Abstract

This chapter contributes to the OCA endogeneity hypothesis and emphasises the EU countries’ changes in economic growth related to the main milestones of the European Integration Process. Our multiple-steady-state approach substitutes for capital thresholds by euro adoption. Thus, we suppose two specific steady states for two groups of countries: (1) euro member states; and (2) non-member states. We discuss continuously increasing heterogeneity over the long-run in single-currency regimes and identify the limits of single-policy and regulatory-framework efficiency. Moreover, the single regulatory framework causes excessive restrictions in the countries with lower productivity and capital formation and simultaneously, weak regulation in countries with higher levels of potential growth. Consequently, the negative effects of excessive restrictions are not balanced by expansionary policy because over the long term, economic growth is much more sensitive to restrictions. Finally we conclude that heterogeneity undermines the potential economic growth in Europe as a whole.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

From a theoretical perspective, a currency union can be expected to increase trade and financial integration primarily due decreased transaction costs and exchange rate risks. Both of these factors should sustain long-term productivity and economic growth. The first authors to empirically verify this hypothesis are Rose and Engels (2002). They examine the criteria for Mundell’s concept of an optimum currency area and find that members of currency unions are more integrated than countries with their own currencies. They apply the two-state approach and data for more than 200 countries and quantify the impact of a single currency for trade and output. They concluded that the use of a single currency significantly boosts international trade. More specifically, their estimations suggest that a one percent increase in trade raises income per capita by approximately 1/3 of 1 % over a 20-year period. For example, Poland’s decision to join the euro zone will result in an income increased as high as 20 % over 20 years. Many other empirical studies have reacted to these controversial results (Rose and van Wincoop 2001 or Glick and Rose 2002). In 2005, Rose and Stanley conducted a meta-analysis of the effect of common currencies on international trade (Rose and Stanley 2005). Based on 34 empirical studies, they rejected the hypothesis that a currency union has no effect on trade and concluded that a single currency (i.e., a currency union) increases bilateral trade by between 30 and 90 %.

Conversely, many recent studies discuss the fact that European productivity growth has decelerated since the 1990s, whereas American productivity growth has accelerated. Aiginger (2013) notes that the main reasons for the different development of the European countries and the U.S. relate to energy costs (the U.S.’s energy prices are 2/3 lower) and labour costs (the U.S. has a 1/3 advantage in labour costs). Timmer et al. (2011) argues that the primary cause of the European slowdown is the productivity slowdown in traditional manufacturing and other goods production combined with the concomitant failure to invest in and reap the benefits from information and communications technology and market services. The U.S.’s productivity growth from market services is also confirmed by both Jorgenson and Vu (2005) and Triplett and Bosworth (2006). Working hours per capita are very low in the European Union compared to the U.S. (Eichengreen 2007). Blanchard (2004) argues that the difference between the working hours is caused by a trade-off between preferences for leisure and work. Prescott (2004) shows that income taxes correlate to Europe and the U.S.’s different labour participation rates.

Clearly, slowdown in the total factor of productivity, high labour costs and energetic dependency plays a fundamental role in the economic growth of Europe as a whole. Furthermore, there are large asymmetries among the regions and countries within the Eurozone. Timmer et al. (2011) argues that the primary difference in labour productivity growth among the individual European economies is to be found in multi-factor productivity, not in differences in the use of capital per hour worked. Timmer and van Ark (2005) also show that the differences in productivity are larger than differences in factor inputs. They generally note that Europe’s productivity slowdown is primarily driven by the indebted countries (e.g., Spain, Italy and Greece), whereas the Nordic economies are prospering in terms of productivity. The differences between the Nordic and Southern countries with respect to the amount of capital contributed to information and communication technologies are also shown in Timmer et al. (2011). However, the primary difference amongst the European countries lies in their residents’ consumption behaviour.

Compared to the above asymmetric causes on the supply side of the economy, there are much more significant determinants of asymmetric behaviour on the demand side. The key point on the demand side relates to differences in the economic fundamentals that determine money demand (Bosker 2003 or Setzer and Wolff 2009). Following endogenous theories of money, asymmetric investment and economic activity implies credit money creation and heterogeneous distribution of money supply across the Eurozone despite its common monetary policy and common money market (Poměnková and Kapounek 2013). Finally, asymmetric money demand and investment activity implies asymmetries in individuals’ behaviour and causes asymmetries in their consumption expenditures. Moreover, fiscal policies (which could theoretically reduce asymmetries) in practice have been pro-cyclical and have increased asymmetries (Darvas et al. 2005).

What is the effect of the single currency and the European integration process? Traditionally, the theoretical answer to this question cites endogeneity and the specialisation hypothesis (Frankel and Rose 1997). Frankel and Rose (1997) argue that increased trade in a common currency area leads to industrial specialisation among regions in the goods for which they have a comparative advantage. The authors who contribute to this discussion include both Krugman (1993) and Bayoumi and Eichengreen (1992, 1996). The wide-ranging discussions on this issue are summarised in Krugman’s specialisation effect, which is said to lead to economies’ divergence. Subsequently, Horváth and Komárek (2002, pp. 16) argue that ‘the problem with Krugman’s view is that it implicitly assumes that regional concentration of industry will not cross the borders of the countries that formed the union, while borders will be less relevant in influencing the shape of these concentration effects.’ If that is true, then autonomous monetary policy is an inefficient method of stabilising asymmetric shocks within a currency union, which could be relatively closed to the outside world. The empirical perspective on this issue is provided by Landesmann (2003), who identifies significant differentiation across regions and countries in both Central and East Europe related to both industrial ‘up-grading’ and remaining ‘locked into’ low-skill production areas. Finally, Landesmann (2003) proposes that regional differentiation constitutes a substantial challenge for cohesion policies. However, according to recent empirical evidence, the effects of single currency and structural reforms are not entirely clear because political resistance to reforms and adjustment can both expand and limit the relevant instruments (Matthes 2009).

We adopt the assumption that a single currency provides an institutional advantage that has a direct impact on potential output. We follow the empirical foundations of growth econometrics provided by Durlauf et al. (2005), especially his assumption of the capital thresholds that divide two groups of countries. In our theoretical model, we substitute the capital thresholds by the institutional factor (single currency adoption).

Duval and Elmeskov (2006), pp. 31 note that ‘European countries have widely different starting points as regards structural policy settings and therefore different needs in terms of reform. As well, even similar structural reforms may well have different supply and demand-side effects across countries—in part because reform will interact with pre-existing institutions and structural policy settings—which would make the overall effect on area-wide inflation and demand-pressure hard to predict and to factor into monetary policy.’ We assume that two groups of countries obey separate growth regimes (Durlauf et al. 2005). Simultaneously, their thresholds are provided by currency union membership and all other related institutional determinants. Finally, we focus on the specific monetary issues that arose during the European integration process and their impact on asymmetries. Two groups of countries desire a specific monetary policy and financial regulation. We argue that the common character of monetary policy framework and regulation has a negative impact not only on long-term economic performance but also on potential output.

1 Brief Review on Optimum Currency Area Theory

The European integration process is theoretically supported by optimum currency area (OCA) theory, which originates from debates about fixed versus flexible exchange rates, treating a common currency as the extreme case of a fixed exchange rate. A system of fixed exchange rate, applied through the gold standard mechanism, was blamed by many economists for the post-1929 world-wide depression. Mundell (1961) begins with the simple idea that flexible exchange rates are based on regional currencies, not national currencies, if macroeconomic shocks affect regions differently. However, an economy with a fixed exchange-rate regime does not have monetary policy independence because the disparity of interest rates among reasons will lead to unsustainable balance of payment imbalances. Within the fixed exchange-rate region, market-based adjustment mechanisms must be applied to cope with asymmetric shocks/factor mobility. Inspired by Keynes and his price and wage rigidities assumptions, Mundell argues that if there is a high degree of labour mobility within a region, then its member states should employ a fixed exchange rate amongst themselves and a flexible exchange rate against the rest of the world.

The key issue in OCA theory is that of macroeconomic policy efficiency in an open economy. McKinnon (1963) supports OCA theory assumptions and argues that currency devaluation is ineffective in very open economies because prices and wages immediately increase. A large currency area is less open than its member countries and therefore, the efficiency of its exchange rate policy increases. In contrast to Mundell, McKinnon not only distinguishes labour mobility among regions but also focuses on inter-industrial immobility. Labour mobility among industries reduces factor movement between regions. Consequently, the effects of adjustment mechanisms to prevent drops in income vanish. Kenen (1969) further develops this effect and argues that regions are defined not by their geography or by their politics, but by their activities. He assumes that perfect inter-regional labour mobility requires perfect occupational mobility, which can only come about when labour is homogenous. Based on the same assumption, OCA member states should display very similar skill requirements. In this context, structural synchronisation is an important condition of OCA, thus affecting the efficiency of a market-based adjustment mechanism.

Kenen (1969) assumes that diversified economies with inter-industrial mobility are good candidates to join OCA because diversification helps them to adjust rapidly to negative external shocks. A diversified economy with a diversified export sector is more stable if those shocks are uncorrelated. Krugman (1993) notes that economic integration leads to regionally concentrated industries (e.g., automobile plants in Michigan). Subsequently, regionally concentrated industries could lead to asymmetric shocks within a currency region.

The traditional version of OCA theory is supplemented by Corden (1972), who argues that joining a currency area is related to a loss of control over monetary policy and exchange rates. These arguments followed by new theoretical development of OCA that focuses more on the benefits and costs of adopting a common currency. On the basis of the theoretical principles, the costs are minimised and benefits maximised with high degrees of cyclical and structural synchronisation.

In summary, we suppose that the benefits of joining a currency union provide an institutional advantage that increases total-factor productivity and long-term output. According to the endogeneity hypothesis (Frankel and Rose 1998), the benefits will be maximised ex post.

However, Imbs et al. (2011) show that the European integration process was accompanied by dynamic evolution of structural changes in sectoral production, which led to geographically dispersed activity. In the peripheral countries (mostly in Southern and Eastern Europe) sectoral diversification led to agglomeration, heterogeneous regions and integration processes that had different impacts at the national and regional levels. Conversely, in the core member states (mostly in Western Europe), sectoral specialisation led to diversification because the regions integrated with each other based on each region’s comparative advantages.

2 Multiple-Steady-State Growth Model

The theoretical multiple-steady-state model assumes that there are heterogeneous sets of countries that obey separate growth regimes. The model is a variant of the Solow model of economic growth with threshold non-convexities in institutional factors provided by the single currency. The key question is whether multiple steady states exist. If so, the system has two steady states (two equilibria) to which economies tend. In the original assumption provided by Durlauf et al. (2005), the threshold k T is given by different capital stocks. According to his assumption, the solid curve represents multiple steady states and dashed curve nonlinearities (Fig. 1).

Non-linearity vs. multiple steady states

Our multiple-steady-state approach explains the long-term economic growth between euro member states and non-member states (solid curve). In that case, we can expect a single-currency regime to result in continuously increasing heterogeneity over the long term. Conversely, if the economies do not tend to the different steady states, there is nonlinearity in the growth process (dashed line) and over the long term, countries will converge to a single steady state.

3 Empirical Evidence

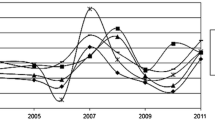

The identification problem is conditioned by insufficient observations that would allow one to distinguish the differences in the long-run behaviour of the countries that start with capital stocks at k T. Figure 2 describes the evolution of the European integration process divided into the three sub-sample periods. The crosses represent the core euro area member countries (Belgium, Germany, Spain, France, Italy, Netherlands, Austria, Portugal and Finland). The rest of the countries are the current EU Member States that had not adopted single currency by the year 1999: Bulgaria, Czech Republic, Denmark, Estonia, Greece, Croatia, Cyprus, Latvia, Lithuania, Hungary, Malta, Poland, Romania, Slovenia, Slovakia, Sweden and United Kingdom. Ireland, Luxembourg and Malta were excluded due to outliers and structural breaks. Data series (GDP and gross fixed capital formation) are averages of EUR per capita in 2005 prices.

Evolution of the European integration process (Eurostat)

The first period represents the period between the common market and currency union stages (1990–1999). GDP per capital exceeds 10,000 euros in all of the euro-area countries, including Cyprus, United Kingdom, Sweden and Denmark. However, there are no substantial non-linearities and multiple-steady states in the figure. Conversely, in the second period we can distinguish among three groups of countries. The first group is represented by GDP per capita of more than 20,000 euros and gross capital formation per capita that exceeds 3.5,000. The group is composed of all of the core euro area member countries (except Portugal), Denmark, Sweden and United Kingdom. The second cluster is composed of Portugal, Slovenia, Greece and Cyprus. The third cluster is composed of the rest of the EU member countries.

Thus, following single-currency adoption (between 2000 and 2007) we can distinguish three groups of countries that tend towards three steady states. This period was typical of the credit-boom bust cycle in the most of the new EU Member States. Rapid credit growth and a high level of liquidity in the global markets were followed by the particular attractiveness of “new Europe” for capital flows. The lending boom was associated with the excessive consumption growth that resulted in vulnerabilities during the financial crisis, especially in the CEECs. After 2007, growth forecasts for CEECs (especially for private consumption) were significantly revised downward. Consequently, several CEECs allowed their currencies to depreciate massively so that they could improve competitiveness and cope with both capital flight and sudden stops of capital inflows. The vulnerabilities that accumulated during the pre-crisis period were further increased by adverse income shocks, leading to reforms in the European supervisory architecture.

Liquidity and solvency shocks during the crisis contributed to changes in output across Europe. The European recession affected growth through three different channels: capital accumulation, labour input and total factor productivity (Halmai and Vásáry 2012). The same results are presented in Fig. 2. Although the gross fixed capital formation and GDP per capital increased in Sweden, Finland, Germany and Belgium, most other countries experienced decline.

Finally, following the financial crisis (2008–2013) we can identify two steady states.Footnote 1 The first group is composed of the core euro-area countries (Belgium, Germany, Spain, France, Italy, Netherlands, Austria, Finland), United Kingdom, Sweden and Denmark. The second group is composed of Bulgaria, Czech Republic, Estonia, Greece, Cyprus, Latvia, Lithuania, Hungary, Poland, Romania, Slovenia, Slovakia, Portugal, Greece and Cyprus. In relation to our theoretical background, we can note that three countries that grouped during 2000–2007 (Portugal, Slovenia, Greece and Cyprus) changed their steady states to approach those of the other peripheral countries.

4 Policy Implications

The traditional debates about the heterogeneous transmission mechanisms for both real and monetary shocks began immediately after the introduction of a common currency in the euro area (Eijffinger and de Haan 2000 or Mihov 2001). A wide range of literature focuses on institutional, financial, consumption and housing heterogeneity and its impact on the efficiency of monetary policy in the currency area. However, recent theoretical and empirical papers seek to identify the optimal EU-level governance structure and especially whether and which macro-prudential regulatory framework is efficient in the heterogeneous currency union. The theoretical framework for internationally co-ordinated regulation supplies arguments for the need not only to maintain the field for competition but also to avoid regulatory races to the bottom (Jeanne 2014). However, the key issue is that the assumed heterogeneity implies that regulation at the international (EU) level may have to be restricted to a few countries and not implemented across the entire currency area. Moreover, the limited efficiency of monetary stabilisation tools at the EU level is emphasised by national budgets’ fiscal capacities and their pro-cyclical effects.

According to the theoretical discussion and empirical results, we can conclude that Europe’s heterogeneity will increase due to the existence of multiple steady states. If so, the single regulatory framework will cause heterogeneous levels of restriction in different countries. Excessive restrictions will negatively affect long-run economic growth, especially in countries with lower productivity and capital formation. Conversely, these negative effects will not be sufficiently balanced by weak regulation in the countries with a higher level of potential growth. In summary, over the long term, economic growth is much more sensitive to restrictions. Thus, the centralisation of monetary policy, especially with respect to the regulatory framework, could undermine potential economic growth across Europe.

The assumption of Europe’s heterogeneity is adopted by many empirical and theoretical models. Schoenmaker (2013) differentiates between a centralised model, in which the ECB controls policy instruments and national monetary and regulatory authorities provide recommendations according to local conditions, and a de-centralised model, in which the ECB provide the overall policy framework and national monetary authorities control instruments. Rubio (2014) proposes a Taylor-type rule for loan-to-value ratios and distinguishes among four types of asymmetries: (1) non-synchronised business cycles; (2) financial accelerator effects; (3) differences in borrowers’ labour income shares; and (4) asymmetries in the variable and fixed rates of mortgages.

In summary, key issues and questions addressed in the conceptual frameworks include which instruments follow the heterogeneous currency union appropriately and how to implement these instruments at the national and EU levels in accordance with their efficiency and efficacy.

5 Summary

The chapter provides theoretical evidence of the growing heterogeneity of economic growth among the EU Member States over the long term and discusses the appropriateness of the single monetary policy framework with respect to recent changes in the EU’s regulatory architecture. The traditional theoretical background is represented by the OCA theory. Our contribution is to substitute the institutional factor (i.e., single-currency adoption) for capital thresholds in the theoretical multiple steady-state model.

The effects of the single currency and the European integration process were discussed in the context of traditional endogeneity and the specialisation hypothesis. We discussed sectoral diversification and agglomeration to show that the core euro-area member countries tend to different steady states than do peripheral countries.

Finally, we showed that the single currency provides the institutional advantage that increases total-factor productivity and output over the long term. However, the benefits of a single currency are utilised differently by different European countries. In the future, therefore, the policy framework should adapt its instruments to the heterogeneous currency union and combine monetary and other authorities at the national and EU levels.

Notes

- 1.

Following our theoretical background and detailed analysis of growth components, there is a potential for a third steady state, which distinguish core euro-area countries into two groups.

References

Aiginger K (2013) The necessity and feasibility of a new growth path for Europe. OECD Eco Seminar, Paris, 20 June 2013

Bayoumi T, Eichengreen B (1992) Shocking aspects of monetary unification. NBER working paper, no. 3949

Bayoumi T, Eichengreen B (1996) Ever closer to heaven? An optimum-currency-area index for European countries. Center for International and Development Economics Research (CIDER) working papers C96–078, University of California at Berkeley

Blanchard OJ (2004) The economic future of Europe. J Econ Perspect 18(4):3–26

Bosker EM (2003) Eurozone money demand: time series and dynamic panel results. De Nederlandische Bank working paper, No. 750

Corden W (1972) Monetary integration, essays in international finance. International Finance Section, No. 93, Princeton University

Darvas Z, Rose AK, Szapary G (2005) Fiscal divergence and business cycle synchronization: irresponsibility is idiosyncratic. NBER working paper, no. 11580

Durlauf SN, Johnson PA, Temple JRW (2005) Growth econometrics. In: Aghion P, Durlauf S (eds) Handbook of economic growth, vol 1, 1st edn. Elsevier, Amsterdam, pp 555–677

Duval CFR, Elmeskov J (2006) The effects of EMU on structural reforms in labour and product markets. ECB working paper, no. 596

Eichengreen B (2007) The European economy since 1945: coordinated capitalism and beyond. Princeton University Press, Princeton

Eijffinger S, de Haan J (2000) European monetary and fiscal policy. Oxford University Press, Oxford

Frankel JA, Rose AK (1997) Economic structure and the decision to adopt a common currency.Seminar Papers 611, Stockholm University, Institute for International Economic Studies

Frankel JA, Rose AK (1998) The endogeneity of the optimum currency area criteria. Econ J R Econ Soc 108(449):1009–1025

Glick R, Rose AK (2002) Does a currency union affect trade? The time-series evidence. Eur Econ Rev 46(6):1125–1151

Halmai P, Vásáry V (2012) Growth crisis in the main groups of the EU member states comparative analysis. IWH Halle discussion paper

Horváth R, Komárek L (2002) Theory of optimum currency areas: a framework on discussion about monetary integration. Czech J Econ Finance 52(7–8):386–407

Imbs J, Wacziarg R, Montenegro C (2011) Economic integration and structural change [presentation]. 5 Oct 2011. World Bank [online] Available at: http://witer-esources.worldbank.org. Accessed 15 Apr 2014

Jeanne O (2014) Macroprudential policies in a global perspective. NBER working paper no. 19967, Mar 2014

Jorgenson DW, Vu K (2005) Information technology and the world economy. Scand J Econ 107(4):631–650

Kenen P (1969) The theory of optimum currency areas: an eclectic view. In: Mundell RA, Swoboda AK (eds) Monetary problems in the international economy. University of Chicago Press, Chicago

Krugman P (1993) Lessons of Massachusetts for EMU. In: Giavazzi F, Torres F (eds) Adjustment and growth in the European Monetary Union. Cambridge University Press, New York, pp 241–261

Landesmann M (2003) The CEECs in an enlarged Europe: patterns of structural change and catching-up. In: Handler H (ed) Structural reforms in the candidate countries and the European Union, Austrian Ministry for Economic Affairs and Labour. Economic Policy Center, Vienna

Matthes J (2009) Ten years EMU – reality test for the OCA endogeneity hypothesis, economic divergences and future challenges. Intereconomics 44(2):114–128

McKinnon R (1963) Optimum currency area. Am Econ Rev 53(4):717–725

Mihov I (2001) Monetary policy implementation and transmission in the European monetary union, economic policy: a European forum, vol 33, pp 396–402, Oct 2001

Mundell RA (1961) A theory of optimum currency areas. Am Econ Rev 51(4):657–665

Poměnková J, Kapounek S (2013) heterogeneous distribution of money supply across the Euro area. In: Proceedings of the 10th international scientific conference: economic policy in the European union member countries: selected papers, pp 268–279

Prescott EC (2004) Why do Americans work so much more than Europeans? Fed Reserv Bank Minn Q Rev 28:2–13

Rose AK, Engel C (2002) Currency unions and international integration. J Money Credit Bank 34(4):1067–1089

Rose AK, Stanley TD (2005) A meta-analysis of the effect of common currencies on international trade. J Econ Surv 19(3):347–365

Rose AK, van Wincoop E (2001) National money as a barrier to international trade: the real case for currency union. Am Econ Rev 91(2):386–390

Rubio M (2014) Macroprudential policy implementation in a heterogeneous monetary union. Centre for Finance, Credit and Macroeconomics, University of Nottingham, Working paper 14/03

Schoenmaker D (2013) An integrated framework for the banking union: don’t forget macro-prudential supervision. Economic papers, No. 495, European Commission

Setzer R, Wolff GB (2009) Money demand in the euro area: new insights from disaggregated data. DG ECFIN economic papers, No. 373

Timmer MP, van Ark B (2005) Does information and communication technology drive EU-US productivity growth differentials? Oxf Econ Pap 57(4):693–716

Timmer MP, Inklaar R, O’Mahony M, van Ark B (2011) Productivity and economic growth in Europe: a comparative industry perspective. International Productivity Monitor, Centre for the Study of Living Standards, vol 21, pp 3–23

Triplett JE, Bosworth BP (2006) Baumlo’s disease has been cured: IT and multi-factor productivity in U.S. service industries. In: Jansen DW (ed) The new economy and beyond: past, present, and future. Edward Elgar, Cheltenham, pp 34–71

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Kapounek, S. (2016). Long-Run Heterogeneity Across the EU Countries. In: Huber, P., Nerudová, D., Rozmahel, P. (eds) Competitiveness, Social Inclusion and Sustainability in a Diverse European Union. Springer, Cham. https://doi.org/10.1007/978-3-319-17299-6_3

Download citation

DOI: https://doi.org/10.1007/978-3-319-17299-6_3

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-17298-9

Online ISBN: 978-3-319-17299-6

eBook Packages: Economics and FinanceEconomics and Finance (R0)