eco-energy, and advice and training (one indication). The “older” companies, i.e. between 10 and 24 years of activity in the market, are mainly active in the area of industrial processing (ten indications) and trade (seven indications). On the other hand, the smallest enterprises in this age class are computer science (four indications) and building & construction (three indications). Companies that operate at least 25 years are dominated by building & construction (three indications) (Table 5).

All studied companies operate on the scales of: national (9–16 voivodships in Poland) and regional (1–8 voivodships in Poland). On the local scale (one city/municipality/district) there are 58 companies. It can therefore be assumed that 58 companies operate both locally and regionally and nationally. Only 25 companies operate on the European scale (at least one country in Europe outside Poland) and 5 companies on the international scale (at least one country in the world outside Europe, including outside Poland). This may indicate that the surveyed enterprises are still at a low level of internationalization of the activity (Table 6).

Among local, regional and national companies dominate the “young” (4–15 years of activity)—more than half of the enterprises in each of the three classes mentioned in the scale of their activity. Among companies operating from the local to the European level, the “old” companies i.e. over 25 years of activity on the market are the smallest group. On the other hand, there are companies that are internationally active, both “very young” (4–9 years old) and somewhat “mature” in the market (16–24 years) (Table 6).

Regardless of the scale of operations, small businesses dominate in each of the five classes (local, regional, national, European and international). The smallest disproportions between the share of small and medium enterprises are in the case of European and international scale (Table 7).

Of the companies operating on a local, regional and national scale, the largest number of companies are involved in trade, computer science and industrial processing (11 indications). A significant group of the companies deals with building & construction, financial services, as well as advice and training (7–8 indications). Least enterprises operate in media and recycling (1–2 indications). Among companies operating on a European scale industrial processing dominates (11 indications). Moreover, on a European scale, there are five computer science companies, three companies in each other branch: building & construction and trade, as well as two companies in financial services, and one in media branch. On the other hand, the companies dealing with computer science dominate in the international scale, while one company deals with industrial processing (Table 8).

6.3 Results of the Research

Over the past 5 years, the studied companies have implemented ICTs in the following areas: data storage and processing (49 indications), creation and sharing of knowledge to employees and partners (46 indications), acquisition of key business data (46 indications), planning, forecasting and scheduling of processes (35 indications), as well as construction of IT technical infrastructure (32 indicators), customer service (31 indications) and business relationships (30 indications). Least ICT deployment has been reported in the field of on-site communication (8 indications) (Fig. 13).

ICT deployment areas in the surveyed enterprises in the last 5 years. (Own elaboration; N = 60; multiple choice question)

The most commonly reported respondents’ benefits to businesses stemming from the use of ICTs include: increased revenue (56 indications), increased customer base or increased market share (55 indications), increased flexibility (54 indicators), as well as the increase in business innovation (42 indications) and improvement of administrative processes (41 indications). In turn, the least often indicated benefits are: reduction of excessive IT infrastructure (4 indications), development of incomplete IT infrastructure (5 indications) and improvement of communication in the enterprise (10 indications) (Fig. 14).

Basic business benefits of using ICTs. (Own elaboration; N = 60; multiple choice question)

Least, i.e. less than 23,631 EUR (i.e. 100,000 PLNFootnote 4) on average per year, for the maintenance and development of information and communication technology is mainly spent on “old” companies, i.e. over 10 years of operation on the market. The average age of enterprises in this cost bracket is over 15 years. A similar situation occurs in the case of expenditure in the range 23,632–70,893 EUR (i.e. 101,000–300,000 PLN). In this case, the average age of enterprises is also over 15 years. For a cost level below 70,893 EUR (i.e. 300,000 PLN) there is a large dispersion of the age of enterprises—both very young and old. In the range of expenditure on maintenance and development of information and communication technologies at the level of 70,894–118,156 EUR (i.e. 301,000–500,000 PLN), “relatively young” companies dominate. The dispersion of the age of enterprises in this compartment is small (except for one enterprise). In the expenditure range of 118,157–165,418 EUR (i.e. 501,000–700,000 PLN) there is only one “young” company. In general it can be observed that the younger the company, the greater the cost of maintaining and developing ICTs.

Most of the companies surveyed bear the costs of maintenance and development of ICTs at the level of 23,632–70,893 EUR (i.e. 101,000–300,000 PLN) (41 indications). There are both “young” and “old” companies in this range. In 11 companies, costs are below 23,631 EUR (i.e. 100,000 PLN). Over 70,894 EUR (i.e. 300,000 PLN) is listed by 8 companies (Fig. 15).

Average yearly cost of living and development of ICT in the company over the last 5 years. (Own elaboration; N = 60)

In the group of companies, which bear the costs of maintenance and development of ICT at less than 23,631 EUR (i.e. 100,000 PLN), the largest group is small enterprises (10 indications). In the cost range 23,632–70,893 EUR (i.e. 101,000–300,000 PLN) also dominates a group of small companies (26 indications), although medium-sized companies (15 indications) are also significant. In the range 70,894–118.156 EUR (i.e. 301,000–700,000 PLN) medium companies (6 indications) predominate.

The most important criteria for selecting ICTs in the opinion of the surveyed companies are: the ability to update the technology (54 indicators), the provision of IT infrastructure by the supplier (48 indications), the popularity of technology in the branch (39 indications). The least important criteria are: low cost of implementation (11 indications) and low maintenance and development costs (16 indications). For respondents, the technology provider’s prestige (19 indications) is also relatively small criterion (Fig. 16).

Key criteria for choosing ICT in the surveyed enterprises. (Own elaboration; N = 60; multiple choice question)

The basic and most important threats resulting from the use of ICTs are: rapid technological downturn (53 indications), cost increases (52 indications), and difficulty in handling/using technology by employees and managers (41 indications). The least important threats are, in turn, too many functions (1 indication) and too much reduction in IT infrastructure in the enterprise (2 indications) (Fig. 17).

Threats arising from the use of ICTs. (Own elaboration; N = 60; multiple choice question)

All of the companies surveyed use ICTs to interact with various groups of internal stakeholders , such as specific teams of employees, internal departments or individual organizational units, or management staff, etc. ICT is used by 57 companies in contacts with external stakeholders, by 51 companies to contact with media organizations. It is also worth mentioning that five of the surveyed companies use ICT to establish and maintain relationships with various public administrations (Fig. 18).

Stakeholder groups with which companies enter into relationships with the use of ICTs. (Own elaboration; N = 60; multiple choice question)

6.4 Discussion and Conclusions

The surveyed companies differ in terms of age, scale and leading business profile, as well as size (based on the number of employees). The least numerous is the group of large companies, however, this is due to the specificity of the NewConnect market, which is dedicated to small and medium enterprises. The “young” companies (up to 15 years of activity on the market) also dominate. Research sample companies are predominantly engaged in activities that operate on a national scale, fewer are European or international actors. However, there is a slight tendency for the gradual internationalization of these entities—with the prolongation of their activity on the market. This is the most desirable situation, as it demonstrates the development of companies listed on the NewConnect market. Most of the surveyed companies operate in trade, industrial processing and computer science. However, it is worth noting that among the companies with the largest scale of activity and at the same time “the youngest” computer science dominates, which is one of the basic profiles of innovative enterprises. In addition, in the “older” and medium-sized enterprises less innovative core business profiles predominate than in “young” and small enterprises.

According to presented research results it can be noted, first of all, that companies do not appreciate the scale of ICT deployment or the problems they face. More problems with new technologies have “old” companies. This situation may be a reflection of the fact that these companies are still at a low level of internationalization. The larger the scale, the greater share of the “older” companies. It need to be noted, however, that relatively a lot of the “young” companies operate in a different way, immediately set up another (larger) scale of activity. The “young” companies spend more on ICTs, are more flexible and innovative. Less interest of enterprises (mainly the “older” ones) in the large number of ICT functions is due to lack of knowledge and concerns on the part of users—companies do not know how to use it (hence the service and training are so important). Less interest in ICTs is driven by the desire to reduce the risk of unprofitable solutions/investments (choosing popular solutions, a reputable provider) and less financial opportunities, experience—hence the interest in providing infrastructure, training, etc.

The main areas of ICT deployment in the surveyed companies are data acquisition from internal and external sources as well as data processing. These are the foundations for knowledge management processes, which are rather the standard used in every enterprise, resulting from the need to conduct market analysis (competitors and cooperatives) and to perform planning functions. On the other hand, the more “advanced” areas of business operations and related complex processes are no longer of great interest in ICT implementation. Examples include, among others, customer support, administrative process support, promotional activities, or reporting and analysis/evaluation of business. It is quite important for businesses to use ICT to build business relationships.

Concentration mainly on data processing, knowledge management and relationships with external parties is to some extent expected by companies for the benefits of ICT implementation. The basic expected benefits are revenue growth, increased flexibility of the enterprise, strengthening of business processes, or increase of innovativeness. It is worth emphasizing, however, that relatively small capital expenditures and a focus on data management may not be sufficient to achieve the expected results of ICT implementation in the short term. Then there may be some kind of dissonance and disappointment with the implementation measures taken and the involvement of business owners/managers in the further development of ICT in the enterprise. In order to achieve tangible business benefits, especially in companies operating in competitive and innovative industries (even micro, small and medium enterprises), it is necessary to continually invest in IT infrastructure (i.e., technical infrastructure), as it is constantly changes , offering new functionality to users. Suspending ICT investment may even lead to IT and information exclusion in the long term, which may also limit its potential to enter into business relationships (e.g. network/virtual infrastructure) and hinder access to resources (reducing the company’s innovation potential). This is especially important for micro, small and medium enterprises that do not have sufficiently large financial resources to acquire other resources themselves or create innovations (e.g. innovative networks of companies responsible for creating and developing open innovation).

Targeting the surveyed enterprises to increase operational flexibility (understood as, inter alia, the ability to respond quickly to changes within the organization and the environment, and to the efficiency of information and decision processes) is reflected in the structure of the criteria to be followed in selecting ICT companies. Owners/managers are primarily concerned with the ability to rapidly upgrade technology, provide IT infrastructure, additional services, and a large number of features and the ability to integrate technology with third parties. It also welcomes the fact that entrepreneurs are not guided primarily by the costs of acquiring, implementing and developing ICT. However, such an approach may also be of concern, mainly because the surveyed companies point out that the level of ICT investment is not high. Therefore, ICT costs must be taken into account in order to ensure that, for example, the IT budget in an enterprise (if developed) is respected. In addition, most of the surveyed companies operate in innovative and capital-intensive industries, where dedicated IT solutions are not cheap and can pose a serious burden on the company’s budget. Examples may be found in industry: computer science, industrial processing, or financial services. The low importance of the ICT cost criterion may also indicate that these technologies are not being implemented in core business processes, or are not advanced and essential technologies but rather basic, ad hoc tools such as communications applications, spreadsheets or databases. However, it must be borne in mind that the impact of this type of technology on the level of innovation and thus the competitiveness of enterprises (especially those listed on the NewConnect market) can be indirect and insignificant. So, the question is whether it is worth investing in such “small” and “ad hoc” IT solutions?

The above-mentioned situation is very likely because it is confirmed by respondents’ responses to the basic threats that may be associated with the implementation of ICT in enterprises. The main threats in the opinion of respondents include: rapid technology update, cost increase and difficulty in handling and using technology by employees and managers. Perhaps owners/managers, in an effort to reduce the risk of unprofitable ICT investments, are investing in cheaper and temporary—and therefore more “safe” in the short term—solutions with less analytical and decision-making potential, thus offering less contribution to value creation for internal and external stakeholders . However, taking into account the age of the surveyed companies, this is a rather normal situation, as the “young” players are dominant in the sample, which do not yet have a solid network of external relations and a well-developed IT infrastructure and are constantly searching for new and “best” solutions (calculating the cost of investing in ICT).

Researched companies are quite willing and on a large scale use ICT to create and maintain relationships with external stakeholders —although this should be viewed rather as “intentions” of enterprises rather than the present state. This is, however, a positive situation, indicating the ability (or willingness) of the surveyed companies to create and maintain relationships with external parties, giving rise to, for example, access to network structures (distributed information and geographically dispersed). It is worth recalling, however, that these companies are primarily interested in acquiring and processing data from the environment, and are less likely to focus on providing their own information resources. This approach to networking is not appropriate because it can be inconsistent with the overriding purpose of the entire network. The use of ICTs within enterprises can also be beneficial, inter alia, in the area of streamlining information and decision processes and knowledge management processes. One should keep in mind the aforementioned continuity in financing the development of ICT in enterprises as well as successively increasing the functionality of the ICTs used.

Questions and Activities

-

1.

What are the basic functions of ICTs in managing contemporary enterprises ?

-

2.

What are the basic attributes of companies listed on OTC markets? What are these attributes?

-

3.

How can ICTs influence on the development of OTC-listed enterprises as well on the development of individual industries and sectors in the EU?

-

4.

What are the basic threats associated with the implementation of ICTs in enterprises listed on OTC markets in the EU? Are the hazards in each EU country (i.e. on each national OTC market) the same? If YES/NO, what does it depend on?

-

5.

Why different OTC markets in the EU have different financial results? Does the different level of development of OTC markets in the EU affects the scale, scope and complexity of implementing ICTs in enterprises listed in these markets?

-

6.

Why does the British OTC market differentiate from other European OTC markets?

-

7.

What impact on the virtualisation and internationalization of OTC-listed businesses may have on the implementation of ICTs in these enterprises?

-

8.

How can the enterprise’s age and scale of operations influence the scope and complexity of implementing ICTs in OTC-listed companies? What is the significance of the criterion of cost of acquisition, implementation and improvement of ICTs?

-

9.

Try to develop 4-5 good practices for companies listed on the European OTC markets (e.g. for the Slovak, Greek, Cypriot and Hungarian markets) in the field of ICTs implementation—based on the example of a case study of the Polish market.

Notes

- 1.

Since October 2004 it has been operating as MTF market.

- 2.

The analysis includes 2014 due to the availability of data.

- 3.

Calculated as the quotient of shares turnover on the market to the capitalization of shares.

- 4.

All conversions from PLN to EUR were made due to the EUR exchange rate of the day 28.06.2017—according to the National Bank of Poland; 1 EUR = 42,317 PLN.

References

Adamczewski P (2015) ICT-aided of smart organization in Polish SME. Nierówności Społeczne a Wzrost Gospodarczy 44(4 part 1):7–21

Adamczewski P (2016) Knowledge management in modern organisation based on 3rd platform ICT systems. Torun Bus Rev 15(4):61–68

Bakonyi J (2017) Digital competences in the ımplementation of the concept of dynamic capabilities. Studia i Prace WNEIZ US 48(3):107–117

Borodzicz EP (2005) Risk, crisis & security management. Wiley, Chichester

Bratianu C (2013) The triple helix of the organizational knowledge. Manag Dyn Knowl Econ 1(2):207–220

Bratnicka-Myśliwiec K (2016) The impact of information technology on the dynamics of the creative entrepreneurial organization. e-mentor 5(67):40–45

Chomiak-Orsa I (2016) The ımportance of modern ICT in improving intra-organisational communication. Informatyka Ekonomiczna. Bus Informatics 1(39):46–55

Ciesielska D (2008) The effect of ınformation and knowledge on value based management. In: Herman A, Szablewski A (eds) Value creation in the era of service economy. Warsaw School of Economics Publishing House, Warsaw, pp 47–63

Danielsson J, Shin HS, Zigrand J-P (2009) Risk appetite and endogenous risk. http://www.lse.ac.uk/fmg/researchProgrammes/paulWoolleyCentre/pdf/second%20Confernc%20Papers/Zigrand.pdf. Accessed 20 Apr 2017

Dohn K, Gumiński A, Matusek M, Zoleński W (2014) IT tools ımplemented in the ınformation system supporting management in the range of knowledge management in mechanical engineering enterprises. Inf Syst Manag 3(1):3–15

Doligalski T (2013) Internet in the management of customer value. Warsaw School of Economics Publishing House, Warsaw

Dziembek D (2010) The objectives of the use of information technologies. In: Nowicki A, Turek T (eds) Information technologies for economists. Tools. Applications. Publishing House of Wrocław University of Economics, Wrocław, pp 38–44

Feder-Sempach E (2010) Alternative markets in the Euro Zone and the European Union vs. NewConnect – comparative analysis. Acta Universitatis Lodziensis. Folia Oeconomica 238:35–45

Gai P, Vause N (2005) Measuring investors’ risk appetite. Bank of England Working Paper Series No. 283. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=872695. Accessed 4 May 2017

Gonciarski W (2012) Management challenges in the era of digital technology. In: Sołek C (ed) Management dilemmas in the information technology era. Military University of Technology, Warsaw, pp 11–36

González-Hermosillo B (2008) Investors risk appetite and global financial market conditions. IMF Working Paper No. 08/85. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1119425. Accessed 12 June 2017

Hadad S (2017) Knowledge economy: characteristics and dimensions. Manag Dyn Knowl Econ 5(2):203–225

Hamel G (2012) What matters now. How to win in a world of relentless change, ferocious competition, and unstoppable ınnovation. Jossey-Bass, San Francisco, CA

Hammer M (2001) The agenda. What every business must do to dominate the decade. Three Rivers Press, New York, NY

Jankowska B (2015) Cluster organization as a pro-ınternationalization form of cooperation in the SME sector – a Polish case in the European context. J Econ Manag Univ Econ Katowice 22:54–74

Januszewski A (2008a) The functionality of the information management systems. Part 1. Integrated transactional systems. Wydawnictwo Naukowe PWN, Warsaw

Januszewski A (2008b) The functionality of the information management systems. Part 2. Business intelligence systems. Wydawnictwo Naukowe PWN, Warsaw

Kaplan RS, Norton DP (2011) Alignment: using the balanced scorecard to create corporate synergies. Gdańskie Wydawnictwo Psychologiczne, Sopot

Kasiewicz S, Rogowski W (2006) Risk and growth in company value. Kwartalnik Nauk o Przedsiębiorstwie 1:34–41

Kicia M (2011) Risk management – a key competence of contemporary enterprise. In: Kurkliński L (ed) Risk management – reactions and challenges after the crisis. Biuro Informacji Kredytowej S.A, Warsaw, pp 54–67

Kołodziejczyk A (2015) Technology megatrends in network business models. In: Perechuda K (ed) Advanced business models. Publishing House of Wrocław University of Economics, Wrocław, pp 81–92

Larose DT (2006) Discovering knowledge in data. An introduction to DATA MINING. Wydawnictwo Naukowe PWN, Warsaw

Lipińska A (2012) Knowledge management of companies in the information society. Theory and practice. In: Sołek C (ed) Management dilemmas in the ınformation technology era. Military University of Technology, Warsaw, pp 93–100

Matheson D, Matheson J (1998) The smart organization. Harvard Business School Press, Boston, MA

NewConnect (2015) Raport o rynku NewConnect 2015. Podsumowanie funkcjonowania pierwszej alternatywnej platformy obrotu w Polsce. Giełda Papierów Wartościowych w Warszawie. https://www.gpw.pl/pub/files/PDF/2015-05-25_NEWCONNECTraport2015.PDF. Accessed 15 May 2017

Niklewicz-Pijaczyńska M (2013) Breakthrough ınnovations in open ınnovation model and free revealing economics. J Manag Finance 11(4 part 3):335–351

Nowicka K (2017) Cloud computing – a sine qua non condition for sharing economy. In: Poniatowska-Jaksch M, Sobiecki R (eds) Sharing economy. Warsaw School of Economics Press, Warsaw, pp 69–88

Nowicki, A. (2010). Identification of information technologies. In: A. Nowicki, & T. Turek (Eds.), Information technologies for economists. Tools. Applications (pp. 44-58). Wrocław: Publishing House of Wrocław University of Economics.

Orzechowski R (2008) Effective IT management and IT governance. In: Herman A, Szablewski A (eds) Value creation in the era of service economy. Warsaw School of Economics Publishing House, Warsaw, pp 85–106

Osbert-Pociecha G (2011) The process of organizational learning as a way to uncertainty. Master Bus Admin 3(110):49–62

Pauka M (2010) Alternative investment market in Poland. Acta Universitatis Lodziensis. Folia Oeconomica 233:317–326

Perechuda K (2015) Advanced business models – fundamental dimensions: corporate architecture, space, invisibility. In: Perechuda K (ed) Advanced business models. Publishing House of Wrocław University of Economics, Wrocław, pp 11–18

Pietrzykowski M (2016) Strengthening the internationalisation and commercialization of clusters and cluster organisations by upgrading managerial competencies: selected cases from Poland and Lithuania. Studia Oeconomica Posnaniensia 4(5):160–183

Pindelski M, Mrówka R (2014) Big data visualizations in the identification of management problems. Research Papers of Wrocław University of Economics. Manag Forum 5(363):18–28

Rummler GA, Brache AP (2000) Improving performance. How to manage the white space on the organization chart. Polskie Wydawnictwo Ekonomiczne, Warsaw

Sage, A.P. (2009). Systems reengineering. In: A.P. Sage, & W.B. Rouse (Eds.), Handbook of systems engineering and management (pp. 923-1026). Hoboken, NJ: Wiley

Sage AP, Rouse WB (2009) An ıntroduction to systems engineering and systems management. In: Sage AP, Rouse WB (eds) Handbook of systems engineering and management. Wiley, Hoboken, NJ, pp 1–63

Shapiro C, Varian HR (2007) Information rules: a strategic guide to the network economy. Helion, Gliwice

Silver N (2014) The signal and the noise: why so many predictions fail – but some don’t. Helion, Gliwice

Sirkin HL, Hemerling JW, Bhattacharya AK (2008) Globality. Competing with everyone from everywhere for everything. Headline Publishing Group, London

Skrzypek E (2015) The place of e-learning in knowledge management. Nierówności Społeczne a Wzrost Gospodarczy 44(4 part 2):239–251

Sobińska M (2015) IT management business model – sourcing IT services. In: Perechuda K (ed) Advanced business models. Publishing House of Wrocław University of Economics, Wrocław, pp 93–104

Sobińska M (2016) Cloud computing vs. knowledge management – challenges, opportunities and threats. Informatyka Ekonomiczna. Bus Informatics 1(39):83–97

Stępniak C (2010) The company as an object of applications of information technologies. In: Nowicki A, Turek T (eds) Information technologies for economists. Tools. Applications. Publishing House of Wrocław University of Economics, Wrocław, pp 17–31

Surma J (2008) Supporting value based management by business ıntelligence. In: Herman A, Szablewski A (eds) Value creation in the era of service economy. Warsaw School of Economics Publishing House, Warsaw, pp 107–117

Suszyński C (2013) Business enterprise: the ıntegration of approaches. Theoretical dilemmas vs. challenges of practice. Warsaw School of Economics Press, Warsaw

Turek T (2010) The concept of information technology. In: Nowicki A, Turek T (eds) Information technologies for economists. Tools. Applications. Publishing House of Wrocław University of Economics, Wrocław, pp 32–38

Wereda W (2013) Value creation and stakeholders in the model of the intelligent municipality – theoretical perspective. Journal Przedsiębiorczość i Zarządzanie SAN in Lodz 13(part II):243–257

Wereda W (2014) The nature of stakeholders in changing environment of the organizations. In: Domańska Szaruga B, Stefaniuk T (eds) Organization in changing environment. Conditions, methods and management practices. Publishing House Studio Emka, Warsaw, pp 117–126

Wereda W, Woźniak J (2015) Risk criterion in the “agile” organization. Modern Manag Syst 10:61–87

Wiersema F (2002) The new market leaders. Who’s winning and how in the battle for customers. Simon & Schuster UK, London

Woźniak J (2013) Intrapreneurial activities as a determinant of economic security of business organizations – specification of ciricumstances and dependences. Modern Manag Syst 8:21–36

Woźniak J, Zaskórski P (2015) System aspects of designing and improving an organization and shaping its security. In: Woźniak J (ed) Designing and improving an organization in terms of its security and improving the information and decision-making processes. Military University of Technology, Warsaw, pp 99–154

Wrycza S (ed) (2010) Economic informatics. Polskie Wydawnictwo Ekonomiczne, Warsaw

Zaskórski P (2012) Information asymmetry in the process management. Military University of Technology, Warsaw

Zaskórski P (2015) Management information systems as an environment of designing and improving an organization. In: Woźniak J (ed) Designing and improving an organization in terms of its security and improving the ınformation and decision-making processes. Military University of Technology, Warsaw, pp 183–223

Żeliński J (2017) Business analysis. Practical organization modeling. Helion, Gliwice

Ziółkowska B (2015) Benefits of virtual business and enterprises in Poland. Zeszyty Naukowe Politechniki Śląskiej Seria: Organizacja i Zarządzanie 86:231–240

Zygmanowski P (2014) Rynek NewConnect i jego europejskie odpowiedniki. http://www.ncbiuletyn.pl/czytaj/1761-rynek-newconnect-i-jego-europejskie-odpowiedniki.html. Accessed 10 May 2017

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 Springer International Publishing AG, part of Springer Nature

About this chapter

Cite this chapter

Woźniak, J., Wereda, W. (2018). Information and Communication Technologies (ICTs) in Enterprises on the Over The Counter (OTC) Markets in European Union: Case Study of Polish NewConnect Market. In: Dima, A. (eds) Doing Business in Europe. Contributions to Management Science. Springer, Cham. https://doi.org/10.1007/978-3-319-72239-9_20

Download citation

DOI: https://doi.org/10.1007/978-3-319-72239-9_20

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-72238-2

Online ISBN: 978-3-319-72239-9

eBook Packages: Business and ManagementBusiness and Management (R0)