Abstract

The study investigates the evolution of financial literacy in Italian adults. Using three surveys from the years 2013, 2017, and 2020, we measure the financial literacy index and its components (financial knowledge, financial attitude, and financial behavior) using the OECD definition. The results show that financial literacy has decreased overall since 2013 in all three components. The gender gap persists, although the distance between the financial knowledge of women and men has shrunk. Moreover, results of the CART analysis show that the importance of the socioeconomic explanatory factors also changes over time; repeated baseline surveys of financial literacy of the adult population are therefore crucial for designing effective financial education programs.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

- Financial literacy

- Financial education

- Classification and Regression Tree

- Pooled cross-sectional analysis

7.1 Introduction

Since the global financial crisis, financial literacy has become an essential life skill in modern economies (OECD, 2020). Indeed, in the last two decades, financial services and products have become more complex but more easily accessible by final users, with the intermediation role of financial consultants much weakened or even absent. At the same time, financial markets are changing rapidly, with new technologies and the spread of new financial providers in a FinTech ecosystem. Moreover, individuals are increasingly called on to make more financial decisions than before, including planning for retirement or investing in additional education (Lusardi, 2019). For these reasons, financial education today plays a vital role in the policy agenda. It is globally recognized that financial literacy is an essential indicator of an individual’s ability to make a wise financial decision and that financially literate individuals are a vital ingredient for the wealth and health of an economy and society as a whole (Lusardi & Mitchell, 2014).

At the national and international level, several surveys exist nowadays that help measure, compare, and detect the determinants of the level of financial literacy of targeted individuals (adult population, teenagers, college students).

However, although studies on financial literacy have multiplied in recent years, to the best of our knowledge, there have been few empirical analyses on the evolution and determinants of the change in the level of financial literacy of a population. In fact, to date, the literature has mainly investigated the differences in financial literacy between countries (Atkinson & Messy, 2012; Borodich et al., 2010; Di Salvatore et al., 2018; Lusardi, 2019; Lusardi & Mitchell, 2014; Nicolini et al., 2013). These studies underline that the level of financial literacy across countries differs quite widely, although sharing a disappointing fact, i.e., being low.

This study aims to fill this gap by investigating the evolution of Italy's level of financial literacy over time and the determinants that explain such change.

Little research has investigated how financial literacy changes over time as noted above. Most literature consists of reports showing the evolution of the level of financial literacy. It tends not to focus on the determinants of changes over time or the causal effects of financial literacy, which is mainly measured in terms of financial knowledge, on financial outcomes such as retirement planning, stock market participation, ability to meet unexpected expenses, wise credit card behavior, etc. For instance, the FINRA Foundation’s National Financial Capability Study (NFCS) of 2019 included an annual report on the financial literacy of the US population. Results show an evident decline in financial literacy over nine years, from the first survey in 2009 to the last in 2018, though the differences in successive waves are minor.

Moreover, this study highlights that the decrease in financial literacy is more prominent for younger and middle-aged adults (18–34 and 35–54 years old) and smaller for adults over 55. The authors explain this by the disappearance from public awareness of the high-inflation, high-interest rate environment of the 1980s. Most Americans, except those who experienced that period firsthand as adults, are becoming less aware of these fundamental issues, which are central to the NFCS financial literacy quiz.

Taking stock of the same longitudinal data, Angrisani et al. (2020) investigate the evolution of financial literacy over time and shed light on the causal effect of financial knowledge on financial outcomes. Over a six-year observation period, they find that financial literacy has significant predictive power for future financial outcomes, even after controlling for baseline financial characteristics and a comprehensive set of demographic and individual factors that influence financial decision-making. Schmeiser and Seligman (2013) reach a different result. Using longitudinal data from the US Health and Retirement Study, they examine whether some of the questions previously used as measures of financial literacy are consistent measures of financial knowledge and effective predictors of future changes in wealth. They find that individuals’ answers to financial literacy questions show a great degree of inconsistency over time. Good performance in a financial literacy quiz has little predictive power for future accumulated wealth or resilience to financial shocks. Outside the US, PISA, the OECD's Programme for International Student Assessment, an international longitudinal study, has measured the level of financial literacy of teenagers, among other indicators, every three years since 2012. Findings for 2012, 2015, and 2018 (https://www.oecd.org/pisa/) highlight that, on average across OECD countries/economies, mean performance in financial literacy did not change significantly between 2012 and 2018, although it improved by 20 score points between 2015 and 2018. In the case of Italian teenagers, the average level of financial literacy is stable and low, throughout the period, despite significant efforts made by public and private institutions to invest in financial education programs.

Although panel surveys depict a situation where financial literacy is either stable or even declining over time, no study has attempted to define the determinants of these disappointing outcomes. To fill this gap in the literature, this study analyses the evolution of the financial literacy index of Italian adults measured in 2013, 2017, and 2020, disentangling the evolution of its main components (financial attitude, financial behavior, financial knowledge) as described by the OECD,Footnote 1 by year and socio-demographic characteristics of the sample. Univariate and Classification and Regression Tree (CART) analyses are used to achieve this.

More specifically, our study addresses the following research questions: (a) Has the level of financial literacy in Italy improved over the last decade?; (b) Does the change in financial literacy correlate with the socioeconomic and socio-characteristics of respondents to identify specific clusters in need of financial education?; and (c) Do these clusters change over time as financial literacy changes?

To answer these questions, we collect information from the three representative surveys on Italian adults’ financial literacy and competences conducted in 2013 (PattiChiari and a group of Italian Universities), in 2017, and in 2020 (Banca d’Italia). The data collected makes it possible to measure an overall financial literacy index and highlight its main components (knowledge, behavior, and attitude). Socio-demographic and socioeconomic characteristics of Italian adults are also included and matched with the financial scores.

It is found that despite the proliferation of educational programs, the financial literacy of Italian adults worsened during the period considered. Although the financial knowledge component shows a slight improvement since 2017, the drop in the level of financial attitude, but above all in the level of financial behavior, yields a disappointing evolution of the overall score of financial literacy in Italy. Among the socio-demographic explanatory variables, the worsening of the financial literacy level of younger people is particularly striking. Despite these frustrating outcomes, some improvements are worth mentioning. There is, for example, the closure of the gender gap where women are at a disadvantage on financial issues. First, Italian women’s attitude toward money and saving is similar to that of men in all three survey rounds. Second, importantly, a slow and persistent improvement characterizes female financial knowledge, compared to the declining trend among males. The multivariate analysis highlights that explanatory factors change over time and concern: (a) the survey year, with 2013 adults being in a better position compared to subsequent surveys; (b) the level of education, with highly educated individuals better off in 2013 in terms of financial literacy; (c) the employment status, which also hides a generational issue since the least financially literate are students and individuals in search of a job, i.e., mainly younger people; and (d) geographical area, with adults (and in particular, women) living in the North-Eastern part of Italy being in a better position.

The paper makes several contributions to knowledge in the field. As noted above, to the authors’ knowledge, this is the first paper to analyze the evolution of financial literacy of an adult population over time. Secondly, thanks to the availability of survey data over a seven-year horizon, our study of the determinants of financial literacy is extensive and enriched compared to the extant literature. Finally, our pooled cross-sectional study shed light on the evolution of the clusters of the adult population that is in major need of educational programs.

The remainder of the paper is organized as follows. Section 7.2 describes the survey instruments and the sample. Section 7.3 depicts the intertemporal evolution of the financial literacy index and its components. Section 7.4 contains the empirical analysis. Section 7.5 reports the results of our empirical methods, and Sect. 7.6 concludes.

7.2 Survey Instrument and Sample

7.2.1 Survey Instrument

Methods to measure financial literacy vary according to the conceptual definitions used, encompassing different sets of knowledge, skills, and behaviors covering various financial topics. Topics include budgeting, managing money, credit, and debt effectively; assessing the needs for insurance and protection; evaluating the different risks and returns involved in savings and investment options; saving for long-term goals; and understanding the capital market system and financial institutions. Since 2009, the OECD International Network on Financial Education (INFE) has developed a survey instrument to capture people's financial literacy from different backgrounds in a wide range of countries. The survey comprised good practice questions drawn from existing financial literacy questionnaires.Footnote 2

The OECD-INFE has defined financial literacy as “A combination of awareness, knowledge, skill, attitude, and behavior necessary to make sound financial decisions and ultimately achieve individual financial wellbeing”, and the core questions in the survey cover those aspects of knowledge, behavior, and attitudes that are associated with the overall concept. The questions include a range of contexts, including accessing financial services, budgeting, and money management, and planning for the future. There are also questions on important socio-demographic details of the participants, including age, gender, and income. Almost all the questions relate directly to the individual answering the question. However, some information is collected about the household, including total household income and the number of people living with the respondent. Finally, the questionnaire was designed to be used in face-to-face or telephone interviews.

After its release and widespread use in national surveys,Footnote 3 the questionnaire was first revised in 2015 (OECD-INFE, 2015) and again in 2018 (OECD-INFE, 2018). These revisions do not, however, prevent comparisons of survey results across years, and precautions are taken relating to this, and are briefly described below. Certain modifications, additions, and deletions were deemed appropriate because the state of knowledge and the financial landscape change rapidly. The questionnaire needs to provide cross-comparable data on emerging and important topics, such as digital financial services, crypto-assets, trust, integrity, and financial consumer protection, while still providing the depth of information necessary to inform a national strategic approach financial education (OECD-INFE, 2018).

Based on the OECD-INFE first version of the questionnaire, at the beginning of 2014 a consortium of Italian banks (PattiChiari) and a group of universities plus a research Centre (Invalsi) ran the first wave of the survey on 1000 adult individuals (http://www.feduf.it/container/scuole/ricerche); the two following waves (2017 and 2020) of the survey were run by the Bank of Italy based on the harmonized (2015 version) and the revised questionnaire (2018 version) on approximately 2500 adult individuals (di Salvatore et al., 2018).

As defined by the OECD, financial literacy is composed of three distinct aspects: knowledge, behavior and attitudes, which are measured by three respective indexes, i.e., a financial knowledge index (FKI); a financial attitude index (FAI), and a financial behavior index (FBI).

The knowledge component aims to assess the understanding of basic concepts that are a prerequisite for making sound financial decisions. Knowledge is based on the topics that have become the standard in the literature on financial literacy (Lusardi & Mitchell, 2014): understanding simple and compound interest, inflation, the positive relationship between financial risk and financial return, and the benefits of portfolio diversification. The FKI ranged from 0 to 8 in the first version of the toolkit and from 0 to 7 in the most recent; it is calculated as the sum of correct answers to the set of financial knowledge questions where each correct answer counts as one point and each wrong answer counts as zero. In the survey used in the 2013 wave, the research group eliminated questions that were merely testing a simple mathematical skill (e.g., division) or testing the same concept with two different instruments. The 2013 questionnaire contained only five questions related explicitly to calculating simple and compounding interest (two questions), understanding how inflation works (one question), the link between risk and return (one question), and the power of risk diversification (one question). In order to guarantee the comparability across waves, the FKI is constructed considering only these five questions (see Annex 1 for details).

The second component measures how a person’s behavior impacts on his/her financial well-being. Greater ability to properly manage financial resources reflects higher financial literacy. In particular, the behavior index is based on questions assessing whether people manage family financial resources by planning a budget, are able to make ends meet while paying debts and utilities with no concerns, and acquire information before making investments. As above, the financial behavior index counts positive behaviors exhibited; it takes a maximum value of 9, and a score of 6 or more is considered to be relatively high. Of the three indexes, the FBI is the one that has undergone the biggest changes in the formulation of questions and subsequent construction of the index itself (see Annex 1 for details) also for the two subsequent waves (2017 and 2020). As a consequence, in the descriptive statistics, we propose two different versions of the index so as to guarantee its comparability through the years.

Finally, the attitudes component evaluates preferences, beliefs and non-cognitive skills which are likely to affect personal well-being. Following INFE methodology, this component is meant to capture attitudes toward precautionary saving and planning for the future. If individuals have a negative attitude toward saving for their future, for example, it is argued that they will be less inclined to save. Similarly, if they prefer to prioritize short-term wants, they are unlikely to save for an emergency or make long-term financial plans (Atkinson & Messy, 2012). Therefore, the financial literacy survey includes three scaled attitudinal questions that ask people about whether they agree or disagree (on a scale from 1 to 5) with particular statements that capture their disposition or preferences: “I find it more satisfying to spend money than to save it for the long term”, “I tend to live for today and let tomorrow take care of itself”, and “Money is there to be spent”. The FAI is created by adding together the responses to each of the three questions, and then dividing by 3, so the score ranges between 1 and 5. The score is considered to be high when it is above 3. In general, individuals who disagree with the statements tend to have a longer-term view.

In order to assess overall levels of financial literacy, the three indexes are added, giving a single measure that considers the various aspects of financial literacy, including financial planning for the future, choosing financial products, and managing money on a day-to-day basis. The Financial Literacy Score can take a minimum value of 1 and a maximum value of 19, given by a maximum of 5 points from the knowledge index, 9 from behavior, and 5 from attitudes. There are no penalties for wrong answers, so “I don’t know” and no response are treated as “wrong” answers.

Waves 2 and 3 of the Italian survey also include questions to assess the respondents’ level of self-confidence. These were not present in the first version of the questionnaire and will be analyzed below in discussing responses and differences between 2017 and 2020.

7.2.2 Sample

As detailed in the OECD-INFE toolkit, (i) the survey should be of adults, i.e., individuals aged between 18 and 79; (ii) the interviews should preferably be made by telephone or face to face, to overcome issues related to low levels of literacy; and (iii) a minimum sample size of 1000 participants per country should be collected for international comparisons.

The three rounds of the Italian survey followed these requirements, and the samples were stratified per quota based on gender, age, geographical area, and municipality size. The samples were thus representative of the Italian population with regards to gender, age, geographical location, and the dimension of municipalities. Table 7.1 reports the distribution of the samples relative to main socio-demographic variables.

In 2013, the sample of 1247 respondents was collected using CATI (Computer Assisted Telephonic Interviews). Of the subjects interviewed, 300 were interviewed by cell phone, and the others by landline. Of the individuals surveyed, 52.04% were female. Most respondents (76.5%) were under 64 years old. The respondents’ average educational level was: 31% were educated up to higher secondary level, 11% were university graduates, and 58% had at most a middle-school-level education. Approximately half of the respondents (49.6%) were inactive and not seeking employment; the remaining were unemployed (8.3%) or employed (41.1%).

In 2017, the survey was run on approximately 2376 adults. The survey was carried out using two different methodologies: 49.6% of individuals responded on a tablet designed to be easily used by all population subgroups, including the less educated and the elderly. The others were interviewed personally using CAPI (Computer Assisted Personal Interviews). Compared to the 2013 sample, older adults increased from 25 to 26%. The level of education also increased slightly, with “high school or above” rising from 11 to 19.4%. Approximately 46% of the sample were inactive and not seeking employment; the remaining respondents were either unemployed (10.2%) or employed (44.4%).

The last survey wave, carried out in early 2020, involved an overall sample of about 2000 individuals interviewed using CAPI. The aging trend of the Italian population is confirmed by the constant increase in the percentage of over 65s on the total number of respondents. There was a noticeable drop in the highest level of educational attainment; only 15% obtained a high school diploma or a college degree compared to 19% in the 2017 sample. The percentage of unemployed, either searching for a job or not seeking employment, also fell. There is also a drop in the rate of women interviewed; it fell from 52% in 2013 and 2017 to 48% in 2020.

7.3 The Intertemporal Evolution of Financial Literacy Levels: Descriptive Statistics

The average level of financial literacy of Italians shows a statistically significant negative trend, falling from almost 12% in 2013 to a mere 10% in 2020 (Table 7.2).

The drop in the overall index is attributable to the fall in all its three components, and in particular to FBI. Financial knowledge recorded a small drop of 0.04 points, while behavior and attitude drop by 1.42 and 0.30 points, respectively (Fig. 7.1).

Global Financial Literacy Index evolution (Figure reports the Global Financial Index evolution across 2013, 2017, and 2020. The indicator is made up of three components—knowledge, attitude, and behavior. The differences in means of each indicator across years are always statistically significant at 99%)

Table 7.3 reports the median, mean values, and standard deviation of the Financial Knowledge Index (FKI) across the three waves. In the period under investigation, the mean value of the FKI decreased from 2.59 points in 2013 to 2.36 in 2017 to return in 2020 close to the initial value of the first survey 2.55. Note that the median value, on the other hand, shows an increase in 2020, from 2 to 3 points, indicating that half of the sample’s knowledge has in fact improved. As noted in Sect. 7.2, the index measures the level of knowledge of basic financial concepts which are considered as a prerequisite for making sound financial decisions. In fact, responding correctly to all five questions does not imply that individuals are financial experts, but only that they know basic concepts of personal finance. The results suggest that on average Italians have knowledge of fewer than half the financial concepts investigated.

There is a significant variation of attitude across surveys. From 2013 to 2020, the Financial Attitude Index decreases from 3.32 to 3.03, suggesting that individuals’ attitudes tend less toward the long term (Table 7.4).

Similarly, the FBI shows a decrease of the mean and median values and also in the measure of variability (Table 7.5). As noted in Sect. 7.2, the wording of the items chosen to measure financial behavior changed across the surveys. Specifically, in the 2017 and 2020 surveys, the responses on “active saving” did not include “cash deposited in a bank account” as an option. Differences also emerged with regard to the question about the ways in which individuals buy their financial products (“shopping around”), by simply relying on the advice of their bank or friends, or making comparisons using independent advice. Table 7.6 thus reports the FBI without the two items, “active saving” and “shopping around”, which changed. The drop in the index is less pronounced, with a decrease of 1.06 points. However, the downward trend is confirmed.

The interested reader can refer to Annex 2 for a discussion of the changes item by item in the three components of the Financial Literacy Index

7.3.1 Socio-demographic Characteristics

Figures 7.2, 7.3, 7.4, and 7.5 show the evolution of the index of Financial Literacy according to main socio-demographic characteristics of the respondents, education, age, and gender.

FLI and educational attainment (Figure shows the level of financial literacy index among the different level of education observed in the different surveys)

FLI and age distribution (Figure shows the level of financial literacy index among the different age observed in the different surveys)

FLI and gender (Figure shows the level of financial literacy index of male and female observed in the different surveys)

Gender and the components of financial literacy (Figure shows the level of financial knowledge, attitude, and behavior distinguishing between male and female observed in the different surveys)

Results are in line with international evidence of the determinants of financial literacy levels (Lusardi & Mitchell, 2014). Graduates have a higher degree of financial literacy than individuals with lower educational levels. Financial literacy increases with age up to a turning point, corresponding to the retirement age (Mazzonna & Peracchi, 2020; OECD, 2016) and males are more financially literate than females.

It is worth focusing on the temporal evolution with respect to age and gender. The largest drop in the level of financial literacy is recorded for the age bracket “18–24 years”, which also presents the lowest level of overall literacy. The FLI has remained stable in recent years for the three age brackets that include individuals at their initial and middle stages of working life.

The gender gap that characterized the population in 2013 seems to have closed in 2017 and 2020, reflecting mainly a marked worsening in male financial literacy. This is clear in the changes in the three components of financial literacy between 2013 and 2020 (Fig. 7.5). Women’s attitude toward money and saving is similar to that of men, and this is constant in all three waves. On the other hand, women score lower than men when it comes to demonstrating financial knowledge or savvy behavior, a result found in much literature (Lusardi & Mitchell, 2014). It is, however, worth pointing out the slow and persistent pace of improvement that characterizes female answers to the FK items, as opposed to the decrease for males.

7.4 Empirical Methods

The descriptive statistics have highlighted a worsening in financial literacy, with the two components of attitude and behavior being the driving forces of such deterioration. This section analyzes the determinants of this evolution over the years through the Classification and Regression Tree methodology that helps define groups of individuals connected by the same level of financial literacy (and similar financial education needs).

7.4.1 CART Analysis

The CART (Classification and Regression Tree) methodology is a non-parametric tree-structured recursive partitioning method introduced by Breiman et al. (1984). In general, it is an alternative approach to nonlinear regression. It is a method that belongs to binary decision tree approaches built by repeatedly splitting a node into two child nodes, beginning with the root node containing the whole sample. The use of CART analysis in this work helps to facilitate the use of covariates where we can explore the influence of many variables on the respondents’ variable (Financial literacy index).

In regression tree terms, let T represent the dependent variable and X = (X1, X2, …, Xp) be a vector of p covariates. The method involves two main stages to build the regression tree: growing and pruning. In growing, the T is recursively partitioned into subsets. Each partition is obtained by examining every possible binary split along the observed data T for each predictor variable X1, X2, …, Xp and selecting that which most reduces the variability of the node regarding the predicted variable. The result is a sequence of nested trees, with increasing leaves (terminal nodes), until no more splits are possible and the fully grown tree is reached. The pruning stage of the fully grown tree aims then to select the best sub-tree and consists of declaring an internal node as terminal and deleting all its descendants.

In the analysis, we obtained the tree using the following criteria:

-

Minimum number of cases in the parent node: 100;

-

Stopping rule for a terminal node: 50;

-

Tree pruning to avoid overfitting with a maximum acceptable difference in risk between the pruned and the sub-tree of 3 standard error; and

-

Missing data handled by surrogate splits.

The dependent variable of our analysis is the financial literacy index (FLI).Footnote 4 Explanatory variables are included and explained in Table 7.7.

7.4.2 Explanatory Variables

In X, we consider socio-demographic, socioeconomic variables, and a variable on the survey's year. As suggested by previous literature (Cucinelli et al., 2019; Lusardi, 2019; Lusardi et al., 2010), among socio-demographic and socioeconomic variables we include: (i) gender, measured with a categorical variable with two categories: female and male; (ii) age, measured using an ordinal variable with four categories: 18–24, 25–44, 45–64, and = ≥65 years old; (iii) citizenship, measured with a categorical variable with two categories: Italian and not Italian; (iv) geographical area in which the respondent lives; (v) family components number, measured with an ordinal variable with four categories: one component, two components, three components, four components, or more; (vi) employment status, measured using a categorical variable with six categories: employee, self-employed, student, retired, housewife, and looking for a job; and (vii) educational level, measured using an ordinal variable with four categories: primary education, lower secondary education, upper secondary education, and university education or more. Moreover, we include an ordinal variable for the survey year with three categories (2013, 2017, and 2020).

Table reports the description of socio-demographic and socioeconomic variables used in the analysis.

7.5 Results and Discussion

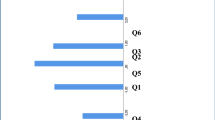

Figure 7.6 reports the most significant explanatory variables of the level of financial literacy in the three surveys, in order of statistical relevance. The Survey year shows the highest level of importance, followed by Employment condition, Level of education, Age, Gender, and Geographical area. The Citizenship and number of family components are the variables with the lowest level of importance.

Main explanatory factors of the Financial Literacy tree (Figure shows the most significant explanatory factors of the financial literacy index)

The final nodes of the FLI pruned tree identify 6 clusters as reported in Table 7.8 and Fig. 7.7 while Table 7.12 in the Annex explores the sociological characteristics of the identified groups. The first cluster includes individuals scoring the highest financial literacy, with an average FLI of 12.459. It consists of 567 respondents of the 2013 survey, with a medium to a high level of educational attainment, essentially young men workers. The second group presents an average FLI equal to 11.011 and is composed of 589 respondents of the 2013 survey with a medium to low level of education, mainly non-working older women. These two nodes underline that in 2013 the level of education was the first discriminant that described the level of financial literacy. Looking at the two other surveys (2017 and 2020), our results suggest that the level of education becomes less critical, leaving room for the type of employment of respondents. This may indicate that the many financial education programs carried out since 2013 have reduced the differences among individuals with different levels of education. These programs were mainly addressed to students of primary and secondary schools and women in general, increasing the level of financial literacy of these two parts of the population.

Tree diagram of Financial literacy indexes–in figure “2020” instead of “2022” (Figure reports the stylized CART with the six clusters)

In the last two surveys, the employment status becomes the most critical discriminant. Retired, self-employed, employed, and housewives show a higher level of financial literacy than students and people looking for a job. This classification also hides an age difference between the two clusters; cluster 3 comprises young people, aged 18–24 years, equally distributed between males and females. The level of education returns to be important when we look at the differences within the group of employed, housewives, retired, and self-employed individuals, which comprises so many different types of individuals by their working status. Again, individuals with a higher educational level show a higher financial literacy, 10.924. Finally, for those less literate, the geographical area where they live seems essential in describing the differences in financial literacy. In general, respondents who live in the South of Italy show a lower financial literacy index (9.358). In comparison, individuals who live in the North and center of Italy show a higher financial literacy index (10.290). Interestingly, the three subsequent clusters identified by the CART are in the majority composed of women, where the first discriminating factor is being in the job market (cluster 4) or not (cluster 5 and 6) and subsequently the residence area (North versus South), confirming the results of Cucinelli et al. (2019) who highlighted the importance of local factors in shaping the financial literacy level of Italian adults.

Table reports the characteristics of the six clusters defined by the regression tree.

To summarize, the CART results suggest significant differences between groups of individuals. Differences emerge concerning: (a) the survey year, with 2013 adults being in a better position compared to subsequent surveys; (b) the level of education, with highly educated individuals better off in terms of financial literacy; (c) employment status, which also hides a generational issue, since the least financially literate are students and individuals in search of a job, i.e., mainly younger people; and (d) geographical area, with adults (and in particular, women) living in the North-Eastern part of Italy being in a better position.

Our results further confirm that the “one-size-fits-all” strategy fails in education. In reality, financial education programs need to be planned and designed, considering the differences mentioned above. It is crucial to tailor educational programs to specific audiences with similar characteristics. In particular, in the most recent surveys, it emerges that the most fragile in terms of financial literacy are those with lower educational attainment, whatever their occupational status (employed or self-employed versus housewife or retired).

7.6 Conclusions

Previous literature has focused on the determinants of financial literacy, considering both socio-demographic and socioeconomic characteristics of individuals. A more recent strand of literature has analyzed the macro-ecological variables that characterize the context in which individuals live. What these studies have in common is that they focus on survey data from just one year. Our contribution to the literature is to study the evolution of financial literacy and its components over a more extended period, at three points in time (2013, 2017, and 2020).

To our first research question (Has the level of financial literacy in Italy improved over the last decade?), we provide evidence of a negative answer. However, among disappointing results, the reduction of the gender gap, thanks to an improvement in female financial knowledge, can be considered a glimmer of light.

About our second and third research questions (Does financial literacy measured over time correlate with the socioeconomic and socio-characteristics of respondents?; Do these clusters change over time as financial literacy changes?), our results underline that these factors are indeed useful in identifying clusters homogeneous in their need of financial education. And more importantly, the clusters change over time as financial literacy changes: if in 2013 the most discriminant variable was the level of education, in the subsequent surveys (2017 and 2020), the level of education gives way to the employment condition, suggesting that the programs of financial education carried out since the first survey were able to reduce the differences among people with different level of education. In more recent years, the employment condition becomes more important in discriminating among Italian adults, with students and individuals looking for a job being less financially literate than others. This result provides important support to the very recent attempts of universities and the national strategy for financial education to target college students of noneconomic fields with personal finance courses. Finally, we provide further support to those studies which underlined the role and impact of local factors in defining the financial literacy of respondents (Cucinelli et al., 2019; De Beckker et al., 2020).

These findings are important to define future financial education programs. As well known, the “One-size-fits-all” programs cannot be successful considering socio-demographic differences highlighted by our analysis. In future, considering the differences in terms of employment status and geographical area in which individuals live becomes crucial to decrease the differences in the financial literacy levels. Moreover, our results underline that the importance of the socioeconomic explanatory factors also changes over time; repeated baseline surveys of financial literacy of the adult population are therefore crucial for designing effective financial education programs.

Given the disappointing results of our research, it is crucial today to rethink and reflect on the structure and content of educational initiatives to improve their performance and achieve their final goal of promoting the financial literacy of Italian adults.

Along this line, the discussion should focus on how to structure new financial education initiatives, whether they are designed as lifelong programs or as simply on the job initiatives; whether it is more useful to lever digital and user-friendly modules or traditional face-to-face lectures; and finally, whether non-cognitive approaches are needed (as in Bocchialini et al., 2022, this volume). Most importantly, initiatives should be planned, designed, and monitored according to the best practices outlined for the implementation of effective educational programs. Two relevant references in this regard are the guidelines proposed by the Italian National Strategy for Financial Education (Comitato per la programmazione e il coordinamento delle attività di educazione finanziaria) and the fifteen indicators developed by a multidisciplinary team of scholars for the National Observatory of Economic and Financial Education (ONEEF)Footnote 5 as useful instruments to design—ex-ante—and evaluate—ex-post—the effective financial education projects.Footnote 6

Future research should focus on the evolution of financial literacy considering panel data on a sample of the same individuals that in different years attend the survey, also asking them whether they have attended educational programs during the period between the two surveys. Moreover, when comprehensive databases on financial education programs become available, future research can use more precise measures for such programs.

Notes

- 1.

- 2.

- 3.

- 4.

Annex 3 reports the results of CART analysis applied to the financial knowledge index, the financial attitude index, and the financial behaviour index.

- 5.

ONEEF is a National Observatory of Economic and Financial education. It was founded in 2016 by an inter-university pool of scholars and practitioners with different disciplinary background (economists, sociologist, pedagogists, and psychologist.). It has three main goals: (a) to monitor with a standardize procedure all the project on financial and economic education run in Italy and provide public data for free to those who are interested in the field; (b) to provide guidelines to improve the quality of the design of financial education projects; and (c) to sustain networking among public, private, and ONG subjects which run economic and financial education projects in Italy and, if possible, abroad.

- 6.

Each area has detailed questions to help designing an effective project (for example, “Are the goals following the S.M.A.R: T. model?”, “Do you know the level of recipients’ financial literacy?” “what kind of monitoring or evaluation come along with the project?” https://oneef.unimib.it/i-15-indicatori-oneef/.

- 7.

The Don’t Know answer includes the option “I prefer not to answer”.

References

Angrisani, M., Burke, J., Lusardi, A., & Mottola, G. R. (2020). The stability and predictive power of financial literacy: Evidence from longitudinal data (NBER Working Paper No. w28125).

Atkinson, A., & Messy, F. (2012). Measuring financial literacy: Results of the OECD/International Network on Financial Education (INFE) pilot study (OECD Working Papers on Finance, Insurance and Private Pensions, No. 15). OECD Publishing.

Borodich, S., Deplazes, S., Kardash, N., & Kovzik, A. (2010). Comparative analysis of the levels of financial literacy among students in the US, Belarus, and Japan. Journal of Economics and Economic Education Research, 11(3), 71–86.

Breiman, L., Friedman, J., Olshen, R., & Stone, C. (1984). Classification and regression trees. Chapman and Hall, Wadsworth.

Cucinelli, D., Trivellato, P., & Zenga, M. (2019). Financial literacy: The role of the local context. Journal of Consumer Affairs, 53(4), 1874–1919.

De Beckker, K., De Witte, K., & Van Campenhout, G. (2020). The role of national culture in financial literacy: Cross-country evidence. Journal of Consumer Affairs, 54(3), 912–930.

di Salvatore, A., Franceschi, F., Neri, A., & Zanichelli, F. (2018). Measuring the financial literacy of the adult population: the experience of Banca d’Italia. QEF N. 435.

FINRA Foundation. (2019). National financial capability study. https://www.finrafoundation.org/sites/finrafoundation/files/NFCS-Report-Fifth-Edition-July-2022.pdf

Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8. https://doi.org/10.1186/s41937-019-0027-5

Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Litterature, 52(1), 5–44.

Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial literacy among the young. Journal of Consumer Affairs, 44(2), 358–380.

Mazzonna, F., & Peracchi, F. (2020). Are older people aware of their cognitive decline? (Misperception and Financial Decision Making, IZA DP No. 13725).

Nicolini, G., Cude, B. J., & Chatterjee, S. (2013). Financial literacy: A comparative study across four countries. International Journal of Consumer Studies, 37(6), 689–705.

OECD. (2015). National strategies for financial education. OECD/INFE Policy Handbook.

OECD. (2016). OECD/INFE international survey of adult financial literacy competencies. OECD. www.oecd.org/finance/OECD-INFE-International-Survey-of-Adult-Financial-Literacy-Competencies.pdf

OECD. (2020). OECD/INFE 2020 international survey of adult financial literacy. www.oecd.org/financial/education/launchoftheoecdinfeglobalfinancialliteracysurveyreport.htm

OECD/INFE. (2018). Toolkit for measuring financial literacy and financial inclusion.

Schmeiser, M. D., & Seligman, J. S. (2013). Using the right yardstick: Assessing financial literacy measures by way of financial well-being. Journal of Consumer Affairs, 47(2), 243–262.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendices

Annex 1

The construction of the financial literacy index and its components

The overall Financial Literacy Index is the sum of points scored in each of the three components of the index itself: financial knowledge, financial attitude and financial behavior.

Financial knowledge ranges from 0 to 5 points

Text | Possible responses | Purpose |

|---|---|---|

Imagine that 5 brothers have to wait for one year to get their share of $1000 and inflation stays at 1%. In one year’s time will they be able to buy… | Multiple choice [correct response “less than they could buy today”—1 point] | To test the ability to understand how inflation impacts on purchasing power |

Suppose you put $100 into a savings account with a guaranteed interest rate of 2% per year. You don’t make any further payments into this account and you don’t withdraw any money. How much would be in the account at the end of the first year, once the interest payment is made? | Open response [correct response $102—1 point] | To test the ability to calculate simple interest on savings |

And how much would be in the account at the end of five years [add if necessary: remembering there are no fees or tax deductions]? Would it be…] This question builds on previous question | Multiple choice [correct response more than $110—1 point] | To test whether the respondent is aware of the additional benefit of compounding |

An investment with a high return is likely to be high risk/or If someone offers you the chance to make a lot of money it is likely that there is also a chance that you will lose a lot of money | True/False [correct response is true—1 point] | To test whether the respondent understands the typical relationship between risk and return |

It is usually possible to reduce the risk of investing in the stock market by buying a wide range of stocks and shares/or It is less likely that you will lose all of your money if you save it in more than one place | True/False [correct response is true—1 point] | To test whether the respondent is aware of the benefit of diversification |

Financial attitude score ranges from 1 to 5

(sum of the points scored in each item and then divided by 3)

Text | Possible responses | Purpose |

|---|---|---|

I find it more satisfying to spend money than to save it for the long term | 5 point scale: 1 = completely agree; 5 = completely disagree | These questions are intended to indicate whether the respondent focuses exclusively on the short term (agrees) or has a preference for longer-term security (disagrees) |

I tend to live for today and let tomorrow take care of itself’ | ||

Money is there to be spent |

Financial behavior ranges from 0 to 9

(sum of 8 items each of them 0 or 1 point with the exception of question “Choosing products” that takes the values 0, 1 or 2)

Text | Possible responses | Value toward final score |

|---|---|---|

Considered purchase | 5 point scale: 1 = completely agree; 5 = completely disagree | 1 point for respondents who put themselves at 1 or 2 on the scale. 0 in all other cases |

Timely bill payment | 5 point scale: 1 = completely agree; 5 = completely disagree | 1 point for respondents who put themselves at 1 or 2 on the scale. 0 in all other cases |

Keeping watch of financial affairs | 5 point scale: 1 = completely agree; 5 = completely disagree | 1 point for respondents who put themselves at 1 or 2 on the scale. 0 in all other cases |

Long term financial goal setting | 5 point scale: 1 = completely agree; 5 = completely disagree | 1 point for respondents who put themselves at 1 or 2 on the scale. 0 in all other cases |

Responsible and has a household budget | YES/NO | 1 point if personally or jointly responsible for money management and has a budget. 0 in all other cases |

Borrowing to make ends meet | This is a derived variable that combines a question about running short of money and one that identifies a range of different ways in which the respondent made ends meet the last time they ran short of money. The derived variable indicates people who are making ends meet without borrowing | 0 if the respondent used credit to make ends meet. 1 in all other cases |

Active saving | This question identifies a range of different ways in which the respondent may save. People who refused to answer score 0 | 1 point for any type of active saving (excluding letting money build up in a current account as this is not active). 0 in all other cases |

Choosing products | This is a derived variable drawing information from 2 questions. It is only possible to score points on this measure if the respondent had chosen a product: those with no score on this measure have either refused to answer, not chosen a product, or not made any attempt to make an informed decision | 1 point for people who had tried to shop around or gather any information. 2 points for those who had shopped around and gathered independent information. 0 in all other cases |

Annex 2

Evolution of FKI, FBI and FAI item by item

Financial Knowledge Index

2013 | 2017 | 2020 | ||||

|---|---|---|---|---|---|---|

Questions | Correct (%) | DNKFootnote 7 (%) | Correct (%) | DNK (%) | Correct (%) | DNK (%) |

The effects of inflation | 63.00 | 18.0 | 47.80 | 19.3 | 50.47 | 16.4 |

Simple interest rate calculation | 33.18 | 34.3 | 46.37 | 31.1 | 59.45 | 25.3 |

Compound interest rate calculation | 35.00 | 23.4 | 32.20 | 23.6 | 28.99 | 21.1 |

The power of diversification | 46.52 | 23.3 | 36.35 | 38.3 | 51.31 | 24.5 |

The relationship between risk and return | 81.70 | 6.7 | 73.35 | 17.3 | 64.74 | 17.2 |

The Financial Knowledge Index declines due to the reduction of the individuals’ knowledge of all topics composing the index, except for the simple interest rate item.

Financial attitude index

The FAI is measured using three different sentences that evaluate the attitude towards saving individuals (money, planning, and future). Results are reported in Figures 7.8, 7.9, and 7.10.

I tend to live for today and let tomorrow take care of itself (Note Figure reports the first item that composes the Financial Attitude Index and the five classes of answers: [i] 1 totally agree; [ii] 2 agree; [iii] 3 indifferent; [iv] 4 disagree; and [v] 5 totally disagree)

I find it more satisfying to spend money than save it for the long term (Note Figure reports the first item that composes the Financial Attitude Index and the five classes of answers: [i] 1 totally agree; [ii] 2 agree; [iii] 3 indifferent; [iv] 4 disagree; and [v] 5 totally disagree)

Money is there to be spent (Note Figure reports the first item that composes the Financial Attitude Index and the five classes of answers: [i] 1 totally agree; [ii] 2 agree; [iii] 3 indifferent; [iv] 4 disagree; and [v] 5 totally disagree)

From 2013 to 2020, the financial attitude of individuals decreases, in terms of both attitude towards savings and consideration of the future.

Financial Behavior Index

See Figures 7.11, 7.12, 7.13, 7.14, 7.15, 7.16, 7.17, and 7.18

Before I buy something, I carefully consider whether I can afford it (Note Figure reports answers given in the two surveys by respondents that were asked to evaluate whether they could afford their purchases)

I pay my bills on time (Note Figure reports answers, where one is given in the two surveys by respondents that were asked to answer if they pay their bills on time)

I keep a close personal watch on my financial affairs (Note Figure reports answers given in the two surveys by respondents that were asked to evaluate if they keep a close personal watch on their financial affairs)

I set long-term financial goals and strive to achieve them (Note Figure reports answers given in the two surveys by respondents asking if they set long-term financial goals and strive to achieve them)

I am responsible for making day-to-day decisions about money in my household (Note Figure reports answers given in the two surveys by respondents that were asked to evaluate if they are responsible for making day-to-day decisions about money in their household)

Active saving (Note Figure reports answers given in the two surveys by respondents asking if they have some form of active saving. In 2013 surveys, the item provided the following answers: saving cash at home or in your wallet; building up a balance of money in your bank current account; paying money into a savings account; buying financial investment products, other than pension funds; or in some different ways, including remittances, buying livestock, gold, or property. Among the diverse options offered, saving cash in a bank account was not considered a form of active saving. In subsequent surveys, “building a balance in a current account” was dropped as it is not regarded as active saving; new options were added to consider different investment forms, including crypto-assets)

I didn’t have negative savings during the last 12 months, and if I did, I didn’t borrow to make ends meet (Note Figure reports answers given by respondents who had positive savings or did not borrow to make ends meet in case of negative savings)

Financial product choice (Note Figure reports answers by respondents to the question about financial product choice. In particular, they are asked whether or not they have acquired information to make an informed buy [1 point for people who had tried to shop around or gather any information; 2 points for those who had shopped around and gathered independent information; and 0 all other cases])

Annex 3

CART analysis on the components of financial literacy index

1. Financial Knowledge Index

Importance of the independent variables for the construction of the FKI tree

2. Financial Attitude Index

Importance of the independent variables for the construction of the FAI tree

3. Financial Behavior Index

See Fig. 7.21, Tables 7.11 and 7.12

Importance of the independent variables for the construction of the FBI tree

Rights and permissions

Copyright information

© 2023 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this chapter

Cite this chapter

Bongini, P., Cucinelli, D., Zenga, M. (2023). Does Financial Literacy Progress Over Time? An Analysis of Three Surveys in Italy. In: Wachtel, P., Ferri, G., Miklaszewska, E. (eds) Creating Value and Improving Financial Performance. Palgrave Macmillan Studies in Banking and Financial Institutions. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-031-24876-4_7

Download citation

DOI: https://doi.org/10.1007/978-3-031-24876-4_7

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-031-24875-7

Online ISBN: 978-3-031-24876-4

eBook Packages: Economics and FinanceEconomics and Finance (R0)