Abstract

Financial service providers continually strive to develop innovative financial products and services that address customer needs and aim to improve customers’ financial well-being. Previous studies discovered that psychological need satisfaction is positively associated with psychological well-being and growth, while psychological need frustration is associated with problematic behaviour and ill-being. However, uncertainty still exists as to whether psychological needs are associated with financial well-being. Furthermore, whereas psychological need satisfaction is associated with positive day-to-day behaviours such as exhibiting self-control, psychological need frustration has been associated with irresponsible spending. Spending can be a psychological coping mechanism, and as such, the regulation of spending behaviour may aid financial well-being. Therefore, the main purpose of this article is to explore the relationship between psychological needs and financial well-being, and to assess whether consumer spending self-control can act as a regulating mechanism in this relationship. Data were collected by means of a self-administered questionnaire distributed via an online paid-for consumer panel to credit-active South African consumers. The results revealed that CSSC had a mediating effect on the relationships between psychological needs and financial well-being. This highlights the importance of developing and promoting consumer spending self-control as a strategy for financial well-being.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The competitive nature of the financial industry as well as the increase in consumer debt emphasises the value of gaining a deeper comprehension of consumers in terms of their needs and spending (Gerth et al. 2021; Leandro and Botelho 2022). Previous research considered the effects of various influences on spending behaviour, such as economic factors (Lusardi and Mitchell 2014), consumption values (Dittmar 2005) and individual biases and orientations (Guzman et al. 2019). In addition, spending has also been shown to be a psychological coping mechanism in cases of emotional and situational frustrations (Rice et al. 2020). Therefore, understanding the regulation of spending behaviour to aid financial well-being becomes important since it has implications for individual and societal economic health, for example, long-term economic stability (Brüggen et al. 2017; Lusardi and Mitchell 2014). This is important since a lack of psychological coping mechanisms may lead to excessive spending and debt (Leandro and Botelho 2022). A scholarly analysis to uncover the role of consumer spending self-control in the relationship between psychological needs and financial well-being can help financial providers develop interventions to guide consumers toward healthier spending habits.

Self-control enables people to stay committed to long-term goals, save more, spend less, manage their finances better, resist temptation and avoid instant gratification (Miotto and Parente 2015; Kim 2022). Thus, people’s ability to exercise self-control influences the degree to which financial and consumption behaviours are controlled and, subsequently, the level of financial well-being (or ill-being) experienced (Baumeister 2002; Miotto and Parente 2015). More specifically, consumer spending self-control (CSSC), that is, the regulation of spending-related beliefs and decisions aligned with self-induced standards or goals (Haws et al. 2012), provides a rich avenue for further investigation as CSSC also contributes to financial well-being (Ponchio et al. 2019).

Theoretically, the self-determination macro-theory provides a lens to explore how people engage in activities to proactively advance towards optimal development and functioning within their environment (Ryan et al. 2021), such as the development of financial well-being. Within the self-determination theory, the basic psychological needs mini-theory indicates that humans have innate psychological needs essential for development and well-being (Chen et al. 2015b; Ryan and Deci 2000). In addition, the causality orientations mini-theory within the self-determination theory, considers how people regulate their behaviour which supports the role of a regulatory system (such as CSSC) in spending behaviour (Deci and Ryan 1985; Hagger and Hamilton 2021). Thus, the regulation of the relationship between psychological needs and financial well-being may be better understood by exploring CSSC as a regulatory mechanism within this relationship.

The main objective of this study is to explore the role of consumer spending self-control (CSSC) in the relationship between psychological needs and financial well-being. This study is the first to explore the association between psychological needs and financial well-being which contributes to the advancement of scholarly understanding in both psychological and financial domains. Moreover, evidence suggests that developing and promoting CSSC may be a promising strategy to improve financial well-being (Haws et al. 2012). The significance of focusing on CSSC lies in its potential to fill current knowledge gaps in the interdisciplinary dialogue between behavioural psychology and financial decision-making. Findings will also inform theoretical frameworks and guide practical interventions. Finally, and central to the contribution, this study examines whether CSSC is a mechanism through which psychological needs are associated with financial well-being, previously unexplored. By considering CSSC, the research contributes to a better comprehension of the processes that link psychological factors to financial outcomes, which allows for the refinement of existing theories and models that capture the interplay between the psychology and financial domains.

This paper commences by arguing for the important role of CSSC between psychological needs and financial well-being based on the self-determination theory. Thereafter, the methodology used and the results are explained. Finally, the article concludes by providing practical marketing implications for financial service providers based on the findings, as well as acknowledgements of the limitations.

Theoretical background

Financial well-being

Financial well-being refers to a state of feeling content and worry-free about one’s financial situation (Chatterjee et al. 2019) and can be measured through objective and/or subjective measures (Losado-Otalaro and Alkire 2019). Objective financial measures provide evidence of an individual’s financial status, whereas subjective measures relate to people’s mental assessments (perceptions and emotions) of their financial situation (Losado-Otalaro and Alkire 2019). In the end, only individuals can evaluate their well-being and tell whether their financial situation is healthy (Brüggen et al. 2017). Thus, irrespective of the objective financial position people are in, it is their personal assessment of their financial situation that directs their level of financial well-being (Brüggen et al. 2017). As such, the subjective measure of the Consumer Financial Protection Bureau (2019) was included in this study. This definition of financial well-being refers to “the extent to which someone’s financial situation and the financial capacity that they have developed, provide them with security and freedom of choice” and has been incorporated in several previous studies (Abrantes-Braga and Veludo-de-Oliveira 2019; Dickason-Koekemoer and Ferreira 2019).

Psychological needs and financial well-being

The basic psychological needs theory within the self-determination theory identifies three psychological needs, namely autonomy, competence and relatedness (Chen et al. 2015a; Ryan and Deci 2000), which are fundamental components to ensure healthy psychological and social development, as well as overall well-being (). Autonomy relates to choice and control and recognises the individuals’ desire to make their own decisions and ensure their activities are aligned with their goals and sense of self. Competence relates to feeling capable and effective in one’s doings which is evident in people’s willingness to learn and adapt to new challenges in changing social environments. Relatedness refers to the need for belonging and to be connected to others as opposed to feeling excluded and lonely (in the case of related frustration).

Although the three needs for autonomy, competence and relatedness are distinctive, they are also complementary and need to function as a unit to ensure optimal development (Deci and Ryan 2000). Therefore, studies increasingly consider a composite psychological need satisfaction score to determine an overall level of psychological need satisfaction (Sebire et al. 2009; Thøgersen-Ntoumani et al. 2011). When all three psychological needs are satisfied, better physical and psychological well-being are experienced (Chen et al. 2015a; Ryan et al. 2008). Conversely, psychological need frustration is related to several negative consequences, such as depression, stress, burn-out, eating disturbances, self-control failure, aggressive behaviour and increased protective and wrongful behaviour (Chen et al. 2015b).

The positive relationship between psychological need satisfaction, and physical and psychological well-being has been well-established and documented across various domains (Chen et al. 2015a; Deci and Ryan 2000). However, the influence of psychological need satisfaction on specifically financial well-being has not yet been examined. Furthermore, since financial well-being is seen as a subset of subjective well-being (Chatterjee et al. 2019), it is expected that a similar positive relationship should exist between psychological need satisfaction and financial well-being. It is therefore hypothesised that:

H1a

There is a positive relationship between psychological need satisfaction and financial well-being.

Aligned with the principles of the self-determination theory, psychological need frustration is associated with lower levels of well-being and, in some cases, even ill-being (Chen et al. 2015b). When faced with psychological need frustration people can engage in irresponsible spending and poor financial decision-making behaviour which could have detrimental effects on financial well-being (Barbić et al. 2019). It is, therefore, hypothesised that:

H1b

There is a negative relationship between psychological need frustration and financial well-being.

Psychological needs and consumer spending self-control

As per the self-determination theory, psychological needs are related to social and personal development (Ahmad et al. 2013), and therefore people adapt their behaviours to social contexts to support these psychological needs (Centre for Self-Determination Theory 2022). Also related to the ability to adapt behaviour is consumer spending self-control (CSSC) which, by definition, is the ability to observe and monitor spending-related behaviour (Haws et al. 2012). Psychological need satisfaction is thus related to positive outcomes, whereas psychological need frustration is related to negative outcomes, which can be an adoption or breakdown in self-control (De Ridder et al. 2012). Hereby, there should be a relationship between psychological need satisfaction and CSSC as well as psychological need frustration and CSSC. It is, therefore, hypothesised that:

H2a

There is a positive relationship between psychological need satisfaction and CSSC.

H2b

There is a negative relationship between psychological need frustration and CSSC.

Consumer spending self-control and financial well-being

The degree to which people exercise self-control influences the extent to which they control their financial behaviours and, consequently, financial well-being (Kim 2022; Miotto and Parente 2015). Practising greater self-control leads to less spending, less engagement in impulsive spending and a higher tendency to save—all important factors contributing to greater financial well-being (Baumeister 2002; Norvilitis and MacLean 2010). Conversely, individuals exhibiting lower self-control encounter challenges to adequately manage their finances which increase their risk of becoming indebted, and as a result they experience lower levels of financial well-being (Miotto and Parente 2015). Furthermore, the ability to control spending through CSSC can be a vital part to ensure stable consumption and financial behaviour (Barbić et al. 2019; Haws et al. 2012; Ponchio et al. 2019), and therefore the following hypothesis was set:

H3

There is a positive relationship between CSSC and financial well-being.

Psychological needs, consumer spending self-control and financial well-being

The self-determination theory states that consumers will differ with regard to the interpretation of their actions originating from the self (that is, autonomous actions) or actions controlled by external events (Deci and Ryan 1985). Such actions, according to the causality orientations mini-theory, serve to regulate behaviour as generalised traits (Hagger and Hamilton 2021) and also integrate impulses, needs, emotions and motives to ensure optimal development and functioning for one’s well-being (Ryan et al. 2021). CSSC is an example of such an autonomous regulatory trait system, specifically because CSSC refers to how people regulate their spending thoughts and behaviour (Haws et al. 2012).

In addition, psychological need satisfaction is associated with adaptive and cautious decision-making behaviour (Davids 2022) such as CSSC. Conversely, psychological need frustration is associated with self-control failure and may thus be negatively associated with CSSC (Vansteenkiste and Ryan 2013). In turn, controlling one’s spending further contributes to stable consumption and financial behaviour, enabling people to plan and manage their finances better, thereby increasing their financial well-being (Barbić et al. 2019; Haws et al. 2012; Miotto and Parente 2015). Thus, it is expected that CSSC acts as an intervening variable between psychological need satisfaction and financial well-being and between psychological need frustration and financial well-being. It is, therefore, hypothesised that:

H4a

CSSC mediates the relationship between psychological need satisfaction and financial well-being.

H4b

CSSC mediates the relationship between psychological need frustration and financial well-being.

Research methodology

Sampling, measurement and data collection

This is a descriptive, cross-sectional study that collected data using an online self-administered questionnaire through an online paid-for consumer panel. Convenience sampling was used to collect data from South Africans who were credit active, 18 years or older and permanently employed or self-employed. Credit-active consumers are those individuals obliged to pay credit and/or service providers for products and/or services delivered (National Credit Regulator 2019). The questionnaire was pretested among a sample of 100 respondents.

To measure the constructs of the study, the questionnaire included the Basic Psychological Need Satisfaction and Frustration Scale (BPNSFS) with 12 items each, to determine to what extent psychological needs are satisfied or frustrated (Chen et al. 2015a). A 7-point Likert-type scale was used (1 = ‘not at all true’, 7 = ‘completely true’). Separate composite scores for psychological need satisfaction and psychological need frustration were calculated. CSSC was measured using the 10-item CSSC scale by Haws et al. (2012) to determine people’s ability to control their spending behaviour. The 10-item Financial Well-Being Scale (Consumer Financial Protection Bureau 2019) was used to determine respondents’ level of financial well-being. Both aforementioned scales used a 7-point Likert-type scale (1 = ‘strongly disagree’, 7 = ‘strongly agree’).

Data analysis

Descriptive statistics were calculated using SPSS Statistics version 28. To consider common method bias, three separate analyses were performed which showed a shared variance of 22% among the constructs. The afore-mentioned analyses included the Harman’s single-factor test, an assessment of the common variance among all variables in the model and the inclusion of a marker variable unrelated to the constructs in the model, namely relative deprivation (i.e. the negative feelings of resentment and frustration experienced in response to the belief that one is missing out on a desired and earned end result compared to others in society) (Walker and Smith 2002). Mplus version 8.3 was used to conduct co-variance-based structural equation modelling (CB-SEM) of the relationships identified for the study. The MLM estimator, with standard errors and mean-adjusted Chi-square (χ2) test statistic (also referred to as the Satorra–Bentler χ2 test), a more robust estimator to use when data are not normally distributed, was used (Muthén and Muthén 1998–2017). To test for mediation effects, Hayes’ Process Macro for SPSS version 3.5 (Model 4) was used (Hayes 2018).

Findings

Sample profile

The final realised sample included 608 respondents with slightly more male (52.6%) than female respondents (47.4%). The average age of respondents was 36 years, and the age bracket ranged from 18 to 85 years. Credit cards (64.6%) were the more popular credit products used by respondents, followed by personal loans (50.5%) and retail accounts (49.5%). Other credit products listed by respondents included cell phone contracts, as well as insurance and educational loans. A personal loan was the credit product most likely to be in arrears (19.6%), followed by retail accounts (15.3%) and credit cards (13.0%).

Linear hypothesised relationships

Assessment of the measurement model

The initial measurement model was respecified to address items not performing well in terms of model integrity, model fit or construct validity (Hair et al. 2010). Since the AVE for some constructs was below the required 0.5 threshold, items with factor loadings below 0.6 were removed (Field 2013; Hair et al. 2010), which included eight psychological need satisfaction, four psychological need frustration and six financial well-being items. The final re-estimated measurement model fit the data well, with all fit indices adhering to the recommended cut-off points. Table 1 summarises the validities and reliabilities for the final re-estimated measurement model.

Table 1 shows that all items had standardised estimates greater than 0.6 and were statistically significant (p < 0.05) (Hair et al. 2010). The AVE scores for psychological need satisfaction (AVE = 0.647), CSSC (AVE = 0.565) and financial well-being (AVE = 0.572) all measured greater than 0.5. Even though psychological need frustration had an AVE score below the threshold of 0.5 (AVE = 0.460), the construct’s composite reliability score was above 0.6, thus making it possible to retain for further analysis (Fornell and Larcker 1981). Reliability was confirmed with all Cronbach’s alpha and composite reliability scores greater than 0.7 (Hair et al. 2010). In terms of discriminant validity, results showed that the AVE’s square root for each construct exceeded the correlation of each construct pair (Fornell and Larcker 1981).

Assessment of the structural model

The next step was to assess the structural model and specified structural paths for model fit against several indices—of which all showed adequate fit. The Satorra–Bentler χ2/df ratio was 2.29 (670.58/294) which was below the recommended cut-off value of 3 (Hair et al. 2010). The Root-Mean-Square Residual (RMSEA) was 0.046 and well below the 0.08 cut-off (MacCallum et al. 1996). Next, both the Comparative Fit Index (CFI) and Tucker–Lewis Index (TLI) values were above the 0.9 cut-off value, namely 0.94 and 0.93, respectively (Hu and Bentler 1999). Finally, the Standardized Root-Mean-Squared Residual (SRMR) was 0.049, also below the recommended cut-off of 0.08 (Hu and Bentler 1999). Consequently, the structural paths (standardised estimates) could be further investigated for significance. Results are summarised in Table 2.

Table 2 shows a significant positive relationship between psychological need satisfaction and financial well-being (estimate = 0.157; p = 0.001), and a significant positive relationship between psychological need satisfaction and CSSC (estimate = 0.264; p < 0.001). H1a and H2a were, therefore, supported. Further, the negative relationship between psychological need frustration and financial well-being (estimate = -0.070; p = 0.062) was not significant, thereby not supporting H1b. Similarly, there was not support for H2b in that the negative relationship between psychological need frustration and CSSC (estimate = − 0.057; p = 0.239) was not significant. There was, however, support for H3 indicating a positive, significant relationship between CSSC and financial well-being (estimate = 0.562; p < 0.001).

Mediation hypothesised relationship

Table 3 outlines the bootstrapping results of the direct and indirect effects of the mediation analyses calculated at an OLS 95% interval. This study considered the mediation component effect between two variables in the mediation model commonly done during regression analysis to provide more depth to the interpretation of the results. Hereby, the standardized β estimate represents the change in financial well-being for every 1 standard deviation change in the mediator. Specifically, Cohen’s (1988) guidelines on coefficient β effect sizes include values between 0.10 and 0.29 as small, between 0.30 and 0.49 as medium and greater than 0.50 as large.

Table 3 (H4a) shows that CSSC had a mediating effect on the relationship between psychological need satisfaction and financial well-being (LLCI = 0.101; ULCI = 0.224). The direct effect was also significant (LLCI = 0.114; ULCI = 0.280) indicating partial complementary mediation. In other words, a part of the relationship between psychological need satisfaction and financial well-being was explained by CSSC, with CSSC becoming one mechanism through which psychological need satisfaction is associated with financial well-being. H4a was, therefore, supported.

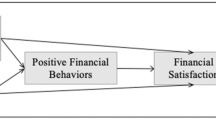

The indirect effect (LLCI = − 0.147; ULCI = -0.044) and the direct effect (LLCI = − 0.217; ULCI = − 0.059) for H4b were significant. Hereby, findings show that CSSC had a partial mediating effect on the relationship between psychological need frustration and financial well-being, supporting H4b. However, the mediation effect is very small (− 0.094) and therefore not practically significant (Nieminen 2022) which signals that the finding should be interpreted with caution. The standardised estimate results are outlined in Fig. 1.

Standardised estimate results of the conceptual framework

Discussion and implications

This study investigated the relationships between psychological need satisfaction/frustration, CSSC and financial well-being. Besides contributing to the body of knowledge on CSSC, the study also added knowledge on the impact of psychological needs on financial well-being. In addition, this study is a first attempt at validating the CSSC scale in a South African context. The overall study has several academic implications, and findings suggest that scholars in psychology and finance should collaborate to develop integrated frameworks that consider both psychological needs and economic factors in understanding financial well-being. Likewise, scholars in education and finance can collaborate to develop and assess the effectiveness of financial education interventions that address the enhancement of spending self-control as a pathway to improving financial well-being.

Hypotheses 1a and 2a indicated that psychological need satisfaction has a positive relationship with both CSSC and financial well-being. This implies that when individuals feel their psychological needs are met, their probability to exercise self-control over their spending impulses may increase, with the expectation that they will also be more likely to make informed financial decisions. This supports findings from a study by Park and Martin (2022) which indicated that psychological factors are related to financial behaviour. Understanding the psychological tendencies that influence customers' financial behaviours opens up several managerial solutions for financial institutions. First, financial providers can develop customised financial plans, investment portfolios or budgeting tools that align with customers' psychological needs and financial goals (Lin et al. 2021). This can be done by leveraging customer data and utilising customer segmentation techniques to design interventions that address consumers' psychological needs alongside financial education. This dual approach may lead to more comprehensive solutions, positively impacting clients' overall financial health. Second, marketers can refine their communication strategies to resonate with consumers at a deeper psychological level offering, for example, personalised services, loyalty programmes and targeted engagement initiatives. Hypotheses 1b and 2b were not supported, suggesting that there may be different factors at play than psychological need frustration, including moderating or mediating factors that affect CSSC and financial well-being.

Hypothesis 3 provided empirical evidence that higher levels of CSSC are associated with greater financial well-being, adding to previous studies investigating the relationship between general self-control and well-being and general self-control and financial well-being (Baumeister 2002; Norvilitis and MacLean 2010). In this regard, financial institutions can develop targeted financial education programmes (i.e. workshops or online resources) to strengthen consumers' self-control mechanisms. Next, financial service providers can consider developing personal financial control tools for individuals to help them set their financial goals and track their spending which can also involve offering incentives or rewards that align with the financial objectives of customers (Kim 2022; Lin et al. 2021). Here personalised communication based on spending patterns (by providing real-time financial insights or approaches to incentivise sensible financial habits) can help to guide consumers toward better financial decisions. Finally, financial institutions can refine their credit risk assessment models by incorporating indicators of self-control which may lead to more accurate risk profiling and better-informed lending decisions.

The overall objective of this study was to explore the role of consumer spending self-control in the relationship between psychological needs and financial well-being. The results showed that CSSC was a complementary mechanism through which a part of the relationship between psychological needs and financial well-being can be explained.

Firstly, when individuals experience psychological need satisfaction, their ability to control their spending serves as a mechanism that strengthens the positive impact of psychological need satisfaction on financial well-being (H4a). This highlights the importance of developing and promoting CSSC as a strategy for financial well-being. In this regard, financial service providers can offer financial education seminars or offer products/services that contribute to financial well-being (e.g. an investment opportunity that renders favourable returns over 10 years). Supporting programmes could include elements of financial literacy, budget management, impulse control and/or long-term goal setting (Kim 2022; Sabri et al. 2023). In addition, marketing communication messages can highlight the importance of having control over spending now to reap the benefits later (e.g. pay more than the required amount on credit-card debt to become debt-free sooner). Finally, financial institutions can use data analytics to identify patterns and offer timely interventions, such as alerts related to spending patterns.

Secondly, Hypothesis 4b indicated that when individuals experience psychological need frustration, it can indirectly impact financial well-being by diminishing CSSC. Lack of self-control can lead to impulsive or irresponsible financial decisions, excessive spending and a lack of savings, leading to poorer financial well-being (Kim 2022). Even though the finding showed low practical significance, it remains important to lower psychological need frustration. As a start, financial institutions should ensure that they have mechanisms such as customer surveys or feedback opportunities for addressing customer frustration related to psychological needs. Here, timely interventions, such as targeted support or educational materials, can mitigate the negative effects on spending self-control.

Limitations and future research opportunities

While this cross-sectional study offered valuable insights, there is limited ability to generalise the findings to broader populations, an inability to offer insight into how variables change over time, and the findings are observational. Therefore, longitudinal studies that track consumer spending across multiple time points should be considered in future.

Due to the cross-sectional, personal and sensitive nature of psychological need frustration, CSSC and financial well-being, respondents might provide answers which would portray them in a good light (Tangney et al. 2004), although common method bias results were below the 50% threshold. Yet, this 50% threshold is considered fragile, especially in situations where there are many indicators of latent constructs as is the case in this study. Future studies could consider employing alternative common method bias methods such as bifactor models to detect and control for common method bias (Podsakoff and Organ 1986).

One has to acknowledge the potential weakness of the measure of the latent ‘psychological need frustration’ construct due to its low AVE value, which in future research may necessitate scale revision in contexts different from where it was developed. Future research could also incorporate objective measures when gauging financial well-being, such as income, debt-to-income ratio, credit limits, savings and debt levels (Abrantes-Braga and Veludo-de-Oliveira 2019).

Another possible limitation is the lack of control for age and gender in the structural equation model. Future models could consider controlling for these variables since unaccounted biases of covariates may lead to spurious relationships between variables. Lastly, the partial mediating effect of CSSC between psychological needs and financial well-being suggests that future research can consider other contributing factors, such as income, financial literacy, social support or lifespan. For example, key life events such as marriage, parenthood or retirement can influence spending patterns and financial well-being and be worthwhile future research avenues.

References

Abrantes-Braga, F.D.M.A., and T. Veludo-de-Oliveira. 2019. Development and validation of financial well-being related scales. International Journal of Bank Marketing 37 (4): 1025–1040.

Ahmad, I., M. Vansteenkiste, and B. Soenens. 2013. The relations of Arab Jordanian adolescents’ perceived maternal parenting to teacher-rated adjustment and problems: The intervening role of perceived need satisfaction. Developmental Psychology 49: 177–183.

Barbić, D., A. Lučić, and J.M. Chen. 2019. Measuring responsible financial consumption behaviour. International Journal of Consumer Studies 43: 102–112.

Baumeister, R.F. 2002. Yielding to temptation: Self-control failure, impulsive purchasing and consumer behaviour. Journal of Consumer Research 28: 670–676.

Brüggen, E.C., J. Hogreve, M. Holmlund, S. Kabadayi, and M. Löfgren. 2017. Financial well-being: A conceptualization and research agenda. Journal of Business Research 79: 228–237.

Consumer Financial Protection Bureau. 2019. Find out your financial well-being. [Online] Available from: https://www.consumerfinance.gov/consumer-tools/financial-well-being/. Accessed 18 Dec 2022.

Centre for Self-Determination Theory. 2022. The theory, https://selfdeterminationtheory.org/the-theory/. Accessed 15 Oct 2022.

Chatterjee, D., M. Kumar, and K.K. Dayma. 2019. Income security, social comparisons and materialism: Determinants of subjective financial well-being among Indian adults. International Journal of Bank Marketing 37 (4): 1041–1061.

Chen, B., J. Van Assche, M. Vansteenkiste, B. Soenens, and W. Beyers. 2015a. Does psychological need satisfaction matter when environmental or financial safety are at risk? Journal of Happiness Studies 16: 745–766.

Chen, B., M. Vansteenkiste, W. Beyers, L. Boone, E.L. Deci, J. Van der Kaap-Deeder, B. Duriez, W. Lens, L. Matos, A. Mouratidis, R.M. Ryan, K.M. Sheldon, B. Soenens, S. Van Petegem, and J. Verstuyf. 2015b. Basic psychological need satisfaction, need frustration, and need strength across four cultures. Motivation and Emotion 39: 216–236.

Cohen, J. 1988. Statistical power analysis for the behavioral sciences, 2nd ed. Hillsdale, MI, USA: Erlbaum.

Davids, E.L. 2022. The interaction between basic psychological needs, decision-making and life goals among emerging adults in South Africa. Social Sciences 11 (7): 316.

De Ridder, D.T.D., G. Lensvelt-Mulders, C. Finkenauer, F.M. Stok, and R.F. Baumeister. 2012. Taking stock of self-control. A meta-analysis of how trait self-control relates to a wide range of behaviors. Personality and Social Psychology Review 16 (1): 76–99.

Deci, E.L., and R.M. Ryan. 1985. The general causality orientations scale: Self-determination in personality. Journal of Research in Personality 19: 109–134.

Deci, E.L., and R.M. Ryan. 2000. The “what” and “why” of goal pursuits: Human needs and the self-determination of behaviour. Psychological Inquiry 11 (4): 227–268.

Dickason-Koekemoer, Z., and S. Ferreira. 2019. A conceptual model of financial well-being for South African investors. Cogent Business and Management 6 (1): 1676612.

Dittmar, H. 2005. A new look at “compulsive buying”: Self-discrepancies and materialistic values as predictors of compulsive buying tendency. Journal of Social and Clinical Psychology 24: 832–859.

Field, A. 2013. Discovering statistics using IBM SPSS statistics, 4th ed. Los Angeles, CA: Sage.

Fornell, C., and D.F. Larcker. 1981. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 18 (1): 39–50.

Gerth, F., V. Ramiah, E. Toufaily, and G. Muschert. 2021. Assessing the effectiveness of Covid-19 financial product innovations in supporting financially distressed firms and households in the UAE. Journal of Financial Services Marketing 26: 215–225.

Guzman, F., A. Paswan, and N. Tripathy. 2019. Consumer centric antecedents to personal financial planning. Journal of Consumer Marketing 36 (6): 858–868.

Hagger, M.S., and K. Hamilton. 2021. General causality orientations in self-determination theory: Meta-analysis and test of a process model. European Journal of Personality 35 (5): 710–735.

Hair, J.F., W.C. Black, B.J. Babin, and R.E. Anderson. 2010. Multivariate data analysis, 7th ed. Upper Saddle River, NJ: Pearson Prentice Hall.

Haws, K.L., W.O. Bearden, and G.Y. Nenkov. 2012. Consumer spending self-control effectiveness and outcome elaboration prompts. Journal of the Academy of Marketing Science 40: 695–710.

Hayes, A.F. 2018. Introduction to mediation, moderation and conditional process analysis: A regression-based approach, 2nd ed. New York, NY: The Guilford Press.

Hu, L., and P.M. Bentler. 1999. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal 6 (1): 1–55.

Kim, M. 2022. Two sides of the same coin: The simultaneous effects of spending and saving needs on budget estimation. Journal of Financial Services Marketing 27: 360–371.

Leandro, J.C., and D. Botelho. 2022. Consumer over-indebtedness: A review and future research agenda. Journal of Business Research 145: 535–551.

Lin, A.J., H.Y. Chang, S.W. Huang, and G.H. Tzeng. 2021. Criteria affecting Taiwan wealth management banks in serving high-net-worth individuals during COVID-19: A DEMATEL approach. Journal of Financial Services Marketing 26: 274–294.

Losado-Otalaro, M., and L. Alkire. 2019. Investigating the transformative impact of bank transparency on consumers’ financial well-being. International Journal of Bank Marketing 37 (4): 1062–1079.

Lusardi, A., and O.S. Mitchell. 2014. The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature 52 (1): 5–44.

MacCallum, R.C., M.W. Browne, and H.M. Sugawara. 1996. Power analysis and determination of sample size for covariance structure modelling. Psychological Methods 1 (2): 30–49.

Miotto, A.P.S.C., and J. Parente. 2015. Antecedents and consequences of household financial management in Brazilian lower-middle-class. Revista De Administração De Empresas 55 (1): 50–64.

Muthén, L.K. and Muthén, B.O. 1998–2017. Mplus user’s guide. Los Angeles, CA: Muthén and Muthén.

National Credit Regulator. 2019. Credit bureau monitor: third quarter—September 2019. [Online] Available from: https://www.ncr.org.za/documents/CBM/CBM%20Q3%202019.pdf. Accessed 19 Jan 2022.

Nieminen, P. 2022. Application of standardized regression coefficient in meta-analysis. BioMedInformatics 2 (3): 434–458.

Norvilitis, J.M., and M.G. MacLean. 2010. The role of parents in college students’ financial behaviours and attitudes. Journal of Economic Psychology 31: 55–63.

Park, H., and W. Martin. 2022. Effects of risk tolerance, financial literacy, and financial status on retirement planning. Journal of Financial Services Marketing 27: 167–176.

Podsakoff, P.M., and D.W. Organ. 1986. Self-reports in organizational research: Problems and prospects. Journal of Management 12 (4): 531–544.

Ponchio, M.C., R.A. Cordeiro, and V.N. Gonçalves. 2019. Personal factors as antecedents of perceived financial well-being: Evidence from Brazil. International Journal of Bank Marketing 37 (4): 1004–1024.

Rice, A., Y.L. Garrison, and W.M. Liu. 2020. Spending as social and affective coping (SSAC): Measure development and initial validation. The Counseling Psychologist 48 (1): 78–105.

Ryan, R.M., and E.L. Deci. 2000. Self-determination theory and the facilitation of intrinsic motivation, social development and well-being. American Psychologist 55 (1): 68–78.

Ryan, R.M., Patrick, H., Deci, E.L. and G.C. Williams. 2008. Facilitating health behaviour change and its maintenance: interventions based on self-determination theory. The European Health Psychologist 10: 2–5.

Ryan, R.M., E.L. Deci, M. Vansteenkiste, and B. Soenens. 2021. Building a science of motivated persons: Self-determination theory’s empirical approach to human experience and the regulation of behaviour. Motivation Science 7 (2): 97–110.

Sabri, M.F., M. Anthony, and S.H. Law. 2023. Impact of financial behaviour on financial well-being: evidence among young adults in Malaysia. Journal of Financial Services Marketing. https://doi.org/10.1057/s41264-023-00234-8.

Sebire, S.J., M. Standage, and M. Vansteenkiste. 2009. Examining intrinsic versus extrinsic exercise goals: Cognitive, affective, and behavioral outcomes. Journal of Sport and Exercise Psychology 31: 189–210.

Tangney, J.P., R.F. Baumeister, and A.L. Boone. 2004. High self-control predicts good adjustment, less pathology, better grades and interpersonal success. Journal of Personality 72 (2): 271–324.

Thøgersen-Ntoumani, C., N. Ntoumanis, J. Cumming, and N.L.D. Chatzisarantis. 2011. When feeling attractive matters too much to women: A process underpinning the relation between psychological need satisfaction and unhealthy weight control behaviors. Motivation and Emotion 35 (4): 413–422.

Vansteenkiste, M., and R.M. Ryan. 2013. On psychological growth and vulnerability: Basic psychological need satisfaction and need frustration as a unifying principle. Journal of Psychotherapy Integration 3: 263–280.

Walker, I., and H.J. Smith. 2002. Fifty years of relative deprivation: Development and integration. Cambridge, UK: Cambridge University Press.

Funding

Open access funding provided by University of Pretoria. The study was funded by Banking Sector Education and Training Authority, 475.4710.675000, Laureane du Plessis.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

du Plessis, L., Jordaan, Y. & van der Westhuizen, LM. Psychological needs and financial well-being: the role of consumer spending self-control. J Financ Serv Mark (2024). https://doi.org/10.1057/s41264-024-00270-y

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41264-024-00270-y