Abstract

We examine the developments in the Turkish banking industry in the context of capital and financial inflows specifically focusing on cross-border banking liability. First, we analyse how the Turkish economy, as an emerging market, has been affected by capital and financial inflows. Against this backdrop, we describe the transformation of the Turkish banking sector, paying special attention to the post-2001 period. In particular, we also investigate the impact of cross-border liability on the performance of Turkish banks. Finally, we evaluate the current outlook of the Turkish banking sector and offer some policy recommendations.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

JEL Codes

1 Introduction

The Turkish economy has increasingly become more integrated into the global economy through not just trade but also capital flows. In the aftermath of the 2001 banking and financial crises, the process of capital integration of the Turkish economy with the rest of the world has moved into a new phase supported by structural financial reforms and political stability.

Capital inflows can provide substantial benefits for emerging countries at the expense of additional risks. Capital inflows can stimulate domestic investment through lending, thereby increasing growth rates and living standards. They also supply necessary funds for developing countries that make it easier for them to sustain their budget deficits. On the other hand, capital inflows lead to current account deficits , market bubbles, lending booms, volatile and short-run flows, and exchange rate fluctuations risks, which are even prevalent in countries having sound economic fundamentals (Calvo et al. 1996; Mishkin 2009; Caballero 2016). Emerging market economies (EMEs) have implemented several macroprudential policies to minimize the risks associated with capital flows and increase their potential benefits.

Banks, as intermediaries of financial flows between domestic and global markets, play a significant role in managing the trade-off between these benefits and risks. Banks also act as a bridge between foreign loans (cross-border liability) and domestic lending. In recent years, EMEs have witnessed a rapid growth in bank credits . Simultaneously, there has been an increasing trend towards the internationalization of EMEs banking through cross-border banking (i.e., non-core) liability (Fig. 1) (BIS 2014). Therefore, any overuse or abuse of cross-border liability by EME banks to meet domestic lending demand could create a banking crisis or financial turbulence since cross-border banking liability directly affects the level of domestic lending, especially when the domestic banking sector cannot find enough core liability (i.e. domestic deposit).

Cross-border total banking liability by emerging regions (billion USD) (Source: BIS)

Since 2002, Turkish domestic deposits have grown significantly as a result of financial deepening and overall income growth. Likewise, the Turkish economy’s credit growth has increased during the same period. However, as the loan-to-deposit ratio exceeded the critical level of one in 2011, the Turkish banking sector gradually started to rely increasingly on cross-border liability.Footnote 1 This higher reliance on cross-border liability may have increased banking risks related to maturity mismatch, currency mismatch, liquidity , short-/long-term foreign exchange (FX) liability, and interest and exchange rates. In response to larger access to non-core liability (banking foreign loan inflow) and sudden stop/volatile financial flows, the Central Bank of Turkey (CBRT) started to implement new policies (such as interest rate corridor and reserve option mechanism) and changed its reserve requirement rate for non-deposit FX liability to deal with these potential risks. As a consequence of macroprudential policies, foreign borrowing in the Turkish banking sector creates little short-term risk due to non-deposit FX liability. However, because the loan-to-deposit ratio of the sector exceeds the 100% threshold, there would still be a problem because the higher reliance on foreign sources makes the domestic banking system more vulnerable to external shocks.

In this chapter, we examine the developments in the Turkish banking industry in the context of capital and financial flows, specifically focusing on cross-border banking liability (non-core). In the first part, we briefly analyse how the Turkish economy, as an EME, has been affected by capital and financial inflows. Then, we touch upon how different types of financial inflows and the banking sector are interrelated especially through cross-border liability. In the second part, the transformation of the Turkish banking sector will be described by focusing on the post-2001 period. Then we investigate the association between cross-border liability (non-core) and the performance of Turkish banks. Afterward, we examine the current outlook for the Turkish banking sector. Finally, we conclude with policy recommendations.

2 The Turkish Economy and Financial Inflows

The Turkish economy has demonstrated similar characteristics to other emerging economies. The prevailing facts regarding financial flows observed in the other EMEs and the impacts of these flows specified in the literature, such as lower interest rates, market bubbles, lending booms, and monetary expansion, have been true for the case of Turkey as well (Calvo et al. 1996). As an example, in Fig. 2 we show the first 10 countries with the largest international investment deficits (IIDs) (financial assets: e.g. foreign direct investment (FDI), portfolios, loans). Turkey has the ninth largest international trade deficit in the world economy (ranked between Mexico and Indonesia). More importantly, Turkey has the fifth highest ratio of IID to GDP.Footnote 2 We need to look at the composition of financial flows into a country to understand its international investment position.

International investment deficit positions (billion USD) (Source: International Monetary Fund)

The composition of financial flows in the Turkish economy can be seen in Fig. 3. The total share of FDI in financial flows is smaller than that of other categories but follows a stable pattern, while portfolio inflows are more volatile compared to other inflows. We observe an increasing trend in financial inflows since 2003, albeit with high volatility.

Turkey’s financial account composition (million USD) (Source: CBRT)

The large swings in financial inflows inevitably influence the macroeconomic environment by affecting firms’ and banks’ balance sheets, their access to credit , lending behaviour, pricing dynamics, and import /export structure. To address potential risks created by short-run/volatile financial flows, which have started to rise again since the 2008 financial crisis , the CBRT has been very actively and successfully managing the volatile and sudden stop in financial flows through traditional and new macroprudential tools. For instance, the active use of the interest rate corridor (widening or narrowing) and the reserve option mechanism by the CBRT in 2010 reduced the lower bound of the interest rate (borrowing rate) and increased the reserve option coefficient during large capital inflows, restricting the supply of foreign currency and its depreciation (Aysan et al. 2015). Moreover, the ratio of current account deficit to GDP was again reduced to a critical level of 5% (CBRT 2016; Roubini and Wachtel 1999).

During the same period, the Borsa Istanbul stock exchange’s main BIST 100 index rose about 700% from an average of 10,000 to around 80,000, and the secondary-market bond rate with 2-year maturity decreased from 65% to 9%, while the USD/TL exchange rate was stable between 2002 and 2014. The exchange rate showed a declining trend between 2003 and 2009 but then increased as a result of the US Federal Reserve (Fed)’s announcement of possible systematic interest rate hikes in 2014. Real consumption doubled over 2002 levels. The M1 money supply in the Turkish economy rose about 1700% between 2002 and 2015. One of the main characteristics of this period is the high appreciation of Turkish housing prices, especially in big cities. All these facts are consistent with the financial inflow literature.

3 Types of Financial Flows and Banking Through Non-core Liabilities

Financial flows are comprised of various components such as FDI , portfolios, deposits, credit , and reserves that differ based on the maturity (long, short) or nature of the claim (equity, debt). Each component has a different effect on the financial system and banking industry (Caballero 2016). It is held that equity-based inflow is not damaging compared to debt-based inflow. For instance, equity-based inflow FDI is steady and usually demonstrates long-run characteristics, while debt-type inflows, such as deposits or credit (through banking), have short-run and sudden-stop characteristics. One crucial component of financial inflows is cross-border banking liability (bank loans, debt securities inflows). Although the share of banking industry credit inflow (cross-border loan liability) in overall financial inflow is low, it could adversely affect the financial system stability because of its volatile and procyclical nature, especially in emerging economies depending on the global and domestic risk perceptions (Bruno and Shin 2014; Shin 2014; Cowan et al. 2007). Concerns related to cross-border banking credit inflows can be observed through banks’ balance-sheet transactions, and they can influence banks’ lending behaviours since they are directly related to how banks manage their external and internal balance-sheet liabilities. The main funding source of domestic banks is domestic savings, which make up the deposit part of the balance-sheet liability, the so-called core liability. However, bank deposits heavily depend on the performance of the domestic economy, specifically on households’ savings rates, which constrain the size of the overall internal funding source. If demand for domestic credit grows faster than the supply of total domestic deposits, banks turn to foreign funds to finance the excess demand for domestic credits . Especially during a credit boom period, we observe that banks in emerging economies such as Turkey and Brazil try to increase their lending capacity by borrowing from abroad using the international banking system. Figure 4 shows the cross-border banking liability for some emerging countries.

Cross-border banking liability (all instruments, million USD) (Source: BIS)

This kind of credit inflow or wholesale funding from foreign creditors increases the non-core liabilities of banks’ balance sheets. It is important to note that banking industry credit inflow (wholesale foreign funding ) is unstable compared to domestic deposits since it depends on international capital market conditions and risk perceptions (Hermann and Mihaljek 2010). Therefore, how banks improve their ability to lend through equity and debt (internal or external) is crucial. For example, Hahm et al. (2013) find that the non-core liabilities of banks are the most pronounced indicator of financial vulnerability during lending booms since they directly affect the risk variables of an economy such as maturity mismatch, liquidity , short-/long-term FX liability (non-deposit and deposit), and interest and exchange rates.

One of the main factors affecting domestic banking cross-border liability is exchange rate as domestic banks borrow and pay back foreign wholesale loans in foreign currency, for example in USD and euros. Economists have been studying how financial inflows and exchange rates are interrelated. For instance, Bruno and Shin (2014) show that local currency appreciation has a major impact on the foreign borrowing of domestic banks. Therefore, exchange rate volatility might harm banks’ balance sheets through maturity mismatch and the time horizon of their debt positions.

Apart from cross-border liability, normally domestic currency appreciation is expected to reduce the amount of capital inflows since capital inflow would earn a lower return in a non-appreciation period. If policymakers intervene in the foreign exchange market to limit appreciation and control capital inflows, they may encourage additional capital inflows and create extra-market distortions in the short run. Regarding cross-border banking liability and the balance-sheet perspective, domestic currency appreciation is believed to positively affect banking performance since banking credit inflow depends mainly on borrowing in foreign currency and lending in domestic currency. Therefore, policymakers should be very careful in their attempts to control capital inflows and appreciation. Their policies may influence the real economy and financial system in unintended ways. Evidence suggests that EME banks have learned how to deal with or dampen exchange rate fluctuations following the 2008 financial crisis (Brunnermeier et al. 2012). Foreign currency reserves and FX asset/liability composition (long vs. short) in EME banks’ balance sheets are shelters against exchange rate fluctuations and financial crises that minimize the damage from external factors.

4 Turkish Banking Sector

4.1 Pre-2001 Developments

After transforming its economy into a fully liberalized market in the 1980s, Turkey began to receive its first huge volume of capital inflows by the end of the 1980s (Agenor et al. 1997). Significant structural economic reforms , such as the convertibility of the domestic currency, free capital movement, and liberalization of loan and deposit rates and the foreign exchange regime were implemented during the middle of the 1980s, and as a result, Turkey has integrated into the global financial system.

Turkey’s integration into the global financial system has advantages and risks. As a result of liberal market reforms , the Turkish financial and banking sector made rapid progress. With the entrance of new private and foreign banks, the share of public banks in the total industry fell precipitously. The new entries made the industry more competitive and more institutionalized. Nonetheless, from this point the Turkish economy has had a short-term capital inflow problem. In addition to short-term capital inflows, high inflation, increasing public debt, current account deficits, and dollarization were negative characteristics of the period between 1989 and 2000. During that period, the annual average inflation rate was 72%, distorting the efficiency of monetary/fiscal policy and increasing the uncertainty of economic transactions. The average ratio of external or foreign debt (including public) to GNP was about 47% and increased to 78% for 2000–2001, as a result of public budget deficit financing. During this period, the main objective of the private banks was to provide short-term funds to the public sector by borrowing from abroad, which allowed them to earn the simple interest spread but exposed them to exchange rate risk, while public banks had poor performance mainly because of political intervention and mismanagement. Given all these facts, Turkey experienced several crises resulting from domestic and global events. Among them were the 1991 Gulf War, the 1994 Mexican currency crisis, the 1997 devaluation, the 1997 East Asian financial crisis , the 1998 Russian financial crisis , and the 2000–2001 banking liquidity and FX crises in Turkey (Mercan et al. 2003). In particular, the general outlook and disappointing performance of the Turkish banking industry and political instability were considered to be major consequences of the 2000 and 2001 economic crises. As a result, the primary measures taken to restore the Turkish economy focused on the structural issues of the banking and financial industry.

4.2 Post-2001 Developments

With the Banking Sector Restructuring Programme following the 2001 banking crisis , authorities aimed to increase the efficiency of state banks, solve the problems of the insolvent banks transferred to the Saving Deposit Insurance Fund (SDIF), strengthen the balance sheets of private banks, and broaden the supervisory and regulatory scopes by the Banking Regulatory and Supervisory Agency (BRSA). Certain criteria about deposit insurance, capital adequacy, non-performing loans, ownership, FX position, and liquidity management were established to make the supervisory and regulatory framework function well. For instance, under the new FX regulation, banks were not allowed to increase their FX positions to more than 20% of their equity. In the years following the regulatory and supervisory measures, the overall size of the banking industry shrank. The number of banks, branches, and employees significantly declined. The period between 2001 and 2004 is known as the period of recovery and stabilization of the Turkish banking sector (Akın et al. 2009).

After the recovery and stabilization period, the Turkish banking sector entered a new phase in which political stability, economic growth, and external factors such as EU membership negotiations and global macroeconomic recovery played important roles in this development. From 2004 to 2008, the total USD-valued assets increased by 183% and total equity rose by about 156% (Fig. 5).

Turkish banking industry (million USD) (Source: BRSA)

The number of employees in the banking industry increased by about 25%, and the number of branches rose by about 80%. During the same period, five additional foreign commercial banks entered the Turkish market, and the Turkish banking industry was able to borrow large amounts of money from international financial markets through syndication and securitization loans in which the total amount of cross-border liabilities rose from 4.3 billion USD in 2004 to 27 billion USD in 2008.

Even though there was an increase in the number of employees and branches in the Turkish banking sector between 2008 and 2011, global economic and financial conditions depressed banking activities. During this period, the total assets, total lending, and cross-border inflows declined. The period between 2011 and 2015 was dominated by internal conflict in 2013, political uncertainties that resulted from governmental elections in 2015, and change in the Fed’s interest rate policy. Also, increased risk perception towards EMEs and lower growth rates of the Chinese economy shaped this period. Moreover, tighter domestic prudential regulations on credit , a rise in interest rates, and lower economic growth put pressure on banking activities and lending in the last 2 years of this period (CBRT 2015). Although these internal and external factors might have short-run negative impacts on the banking industry and lending activities, the Turkish banking industry is expected to progress and grow as it has in the past. When global economic and financial conditions improve, rising GDP growth rates and domestic political stability could foster international financial flows into Turkey and stimulate domestic investment .

4.3 The Turkish Banking Sector and Non-core Liabilities

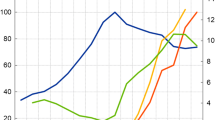

In recent years, EMEs have witnessed rapid growth in bank credit . Simultaneously, emerging economies have faced an increasing trend in cross-border banking credit that has led to greater profitability through higher interest rate spreads but is also a new risk factor for financial intermediation. In EMEs such as Turkey, Korea, and Mexico , the share of wholesale funding in total liabilities has increased in the last decade (BIS 2016). Like other EMEs, total syndication and securitization loans (cross-border liability) in the Turkish banking industry have risen steadily since 2002 (Fig. 6).

Syndication and securitization loans (million USD left axis) and total lending/total deposits (% right axis) (Source: BRSA)

Between 2003 and 2008, banks were increasingly able to borrow from abroad, but global financial turbulence reversed this inflow because of changes in the global risk perception. Then the Turkish banking industry started to receive a high volume of foreign credit again from the beginning of the second quarter of 2013 until the second quarter of 2015. The year 2012 and the last two quarters of 2015 were dominated by elections and domestic conflicts, which increased the country’s risk level and discouraged international investors’ willingness to lend.

Cross-border banking liability is crucial for domestic lending, especially when the banking sector cannot find enough core liability (domestic deposits). Domestic deposit growth has followed a strong path in the Turkish economy, resulting from financial deepening and general income growth since 2002. Simultaneously, the trend in credit growth outpacing domestic deposit growth has also increased during the same period. But the sector’s loan-to-deposit ratio exceeded the critical level of one in 2011, which in turn increased banks’ reliance on foreign funding . As the domestic credit growth/level has been larger than the domestic deposit growth/level, banks have started to turn to foreign markets (external borrowing) (Fig. 6). The high correlation between lending to deposit ratio and cross-border liability to asset ratio since 2010 might be a potential risk that should be taken into account. The increasing reliance of the Turkish banking sector on cross-border liability might create risks such as credit risk, funding risk, maturity mismatch, currency mismatch, liquidity , short/long-term FX liability, and interest and exchange rate fluctuations (Adrian and Shin 2009; Hills and Hoggarth 2013; Allen 2011). For instance, when banks expand their balance sheets through cross-border liability, their borrowing has a shorter maturity than lending. This may make banks vulnerable to a maturity mismatch problem.

Banking non-core liability is directly associated with liquidity risk. Concerning liquidity risk, the Turkish banking industry has two concentrations : one around TL assets and core liabilities, the other around FX and non-core liabilities. Generally speaking, Turkish banks seem to be successful at containing their liquidity risk, including TL and FX. However, it is still important to manage the liquidity risk associated with external financing (non-core liabilities). Banking industry USD-valued external debt increased from 2009 but started to decrease in early 2015 owing to internal and external risks. However, the growth rate of foreign debt is still positive under an exchange-rate-adjusted effect (CBRT 2015).

To deal with the potential risks, the monetary authorities in emerging economies may implement policies and regulations to strengthen the resilience of the banking industry against risks associated with non-core liabilities. Monetary authorities in EMEs have carried out macroprudential regulations such as raising non-deposit FX reserve requirement, attracting foreign bank entry, and stronger supervision (BIS 2009). In addition, the interest rate corridor and reserve option mechanism were new policy tools that started to be implemented in 2010 by the CBRT to reduce risks related to volatile short-term capital inflows and control currency appreciation/depreciation (Aysan et al. 2015). These new tools are crucial because when volatile capital flows are not managed properly by monetary authorities, the sudden appreciation or depreciation of foreign exchange might occur. These sudden ups and downs inevitably affect banks’ balance sheets and lending activities adversely. Based on the empirical evidence from Turkey, Aysan et al. (2015) show that these new policy tools have been effective at minimizing the impacts of volatile cross-border capital inflows.

The composition of foreign financing also changed owing to the new arrangement of the CBRT that aimed to foster external financing with long-term maturities. The CBRT recently increased the reserve requirement ratios for non-deposit FX liability with a maturity of less than 3 years. In response to this change, there was an increase in long-term external financing and a decrease in foreign funding with short-term maturities. The short-term foreign liabilities as a share of total foreign liabilities decreased from 58% in 2014 to 33% in 2015. Further, the average maturity of foreign liabilities of banks rose to 51 months, and the average maturity of syndicated loans increased from 12 to 15 months (CBRT 2015).

Interest rate and exchange rate fluctuations might create a risk of maturity mismatch between banks’ assets and liabilities. Since 2013, the average maturity of banks’ assets has been fluctuating between 19 and 21 months, while liabilities exhibit a more stable and smoother pattern at 3 months. During this period, the maturity of loans (interest-rate sensitive) and long-term TL deposits as a share of total deposits have been declining, whereas the share of FX assets and liabilities have been rising. The total amount of FX liabilities is higher than FX assets, and FX liabilities as a share of total liabilities has been increasing. According to the CBRT’s 2015 financial report, the impact of exchange rate fluctuations on Turkish banks’ balance sheets is very limited since banks take on-balance-sheet short and off-balance-sheet long positions simultaneously. Therefore, net FX positions of the banking industry follow a steady trend (CBRT 2015). Instead, the banking industry’s long-term maturity TL assets and liabilities are more sensitive to interest rates compared to maturities up to 1 year (CBRT 2015).

4.4 Overall Outlook and Some Policy Recommendations

As of 2016, 52 banks operate in the Turkish banking industry, including 34 commercial banks (3 publicly owned, 9 privately owned with domestic holders and 15 privately owned with foreign holders), 13 investment and development banks, and 5 participation banks. Six international commercial banks have branches in Turkey (BAT 2016). Over the last 15 years, the total assets of the Turkish banking industry have risen by about 505%, valued at 821 billion USD, and total equities have increased by 416%, valued at over 91 billion USD. As can be seen in Fig. 7, the general profitability of the Turkish banking sector has experienced a noticeable decline in all measures including net interest margin (NIM), return on assets (ROA), and return on equity (ROE) since 2002. During this period, ROE diminished less than ROA since total banking assets grew more than total equities and the steady fall in interest rates kept downward pressure on NIM.

Turkish banking profitability (%) (Source: BRSA)

To deal with declining profitability, the banking sector intends to increase efficiency, more effectively use technology , and minimize costs. A closer look at the numbers shows that the strong and well-designed domestic supervisory and regulatory framework is likely to support the banking sector’s positive outlook. Risk indicators such as liquidity risk, capital adequacy, and non-performing loans reflect a stable and promising signal for the future. Cross-border liability (non-core) will continue to be the primary funding sources for domestic lending given that domestic deposits and the savings rate continue to be low while domestic lending is on an upward trend. Although increased reliance on wholesale foreign borrowing does not create any short-term risk in terms of non-deposit FX liability, it is likely to be one of the risk factors that the banking sector will confront until it finds less risky funding sources, other than foreign funding , for its lending activities. In fact, the Turkish banking sector should devise a new road map, in line with its solid appearance, to be classified as one of the top banking systems among EMEs. In this context, we have some general and specific policy recommendations for the sector.

The interest income of Turkish banks dominates their non-interest income (Aydemir and Ovenc 2016). Unlike EMEs, one of the key features of developed countries’ banking sectors is that they have higher trading income compared to interest income to hedge against interest rate risk. Hence, we recommend that the Turkish banking sector increase its trading income capacity through hedging, direct investment , or investment partnerships. These kinds of trading activities and investment partnerships might help the sector to increase its profitability and shield the sector against possible risks.

In today’s international financial system, advanced economies and global banks capture the lion’s share of cross-border banking inflows. Against this backdrop, increasing the capacity of regional financial integration between the Turkish and other EMEs’ banks would be beneficial. This kind of integration, through creative and efficient partnership models, has the potential to instigate a new momentum towards cross-border liability expansion and might eventually reduce the global risks associated with capital flows from advanced economies. In this regard, the Turkish banking sector could seek to enter new markets in countries with which Turkey has historically maintained good relationships and has high levels of economic integration in other sectors. Opening new branches in neighbouring countries that Turkey trades with actively could reduce Turkey’s dependence on non-core liabilities from advanced economies.

Given the difficulties in efficiently coordinating cross-border inflows and a lack of global regulation, the CBRT and other authorities should continue to closely monitor cross-border financial inflows. Measures should be pursued vigorously to attract long-term cross-border banking liabilities. Effective policies and regulations that stimulate domestic savings and long-term investment positions might reduce the banking sector’s reliance on cross-border foreign funding . Although the macroprudential policies implemented by the CBRT have helped manage capital flows and cross-border banking liability in the short term, we should keep in mind that these policies are only the second-best solutions until long-term structural reforms yield the desired results with respect to increasing savings rates and productivity and lowering inflation and current account deficits (Kara 2016).

To limit the extent to which the banking and financial system is adversely affected by exchange rate fluctuations and outflows, a Tobin tax imposed on short-term financial capital might be considered an option. Indeed, following the East Asian and Latin American crises, Malaysia and Chile successfully implemented such a policy (Rajan 1998). The Malaysian authorities imposed controls on capital flows and foreign exchange transactions to deal with speculative capital movements (Kim 2003). The possibility of levying such a tax on some types of financial flows was discussed in Turkey after the 2001 banking and financial system crisis , and it is a hot topic among economists and authorities whenever current account deficits create a risk for the country. Apart from the current account risk, this kind of tax might dampen speculative flows into the Turkish economy.

Asset price bubbles, especially in real estate markets, have a direct impact on the excessive use of credits and, therefore, on cross-border banking liability. Effective use of monetary policy (i.e. interest rate) and macroprudential regulations could help reduce the systemic risks related to market bubbles. Given the facts that real estate prices vary by region and some cities have different economic fundamentals than others, using a tight monetary policy to address asset price bubbles might cause unintended consequences. For instance, while a rise in the interest rate might limit and control asset prices in some markets, it might also negatively affect real estate markets in cities that do not have bubbles. In such circumstances, in lieu of monetary policy, macroprudential policies such as fine-tuning of loan-to-value ratios would be more effective at dealing with market bubbles (Allen 2011). In this regard, the CBRT should actively continue using these targeted macroprudential policies to address systemic bubble risks.

The problems faced by banks, such as maturity mismatches, currency mismatches, and exchange rate volatility , are partly shaped by the nature of cross-border banking flows. Central banks play a critical role in reducing risks associated with these problems. Specifically, during shortages of foreign reserves, the timely intervention of the central bank to provide adequate reserves to the banking sector is vital, so that attempts to harm the credibility of the central bank should be avoided at all costs. To maintain its credibility, the central bank must not only be independent of outside pressure but also needs to be a good communicator. These qualities would help resolve ambiguities that arise in the course of the central bank’s work, especially in dealing with problems related to cross-border banking inflows.

5 Conclusion

Since the early 2000s, the Turkish banking sector has continued to prosper significantly and gradually become more integrated into global financial markets . The strong and well-designed domestic supervisory and regulatory framework is likely to support the banking sector’s positive outlook. Risk indicators such as liquidity risk, capital adequacy, and non-performing loans reflect a stable and promising signal for the future. To deal with falling profitability, the banking sector must do its best to minimize costs, increase efficiency, and better utilize technological innovations .

Domestic deposit growth has followed a strong trajectory in the Turkish economy as a result of the financial deepening and overall income growth that have occurred since 2002. Likewise, the Turkish economy’s credit growth has also increased during the same period. The high correlation between lending-to-deposit ratio and cross-border-liability-to-asset ratio since 2010 might be a potential risk that should be taken into account. Cross-border liabilities (non-core) seem to be a key funding source for domestic lending, given that domestic deposit and savings rates in Turkey continue to remain low while domestic demand for lending is on an upward trend.

Although the increased reliance on wholesale foreign borrowing does not create any short-term risk in terms of non-deposit FX liability, maturity mismatch, currency mismatch, and liquidity , it is likely to be one of the risk factors that the banking sector should confront until it finds alternative, less-risky financing sources since higher reliance on foreign wholesale funding makes the domestic banking system more vulnerable to external shocks. In fact, the Turkish banking sector should come up with an updated road map, in line with its solid appearance, to be classified as one of the top banking systems among the EMEs.

Notes

- 1.

Turkish banking sector total cross-border liability has increased from USD 7.3 billion to USD 103 billion since 2002. Especially during the last 5 years, total cross-border banking liability to banking total assets rose on average from 8% to 13%.

- 2.

We calculate the ratio of IID to GDP using a 2014 data set of 15 countries that had the highest international investment deficit. For instance, USA’s IID-to-GDP ratio was around 0.4, while Turkey had a ratio of 0.55. Greece, Portugal, and Spain were among the top three countries that had the highest IID to GDP ratio.

References

Adrian, Tobias, and Hyun Song Shin. 2009. Money, Liquidity, and Monetary Policy, FRB of New York Staff No. 360. New York: Federal Reserve Bank of New York.

Agenor, Pierre-Richard, C. John McDermott, and Murat Üçer. 1997. Fiscal Imbalances, Capital Inflows, and the Real Exchange Rate: The Case of Turkey. European Economic Review 41 (3): 819–825.

Akın, G. Gülsün, Ahmet Faruk Aysan, and Levent Yıldıran. 2009. Transformation of the Turkish Financial Sector in the Aftermath of the 2001 Crisis. In Turkey and the Global Economy: Neo-Liberal Restructuring and Integration in the Post-Crisis Era 73.

Allen, Franklin. 2011. Cross-Border Banking in Europe: Implications for Financial Stability and Macroeconomic Policies. Washington, DC: CEPR.

Aydemir, Resul, and Gokhan Ovenc. 2016. Interest Rates, the Yield Curve and Bank Profitability in an Emerging Market Economy. Economic Systems 40 (4): 670–682.

Aysan, Ahmet Faruk, Salih Fendoğlu, and Mustafa Kilinc. 2015. Macroprudential Policies as Buffer Against Volatile Cross-Border Capital Flows. The Singapore Economic Review 60 (01): 1550001.

BAT (The Banks Association of Turkey). 2016. Banks and Banking Sector Information. http://www.tbb.org.tr/en/banks-and-banking-sector-information/member-banks/list-of-banks/34. Accessed 15 Sep 2016.

BIS (Bank for International Settlements). 2014. EME Banking Systems and Regional Financial Integration, Committee on the Global Financial System, CGFS Papers 51. http://www.bis.org/publ/cgfs51.pdf. Accessed 10 Jan 2016.

———. 2009. Capital Flows and Emerging Market Economies, Committee on the Global Financial System, CGFS Papers 33. http://www.bis.org/publ/cgfs33.pdf. Accessed 10 Jan 2016.

———. 2016. Locational Banking Statistics. http://www.bis.org/statistics/bankstats.htm?m=6%7C31%7C69. Accessed 15 Apr 2016.

Brunnermeier, Markus, José De Gregorio, Barry Eichengreen, Mohamed El-Erian, Arminio Fraga, Takatoshi Ito, P. R. Lane et al. 2012. Banks and Cross-Border Capital Flows: Policy Challenges and Regulatory Responses, Committee on International Economic Policy and Reform. Washington, DC: Brookings.

Bruno, Valentina, and Hyun Song Shin. 2014. Cross-Border Banking and Global Liquidity. The Review of Economic Studies 82 (2): 535–564.

Caballero, Julián A. 2016. Do Surges in International Capital Inflows Influence the Likelihood of Banking Crises? The Economic Journal 126 (591): 281–316.

Calvo, Guillermo A., Leonardo Leiderman, and Carmen M. Reinhart. 1996. Inflows of Capital to Developing Countries in the 1990s. The Journal of Economic Perspectives 10 (2): 123–139.

CBRT (The Central Bank of Turkey). 2015. Financial Stability Report. http://www.tcmb.gov.tr/wps/wcm/connect/TCMB+EN/TCMB+EN/Main+Menu/PUBLICATIONS/Reports/Financial+Stability+Report/2015/Financial+Stability+Report-November+2015%2C+Volume+21/. Accessed 5 June 2016.

———. 2016. Monetary Policy, Interactive Charts, Current Account Balance. http://www.tcmb.gov.tr/wps/wcm/connect/TCMB+EN/TCMB+EN/Main+Menu/PUBLICATIONS/Reports/Financial+Stability+Report/2016/Volume+23/. Accessed 5 Mar 2017.

Cowan, Kevin, De Jose Gregorio, Alejandro Micco, and Christopher Neilson. 2007. Financial Diversification, Sudden Stops and Sudden Starts. Banco Central de Chile. https://core.ac.uk/download/pdf/6642643.pdf. Accessed 22 Aug 2016.

Hahm, Joon-ho, Hyun Song Shin, and Kwanho Shin. 2013. Noncore Bank Liabilities and Financial Vulnerability. Journal of Money, Credit and Banking 45 (s1): 3–36.

Herrmann, Sabine, and Dubravko Mihaljek. 2010. The Determinants of Cross-Border Bank Flows to Emerging Markets: New Empirical Evidence on the Spread of Financial Crises, Bundesbank Series 1 Discussion Paper No. 2010,17.

Hills, Bob, and Glenn Hoggarth. 2013. Cross-Border Bank Credit and Global Financial Stability. Bank of England Quarterly Bulletin Q2: 126–136.

Kara, Hakan. 2016. Turkey’s Experience with Macroprudential Policy, BIS Paper No. 86q.

Kim, Young-Chul. 2003. Understanding the Silence Amid Turmoil: The Tobin Tax and East Asia. In Debating the Tobin Tax, ed. J. Weaver, R. Dodd and J. Baker, 135–150. Washington, DC: New Rules for Global Finance Coalition.

Mercan, Muhammet, Arnold Reisman, Reha Yolalan, and Ahmet Burak Emel. 2003. The Effect of Scale and Mode of Ownership on the Financial Performance of the Turkish Banking Sector: Results of a DEA-Based Analysis. Socio-Economic Planning Sciences 37 (3): 185–202.

Mishkin, Frederic S. 2009. Why We Shouldn’t Turn Our Backs on Financial Globalization. IMF Staff Papers 56 (1): 139–170.

Rajan, Ramkishen. 1998. Restraints on Capital Flows: What Are They? No. 22383. East Asian Bureau of Economic Research.

Roubini, Nouriel, and Paul Wachtel. 1999. Current-Account Sustainability in Transition Economies. In Balance of Payments, Exchange Rates, and Competitiveness in Transition Economies, ed. M.I. Blejer and M. Škreb, 19–93. Boston: Springer.

Shin, Hyun Song. 2014. The Second Phase of Global Liquidity and Its Impact on Emerging Economies. In Volatile Capital Flows in Korea, ed. K. Chung, S. Kim, H. Park, C. Choi, and H.S. Shin, 247–257. New York: Palgrave Macmillan.

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2018 The Author(s)

About this chapter

Cite this chapter

Aydemir, R., Ovenc, G. (2018). Capital Inflows and Banking in the Turkish Economy. In: Aysan, A., Babacan, M., Gur, N., Karahan, H. (eds) Turkish Economy. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-319-70380-0_8

Download citation

DOI: https://doi.org/10.1007/978-3-319-70380-0_8

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-319-70379-4

Online ISBN: 978-3-319-70380-0

eBook Packages: Economics and FinanceEconomics and Finance (R0)