Abstract

This chapter first offers a brief review of the conceptual aspects related to the ‘smile curve hypothesis’. Moreover, we use data on inward foreign direct investments (FDIs) to provide an empirical assessment of the functional specialization of economies belonging to North American, Asian and European production networks, and the upgrading/downgrading trajectories they experienced over time. Finally, in line with the prediction of the smile curve, we provide descriptive evidence of the negative association between, on the one hand, the specialization of economies in production with respect to the most upstream and downstream stages of global value chains (GVCs) and, on the other hand, their capability to capture value in GVCs.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

An extensive and expanding literature has documented, and reflected upon, the increasing fragmentation of production on a global scale that has taken place since the 1980s. This process has led to a growing trade in intermediate products and services as well as a surge in cross-border investments, especially in the form of vertical foreign direct investments (FDIs) and interfirm alliances involving actors from all over the world, engaged in different production stages (UNCTAD, 2011, 2013). International economics, economic geography and international business literature devoted great attention to the resulting worldwide dispersion of inter- and intra-firm webs of production and trade that have been referred to in multiple ways, including global commodity chains (Gereffi, 1999; Gereffi & Korzeniewicz, 1994), global value chains (GVCs; Kaplinsky, 2000; Gereffi et al., 2001), global production networks (Coe et al., 2008; Henderson et al., 2002) and global factory (Buckley, 2009a, 2009b; Buckley & Strange, 2015).

Notably, the rise of GVCs prompted firms to increasingly specialize in specific value chain functions, which are conceived as the full set of business activities—from those concerning the conception of goods to the ones relating to their fabrication and commercialization—carried out to develop and bring a product to market (Bernard & Fort, 2015; Feenstra, 1998; Sturgeon & Gereffi, 2009). The result has been the emergence of an ever finer international division of labour that occurs mainly at the level of individual production stages within sectors, also called “tasks” (Grossman & Rossi-Hansberg, 2008).

This transformation, together with the increasingly uneven distribution of value across actors performing different business activities, has been often associated with the “smile curve”, first proposed at the beginning of the Nineties by Stan Shih (1996). The smile curve simply illustrates that firms performing the most upstream (e.g., R&D, design and testing) and downstream (e.g., marketing, sales and after-sale services) functions of the value chain, mostly based in developed economies, tend to reap much larger shares of value than actors from developing economies, which mainly perform fabrication activities at the lower segment of the curve (Mudambi, 2008; Shin et al., 2012). Notably, this conception has largely informed the debate on the economic upgrading of countries in GVCs, with special reference to the opportunities for emerging economies to climb the value ladder thanks to the knowledge spillovers and technology transfer they may benefit from due to interactions with MNCs and their foreign affiliates (Gereffi, 1999; Humphrey & Schmitz, 2002; Pahl & Timmer, 2020; Rojec & Knell, 2018).

However, a major lack of micro-data has largely prevented measuring the specialization of economies across GVC functions, its evolution over time and its association with value capture dynamics. Empirical evidence on this matter is mainly based on case studies either on the GVC of specific products (e.g., Ali-Yrkkö et al., 2011; Ali-Yrkkö & Rouvinen, 2015; Dedrick et al., 2010; Linden et al., 2009; Xing & Huang, 2021) or on industry-based measures of “upstreamness” aimed at computing the supply chain position of sectors in terms of distance from final demand (Antràs et al., 2012; Meng et al., 2020; Rungi & Del Prete, 2018). Yet, while case studies can hardly provide general results, sectoral measures based on input-output statistics disregard the business activities undertaken for the realization of products and services, thus failing to detect the value chain functions performed by firms and countries (de Vries et al., 2021).

This contribution draws insights from previous works the authors have conducted at different levels of geographical disaggregation and with distinct focus and purposes (Coveri et al., 2022; Coveri & Zanfei, 2022a, 2022b), and combines them to illustrate an analytical strategy aimed to overcome the limitations of extant empirical studies on GVCs and value capture. In particular, we use data on the geographical location of inward FDIs in different value chain functions to compute indicators of ‘Functional specialization in FDI’ with the aim of offering an empirical assessment of the modern division of labour at a global scale. Moreover, we provide illustrative evidence on the evolution of the FDI-based functional specialization patterns for economies belonging to three major regional blocks, namely North America, East and Southeast Asia, and the EU27 and UK economies—hereafter referred to as “Europe” (Baldwin & Lopez-Gonzalez, 2015). This enables us to deliver an empirical assessment of the upgrading and downgrading trajectories experienced by both advanced and emerging countries over a relatively long period of time. In line with the smile curve hypothesis, we eventually offer descriptive and promising evidence on the negative association between, on the one hand, the specialization of economies in the production compared to upstream and downstream GVC stages and, on the other hand, their capability to capture value in GVCs.

The remainder of this chapter is organized as follows: Sect. 2 provides a background to this contribution, briefly reviewing the theoretical and empirical literature on the smile curve; Sect. 3 describes the data and methods employed; Sect. 4 provides empirical evidence on functional specialization and its link with value capture opportunities and Sect. 5 summarizes our main results and concludes by emphasizing the implications of the analysis offered and avenues for future research.

2 The Smile Curve: Conceptual Aspects and Empirical Evidence

The stylized representation of the international division of labour envisioned by the smile curve hypothesis is such that advanced economies mainly carry out pre-production (i.e., upstream functions such as headquarters, research, design and development) and post-production activities (i.e., downstream functions like branding, marketing, sales and after-sales services), while less developed economies tend to specialize in production functions such as manufacturing and assembly operations. This is supposed to reflect different value capture opportunities in GVCs across countries, with high-income economies specialized in functions at the upper ends of the value chain that can seize much greater returns than lower-income economies specialized in fabrication operations.

Consistently, the steepness of the smile curve reflects the unequal distribution of value across actors performing different stages along the value chains. As summarized by Durand and Milberg (2020), this is largely determined by the uneven degree of market competition across GVC segments. On the one hand, actors performing fabrication activities are subject to a high and increasing global competition, largely due to the growing involvement of low- and middle-income countries, especially China and India, in global production networks orchestrated by MNCs. This generates indeed a strong downward pressure on the remuneration of production activities, leading to a squeeze in the profit margins of firms mostly performing these functions (Baldwin & Evenett, 2015; Kaplinsky, 2000; Milberg & Winkler, 2013; World Bank, 2020).

On the other hand, the increasing role played by intangibles in GVCs provides MNCs—largely based in high-income countries—with the capability to seize large monopoly rents from the control of the most intangible-intensive segments of the value chains (i.e., the most upstream and downstream GVC stages).Footnote 1 This is mainly due to the high economies of scale intangibles give rise to, because of the very low variable costs to be sustained for their deployment once the initial fixed costs to develop or acquire them have been incurred. A second reason is due to the large appropriability of the rents they provide to their owners because of the high and increasing protection that intellectual property—such as patents, designs and copyrights, brands, trademarks and marketing strategies—enjoys, especially since the introduction of the Trade-Related Aspects of Intellectual Property Rights (TRIPS) agreement (Buckley et al., 2022; Chen et al., 2021; Durand & Milberg, 2020; Jaax & Miroudot, 2021; Pagano, 2014; Teece, 1986, 1998; Van Assche, 2020).

As for the empirical evidence on the smile curve, an important advancement was recently provided by Timmer et al. (2019), who computed a measure of ‘functional specialization in trade’ based on the amount of value added which can be traced back to workers employed in different functions for the production of exported goods and services. Consistently with the smile curve, they find that a positive correlation exists between the GDP per capita of economies and their specialization in R&D functions, while a negative relationship emerges between the former and the specialization of countries in fabrication activities. In a subsequent work, Buckley et al. (2020) show that in the last decades the value captured by both pre- and post-production functions has increased faster than that accruing to fabrication activities, hence providing evidence on the “deepening” of the smile curve. Finally, Stöllinger (2021) performed a cross-sectional analysis on the specialization of manufacturing industries in terms of FDIs in different business activities and the value added to gross output ratio, finding a negative relationship between the relative specialization of industries in production activities and the latter.

In what follows, we offer complementary evidence to that provided by these works, extending the analysis on both the cross-sectional and longitudinal dimensions of specialization of economies in different value chain activities and its association with value capture in GVCs. Our contribution to this literature is twofold. First, we offer an empirical assessment of the international division of labour predicted by the smile curve hypothesis. In doing this, we also question whether major upgrading or downgrading trajectories have been followed by world economies with different levels of economic development, and report evidence on the changing functional specialization of countries belonging to the North American, Asian and European production networks. Second, we provide a descriptive analysis aimed at illustrating whether the relationship between the functional specialization of economies and their capability to capture value in GVCs conforms to that predicted by the smile curve hypothesis.

For this purpose, we compute indicators of functional specialization based on high-quality proprietary data on inward FDIs distinguished according to the GVC function they are aimed to perform. These indicators, together with the dataset used, are briefly described in the next section.

3 The fDi Markets Database

fDi Markets is an online database provided by fDi Intelligence—a specialist division of Financial Times Ltd—which collects detailed information on announced cross-border greenfield investments (i.e., new wholly owned subsidiaries, including joint ventures whenever they lead to a new physical operation) covering all sectors and countries worldwide from 2003 onwards. Information on investment projects is drawn from several publicly available sources, including nearly 9000 media sources, over 1000 industry organizations and investment agencies, as well as data purchased from market research and publication companies. The detected projects are cross-referenced against a plurality of sources and over 90% of projects are validated with company sources (Castellani et al., 2013; Castellani & Pieri, 2013).

A distinctive feature of the fDi Markets database consists in reporting the main business activity—that is, the value chain function like R&D, design and development, manufacturing, sales and marketing and support—each FDI project is aimed to perform. As we will show in the next subsection, this is the key information we will use to compute our indicator of functional specialization of the economies. In particular, we classify value-adding functions in the three canonical stages of the value chain, that is, the upstream, production and downstream segments (Baldwin & Evenett, 2015; Mudambi, 2008; Porter, 1985) following the ‘sequential ordering’ of business activities inspired by Sturgeon (2008) and adapted from Crescenzi et al. (2014).Footnote 2 Then, we compute the Balassa’s (1965) index of revealed comparative advantage based on inward FDIs in these three GVC stages. We call this ‘functional specialization in FDI’ (FS). Following Stöllinger (2021) and Zanfei et al. (2019), this indicator is therefore an inward FDI-based specialization index which captures for the i-th country in a given year the relative attractiveness of investments in the a-th stage of the value chain. Formally, it is calculated as follows:

where the share of inward FDIs related to a given GVC stage over total inward FDIs received by a given economy (the numerator) is normalized according to the share of inward FDIs in the same stage over total inward FDIs for the world as a whole, namely the global average (the denominator).Footnote 3

Notably, cross-border capital flows have represented a key driver of modern international dispersion of value-adding functions and contributed to the growing involvement of low- and middle-income countries in GVCs (UNCTAD, 2013). By revealing how capable countries are to attract foreign capital in specific functions compared to others, this metric likely reflects actual comparative advantages of economies as defined by currently available technologies and factor endowments (Baldwin & Evenett, 2015; Hausmann & Rodrik, 2003; Nachum et al., 2000; Waldkirch, 2011). Accordingly, we contend that the functional specialization in FDI can provide a good proxy for the position occupied by countries in the international division of labour.

4 Empirical Evidence

4.1 Assessing the Functional Division of Labour Using FDI Data

This section exploits our FS indicator to provide a broad empirical overview of the functional division of labour at a global scale and the evolving functional profiles of the economies composing three major global production networks, namely North America, East and Southeast Asia and Europe (Baldwin & Lopez-Gonzalez, 2015; Stöllinger et al., 2018). Recent contributions have indeed shown that countries belonging to each of these three macro-regions have stronger GVC linkages in terms of both trade (Stöllinger et al., 2018; Xiao et al., 2020) and FDI flows (Zanfei et al., 2019) as compared to economies belonging to a different macro-regional block.Footnote 4 Recent studies using similar indicators based on FDI have highlighted differences in functional specialization across individual countries and between broad aggregates of advanced and developing economies (Stöllinger, 2021), and between the most developed regions by comparing North American and EU patterns (Coveri & Zanfei, 2022a). Building on these studies, we here focus on different national aggregates within macro-regions of the world to capture both similarities and differences in specialization patterns. We first of all unpack North America to compare the functional specialization of the USA and Canada with that of their low-wage neighbouring country, that is, Mexico. As for East and Southeast Asia, we compare the functional specialization of Japan and the Four Asian Tigers with that of China and the Southeast Asian economies.Footnote 5 Finally, the European economies are classified into four groups, namely Core, Finance, South periphery and East periphery.Footnote 6

Figure 8.1 reports, for each macro-region, the functional specialization of the country groups by either pooling observations across all years from 2003 to 2018 (top graphs, panels a) or accounting for yearly data in a dynamic perspective (bottom graphs, panels b).Footnote 7 Looking at graphs pooled over the whole period, Panel 1a highlights that Mexico is highly specialized in the production stages of GVCs (the FS index is higher than 1.6), while reporting an FS index lower than one in downstream and upstream functions. As expected, we find that the opposite holds for the USA and Canada. Notably, Panel 1b shows that this functional division of labour has deepened over time. Except for the last two years, the FS in production activities of Mexico has steadily increased over the period, while its specialization in upstream functions has been around 0.5 from 2003 to 2012 and has further decreased since 2013. The opposite is true for the USA and Canada, which increased their FS in upstream activities since 2010 while reducing their specialization in production operations over the 2003–2008 period and even further from 2011 to 2018.

Functional specialization in FDI for North America, East and Southeast Asia and Europe, 2003–2018. (Source: Authors’ elaboration based on fDi Markets data. Note: Panels 1a, 2a and 3a report the functional specialization in FDI of economies computed over the whole period of investigation. Panels 1b, 2b and 3b report the three-year moving average of the FS of economies from 2003 to 2018)

Panel 2a shows that a clear functional hierarchy also exists in the case of economies belonging to the East and Southeast Asian production network. In fact, the Four Asian Tigers report a remarkably high specialization in the most intangible-intensive functions at the upper ends of the value chains. Similarly, Japan results strongly specialized in downstream functions, while its FS index in upstream activities is slightly lower than one. Both these economies show an FS index in production stages lower than 0.5. Conversely, China and especially the Southeast Asian economies report a remarkable specialization in production functions, while resulting despecialized in upstream and downstream activities. Nonetheless, while Southeast Asia shows a very low specialization in upstream functions, China reports an FS index equal to about 0.9 in these activities. As highlighted by Panel 2b, China has indeed followed a functional upgrading trajectory by increasing its specialization in upstream activities since 2003, which led this country to consolidate an FS index in these activities equal to one since 2010. This appears to be true also for Southeast Asian economies, although to a lower extent. Since 2007, the latter countries have moved along GVCs by reducing their specialization in production and increasing their specialization in downstream functions, while slightly improving their specialization in upstream functions since 2012 (but in 2018 this was still about 0.5). Finally, the Asian Tigers show a rather steady functional profile over the period, maintaining an FS index higher than one in upstream and downstream functions and lower than 0.5 in production operations, while Japan has consolidated its specialization mainly in downstream activities (with an FS index in upstream activities oscillating between 0.8 and 1.15).

Finally, a clear division of labour seems to emerge when comparing across European economies. The East periphery is the only country group specialized only in production stages (with the FS index resulting equal to about 1.8 in these activities). Conversely, the other three groups of countries (Core, Finance and South Periphery) are despecialized in this GVC segment. As expected, Core and Finance economies exhibit an FS index higher than one in the two most intangible-intensive stages of the value chain, while the South periphery is specialized in downstream but not in upstream functions. Nonetheless, when looking at the evolution of the FS index over time, interesting functional patterns emerge. Panel 3b shows indeed that the economies belonging to the East periphery have remarkably increased their specialization in production stages over the period under investigation; at the same time, these economies have also steadily increased their specialization in the most upstream functions since 2008. Such patterns might signal their ability to upgrade their technological capabilities to develop higher value-adding functions alongside manufacturing operations. A similar upgrading trajectory seems to have been pursued by economies of the South periphery in the post-Great Financial Crisis period, which reports FS index in upstream activities higher than one since 2015.

Overall, our findings are consistent with the idea that the spatial division of labour spurred by the rise of GVCs is featured by low- and middle-income “factory economies”, mainly performing fabrication and assembly operations, and advanced “headquarter economies”, mainly carrying out the most upstream and downstream stages of GVCs (Baldwin, 2013; Baldwin & Lopez-Gonzalez, 2015).Footnote 8 Most notably, while a substantial heterogeneity is observed in the dynamics of functional specialization within these three major global production networks, the evidence provided also shows that functional hierarches are rather persistent over time.

4.2 Functional Specialization and Value Capture in GVCs

In order to offer suggestive evidence on the relationship between the functional specialization of macro-regions and their capability to capture value in GVCs, in this section we introduce an indicator of Relative Functional Specialization (RFS). This is a composite index aimed at jointly accounting for the level of functional specialization of the economies in upstream, production and downstream stages of the value chain. In logarithmic terms, the RFS index is computed as follows:

where \( F{S}_{i,t}^a \) is the index of functional specialization in FDI as computed by expression (1) and related to the a-th GVC stage.Footnote 9

As for a proxy of value capture in GVCs, we follow Kowalski et al. (2015) and measure value capture in GVCs by using data provided by the UNCTAD-Eora GVC Database (Casella et al., 2019) on the domestic value added embodied in exports (DVA) per capita (Koopman et al., 2014; Los et al., 2016). This indicator can be regarded as a measure of the gains that countries capture domestically from trade in GVC, since it focuses on the amount of value added that is retained by domestic actors involved in export chains. More precisely, it includes the value added captured by domestic firms directly exporting, together with value added generated by all other domestic firms indirectly contributing to exports of the former; by the same token, it excludes value added imported from abroad, that is, the value-added content coming from foreign producers which are embodied in imported intermediates used by domestic, direct and indirect, exporting firms. In this sense, the domestic value added in exports measures the value added captured by domestic firms participating in the country’s export chains.

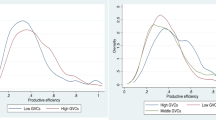

Figure 8.2 shows the relationship between the RFS index and the DVA per capita at the macro-regional level. As expected, a negative association emerges, suggesting that higher specialization of countries in the most intangible-intensive segments of the value chain is associated with higher value capture in GVCs. Figure 8.3 reports the same descriptive exercise at the country level, considering economies belonging to the macro-regions under investigation. Once again, a strongly negative relationship results between the functional specialization of economies in production compared to upstream and downstream functions and the amount of value added seized domestically by economies.Footnote 10

Relationship between RFS index and DVA per capita at macro-region level, average 2003–2018. (Source: Authors’ elaboration)

Relationship between RFS index and DVA per capita at country level, average 2003–2018. (Source: Authors’ elaboration)

5 Conclusions

The “slicing up” of value chains across countries has given rise to a finer international division of labour which increasingly occurs at the level of individual value-adding functions (Sturgeon, 2008; Sturgeon & Gereffi, 2009; Timmer et al., 2014). A major driver of this process has been the massive growth of cross-border investment flows, which has contributed to the growing involvement of low- and middle-income countries in GVCs. In this context, the ‘smile curve’ has gained increasing attention as a sort of stylized fact able to summarize the most salient features of the modern international division of labour and the associated distribution of value along GVCs.

In this chapter we offered a brief review of the building blocks of the ‘smile curve economics’ and provided evidence on the functional specialization of economies belonging to the three major regional blocks, namely North America, East and Southeast Asia and Europe. Lastly, we merged our indicators on functional specialization in FDI together with data on trade in GVC in order to provide descriptive evidence on the relationship between the functional position of countries and their capability to capture value in GVCs.

Three main findings emerge from our empirical investigation. First, as predicted by the smile curve, the most upstream and downstream value chain functions are mainly performed by the most developed countries, while production operations at the lower end of the value chain are mainly the prerogative of less developed world macro-regions. Second, the observed specialization patterns largely consolidated over the period under investigation, although a substantial heterogeneity emerged in the dynamics of functional specialization within the three global production networks considered. Third, and consistently with the predictions deriving from the smile curve, we provided evidence suggesting that higher specialization in the intangible-intensive segments of the value chain is associated with greater value capture opportunities in GVCs.

Finally, several implications can be drawn from our contribution, which in turn open up promising avenues for future research. Here we would like to highlight two that we consider particularly meaningful. A first implication of our analysis is that, although GVCs have enabled an increasing number of low- and middle-income countries to join the global capitalist space, this has so far only partially changed the economic and technological hierarchies across world economies. On the one side, a clear division of labour emerges within each of the three macro-regions we focused on, with high-income countries that have largely consolidated their specialization in the most intangible-intensive functions while less developed countries appear greatly specialized in production operations. On the other side, countries like China and economies belonging to the Southeast Asia and to the East and South periphery of Europe seem to have experienced forms of functional upgrading, especially by increasing their specialization in the most upstream or downstream GVC stages. This asks for further research aimed to disentangle the developmental policies and the economic, technological and institutional conditions which have allowed these countries to improve their domestic capabilities and move up the value ladder, while others failed to follow a similar path (e.g., Mexico).

A second implication which can be drawn from our investigation concerns the role played by intangibles in GVCs. The evidence that we provided on the strongly positive association between the specialization in the most intangible-intensive functions and the value added captured domestically by countries points out to the monopoly rents that actors controlling the pre- and post-production stages of the value chain can reap at the detriment of tangible-intensive producers, whose profit margins are squeezed and investment opportunities frustrated. In fact, the cumulative character of intangibles coupled with the high appropriability of rents they give rise to (especially due to the increasing protection of intellectual property rights like patents, brands and designs) can insulate those controlling these crucial assets—that we showed being mainly based in high-income economies—from potential competitors from emerging economies. This is likely to hinder the opportunity for the latter to enter the most profitable segments of GVCs, thus contributing to perpetrating income inequality across countries. This aspect should be more fully considered in future research aimed at deepening the distributional and developmental impacts of the current intellectual property regime on low- and middle-income economies involved in GVCs.

Notes

- 1.

- 2.

According to the classification adopted, upstream functions include headquarters activities, R&D, design and testing, education and training, and ICT-related infrastructure operations; production functions include fabrication, recycling and extraction activities; finally, downstream functions include activities mainly related to marketing and advertising, sales and after-sale services, and logistics, distribution and transportation.

- 3.

As criteria for value estimation are not made explicit, we perform our investigation relying on the number of FDI projects rather than on the value of capital involved. Consistently, several empirical works using fDi Markets have been performed exploiting the number of FDI projects rather than the data on capital investment (Castellani et al., 2013; Castellani et al., 2016; Castellani & Pieri, 2013, 2015; Crescenzi et al., 2014, 2015; Ramasamy et al., 2012). Note also that a limitation of fDi Markets concerns the inclusion of greenfield investments only (as well as major extensions of existing projects), while it does not cover information on mergers and acquisitions (M&As).

- 4.

This is largely due to common free trade and investment-related agreements (i.e., NAFTA and ASEAN in the case of North American and Southeast Asian economies), to a political and economic union (i.e., the European Union in the case of the Europe) as well as to their geographical proximity (Inomata, 2013; Xiao et al., 2020).

- 5.

The Four Asian Tigers include Hong Kong, Singapore, South Korea and Taiwan. The Southeast Asian region encompasses Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Thailand, Timor-Leste and Vietnam. Except Timor-Leste, all these countries belong to the Association of Southeast Asian Nations (ASEAN).

- 6.

The country composition of each group is the following: Core includes Austria, Belgium, Denmark, Finland, France, Germany and Sweden; Finance includes Cyprus, Ireland, Luxembourg, Malta, Netherlands and the UK; South periphery includes Greece, Italy, Portugal and Spain; East periphery includes Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia and Slovenia. This classification of European economies is adapted from Grabner et al. (2019).

- 7.

In order to avoid biases in the computation of our FS index, our sample includes countries which received a number of total inward FDIs (three-year moving average) larger than zero in each year. Moreover, we exclude tax havens and countries resulting in extreme outliers in terms of number of inward FDIs (largely because they are ‘Oil and Gas’ producers), that is, Aruba, Bahamas, Bahrain, Bermuda, Cayman Islands, Equatorial Guinea, Iceland, Kuwait, Macau, Norway, Oman, Puerto Rico, Qatar, Saudi Arabia, Seychelles, Switzerland, Trinidad & Tobago and the United Arab Emirates.

- 8.

This is consistent with evidence on the “functional specialization in trade” provided by Timmer et al. (2019), who found that advanced countries have steadily despecialized in fabrication operations, instead increasing their specialization in the most knowledge-intensive activities such as R&D, management and marketing.

- 9.

The RFS index was first computed by Stöllinger (2021). We added a constant equal to one to both the numerator and denominator to allow the calculation of the RFS index also for those observations reporting zeroes at the denominator (i.e., showing a FS equal to zero in both upstream and downstream GVC stages).

- 10.

Coveri and Zanfei (2022b) investigate the link between the RFS index and the DVA per capita by means of a fixed-effects model—including several control variables—on a balanced panel dataset of 102 countries over the period 2003–2018. Estimate results confirm that a higher specialization in production compared to upstream and downstream functions is negatively associated with value capture in export chains.

References

Ali-Yrkkö, J., & Rouvinen, P. (2015). Slicing up global value chains: A micro view. Journal of Industry, Competition and Trade, 15, 69–85.

Ali-Yrkkö, J., Rouvinen, P., Seppälä, T., & Ylä-Anttila, P. (2011). Who captures value in global supply chains? Case Nokia N95 smartphone. Journal of Industry, Competition and Trade, 11, 263–278.

Antràs, P., Chor, D., Fally, T., & Hillberry, R. (2012). Measuring the upstreamness of production and trade flows. American Economic Review, 102(3), 412–416.

Balassa, B. (1965). Trade liberalisation and “Revealed” comparative advantage. The Manchester School, 33(2), 99–123.

Baldwin, R. (2013). Trade and industrialisation after globalisation’s second unbundling: How building and joining a supply chain are different and why it matters. In R. C. Feenstra & A. M. Taylor (Eds.), Globalization in an age of crisis: Multilateral economic cooperation in the twenty-first century (pp. 165–212). University of Chicago Press.

Baldwin, R. E., & Evenett, S. J. (2015). Value creation and trade in 21st century manufacturing. Journal of Regional Science, 55, 31–50.

Baldwin, R. E., & Lopez-Gonzalez, J. (2015). Supply-chain trade: A portrait of global patterns and several testable hypotheses. World Economy, 38(11), 1682–1721.

Bernard, A. B., & Fort, T. C. (2015). Factoryless goods producing firms. American Economic Review, 105, 518–523.

Buckley, P. J. (2009a). The impact of the global factory on economic development. Journal of World Business, 44(2), 131–143.

Buckley, P. J. (2009b). Internalisation thinking: From the multinational enterprise to the global factory. International Business Review, 18(3), 224–235.

Buckley, P. J., & Strange, R. (2015). The governance of the global factory: Location and control of world economic activity. Academy of Management Perspectives, 29(2), 237–249.

Buckley, P. J., Strange, R., Timmer, M. P., & de Vries, G. J. (2020). Catching-up in the global factory: Analysis and policy implications. Journal of International Business Policy, 3, 79–106.

Buckley, P. J., Strange, R., Timmer, M. P., & de Vries, G. J. (2022). Rent appropriation in global value chains: The past, present, and future of intangible assets. Global Strategy Journal.

Casella, B., Bolwijn, R., Moran, D., & Kanemoto, K. (2019). Improving the analysis of global value chains: The UNCTAD-Eora Database. Transnational Corporations, 26(3), 115–142.

Castellani, D., Jimenez, A., & Zanfei, A. (2013). How remote are R&D labs? Distance factors and international innovative activities. Journal of International Business Studies, 44(7), 649–675.

Castellani, D., Meliciani, V., & Mirra, L. (2016). The determinants of inward foreign direct investment in business services across European regions. Regional Studies, 50(4), 671–691.

Castellani, D., & Pieri, F. (2013). R&D offshoring and the productivity growth of European regions. Research Policy, 42(9), 1581–1594.

Castellani, D., & Pieri, F. (2015). Outward investments and productivity. Evidence from European regions. Regional Studies, 50(12), 1945–1964.

Chen, W., Los, B., & Timmer, M. P. (2021). Factor incomes in global value chains: The role of intangibles. In C. Corrado, J. Haskel, J. Miranda, & D. Sichel (Eds.), Measuring and accounting for innovation in the 21st century. University of Chicago Press, ch. 10.

Coe, N. M., Dicken, P., & Hess, M. (2008). Global production networks: Realizing the potential. Journal of Economic Geography, 8, 271–295.

Corrado, C., Criscuolo, C., Haskel, J., Himbert, A., & Jona-Lasinio, C. (2021). New evidence on intangibles, diffusion and productivity. OECD Science, Technology and Industry Working Papers, no. 2021/10.

Corrado, C., Hulten, C., & Sichel, D. (2005). Measuring capital and technology: An expanded framework. In C. Corrado, H. Haltiwanger, & D. Sichel (Eds.), Measuring capital in the new economy (pp. 11–46). University of Chicago Press.

Coveri, A., Paglialunga, E., & Zanfei, A. (2022). Functional specialization in FDI and the geography of value capture in contemporary capitalism. In Paper presented at the Evolutionary Economic Geography Workshop, University College Dublin (UCD), Dublin, 6th June 2022.

Coveri, A., & Zanfei, A. (2022a). Who wins the race for knowledge-based competitiveness? Comparing European and North American FDI patterns. The Journal of Technology Transfer. https://doi.org/10.1007/s10961-021-09911-z

Coveri, A., & Zanfei, A. (2022b). Functional division of labour and value capture in global value chains: A new empirical assessment based on FDI data. Review of International Political Economy. https://doi.org/10.1080/09692290.2022.2152074

Crescenzi, R., Pietrobelli, C., & Rabellotti, R. (2014). Innovation drivers, value chains and the geography of multinational corporations in Europe. Journal of Economic Geography, 14, 1053–1086.

Crescenzi, R., Pietrobelli, C., & Rabellotti, R. (2015). Location strategies of multinationals from emerging countries in the EU regions. LSE ‘Europe in Question’ Discussion Paper No. 93/2015.

de Vries, G., Jiang, A., Lemmers, O., & Wei, S.-J. (2021). Firm productivity and functional specialisation. World Economy, 44, 1232–1260.

Dedrick, J., Kraemer, K. L., & Linden, G. (2010). Who profits from innovation in global value chains? A study of the iPod and Notebook PCs. Industrial and Corporate Change, 19, 81–116.

Durand, C., & Milberg, W. (2020). Intellectual monopoly in global value chains. Review of International Political Economy, 27(2), 404–429.

Feenstra, R. C. (1998). Integration of trade and disintegration of production in the global economy. Journal of Economic Perspectives, 12, 31–50.

Gereffi, G. (1999). International trade and industrial upgrading in the apparel commodity chain. Journal of International Economics, 48(1), 37–70.

Gereffi, G., Humphrey, J., Kaplinsky, R., & Sturgeon, T. J. (2001). Introduction: Globalisation, value chains and development. IDS Bulletin, 32(3), 1–8.

Gereffi, G., & Korzeniewicz, M. (1994). Commodity chains and global capitalism. Praeger.

Grabner, C., Heimberger, P., Kapeller, J., & Schutz, B. (2019). Structural change in times of increasing openness: Assessing path dependency in European economic integration. Journal of Evolutionary Economics, 30, 1467–1495.

Grossman, G. M., & Rossi-Hansberg, E. (2008). Trading tasks: A simple theory of offshoring. American Economic Review, 98, 1978–1997.

Haskel, J., & Westlake, S. (2018). Capitalism without capital: The rise of the intangible economy. Princeton University Press.

Hausmann, R., & Rodrik, D. (2003). Economic development as self-discovery. Journal of Development Economics, 72(2), 603–633.

Henderson, J., Dicken, P., Hess, M., Coe, N., & Yeung, H. W.-C. (2002). Global production networks and the analysis of economic development. Review of International Political Economy, 9(3), 436–464.

Humphrey, J., & Schmitz, H. (2002). How does insertion in global value chains affect upgrading in industrial clusters? Regional Studies, 36(9), 1017–1028.

Inomata, S. (2013). Trade in value added: An east Asian perspective. ADBI Working Paper, no. 451.

Jaax, A., & Miroudot, S. (2021). Capturing value in GVCs through intangible assets: The role of the trade–investment–intellectual property nexus. Journal of International Business Policy. https://doi.org/10.1057/s42214-020-00086-2

Kaplinsky, R. (2000). Globalisation and unequalisation: What can be learned from value chain analysis? Journal of Development Studies, 37(2), 117–146.

Koopman, R., Wang, Z., & Wei, S.-J. (2014). Tracing value-added and double counting in gross exports. American Economic Review, 104, 459–494.

Kowalski, P., Lopez-Gonzalez, J., Ragoussis, A., & Ugarte, C. (2015). Participation of developing countries in global value chains. OECD Trade Policy Papers, no. 179. OECD Publishing.

Linden, G., Dedrick, J., & Kraemer, K. L. (2009). Who captures value in a global innovation system? The case of Apple’s iPod. Communications of the ACM, 52(3), 140–144.

Los, B., Timmer, M. P., & de Vries, G. J. (2016). Tracing value-added and double counting in gross exports: Comment. American Economic Review, 106(7), 1958–1966.

Meng, B., Ye, M., & Wei, S.-J. (2020). Measuring smile curves in global value chains. Oxford Bulletin of Economics and Statistics, 82(5), 988–1016.

Milberg, W., & Winkler, D. (2013). Outsourcing economics. Global value chains in capitalist development. Cambridge University Press.

Mudambi, R. (2008). Location, control and innovation in knowledge-intensive industries. Journal of Economic Geography, 8, 699–725.

Nachum, L., Dunning, J. H., & Jones, G. G. (2000). UK FDI and the comparative advantage of the UK. World Economy, 23, 701–720.

Pagano, U. (2014). The crisis of intellectual monopoly capitalism. Cambridge Journal of Economics, 38(6), 1409–1429.

Pahl, S., & Timmer, M. P. (2020). Do global value chains enhance economic upgrading? A long view. Journal of Development Studies, 56(9), 1683–1705.

Porter, M. E. (1985). The competitive advantage: Creating and sustaining superior performance. Free Press.

Ramasamy, B., Yeung, M., & Laforet, S. (2012). China’s outward foreign direct investment: Location choice and firm ownership. Journal of World Business, 47(1), 17–25.

Rojec, M., & Knell, M. (2018). Why is there a lack of evidence on knowledge spillovers from foreign direct investment? Journal of Economic Surveys, 32(3), 579–612.

Rungi, A., & Del Prete, D. (2018). The smile curve at the firm level: Where value is added along supply chains. Economics Letters, 164, 38–42.

Shih, S. (1996). Me-too is not my style: Challenge difficulties, break through bottlenecks, create values. The Acer Foundation.

Shin, N., Kraemer, K. L., & Dedrick, J. (2012). Value capture in the global electronics industry: Empirical evidence for the smiling curve concept. Industry and Innovation, 19(2), 89–107.

Stöllinger, R. (2021). Testing the smile curve: Functional specialisation and value creation in GVCs. Structural Change and Economic Dynamics, 56, 93–116.

Stöllinger, R., Hanzl-Weiss, D., Leitner, S. M., & Stehrer, R. (2018). Global and regional value chains: How important, how different? Vienna Institute for International Economic Studies.

Sturgeon, T. (2008). Mapping integrative trade: Conceptualising and measuring global value chains. International Journal of Technological Learning, Innovation and Development, 1, 237–257.

Sturgeon, T., & Gereffi, G. (2009). Measuring success in the global economy: International trade, industrial upgrading, and business function outsourcing in global value chains. Transnational Corporations, 18, 1–35.

Teece, D. J. (1986). Profiting from technological innovation: Implications for integration, collaboration, licensing and public policy. Research Policy, 15(6), 285–305.

Teece, D. J. (1998). Capturing value from knowledge assets: The new economy, markets for know-how, and intangible assets. California Management Review, 40(3), 55–79.

Timmer, M. P., Erumban, A. A., Los, B., Stehrer, R., & de Vries, G. J. (2014). Slicing up global value chains. Journal of Economic Perspectives, 28, 99–118.

Timmer, M. P., Miroudot, S., & de Vries, G. J. (2019). Functional specialisation in trade. Journal of Economic Geography, 19(1), 1–30.

UNCTAD. (2011). World investment report 2011. Non-equity modes of international production and development. United Nations.

UNCTAD. (2013). World investment report 2013. Global value chains: Investment and trade for development. United Nations.

Van Assche, A. (2020). Trade, investment and intangibles: The ABCs of global value chain-oriented policies. OECD trade policy papers, No. 242. OECD Publishing.

Waldkirch, A. (2011). Comparative advantage FDI? A host country perspective. Review of World Economics, 147(3), 485–505.

World Bank. (2020). World development report 2020. Trading for development in the age of global value chains. World Bank.

Xiao, H., Meng, B., Ye, J., & Li, S. (2020). Are global value chains truly global? Economic Systems Research, 32(4), 540–564.

Xing, Y., & Huang, S. (2021). Value captured by China in the smartphone GVC – A tale of three smartphone handsets. Structural Change and Economic Dynamics, 58, 256–266.

Zanfei, A., Coveri, A., & Pianta, P. (2019). FDI patterns and global value chains in the digital economy. Working Papers Series in Economics, Mathematics and Statistics, No. 3. University of Urbino.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2023 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this chapter

Cite this chapter

Coveri, A., Paglialunga, E., Zanfei, A. (2023). Assessing Value Capture in GVCs: Conceptual Issues and Evidence at the Country Level. In: Lee, J.M., Ibarra-Olivo, J.E., Lavoratori, K., Li, L.(. (eds) Inequality, Geography and Global Value Chains. The Academy of International Business. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-031-24090-4_8

Download citation

DOI: https://doi.org/10.1007/978-3-031-24090-4_8

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-031-24089-8

Online ISBN: 978-3-031-24090-4

eBook Packages: Business and ManagementBusiness and Management (R0)