Abstract

In this chapter, we propose a novel methodology that aims at establishing what is the role of “location” in shaping firm growth. Along with the traditional determinants (like, e.g., age, size, financial constraints and others), geographical location is alleged to drive firm growth. The current literature typically relies on location variables that suffer from a lack of empirical robustness (Duranton and Overman, Testing for Localisation Using Micro-geographic Data, The Review of Economic Studies, 72: 1077–1106, 2005; Arbia et al., Clusters of Firms in an Inhomogeneous Space: The High-Tech Industries in Milan. Economic Modelling, 29(1): 3–11, 2012). Indeed, the use of administrative partitions to test such hypotheses (such as provinces, regions and municipalities) introduces a statistical bias arising from the arbitrariness of their definition. To disentangle these shortcomings, we make use of a locational measure based on the Getis’ local K-function (Getis, Interaction Modelling Using Second-Order Analysis. Environment and Planning A, 16: 173–183, 1984). This measure allows us to distinguish between Marshallian and Jacobs spatial externalities which exert their effects at different distances. Our empirical analysis focuses on a database which includes 8300 Italian limited liabilities manufacturing companies observed in the period from 1996 to 2004. Our empirical results show that the relationship between firm growth and spatial factors is complex and it depends on the structural characteristics of firm as well as from the spatial scale of geographical analysis.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

Jel Codes

1 Introduction

The New Economic Geography reckons that localization economies and urbanization economies are important phenomena (Krugman 1991; Glaeser et al. 1992; Arbia 2001; Audretsch and Dohse 2007), but empirical studies adopting this framework do not offer clear insights on how such spatial effects differently affect firms that are not comparable in terms of structural dimensions and behavioral aspects (Fujita et al. 1999; Frenken et al. 2014). A few exceptions relate to studies that take into account the location of the firm and the nature of geographical interactions among firms in a local context (Duschl et al. 2011; Barbosa and Eiriz 2011; Antonietti et al. 2013).

Indeed, the presence of positive externalities in a region does not guarantee that all the firms in that region benefit from them, or at least not to the same extent. More specifically, externalities can produce different effects on growth dynamics if we consider (a) small firms (SMFs) as opposed to large ones and (b) young firms as opposed to older ones (Brown and Rigby 2010).

Firms growth, as measured by employment growth, is often the objective variables in this field of research (Beaudry and Swann 2009; Beaudry and Schiffauerova 2009; Raspe and Van Oort 2008, 2011).Footnote 1 Theoretically, location within a geographically concentrated area, or an agglomeration, may result into greater firm efficiencies due to labor market pooling, to the provision of non-traded inputs, or to the development of specialized intermediate goods knowledge externalities and knowledge spillovers. These locational advantages may foster regional growth supporting the expansion of individual firm (Audretsch and Dohse 2007). In addition, vertical relationships in downstream markets can entail the expansion of firms—in particular small firms—driving the growth of sales. Taking into account the dynamics of innovation processes, we can postulate that the diversity of complementary economic activity is more conducive to growth than specialization (Glaeser et al. 1992; Feldman and Audretsch 1999). Indeed, we expect that localization economies stimulate incremental and process innovations, thus leading to higher productivity. In contrast, Jacobs economies are expected to spur more radical innovations through the recombination of existing knowledge, thus leading to the creation of new employment (Frenken et al. 2007). This effect, in turn, would imply that employment growth would benefit from diversification, while productivity would increase with specialization of industrial activities. Despite the richness of theoretical paradigms, however, there is still little empirical evidence on the impact of location on growth at the firm level (Acs and Armington 2004).

The present chapter proposes a new approach to empirically assess the role of localization and agglomeration economies in shaping the patterns of firm growth. In particular, our method is based on the use of firm-level measures of specialization and diversity (based on the local K-function; see Getis 1984) associated to the specification of a quantile regression.

In line with a recent stream of literature which makes use of distance-based measures (see Duranton and Overman 2005; Espa et al. 2013; Arbia et al. 2010, 2012; Marcon and Puech 2010), the Getis local K-function (Getis 1984; Getis and Franklin 1987) can be used to define firm-level indicators able to endogenize the emergence of spatial externalities and to overcome two methodological shortcomings of region-level measures, namely (a) the arbitrary definition of the spatial observational units (such as provinces, regions and municipalities) and (b) the restrictive assumption of spatial homogeneity within regions. We argue in favor of the use of the local K-function to empirically distinguish between Marshall-Arrow-Romer externalities (MAR) and Jacobs externalities (JAC). The former refers to knowledge spillovers accruing to firms operating in the same industry, while the latter are pure agglomeration economies arising from knowledge spillover external to the industry in which the local firm operates. Moreover, the local K-function-based measure allows us to detect (separately, but simultaneously) the two types of externalities. This is of primary importance given that previous studies have shown that both kinds of externalities can coexist and can differently affect business enterprises (Beaudry and Schiffauerova 2009).

The empirical analysis reported in this chapter is found on a database of limited liabilities, single-unit manufacturing firms located in Italy in the period 1994–2006. The individual level of observation allows us to effectively study the organic growth of firms and the role of spatial and geographical factors. In particular, we aim at disentangling how much the different kinds of geographical externalities (MAR and JAC externalities) are in place for the different kind of firms of our sample in the time window under investigation.

Our investigation produced a series of interesting results that can be summarized as follows. First of all, small firms experiencing a growth rate above the average benefit more from MAR externalities at long range than from JAC externalities at shorter distance. Secondly, these small firms grow faster than other firms because the effect of MAR externalities on them is bigger. Thirdly, small firms that shrink do not benefit at all from MAR, but only benefit from medium range JAC externalities. Fourthly, small firms that perform extremely bad in terms of employment growth, suffer from short-range MAR. Finally, MAR and JAC externalities bear negligible effects on both medium and large firms.

The rest of the present chapter is organized as the following. Section 4.2 discusses the literature about geographical determinants of firm growth. Section 4.3 explains the methodologies employed for the investigation. Section 4.4 describes the database used. Results are presented in Sect. 4.5. Section 4.6 concludes.

2 The Spatial Determinants of Firm Growth

There are two kinds of reasons why location can be postulated to play a crucial role on the growth of firms. On one side, industries can specialize geographically, due to the fact that proximity (1) favors the intra-industry transmission of knowledge, (2) reduces transport costs of inputs and outputs and (3) allows firms to benefit from a more efficient labor market. Firstly, introduced by Marshall (1890), this approach was further developed into the Marshall–Arrow–Romer (MAR) model (Glaeser et al. 1992; Henderson et al. 1995).

The MAR model states that concentration of an industry in a geographical context facilitates knowledge spillovers between firms and promotes innovation. Indeed, the sectoral specialization encourages the transmission and exchange of tacit or codified knowledge and information that depend on distance (Griliches 1992). Knowledge spillovers are geographically bounded in the place where the knowledge is created (Autant-Bernard 2001; Feldman and Audretsch 1999), alongside the imitation activity, the business interactions and the interfirm circulation of skilled workers. Moreover, economies of scale can be generated from input-sharing activity (e. g. labor equipment and infrastructure) among firms of the same industry (Krugman 1991). All these phenomena can be labeled as localization externalities (or MAR externalities), and they are likely to arise when an industry is relatively large with respect to the whole economy (Frenken et al. 2007).

On the other side, Jacobs (1969) suggests that the sources of knowledge spillovers are external to the industry. Indeed, according to Jacobs (1969) it is the diversity of knowledge within a geographical context which is relevant, because the variety of industries within a geographic region promotes knowledge externalities and innovative activity and leads to economic growth. In this respect, the urban agglomerations play a key role. Therefore, a diversified local production structure gives rise to diversification externalities (called “Jacobs externalities”).Footnote 2

Spatial concentration may affect both the productivity and the growth of firms. Nonetheless, productivity and growth are shaped in a different way by MAR and JAC externalities. Employment growth and innovation would benefit from diversification, while productivity would increase with specialization of industrial activities. In particular, Jacobs economies should spur radical innovations and product innovation (recombination and cross-fertilization of existing knowledge) that lead to new employment creation (Frenken et al. 2007).

Empirical evidence on the effect of localization economies and MAR externalities on the one side and urbanization economies and Jacobs externalities on the other produced different evidences (Frenken et al. 2014). Beaudry and Swann (2009) found, for UK industries, a positive effect of own-sector employment. Maine et al. (2010) find that in the high-technology sectors, firm growth is negatively related to the distance of each firm from the top-ten firms in a cluster (localization diseconomies). Furthermore, younger, and particularly new, firms benefit more from localization economies in terms of growth than older firms (Rosenthal and Strange 2005; Brown and Rigby 2010). Wennberg and Lindqvist (Wennberg and Lindqvist 2010) find evidence of localization economies both in manufacturing and in services sectors. Raspe and Van Oort (2008) study on Dutch firms suggests that agglomeration economies have a positive effect on firm growth in an R&D-intensive environment. Finally, Staber (2001) shows that MAR externalities are present in sectors where knowledge spillovers are present, for example high technology sectors.

Empirical studies concerning Italian firms have mainly focused on size, age and R&D activities (Del Monte and Papagni 2003) as major determinants of growth. They have neglected, at least partially, the second group of determinants. Contini and Revelli (1988) find a negative impact of extant size over the employment growth of manufacturing firms located in the Northern Italy over the period 1980–1986. Similarly, Becchetti and Trovato (2002) estimate a negative growth-size relationship for small and medium-sized Italian manufacturing firms that survive during the 1995–1997 period. Nevertheless, when non-surviving firms are included in the sample, they obtain a significant effect of size on growth rates only for companies employing between 10 and 50 employees, while the workforce expansion of firms with more than 100 employees seems to be independent of size. Del Monte and Papagni (2003) strengthen this last finding by showing that the independence assumption postulated in Gibrat’s Law (Gibrat 1931) is empirically validated in a sample of more than 650 large manufacturing firms examined over the period 1989–1997. Lotti et al. (2003) provide a comprehensive picture of growth patterns for a sample of 1570 manufacturing firms born in January 1987 and tracked until 1993. The study outlines that, in five of the six industrial sectors considered, smaller firms grew faster than their larger counterparts over the entire period 1987–1993, as well as in the year that immediately followed the start-up. Nonetheless, as soon as new entrants approach an acceptable size that shields them from the risk of failure, Gibrat’s Law seems to be reestablished, thus implying no significant difference in the growth behavior between small and large firms.

3 Methodology

This study proposes a series of firm-level regression models in order to investigate the role of internal and external factors on firms growth rates. In particular, we use a quantile regression approach in which the dependent variable is represented by the firm growth rate regressed against internal, external and spatial determinants of growth. Internal and external factors of growth are selected according to the existing literature, while spatial factors are investigated using firm-level measures of agglomeration and localization, that allow us to overcome the limitations arising from the use of aggregate indices and traditional spatial econometric models. Moreover, we estimate separate quantile regression models for small firms (less or equal to 50 employees) and medium and large firms (more than 50 employees) to uncover variations in the impact of spatial factors on firms of different size.

3.1 Measures of Spatial Interaction

3.1.1 The Limits of Regional and Aggregate Measures

We argue that the locational measures commonly used by researchers—such as the Gini (Gini 1912, 1921), Hirschman-Herfindahl (Hirschman 1945), Location Quotient (Florence 1939) and Ellison-Glaeser (Ellison and Glaeser 1997) indices—may not be adequate. In particular, they are computed on regional aggregates built on arbitrary definitions of the spatial observational units (such as provinces, regions and municipalities). Hence, they introduce a statistical bias arising from the discretionally chosen definition of space (i.e., the so-called modifiable areal unit problems bias; see Arbia 1989). As an evidence of that, in reviewing the relevant literature, Beaudry and Schiffauerova (2009) found that the emergence and intensity of agglomeration externalities are strictly dependent on the level of spatial aggregation of data.

3.1.2 A Firm-Level Measure of MAR Externalities

To build up an indicator that opportunely captures Marshall externalities, we rely on the well-established idea in the literature (Glaeser et al. 1992) that the degree of specialization of an industry (rather than its size) can better embody the potential for Marshall externalities in that it expresses the intensity and the density of interactions among firms (Beaudry and Schiffauerova 2009). Accordingly, we build a firm-level distance-based measure of industry specialization that captures the firm’s potential for Marshall externalities. We propose the use of the Getis local K-function (Getis 1984), a statistical measure assessing the degree of spatial interactions among geo-referenced locations. Indeed, in the context of micro-geographic data, which are identified by maps of point events (as represented by their longitude/latitude coordinates), Getis local K-function is an explorative tool that summarizes the characteristics of a spatial distribution of point events relative to its location. If the events of interest are firms (as in our case), this measure allows to statistically test if a given individual firm is localized into a cluster.

For the given ith firm located in a geographical area, the local K-function can be defined as follows:

where E{.} indicates the expectation operator; the term d ij is the Euclidean distance between the ith and jth firms’ locations; I(d ij ≤ d) represents the indicator function such that I = 1 if d ij ≤ d and 0 otherwise; d is a threshold distance and λ represents the mean number of firms per unitary area: a parameter called spatial intensity. Given definition (1), the term λK i(d) can be interpreted as the expected number of further firms located up to a distance d from the ith firm. The local K-function quantifies the degree of spatial interaction between the ith firm and all other firms at each possible distance d, and hence can be exploited to develop a proper locational measure of industry specialization.

Henderson (2003) established that both the number of firms and the level of employment in a region are key determinants of the generation of spillovers within the region. For this reason, we introduce weights in Eq. (4.1) so as to be able to account for the number of employees in each firm. Thus, we obtain the following weighted version of the local K-function,

where e i and e j denote the number of employees of the ith and jth firms, respectively, and μ is the mean number of employees per firm. Therefore, the term λμ 2WK i(d) can be interpreted as the mean of the sum of the products formed by the number of employees of the ith firm and the number of employees of all other firms located up to a distance d of the ith firm.

Turning now to the estimation aspects, following Getis (1984), Getis and Franklin (1987) and Penttinen (2006), a proper unbiased estimator of WK i(d) for a study area containing n firms is given by:

where \( \hat{\lambda} \) is the estimated spatial intensityFootnote 3 and \( \hat{\mu} \) is the mean number of employees per firm computed on the n observed firms. Due to the presence of edge effects arising from the bounded nature of the study area, an adjustment factor, say w ij, is introduced, thus avoiding potential biases in the estimates close to the boundaries.Footnote 4 The adjustment factor w ij expresses the reciprocal of the proportion of the surface area of a circle centered on the ith firm’s location, passing through the jth firm’s location, which lies within the area A (Boots and Getis 1988).

As the last step, we use the function expressed in Eq. (4.3) to obtain a measure of industry specialization with the possibility of specifying a benchmark value allowing to assess if the ith firm is located in a specialized or despecialized industrial area. The most popular approach in the literature (see e.g. Beaudry and Schiffauerova 2009) has been to refer to a relative benchmark, in which an industry in a region is considered specialized (or, alternatively, despecialized) if it is overrepresented (or underrepresented) within the region with respect to the entire economy. A relative measure allows to control for the presence of spatial heterogeneity in the study area and hence is able to identify industry specialization due to the interactions among economic agents (see e.g. Arbia et al. 2012 and Espa et al. 2013).

In light of these considerations, in order to measure firm-level relative industry specialization, we can use the following statistics:

where \( W{\hat{K}}_{i,\mathrm{sector}}(d) \) is the weighted local K-function estimated on the firms belonging to the same sector of activity of the ith firm and \( {\hat{K}}_{i,\mathrm{all}}(d) \) is the weighted local K-function estimated on all firms of the dataset. If, at a given distance d, Kmar i(d) tends to be close to 1, then the ith firm is located in an area (with a spatial extension of radius d) where economic activities are randomly and independently located from each other, implying absence of industry specialization. W, at a given distance d, the functional expressed in Eq. (4.4), is greater than 1, the ith firm is located in a cluster with a spatial extension of d where the firms of its sector of activity are more concentrated than all firms of the dataset, implying presence of industry specialization. Conversely, when at a given distance d, Kmar i(d) is less than 1, the ith firm is located in a dispersed area, where the firms of its sector of activity are less concentrated than all firms of the dataset, implying presence of industry despecialization.

The functional expressed in Eq. (4.4) thus represents a relative measure in that the benchmarking value of random localization is represented by the spatial distribution of all economic activities. Hence, a specific sector exhibits specialization (or despecialization) if its spatial distribution is more concentrated (or dispersed) than the spatial distribution of all economic activities. Therefore, it represents a micro-geographic firm-level version of the Location Quotient and, hence, a proper measure to assess the working of MAR externalities.

3.1.3 A Firm-Level Measure of Jacobs Externalities

Let’s now turn to discuss how to properly measure Jacobs’ externalities. There is a wide consensus in the literature that a proper way to capture this second typology of externalities is through variables representing the extent of diversity of spatially close industries (see Beaudry and Schiffauerova 2009 among others). Coherently, in order to assess the effect of Jacobs externalities, we propose a firm-level distance-based measure of relative locational diversity. Similar to the case of the industry specialization index, we rely on the weighted local K-function. However, here we argue that a proper diversity measure may be provided by the following expression:

where \( W{\hat{K}}_{\overline{i,\mathrm{sector}}}(d) \) is the weighted local K-function estimated on the firms which do not belong to the same sector of activity of the ith firm and \( W{\hat{K}}_{i,\mathrm{all}}(d) \) is the local K-function estimated on all firms of the dataset.

Clearly, Kjac i(d) = 1 represents the benchmark value corresponding to the case of absence of locational diversity. As a result, when Kjac i(d) > 1 the ith firm is located in a cluster with a spatial extension of d where the firms of the other sectors of activity are more concentrated than all firms of the dataset, implying presence of locational diversity.

Conversely, when Kjac i(d) < 1, the ith firm is located in a dispersed area, where the firms of the other sectors of activity are less concentrated than all firms of the dataset, implying presence of locational uniformity. We argue that Kjac i(d) represents a proper measure to assess the working of Jacobs externalities and it is a micro-geographic firm-level version of the Hirschman–Herfindahl index.

3.2 The Model

In this section, we will use the quantile regression approach to present a model linking the locational effects to firm growth. Indeed, it is well known that the growth rates distribution of firms departs significantly from the normal distribution (Bottazzi et al. 2007) so that a standard linear regression model does not seem appropriate because, in this case, the residuals would depart from the assumption of normality. As a consequence, the linear regression model may provide, at best, point estimates of the average effect of the independent variables on the “average firm.” However, the focus on the average firm could hide important features of the underlying relationship given the existence of fat tails in the growth rates distribution (Coad 2007; Coad and Rao 2008). In particular, we aim at investigating the role of firms that have different size and exhibit different abilities to grow (Birch and Medoff 1994).

The quantile regression approach (Koenker and Hallock 2001) permits to estimate the differential effects of a series of independent variables on an objective variable for different quantiles of the distribution of the dependent variable.

We estimate two sets of quantile regressions separately for small and medium-large firms (MLFs) because the literature suggests that the growth behavior of the two groups might be very different (Haltiwanger et al. 2013). In the case of our working dataset, indeed, the range of growth rates for the two groups is very diverse: growth rates of small firms range from around—16% in the lower quantile (20% of all the sample of small firms) to 16.7% in the upper quantile, whereas medium-large firms appear to be more inertial in terms of contractions as measured by the number of employees—they contract at most of around 10%—and grow on average less than smaller firms—15.8% the upper quantile.

We concentrate on regressions of the following quantiles of the growth rate distribution: q25, q50 and q90. The full model is based on the common econometric model used to evaluate the growth performance of business firm (Hall 1987; Audretsch and Dohse 2007; Coad and Rao 2008) but is “augmented” with a set of firm-level indicators that allow to investigate the different aspects of spatial and geographical distribution of firms:

where the dependent variable Δs i, t represents the rate of growth of the i-th firm from year t−1 to year t calculated as difference in logs of size of firm i at year t and size of firm i at year t−1. In addition, in Eq. (4.6) the terms Kmar i, t(d) and Kjac i, t(d) represent the two measures of externalities introduced in the preceding Sect. 4.3.1. In particular, Kmar i, t(d) (for d = 5, 50 and 100 km) represents the firm-specific measures of industry specialization used to assess the effect of Marshallian externalities at short, medium and long range, while Kjac i, t(d) (for d = 5, 50 and 100 km) are the firm-specific measures of locational diversity used to assess the Jacobian externalities (agglomeration effects) related with the economies of urbanization at different distance ranges.

Among the other regressors SP i represents a vector of additional aggregate measures of spatial interactions. Indeed, it should be noted that the specialization and locational diversity explanatory variables to capture agglomeration externalities are firm level and hence computed using data deriving from the firms of our sample. As already mentioned, our sample excludes the multiplant firms, which typically consist of big multinational corporations. This exclusion may cause an underestimation of the two variables and, as a result, a downward bias in the estimate of the associated regression parameters. In order to control for this potential bias, we cover the whole extent of economic activity, and proxy for the latent information about the multiplant firms, using regional aggregated data. In particular, we compute region-level indicators of specialization and diversity. As an indicator of specialization, we employ the common “location quotient” (LQ) which, for a certain combination of region and industry, is given by the ratio of the region’s share of industry employment to the region’s share of total employment. As an indicator of diversity, we employ the inverse of the Krugman specialization index (McCann 2001; de Vor and de Groot 2010) (KRUG), which, for a certain region, indicates how much the employment pattern of the region deviates from the employment pattern of the whole economy. For both indicators, regions are NUTS III regions and industries are defined according to the NACE Rev. 2 classification. We include a dummy (Distr) to signal that firm belongs to a district—as defined by ISTAT—because such administrative agglomeration of companies could benefit from specific policies that are not captured by our measures.

Finally, going back to the description of the regressors in Eq. (4.6), we have that X i,t is a vector of “standard” determinants of growth that include the following:

-

The Log(age i,t) that measures the number of years since the firm was established;

-

The size of firm given by the logarithm of number of employees (Log(sizei,t−1));

-

A proxy for financial constraints as measured by the cash flow (Cash flow t−1);

-

Z I,t is a vector of three systems of dummy variables to control for year, sector of activity and geographical area of activity. Disturbance terms are given by ε i, t.

4 Data

The empirical analysis carried out in this chapter draws on a database containing information for about 8300 Italian limited liabilities manufacturing companies active in the time window from year 1996 to year 2004. The unit of observation is the single location firm and, consequently, results can be easily interpreted and directly compared with those deriving from studies conducted at an establishment level. The primary source of data is the Italian section of Bureau Van Dijk’s database, which provides financial and balance sheet information together with geographic localization information and employment figures. In particular, our sample includes only firms active in the whole period 1996–2004 and operating only in one location.

Employment figures are corrected using the National Social Security Institution—INPS—archives, in particular the monthly social security declarations. This procedure allows to control for the reliability of information about the number of employees, a feature that is considered necessary to undertake a sound analysis of firms’ dynamics involving employment dynamics (Haltiwanger et al. 2013; Neumark et al. 2011). The “adjusted” average number of employees of a firm is given by the yearly average number of employees present in the firm.

The key characteristic that distinguishes our dataset from other similar studies on the growth of Italian firms is the use of single location firms. This level of analysis helps to shed light on the determinants of “organic” growth.

5 Empirical Results

The quantile regressions are first run splitting the sample into small firms (SMFs) and medium-large firms (MLFs) and then into low-tech and high-tech firms. Moreover, we run quantile regression referring to positional means of growth rates given by: 0.25 quantile (q25 henceforth), 0.50 quantile (q50 henceforth) and 0.90 quantile (q90 henceforth).

Table 4.1 reports some descriptive statistics of the variables included in the analysis.

First of all, notice that the average size of the firms is 50 employees while the median size is 34, with a strong evidence of a negative skew. Firms are 21 years old on average. The 0.90 quantile of the firm age (38) years shows that the firms in our sample are relatively young.

A particular attention is devoted to the study of the distribution of the growth rates of firms. Indeed, as mentioned before, the standard regression techniques can lead to incorrect inference about the coefficients if their distribution departs from normality. In order to investigate the shape of growth rate distribution, we estimated a series of normality tests: (a) for all the years separately for small and medium-large firms; (b) pooling together all the years separately for small and medium-large firms. The battery of tests leads us to reject the null hypothesis of normality in all the cases (Table 4.2).

The presence of spatial variability may lead to the violation of the assumption on which Model (6) is based: the independence of growth rates, which in turn results in spatial autocorrelation of model residuals. The proper diagnostic tool for verifying whether the residuals of a micro-geographic firm-level model are spatially correlated is the variogram (Schabenberger and Gotway 2005). For the standardized model residuals the empirical variogram ordinates are the quantities \( {v}_{ij}=\frac{1}{2}{\left({r}_i-{r}_j\right)}^2 \), where r i and r j are the standardized residuals corresponding to the firms at the locations x i and x j, respectively (Diggle and Ribeiro Jr 2007). A plot of v ij against the corresponding distance d ij = ‖x i − x j‖ compared with the envelope of empirical variograms computed from random permutations of the residuals, holding their locations fixed, allows the detection of spatial autocorrelation.

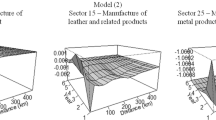

A separate variogram has to be computed on the residuals for each single year t. As a way of illustration, Fig. 4.1 shows a variogram envelope obtained from 999 independent random permutations of the standardized residuals for year t = 2000 for each of the 10th quantile and 90th quantile regression models, with values averaged within distance bands. Since all the empirical variogram ordinates are within the Monte Carlo simulation envelopes, we can conclude that there is no spatial dependence amongst these model’s residuals.Footnote 5

Monte Carlo envelopes for the variogram of the Model (6) standardized residuals (dashed lines) and empirical variogram of residuals (circles) for year t = 2000 and 25th and 90th quantiles

Table 4.3 presents the results of two separate regressions referring to small (less than or equal to 50 employees) and medium-large firms (more than 50 employees), and Table 4.4 presents the results of the separate regressions for high-tech and low-tech firms. The technological sectors are defined according to the definition provided by OECD ISIC REV.3.

For each of these four subsets of firms, the 25th, 50th and 90th quantile regressions have been estimated. In particular, columns 1–3 of Table 4.3 report the results for the small firms, columns 4–6 for the medium-large firms; columns 7–9 of Table 4.4 for the high-tech firms and columns 10–12 for the low-tech firms. We split the sample according to the firm size and level of technology starting from the assumption that they are important mediators in the relationship between the spatial determinants and the growth of firm. The results reported below seem to confirm this intuition.

The first important evidence emerging from the results reported in Table 4.3 is that the way agglomeration externalities (both MAR and JAC) exert their effects on firm growth, strongly depends on the spatial dimension of the industrial site in which firm is located. It can indeed be seen that the regression coefficients associated with the variables Kmar(d) and Kjac(d), (at distance d = 5, 50, 100) can have different signs, different values and different levels of significance depending on the value of the distance d. In particular, from the exam of Table 4.3 it clearly emerges that the small and low-tech firms in 0.90 quantile benefit from positive JAC externalities at a distance of 50 km, while, on the contrary, they are affected by negative JAC externalities at a distance of 100 km. Therefore, a firm may have both a positive and a negative effect from agglomeration externalities at the same time. This implies that when we try to estimate the effect of agglomeration externalities using region-level locational measures (i.e., we refer to a fixed arbitrarily defined spatial scale), what we estimate is indeed more likely to be the combined result of different effects observed at different spatial scales. The opportunity of using firm-level distance-based measures, such as those proposed, is then confirmed. In Sect. 4.3.1, in order to better assess the effects of agglomeration externalities in their whole complexity.

Having in mind this general consideration, we can now look at the results in a greater detail. To start with, let us consider the MAR externalities. According to the level of significance of the parameters associated with the variables Kmar(d), it seems that the annual growth of small firms is not affected by MAR externalities. On the other hand, this type of externality is relevant for the medium-large firms. Indeed, shrinking medium-large firms (q25) are weakly negatively affected by MAR externalities at small distances (d = 5 km) while high growth firms (q90) are positively affected at long distances (d = 90 km). Therefore, medium-large firms tend to suffer from congestion related with the presence of firms of the same industry in the neighborhood and to benefit from large spatial-scale industry specialization.

If we condition the analysis to the technological level of firms, the pattern of MAR externalities is even more complex and produce a rich set of further considerations. MAR externalities are not substantially relevant for low-tech firms, if we exclude only a very weak negative effect observed in the firms characterized by a high level of growth. On the contrary, they tend to have an important role for the high-tech firms. These firms are, indeed, positively affected on the short and long distances (5 and 100 kms, respectively) and negatively affected on the medium distances (50 km), thus suggesting that the effect of MAR externalities is strongly nonlinear in space.

Turning now to the role of JAC externalities, among the small firms, they are relevant only for the q90 firms and exert a positive influence at 50 kms and a negative influence at 100 kms. This very same pattern of nonlinearity in space applies also to the q50 and q90 high-tech firms. Differently, large firms are only positively affected by JAC externalities at 5 km and low-tech firms are not affected in any direction.

In conclusion, the empirical evidence emerging from our estimates does not provide a clear-cut answer to the issue of the relationship between agglomeration externalities and firm growth. They show that this phenomenon is quite complex, because the effect of agglomeration externalities strongly depend on the characteristics of spatial relationships, firms’ size and their technological level. Therefore, we argue that simple and straightforward interpretations of the phenomenon would lead to misleading conclusions.

Having said that, however, we can draw the general indications that MAR externalities produce mostly a negative effect at small and medium distances and a positive effect at large distances, while, on the contrary, JAC externalities have mostly a positive effect at small and medium distances and a negative effect at large distances. This stylized fact suggests the existence of possible complementarities between the two kind of spatial externalities which may have important implications in terms of policies. It indeed suggests that, stimulating the occurrence of positive MAR externalities may, on the other hand, hinder the occurrence of positive JAC externalities and vice versa.

We included in the models the location coefficient calculated at NUTS3 level (LOQ) to refine our firm-level measures of spatial factors. Indeed, this location quotient is introduced in the regression as a further security check for the existence of MAR effects which are not captured by our firm-level measures. Our empirical results show that for small firms the coefficients are significant, but, again, very small and constant over the quantiles. For small firms, the introduction of this term into the regression allow us to rescale all the growth rates over the quantiles in order to correct for residual spatial correlation related to multiplant firms. Medium-large firms, instead, do not present significant coefficients.

With a similar argument we used a proxy of the diversity of environment at provincial level the concentration inverse of the Krugman specialization index. In this case, the effect is significant for small firm at q25 and q50. Medium-large firms benefit from specialization at q50 and q90.

A long literature is devoted to the positive effects on firm performances of industrial district as defined by ISTAT (Beccattini 1989). A firm active in an industrial district can benefit, for instance, find new workforce easily, workforce is specialized, suppliers are easier to reach because they have experience with other firms in the industrial districts, there exist public policies that regard specifically the industrial districts firms. These effects should be distinguished by spatial proximity of firms and agglomeration phenomena; hence, to capture these effects, we introduced a dummy variable identifying firms belonging to an industrial district. Results reveal that being located in a district produces a positive effect on growth of small firms at q25 and q50. Medium-large firms are not affected by being in a district. In other words, larger firms do not benefit from the administrative aspects behind the definition of a district (e.g., the existence of subsidies for firms in a district), but may benefit by the pure market advantages coming from agglomeration.

As for the standard determinants of growth, we observe that the variable Age produces a negative effect on growth for all firms (see Table 4.3): as firms get older, they appear less prone to grabbing opportunities of growth. Another feature that quantile regression allows to capture is fact that the bigger the growth performance of firms, the stronger is the negative linkage. Indeed, coefficients range from −0.009 for small firms in q10 to −0.05 at q90. Similarly, for medium-large firms these coefficients range from −0.02 for q10 to −0.11 for q90. The effect is nonlinear as witnessed by the significance of the coefficient of age squared.

The variable size has a significant effect even if the heterogeneity of signs and magnitudes reveal that the size has a negative effect on growth both for small and medium-large firms. Interestingly, the largest coefficient is found for small firms at the 90th quantile (q90). In this case, the value is equal to −0.25 and significant, thus suggesting that small firms experience an increasing difficulty in growing as their size is bigger.

Liquidity constraints coefficient representing a key factor that can impede growth are introduced through the variable cash flow (an inverse proxy of liquidity constraint). The corresponding coefficients are positive and significant for all the groups of firms. Such factor is more important for medium-large firms compared to small firms across all quantiles.

6 Summary and Conclusions

In this chapter, we carried out an empirical analysis to study how localization economies shape the patterns of firm growth. Our investigation departs markedly from most of the recent literature on the subject, in that we adopt an alternative way of quantifying the effects of spatial externalities based on micro-data. In this respect, we suggested to use the Getis local K-function (Getis 1984; Getis and Franklin 1987) to define firm-level indicators that endogenize the emergence of geographical economies. In this way, we are able to tackle two methodological problems typically arising in empirical work when considering regional aggregated data: (a) the dependence of the results on the particular adopted geographical partition (into, e.g., counties or regions) and (b) the restrictive assumption of spatial homogeneity of the phenomenon within regions which does not allow to take into consideration the intra-regional variability.

Founding on the proposed methodology, we were able to assess empirically the prevalence of Marshall-Arrow-Romer externalities (MAR) on Jacobs externalities (JAC). As it is known, the former refers to knowledge spillovers between firms of the same industry, labor market pooling, transport saving cost and economies of scale arising from shared inputs. The latter are pure agglomeration economies arising from knowledge spillover external to the industry within which firm operates, diversity leading to economic growth and urbanization externalities.

Our exploration involves a large sample of small and medium Italian firms operating in the manufacturing sector over a period of eight years. The modeling is based on a quantile regression framework that better discriminates between the distinctive features of the growth rate distribution.

In summary, we obtained the following stylized facts:

-

The action of the various externalities is a rather complex phenomenon, but there are important empirical evidences that small and medium-sized firms are affected in a different way by MAR and JAC externalities.

-

Small firms, which in the recent past experienced slightly negative growth performance, are positively influenced by JAC diversity. This effect is more evident if the firms operate in low-technology sectors and the externalities are observed at short distances in space.

-

Firms in low-technology sectors that performed well in terms of growth are more likely to exploit both MAR and JAC positive externalities.

-

The effect associated with the two typologies of agglomeration economies varies with the distance threshold used to compute the location indicators. For example, the growth opportunities for medium-large firms operating in low technology sectors are generally negatively affected by MAR externalities, but, conversely, are positively influenced by JAC externalities if observed at 50 kms.

These results may be of interest for policy makers and business practitioners in that they suggest some interesting implications that it is worth to briefly mention here.

First of all, the empirical evidence of different (and sometimes opposite) effects of geographical spillovers on firms depending on their size, on their different technological environment and on their recent growth history, suggest that a “one-size fits-all” approach to industrial policy is doomed to fail or even to produce results that move in the opposite direction with respect to the desired aims.

Secondly, managers and policy makers should be aware of the fact that the structural and strategic choices they implement can significantly mediate the sheer effects associated with geographical location. Indeed, some of these choices can mitigate the negative effects stemming from a higher competition in a given area. Other choices, conversely, allow the firm to absorb most of the knowledge spillovers spreading in the surrounding environment and in this way to exploit them as a growth factor.

Notes

- 1.

- 2.

The literature identifies a third type of externality. It refers to Porter’s (1990) argument, and it is associated with Jacobs idea that competition is better for growth. Strong competition in the same geographical market provides incentives to innovate which, in turn, accelerate the technical progress, the productivity, and, finally, the growth.

- 3.

\( \hat{\lambda}=n/\left|A\right| \), where A is the study area and |A| denotes its surface.

- 4.

Firms located near the boundary of the study area may be close to unobserved firms located outside the study area. Neglecting this circumstance may lead to a biased estimate.

- 5.

The same graphical test of spatial correlation has been performed on the model residuals for all the other years and quantiles as well, leading to the same conclusion of absence of spatial correlation. The results are available upon request to the authors.

References

Acs, Z., & Armington, C. (2004). Employment growth and entrepreneurial activity in cities. Regional studies, 38(8), 911–927.

Andersson, M., & Lööf, H. (2011). Agglomeration and Productivity: Evidence from Firm-Level Data. The Annals of Regional Science, 46, 601–620.

Antonietti, R., Cainelli, G., & Lupi, C. (2013). Vertical Disintegration and Spatial Co-localization: The Case of Kibs in the Metropolitan Region of Milan. Economics Letters, 118, 360–363.

Arbia, G. (1989). Spatial Data Configuration in Statistical Analysis of Regional Economic and Related Problems. Dordrecht: Kluwer Academic Publisher.

Arbia, G. (2001). Modelling the Geography of Economic Activities on a Continuous Space. Papers in Regional Science, 80, 411–424.

Arbia, G., Espa, G., Giuliani, D., & Mazzitelli, A. (2010). Detecting the Existence of Space–Time Clustering of Firms. Regional Science and Urban Economics, 40, 311–323.

Arbia, G., Espa, G., & Giuliani, D. (2012). Clusters of Firms in an Inhomogeneous Space: The High-Tech Industries in Milan. Economic Modelling, 29(1), 3–11.

Audretsch, D. B., & Dohse, D. (2007). Location: A Neglected Determinant of Firm Growth. Review of World Economics, 143(1), 79–107.

Autant-Bernard, C. (2001). The geography of knowledge spillovers and technological proximity. Economics of Innovation and New Technology, 10(4), 237–254.

Barbosa, N., & Eiriz, V. (2011). Regional Variation of Firm Size and Growth: The Portuguese Case. Growth Change, 42(2), 125–158.

Beaudry, C., & Schiffauerova, A. (2009). Who’s Right, Marshall or Jacobs? The Localization Versus Urbanization Debate. Research Policy, 38(2), 318–337.

Beaudry, C., & Swann, P. (2009). Firm Growth in Industrial Clusters of the United Kingdom. Small Business Economics, 32(4), 409–424.

Beccattini, G. (1989). Sectors and/or Districts. In E. Goodman & J. Barnforth (Eds.), Small Firms and Industrial Districts in Italy (pp. 120–133). London: Routledge.

Becchetti, L., & Trovato, G. (2002). The determinants of growth for small and medium sized firms. The role of the availability of external finance. Small business economics, 19(4), 291–306.

Birch, D. L., & Medoff, J. (1994). Gazelles. In L. C. Solmon & A. R. Levenson (Eds.), Labor markets, employment policy and job creation. Boulder: Westview Press.

Bottazzi, G., Cefis, E., Dosi, G., & Secchi, A. (2007). Invariances and Diversities in the Patterns of Industrial Evolution: Some Evidence from Italian Manufacturing Industries. Small Business Economics, 29(1–2), 137–159.

Boots, B. N., & Getis, A. (1988). Point pattern analysis (Vol. 8). SAGE Publications, Incorporated.

Brown, W. M., & Rigby, D. L. (2010). Marshallian Localization Economies: Where Do They Come From and to Whom Do They Flow? Paper presented at the DIME Workshop ‘Industrial Dynamics and Economic Geography’, Utrecht, September.

Coad, A. (2007). A Closer Look at Serial Growth Rate Correlation. Review of Industrial Organization, 31(1), 69–82.

Coad, A., & Rao, R. (2008). Innovation and firm growth in high-tech sectors: A quantile regression approach. Research policy, 37(4), 633–648.

Contini, B., & Revelli, R. (1988). Job Creation and Labour Mobility: The Vacancy Chain Model and Some Empirical Findings. R&P Working Paper N.8.

Del Monte, A., & Papagni, E. (2003). R&D and the Growth of Firms: Empirical Analysis of a Panel of Italian Firms. Research Policy, 32, 1003–1014.

Diggle, P. J., & Ribeiro, P. J., Jr. (2007). Model-Based Geostatistics. New York: Springer.

Duranton, G., & Overman, H. G. (2005). Testing for Localisation Using Micro-geographic Data. The Review of Economic Studies, 72, 1077–1106.

Duschl, M., Schimke, A., Brenner, T., & Luxen, D. (2011). Firm Growth and the Spatial Impact of Geolocated External Factors: Empirical Evidence for German Manufacturing Firms. Working Paper series in Economics n.36. Retrieved from hdl.handle.net/10419/51558.

Ellison, G., & Glaeser, E. L. (1997). Geographic Concentration in U.S. Manufacturing Industries: A Dartboard Approach. Journal of Political Economy, 105, 889–927.

Espa, G., Arbia, G., & Giuliani, D. (2013). Conditional Versus Unconditional Industrial Agglomeration: Disentangling Spatial Dependence and Spatial Heterogeneity in the Analysis of ICT Firms’ Distribution in Milan. Journal of Geographical Systems, 15(1), 31–50.

Feldman, M. P., & Audretsch, D. B. (1999). Innovation in Cities: Science-Based Diversity, Specialization and Localized Competition. European Economic Review, 43(2), 409–429.

Florence, P. S. (1939). Report on the Location of Industry. London: Political and Economic Planning.

Frenken, K., Cefis, E., & Stam, E. (2014). Industrial Dynamics and Clusters: A Survey. Regional Studies, 8, 1–18.

Frenken, K., Van Oort, F., & Verburg, T. (2007). Related variety, unrelated variety and regional economic growth. Regional studies, 41(5), 685–697.

Fujita, M., Krugman, P., & Venables, A. (1999). The Spatial Economy–Cities, Regions and International Trade. Cambridge, MA: MIT Press.

Getis, A. (1984). Interaction Modelling Using Second-Order Analysis. Environment and Planning A, 16, 173–183.

Getis, A., & Franklin, J. (1987). Second-Order Neighborhood Analysis of Mapped Point Patterns. Ecology, 68, 473–477.

Gibrat, R. (1931). Les Ingalits Economiques. Parigi: Sirey.

Gini, C. (1912). Variabilità e mutabilità. Reprinted in Memorie di metodologica statistica. E. Pizetti, & T. Salvemini (Eds.), Rome.

Gini, C. (1921). Measurement of Inequality of Incomes. The Econometrics Journal, 31(121), 124–126.

Glaeser, E., Kallal, H., Scheinkman, J., & Schleifer, A. (1992). Growth of Cities. The Journal of Political Economics, 100, 1126–1152.

Griliches, Z. (1992). R&D and productivity: the econometric evidence. material from Scandinavian Journal of Economics, 94, 251–268.

Hall, B. H. (1987). The Relationship Between Firm Size and Firm Growth in the US Manufacturing Sector. The Journal of Industrial Economics, 35(4), 583–606.

Haltiwanger, J., Jarmin, R. S., & Miranda, J. (2013). Who Creates Jobs? Small Versus Large Versus Young. The Review of Economics and Statistics, 95(2), 347–361.

Henderson, V. (2003). The urbanization process and economic growth: The so-what question. Journal of Economic growth, 8(1), 47–71.

Henderson, V., Kuncoro, A., & Turner, M. (1995). Industrial Development in Cities. Journal of Political Economy, 103(5), 1067–1090.

Hirschman, A. O. (1945). National Power and the Structure of Foreign Trade. Berkeley: University of California Press.

Jacobs, J. (1969). The Economy of Cities. New York: Random House.

Koenker, R., & Hallock, K. F. (2001). Quantile regression. Journal of economic perspectives, 15(4), 143–156.

Krugman, P. (1991). Geography and Trade. Cambridge: MIT Press.

Lotti, F., Santarelli, E., & Vivarelli, M. (2003). Does Gibrat’s Law Hold Among Young, Small Firms? Journal of Evolutionary Economics, 13(3), 213–235.

Maine, E. M., Shapiro, D. M., & Vining, A. R. (2010). The Role of Clustering in the Growth of New Technology-Based Firms. Small Business Economics, 34, 127–146.

Marcon, E., & Puech, F. (2010). Measures of the Geographic Concentration of Industries: Improving Distance-Based Methods. Journal of Economic Geography, 10(5), 745–762.

Marshall, A. (1890). Principles of Economics. London: Macmillan.

McCann, P. (2001). Urban and regional economics. OUP Catalogue.

Neumark, D., Wall, B., & Zhang, J. (2011). Do small businesses create more jobs? New evidence for the United States from the National Establishment Time Series. The Review of Economics and Statistics, 93(1), 16–29.

Penttinen, A. (2006). Statistics for Marked Point Patterns. The Yearbook of the Finnish Statistical Society, 2006, 70–91.

Porter, M. E. (1990). The Competitive Advantage of Nations. London: Macmillan.

Raspe, O., & Van Oort, F. (2008). Firm Growth and Localized Knowledge Externalities. Journal of Regional Analysis and Policy, 38(2), 100–116.

Raspe, O., & Van Oort, F. (2011). Growth of New Firms and Spatially Bounded Knowledge Externalities. The Annals of Regional Science, 46, 495–518.

Rosenthal, S. S., & Strange, W. C. (2005). The geography of entrepreneurship in the New York metropolitan area. Federal Reserve Bank of New York Economic Policy Review, 11(2), 29–54.

Schabenberger, O., & Gotway, C. A. (2005). Statistical Methods for Spatial Data Analysis. Boca Raton: Chapman & Hall/CRC.

Staber, U. (2001). Spatial Proximity and Firm Survival in a Declining Industrial District: The Case of Knitwear Firms in Baden-Wurttemberg. Regional Studies, 35, 329–341.

de Vor, F., & de Groot, H. (2010). Agglomeration Externalities and Localized Employment Growth: The Performance of Industrial Sites in Amsterdam. The Annals of Regional Science, 44, 409–431.

Wennberg, K., & Lindqvist, G. (2010). The Effects of Clusters on the Survival and Performance of New Firms. Small Business Economics, 34(3), 221–241.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Author(s)

About this chapter

Cite this chapter

Arbia, G., Dickson, M.M., Gabriele, R., Giuliani, D., Santi, F. (2021). On the Spatial Determinants of Firm Growth: A Microlevel Analysis of the Italian SMEs. In: Colombo, S. (eds) Spatial Economics Volume II. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-030-40094-1_4

Download citation

DOI: https://doi.org/10.1007/978-3-030-40094-1_4

Published:

Publisher Name: Palgrave Macmillan, Cham

Print ISBN: 978-3-030-40093-4

Online ISBN: 978-3-030-40094-1

eBook Packages: Economics and FinanceEconomics and Finance (R0)