Abstract

The problem of trading FTRs can be understood as one of decision making under uncertainties, where the boundary conditions are set by the laws of physics that govern the electric power flows. Under this setup, a typical FTR desk has to deal not only with standard roles of trading financial products, but also with technical ones of power analytics. Building and operating a successful FTR business is a complex enterprise, with multiple factors to consider. Additionally, the still exotic nature of the product makes standard solutions from the trading industry difficult to use. Accordingly, this chapter describes some of the challenges we currently face while trading FTRs in the US, covering three aspects of the business.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

11.1 Introduction

The problem of trading FTRs can be understood as one of decision making under uncertainties, where the boundary conditions are set by the laws of physics that govern the electric power flows. Under this setup, a typical FTR desk has to deal not only with standard roles of trading financial products, but also with technical ones of power analytics. Building and operating a successful FTR business is a complex enterprise, with multiple factors to consider. Additionally, the still exotic nature of the product makes standard solutions from the trading industry difficult to use. Accordingly, this chapter describes some of the challenges we currently face while trading FTRs in the US, covering three aspects of the business.

The first one deals with the process of building an FTR portfolio and executing the trade (Sect. 11.2). The idea is to go over the different steps mentioning standard practices and most relevant challenges, which are described in the subsections: Data, Analysis, Portfolio Construction, and Trade Execution. The second one (Sect. 11.3) covers alternatives for managing risk and the role played by the FTR desk. Also here, the goal is to describe current situation and open issues, which are elaborated in the sub-sections: Managing Current Exposure, Risk Management, Interaction with Other Desks, and Profile of the “FTR Trader”. The third one (Sect. 11.4) mentions a potential evolution of the FTR business. A brief description of alternative scenarios is mentioned in the sub-section: Next Steps. Finally, this chapter concludes with a summary of challenges we encounter in the real life operation of an FTR business.

11.2 Building an FTR Portfolio and Executing Trade

11.2.1 Data

Currently in the US there are six markets where it is possible to trade FTRs: PJM, MISO, ISONE, NYISO, CAISO, and ERCOT (The ISO/RTO Council 2012). The general concepts are the same in all of them; however, there are differences in implementation. The first barrier faced in dealing with FTRs is the lack of standards in producing and publishing relevant market data. This problem has implications in three sub-problems: gathering, normalizing, and storing in database. The first one deals with identifying the best places to collect and implementing systematic processes to capture data. The second one relates to the most laborious task, normalizing the data which includes, among other things, mapping different names to the same physical element and with the same format. This task cannot be fully automated, requiring laborious manual intervention. And finally, the third one refers to the efficient storage of data in master database. The main source of raw data comes from the ISOs which can be classified as indicated in Table 11.1

There is an additional set of data coming from ISOs’ meetings (committees, subcommittees, task forces, working groups, etc.) which provide very valuable information. In small to mid-size companies, the task of following these meetings is performed by the FTR desk, however this additional function is difficult to accomplish properly, considering the number of activities to cover. Large organizations, on the other hand, have Market Affairs teams or Regulatory Policy teams dedicated to this function. However, due to the technical details involved, it is difficult for them to identify exactly what may be valuable for different areas of the company. Sometimes, companies complement their coverage subscribing to services provided by Market Specialists/Consultants.

In general, the topics discussed in these meetings are relevant to the FTR business, however, on specific instances they are critical to understand or value substantial changes in the market. Companies that can translate this type of information into trading signals have a clear advantage. Definition of new interfaces, retirement of reliability must run units, implementation of special protection schemes on active binding constraint, redefinition of load pockets, derates on critical facilities, are few examples of topics presented in some of the mentioned meetings and that generally impact the market.

Unfortunately, it is usually difficult to automate the identification and collection of relevant information from written documents (or voice records). State of the art software that can interpret text/voice, like the ones used in equities trading (RavenPack 2012), should facilitate this task.

In addition, there are services provided by third parties that help having a better picture of the market dynamics. Some of them are listed in Table 11.2.

Clearly, the objective in this initial step is to concentrate, normalize, and store all these diverse data in an efficient manner. However, implementing and managing this task is very challenging.

An operation covering PJM and MISO which is evaluating to build an infrastructure to manage 2 years of data would have to consider for instance the following requirements:

-

Dimensionality: building database with around 210 tables, three billion records, and 400 GB of disk space

-

Dispersion of data sources: maintaining 15 web data collectors (scrapers)

-

Lack of standards: mapping and normalizing 50,000 records

The scale of this problem is equivalent to the one managed by a leader mobile telecom operator serving four million customers.

11.2.2 Analysis

The next step is to process the data looking for trading signals. Here we consider two alternative approaches, one based on fundamental analysis, and the other based on quantitative analysis.

The fundamental based approach relies on the fundamentals of power systems to explain the occurrence of congestion. There are different options to perform this analysis but all of them share the principle of linking congestion events with particular scenarios of supply, demand, transmission, and operation of the system. AC and DC Power Flow models, Optimal Power Flow analysis, Unit Commitment Security Constrained OPF simulations, are some of the concepts or methodologies commonly used to perform this task (Wood and Wollenberg 1996). Typically, this analysis is performed using some of the standard software products available in the industry (e.g. PSSE, PowerWorld Simulator, DAYZER, SCOPE, GEMAPS).

The quantitative based approach relies on principles of statistical analysis to process large amounts of data to identify overall trends. There are different alternatives to perform this task but all of them share the same idea of objectively identifying trends or patterns out of noisy data. Linear and Non-Linear Regressions, Data Mining, Time Series Analysis, Principal Component Analysis, are some of the concepts or methodologies commonly used to perform this task (Nisbet et al. 2009). In this case, the analysis is done using proprietary models written in technical-oriented programming languages (e.g. Matlab, Mathematica, R, C#, Java)

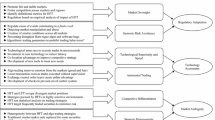

For both approaches, the process follows the sequence indicated in Fig. 11.1.

Analysis flowchart

The objective in this step, independently of the approach, is to obtain trading signals. In terms of FTRs, trading signals refer to bullish or bearish views on congestion. However, if the inputs for the quantitative approach are prices, then trading signals could be source-sink paths.

To finish, it is necessary to quantify the relevance of the simulated signals (ranking), which are obtained comparing expectation (edge) relative to dispersion (conviction).

Some of the challenges include:

-

Confidence in data: unfortunately, it is not rare to observe changes in relevant published information after the auction is closed, invalidating the simulated signals.

-

Technology barrier: building and processing complex simulations (e.g. Unit Commitment Security Constrained OPF runs) for large systems is still beyond most operations’ technical capabilities.

11.2.3 Portfolio Construction

In context of the standard optimization problem solved by the ISOs, congestion refers to transmission binding constraints (BCs), which are specified as monitor element (monitor) and contingent element (contingency) (Schweppe et al. 1998). Not all BCs share the same drivers, therefore, they have different behaviors. Some of these drivers are listed in Table 11.3. In order to be systematic in this classification, it is necessary to quantify these behaviors (e.g. using higher moments).

One of the main differences between FTRs and other financial products is that the selection of the contract to trade, source-sink path (path), is a decision variable. Depending on the strategy, it may be even more relevant selecting a path than pricing it.

Here, it is necessary to remark that a path is impacted by active BCs with positive or negative contribution depending on its exposure. Accordingly, a long exposure refers to paths that have positive correlation to a target BC, receiving positive revenues when the BC is active. Bullish views tend be expressed by paths with long exposure to the associated BC. On the other hand, a short exposure refers to paths that have negative correlation to a target BC, receiving negative revenues when the BC is active. Bearish views tend to be expressed by paths with short exposure to the related BC. Following the same logic, a long-short exposure refers to paths that have positive correlation to one target BC and negative correlation to a different one. Combining bullish and bearish views can be expressed by paths with long-short exposures. In addition, counterflow is a particular case of exposure to a BC different from the desired one. In general the expression refers to adverse congestion that produces revenues with the opposite sign to the expected when initiated the trade.

In markets with limited number of CPNodes, it is difficult to select source-sink pairs that have exposure to a single or dominant BC. Here there are two side effects to consider, one is the cost of paying for undesired BCs, and the other is counterflow risk. In the case of Obligation FTRs, the second issue is maybe FTR Traders’ most feared risk. To address this problem, some ISOs have implemented Option FTRs (Pameshwaran and Muthuraman 2009).

The construction of the bidding curve requires definition of Auction, Period, Source, Sink, Time of Use (On Peak, Off Peak), Trade Type (Buy, Sell), Hedge Type (Obligation, Option), Price, and Volume. To simplify the pricing for different periods, it is usual to work in $/MWh terms and then convert it to $/MWPeriod before submitting. In this problem, Price, Volume and Shape of the Bidding Curve are the key decision variables. Figures 11.2 and 11.3 describe the accepted formats for bidding curves.

Step function bid curve

Piece-wise bid curve

An interesting characteristic of FTRs is that price (P) and quantity (Q) are unknown before executing the trade. We only have control over maximum price to pay/minimum price to receive, and maximum volume to clear. So, FTR auction simulators are built to evaluate contingent performances of the working portfolio. Adjustments in bidding curves are made until differences between simulated and target portfolios are acceptable. Finally, we obtain the portfolio to be submitted in the FTR auction.

Some notable challenges include:

-

Counterflow risk: limited number of CPNodes available for trading Obligation FTRs (in some ISOs) makes difficult selecting source-sink paths with limited counterflow exposure. Furthermore, not all ISOs have Option FTRs.

-

P and Q are unknown: acquiring FTRs from auctions adds a new layer of complexity in the risk taking process. The uncertainty associated with price and quantity results in getting a cleared portfolio different from the targeted one.

11.2.4 Trade Execution

The trade execution is a simple process; however, there are some requirements to satisfy and validations to perform. The first requirement is related to collateral to support FTR bids. Here again, each ISO has different level of collateralization requirement according to its credit policy, but all of them share the principle that to participate in the FTR auction, a market participants has to have sufficient capital.

Then, the CPNodes used in the different paths have to be valid for the particular FTR auction we plan to submit. For example, CPNodes valid for prompt auctions may not be necessarily valid for non-prompt auctions. Sometimes, during early stages of the portfolio construction the valid CPNode list for the next auction is not available, therefore it is a good practice to implement a CPNode validation step.

Furthermore, it is necessary to convert the target portfolio to the accepted format (xml files). Although this formatting process is not complex, the cost paid for mistakes here can be enormous. For example, changing sources for sinks automatically converts long exposures into short exposures (or vice versa), or using the wrong number of hours for a given period changes the bidding prices.

The submission is implemented electronically, through secure sites, uploading xml files manually or through programmatic interfaces. As mentioned before, the cost of operational mistakes in this step could be high. Therefore, a prudent step is to validate that the submitted portfolio is exactly the portfolio we wanted to submit.

After this final validation, the trading execution is concluded. Auction results, in general, are published within 10 days.

Some relevant challenges in FTR trade execution are:

-

Prone to costly mistakes: it is common to have several auctions overlapping during the same period of time. For small/mid-size operations, in particular, this issue creates substantial pressure when controlling and validating different portfolios/auctions. In large operations, on the other hand, this problem is reduced; however, distractions from crowded trading floors work against them too. Compounded by the fact of dealing with an almost illiquid product, mistakes in trading execution could be just too high to bear.

-

Execution infrastructure: building a robust infrastructure is critical to mitigate execution risk. However, here also the lack of standards creates some frictions that require special treatments.

11.3 Managing Risk and the Role Played by the FTR Desk

11.3.1 Managing Current Exposure

Currently, and depending on the ISO, it is possible to trade FTRs from 3 years to 1 month forward (Long-Term: 1–3 years, Annual: 1 year, Balance of the Year: less than 1 year, Monthly: 1 month).

This temporal discretization goes in line with different market needs. The power market evolves over time, so does our trading signals, convictions and target portfolios. So, it is common to start accumulating core positions in Long-Term Auctions and/or Annual Auctions and then adjusting the portfolio in Monthly/Balance of the Year Auctions. The last opportunity we have for implementing this strategy is during the Monthly Auction just before delivery.

However, because of the few opportunities we have to trade (in comparison with other financial products), it is very difficult to arrive to delivery with a balanced portfolio. An alternative to improve this situation is to trade FTRs in secondary markets. Most ISOs have implemented an environment for this purpose. Unfortunately, participation has been minor. On the other hand, attempts to build a bilateral market for predefined paths have gained some interests. However, the reality is that most FTR paths target idiosyncratic factors which are difficult to match in bilateral trades, limiting the attractiveness of the concept.

During delivery, the FTR portfolio is subject to DA congestion. In case we prefer to get exposed to RT congestion, then it is possible to do it using some of the daily DA-RT swaps available in the market. The most common DA-RT product is Virtual Bidding (VB) (Metin et al. 2010), which is a contract specified by hour and CPNode. There are two products, INC that settles as the difference in LMPs between DA and RT, and DEC that settles as the difference in LMPs between RT and DA.

The strategy requires to INC at source and DEC at sink of the FTR we want to get exposure from RT market. This strategy is easy to implement however transaction cost can be significant. Furthermore, there is volumetric risk when clearing unbalanced portfolio results in net long/short exposure to absolute LMP instead of desired locational spread. Additionally there is spread risk which refers to price taker strategy predisposed to unlimited DA congestion cost.

To address these risks, some ISOs have implemented a product that trades balanced spreads (e.g. Up to Congestion contracts in PJM), which settles as the difference in LMPs between RT and DA (PJM 2012). In this case the strategy requires using the same source and sink of the FTR we want to get exposure from RT market. In case they are not available, then use some proxy CPNodes at the expense of getting different BCs’ exposure. The main advantage here is that this product solves both volumetric and spread risks.

There are two other aspects of relevance about these DA-RT contracts. The first one relates to Transaction Costs, which sometimes can be significant. Furthermore, these costs are known after the fact, turning it difficult to incorporate properly in the trading strategy. Moreover, this friction limits the success of its original goal of improving convergence between DA and RT markets.

The second one is more controversial, and is related to the impact that this activity has in DA results. These strategies, Virtual Injections and Virtual Withdraws, create additional power flows in the DA solution, and consequently affect DA congestion. Furthermore, in the case of using proxy CPNodes, DA congestion may diverge from the expected based on fundamentals (phantom congestion). However, the most problematic issue arrives when strategic bidding creates DA congestion on purpose to increase FTR revenues (or the value of any other contract that settles on DA prices). Strict monitoring is necessary to identify and mitigate these behaviors.

In the OTC market, the alternatives for proper portfolio rebalancing are even more limited. Even though there are products that have good liquidity (ICE 2012), the main limitation is the weak correlation between these OTC products and FTR portfolios. A reason for this observation is that the typical factors that explain most dynamics in OTC products are less relevant for FTR portfolios. On the contrary, specific FTR paths provide complementary value to OTC portfolios.

Based on these reasons, the concept of active portfolio management to optimize current exposure is difficult to implement in the case of FTRs.

Some of the current challenges include:

-

Liquidity: opportunities to trade FTRs are few, in general once a month with limited volume in reconfiguration auctions. Furthermore, the secondary market has not developed as anticipated, and the OTC products are poorly correlated with FTRs.

-

Transaction costs: during delivery, there is a possibility to move part of the DA exposure to RT, however transaction costs for VB (including operating reserve charges, volumetric and spread risks) have worked against this strategy.

11.3.2 Risk Management

It is necessary to consider the different components of risk involved in the whole process before, during, and after the auction. Before the auction, the main risks come from inaccuracies in data, assumptions, models, and/or their usage in Analysis and Portfolio Construction steps. Procedures to control this type of risk include performing quality control of data, validating models and hypothesis, and verifying most recent published information. Within the risk management process, these risks tend to be part of Operational Risk and Modeling Risk considerations.

During the auction, the main risks come from operational mistakes and/or technology failures during Trade Execution. Procedures to control these risks include submitting preliminary portfolios to test own infrastructure/technology, performing validation of submitted portfolio against target portfolio, and building and testing technology back-up infrastructure. Within the risk management process, these risks tend to be part of the Operational Risk and Execution Risk concerns.

After the auction, the main risks come from the impact of realized congestion on cleared portfolio. Here, it is important to recognize two levels of realizations. On one hand, a normal range, where congestion is related to drivers such as weather events, unexpected outages, over/under-commitment, etc., which tend to produce transitory patterns. On the other hand, an extraordinary range, where congestion is related to a permanent pattern change. Furthermore, and primarily due to non-storage nature of electricity (wholesale level) and operational constraints (ramping, operating procedures, localized inflexibility due to outages), it is observed that tail events are a lot more common in FTRs than in other energy products (i.e. leptokurtosis) (Adamson et al. 2010). Within the risk management process, these risks tend to be part of the Market Risk, Liquidity Risk, and Credit Risk concerns. Additionally, Underfunding Risk and Default Risk require special considerations.

The standard risk management role includes periodic evaluation of Value at Risk (VaR), which tends to provide a good indication of risk involved in a portfolio for a normal range of realizations. To complement this metric, some forms of Stress Testing and Concentration Analysis are also performed looking for risk associated with realizations in the extraordinary range. These evaluations are part of the Market Risk assessment and are described below.

-

VaR: the maximum loss that will not be exceeded with a given probability (confidence level) over a given period of time. In general, a simulative model is created, using historical congestion realizations adjusted by seasonality and giving more weights to more recent realizations. This approach is very flexible and easy to implement, however it ignores congestion patterns not present in the historical sample.

-

Stress Testing: this analysis is performed for specific scenarios looking for extreme realizations. The key issues are, calculating net exposure for different BCs, and defining under which circumstances the portfolio is exposed to counterflow.

-

Concentration Analysis: the basic approach is to use a risk aggregator to convert source-sink paths in net exposure (MW) for each branch monitored in DA market.

Sometimes to complement these three metrics, the risk management function also calculates Conditional Value at Risk (CVaR) that is more sensitive to the shape of the loss distribution in the tail of the distribution (Uryasev 2001).

With this information, the risk manager evaluates Liquidity Risk. The basic idea is to make sure that the company has allocated enough capital to the FTR account to pay invoices. Given the uncertainties and assumptions involved in different calculations, a conservative approach is to keep liquid funds to pay invoices equals to a multiple of the current VaR.

Additionally, on a daily basis, a common metric used by different roles within the organization is the Profit and Loss (PL) report. Standard reports include Year to Date PL, Month to Date PL, and Today’s PL. Sometimes Inception to Date PL is also included. Here it is important to clarify the difference between Realized PL and Marked to Market PL.

-

Realized PL: results from calculating the difference between DA revenues and FTR auction cost. This PL is replicable by anyone (FTR inventories and DA prices are public information).

-

Marked to Market PL: results from calculating the difference between future DA revenues (represented by a market quote) and the corresponding FTR auction cost. The challenge here is that there is no liquid forward market for FTRs. As a result, it is common to use models to estimate future revenues adjusted by a liquidity factor. In this case, this model-driven PL is more difficult to replicate and may create disagreements.

These PL refer to gross values, therefore to obtain the net PL it is necessary to include in the calculation Underfunding, Defaults, and Fees/Adjustments.

-

Underfunding: in some ISOs FTR is not a fully funded contract, therefore PL has to be adjusted by this factor. Basically, if the transmission capacity sold ahead of time in the auction is more than the available transmission capacity during delivery, then the ISO does not collect enough revenues to pay its obligations. This problem is not minor, and is currently a topic of debate.

-

Defaults: in case of default events, the ISO socializes the incurred losses among market participants proportional to their participation in the different markets administered by the ISO (even participants with no FTR positions share part of the default cost).

-

Fees and Adjustments: there are some administrative fees per bid and cleared position as well as adjustments in case of corrections in prices or other factors that require proper considerations.

In context of bilateral contracts, the concept of credit risk deals with credit exposure and credit quality associated with counterparties; where credit exposure refers to the magnitude of the risk and credit quality refers to the likelihood of the risk. In the case of FTRs, where there is no specific counterparty besides the ISO, the concept of credit risk is adjusted to include Underfunding and socialized Defaults.

Additionally, the risk involved with policy changes is not minor, also, very difficult to quantify. An alternative approach to deal with regulatory risk is to have an active participation in the different policy meetings relevant to the business. However, as mentioned in section on data (Sect. 11.2.1), this task is not easy to address effectively.

Moreover, some return on risk metrics (e.g. Sharpe ratio) can mislead the risk the portfolio is running if it is not analyzed properly. As explained in section Managing Current Exposure (Sect. 11.3.1), most FTR paths are accumulated in Long-Term/Annual Auctions, therefore setting portfolio’s performance until delivery. A good Sharpe ratio could just reflect that a dominant position acquired in Long-Term Auction is suddenly in the money due to a particular congestion pattern, but does not say much about the other “sleeping” paths.

Finally, and given the specific characteristics of FTRs, it is beneficial to also include some risk management practices used for Alternative Investments, for example similar to the ones described in (Jorion 2009).

Some of the remaining challenges on FTR risk management include:

-

Underfunding: this issue is nowadays a serious concern, at the extreme of making some trading strategies unprofitable. Furthermore, the problem is even adding risk to standard hedges that are not working as designed.

-

MtM models: MtM PL is a metric generally requested not only by groups within the company but also by investors. However, its value can be challenged, creating additional burden to the desk.

-

Path dependence: portfolio performance is strongly dependent on the FTR paths locked in during Long-Term/Annual Auctions, therefore simplistic performance metrics could underestimate the portfolio’s risk.

-

Choosing proper risk management approach: standard models for quantifying risk do not necessarily apply to FTRs. Furthermore, even if risk is properly quantified, nature of product makes difficult to rebalance the portfolio. Therefore, some risk management approaches used for Alternative Investments may be a good complement.

11.3.3 Interaction with Other Desks

Originally, with a single price per control area (or power pool), the focus of transmission analysis was primarily concentrated on inter-ties. However, the arrival of locational pricing shifted the focus to the transmission system within control areas. The immediate reaction has been to allocate more resources to transmission analysis, and then build an FTR desk. Currently, there are multiple players participating in the FTR business such as investment banks, hedge funds, private equity shops, proprietary desks, global energy companies, merchant power plants, municipalities, utilities, cooperatives, service providers, etc.

Independently of the type of player, it is common to have Management, Researchers/Analysts, Risk Takers, and Back Office personnel. The arrival of the FTR desk creates an interesting dynamics, in particular with the Power Desks and Back Office roles. A brief description of these different roles and the link with the FTR desk is described in Tables 11.4 and 11.5.

The strong link between FTR desk and these roles comes from the current relevance that congestion has in power prices. Therefore, it is observed that the desk is a permanent provider of congestion views for different scenarios and time horizons. In particular, it is highly requested when a new congestion pattern arrives in the market. Consequently, nowadays the FTR desk plays a central function within the Power business.

In this case also, the arrival of this new product impacted these teams. In particular, its exotic nature has forced the FTR desk to be creative to explain its business and to be flexible to adapt to standard company’s requirements.

Some main challenges on the interaction of desks include:

-

Diverse interests: the difficulty comes not only from satisfying multiple and sometimes conflicting interests but also from explaining nature of FTR business to diverse audiences.

-

Integration: even though the relevance of the FTR desk in the trading floor has increased, its true value that comes from a full integration has been difficult to materialize.

11.3.4 Profile of the “FTR Trader”

The traditional trading business separates roles among IT, Data, Analytics, and Trading. However, in the case of the FTR business, these roles tend to be self-contained within the FTR desk. Therefore, the “FTR Trader” performs tasks beyond the standard ones. Accordingly, this new profile requires proficiency according to the ones presented in Table 11.6.

Clearly, it is difficult to find candidates who score high in these four skills. Therefore, a more realistic proposal is to build a team with members complementing each other. The recruiting effort is not minor, on one hand the pool of experienced talent is not big (FTR is still a niche), and on the other hand the job itself is very demanding. There is consensus among recruiters that there are only three true job interview questions (Bradt 2011), which in terms of the FTR business refer to:

-

1.

Can you do the job? This question is the one generally addressed in the interviews, where technical skills and specific knowledge (i.e. Transmission, Risk Taking, IT/Data) are evaluated. Moreover, the answers can be quantified properly and comparison among candidates is easier.

-

2.

Will you love the job? This one refers to comparing expectation with reality of the open position. Most of the time the “FTR Trader” has to deal with tasks that can be considered tedious and sometime even repetitive/boring but in the end result critical to the overall success (e.g. normalizing data, reading long reports, analyzing power flow cases). It is very important to communicate this reality to the candidate looking for honest feedbacks.

-

3.

Can we tolerate working with you? Sometimes also known as “The Airport Test”, this question focus on the candidate’s interpersonal skills and how well he/she fits within the existing team’s working culture.

Finally, after building the FTR team and working together for 1 or 2 years, the desk starts to consolidate.

The main two challenges presented in this section are:

-

Recruiting: the pool of experienced talent is not big enough to satisfy current hiring needs. Moreover, recruiting out of school requires substantial investment in training and coaching.

-

Building and consolidating: finding the right candidates is only part of the challenge, it is even more difficult to keep them long enough to consolidate the business. Consolidation is a process that takes time, unfortunately many companies are not patient enough to make it a reality.

11.4 Potential Evolution of the FTR Business

11.4.1 Next Steps

A natural evolution should occur to both the product FTR and the FTR desk. The first one would require addressing some of the issues indentified in this chapter, in particular underfunding and liquidity. The second one would require institutionalizing the whole trading process. This will be even more necessary if additional areas within the US and/or other countries decide to implement LMPs and FTRs.

Also, a good integration between FTR and Structured Products desks providing liquidity beyond the time horizon covered by FTR auctions would be necessary. Tolling agreements, customized deals, load serving contracts, are some of the transactions that require hedging basis risk. Nowadays, this is difficult to achieve considering the limited quotes beyond liquid hubs. That is where FTR desks should appear in the process pricing competitively illiquid locations and working close by Structured Products desks implementing these multipart deals.

Besides, a better interaction with state of the art Quant desks would add complementary skills to this technology intensive business. As time evolves it is becoming more evident of the critical role played by technology in a more globalized business environment.

Here, some of the challenges include:

-

Evolution and consolidation: the real challenge in the next years would be for the current FTR desks to adjust fast enough to a more global and sophisticated trading environment, and for the FTR concept to consolidate as a liquid financial instrument.

-

Expanding beyond the US: attempts to transition towards full LMPs and FTRs in some countries have not evolved beyond initial discussions.

11.5 Conclusions

In the last 10 years, the FTR business has evolved substantially, with more markets to trade and more sophisticated FTR operations. During the early days, traders with their own spreadsheets and simplistic models participated in the market. Nowadays, there are several teams of researchers approaching the problem in a more quantitative manner, running highly sophisticated trading platforms, turning FTRs in a technology driven business.

Moreover, the low correlation between FTRs and global financial markets has made this product very appealing. This fact has attracted the interest from financial institutions and a diverse set of investors. Furthermore, over time, it is expected that the area covered by LMPs and FTRs be sizable enough to allow even more attractive business opportunities.

However, there are still multiple challenges to address before realizing the full value associated with the concepts of LMPs and FTRs. Some of them, as seen from the proprietary trading side, have been discussed in this chapter and are summarized as follows:

-

Data: The volume, dispersion of sources, and lack of standards makes the data management problem the first obstacle to pass. The scale of this problem requires highly sophisticated solutions. However, normalizing data also involves tedious manual intervention.

-

Analysis: Independently of the approach, fundamental-based or quantitative-based, it is critical to have reliable data. Unfortunately, it is not rare to observe changes in relevant published information after the auction is closed, invalidating the simulated signals. Furthermore, building and processing complex simulations for large systems is still beyond most operations’ technical capabilities.

-

Portfolio Construction: The limited number of CPNodes available for trading Obligation FTRs (in some ISOs) makes difficult to select source-sink paths with limited counterflow risk. Option FTRs present an interesting solution to this problem, but unfortunately only two ISOs offer the product and not for all CPNodes. Furthermore, acquiring FTRs from auctions adds a new layer of complexity in the risk taking process. The uncertainty associated with price and quantity results in obtaining a cleared portfolio different from the original targeted portfolio.

-

Trade Execution: The reality of having several auction deadlines overlapping during the same period of time, distractions from crowded trading floors, pressure of dealing with an almost illiquid product, and compounded by the nature of electronic execution, results in a process that is naturally prone to costly mistakes.

-

Managing Current Exposure: Comparing with other financial products, the opportunities to trade FTRs are very few, in general once a month with limited volume in reconfiguration auctions. Furthermore, the secondary market concept has not developed as anticipated, and the OTC products are poorly correlated with FTRs. As a result, and for most practical terms, a portfolio of FTRs is considered illiquid. During delivery, there is a possibility to move part of the DA exposure to RT; however, transaction costs (including operating reserve charges, volumetric and spread risks) have worked against this strategy. Based on these reasons, the concept of active portfolio management to optimize current exposure is difficult to implement.

-

Risk Management: Currently, underfunding is a hot issue. The severity of this problem turns some trading strategies unprofitable. Besides this problem, the standard models for quantifying risk do not apply necessarily to FTRs. Moreover, even if risk is properly quantified, the nature of this product makes difficult to rebalance the portfolio. Therefore, some risk management approaches used for Alternative Investments may be a good complement.

-

Interaction with other Desks: The strong link between FTR and the different Power Desks comes from the current relevance that congestion has in power prices. Therefore, the FTR desk is a permanent provider of congestion views for different scenarios and time horizons. In particular, it is highly requested when a new congestion pattern arrives in the market. Consequently, nowadays the desk plays a central function within the Power business. Also, the arrival of this new product impacted Back Office as well. In particular, its exotic nature has forced the FTR desk to be creative to explain its business. Summarizing, the relevance of the FTR desk in the trading floor has increased, however, its true value that comes from a full integration has been difficult to materialize.

-

Profile of the “FTR Trader”: The traditional trading business separates roles among IT, data, analytics, and trading. However, in the case of the FTR business, these roles tend to be self-contained within the FTR desk. Therefore, the “FTR Trader” performs tasks beyond the standard ones. Accordingly, this new profile requires proficiency in transmission, risk taking, and IT/data. Additionally, on the interpersonal side, he/she has to be able to tolerate the always demanding trading environment. Besides the difficulty in recruiting the right candidates, the business consolidation is a process that takes time.

-

Next Steps: The real challenge in the following years would be for the current FTR desks to adjust fast enough to a more global and sophisticated trading environment, and for the FTR concept to consolidate as a liquid financial instrument.

References

Adamson S, Noe T, Parker G (2010) Efficiency of financial transmission rights in centralized coordinated auctions. Energy Econ 32:771–778

Bradt G (2011) Top executive recruiters agree there are only three true job interview questions. http://www.forbes.com/sites/georgebradt/2011/04/27/top-executive-recruiters-agree-there-are-only-three-key-job-interview-questions. Accessed 6 June 2012

ICE (2012) OTC electricity contracts. https://www.theice.com/otc_electricity.jhtml. Accessed 6 June 2012

Jorion P (2009) Risk management for alternative investments. http://merage.uci.edu/~jorion/varseminar/Jorion-CAIA-isk_Management.pdf. Accessed 6 June 2012

Metin C, Attila H, Philip QH (2010) Virtual bidding: the good, the bad, and the ugly. Electr J 23:16–25

Nisbet R, Elder J, Miner G (2009) Handbook of statistical analysis & data mining applications. Academic, Amsterdam

Pameshwaran V, Muthuraman K (2009) FTR-option formulation and pricing. Electr Power Syst Res 79(7):1164–1170

PJM (2012) Two settlement virtual bidding and transactions. http://www.pjm.com/training/~/media/training/core-curriculum/ip-transactions-201/transactions-201-two-settlement.ashx. Accessed 6 June 2012

RavenPack (2012) RavenPack News Analytics. http://ravenpack.com. Accessed 6 June 2012

Schweppe F, Caramanis M, Tabors R et al (1998) Spot pricing of electricity. Kluwer, Boston

The ISO/RTO Council (2012) IRC Documents. www.isorto.org. Accessed 6 June 2012

Uryasev S (2001) Conditional value at risk (CVaR): algorithms and applications. http://www-iam.mathematik.hu-berlin.de/~romisch/SP01/Uryasev.pdf. Accessed 6 June 2012

Wood A, Wollenberg B (1996) Power generation operation and control. Wiley, New York

Acknowledgements

The Author would like to thank Dr. Carlos Larisson from UNSJ and Dr. Fernando Olsina from CONICET and UNSJ for reviewing early versions of this chapter and for their constructive suggestions. However, the Author is the only responsible for errors that may have occurred.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2013 Springer-Verlag London

About this chapter

Cite this chapter

Arce, J. (2013). Trading FTRs: Real Life Challenges. In: Rosellón, J., Kristiansen, T. (eds) Financial Transmission Rights. Lecture Notes in Energy, vol 7. Springer, London. https://doi.org/10.1007/978-1-4471-4787-9_11

Download citation

DOI: https://doi.org/10.1007/978-1-4471-4787-9_11

Published:

Publisher Name: Springer, London

Print ISBN: 978-1-4471-4786-2

Online ISBN: 978-1-4471-4787-9

eBook Packages: EnergyEnergy (R0)