Abstract

This paper assesses the degree of integration of grain markets in late-Bourbon New Spain using standard econometric tools applied in other international cases. I find that grain market integration in Bourbon Mexico attained a degree comparable to other regions in the world, despite its poor transportation technology. Bourbon Mexico was not a market economy, but markets were effective tools in funneling resources from the countryside to the cities. An increase in prices in a leading market increased prices throughout the viceroyalty. For example, maize prices in Antequera, in the southern region of Oaxaca, within a year absorbed changes in prices in markets as distant as Guadalajara or San Luis Potosí (800 km). Likewise, wheat prices in Mexico City reacted to changes in the flour markets of the Gulf, such as Campeche (900 km away). These findings place grain markets in New Spain at a level of performance that is comparable to that found in the United States and some European regions. Spatial arbitrage (the buying in high-price regions and selling in low-price regions) was a driving force that broke local monopolies, opened the participation to other actors and created more diversified and integrated grain markets.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

18.1 Introduction

In his biannual report of harvest and market conditions for the second semester of 1794, the local magistrate of the jurisdiction of Tepatitlán, located 40 miles east of Guadalajara, reported the maize harvest “was abundant, but because it is scarce in the neighboring jurisdictions of Guanajuato, to an extreme degree, it sells today at eight reales [per fanega] when it usually sells at four.” Underneath this brief statement lies a story of price adjustments that we can reconstruct with the use of evidence of prices from other similar reports.Footnote 1 The shortage affected the mining city of Guanajuato, located 50 leagues to the east, which experienced an increase in prices from 9 reales in the first semester of 1793 to 15 reales in the first semester of 1794. The price difference with Tepatitlán’s typical price (4 reales) was close to the cost of transportation (12 reales per fanega). In the coming months the price surged to 23 reales. By now the difference in prices widely exceeded the costs, making it convenient to buy in Tepatitlán and sell in Guanajuato. The increase in demand translated into higher prices in Tepatitlán, but (as more places engaged in trade) it also increased maize supply in Guanajuato and drove its price down to 19 reales in early 1795, even as the new harvest would only be available by the end of the year. The evolution of prices in the two areas is not explained by a similar climatic trend: as the local magistrate of Tepatitlán made clear, and other reports from Guadalajara confirm, the harvest failure was contained to Guanajuato. It is the mutual dependence of markets that explains the trajectory: Guanajuato’s high price made it irresistible to buy from places such as Tepatitlán, increasing the prices in the producer areas and mitigating prices in the consumer center.

In this essay, I inquire the degree of market integration in late colonial Mexico. By market integration I understand the scenario in which trade connects two localities when the price difference between them exceeds the cost of transportation. The interdependence of markets across the space is the defining characteristic of market integration. Supply and demand forces in one market are not isolated but are propagated through other integrated markets via price adjustments. A major driver of integration is spatial arbitrage: if two markets are integrated, whenever the price difference between them exceeds costs, actors will buy low in one market and sell high in the other one (Ravallion 1986, p. 103; Roehner 2000, p. 179). As actors engage in buying and selling, the extraordinary profits dissipate and the price differential decreases to match transportation and transaction costs. Prices in one market, then, adjust to the other market (and vice versa) to finally restore the price ratio that reflects transportation and transaction costs between the two markets.Footnote 2

Integration does not mean that actors were directly trading from one market to the other. As John H. Coatsworth put it, “markets are not defined by the geographic space in which transactions actually occur, but by the space in which they may potentially occur given appropriate price signals” (1989, p. 539). Moreover, we can generalize the idea of integration to a system of markets in which the exchange between some of its components has effects throughout the system. Two distant consumer markets may not trade with each other but may still adjust to each other because of the existence of chain effects that affect conditions of supply and demand, and hence prices, in their suppliers (Ejrnæs and Persson 2000).

Grain market integration is a central theme, even a subfield, with a long tradition in economic history. The study of grain markets has progressed significantly in the last quarter century. Methodologically, the adoption of error- or equilibrium-correction models, dynamic factor analysis, and other statistical techniques have brought new awareness on the twin processes of adjustment and price convergence. A second revolution is the broadening of the scope to regions outside of Europe (Federico 2018). Against a Euro-centric and lineal interpretation that saw grain markets as progress toward modern economic growth, economic historians have shown that regions that did not share Western institutions, such as China, had a degree of market integration comparable to continental Europe in the eighteenth century (Li 1992; Marks 1998; Shiue and Keller 2007; Wong and Perdue 1992). Dobado-González et al. (2012) similarly showed that it was the entire Atlantic region, including Hispanic America, that evidenced traits of greater market integration in the eighteenth century. Scholars now see grain market integration as contingent on local characteristics, political priorities, and structural factors, rather than a lineal process of ever-increasing penetration of markets (Federico 2018, p. 18). In the case of Mexico, Dobado and Marrero (2005) found that corn market integration was increasing fast by the turn of the twentieth century and was comparable to more advanced economies.

The degree of the integration of grain markets in Mexico’s colonial period has deserved some attention although it has not been studied in detail. Two ideas are clearly discernable. One view proposes that market fragmentation prevailed and this was manifest in the pronounced variability of prices (Garner 1993, pp. 55–57; Hamnett 1986, p. 115; Morin 1979, p. 195; Salvucci and Salvucci 1987). The high variability and volatility in prices is a reminder that transportation costs still loomed large in the connectedness of markets and that these costs were unlikely to have changed over time. High transportation costs limited the frequency of transactions, but they do not necessarily indicate lack of integration. On the other hand, prices in different markets showed a high level of co-movement (Espinosa Morales 1995; Lindo-Fuentes 1980). I showed elsewhere that maize prices in four regional capitals and Mexico City shared a break in the trend in the early 1780s and that they tended to follow a common pattern (Challú 2007, pp. 206–207). The correlation between these series, in absolute values or in their rate of change, is very high and significant. While co-movement is a feature that we come to expect in integrated markets, at the same time it might indicate common climatic changes, changes in the money supply and, more broadly, common shocks that lift or depress prices simultaneously (Klein and Engerman 1990, pp. 14–17; Lindo-Fuentes 1980). These two views are limited in that they do not focus on the dynamic adjustment of prices to changes in price differentials (Ravallion 1986, p. 102).

This essay seeks to bridge the gap in our knowledge about market integration in late colonial Mexico by focusing on a limited set of consistent maize and wheat price series and analyzing them with a standardized set of techniques to measure market integration. Four questions, in particular, guide this inquiry: Were grain markets less integrated in Mexico than in other areas of the world? Given the typical distinction between commercial and subsistence agriculture, were the markets of wheat (the cereal produced for trade) more integrated than the markets of maize (the cereal produced primarily for subsistence)? Was market integration changing over the period? Did grain markets cease working in times of famine, drought, or climatic stress? I deal with these questions by presenting different measures of market integration. I particularly focus on the use of equilibrium- or error-correction models (ECM) since they provide a superior framework to describe the process of dynamic adjustment of prices.

18.2 Maize and Wheat Prices

Prices provide critical information to assess the degree of integration of markets. Maize, wheat, and flour prices from different locations of New Spain are used to assess the degree of market integration. The series include maize, wheat, and wheat flour prices in Antequera (present-day Oaxaca, maize prices only), Campeche (flour only), Guadalajara (only maize), Mexico City, Puebla, San Luís Potosí, Valladolid (present-day Morelia), Veracruz and Zacatecas (only short-run monthly maize series). The locations are mapped in Fig. 18.1. Maize and wheat represented the bulk of agricultural production and of the food supply, and both were widely traded. The prices are primarily based on purchase and sale transactions from different sources that were averaged by year; ancillary information from related products and nearby locations and interpolation filled remaining gaps. The markets were important trading centers on major roads and distant 200 to 900 km from each other. In terms of their population the smallest was San Luis Potosí, which had almost 8600 inhabitants by 1790. Veracruz, Valladolid, Campeche, and Antequera had 16 to 18,000 inhabitants; Guadalajara was near, with 20,000 but was growing very fast and nearing Puebla’s population in the early postindependence. Puebla was near 60,000 inhabitants and Mexico exceeded 100,000.Footnote 3

Locations of price series

The multiple transactions and large volumes of trade diffuse the effect of outliers. The use of annual averages further helps reduce the error in measurement, and it does not hinder detecting patterns in price movements given our knowledge of the speed of adjustment of prices in other international cases (MacKinnon 1996, pp. 614–615; Froot et al. 2019). Higher frequency data would have certainly been preferable to do a more fine-grained estimation of changes over time and to avoid the smoothing effect of price aggregation (Taylor 2001), but the monthly or quarterly series ran for short periods of 1–5 years (with the exception of Mexico City) that are unsuitable to obtain reliable estimates of price adjustment. Still, in the case of the estimation of volatility I used higher-frequency data to calculate more precise estimates that are comparable to other international cases.

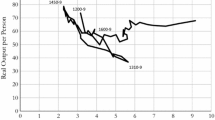

The population experienced increasing difficulties in obtaining their food supply in this period, most especially since the 1780s. The trajectories of cereal prices attest to these difficulties. The spikes circa 1749–1750, 1785–1786, and 1808–1809 coincide with the three main famines of this time period. Of them, the one in 1785–86 became known as “the year of the famine” for its high mortality. Even in more regular times the changes from year to year were dramatic, more noticeably in the maize series. Yet, underneath the variability there is also a clear increase in the price level in the 1780s. Even after prices receded in the years following the year of the famine, they remained high in comparison with previous decades. The highest consistent level for a prolonged period of time is in the 1810s, when the insurrection, epidemics, and bad harvests disrupted the harvests and commercialization. It is in this context of famine, inflation, and high variability of prices that the question of market integration becomes more pressing to gauge market integration as a way to assess, more generally, the role of markets in the unequal access to food.

Maize was the staple in Mexican diet and it was primarily a subsistence crop. As peasant communities grew in number and were constrained to production in their existing lands we can expect that the pressures to retain it locally increased (Van Young 1981, pp. 80–87). In general its price was low relative to the high transportation costs, implying that maize traveled short distances. The closest distance between two of the locations was 220 km, long enough that it would be unprofitable to conduct trade except in extraordinary circumstances. On top of high transportation costs, maize harvests were highly variable, since maize was not irrigated and long-term storage was problematic. From a regulatory point of view, local authorities could impose restrictions on trade potentially limiting the degree of market integration (Challú 2013).

Wheat was a more expensive crop, which meant that transportation costs weighed less on its price and made it possible to travel over longer distances. The population of the cities was the primary destination of wheat and for that reason wheat production was more oriented to the market than maize. The locations used in the analysis include San Luis Potosí in the west and northern region, Mexico City in the center, and Puebla, Valladolid, and Veracruz in the south. Some of these locations traded with each other: Valladolid supplied Mexico City, Puebla supplied Mexico City and Veracruz, and the latter supplied Campeche. Wheat was traded primarily in wholesale operations in flour mills. There were few regulations at the wholesale level and, by contrast to maize, use of prohibitions to trade was extremely exceptional. Compared to maize, wheat is the most favorable crop for market integration: it was produced for the market, it had a higher price-to-volume ratio and was less encumbered by the interference of local authorities. Our work will shed light on whether these advantages translated into a higher degree of market integration.

Such differences between maize and wheat are important to address Regina Grafe’s criticism that grain products were targeted in public policies as a response to moral economic expectations and not market expectations (2012, pp. 41–45). There are two responses to this potential criticism. First, by studying maize and wheat market integration I do not intend to make broader inferences about the degree of penetration of markets throughout the Mexican economy. I am primarily concerned with how the market mediated the access to food and facilitated transfers from producing to consuming areas. Although corn was not just food but also the fuel on which the mining economy and transportation ran, a broader set of products would be better suited to evaluate the integration of the economy as a whole. Second, the differences in types of regulation and market structure of corn and wheat provide us with two contrasting cases of substitute cereal products, helping to balance the bias introduced by relying in only one product.

18.3 Volatility

One important characteristic of maize and wheat prices that can be discerned in Appendixes 1 and 2 is the high degree of variation from one year to another. The expectation is that well-integrated markets feature less volatility than isolated markets because traders move grain from lower-price regions to profit with high prices, and in doing so reduce the peak prices (as we showed in the story of Guanajuato in 1794 that opened this essay). Volatility helps assess changes in market integration over time and draw comparisons with other international cases, although comparisons across products and countries also need to take into account the differences in cultivation and storage (Reher 2001; Salvucci and Salvucci 1987, pp. 77–78).

In Table 18.1, I use two different approaches to calculate price volatility within each series. Panel A shows the coefficient of variation of maize and wheat prices for series with more than 10 years of continuous information. The coefficient of variation is the standard deviation as the percentage of the series average. It is a rough measure of volatility that facilitates the comparison with other international cases. Panel B summarizes the typical monthly variation in maize prices in a slightly different set of locations; in most cases, we only have continuous runs of monthly data from one to five continuous years. Nevertheless, Panel B’s indication of monthly volatility has the advantage of providing a more relevant measure of how the swings in prices affected consumers, and it follows the same methodology used in studies from China and Europe (Persson 1999; Shiue and Keller 2007, pp. 106–113).

The first noticeable pattern is that the price of maize was considerably more volatile than wheat or flour. In Table 18.2, Panel A, maize had a coefficient of variation in the 26–55% range, while the range of wheat and flour was 16–42%. At first glance this difference seems to confirm the notion that wheat and flour were products channeled through markets, while maize was primarily a subsistence crop marginally traded. Yet, other factors beyond market integration have an effect. First and foremost, wheat harvest was more stable and predictable output because it was often cultivated in irrigated lands. A second factor that explains the difference in price volatility is that wheat could be stored for longer periods and had immense storage facilities in the mills of major cities, particularly those in Mexico City and Puebla. Such facilities could not be easily switched from one crop to another. By contrast, maize was less suitable for storing because its higher moisture content made it more vulnerable to spoiling.

From a geographic point of view, Mexico City, Valladolid, and Puebla had the lowest degree of volatility, while the western and northern locations of Guadalajara, San Luis Potosí, and Zacatecas had the highest. The pattern is consistent in the two cereals and in the two frequencies (annual or monthly). The major explanation for the difference is that the markets in the north and western regions were tightly connected to the demand in the mines, which were in arid areas and relied on shipments from long distances. The three locations (one of which was a major mining center itself) had to compete with demand from other mining centers as well, such as Guanajuato, Real de Catorce, and Sombrerete, among others. If the rains failed, not only was the grain supply scarcer but transportation was even more difficult as the pastures were nonexistent, increasing the consumers’ dependence on maize and freight costs (Suárez Argüello 1997, p. 183). The case of Guadalajara surrounded by fertile areas but also close to the supply areas of the mining districts illustrates the limitations of volatility as a benchmark of market integration: the high variations in prices were likely produced by it being integrated to markets, than by its lack of integration.Footnote 4

There were no significant changes in the long run in maize price volatility before and after 1780, a pivotal moment in economic and political trends (Challú 2010). The coefficient of variation of annual prices was roughly the same before and after 1780: 41% in the four maize series that span the entire period. The standard deviation of monthly differences had a very moderate increase (from 17% to 19%). While the lack of improvements in volatility can be taken as a sign of no major changes in market integration, this finding has to be countered by the greater level of climatic volatility that affected harvests and, hence, prices. The frequency of El Niño events, tree-ring reconstructions of drought conditions, and documentary evidence point to more variability and more climatic stress after 1780, which should have made supply more variable. Two generalized famines also took place after 1780 (in 1785 and 1809), compared to one before 1780 (1750), and conditions were critical in the 1810s. If anything, we should expect that these conditions should have produced a higher degree of volatility in the price series if markets were dysfunctional.

Compared with other contemporary cases in other regions of the world, grain prices in Mexico were more volatile than in Western Europe, but they were comparable to Spain and lower than in India (Table 18.2). The volatility of annual maize prices was particularly very high and only inferior to that of Indian wheat. Wheat and maize monthly variations, however, show Mexico much more in line with the European cases. We can see the same factors operating here that I pointed out in the differing volatility of maize and wheat in Mexico. The highest measurements of variation correspond to rain-dependent crops: wheat in India and maize in Mexico. At the other end of the spectrum, the Yangtze Delta and Southern China in the Qing period both enjoyed an outstanding system of grain storage and extensive use of waterways for grain transportation as well as irrigation; to a lesser degree similar conditions apply to Western Europe in this period (Shiue and Keller 2007; Studer 2008). The high variation in annual and monthly grain prices was not necessarily related to market failures or the absence of spatial arbitrage. The use of irrigation, the climatic cycle, and the availability of storage made maize prices intrinsically volatile.

18.4 Dispersion of Prices Across Different Markets

The spread of prices across central Mexico remained at similar levels over the period. Spread and volatility may arise some confusion, since both deal with variations in prices. While in the previous section I measured volatility through different measures of variation of prices within each series, here I measure the geographical dispersion of prices by calculating, in any given year, the coefficient of variation of prices in all different locations (Fig. 18.2). The locations examined here are Guadalajara, Mexico, San Luis Potosí, and Valladolid, which have a reasonably long overlap in their price series.Footnote 5 The average for the entire period was close to 29%, and 28% for the period after 1780. The prices of wheat in Mexico City, Puebla, San Luis Potosí, and Valladolid from 1757 to 1775 (the only period in which they overlap) had a slightly lower dispersion of prices: 23%. The difference between the geographic dispersion of maize and wheat prices is primarily attributable to transportation costs. Wheat has a lower coefficient of variation because transportation costs weigh less relative to the price. This logic also implies that the flat trend indicates the absence of major improvements in transportation costs.

Coefficient of variation in maize prices. Notes: The coefficient of variation is constructed as the standard deviation of the prices of Guadalajara, Mexico City, San Luis Potosí, and Valladolid, divided by their average. The marked years correspond to famines

The coefficient of variation in times of famine provides a good indication of whether markets were working more or less efficiently under such circumstances. If failing markets were behind a given famine, we would expect the coefficient of variation to be higher than average as speculation or barriers to trade placed limited the exchange of grain. Figure 18.2 shows that the famine of 1750 had a larger than average dispersion of prices and was followed in the next 2 years by the historical maximum of the series as conditions improved in the Bajío but remained bleak in Mexico City. This high point is indicative of limitations in the way markets corrected distortions. Yet, in the next two famine events, the coefficient of variation was not remarkably different than the average. In the 1785–1786 crisis, as prices shot up the variations from the high average were close to the average. The low coefficient of variation is even more remarkable because the authorities explicitly authorized restrictions to trade, but did not intervene prices. Similarly, the famine of 1808–1809 had below-average dispersion, although it increased in 1810 in part due to the disruptions of the insurrection to grain trade. These last two famine crises show that markets seemed better able to adjust to shocks in supply and this coincides with observations that volatility improved in the last two famines of the period. This increased ability to adjust does not mean that famines were less devastating, but rather that markets performed as expected in these events.

The spread of prices in Mexican maize and wheat markets was comparable to other grain markets in the world, even despite the highly localized tendency of its trade and the poor, mule-based transportation network. The average coefficient of variation across central Mexican markets was 29 percent for maize and 23 percent for wheat. In India, from 1760 to 1820, the coefficient of variation in rice prices was 60 percent, although it was a geographically larger area with many locations. In early eighteenth-century France, it was 30 percent in normal years and hit 45 percent during three famine episodes. In four states of the northeastern United States, from 1780 to 1820, the coefficient of variation was lower but not by much: 26 percent for maize and 20 percent for wheat. Only in the rice markets in northern China was the coefficient of variation remarkably lower: about 12 percent from 1738 to 1818 (Li 2000, p. 675; O’Gráda 2000, p. 721; Studer 2008).Footnote 6 In most of these areas there was no trend, like in the case of Mexico. It was not until the mid-nineteenth century when price convergence took place in Europe, India, China, and the United States (Jacks 2005; Studer 2008). This process was delayed in Mexico until the relatively late construction of railroads in the last quarter of the nineteenth century. At that point prices converged and the coefficient of variation became, once again, comparable to other international cases (Dobado and Marrero 2005, pp. 110–111).Footnote 7

18.5 Adjustment to Shocks in Price Ratios

The problem of the measures of volatility and price spread used so far is that they do not distinguish between effects of spatial arbitrage, long-run price differentials, and storage. As we have seen, wheat prices were more stable than maize prices, but this tells us little to nothing about whether traders and producers from a given region were willing to send maize to a region experiencing a shortage and having high, attractive prices. Similarly, we cannot surmise from this data the extent to which the higher coefficient of variation of maize prices related to inefficiencies in maize markets or to the larger weight of transportation costs in a low-cost crop.

Equilibrium- or error-correction models (ECM) allow us to overcome these deficiencies and test if a long-run equilibrium price between two markets existed, and how fast prices adjusted to restore the equilibrium. In different variants they have been widely used in contemporary and historical studies of grain markets (Bateman 2011; Llopis Agelán and Sotoca 2005; O’Grada 2003; O’Gráda and Chevet 2002; Persson 1999; Shiue and Keller 2007; Studer 2008). Here I adopt, with minor modifications, Studer’s equilibrium-correction model used in his analysis of annual grain price series of India (Persson 1999, pp. 114–130; Studer 2008, pp. 408–409):

The subindices i and j designate the two markets in the pair, t is the time unit (the year), p is the log price, ∆p is the annual change in the price, and ε is the error term, the variation from the expected long-run equilibrium value in a given year and location. This type of model is known as equilibrium or error-correction because the present value of the variable corrects the errors caused in the equilibrium level (p[i,t–1] – p[j,t–1] + τ). The speed of the adjustment in each market is determined by the coefficients α, which have a range of 0 (no adjustment) to 1 (full adjustment in one time unit). We refer to the sum of both α coefficients as the γ, which represents the speed at which both markets restore the long-run equilibrium level. We calculate γ as a differentiated derivation of the previous equations:

where γ is the sum of α1 and α2. The coefficients are obtained with ordinary regressions for each possible market pair, and are calculated for the entire period, and also for the pre- and post-1780 subperiods.Footnote 8

What results are expected if markets are integrated? First, in a condition of market Integration, we expect that γ is significantly different than zero and rejects the Augmented Dickey-Fuller unit root test. If γ is not significantly different from zero, we cannot conclude that there is a long-run equilibrium price that causes one or both markets to adjust, as is expected in a scenario of market integration (Froot et al. 2019; Studer 2008). Time aggregation and perhaps the time span of the series likely introduce downward biases in these calculations that run against the hypothesis of market efficiency (Taylor 2001). Second, we also expect that the coefficients for γ and α1 are bound by 0 and − 1, and that α2 is bound by 0 and 1. The closer γ is to −1, the faster the equilibrium price is restored in one time unit. The speed of adjustment is an indicator of market integration, in that it reflects how fast actors respond (through spatial arbitration) to the profit incentives generated by a relative rise in prices. The ratio between the maximum and minimum absolute α indicates how symmetrically the two markets adjust to changes in the equilibrium price. If only one market has a significant α, the system is said to be “weakly exogenous” in that only one market is correcting to the equilibrium level. While mutual adjustment is an indicator of greater market integration, we can expect that larger markets are less influenced by small-size markets. Third, in a process of reductions of transportation costs and reduction of other trade costs, we expect the constant τ to decline. However, we do not expect this long-run differential to fall in this time period given that there were no major changes in transportation technologies (Bateman 2011; O’Rourke and Williamson 1999). Fourth and final, as Studer (2008) aptly indicates, the correlation between the regression residuals of Eqs. (18.1 and 18.2) measures the degree of co-movement between the two markets. Both prices may move together in response to common shocks (such as climatic conditions, economic conditions), but it is also a sign that traders are acting upon common information that is shifting prices in expectation of future changes (Roehner 2000, p. 179).

My results of the ECM models for the twenty market pairs, shown in Table 18.3, indicate that prices in each pair were adjusting to a long-term equilibrium level, that is, that a change in prices in the price ratio initiated a mechanism of price correction. Let us first focus on the total adjustment to shocks in the equilibrium (γ) and co-movement (ρ). All γ coefficients in all pairs reject the unit-root test, which indicates the existence of a long-term equilibrium level. Almost all α and γ coefficients are in the expected range, from 0 to 1 (and the exceptions are not significantly different from those boundaries). Looking at the total adjustment speed (γ), on average maize prices absorbed 87% of a shock in one year, and wheat prices 74%. That means that, according to our calculations, it took 14 and 16 months, respectively, to correct the prices to the equilibrium level, although in almost all pairs the γ coefficient is not significantly different than the unity, which indicates a full correction in one year. Only three cases have a speed of adjustment below 0.7 and they all involve the northern town of San Luis Potosí. These coefficients are likely to be biased toward a slower estimate because the annual data likely aggregate too much of the change that can be better gauged with a higher-frequency series. The true estimate of speed adjustment is 20–30 percent faster according to Taylor’s analysis (2001, p. 7).

The results of the ECM models for the 20 market pairs indicate that prices in each pair were adjusting to a long-term equilibrium level, that is, that a change in prices in the price ratio initiated a mechanism of price correction. Let us first focus on the total adjustment to shocks in the equilibrium (γ) and co-movement (ρ). All γ coefficients in all pairs reject the unit-root test, which indicates the existence of a long-term equilibrium level. Almost all α and γ coefficients are in the expected range, from 0 to 1 (and the exceptions are not significantly different from those boundaries). Looking at the total adjustment speed (γ), on average maize prices absorbed 87% of a shock in one year, and wheat prices 74%. That means that it took 14 and 16 months, respectively, to correct the prices to the equilibrium level, although in almost all pairs the γ coefficient is not significantly different than the unity, which indicates a full correction in one year. Only three cases have a speed of adjustment below 0.7 and they all involve the northern town of San Luis Potosí.

Most pairs involve markets of unequal importance, and such importance typically reflects on an unequal correction to price shocks. One market in the pair typically had an adjustment that was three to four times larger than the other market. This unbalance is shown in the ratio of maximum-to-minimum alpha. Even more, in 13 of the 20 pairs, the lowest alpha is not significantly different than zero, meaning that one market is “weakly exogenous” to the equilibrium-correction mechanism. The weakly exogenous market is said to be a “leader” and the other the “follower.” There are two patterns that stand out in the leader-follower structure of market pairs in Bourbon Mexico. First, is that, with some exceptions, the smallest market in the pair is the follower and the most important is the leader. This is particularly obvious in the maize market pairs: Mexico City is always the leader and, on the other end, San Luis Potosí is always a follower. Second, the market size pattern breaks in the case of Veracruz, which is always a leader in price adjustment. Even Mexico City is a follower of Veracruz. The Veracruz market not only supplied its own population (of a size comparable to San Luis Potosí), but its importance lay in the fact that it supplied the fleets, other towns in the Gulf of Mexico (such as Campeche) and Havana. This trade is typically considered of importance for the Puebla region, but the fast adjustment in Mexico City and Valladolid suggests that the flour export trade was also consequential to grain markets elsewhere in the viceroyalty (Sennhauser 1996, pp. 107–109; Stein and Stein 2003, pp. 245–246; Suárez Argüello 1985, pp. 112–117).

The τ coefficients show that the long-run price differential between markets reflects trade costs only in markets that directly traded with each other (Jacks 2005, p. 384; Roehner 2000). In maize markets direct trade between even the closest of these markets was extraordinary. Only in 2 years the price differential exceeded the transportation cost between Mexico City and Valladolid. Instead, the price differential (τ) between markets with no direct trade primarily responds to the gap between high-price consumer markets, and low-price producer markets. By contrast, transportation costs weigh heavily in the case of wheat and flour, where many of the pairs had direct trade. The τ coefficients are, in general, reflective of transportation costs. Consider, for instance, how the τ of Valladolid and Puebla is equivalent to the sum of the τ’s of Mexico–Valladolid and Mexico–Puebla. Such proportionality in trade costs is a good indicator of consistency in the series.

The distance and transportation cost between markets is also an important factor behind the co-movement of prices. We measure co-movement in ρ, which is the Pearson correlation between the residuals of the two ECM equations. A high ρ indicates that common trends were important drivers of local prices. Common climatic and economic cycles as well as short-term price adjustments are behind this co-movement (Studer 2008). We discussed before the similarities in the evolution of the price series and the ρ confirms this perception. The average correlation between the residuals of the ECM equations is 0.60 and 0.55 for maize and wheat, respectively, meaning that over 30% of the annual variations are explained by the common movement of prices from one year to another. We expect that common trends are stronger the closer the markets are, and our results confirm this expectation. In maize market pairs there is a clear distance-co-movement gradient. Markets within 200 miles had a co-movement coefficient above 0.7, while those farther than 450 miles had a co-movement of less than 0.55. The shorter periods and the use of boat shipments to supply Campeche complicate the picture in the wheat market pairs. If we compare the series by those with coverage before and after 1780, the degree of co-movement does trace distance closely. Before 1780 (rows 1–6), the pairs under 200 miles (Mexico–Puebla and Mexico–Valladolid) have a ρ over 0.55, while the other pairs have a very low ρ, in the 0.10–0.19 range. In the series covering the post-1780 period (rows 1 and 7–10), transportation cost (the lowest in the case of Veracruz–Campeche, and proportional to distance in the other cases) is well related to co-movement.

The results contrast with the characterization that grain market was fragmented in colonial Mexico. The comparison between maize and wheat markets, and between the southern market of Antequera with those in the western and northern highlands illustrate this point. First, there is no substantial or significant difference between market integration in maize or wheat markets. Maize was the crop primarily destined to subsistence and the major production in peasant households. Wheat, by contrast, was the crop oriented to the market and primarily taking place in haciendas. There is no substantial or significant difference between the two products: both were similarly responsive to shocks in equilibrium prices.Footnote 9 The case of Antequera similarly defies expectations of market fragmentation. Antequera was a provincial capital surrounded by a predominant indigenous, peasant agriculture. Supply typically involved the neighboring valleys and had a shorter reach than most of the other markets considered in the analysis. Despite its distance and stronger reliance on peasant agriculture for its supply, maize prices in Antequera showed similar if not better signs of market integration to other markets than Guadalajara and Valladolid. Antequera suggests the interdependence of local grain markets even in the absence of direct trade.

Instead of market fragmentation, my findings in Table 18.3 support the idea that there was a certain degree of market integration. This is certainly not the equivalent of a market economy and does not also mean that changes were instantaneous, as they will become later in the nineteenth century, but it points to a certain level of integration in which, within 1–2 years, changes in major markets and common trends affected all corners of the viceroyalty (or at least its central region). A 10% rise in the price of maize in Mexico City increased, within one year, 6.5–8.5% the prices in all other locations. A similar 10% increase in the price of flour in the Gulf markets produced an adjustment of 4.3% in Valladolid and 5% in Mexico City and of a likely similar dimension in San Luis Potosí. Antequera’s maize prices reacted to prices from as far as Guadalajara. Market integration and common economic trends (reflected in the high degree of co-movement of prices) made local prices dependent on changes from other corners of the viceroyalty.

To further corroborate the assertion of a high level of market integration, we compare the findings for Mexico with four international cases in Table 18.4. The speed of adjustment was similar or higher than other contemporary cases. We rely for the comparison on comparable studies (India, Spain, and Western Europe), and our own analysis based on published series (Northeast United States and Mexico at the turn of the twentieth century). The case of Spanish wheat markets is the most revealing in that Mexico and Spain shared similar institutions and a fragmented geography (Coatsworth and Tortella Casares 2002). Market integration was incipient in Spain in the eighteenth century. The price ratios between Spanish wheat markets were stationary, like in Mexico, but the speed of adjustment was much slower: 0.45, implying that the price correction took more than 2 years to close the gap opened by a shock. The speed of adjustment was faster in India wheat and rice markets. The large majority of price ratios were stationary and the adjustment was faster: 0.64 (19 months to correct). Perhaps the halting effect of the Monsoon season on trade, or the fragmentation of authority in this period (the sample includes cities under native and British control) put India in disadvantage in this time period. It was only by the late nineteenth century, when India was unified under one authority and railroads provided fast connections, that the average speed of adjustment became comparable to Mexico’s.

The performance of grain markets in Bourbon Mexico resembles much more that of emerging market economies such as western Europe (Persson 1999) and the northeast United States (Rothenberg 1992), as well as India in the late nineteenth century (Studer 2008). In four maize markets in the United States, price corrections took 15 months. Grain markets in central Mexico, in fact, were comparable with those of the turn of the twentieth century in Mexico (and India) when railroads resolved most of the problems of communication, information flowed much more efficiently and there were no domestic barriers to trade (Dobado and Marrero 2005). Only when we compare Mexico’s annual estimates with monthly estimates from Western Europe, particularly those of the mid and late nineteenth century, do we find that Mexico lagged. The comparison is not straightforward in that the higher frequency of European data provide a more fine-grained analysis and eliminates the bias of the low-frequency data that is present in the other studies that rely on annual series (Studer 2008, p. 412–413; Taylor 2001). The difference between Mexico’s 14-month and Europe’s 12-month adjustments point is remarkably close, even more if we consider the likely time aggregation bias that makes the Mexican estimates higher. All points to the fact that Mexican grain markets did not respond less efficiently than the most integrated grain markets of the time.Footnote 10 It was later in the nineteenth century when it is apparent that Mexican grain markets lagged behind Europe, although only higher frequency data would allow a better comparison.

Where there changes over time? The longer maize prices allow a break-down by subperiods in order to assess how market integration changed over time. A summary of changes in the average speed of adjustment (γ), co-movement (ρ) and the balance in the adjustment of each market is reported in Table 18.5. The periodization pivots in 1780. In the first panel, all available series are used in constructing the average, that is, the second period includes Antequera. In the second panel, only the four markets with long series are used, and the periods have the same dimension. The 1810s were excluded because civil war and the fragmentation of monetary authority very likely had a negative effect on market integration. Given that the frequency is annual, the number of observations is limited and it should therefore be noted that this affects the reliability of the results.

From these data we glean some changes in market integration over time. Panel A shows that the speed of adjustment (γ) and co-movement (ρ) were very similar. When we constraint the comparison to comparable sets and we eliminate the 1810s (Panel B), a picture of improvements in market integration more clearly emerges. The speed of adjustment increased 11 points, from 0.81 to 0.92, and common movements climbed from 0.57 to 0.80. The results are consistent with moderate improvements in market integration from 1780 to 1809. More cases and higher-frequency data would be needed to sort out these hints of tighter integration, but at this point the most important feature that stands out in the equilibrium-correction analysis is the consistently high degree of adjustment throughout the period, and a seeming deterioration in market integration after the outbreak of insurgency in 1810.

18.6 Mutual Adjustment of Maize and Wheat Prices

If markets were efficient in responding to changes in supply and demand, we should not only expect spatial market integration but also an adjustment between prices of substitute products. If maize becomes more expensive, then wheat would become a more attractive substitute; as its demand increases its price would increase as well. We can approach this issue in an equilibrium correction framework as we approached the issue of spatial market integration. Did an equilibrium relationship exist between the price of maize and wheat? If so, how fast did prices adjust to correct a shock?

Table 18.6 displays the results of the equilibrium-correction models for maize and wheat in three markets. The better availability of data for Mexico City makes it possible to use quarterly data to provide a more accurate measurement of the adjustment speed. The coefficients are very consistent across the cases. They all confirm that a long-run equilibrium relationship existed between the prices of the two products. The differential in prices was also significant—wheat was more expensive than maize (about twice, on average, when using the same unit of measurement). Maize adjusted 57–61% of the shock in the equilibrium within one year (using annual data), and the response of the price of wheat is much slower and insignificant outside of Mexico City. The more detailed use of quarterly data enables to identify a faster adjustment than the annual data: within three quarters (9 months) the prices have corrected the shock and restored equilibrium. Overall, the conclusion of this analysis is that the two major cereals in New Spain were not independent of each other. Instead, maize and wheat were part of an integrated grain market in which shocks in the price in one product, or in one region, initiated changes in price levels in other regions and products. The mutual adjustment of maize and wheat markets extended the micro-effects that connected distant markets with each other even in the absence of direct trade.

18.7 Shortages and Market Integration

The issue of market integration is of particular interest when considering the severe droughts, other strong climatic shocks, and recurrent famines that debilitated the Mexican highlands in the late colonial period. In this section I examine the relationship between food shortages and market integration, and I compare the effects of food shortages on the maize and wheat markets. Previously, I showed that famine times were not remarkably different from the point of view of the spread of prices. Here I extend the equilibrium-correction models to gauge the extent to which shortages affected the integration of markets.

The approach I follow here is a cross-panel regression of the price differentials, in which the coefficient for the total speed of adjustment (γ) is interacted with a variable of climatic conditions in order to evaluate their effect on the speed of adjustment.Footnote 11 I proceed by extending Eq. (18.3) (the simplified version of the ECM):

where each market pair combination (i, j) forms a panel, q is pi – pj, C is a binary (“dummy”) variable of climatic conditions that offsets the long-term price differential, ϑ is the interaction term, and μi,j is the pair’s fixed effect. The coefficients γ, φ, and ϑ remain constant for all the pairs because I intend to gauge the common effect of climatic conditions on adjustment speeds and price differentials in all market pairs. Given that the adjustment speeds of the six market-pair regressions were in a similar range, having a fixed γ effect is not a problematic assumption. The sum of γ and ϑ is the adjustment speed under the conditions of climatic adversity.

I use droughts as indicators of climatic conditions. There were 23 years with known droughts in central Mexico, which are marked in a dummy variable. Droughts may have a double effect on grain trade: on the one hand, the increase in prices stimulates long-distance trade, but lack of pasture and more expensive fodder raise transportation costs. I also create another variable to identify the 8 years with famines: 1748–1750, 1785–1786, and 1808–1810. These famines had the lethal climatic combination of summer drought and fall frost that cannot be accurately captured in the drought variable. These generalized famines prompted strong reactions of central and local authorities, mostly to limit trade to guarantee the supply of local producer communities. If famines had a climatic origin, the effect should be similar to a drought; but if they stemmed from increased barriers to trade, then the mutual adjustment of prices should be slower.

The interactions of crisis years and the speed of adjustment, reported in Table 18.7, provide a key insight on how the maize and wheat markets operated. The adjustment during famine years was somewhat slower than in normal years but the difference is not statistically significant. This finding casts doubt on the idea that sharp increases in prices were caused by market failures or that interventionism was a powerful factor in either deterring or stimulating markets. Instead, the results suggest that the market continued to function properly during times of famine conditions. By contrast, the effects of drought conditions on the adjustment speed were significant and the change in adjustment speed was much more pronounced. However, the changes in adjustment speeds for maize and wheat occurred in opposite directions: a drought year slowed down the adjustment in maize prices from 15 to 19 months and accelerated the adjustment of wheat prices from 18 to 12 months.Footnote 12 These differences provide a key insight on the two markets. On the one hand, maize, as a subsistence crop grown in nonirrigated lands was more susceptible to droughts and climatic anomalies. Being so critical to the livelihood of peasants and workers, local communities and even the hacendados were more likely to retain the grain (maize) in times of crisis, which would translate in a slower speed of adjustment. This slower speed of adjustment explains the establishment of grain purchasing commissions in the cities to secure the provisioning of the population (Challú 2013). On the other hand, wheat was less susceptible to climatic risk as it was grown in irrigated lands, and it was predominantly produced in haciendas for the market. The faster adjustment for wheat prices was likely a response to the slower adjustment of maize as cities relied more heavily on wheat under conditions of food shortages caused by drought. While, on average, we found that maize and wheat had similar speeds of adjustments they had a different type of response in drought and normal years.

18.8 Conclusion

I initiated my inquiry into grain market integration with the expectation that Mexican grain markets were segmented relative to other international experiences. I also anticipated a “two gear” grain market, in which the “commercial” crop, wheat, had more price convergence and adjusted faster to shocks than the “subsistence” crop, maize. The prevailing narrative about Mexican grain markets emphasizes prohibitive transportation costs for bulk products such as maize under normal climatic circumstances. This prevailing narrative postulates that wheat, sold at a premium price, was the only viable commercial crop preferred by profit-driven farmers. Similarly, in some accounts maize and wheat are considered separate markets, in which wheat catered to the Spanish population, and maize to the lower classes and natives (Crossgrove et al. 1990). In other related views, markets are presented as broad (encompassing multiple actors), but stunted in that geography and elite collusion created insurmountable barriers (Salvucci 1999). This analysis of prices further challenges these characterizations of grain markets.

The alternative thesis that I present is that Bourbon Mexico had a high degree of grain market integration considering the limitations of its geography, technology, and communications. In the majority of market pairs analyzed here the estimated adjustment speed to shocks to the equilibrium level was close to the theoretical maximum, one. Moreover, the high degree of co-movement of the series (the ρ parameter) suggests that shocks were corrected within a year and that this analysis would benefit from monthly series. From a comparative perspective, the only measure in which Mexico was behind markets usually considered as integrated was the volatility of maize prices, which may well be related to the strong dependence of maize on variable summer rainfall. In all other comparisons price spreads and adjustment speeds compared favorably with other scenarios involving similar distances and geography. Grain markets in Mexico corrected a price disequilibrium faster, for instance, than in Spain and as fast as in other regions of the world. These general conclusions are corroborated by contemporaries who compared Mexico with Europe and did not cast Mexico in a negative light in regard to market integration. For example, Yermo in his report on the state of agriculture after the 1785–86 famine indicated that the grain trade in Mexico was less regulated than in Spain, and that it was such lack of regulation propagated climatic made prices more variable than in Europe (Florescano 1981, p. 620). Likewise, Humboldt criticized the extent of poverty and inequality in Mexico, but he praised the supply of grain to the cities (Humboldt 1811, p. 444–483).

Despite the prevailing view of fragmented markets, my findings on Mexican grain markets as integrated and efficient for their time is consistent with a historical scholarship that has revealed a high degree of versatility in the Mexican economy in this period. Commercial organization was more sophisticated and had more complex trade networks than previously thought, featuring a growing degree of specialization (Gálvez and Ibarra 1997; Miño Grijalva 2001; Moreno Toscano 1998; Van Young 1981); financial instruments facilitated long-distance and inter-temporal transactions (Pérez Herrero 1988); a well-organized and efficient transportation industry, the arriería, connected local markets despite tremendous geographic obstacles (Suárez Argüello 1997). The efficiency of grain markets challenges the notion that Mexican underdevelopment can be traced to backward institutions or an immutable colonial legacy (Sokoloff and Engerman 2000). Instead, our findings highlight the deep roots of markets in Mexico (Coatsworth 1978, 2008; Tutino 2011).

While it is true that the tyranny of distance limited the scope of most grain transactions to short distances, I have shown that the connections between grain markets extended over long distances throughout central Mexico. All corners of central Mexico were interconnected, making a large regional focus such as this one is an appropriate and necessary scale to examine food supply. The precise nature of these interconnections escapes the possibility of a quantitative analysis, but the major mechanisms that connected distant markets likely involved the integration of maize and wheat markets and chain connections between intermediate markets. Wheat markets operated at longer distances and likely sped up the price adjustments in the substitute product (maize). In another place, I showed a dense mesh of social and geographic relationships that substantiates the hypothesis that chained connections at the local sphere created indirect links between distant markets (Challú 2013).

The indicators of market integration did not change in major ways in the period under analysis. The higher degree of co-movement of prices, as well as the more balanced adjustment from 1780 to 1809 indicate small improvements in market integration, but volatility and dispersion of prices remained similar over time. In this, late colonial Mexico is no different than other areas in the world, since it is in the nineteenth, not the eighteenth century, when the revolution in grain markets took place as improvements in transportation first integrated national markets, and then international markets (Bateman 2011; Federico et al. 2021; O’Rourke and Williamson 1999). But this is not to say that nothing changed before the transportation revolution. Federico et al. (2021) convincingly argue that there were integrating forces operating in the early modern period and the eighteenth century in Europe, while Dobado-González et al.’s (2012) analysis of Atlantic wheat markets find substantial progress in market integration over the eighteenth century. All maize price series show a simultaneous and significant increase in prices in the 1780s and the 1800s, suggesting that actors adjusted their expectations of the equilibrium price upwards. Because all markets were well integrated and prices adjusted to each other, the inflationary trend affected the entire territory and did not spare even those rural areas with abundant supply. The 1810s were also a time in which markets lost the high degree of integration of previous years, a finding that coincides with existing knowledge about the disruption of markets and the fragmentation of monetary authority (Irigoin 2010). Economic policies and political arrangements that favored trade to supply cities and mining centers seem to be particularly relevant in creating the conditions for market efficiency that we see in this study (Federico 2018, p. 23).

At the time when markets were still successfully integrated prior to 1810, there were both positive and negative results for average Mexicans trying to meet their nutritional demands. Due to the ability to trade across significant distances a good harvest in a given area likely lowered prices in other areas. And yet the opposite was also true. A rising urban population and an increase in inequality that favored those with higher purchasing power created a demand for marketable food; in the countryside, the increasing power of landowners and the loss of autonomy in peasant agriculture similarly skewed the access to food. As prices raised in the last quarter of the eighteenth century due to increased demand and limitations in supply, the urban dwellers found an advantage in attaining grain because rural producers would be more motivated to sell scarce crops to the higher bidder in urban areas, as opposed to those in other rural districts with less purchasing power. Integrated markets helped the urban population and underlie the relative declines in wellbeing for rural dwellers as well as the immigration to the cities.

18.9 Appendix: Challú on Murray

John Murray and I met regularly in the late 2000s. He was a Professor of Economics at the University of Toledo, and I was an Assistant Professor of History at Bowling Green State University. We first met at the annual conference of the Economic History Association, and we then started meeting more regularly, eventually in the context of a formalized mentoring grant that let us carve out time for meetings and discussion of work in progress. John was not only encouraging but also an inspiration and a springboard for ideas about how I was approaching the study of grain markets in late colonial Mexico. I particularly recall with joy our discussion of panels on market integration at the World Economic History Congress in Utrecht in 2009. Later, John and I discussed the findings and arguments that I eventually put into this chapter. His influence is reflected in two ways. First, John was interested in studies of market integration that exceeds the traditional use of price convergence and that emphasizes the importance of policies and political arrangements, as demonstrated in the joint study of John and Javier Silvestre on European coal markets. Second, John also encouraged me to connect economic arguments, social history, and narrative. I hope that this contribution honors his legacy.

Notes

- 1.

Archivo General de Indias [Seville, Spain], Indiferente General, 1560, report from Guadalajara, February 1795.

- 2.

Federico (2018) distinguishes price convergence as the outcome of integrated markets, and the speed of adjustment as an indicator of market efficiency. Both measures, convergence and speed of adjustment, are the key metrics to compare and assess the integration of markets.

- 3.

- 4.

In smaller markets this is even more true, as it is illustrated in the semester reports of harvests and prices in the case of Tepatitlán, with which we opened the chapter. On market size and volatility, see Salvucci and Salvucci (1987, p. 78).

- 5.

Use of alternative subsets using isolated observations (e.g. from Antequera, Puebla or Zacatecas) from other locations does not change these conclusions.

- 6.

The calculation for the United States is based on the series of Maryland, Massachusetts, Pennsylvania and Vermont, via “Global Price and Income History,” http://gpih.ucdavis.edu

- 7.

Using data kindly facilitated by Rafael Dobado, the average coefficient of variation in maize prices for a similar subset of locations was 19%, that is, an improvement in ten points from our figures.

- 8.

In a standard regression, Eq. (18.3) becomes ∆(p1,t – p2,t) = a + b * (p1,t–1 – p2,t–1) + εt, where b = γ, a = γτ; b is expected to be negative.

- 9.

The greater reliance of storage in wheat trade may explain its slightly slower speed of adjustment (Shiue and Keller 2007, p. 1204).

- 10.

China also had a high degree of market integration in this time period, but the metric is not comparable (Shiue and Keller 2007). Another comparative point is Froot et al. (2019), which studied deviations from the law of one price in annual differentials of commodity prices between England and Holland from the fourteenth to the twentieth century. Their approach is similar to our Eq. (18.3) but without a constant (that is, plain deviations from the law of one price). The γ for their entire period (from the fourteenth to the twentieth century) is 0.21; our average γ using the same methodology (averaged across all our maize and wheat market pairs) is 0.39.

- 11.

- 12.

El Niño events had similar effects but lacked statistical significance.

References

Bateman VN (2011) The evolution of markets in early modern Europe, 1350–1800: a study of wheat prices. Econ Hist Rev 64:447–471

Challú AE (2007) Grain markets, food supply policies and living standards in late colonial Mexico. Harvard University, Cambridge

Challú AE (2010) The great decline: biological well-being and living standards in Mexico, 1730–1840. In: Salvatore RD, Coatsworth JH, Challú AE (eds) Living standards in Latin American history: height, welfare, and development, 1750–2000. Harvard University David Rockefeller Center for Latin American Studies, Cambridge, pp 23–67

Challú AE (2013) Grain markets, free trade and the Bourbon reforms: the real Pragmática of 1765 in new Spain. Colon Lat Am Rev 22:400–421

Coatsworth JH (1978) Obstacles to economic growth in nineteenth-century Mexico. Am Hist Rev 83:80–100

Coatsworth JH (1989) Comments on “The economic cycle in bourbon central Mexico: a critique of the Recaudación del diezmo líquido en pesos,” by Ouweneel and Bijleveld. II. Hispanic Am Hist Rev 69:538–545

Coatsworth JH (2008) Inequality, institutions and economic growth in Latin America. J Lat Am Stud 40:545–569

Coatsworth JH, Tortellas Casares G (2002) Institutions and long-run economic performance in Mexico and Spain, 1800–2000. Paper prepared for presentation at the XIIIth Congress of the International Economic History Association, Buenos Aires, Argentina, July 2002

Crossgrove W, Egilman D, Heywood P, Kasperson J, Messer E, Wessen A (1990) Colonialism, international trade, and the nation-state. In: Newman LF, Crossgrove W, Kates RW, Matthews R, Millman S (eds) Hunger in history: food shortage, poverty and deprivation. Wiley-Blackwell, New York, pp 215–240

Dobado R, Marrero GA (2005) Corn market integration in Porfirian Mexico. J Econ Hist 65:103–128

Dobado-González R, García-Hiernaux A, Guerrero DE (2012) The integration of grain markets in the eighteenth century: early rise of globalization in the west. J Econ Hist 72:671–707

Ejrnæs M, Persson KG (2000) Market integration and transport costs in France 1825–1903: a threshold error correction approach to the law of one price. Explor Econ Hist 37:149–173

Espinosa Morales S (1995) Análisis de precios de los productos diezmados. El Bajío oriental. 1665-1786. In: García Acosta V (ed) Los Precios de Alimentos y Manufacturas Novohispanos. Mexico City, Centro de Investigaciones y Estudios Superiores en Antropología Social and Instituto Mora, pp 122–172

Farris N (1982) Maya society under Spanish rule. Princeton University Press, Princeton

Federico G (2018) Market integration. In: Diebolt C, Haupert M (eds) Handbook of cliometrics. Springer, Berlin, pp 1–26

Federico G, Schulze MS, Volckart O (2021) European goods market integration in the very long run: from the black death to the first World War. J Econ Hist 81:276–308

Florescano E (1981) Fuentes para la historia de la crisis agrícola de 1785–1786. Archivo General de la Nación, Mexico City

Florescano E (1995) Breve historia de la sequía en México. Universidad Veracruzana, Xalapa

Froot KA, Kim M, Rogoff K (2019) The law of one price over 700 years. Ann Econ Financ 20:1–35

Gálvez MA, Ibarra A (1997) Comercio local y circulación regional de importaciones. La feria de San Juan de Lagos en la Nueva España. Hist Mex 46:581–616

Garner R (1993) Economic growth and change in bourbon Mexico. University Press of Florida, Gainesville

Grafe R (2012) Distant tyranny: markets, power, and backwardness in Spain, 1650–1800. Princeton University Press, Princeton

Hamnett BR (1986) Roots of insurgency: Mexican regions, 1750–1824. Cambridge University Press, Cambridge

Humboldt A (1811) Political essay on the Kingdom of New Spain. Longman, Hurst, Rees, Orme, and Brown, London

INEGI (2014) Estadísticas Históricas de México. INEGI, Mexico City

Irigoin A (2010) Las raíces monetarias de la fragmentación política de la América española en el siglo XIX. Hist Mex 59:919–979

Jacks DS (2005) Intra- and international commodity market integration in the Atlantic Economy, 1800–1913. Explor Econ Hist 42:381–413

Klein H, Engerman SL (1990) Methods and meanings in price history. In: Johnson L, Tandeter E (eds) Essays on the price history of eighteenth-century Latin America. University of New Mexico Press, Albuquerque, pp 9–21

Li LM (1992) Grain prices in Zhili province, 1736–1911: preliminary study. In: Rawski TG, Li LM (eds) Chinese history in economic perspective. University of California Press, Berkeley, pp 69–99

Li LM (2000) Integration and disintegration in North China’s grain markets, 1738–1911. J Econ Hist 60:665–699

Lindo-Fuentes H (1980) La utilidad de los diezmos como fuente para la historia económica. Hist Mex 30:273–289

Llopis Agelán M (2001) El mercado de trigo en Castilla y León, 1691–1788: arbitraje espacial e intervención. Historia Agraria 25:13–68

Llopis Agelán E, Sotoca S (2005) Antes, bastante antes: La integración del mercado español del trigo, 1725–1808. Historia Agraria 36:225–262

MacKinnon JG (1996) Numerical distribution functions for unit root and cointegration tests. J Appl Econ 11:601–618

Marks RB (1998) Tigers, rice, silk, and silt: environment and economy in late imperial South China. Cambridge University Press, Cambridge

Martín Ornelas JM (2008) La organización económica regional y el abasto urbano: el trigo y el maíz en Zacatecas, 1749–1821. Universidad Autónoma de Zacatecas, Zacatecas

Miño Grijalva M (2001) El mundo novohispano: Población, ciudades y economía, siglos XVII y XVIII, Fideicomiso Historia de las Américas. El Colegio de México, Fondo de Cultura Económica, Mexico City

Moreno Toscano A (1998) Economía regional y urbanización: ciudades y regiones en Nueva España. In: Silva Riquer J, López Martínez J (eds) Mercado Interno En México. Siglos XVIII–XIX. Instituto Mora, Mexico City, pp 64–93

Morin C (1979) Michoacán en la Nueva España del siglo XVIII: Crecimiento y desigualdad en una economía colonial. Fondo de Cultura Económica, Mexico City

O’Gráda C (2000) Black ‘47 and beyond: the great Irish famine in history, economy, and memory. Princeton University Press, Dublin

O’Grada C (2003) Adam Smith and Amartya Sen: markets and famines in pre-industrial Europe. Working Paper

O’Gráda C, Chevet JM (2002) Market segmentation and famine in ancien régime France. J Econ Hist 62:706–733

O’Rourke KH, Williamson JG (1999) Globalization and history: the evolution of a nineteenth-century Atlantic economy. MIT Press, Cambridge

Pérez Herrero P (1988) Plata y libranzas: la articulación comercial del México borbónico. Centro de Estudios Históricos and Colegio de México, Mexico City

Persson KG (1999) Grain markets in Europe 1500–1900: integration and deregulation. Cambridge University Press, Cambridge

Ravallion M (1986) Testing market integration. Am J Agr Econ 68:102–109

Reher DS (2001) Producción, precios e integración de los mercados regionales de grano en España. Revista de Historia Económica 19:539–572

Roehner BM (2000) The correlation length of commodity markets 1. Empirical evidence. Eur Phys J B 13:175–187

Rothenberg WB (1992) From market-places to a market economy: the transformation of rural Massachusetts, 1750–1850. University of Chicago Press, Chicago

Salvucci R (1999) Agriculture and colonial heritage. In: Adelman J (ed) Colonial legacies: the problem of persistence in Latin American History. Routledge, New York

Salvucci R, Salvucci L (1987) Crecimiento económico y cambio de la productividad en México, 1750-1895. HISLA. Revista Latinoamericana de Historia Económica y Social 10:67–89

Sennhauser RW (1996) Veracruz y el comercio de harinas en el Caribe español, 1760–1830. Estudios de historia social y económica 13:107–122

Shiue CH, Keller W (2007) Markets in China and Europe on the eve of the industrial revolution. Am Econ Rev 97:1189–1216

Sokoloff KL, Engerman SL (2000) History lessons: institutions, factor endowments, and paths of development in the new world. J Econ Perspect 14:217–232

Stein SJ, Stein BH (2003) Apogee of empire: Spain and New Spain in the age of Charles III, 1759–1789. Johns Hopkins University Press, Baltimore

Studer R (2008) India and the great divergence: assessing the efficiency of grain markets in eighteenth-and nineteenth-century India. J Econ Hist 68:393–437

Suárez Argüello CE (1985) La politica cerealera en la economía novohispana: el caso del trigo. Centro de Investigaciones y Estudios Superiores en Antropología Social, Mexico City

Suárez Argüello CE (1997) Camino real y carrera larga: la arriería en la Nueva España durante el siglo XVIII. Centro de Investigaciones y Estudios Superiores en Antropología Social, Mexico City

Taylor AM (2001) Potential pitfalls for the purchasing-power-parity puzzle? Sampling and specification biases in mean-reversion tests of the law of one price. Econometrica 69:473–498

Tutino J (2011) Making a new world: founding capitalism in the Bajío and Spanish North America. Duke University Press, Durham

Van Young E (1981) Hacienda and market in eighteenth-century Mexico: the rural economy of the Guadalajara Region, 1675–1820. University of California Press, Berkeley

Wong RB, Perdue PC (1992) Grain markets and food supplies in eighteenth-century Hunan. In: Rawski TG, Li LM (eds) Chinese history in economic perspective. University of California Press, Berkeley, pp 126–144

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2022 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this chapter

Cite this chapter

Challú, A.E. (2022). Grain Market Integration in Late Colonial Mexico. In: Gray, P., Hall, J., Wallis Herndon, R., Silvestre, J. (eds) Standard of Living. Studies in Economic History. Springer, Cham. https://doi.org/10.1007/978-3-031-06477-7_18

Download citation

DOI: https://doi.org/10.1007/978-3-031-06477-7_18

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-06476-0

Online ISBN: 978-3-031-06477-7

eBook Packages: Economics and FinanceEconomics and Finance (R0)