Abstract

The rise of the Russian Federation, Kazakhstan and Ukraine as world wheat exporters has been accompanied by uncommonly volatile international commodity prices. This chapter will explore the role of the wheat-producing Commonwealth of Independent States (CIS) countries in the volatility of international wheat prices. Studies of the connection between CIS wheat trade and international price volatility have predominantly focused on export restraints imposed by these countries between 2006 and 2011. We explore the literature on export restraints and price volatility, noting the short- and long-run effects of restraints. We also go beyond export restraints as a source of international price instability, pointing to two further potential sources of price volatility: production volatility and growing state intervention in grain markets in the wheat-producing CIS countries. Production volatility is caused mostly by weather variation and other agronomic factors. Such volatility has an understandable scientific basis, and can be controlled by the use of more inputs and better agronomic practices. Political border interventions aimed at limiting grain exports are of a different nature, since they are highly unpredictable. In this respect they are akin to the increased state measures, aimed at ‘stabilising’ and exerting state control over grain markets observed in the CIS wheat sector since 2001. Taken together, these policies do not bode well for the stability of grain prices in the future.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

1 Introduction

The international grain-trading system is in an era in which new exporters are taking a larger role in international wheat markets. The exporters of the Commonwealth of Independent States (CIS) are relatively new to world export markets. In 1999–2001 (three year average) they captured only 9 % of total world wheat exports. By 2009–2011 this proportion had more than doubled to 21 %. As world wheat demand increases, the dependence on new exporters will continue and will probably grow. According to forecasts by the Organisation for Economic Co-operation and Development (FAO), the Food and Agriculture Organization of the United Nations (FAO) (OECD-FAO 2015) and the Economic Research Service of the United States Department of Agriculture (USDA ERS), the CIS exporters will significantly increase their share of world exports over the next 10 years, primarily at the expense of the United States.

The rise of these CIS countries as world wheat exporters has been accompanied by uncommonly volatile commodity prices. According to many studies (Brown et al. 2008; Dollive 2008; Welton 2011; Headey 2011; Sharma 2011) the CIS countries have themselves contributed to the volatility of prices. High price volatility can be characterised as a situation when prices fluctuate significantly and unpredictably over a short time. There are therefore two aspects to volatility: variability and uncertainty.Footnote 1 Variability describes the movement of prices, while uncertainty refers to the unpredictability of that movement (Prakash 2011). Whereas households may cope with predictable variation (risk), unpredictable changes are more a cause for concern. When unpredictable changes surpass a certain critical threshold and persist at those levels, traditional policy prescriptions and coping mechanisms are likely to fail (Wolf 2005).

Volatile prices are a cause for concern, first, because they tend to be associated with higher prices. It is in principle possible to have low but volatile prices, but the variability and unpredictability of such prices usually increase them. Higher food prices have a disproportionately negative effect on the living standards of poorer households, since a higher proportion (often 60–75 %) of the poor’s expenditures are on food (Prakash 2011). Second, volatile food prices, with their combination of variability and uncertainty, make households more vulnerable to the erosion of living standards. Gradually rising food prices are far less destructive for poor households, because they give time for households to adapt and cope with the increases.

The purpose of this chapter is to explore price volatility in the CIS wheat producers. Wheat is chosen because of its key role in food security. We explore two possible sources of price volatility: production and export volatility. Production volatility is characterised more by risk, since production in these countries exhibits a high coefficient of variation, but this is a long-standing issue with an understandable agronomic basis. Export volatility is another possible source of price volatility, although it is characterised more by uncertainty, since exports are affected by political interventions in grain markets, which are far less predictable than normal weather-related year-to-year yield variations. We conclude with some observations on how production and export volatility in these countries could be addressed.

1.1 Emergence of Russia, Ukraine and Kazakhstan on World Wheat Markets

Wheat is the most important grain produced and exported in the Russian Federation, Ukraine and Kazakhstan (RUK), making up 58 % of production and 59 % of grain exports in 2013. Exports of wheat from these countries have made a quantum leap, climbing from 8.9 million tonnes at the turn of the century to an average of 28.5 million tonnes in 2009–2011. The OECD and FAO project that this region will continue to increase its market share to 28 % of world wheat exports by 2020–2022 (Table 1).

The evolution of the share of the world market for wheat shows the sizeable change that took place in the first decade of the twenty-first century and the further changes that are expected to take place by 2020–2022. According to forecasts, the USA will lose the most market share as a result of the expanding wheat exports of RUK, but the other ‘traditional’ wheat exporters such as Canada, Australia and the European Union (EU) will also lose market share (Fig. 1).

Major wheat exporters, share of global market. Source: Table 1

1.2 The Contribution of Russian, Ukraine and Kazakhstan to Wheat Market Price Volatility

The literature on the role of RUK in price volatility has focused on individual instances of export restraints imposed in 2007/2008 and 2010, noting three causal connections between export restraints and price volatility:

1. ‘Cascading effect’ of export restrictions in 2007/2008. Dollive (2008) stated that the Ukrainian grain export ban established on 1 March 2007, followed by export quotas on wheat (from November 2007), led to a cascading effect, causing other countries to enact restrictions as well. Although Ukraine enacted export quotas starting in October 2006 (World Bank 2008), the export ban in the following year forced buyers to look to other sources for grain exports, raising prices and putting pressure on other suppliers, including Kazakhstan and Russia. This added demand on other suppliers in the region caused their stocks-to-use ratios to fall, leading them to enact grain-export restraints. This cascading effect affected the entire global market by encouraging further export restraints and higher prices. The unpredictability of the ‘cascading’ effect on supplies and prices tended to raise prices above levels consistent with market supply–demand fundamentals.

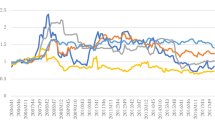

Kobuta et al. (2012) juxtaposed export policy changes for wheat from January 2006 to December 2010 with the price of third-class wheat on Ukrainian markets. The juxtaposition appears to show an exacerbation of price increases after the imposition of export constraints in 2006/2007 as well as 2010. On the other hand, the fall in wheat prices starting in March 2008 clearly predated the relaxation of export constraints, just as the initial rise in wheat prices did in July 2010 (Fig. 2). The behaviour of prices in Fig. 2 is consistent with the ‘cascading’ explanation by Dollive (2008).

Prices of third-class wheat in Ukraine and export restrictions. Source: Kobuta et al. (2012)

2. Diminished supply response due to dampened integration of domestic producer prices into world markets. Gotz et al. (2013) noted that an indirect effect of export restraints is the increase in grain supplies remaining on domestic markets. This ‘oversupply’ of grain on domestic markets drove down its price. Gotz et al. (2013) showed that the export restrictions introduced by Russia and Ukraine in 2007/2008 temporarily reduced the degree of integration of domestic and world wheat markets, increasing market instability and reducing the supply response of producers for the following marketing year. The effects were more severe in Ukraine, where an outright ban and quotas were used, whereas Russia relied mainly on export taxes.Footnote 2

3. In the longer run, the increased political uncertainty caused by government intervention decreased investment incentives for Russian and Ukrainian agriculture. Gotz et al. (2013) and Kobuta et al. (2012) noted that unpredictable state interventions in grain markets, exemplified by export restrictions, probably diminished incentives for investment in the sector, thus lowering long-run growth prospects. Thus, unpredictable export restraints can inhibit the supply response to high grain prices, thus increasing the likelihood of continued high prices and further price volatility.

While the connections between unpredictable export restraints and price volatility are well taken, by focusing exclusively on these individual instances of export restraints the literature emphasises only one of a number of potential sources of volatility represented by the emergence of RUK onto world markets as significant wheat exporters. In this chapter, therefore, I will focus on two further potential sources of volatility. The first is production volatility. The reason given by the authorities for grain export restrictions in 2007/2008 and 2010 was to prevent the growth of domestic food prices as a result of unexpectedly low grain harvests. Wheat yield and production volatility in RUK since 2000 has been the highest among the main wheat exporters. Reducing the variance of wheat yields and production would reduce a potential source of price volatility in world markets.

Second, it should be recognised that grain export limitations are not isolated instances. Rather, they are part of a general pattern of political intervention in agricultural markets and protectionism by the governments of Russia, Ukraine and Kazakhstan. Political intervention in agricultural markets, particularly wheat markets, has been on the rise since 2010, as is protectionism overall. Thus, the grain-export limitations should be seen as part of a general pattern of government intervention that is increasing in scope and severity. Addressing this new protectionism through more robust international agreements is another way to reduce a potential source of price volatility in world markets.

1.3 Production Volatility in Russia, Ukraine and Kazakhstan

A characteristic shared by all leading exporting countries is that production is far more variable than consumption. Figure 3 illustrates this observation using the example of RUK, where historical data to the end of 2012 show a relatively smooth wheat-consumption curve, but quite variable production. A comparison of production between countries (Fig. 4) shows that production in RUK was more variable than elsewhere, particularly after 2000. In fact, if the standard deviation of production in RUK is taken as 100, then the corresponding figures for Australia (30), the USA (33), Argentina (14), the EU (52) and Canada (17) were far less.

Wheat: aggregate production, consumption and export of RUK, 1992–2022 (forecasts begin in 2013). Source: OECD/FAO Agricultural Outlook, 2013–2022 database

Wheat: production of selected major exporters, 1992–2013. Source: OECD/FAO Agricultural Outlook, 2013–2022 database

A proper comparison of the variability of production should take into account both the standard deviation as well as the level of production. A given standard deviation of production with a small mean is in reality much more variable than the same standard deviation with a large mean. The coefficient of variation is a measure of variance that takes into account both the standard deviation of a series as well as the mean of the series.Footnote 3 Table 2 illustrates that the coefficients of variation of yields, production and exports in RUK have tended to be higher than in the traditional exporting countries. The only exception is Australia, where wheat yields are much closer to those in Kazakhstan than the other major exporters. Russia and Ukraine are by far the most volatile exporters.

2 Rapid Growth as an Explanation for Production Volatility

Table 1 showed that exports in RUK grew quite rapidly. The same can be said for production as well. Growth of wheat production in RUK was the fastest of all leading exporters (Table 3) between 1999/2001 and 2009/2011. RUK, along with the European Union, also had the fastest growth in exports. There is a high correlation between the rapid growth of exports and their volatility. The correlation coefficient between the average growth rates per annum and the coefficient of variation for 2000–2012 was 0.74. It is unclear why rapid growth and volatility are correlated, but it appears that they are.

3 Low-Input Applications as an Explanation for Production Volatility

Year-to-year yield (and grain-quality) fluctuations in rain-fed crops are mostly a function of weather-related phenomena: rainfall amount and distribution throughout the year, temperature distribution and resulting evapotranspiration, and length of growing season—all these factors play a role in annual yields. Winter wheat has the added issue of requiring sufficient snow cover over the winter period to avoid damage. One way to solve much of this problem is irrigation, but this is not, and never will be, practical for most rain-fed cropland. Intuitively, zero-tillage systems should decrease the year-to-year yield variability given that the soil is not disturbed, thereby conserving moisture.

Year-to-year input use may also contribute to yield stability, just as it raises the level of yields. Table 4 shows fertiliser applications for wheat for a number of exporters. Russia and Ukraine apply less fertiliser per hectare than the traditional exporters. This is reflected in the level of their yields, but also may contribute to yield variability. In fact, comparing the leading exporters of wheat in the world, there is a distinct negative correlation between the variability of yields and their level (−0.68). In other words, the higher the yield, the less variable are yields from year to year. Correspondingly, the lower are the yields, the higher the variability of yields (Table 5).

4 Increasing Winter-Wheat Cultivation in Russia as an Explanation for Production Volatility

One final factor influencing the volatility of wheat yields is the difference between spring and winter wheat. Spring wheat is planted in the spring and harvested in the autumn, whereas winter wheat is planted in the autumn, undergoes a period of vernalisation (a period of 30–60 days of cold weather from 0 °C to 5 °C) during the winter months, and then begins to grow in the spring to be harvested in the autumn. Although spring wheat has lower yields, they tend to be less volatile than winter wheat. Winter wheat has higher yields, but, because of vernalisation, is more affected by the environment, and therefore has more variable yields.

About 95 % of wheat in Kazakhstan is spring wheat and the same proportion is winter wheat in Ukraine. Thus, in these two countries any increase in yield volatility could not be attributed to the increased area under winter wheat. However, Russia has been undergoing a rapid transition from spring- to winter-wheat production since 1998 (Fig. 5). In 1998 only 32 % of total land sown with wheat had winter wheat, but by 2010 that proportion had increased to 48 %. Figure 5 indicates that spring-wheat yields are less variable than winter-wheat yields. In fact, from 2000 to 2010, the coefficient of variation for spring-wheat yields was 9.7, while for winter wheat it was 13.0.

5 Export Volatility in Russia, Ukraine and Kazakhstan

Table 2 indicates that exports were more volatile in RUK than in other major exporters during 2000–2012. Russia and Ukraine had the most volatile exports, with coefficients of variation of 71 and 62, compared with 13 in the United States, 17 in Canada and 28 in the EU-27. Production variability itself is a reason for export volatility, since in all countries domestic consumption is quite regular, and the difference between production and consumption is net exports. With the greater production variability of RUK, then, inevitably comes added volatility of exports. In addition, greater production variability would seem to offer more opportunities for political intervention in the name of protecting consumers from rising prices.

5.1 Political Export Restraints

The elevated fluctuations of yields in RUK are caused by weather variation and other agronomic factors. Thus, they seem to be more of the nature of risk, which has an understandable scientific basis, and can be controlled by higher input applications and better agronomic practices, including wider use of low-till agriculture. Political border interventions aimed at limiting grain exports are of a different nature, since they are highly unpredictable. Table 6 illustrates that during the crop years 2006/2007 to 2011/2012 RUK were plagued by a number of non-tariff barriers to grain trade. It is this policy volatility that increased the coefficient of variation of exports well above that of production. Such policy volatility can increase the volatility of world prices through the mechanisms noted in the literature on the connection between export restraints and price volatility (Brown et al. 2008; Dollive 2008; Welton 2011; Headey 2011; Sharma 2011).

It should be noted that Kazakhstan seemed less prone than Ukraine and Russia to political interventions aimed at limiting grain exports, since the Kazakh government did not impose restrictions on grain exports in 2010, despite pressure from the Russian government (Oshakbaev 2012).

5.2 Politicised State Intervention in Grain Markets

Political border interventions are part of a wider politicisation of grain and particularly wheat markets that can be observed in RUK in the 2000s. Grain, and particularly wheat, markets have long been politicised in Russia and Ukraine. Regional authorities restricted the movement of grain, and state parastatal organisations supplied inputs and procured wheat in the 1990s (Serova 2000; Brümmer and Zorya 2005; Chapko and Sedik 1998). However, grain-export restrictions with implications for world markets started only when the CIS exporters became global grain exporters in the 2000s. Essentially, only then did domestic political interventions in RUK become an issue for global grain markets.

An example of the politicisation of grain markets is that, in all three countries, state grain interventions and state grain intervention/trading/export agencies appeared in the 2000s and have quickly become the largest purchasers and holders of grain in the countries. In Russia, state grain interventions began in 2001 with the intent of stabilising prices on food markets by purchasing grain when harvests were large and selling grain when harvests were low. In practice, most of the interventions were grain purchases, because Russia consistently produced more grain than was necessary for domestic consumption. Export opportunities were limited by export infrastructure, particularly the bottleneck at the Novorossiysk port, which allowed a maximum shipment of 2–2.5 million tonnes per month (Azarieva 2014). During the 2008/2009 marketing year, the state purchased 9.6 million tonnes of grain, accounting for 9 % of the total harvest, in an effort to support domestic grain prices. This included 7.5 million tonnes of wheat, which is 11.8 % of the wheat harvest or 23.6 % of marketed wheat (Evdokimova 2011). At the end of the 2009/2010 marketing year nearly half of all grain stocks in Russia were in the state grain-intervention fund (Azarieva 2014).

In 2009 the Russian government considerably expanded its role in the grain sector by establishing the state-owned United Grain Company (UGC). The UGC was formed by revamping the Agency for Food Market Regulation, the government organisation responsible for grain interventions and ensuring the safety of the state grain fund. The UGC expanded the mandate of the organisation to include the reconstruction and modernisation of grain infrastructure and grain export. It did this by acquiring storage elevators, flour mills, cereal companies, port facilities, and storage and trans-shipment facilities. The accumulated general storage facilities and trans-shipment grain facilities for export made the UGC the company with the largest infrastructure and export facilities on the Russian market (Azarieva 2014). In 2010 the Russian government reformed grain rail transport by creating one large monopoly grain-transport company, Rusagrotrans, which owned nearly all grain railway carriages in the country (Azarieva 2014).

In sum, the Russian state now controls much of the grain storage, transport and export facilities, as well as rail-transport prices and grain-storage prices (through its large role as a purchaser of grain-storage services in private elevators). It has taken an active role in both investing in and attracting private investment for export facilities, as well as infrastructure for grain transport.

In Kazakhstan the State Food Contract Corporation was created in 1995, and was subsequently reorganised in 1997 into a state-owned entity. The purpose of the Corporation was originally to purchase and store the state reserve. However, the mandate of the organisation grew, and the Corporation buys and sells, stores, finances, invests in and exports grain. In 2012 the Corporation was the largest holder of grain in Kazakhstan. Besides the state reserve, the Corporation finances the production of grain, sells it on domestic markets and exports it. In 2009 the Corporation became the largest grain trader in Kazakhstan, buying up 30 % of the wheat harvest. The Corporation is not well liked by farmers in Kazakhstan, primarily because since 2010 each farm with a sown area over 500 ha is obliged to sell 20 % of its harvest to it. Since the Corporation has a so-called counter-cyclical price policy, in 2010 it purchased wheat at lower than market prices (Oshakbaev 2012: 52–53).

In Ukraine the architecture of state involvement in the grain sector is even more complex than in the other two countries; it has a preponderance of state institutions with seemingly overlapping mandates. In 1996 the state joint-stock company Khlib Ukrainy was formed as the successor to the State Central Administration Board for Grain Products and the Central Administration Board for the Mixed Fodder Industry. Khlib Ukrainy was essentially a vast conglomerate of flour mills, storage elevators, grain transport companies and other grain-related infrastructure. The purpose of the conglomerate was to ensure a vehicle to enact state policy in the sector. Until 2005 Khlib Ukrainy was active in purchasing grain for the state, as well as in providing producers and commercial companies with services related to processing, storage, transport and production of grain products for farms and the retail sector. In August 2010 the government of Ukraine established the State Food and Grain Corporation as a successor organization to Khlib Ukrainy, transferring to it the main assets of the latter, such as elevators, mills, grain export and transport facilities. In addition to production, financial, storage, processing, transport and other services, the State Food and Grain Corporation is one of the five largest grain traders in Ukraine, and received a fifth of grain export quotas in 2010/2011 (Kobuta et al. 2012).

The state budget organisation the Agrarian Fund was established in 2005 with the mandate to implement government price regulation in the grain sector and to carry out state interventions on grain markets. However, the tasks assigned to the Agrarian Fund grew over time, extending to forward purchases of grain, grain financing, buying and selling of grain and flour, sugar intervention purchases, and sales of diesel fuel and fertiliser. FAO figures on market price support for wheat during 2005–2010 show that Ukrainian domestic wheat prices were consistently below world prices, meaning that efforts by the government to support wheat prices through the Agrarian Fund seem to have been rather ineffective. Moreover, while the agency was intended to exert control over retail prices for bread and bread products, it was not able to carry out this function either (Kobuta et al. 2012).

A third state-owned operator on grain markets is the State Reserve Agency, charged with purchasing food, including grains, for the state reserve. This mandate overlaps with that of the Agrarian Fund, with the result that uncoordinated actions by the two agencies tend to undermine efforts by the Agrarian Fund to establish minimum prices for grain.

To summarise, the state in RUK has taken a larger and larger role in grain markets through controlling ownership in the ‘commanding heights’ of the grain sector and an ever-expanding mandate for ‘stabilising’ markets through buying, selling, transporting, exporting, storing, processing and producing grain products. However, the consistent, stabilising effects of these interventions are difficult to discern. Rather, the ever-growing role of the state in these markets adds a degree of uncertainty that seems to have far from a stabilising effect.

5.3 The New Protectionism

In 2008, in the wake of a surge of protectionism in the world, G20 leaders publicly committed themselves to creating no new distortions to global commerce. However, citing data from the Global Trade Alert website (www.globaltradealert.org), which chronicles protectionist trade measures by national governments, Evenett (2013) showed that, rather than diminishing, the G20’s resort to protectionism has picked up over time; total protectionist measures in 2012 registered a 23 % increase over 2009. Many of these were of the ‘murky’ variety, such as preferential treatment, loan forgiveness and bailouts. The increase in beggar-thy-neighbour protectionism is not limited to the G20. The same may be said for the governments of the ten next-largest trading nations (as measured by the sum of their total value of annual imports and exports).

The EU-27, Germany, Italy, China, Russia and Kazakhstan have been some of the leading figures in this increased protectionism. Among individual countries, Russia led the list by the number of discriminatory protectionist measures imposed between November 2008 and November 2012. Interestingly, Ukraine did not make the top 10 lists of protectionist countries measured by any of the ranking criteria in Table 7.

The rapid increase in the role of the government in grain markets in RUK, as well as the grain-export restraints, can be understood as a part of this rising wave of protectionism that began in 2007/2008 and has continued since that time. It is symptomatic of this affinity that the leading sector by number of discriminatory measures affecting commercial interests since November 2008 has been agricultural products, horticulture and market gardening (Evenett 2013).

6 Conclusions

The purpose of this chapter has been to explore volatility in the wheat-producing CIS countries in an effort to gauge their past and potential future role in supporting price volatility. We explored two possible sources of price volatility: production and export volatility. It was found that the coefficient of variation for production and export in 2000–2012 was higher in RUK than in other, more traditional, exporters. While production variability can be partly explained by its rapid increase, by low input applications and by a rapid change from less to more volatile yield varieties, the political export restraints seem to be part of a larger politicisation of grain and particularly wheat markets in RUK and of a rising wave of protectionism.

The high fluctuations of yields in RUK are caused by weather variation and other agronomic factors. Thus, they seem to be more of the nature of risk, which has an understandable scientific basis and can be controlled by higher input applications and better agronomic practices, including wider use of low-till agriculture. Political border interventions aimed at limiting grain exports are of a different nature, since they are highly unpredictable. In this respect they are akin to the increased state measures aimed at ‘stabilising’ and exerting state control over grain markets observed in RUK since 2001. Grain export limits may also be understood as part of a new wave of protectionism that can be observed on world markets since 2007/2008. Taken together, these policies do not bode well for the stability of grain prices in the future.

Notes

- 1.

There is a difference between risk and uncertainty. Risk refers to uncertain events, where the distribution of outcomes is known. Uncertainty refers to events for which the distribution of outcomes is unknown and probabilities assigned to events cannot be assigned.

- 2.

Interestingly, however, the excess grain on domestic markets did not stop retail prices for retail grain products from rising. Welton (2011) cited Russian statistics showing that, despite the wheat-export restrictions enacted in 2007, wheat-flour prices rose by 17 % in 2007 and 41 % in 2008. Bread prices rose by 16 % in 2007 and 30 % in 2008. In 2010, despite the grain-export ban, flour prices rose by 18 % from July to December 2010, and bread prices rose by 10 %. Commenting on the differences between food price rises and grain availability, President Medvedev blamed the price increases on speculators (Moscow Times 2010).

- 3.

The coefficient of variation is defined as the standard deviation of a series divided by the mean.

References

Azarieva, J. (2014). Grain and power in Russia 2001–2011. (Doctoral thesis, Hebrew University of Jerusalem, Israel).

Brown, N., Laffan, J., Wight, M. (2008). High food prices, food security and the international trading system, paper presented at the Informal National Food Pricing Summit, Sydney, 29–30 September 2008.

Brümmer, B., Zorya, S. (2005). Wheat/flour price transmission and agricultural policies in Ukraine: A Markov-switching vector error correction approach, paper presented at the 11th Congress of the EAAE (European Association of Agricultural Economists), Copenhagen, Denmark, 23–27 August 2005.

Chapko I, Sedik D (1998) The Ukrainian wheat market in 1997: Poltava oblast case study, CPER Occasional Papers, Iowa State University.

Dollive, K. (2008). The impact of export restraints on rising grain prices, Working Paper No 2008-09-A, US International Trade Commission, Office of Economics. http://www.usitc.gov/publications/332/EC200809A.pdf

Evdokimova, N. (2011). Marketing interventions on the grain market, All-Russian Nikonov Institute of Agrarian Problems and Informatics. http://www.viapi.ru/publication/e-biblio/detail.php?IBLOCK_ID=45&SECTION_ID=1069&ELEMENT_ID=30605

Evenett, S. (2013). What restraint? Five years of G20 pledges on trade, 14th GTA Report, Centre for Economic Policy Research. http://www.globaltradealert.org/sites/default/files/GTA14_0.pdf.

Federal State Statistics Service (Russian Federation). (2009). Agriculture, hunting and forestry in Russia 2009. Moscow: Federal State Statistics Service.

Federal State Statistics Service (Russian Federation). (2011). Agriculture, hunting and forestry in Russia 2011. Moscow: Federal State Statistics Service.

Federal State Statistics Service (Russian Federation). (2013). Agriculture, hunting and forestry in Russia 2013. Moscow: Federal State Statistics Service.

Food and Agriculture Organization of the United Nations fertilizer use database (FAO-FERTISTAT). (2014). http://www.fao.org/ag/agp/fertistat/.

Food and Agriculture Organization of the United Nations statistical database (FAO-FAOSTAT). (2014). http://faostat3.fao.org/home/E.

Food and Agriculture Organization of the United Nations (FAO-GIEWS). (2014). GIEWS country policy monitoring main food-related policy measures (from 1 Jan 2008 to 11 Oct 2011). http://www.fao.org/giews/countrybrief/.

Gotz, L., Glauben, T., & Brummer, B. (2013). Wheat export restrictions and domestic market effects in Russia and Ukraine during the food crisis. Food Policy, 38, 214–226.

Headey, D. (2011). Rethinking the global food crisis: The role of trade shocks. Food Policy, 36, 136–146.

Interstate Statistical Committee of the Commonwealth of Independent States (CISSTAT). (2010). Official statistics of the countries of the Commonwealth of Independent States (2010–15) (CD-ROM).

Kim, J. (2010). Recent trends in export restrictions, OECD Trade Policy Papers, No. 101, OECD Publishing. 10.1787/5kmbjx63sl27-en.

Kobuta, I., Sikachyna, O., & Zhygadlo, V. (2012). Wheat export economy in Ukraine (Vol. Policy Studies on Rural Transition No 2012–4). Budapest: FAO Regional Office for Europe and Central Asia. http://www.fao.org/docrep/017/aq344e/aq344e.pdf.

Moscow Times. (2010, 3 September). Medvedev warns speculators after food prices rise.

OECD/Food and Agriculture Organization of the UN (OECD/FAO). (2015). OECD-FAO agricultural outlook 2015. Paris: OECD Publishing.

Oshakbaev, R. (2012). The grain export economy in Kazakhstan: Wheat export outlook and analysis, Policy Studies on Rural Transition No 2012–6. Budapest: FAO Regional Office for Europe and Central Asia. http://www.fao.org/fileadmin/user_upload/Europe/documents/Publications/Policy_Stdies/Kazakhstan_ru.pdf.

Prakash, A. (2011). Why volatility matters. In: A. Prakash (ed.), Safeguarding food security in volatile global markets. Rome: Food and Agriculture Organization of the United Nations (FAO).

Reynolds, M., Pietragalla, J., & Braun, H. (2008). International symposium on wheat yield potential: Challenges to international wheat breeding. Veracruz El Batan, Mexico: CIMMYT.

Serova, E, (2000). Russia. In: A. Valdes (ed.) Agricultural support policies in transition economies, World Bank Technical Paper No 470, Washington, DC: World Bank. http://www-wds.worldbank.org/servlet/WDSContentServer/WDSP/IB/2000/08/14/000094946_00072405371430/Rendered/PDF/multi_page.pdf.

Sharma, R. (2011). Food export restrictions: Review of the 2007–2010 experience and considerations for disciplining restrictive measures, FAO Commodity and Trade Policy Research Working Paper No 32, Rome. http://www.fao.org/fileadmin/templates/est/PUBLICATIONS/Comm_Working_Papers/EST-WP32.pdf

State Statistics Service of Ukraine. (2010). Application of mineral and organic fertilisers for crops in 2009. Statistical Bulletin, Kiev.

State Statistics Service of Ukraine. (2012). Application of mineral and organic fertilisers for crops in 2011. Statistical Bulletin, Kiev.

State Statistics Service of Ukraine. (2013). Application of mineral and organic fertilisers for crops in 2012. Statistical Bulletin, Kiev

State Statistics Service of Ukraine. (2014). Application of mineral and organic fertilisers for crops in 2013. Statistical Bulletin, Kiev.

Welton, G. (2011). The impact of Russia’s 2010 grain export ban. Oxfam Research Reports, Oxfam International. https://www.oxfam.org/sites/www.oxfam.org/files/rr-impact-russias-grain-export-ban-280611-en.pdf

Wolf, H. (2005). Volatility: Definitions and consequences. In J. Aizenman & B. Pinto (Eds.), Managing economic volatility and crises: A practitioner’s guide. Cambridge: Cambridge University Press.

World Bank. (2008). Competitive agriculture or state control: Ukraine’s response to the global food crisis, Europe and Central Asia Region, Sustainable Development Unit Report No 44984-UA, World Bank. http://siteresources.worldbank.org/INTUKRAINE/Resources/WorldFoodCrisisandRoleofUkraine.pdf

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Sedik, D. (2017). The New Wheat Exporters of Eurasia and Volatility. In: Gomez y Paloma, S., Mary, S., Langrell, S., Ciaian, P. (eds) The Eurasian Wheat Belt and Food Security. Springer, Cham. https://doi.org/10.1007/978-3-319-33239-0_8

Download citation

DOI: https://doi.org/10.1007/978-3-319-33239-0_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-33238-3

Online ISBN: 978-3-319-33239-0

eBook Packages: Economics and FinanceEconomics and Finance (R0)