Abstract

It is interesting to observe that artificial intelligence is gaining popularity in both developing and developed countries as it attracted the interest of accounting, business, and management professionals. This necessitates the need to scrutinise the interaction between artificial intelligence and money laundering. There is an ongoing debate concerning the justifications of artificial intelligence in dealing with money laundering. In this regard, the Southern Africa region is no exception to money laundering just like any other region. As such, the application of artificial intelligence appears to be a rational strategy to curb financial leakages in the finance sector. Although there is an increase in the adoption of artificial intelligence, scanty is known concerning the association between the application of artificial intelligence and money laundering, especially in the Southern Africa region. In this respect, this research aims to provide the effects of artificial intelligence on money laundering in the Southern African region. The study adopted the structured literature review methodology and then six positive effects were observed. These are detecting money laundering activities, enhancing legal compliance, augmenting customer behavioural analytics, detecting money laundering networks, robust financial crime risk computation, and informing evidence-based policy formulation. However, the negative effects are in the form of infringing customer privacy rights, and poor data governance. Despite the existence of few negative effects, it is concluded that artificial intelligence helps to combat money laundering in the Southern African region. As such, it is suggested that financial institutions should up-skill their personnel and up-scale their business intelligence projects.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Recently, the cases of money laundering are increasing exponentially, and other crimes related to finance are growing worldwide. It is an open secret that the techniques and tools used by financial criminals to evade their detection are considered to be more sophisticated than before (Alexandre & Balsa, 2023; Meiryani et al., 2023; Singh & Lin, 2021). As such, many financial and government institutions are heavily investing in advanced technology so as to deal with financial crimes effectively and efficiently like money laundering. This implies that governments and banks are at the forefront when it comes to curbing money laundering programmes. In this regard, advancement in machine learning is widely accepted as a powerful tool to institutionalise anti-money laundering programmes (Pavlidis, 2023). This heightens the need for artificial intelligence adoption by financial institutions across the world.

Globally, the adoption of machine learning as a form of artificial intelligence helps governments and financial institutions to monitor financial transactions in an effort to detect suspicious transactions. A combination of advanced algorithms and machine learning helps financial institutions to effectively monitor money laundering transactions in real-time (Stears & Deeks, 2023; Xia et al., 2022). Traditionally, financial institutions used expert judgment, elementary statistical indicators, and red flags as techniques to detect suspicious financial transactions. Nonetheless, these tools are longer efficient and effective in the twenty-first century as they cannot capture advanced trends in money-laundering behaviours. With this in mind, it appears that machine learning helps banks to build a more granular and sophisticated algorithm to detect money laundering activities (Weber et al., 2023). Nevertheless, it requires massive investment in advanced technologies in the financial sector.

Going forward, combating money laundering is the greatest challenge of the twenty-first century when it comes to the financial sector. Most financial institutions employ manual and repetitive tasks that cannot efficiently and effectively combat advanced money laundering activities. Given the high volume and velocity of financial data, artificial intelligence capabilities are the need of the hour in trying to reduce money laundering activities across the globe (Couchoro et al., 2021; Meiryani et al., 2023). In spite of the essence of artificial intelligence, it is of paramount importance to assess how artificial intelligence applications can reduce money laundering. Moreover, there is an ongoing debate related to how artificial intelligence can replace human synthesis and human decision-making processes (Alexandre & Balsa, 2023; Xia et al., 2022). In this regard, one may argue that a hybrid approach towards money laundering appears to be a better option. A hybrid approach to combating money laundering involves the use of both artificial intelligence applications, and human processes and insights. This suggests that the deployment of artificial intelligence programmes or humans in isolation cannot drive the best outcomes when it comes to combating money laundering.

In light of the above, money laundering activities range from 2% to 5% of the global Gross Domestic Product (GDP) (Craig, 2019). In trying to arrest money laundering activities, it must be noted that the adoption of artificial intelligence applications comes with costs. In this sense, artificial intelligence programmes require large sums of money in terms of sourcing applications and training human resources. However, artificial intelligence adoption can drive operational efficiency in fighting against money laundering (Searle et al., 2022). This implies that costs related to customer screening, transaction monitoring, and customer due diligence can be significantly reduced by adopting artificial intelligence in the financial service.

In the context of Africa, many African countries experienced a great challenge of money laundering in the past three decades as they mainly rely on cash transactions and weak legal institutions (Couchoro et al., 2021). Moreover, it is a mammoth task for the African governments owing to the deregulation of the financial sectors (Latif, 2022). It is within this that Issah et al. (2022) argued that African countries lose US$50 billion per year related to money laundering. In trying to curb money laundering, South Africa adopted the first money laundering legislation in 1992 to deal with proceeds from the Drugs and Drug Trafficking Act 140 of 1992. In 2001, it adopted the Financial Intelligence Centre (Chitimira & Warikandwa, 2023). It is well-documented that before 1998 South African financial institutions were poorly regulated when it comes to money laundering activities (Chitimira, 2021). More interestingly, the non-profit sector of South Africa is exposed to economic crimes like terrorist financing and money laundering (Bissett et al., 2023).

The government of Zimbabwe appears to be struggling to adhere to international measures to deal with money laundering and terrorism financing. In early 2020, Pretoria Portland Cement Limited, Old Mutual, and Seed Co. International were investigated for activities related to money laundering in fungible stocks (Chitimira & Ncube, 2021). Despite the availability of various money laundering cases, much less is known about money laundering in Southern and Eastern Africa (Basel Institute on Governance, 2020; Goredema, 2004; Issah et al., 2022). More worryingly, an interaction between artificial intelligence and money laundering is under-researched in Southern Africa. Against these knowledge gaps, the main objective of this study is to establish the effects of artificial intelligence on money laundering in Southern Africa.

The remained parts of this paper are structured as follows: the second section covers the conceptualisation of money laundering and artificial intelligence. The third section covers the structured literature review methodology whereby the search strategy and the process of doing a structured review are reported. In the fourth section, issues related to the results of the current study are reported. Notably, a discussion of the results is also provided. The fifth section covers the implications of the study. Lastly, issues surrounding the areas for further research are presented in detail.

1.1 Conceptualisation of Money Laundering

It is a fact that there is no standard definition of money laundering in the current literature. This situation has been brought about by the existence of various scholars who defined money laundering from different perspectives. In this regard, some authors defined money laundering from financial, economic, and legal perspectives. Generally, money laundering is defined as cunning efforts to disguise the origin of crime proceeds (Zondo, 2022). Notably, the legal perspective of conceptualising money laundering dominates other perspectives such as financial and economic perspectives. From a legal perspective, money laundering refers to “transferring illegally obtained money through legitimate people or accounts so that its original source cannot be traced” (Han et al., 2020, p. 212).

1.2 Anti-Money Laundering Policies

Anti-money laundering can be defined as regulations, laws, and procedures designed to prevent criminals from cleaning illegal or dirty funds to be legitimate income. There are various anti-money laundering policies such as rule-based policy, risk-based policy, enforcement and detection, and general data protection regulation (Xia et al., 2022). Firstly, the rule-based policy deal with the framework designed to prevent, detect, and suppress illicit financing. The principles of the rule-based policy are transparent and clear policies that can be easily adopted by financial institutions as a way to ensure compliance. These rules are used to detect suspicious financial behaviour. However, the high level of transparency of such rules makes it very easy to bypass. Secondly, a risk-based policy allows the financial institution more discretion concerning what to report. This means they are responsible for reporting which can lead to over-reporting or under-reporting. As such, financial institutions are free to assess transaction risks and client risks by detecting outlier behaviour. Thirdly, enforcement and detection deal with making money laundering a criminal act. This means that different countries may have different law enforcement methods given that we do not have a “one-size-fits-all” approach to enforcement. Some of the commonly used methods include sanctions, demanding transparency from financial institutions, exports and imports monitoring, filing of financial statements, blacklisting suspicious countries and individuals as well as institutions, prison sentences, fines, and penalties. Fourthly, general data protection regulation addresses the issues related to data ownership, data processing, ethical compliance, and explanatory frameworks for the data and algorithms.

1.3 Money Laundering Stages

In the existing money laundering literature, three phases have been identified which can be used to explain the money laundering process. These three phases are placement, layering, and integration. Firstly, the placement phase is whereby the revenue from illegal or criminal activities is converted into financial instruments, or the cash is deposited in a financial institution. Secondly, the layering phase is whereby the funds from illegal activities are transferred to a network of individual or financial institutions via cheques, wire transfers, money orders, and other techniques. The money launders have the robust capabilities and competencies of utilising advanced technology like electronic payments, online banking, and cryptocurrencies to move dirty cash across the world (Bissett et al., 2023). Thirdly, the integration phase is whereby legitimate assets and properties are being purchased using funds from illegal activities. Integration can also be in the form of continuous financing of criminalised entities. At this final phase of money laundering, illegitimate money becomes part and parcel of the legitimate economy.

1.4 Money Laundering in Southern Africa

It is an open secret that the Southern African countries are not immune to money laundering just like other countries across the globe. African countries in Southern Africa are listed as causing significant threats when it comes to money laundering like Botswana, Zimbabwe, and Mauritius (Issah et al., 2022). South Africa is also facing difficulties in dealing with money laundering given that the money launders are well-connected with high-profile individuals. In this regard, Madonsela (2019, p. 123) documented that “the Gupta leaks revealed that between August and September 2013, an amount of R84 million was transferred to a Gupta-owned company, Gate Way Limited, in Dubai. Dubai was a money laundering shop. However, the money immediately left the account again. The items billed by Linkway amounted to R30 million. By 23 September, all of the Free State’s money was washed and delivered to the Guptas in South Africa”. This implies that South African money launders are dealing with people outside the country, especially Dubai. Moreover, the Gupta investigation revealed that the “Guptas moved the proceeds of their business through their shell company called Homix. Shell companies provide the owner with anonymity and are a classical vehicle for money laundering and other illicit financial activities. The term ‘shell company’ generally refers to limited liability companies and other business initiatives with no significant assets or ongoing business activities” (Madonsela, 2019, p. 123). Notably, it has been reported that the Gupta family was also dealing with some public enterprises such as Eskom. Moreover, it was reported that “Bank of Baroda not only failed to report the highly suspicious activities on the Guptas and their associates’ bank accounts but enabled the Guptas to perpetuate their unlawful activities of money laundering” (Zondo, 2022, p. 841). In trying to deal with money laundering, the government managed to set aside ZAR265.3 million for the Financial Intelligence Center to update the anti-money laundering infrastructure.

Following the implementation of the Mutual Evaluation Report (MER), Zimbabwe made some amendments to the Money Laundering and Proceeds of Crime Act and began to execute risk-based supervision frameworks. More interestingly, the Financial Intelligence Unit was also established in Zimbabwe by the Reserve Bank of Zimbabwe. Put simply, the anti-money laundering frameworks in the Zimbabwean context are established through the Money Laundering and Proceeds of Crime Act of Chapter 9:24. This legal framework was amended in 2020. It now gives the government the right to identify, trace, freeze, seize, and eventually confiscate unlawful proceeds from all crimes and acts of terrorism. Interestingly, the Reserve Bank of Zimbabwe, through the Financial Intelligence Unit, works closely with Zimbabwe Revenue Authority (ZIMRA) in combating money laundering in the country when it comes to exports and imports business transactions.

Despite the existence of legal frameworks to deal with money laundering in Zimbabwe, it is discouraging to mention that it appears to be struggling to adhere to international measures related to anti-money laundering and terrorism financing. This is substantiated by skyrocketing money laundering crimes in the Zimbabwean financial sector. For instance, in mid-2020, Ecocash was placed under investigation when it created a fake mobile money platform that allow purchasing of foreign currency on the black market (Chitimira & Ncube, 2021). This implies that the customer’s due diligence was not properly done since some customers were using fake identity documents which led to fake mobile money accounts.

1.5 Artificial Intelligence and Money Laundering

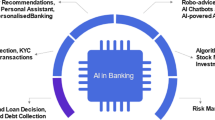

In a quest to combat money laundering, it appears that artificial intelligence in the financial sector can play a paramount role given that advanced technology is reshaping the contemporary business world. With this in mind, it is not surprising to note that artificial intelligence models and approaches can be utilised in the Know Your Customer and Customer Due Diligence processes. The advanced models can allow bankers to detect suspicious businesses through outlier detection software. Consequently, customer behaviour can be monitored automatically as shown by the diagram;

As illustrated in Fig. 1, artificial intelligence approaches can be utilised in determining risk scores and client characteristics. In this respect, robust customer profiling can be ensured by applying artificial intelligence tools in trying to establish the internal people, and external profile, validate Know Your Customer, adverse media, and product holdings. Moreover, the application of artificial intelligence gives room for managers to determine the customer or client links such as known account links, legal entity links, common counterparts, and social networks. Going forward, as indicated in Fig. 1, artificial intelligence in the context of Know Your Customer can allow financial institutions to establish customer activities. These activities can be customer transactions, peer activities, device activity, and profile changes. On the aspect of intelligence, financial institutions can ascertain and scrutinise alerts, screening hits, overrides, cyber, and fraud. In light of the above analysis, it is clear that the application of artificial intelligence models can allow financial institutions to have a deeper understanding of their customer’s behaviour over a given period of time.

Integration between Know Your Customer and artificial intelligence. Source: Craig (2019)

Artificial intelligence can be applied to various stages of money laundering, that is, placement, layering, and integration. In this context, commonly applied tools like random forest (RF) and Support Vector Machines (SVMs) allow financial institutions to classify fraud business transactions employing large and annotated datasets. According to Tang and Yin (2005), artificial intelligence tools are usually applied at both placement and layering stages when large financial data is used to monitor business transactions conducted by the client. Integration as the final stage is very cumbersome to detect since the money has passed the possible detection stages. However, some of the artificial intelligence approaches are being proposed such as news data and enterprise relationships by extracting data from social media in an effort to monitor money laundering at the integration phase. Despite the availability of various money laundering cases, much less is known about money laundering in Southern and Eastern Africa (Basel Institute on Governance, 2020; Goredema, 2004; Issah et al., 2022). More worryingly, an interaction between artificial intelligence and money laundering is under-researched in Southern Africa.

2 Methodology

This study adopted a structured literature review methodology to comprehensively analyse the fragmented literature related to the interaction between artificial intelligence and money laundering. According to Armitage and Keeble-Allen (2008), a structured literature review encompasses a review of a plethora of literature sources with the aim to map science in a specific field of study. The structured literature review offered the researcher an opportunity to critique and evaluate the existing literature in an effort to unpack and identify possible research agendas (Dumay et al., 2016; Massaro et al., 2015; Paul & Criado, 2020; Paul & Feliciano-Cestero, 2021). In the context of this study, the Scopus database, Google Scholar, and other grey sources were used as secondary sources of data. More interestingly, Adams et al. (2017) suggested that grey literature can be used to augment the impact and relevance of organisation and management studies. The first and second tiers of grey literature such as book chapters, a broad range of journals, think-tank reports, government reports, news articles, company publications, and non-governmental organisation (NGOs) studies were used as recommended by Adams et al. (2017). There has been an exponential upsurge in the number of grey literature sources in recent years.

To ensure methodological rigor, this study adopted the following steps that were put forward by Massaro et al. (2015) when it comes to structured literature methodology: define the research question; write a research protocol for the review; determine the articles to include and carry out a comprehensive literature search; develop a coding framework; code the articles and ensure reliability; and critically analyse and discuss the results. In terms of the bibliometric analysis using data extracted from the Scopus database, “money laundering” and “artificial intelligence” were used as the keywords as follows: TITLE-ABS-KEY (money AND laundering AND artificial AND intelligence) AND (LIMIT-TO (PUBYEAR, 2022) OR LIMIT-TO (PUBYEAR, 2021) OR LIMIT-TO (PUBYEAR, 2020) OR LIMIT-TO (PUBYEAR, 2019) OR LIMIT-TO (PUBYEAR, 2018) OR LIMIT-TO (PUBYEAR, 2017) OR LIMIT-TO (PUBYEAR, 2016) OR LIMIT-TO (PUBYEAR, 2015) OR LIMIT-TO (PUBYEAR, 2014) OR LIMIT-TO (PUBYEAR, 2013)). In this respect, 76 documents were extracted for the past 10 years (2012 to 2023). The articles published in 2023 were excluded and non-English articles. Moreover, only articles were considered for bibliometric analysis in this study.

3 Results and Discussion

The bibliometric results provided evidence related to the interaction between money laundering and artificial intelligence. The results revealed that the adoption of artificial intelligence in combating money laundering is gaining traction in the existing body of literature, especially in the context of the financial sector. The bibliometric results permitted the researcher to have a deeper understanding of the general developments in money laundering and artificial intelligence as follows:

As illustrated in Fig. 2, it is observable that there is an increase in publications related to money laundering and artificial intelligence from 2011 to 2022. More interestingly, there was a sharp upsurge in the number of publications from 2018 (2.53%) to 2022 (35.44%). This implies that the researchers were more interested in how artificial intelligence can combat money laundering given the increase in adoption of digital transformation during the COVID-19 pandemic era.

Publication statistics per year from 2012 to 2022

The researcher went further to establish the bibliometric coupling of countries in an effort to establish the most productive countries when it comes to knowledge production in the context of money laundering and artificial intelligence. In this respect, the bibliometric results are presented in the following Fig. 3:

Bibliometric coupling of countries

The information presented in Fig. 3 is linked to the inclusion criteria of countries that were based on a minimum number of publications per each country of 2 documents. Of 44 countries, 23 countries were eligible for analysis. The United States was the most productive country with 10 documents followed by India and the United Kingdom both with 9 documents. China was associated with 5 documents following India and the United Kingdom. Cluster analysis related to bibliometric analysis revealed that Cluster 1 consisted of 10 countries (Brazil, Canada, China, Colombia, Germany, Italy, Russian Federation, Switzerland, United Kingdom, and the United States), Cluster 2 with five countries (Bahrain, Hungary, India, Poland, and Taiwan), Cluster 3 with four countries (Australia, Malaysia, Netherlands, and South Korea), and Cluster 4 with two countries (France and the United Arab Emirates).

In terms of science mapping, the bibliometric analysis of co-occurrences of keywords was performed. As such, a minimum number of occurrences of 5 was used as the threshold. Of the 568 keywords, 19 met the threshold. In this respect, the results are presented in Fig. 4.

Co-occurrences of keywords

The results reported in Fig. 4 show that “artificial intelligence” was the most reoccurring keyword with 56 occurrences followed by “anti-money laundering” with 27 occurrences. Next to anti-money laundering is “laundering” with 26 occurrences and then followed by “money laundering” with 24 occurrences. Nevertheless, it was observed that “computer crime”, “financial crime”, “terrorism”, and “data mining” were associated with the least occurrences of 5. Notably, both “financial fraud” and “deep learning” were just slightly above with 6 occurrences. In the case of cluster analysis of the co-occurrences of keywords, three clusters were extracted from the bibliographic data, that is, the first cluster with 8 keywords (anti-money laundering, data mining, deep learning, financial institution, laundering, learning systems, machine learning, and money laundering), second cluster with 6 keywords (anomaly detection, computer crime, crime, financial crime, financial fraud, and fraud detection), and third cluster with 3 keywords (artificial intelligence, blockchain, finance, risk assessment, and terrorism).

Following the bibliometric analysis of the existing literature on the interaction between money laundering and artificial intelligence, the researcher analysed the literature from Google Scholar and some grey sources such as organisational documents in order to establish the effects of artificial intelligence on money laundering. The positive effects of artificial intelligence on money laundering were established. These are detecting money laundering activities, enhancing legal compliance, augmenting customer behavioural analytics, detecting money laundering networks, robust financial crime risk computation, and informing evidence-based policy formulation. They are discussed as follows:

3.1 Detecting Money Laundering Activities

Detection of money laundering activities emerged as one of the positive effects of the adoption of artificial intelligence in an effort to combat money laundering in the financial sector. It is worth mentioning that detecting money laundering activities is at the center of the anti-money laundering agenda. This can be done by applying the data mining tools. This is supported by some of the extracts from the existing literature, “due to the high volume of daily transactions in banks and financial institutions, the possibility of automated systems that can interact with the massive data, is essential. Methods of detecting money laundering in these systems are usually based on provisions, which include a set of predefined rules and threshold values” (Salehi et al., 2017). Moreover, “in a real-life setting, the procedure to detect suspicious transactions would be run through all transactions for a certain time period” (Jullum et al., 2020). Based on the information, it is apparent to observe that artificial intelligence can help financial organisations in detecting money laundering activities by applying advanced technologies like deep learning, machine learning, and network analysis robust models. With the adoption of artificial intelligence, higher levels of due diligence are enhanced in a manner that can allow the banks to detect suspicious financial transactions normally done by Politically Exposed Persons (PEPs) and high net worth individuals as well as blacklisted persons. Enhanced due diligence is a risk-based approach that aims to identify, assess, and mitigate the risk of money laundering, terrorist financing, and other financial crimes.

3.2 Enhancement of Legal Compliance

The application of artificial intelligence promotes the enhancement of legal compliance. It is an open secret that financial institutions are required to observe the legal provision related to money laundering and terrorism financing, As such, artificial intelligence technologies can play a significant role in promoting legal compliance. A thorough literature review showed that “AML/CFT laws have created a large industry of compliance technology, processes, regulators and professionals, who focus almost exclusively on better compliance processes and technology. Like many regulatory structures, AML/CFT has taken on a life of its own, with a tendency to look for ever bigger and better technological solutions to detect illegal activity” (Bertrand et al., 2020). Interestingly, Domashova and Mikhailina (2021) documented that “the model can be used to form a list of the most important indicators for early detection of organisations involved in money laundering and terrorist financing (ML/TF), as well as to develop adequate recommendations to improve the compliance control process. A software tool in Python was developed that allows solving the tasks of early detection of organisations prone to money laundering”. This suggests that anti-money laundering technologies can assist financial institutions in augmenting their compliance control process. In the context of Zimbabwe, the Reserve Bank of Zimbabwe sets up rules and regulations that financial institutions must follow in order to detect and monitor suspicious transactions. The Zimbabwean banks are expected to produce suspicious transactions report that is generated daily by the system which monitors transactions done by customers if they are in line with their KYC requirements.

3.3 Augmenting Customer Behavioural Analytics

The augmentation of customer behavioural analytics emerged as another positive effect of adopting anti-money laundering technology in the financial sector. Customer behaviour can be analysed using artificial intelligence technologies since different types of customers may present different levels of risk. For instance, PEPs and high-profile customers or PEPs may be more likely to use their positions of power to facilitate illicit financial activity. This is supported by Jensen and Iosifidis (2023) who suggested that “client risk profiling is characterised by diagnostics, i.e., efforts to find and explain risk factors. The literature on suspicious behaviour flagging is characterised by non-disclosed features and hand- crafted risk indices”. Moreover, “compliance teams are also leveraging advanced analytics in a range of preventative financial crime use cases including enriching the KYC process, enhancing sanctions screening performance, and monitoring transactional activity, helping to proactively identify risks and opportunities” (EY Global, 2021). With the application of advanced decision-making models, financial institutions can look at transaction types. Notably, certain types of transactions may also be more likely to be associated with money laundering. For example, large cash deposits or withdrawals and wire transfers to high-risk jurisdictions may raise red flags.

3.4 Detecting Money Laundering Networks

The detection of money laundering networks is another theme that emerged from the study when it comes to the positive effects of artificial intelligence on money laundering. Given the effective adoption of artificial intelligence, financial crimes like money laundering can be reduced. In this context, Lokanan (2022) documented that “banks must adopt cutting-edge technologies like machine learning (ML) and artificial neural networks (ANN) to stay competitive and detect financial crimes. ML is a form of AI that allows computers to learn from data, identify patterns, and make predictions. Banks are already using this technology to detect fraud, assess risk, personalise customer service, and process and interpret large amounts of data. ML technology is particularly well-suited for credit scoring and money laundering detection tasks”. In a similar vein, “more efficient methods of detecting financial transactions could lower the false-positive rate while decreasing or maintaining the number of false negatives - and potentially more accurately detect suspicious transaction typologies within the financial transaction network. A typology is a term used in the field of anti-money laundering” (Visser & Yazdiha, 2020). There are transaction monitoring software that can be applied when monitoring financial transactions and identifying suspicious activities. The KYC databases can be utilised in screening customer transactions.

3.5 Robust Financial Crime Risk Computation

A thorough analysis of the available literature revealed that the adoption of artificial intelligence by financial institutions helps in ensuring robust financial crime risk computation. In this context, Danielsson et al. (2022) accentuated that “AI will give the financial authorities better access to financial information, the regulators may increasingly prefer to exercise control over private sector institutions’ risk appetite, as they already do extensively”. Furthermore, “artificial intelligence/machine learning (AI/ML) predictive models can help process credit scoring, enhancing lenders’ ability to calculate default and prepayment risks (Boukherouaa et al., 2021). Moreover, “all indications are that AI technology is here to stay and will become an increasingly important tool in risk monitoring, modeling, and analytics. Risk professionals will likely have to broaden their abilities, melding domain expertise with highly quantitative and technical skills” (Ahmed et al., 2023).

3.6 Informing Evidence-Based Policy Formulation

It emerged that information extracted from artificial intelligence in the financial sector informs evidence-based policy formulation when it comes to money laundering. It has been noted that policymakers are in need of evidence when formulating laws. In this regard, Surkov et al. (2022) highlighted that “many of these complex algorithms have become critical to the deployment of advanced AI applications in banking, such as facial or voice recognition, securities trading, and cybersecurity”. This can be achieved by strengthening AML laws and regulations, and the government increasing the penalties for money laundering. Also, organisations can enhance their customer due diligence procedures to better identify and verify customers, assess their risk level and monitor their transactions for suspicious activities.

On the other hand, there are negative effects of artificial intelligence on money laundering in the sense that it can lead to infringing on customer privacy. The adoption of artificial intelligence can lead to data security and privacy issues which can lead to a situation whereby customers can reject artificial intelligence-based interfaces. Moreover, poor data governance emerged as the challenge that can emanate from the adoption of artificial intelligence in trying to curb money laundering. It is within this context that Thowfeek et al. (2020) documented that “poor data quantity and quality as a highly underestimated key challenge in the implementation of AI in the banking sector. The realisation of the AI system’s benefits is primarily dependent on its prior training which requires data input and output, and an adequate amount of training data”. The challenges faced by AML in Zimbabwe are related to the informal economy which is large. It is very difficult to track and regulate financial transactions done by Small and Medium Enterprises. Many people and businesses operate outside the formal banking system, which can make it easier to launder money. Corruption is a major issue in Zimbabwe, and it has undermined efforts to combat money laundering. Corrupt officials may be more likely to turn a blind eye to suspicious financial activities.

4 Implications of the Study

This study on the interaction between artificial intelligence and money laundering is connected to theoretical and practical significance. As such, this study proffered evidence related to the effects of artificial intelligence on money laundering. This comprehensive review of scattered and fragmented literature related to artificial intelligence and money laundering extends the boundary of existing knowledge. More importantly, the results of this study help the leadership of financial institutions in the sense that they should embrace artificial intelligence technologies. This could help financial institutions to improve money laundering compliance processes. Interestingly, the knowledge and understanding of the application of artificial intelligence in combating money laundering can assist when assessing the risk profiling of customers. The financial institutions should up-skill their personnel and up-scale their business intelligence projects. Moreover, the policymakers should advocate for the adoption of artificial intelligence in order to strengthen the money laundering regulatory framework. This could strengthen transparency and accountability in the money laundering monitoring process.

5 Areas for Further Research

Based on the bibliometric results from this study, it is evident that little is known about the interaction between artificial intelligence and money from an African perspective. Using the Scopus database, it emerged that South Africa was the only African country that produced two publications pertinent to artificial intelligence and money laundering. Given this gap in the existing literature, it is recommended that more research studies are required from an African perspective with the purpose to extend our understanding of artificial intelligence and money laundering. Moreover, comparative studies between African countries are welcomed so as to capture some of the contextual factors that can influence the effectiveness of artificial intelligence in combating money laundering.

6 Conclusion

This study concentrated on the effects of artificial intelligence on money laundering. Despite the availability of various money laundering cases, much less is known about money laundering in Southern and Eastern Africa. As such, this study adds value through a comprehensive literature review. This has been done by applying bibliometric analysis using the Scopus database. Moreover, some grey sources were incorporated into the thematic analysis. The results established six positive effects of artificial intelligence on money laundering. These themes are detecting money laundering activities, enhancing legal compliance, augmenting customer behavioural analytics, detecting money laundering networks, robust financial crime risk computation, and informing evidence-based policy formulation. However, the negative effects are in the form of infringing customer privacy rights, and poor data governance. Despite the existence of few negative effects, it is concluded that artificial intelligence helps to combat money laundering in the Southern African region. As such, it is suggested that financial institutions should up-skill their personnel and up-scale their business intelligence projects.

References

Adams, R. J., Smart, P., & Huff, A. S. (2017). Shades of grey: Guidelines for working with the grey literature in systematic reviews for management and organisational studies. International Journal of Management Reviews, 19(4), 432–454.

Ahmed, I. E., Mehdi, R., & Mohamed, E. A. (2023). The role of artificial intelligence in developing a banking risk index: An application of adaptive neural network-based fuzzy inference system (ANFIS). Artificial Intelligence Review, 56, 1–23.

Alexandre, C. R., & Balsa, J. (2023). Incorporating machine learning and a risk-based strategy in an anti-money laundering multiagent system. Expert Systems with Applications, 217, 119500.

Armitage, A., & Keeble-Allen, D. (2008, June). Undertaking a structured literature review or structuring a literature review: Tales from the field. In Proceedings of the 7th European conference on research methodology for business and management studies: ECRM2008 (p. 35). Regent’s College.

Basel Institute on Governance. (2020). Basel AML Index: 9th Public Edition Ranking money laundering and terrorist financing risks around the world (p. 42). https://baselgovernance.org/sites/default/files/2020-07/basel_aml_index_2020_web.pdf

Bertrand, A., Maxwell, W., & Vamparys, X. (2020, July). Are AI-based anti-money laundering (AML) systems compatible with European fundamental rights? In ICML 2020 law and machine learning workshop.

Bissett, B., Steenkamp, P., & Aslett, D. (2023). The South African non-profit sector and its vulnerabilities to economic crime. Journal of Money Laundering Control (ahead-of-print).

Boukherouaa, E. B., Shabsigh, M. G., AlAjmi, K., Deodoro, J., Farias, A., Iskender, E. S., & Ravikumar, R. (2021). Powering the digital economy: Opportunities and risks of artificial intelligence in finance. International Monetary Fund.

Chitimira, H. (2021). An exploration of the current regulatory aspects of money laundering in South Africa. Journal of Money Laundering Control, 24(4), 789–805.

Chitimira, H., & Ncube, M. (2021). Towards ingenious technology and the robust enforcement of financial markets laws to curb money laundering in Zimbabwe. Potchefstroom Electronic Law Journal/Potchefstroomse Elektroniese Regsblad, 24(1), 1–47.

Chitimira, H., & Warikandwa, T. V. (Eds.). (2023). Financial inclusion regulatory practices in SADC: Addressing prospects and challenges in the 21st century. https://books.google.co.zw/books?hl=en&lr=&id=Gdu4EAAAQBAJ&oi=fnd&pg=PP10&dq=Financial+Inclusion+Regulatory+Practices+in+SADC:+Addressing+Prospects+and+...&ots=Lk3ORkTsPZ&sig=S4ww9Z3uYObIe7M5QWc3X_oPRF8&redir_esc=y#v=onepage&q=Financial%20Inclusion%20Regulatory%20Practices%20in%20SADC%3A%20Addressing%20Prospects%20and%20...&f=false

Couchoro, M. K., Sodokin, K., & Koriko, M. (2021). Information and communication technologies, artificial intelligence, and the fight against money laundering in Africa. Strategic Change, 30(3), 281–291.

Craig, P. (2019). In today’s digital age we are struggling to prevent new financial crime risks with old technologies. Can AI solutions yield greater impact? https://www.ey.com/en_gl/trust/how-to-trust-the-machine%2D%2Dusing-ai-to-combat-money-laundering

Danielsson, J., Macrae, R., & Uthemann, A. (2022). Artificial intelligence and systemic risk. Journal of Banking and Finance, 140, 106290.

Domashova, J., & Mikhailina, N. (2021). Usage of machine learning methods for early detection of money laundering schemes. Procedia Computer Science, 190, 184–192.

Dumay, J., Bernardi, C., Guthrie, J. & Demartini, P. (2016, September). Integrated reporting: A structured literature review. In Accounting forum (Vol. 40, No. 3, pp. 166–185).

EY Global (2021). How data analytics is leading the fight against financial crime?. https://www.ey.com/en_gl/consulting/how-data-analytics-is-leading-the-fight-against-financial-crime

Goredema, C. (2004). Money laundering in Southern Africa. Incidence, magnitude and prospects for its control. Institute for Security Studies Papers, 2004(92), 11.

Han, J., Huang, Y., Liu, S., & Towey, K. (2020). Artificial intelligence for anti-money laundering: A review and extension. Digital Finance, 2(3–4), 211–239.

Issah, M., Antwi, S., Antwi, S. K., & Amarh, P. (2022). Anti-money laundering regulations and banking sector stability in Africa. Cogent Economics and Finance, 10(1), 2069207.

Jensen, R. I. T., & Iosifidis, A. (2023). Fighting money laundering with statistics and machine learning. IEEE Access, 11, 8889–8903.

Jullum, M., Løland, A., Huseby, R. B., Ånonsen, G., & Lorentzen, J. (2020). Detecting money laundering transactions with machine learning. Journal of Money Laundering Control, 23(1), 173–186.

Latif, L. (2022). Intensifying the fight against corruption and money laundering in Africa. United Nations, Office of the Special Adviser on Africa.

Lokanan, M. E. (2022). Predicting money laundering using machine learning and artificial neural networks algorithms in banks. Journal of Applied Security Research, 1–25.

Madonsela, S. (2019). Critical reflections on state capture in South Africa. Insight on Africa, 11(1), 113–130.

Massaro, M., Dumay, J., & Garlatti, A. (2015). Public sector knowledge management: A structured literature review. Journal of Knowledge Management, 19(3), 530–558.

Meiryani, M., Soepriyanto, G., & Audrelia, J. (2023). Effectiveness of regulatory technology implementation in Indonesian banking sector to prevent money laundering and terrorist financing. Journal of Money Laundering Control, 26(4), 892–908.

Paul, J., & Criado, A. R. (2020). The art of writing literature review: What do we know and what do we need to know? International Business Review, 29(4), 101717.

Paul, J., & Feliciano-Cestero, M. M. (2021). Five decades of research on foreign direct investment by MNEs: An overview and research agenda. Journal of Business Research, 124, 800–812.

Pavlidis, G. (2023). Deploying artificial intelligence for anti-money laundering and asset recovery: The dawn of a new era. Journal of Money Laundering Control, 26(7), 155–166.

Salehi, A., Ghazanfari, M., & Fathian, M. (2017). Data mining techniques for anti-money laundering. International Journal of Applied Engineering Research, 12(20), 10084–10094.

Searle, R., Gururaj, P., Gupta, A. & Kannur, K. (2022, December). Secure implementation of artificial intelligence applications for anti-money laundering using confidential computing. In 2022 IEEE international conference on big data (big data) (pp. 3092–3098). IEEE.

Singh, C., & Lin, W. (2021). Can artificial intelligence, RegTech and CharityTech provide effective solutions for anti-money laundering and counter-terror financing initiatives in charitable fundraising. Journal of Money Laundering Control, 24(3), 464–482.

Stears, C., & Deeks, J. (2023). The use of artificial intelligence in fighting financial crime, for better or worse? Journal of Money Laundering Control, 26(3), 433–435.

Surkov, A., Srinivas, V., & Gregorie, J. (2022). Unleashing the power of machine learning models in banking through explainable artificial intelligence (XAI). Deloitte Insights. Available at: www2.deloitte.com/us/en/insights/industry/financialservices/explainable-ai-in-banking.html

Tang, J., & Yin, J. (2005). Developing an intelligent data discriminating system of anti-money laundering based on SVM. In Proceedings of the 2005 international conference on machine learning and cybernetics (pp. 3453–3457), Guangzhou, China, 18–21 August 2005.

Thowfeek, M. H., Samsudeen, S. N., & Sanjeetha, M. B. F. (2020). Drivers of artificial intelligence in banking service sectors. Solid State Technology, 63(5), 6400–6411.

Visser, F., & Yazdiha, A. (2020). Detection of money laundering transaction network structures and typologies using machine learning techniques.

Weber, P., Carl, K. V., & Hinz, O. (2023). Applications of explainable artificial intelligence in finance—A systematic review of finance, information systems, and computer science literature. Management Review Quarterly, 1–41.

Xia, P., Ni, Z., Zhu, X., He, Q., & Chen, Q. (2022). A novel prediction model based on long short-term memory optimised by dynamic evolutionary glowworm swarm optimisation for money laundering risk. International Journal of Bio-Inspired Computation, 19(2), 77–86.

Zondo, J. R. (2022). Judicial Commission of Inquiry into allegations of state capture, corruption and fraud in the public sector including organs of state report (Vol. 1 of 3 Vol.).

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2024 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Dzingirai, M. (2024). Effects of Artificial Intelligence on Money Laundering in Southern Africa. In: Moloi, T., George, B. (eds) Towards Digitally Transforming Accounting and Business Processes. ICAB 2023. Springer Proceedings in Business and Economics. Springer, Cham. https://doi.org/10.1007/978-3-031-46177-4_26

Download citation

DOI: https://doi.org/10.1007/978-3-031-46177-4_26

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-46176-7

Online ISBN: 978-3-031-46177-4

eBook Packages: Business and ManagementBusiness and Management (R0)