Abstract

The IPCC Special Report on Global Warming of 1.5ºC made clear that urgent action is needed to avoid the threat of climate change and enable sustainable development in line with the United Nation’s Sustainable Development Goals (SDGs) and the Paris climate Agreement. Investment is critical to achieve our global climate and sustainable development goals, and to fill the current investment gap the global community needs to get private investors on board. To this end, investors will want to know how contributing to the SDGs will help them fulfilling liabilities, and meeting clients’ risk-adjusted returns expectations. They also need to know how they could invest in SDGs-relevant activities, particularly in sectors that constitute an untapped potential in high risk markets. This chapter provides investors and financiers with evidence on the business case for SDG-informed capital allocation decision-making, and on the instruments that can help them deploying capital in activities supporting the SDGs.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

The launch of the United Nations’ Sustainable Development Goals (SDGs) in 2015, and the agreement reached in Paris the same year to combat climate change—so-called Paris Agreement—, have provided a strong signal about the political will to transition towards a resource-efficient, low-carbon and resilient growth model. They have made clear that action by the public sector is critical, but not enough to address priority societal challenges like food security, climate change, poverty eradication, inequality and prosperity. The international community counts heavily on the private sector to address such challenges, and the agreement sealed in December 2018 by 196 states at the Katowice Climate Change Summit (COP24)—the “Paris rulebook”—further signal the call for action and the direction of travel.

The private sector has started to react to this call for action. Over 2013–2016, for example, private resources accounted for around 87% of total investments in renewable energy (IRENA and CPI 2018; Buchner et al. 2017). However, while the overall positive trend is good news, we are falling far short of what is needed to achieve global climate and sustainable development goals and, to limit global average warming to 1.5 °C above pre-industrial level—one of the Paris Agreement’s overarching goal. To these ends, as noted by the IPCC’s 2018 Special Report, rapid, far-reaching and unprecedented changes are required in energy, land, urban, infrastructure and industrial systems (IPCC 2018).

To allocate capital towards high-impact projects that address some of the most urgent problems the world is facing, corporations, investors and financiers would need to realize that the SDGs make business sense. Existing estimates are already highlighting the investment case: a study from the Business and Sustainable Development Commission (BSDC), for instance, states that achieving the SDGs could open up US$ 12 trillion (more than 10% of global GDP) worth of market opportunities in food and agriculture, cities, energy and materials, and health and well-being alone, and 380 million new jobs by 2030 (BSDC 2017).

In food and agriculture, in particular, BSDC (2017) estimates that a system in line with the SDGs has the potential to create new economic value of more than US$ 2 trillion by 2030; it would also be much more capable to withstand climate shocks and deliver nutritious, affordable food for a growing world population. The untapped investment potential is significant considering, as a proxy, how much resources are currently flowing towards “climate-smart” agriculture forestry, land-use, and natural resource management measures—about US$ 7 billion according to the latest Buchner et al. (2017) estimates.

In the energy sector, the clean energy investment potential amounts to US$ 360 billion by 2030 according to Tonkonogy et al. (2018) estimates based just on the top eight emerging markets alone. However, even as clean energy technology advances rapidly, and technology costs continue to fall quickly, traditional financing approaches are lagging. What has worked in the past for coal or gas does not necessarily work for renewable energy or other sectors.

The real stumbling block is translating such opportunities and potential into concrete actions. This calls for a structural and systemic change in capital allocation decision-making processes, risk management frameworks, and the use of appropriate disclosure rules and impact assessment metrics. Investors and financiers would need to deeply understand the relevance of the SDGs for their investment and financing strategies, policy and asset allocation; they would need to know how contributing to the SDGs will help them fulfill liabilities and clients’ expectations about risk-adjusted returns (PRI 2017). Further, as noted for instance by the signatories of the Dutch SDG Investing AgendaFootnote 1, they would also need to know through which vehicles and financing models they could invest in SDGs-relevant activities, particularly so in sectors that constitute an untapped potential in high risk markets.

Such a structural and systemic change of the financial systems would need to happen fast to meet the Paris ambition of restricting global warming to well below two degrees Celsius above pre-industrial times and meeting the SDGs. Albeit emissions of greenhouse gases (GHGs) are rising, not falling (International Energy Agency (IEA) 2018a), these goals are not yet out of reach, but could be unless the shifting of financial flows away from high-carbon and climate vulnerable industries and assets towards ‘greener’ and resilient ones steps up a gear (IPCC 2018).

Against this background, this chapter aims to provide investors and financiers with insights on the business case for SDG-informed capital allocation strategies (Sect. 1), and on the instruments that can help deploying capital in activities supporting the SDGs (Sect. 2). It focuses on, in particular, SDG 2 and 13 because of the relevance and cross-cutting nature that agriculture and climate change—the core of these two goals—have for the sustainability of food systems and the achievement of the other SDG goals. Agriculture, the dominant occupation for the world’s poorest people, in fact, accounts for 70% of water use (World Development Indicators 2018) and it is both a victim and a cause of climate change. Unlocking global investments towards sustainable agriculture can hence help make great strides on many SDG goals. The final section concludes and provides suggestions on how to scale up investments.

2 The Business Case for SDG Finance

Financial impacts, regulatory-related pressures, market dynamics and investment opportunities are key reasons why investors and financiers should invest in climate action (SDG 13). These aspects are evidenced by several facts described in the following paragraphs.

2.1 Financial Impacts Stemming from Unmanaged Climate Risks Are Already Evident

If unmanaged, the risks arising from climate change can have direct and/or indirect operational, strategic, financial and social implications that can spread across the investment value chain (BOE 2018; TCFD 2017; GARI 2017), as highlighted by Fig. 1.

Physical climate risks and related implications along the investment value chain. Source: authors’ elaboration

Such risks can emerge from physical climate risks and/or transition risks. The former, physical climate risks, refer to the risks arising from the acute or chronic physical effects of climate change. The latter, transition risk, refer to the risks resulting from the policy, legal, technology and market changes occurring in the shift to a low carbon economy (TCFD 2017). Transition risk—also often described as “stranded asset risk”—may involve the repricing or write-downs of carbon-intensive assets that could quickly become unusable or reduced to lower/zero value.

Registered weather-related loss events, the impact of weather-related events on the earnings disclosed by S&P’s 500 companies, and climate-led rating actions provide good insights on the financial materiality of environmental, climate and social factors.

-

Inflation-adjusted insurance losses have increased from an annual average of around US$10 billion in the 1980s, to around US$ 55 billion over the past decade according to Munich Re NatCatSERVICE statistics (2017). As noted by BoE (2018), if such losses are insured, they can directly affect insurance firms through higher claim. If uninsured, the burden can fall on companies impairing asset values, and reducing the value of investments held by financial institutions. The associated potential financial risk exposure is evident when considering that public and private re/insurance entities only covered about 36% (US$ 80 billion) of the economic damages caused by the exceptional Hurricane Season in the Atlantic in 2017 (Benfield 2018).

-

In 2017, 73 companies (15%) on the S&P 500 publicly disclosed an effect on earnings from weather events according to S&P (2018). The average materiality of events for the companies that quantified it was a significant 6%.

-

S&P (2017) identified 717 cases where climate-related and environmental concerns were relevant to credit rating, and 106 cases where climate-related and environmental concerns factor resulted in a change of rating, outlook, or a CreditWatch action.

If unmanaged, change-related risk could result in US$ 4.2 trillion expected losses and, if global temperatures continue to rise, could reach as much as US$ 43 trillion—30% of the entire stock of manageable assets (EIU 2015).

2.2 Financial Regulators Acknowledge That Climate Change Presents a Systemic Risk to the Financial System

The changing international context defined by the Paris Agreement and the SDGs has strengthened calls for thoughtful consideration on how regulation and policy could be aligned with, and promote, investment practices and sustainable financing to the goals and targets of these landmarks commitments (BCSD 2017a, b). This call for action emerged also in light of the financial regulators’ recognition that climate change and policies to mitigate it could affect the ability of central banks and regulators to meet monetary and financial stability objectives (Carney 2015; BoE 2017). A too rapid transition towards a low-carbon economy could indeed lead to a “climate Minsky moment” (Carney 2018).

Noteworthy regulatory-related development are Article 173 of the French Energy Transition and the recommendations released in 2017 by the Task Force on Climate-Related Financial Disclosure (TCFD)—an initiative established by the Financial Stability Board under the request of the G20. Both assigned enhanced climate-related reporting responsibilities to financial market participants. The former, Article 173, sets out mandatory disclosure requirements to French institutional investors who are now asked to explain whether and how their policies and targets align with national strategies for energy transition. The latter, the TCFD, recommends voluntary consistent disclosure of climate-related risks to companies in the financial and non-financial sectors. By recommending scenario analysis referring at least to the two degrees Celsius scenario envisaged by the Paris Agreement, it prompts to a future-oriented approach for the identification, evaluation and management of climate risks GIIN (2018).

The release of the Task Force’s recommendations prompted several Central Banks and Supervisory authorities across the world to investigate the environmental and climate-related risks for the financial sectors under their responsibilities (NGFS 2018). The Dutch Central Bank, for instance, following an evaluation of the climate risks relevant to the Dutch financial sector, announced the introduction of climate-related risks in its supervisory assessment frameworks (DNB 2017a, b). The Bank of England, following similar work, is looking into enhancing the Prudential Regulation Authority’s approach to supervising the financial risks from climate change, and enhancing the resilience of the UK financial system by supporting an orderly market transition to a low-carbon economy (BoE 2018; GIIN 2018).

2.3 Stakeholders and Shareholder’s Pressures Provide Clear Signals of the Changing Market Dynamics

Many businesses, investors, industry groups and other stakeholders are increasingly vocal about the need to urgently transition to a low-carbon economy to deliver sustainable economic growth.

Key examples of stakeholders and shareholder’s pressures are:

-

Larry Fink, Chief Executive Officer (CEO) of US$ 6.3 trillion asset manager BlackRock Rock, recently called business leaders of the world’s largest public corporations that they need to contribute to society if they want to receive the company’s support (BlackRock 2018a). BlackRock also ramped up its investor-stewardship initiative and proxy voting by making climate risk a primary issue on which to engage portfolio companies (BlackRock 2018b). Other leading asset managers have followed suit.

-

The Climate Action 100+ investors-led initiative—backed by 296 investors with US $31 trillion in assets under management—targets 161 companies considered systemically important greenhouse gas emitters. Its goal is prompting them to act to reduce emissions across the value chain consistent with the Paris Agreement’s below 2° goal (CERES 2018).

-

500+ corporations have committed to set science-based targets on their emissions profile in line with two degree Celsius scenarios, to assist investors in assessing their low-carbon commitments.Footnote 2

-

The wave of billion-dollar legal challenges demanding accountability for climate change to the oil and gas industry. The number of cases across the globe reached more than 1000 suits according to the litigation database of the Sabin Center for Climate Change, and include e.g. the fraud investigations launched by two American state against Exxon, and the law suit launched by nine cities and counties, from New York to San Francisco, to major fossil fuel companies—BP, Exxon Mobil, Chevron, ConocoPhillips and Shell—seeking compensation for climate change damages.

2.4 The SDGs and Climate Change Are Opportunities to Gain Competitive Advantages

The SDGs and the Paris Agreement are opening opportunities for investment and financial innovation. The Business and Sustainable Development Commission (Business Commission for Sustainable Development 2017a, b, c) estimates that SDGs could open up US$ 12 trillion market opportunities for the private sector. Achieving the Paris Agreement holds the potential of generating over US$ 23 trillion in climate investment opportunities according to estimates of the International Finance Corporation (IFC 2016).Footnote 3 FTSE Russell (2018)Footnote 4 estimates that the green economy represents today 6% of the market capitalization of global listed companies, approximately US$ 4 trillion which is about the same size as the fossil fuel sector.

These opportunities translate into the opening up of new markets, and new ways of doing business and serving the existing customer-base to gain competitive advantages (Trabacchi et al. 2018). These manifest as opportunities to finance/invest in e.g.:

-

Products and services helping to identify, assess and manage climate-related risks, or other SDGs-related challenges e.g., technologies to improve efficiency in the use of natural resources such as water

-

Projects or practices that reduce climate-related risk e.g. renewable energy infrastructures

-

Companies offering such products and services

-

Green, social or sustainable securities such as green, social or sustainable bonds issued to raise capital for use in projects or activities with the specific environmental and/or social purposes

-

Investment vehicles targeting sustainable companies or assets.

Banks and investors are already sizing these opportunities. The Bank of England (BoE 2018), for instance, noted that banks are considering the opportunities related to green finance through two main channels: their primary balance sheet activities (i.e. “green” lending activities), and capital markets through e.g. securitization of green projects and assets. Investors are also seeking to enhance their business proposition to contribute to the SDGs. Some have already set ambitious financial targets to communicate their commitment or developed methodologies to identify investment opportunities linked to the SDGs (APG and PGGM 2017, see Fig. 2).

An investor’s view on Sustainable Development Investments. Source: APG and PGGM (2017)

3 Investment Approaches to Drive Capital Towards the SDGs

Despite the relevant pressures and opportunities to seize, capital is not yet flowing at the speed and pace required to ensure a sustainable future. A substantial shift from brown to green is needed. This is particularly evidence by:

-

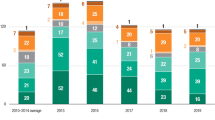

The volume of fossil fuel investments, which still dwarf climate-related investments. When total upstream and downstream investments are included, fossil fuel investment amounted to US$ 825 billion in 2016, more than double climate investments estimated in US$ 383 billion by Buchner et al. (2017).

-

About 60% of world’s total primary energy supply still comes from oil and gas sources (IEA 2018b—2016 data), highlighting that a major shift in the structure of energy systems, and in related capital allocations, still has to happen. As an example, banks’ exposure to the coal and mining industry is still significant. The top 35 global coal-exposed banks are providing around US$75 billion to the coal power industry and £58 billion to the coal mining industry during 2014–2016 (Rainforest Action Network 2017).

Key barriers hindering or slowing down the transition are:

-

Lack of clear and consistent definitions of “sustainable” and “green assets” that in turn leads to a lack of investment opportunities and identifiable green’ assets (HSBC 2018; Green Finance Task Force 2018)

-

Lack of data on the green investment opportunity (FTSE Russell 2018)

-

Inadequate data for measuring both the SDGs and sustainability at large

-

Knowledge, regulatory, risk coverage and viability gaps including e.g. counterproductive subsidies (Trabacchi et al. 2015) or lack of clear guidance on international and national low-carbon trajectories

-

Fund managers and investors’ short-termism, and perception that sustainable investments may come at the expenses of good returns—even though empirical evidence shows the contrary (Nelson 2018)

-

Inadequate integration of sustainability in the duties of institutional investors and their asset managers (HLEG 2018)

-

No alignment of financial incentives and the business models of intermediaries with sustainable development (HLEG 2017)

-

Ultimately, notwithstanding noteworthy process on carbon pricing initiatives, the lack of an adequate and coherent carbon price that would appropriately capture the so-called external costs of activities that produce carbon emissions.

Several efforts are ongoing to tackle these barriers, and innovative tools, approaches and vehicles are emerging to help close the SDG funding gap and tap into the related market opportunity. There is no silver bullet to financing the sustainable development transition. We need to think out of the box and when we find good solutions, we need to scale and replicate them rapidly. New and transformative instruments are needed to strategically use concessional capital to de-risk projects and drive private sector investment.

One example of how to come up with solutions are public-private initiatives such as the Global Innovation Lab for Climate Finance and its national Labs in India and Brazil (the Lab).Footnote 5 The Lab is a public-private initiative engaging leading experts in sustainable investment—from governments, development finance institutions, investment banks, institutional investors and other private institutions. Its goal is to unlock private investment in sustainable development at scale. It identifies, develops, and supports the launch of new solutions that can tackle barriers and attract investment. Since the Lab’s start in 2014, it has developed and launched 35 innovative financial instruments and business models that have mobilized over 1.4 billion dollars for concrete projects in emerging markets. Many of these instruments combine blended finance approaches, with public investors, impact investors, and institutional investors working together to overcome financing or non-financing barriers.

The Lab’s experience highlights two noteworthy investment approaches, blended finance and impact investing.

3.1 Blended Finance Can Attract Private Capital in High Risk Markets

Blended finance—the strategic use of public and/or philanthropic funding to catalyze private sector capital in SDG-related investments (IFC et al. 2017)—holds much promise, particularly to attract private capital in in high risk markets/market segments. Blended finance, in fact, allows to improve the risk-return profile of investments, or improve a project’s probability of reaching financial close and of delivering climate change-related benefits.

The Climate-Smart Lending Platform and the Climate Resilience and Adaptation Finance & Technology Transfer Facility are two examples of innovative blended finance instruments. Their endorsement by the Lab signals their innovative and promising potential.

The Climate-Smart Lending Platform is a mechanism that brings together the tools, actors and finance necessary to help lenders (traditional and non-traditional) to manage climate risk in their loan portfolios, while incentivizing the adoption of climate-smart farming methods by smallholders (see Fig. 3). The Platform aims to scale up climate-smart lending to smallholders, whilst reducing climate-related default risk.

The structure of the Climate-Smart Lending Platform. Source: The Lab (2016)

The Climate Resilience and Adaptation Finance & Technology Transfer Facility is the only commercial investment vehicle to focus exclusively on companies providing technologies and solutions for helping businesses, financiers, and communities to manage climate risks (see Fig. 4). An example could be a company providing precision agriculture data analytics, or drought resistant seeds and crops.

The structure of the climate resilience and adaptation finance & technology transfer facility. Source: The Lab (2017)

3.2 Impact Investing Can Accelerate More Inclusive and Sustainable Financial Markets

Impact investing refers to an investment made into companies, organizations, and funds with the intention to generate social and environmental impact alongside a financial returnFootnote 6. A handful of impact investors have begun to raise capital, create new products and proactively target and incorporate the SDG at various stages of the investment cycle, thus making them the central focus of their investment decision-making.

An example is Blue like an Orange Sustainable Capital and its Sustainable Capital Latin America Fund I (Fund) aimed at catalyzing private debt capital into SDG-relevant companies in Latin America and the Caribbean. The Fund has integrated the SDGs into due diligence, impact target-setting for each investment, and impact monitoring throughout the duration of each loan.

Through the co-financing framework agreement Blue like an Orange established with IDB Invest—a multilateral development bank—the company benefits from IDB Invest’s proprietary evaluation system called DELTA. By using DELTA, IDB Invest can rate the potential impact of a jointly-financed transaction at the outset, set targets, monitor environmental, social, and governance (ESG) compliance, and align its impact with the SDGs. Therefore, by co-financing transactions with IDB Invest, Blue like an Orange can benefit from this tool, enhancing the ability to offer investors state-of-the-art impact reporting.

4 Conclusions

The threat of climate change has never been more daunting. Mobilizing private capital is a critical element of achieving the world’s climate and sustainable development goals. This chapter sheds light on the business case associated with the SDGs and the Paris Agreement for investors and financiers; it also offers insights on concrete instruments and approaches that can help deploying capital in activities supporting the achievement of these goals.

Financial impacts, regulatory-related pressures, market dynamics together with investment opportunities and innovative investment approaches demonstrate a sound business case for SDG investment. Blended finance instruments and impact investment examples embody innovative approaches developed with the purpose of unlocking global investments for SDGs and tackling climate change.

Yet, there is a need to go from pilots to scale. Despite the positive signs, the sustainable finance market is still incipient and a major shift in public and private capital allocations needs to occur if we are to change the structure of economic systems and minimize the impacts of climate-related risks. For this to happen, the success of current approaches can be increased by targeting the high-impact opportunities; adjusting the mix of financing instruments to address the most prevalent risks; and achieving scale through replicating successes, building internal capacity across the finance industry, supporting financial intermediaries and streamlining approval processes.

This, in turn, requires a new collaboration amongst multiple actors, including:

-

Regulators, government related and industry bodies as well as Stock Exchanges, who can play a role in enhancing the availability of clear and consistent definitions of “sustainable” and “green assets”. They can also play a key role in enhancing the availability of SDG and climate-relevant data and promote investors to embrace longer-term horizon to overcome short-termism. The efforts of the High-Level Expert Group on Sustainable Finance established by the European Commission and of the Task Force on Climate-related Disclosures go in this direction and need to scale up further—particularly beyond EU borders.

-

Development banks, philanthropic organizations and practitioners, who can play a role in attracting private capital in high risk markets by helping to expand the reach and breadth of blended finance instruments.

-

Investors and financiers, who can play a role in enhancing data availability and promoting sustainability through the investment chain. They can do so by, for instance, adopting the recommendations of the Task Force on Climate-related Disclosures, scaling up engagement with the companies in their portfolios, and systematically integrating the SDGs and climate-related risks in their in decision-making processes, risk management frameworks and investment/credit policies.

Ultimately, we need to re-frame the climate finance challenge as one of mobilizing financial institution and industry realignment with the Paris Agreement’s Article 2.1.c. Mobilizing the finance sector to fully commit to a holistic approach to climate change, which ensures consistency of all financial flows with the climate and sustainable development goals will allow to truly mainstream SDG considerations into finance.

“Exponential progress is necessary, and it is achievable. The moment has come to move from knowing that it is achievable, to actually achieving it. And that is what we’re gathered here to do. This is an invitation to join the journey of exponential transformation” (cit. Figueres C. 2018)

Notes

- 1.

Launched in 2016, the Dutch SDG Investing Agenda is available at https://www.sdgi-nl.org/.

- 2.

See Science Based Targets website: http://sciencebasedtargets.org/2017/09/18/more-than-300-to-set-science-based-targets/

- 3.

Estimates based on selected sectors in 21 large emerging markets - see IFC (2016) for details on the methodology.

- 4.

See FTSE Russell (2018) for details on the methodology.

- 5.

For more information and the Lab’s impact see https://www.climatefinancelab.org/ and https://www.climatefinancelab.org/wp-content/uploads/2018/04/Lab-Impact-Report-2018.pdf

- 6.

Source: GIIN web site accessible here https://thegiin.org/impact-investing/need-to-know/#what-is-impactinvesting

References

APG and PGGM (2017), Sustainable Development Investments (SDGs), Taxonomies, May 2017, https://www.apg.nl/en/publication/SDI%20Taxonomies/918

Benfield, A. (2018). Weather, climate & catastrophe insight: 2017 annual report. Retrieved from http://www.aon.com/reinsurance/analytics-(1)/impact-forecasting.jsp

Bank of England. (2017). Quarterly bulletin Q2: The Bank of England’s response to climate change. Retrieved from https://www.bankofengland.co.uk/quarterly-bulletin/2017/q2/the-banks-response-to-climate-change

Bank of England (BoE). (2018). Transition in thinking: The impact of climate change on the UK banking sector. Retrieved from https://www.bankofengland.co.uk/prudential-regulation/publication/2018/transition-in-thinking-the-impact-of-climate-change-on-the-uk-banking-sector

BlackRock. (2018a). Larry Fink’s annual letter to CEOs, a sense of purpose. Retrieved from https://www.blackrock.com/corporate/investor-relations/larry-fink-ceo-letter

BlackRock. (2018b). Investment Stewardship, our engagement priorities for 2017-2018. Retrieved from https://www.blackrock.com/corporate/about-us/investment-stewardship/voting-guidelines-reports-position-papers#2018-priorities.

Buchner, B., Oliver, P., Wang, X., Carswell, C., Meattle, C., & Mazza, F. (2017, October). Global landscape of climate finance 2017. Climate Policy Initiative. Retrieved from https://climatepolicyinitiative.org/publication/global-landscape-of-climate-finance-2017/.

Business Commission for Sustainable Development (BCSD). (2017a). Better business better world. Retrieved from http://report.businesscommission.org/uploads/BetterBiz-BetterWorld_170215_012417.pdf

Business Commission for Sustainable Development. (2017b). How the world can finance the SDGs. Retrieved from http://businesscommission.org/our-work/new-report-how-the-world-can-finance-the-sdgs

Business Commission for Sustainable Development. (2017c). Valuing the SDG prize. Retrieved from http://businesscommission.org/our-work/valuing-the-sdg-prize-unlocking-business-opportunities-toaccelerate-sustainable-and-inclusive-growth

Carney M. (2018, April). A transition in thinking and action. Speech by Mark Carney.

Carney M. (2015, September). Breaking the tragedy of the horizon - Climate change and financial stability. Speech by Mark Carney.

CERES. (2018). CERES web site climate action 100+. Retrieved from https://www.ceres.org/initiatives/climate-action-100

De Nederlandsche Bank (DNB). (2017a). Waterproof? An exploration of climate-related risks for the Dutch financial sector. Retrieved from https://www.dnb.nl/en/news/news-and-archive/dnbulletin-2017/dnb363837.jsp

De Nederlandsche Bank. (2017b, October). Increasing climate-related risks demand more action from the financial sector.

Economist Intelligence Unit (EIU). (2015). The cost of inaction: recognizing the value at risk from climate change. Retrieved from https://eiuperspectives.economist.com/sites/default/files/The%20cost%20of%20inaction_0.pdf

EU High-Level Expert Group on Sustainable Finance. (2017). Financing a sustainable European economy – Interim report. Retrieved from https://ec.europa.eu/info/publications/170713-sustainable-finance-report_en

EU High-Level Expert Group on Sustainable Finance. (2018). Financing a sustainable European economy – Final report. Retrieved from https://ec.europa.eu/info/publications/180131-sustainable-finance-report_en

FTSE Russell. (2018). Investing in the global green economy: busting common myths. Defining and measuring the investment opportunity. Retrieved from https://www.ftserussell.com/sites/default/files/ftse_russell_investing_in_the_global_green_economy_busting_common_myths_may_2018.pdf

Global Adaptation & Resilience Investment Working Group (GARI). (2017). An investor guide to physical climate risk & resilience. An introduction. Retrieved from https://garigroup.com/investor-guide

GIIN. (2018). Financing the sustainable development goals: Impact investing in action. Retrieved from https://thegiin.org/research/publication/financing-sdgs

Green Finance Task Force. (2018). Accelerating Green Finance. Retrieved from http://greenfinanceinitiative.org/workstreams/green-finance-taskforce/

HSBC. (2018). ESG moves mainstream. Retrieved from https://www.hsbc.com/news-and-insight/insight-archive/2018/esg-becomes-a-priority

International Energy Agency (IEA). (2018a). Global energy & CO2 status report, 2017. Retrieved from https://www.iea.org/publications/freepublications/publication/GECO2017.pdf

International Energy Agency (IEA). (2018b). Key world energy statistics, 2018. Retrieved from https://webstore.iea.org/download/direct/2291?filename=key_world_2018.pdf

International Finance Corporation (IFC). (2016). Climate investment opportunities in emerging markets. Retrieved from http://www.ifc.org/wps/wcm/connect/news_ext_content/ifc_external_corporate_site/news+and+events/news/new+ifc+report+points+to+%2423+trillion+of+climate-smart+investment+opportunities+in+emerging+markets+by+2030

International Finance Corporation (IFC); European Development Finance Institutions (EDFI); European Bank for Reconstruction and Development (EBRD); African Development Bank (AfDB); Inter-American Development Bank Group (IDBG); Asian Infrastructure Investment Bank (AIIB); European Investment Bank (EIB); Asian Development Bank (AsDB); Islamic Corporation for the Development of the Private Sector (ICD). (2017, October). DFI working group on blended concessional finance for private sector projects, summary report. Retrieved from https://www.publications.iadb.org/en/dfi-working-group-blended-concessional-finance-private-sectorprojects-summary-report

Intergovernmental Panel on Climate Change (IPCC). (2018). Special report on global warming of 1.5°C. Retrieved from http://www.ipcc.ch/report/sr15/.

IRENA and CPI. (2018). Global landscape of renewable energy finance, 2018. Abu Dhabi: International Renewable Energy Agency. Retrieved from https://www.irena.org/publications/2018/Jan/Global-Landscape-of-Renewable-Energy-Finance.

Munich Re NatCatSERVICE Statistics. (2017). https://www.munichre.com/en/reinsurance/business/non-life/natcatservice/index.html

Nelson, E. (2018). When will “socially responsible investing” become just “investing”? Retrieved from https://qz.com/1309419/when-will-socially-responsible-investing-become-just-investing/

NGFS. (2018). First meeting of the Central Banks and Supervisors Network for Greening the Financial System (NGFS) on January 24th in Paris. Retrieved from https://www.banque-france.fr/en/communique-de-presse/first-meeting-central-banks-and-supervisors-network-greening-financial-system-ngfs-january-24th

Principles for Responsible Investments (PRI) (2017). The SDG Investment Case, https://www.unpri.org/sdgs/the-sdginvestment-case/303.article.

Rainforest Action Network. (2017). Banking on climate change. Retrieved from https://www.ran.org/banking_on_climate_change

S&P Global Ratings. (2017). How environmental and climate risks and opportunities factor into global corporate ratings - An update. Retrieved from https://www.spratings.com/documents/20184/1634005/How+Environmental+And+Climate+Risks+And+Opportunities+Factor+Into+Global+Corporate+Ratings+-+An+Update/5119c3fa-7901-4da2-bc90-9ad6e1836801

S&P Global Ratings. (2018). The effects of weather events on corporate earnings are gathering force. Retrieved from https://www.spratings.com/documents/20184/4918240/The+Effects+of+Weather+Events+on+Corporate+Earnings+Are+Gathering+Force_Revised/6f654f4a-2be2-475f-a1cb-096f5b70201a

Trabacchi, C., & Mazza, F. (2015). Emerging Solutions to Drive Private Investment in Climate Resilience. A CPI Working Paper, 2015, https://climatepolicyinitiative.org/publication/emerging-solutions-to-drive-privateinvestment-in-climate-resilience/.

Task Force on Climate-Related Financial Disclosures (TCFD) (2017), Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures (June 2017), https://www.fsb-tcfd.org/publications/final-recommendations-report/

The Global Innovation Lab for Climate Finance (The LAB) (2017), Climate Resilience and Adaptation Finance and Technology Transfer Facility (CRAFT), Instrument Analysis 2017, https://www.climatefinancelab.org/project/climate-resilience-adaptation-financetransfer-facilitycraft/

Tonkonogy, B., Brown, J., Micale, V., Wang X., and Clark A. (2018). Blended finance in clean energy: Experiences and opportunities. A report for the Business & Sustainable Development Commission and the Blended Finance Taskforce, Climate Policy Initiative January 2018. Retrieved from https://climatepolicyinitiative.org/publication/blended-finance-clean-energy-experiences-opportunities/.

The Global Innovation Lab for Climate Finance (The LAB). (2016). Climate smart lending platform. Retrieved from https://www.climatefinancelab.org/project/climate-smart-finance-smallholders/.

The Global Innovation Lab for Climate Finance (The LAB). (2017). Climate Resilience and Adaptation Finance and Technology Transfer Facility (CRAFT), Instrument Analysis 2017, https://www.climatefinancelab.org/project/climate-resilience-adaptation-financetransfer-facilitycraft/.

World Bank Development Indicators (2018) database last accessed on November 2018 available at http://datatopics.worldbank.org/world-development-indicators/themes/environment.html.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 Springer Nature Switzerland AG

About this chapter

Cite this chapter

Trabacchi, C., Buchner, B. (2019). Unlocking Global Investments for SDGs and Tackling Climate Change. In: Valentini, R., Sievenpiper, J., Antonelli, M., Dembska, K. (eds) Achieving the Sustainable Development Goals Through Sustainable Food Systems. Springer, Cham. https://doi.org/10.1007/978-3-030-23969-5_9

Download citation

DOI: https://doi.org/10.1007/978-3-030-23969-5_9

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-23968-8

Online ISBN: 978-3-030-23969-5

eBook Packages: Biomedical and Life SciencesBiomedical and Life Sciences (R0)