Abstract

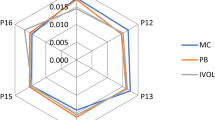

In Chapter 4 we compare three kinds of asset-pricing models, as proposed by Fama and French, Carhart, and Pastor and Stambaugh. The results of the Fama and MacBeth regressions and the GMM test suggest that all candidate risk factors are associated with Tokyo Stock Exchange long-run stock returns.

As to sub-periods we find the Fama and French model can well explain the cross-sectional variations of Japanese stocks, especially in the 1980s. However, after the arrowhead launch the HML factor was no longer significant, while Pastor and Stambaugh’s liquidity innovation factor became significant.

The result suggests the possibility that the launch of the arrowhead trading system at the TSE in January 2010 drastically changed the asset pricing structure, liquidity, and information asymmetry of the stocks listed on the Tokyo Stock Exchange.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

Unable to display preview. Download preview PDF.

Similar content being viewed by others

References

Berk, J and DeMarzo, P. (2011), Corporate Finance ( second edition ). New York: Pearson Education Inc.

Carhart, M. (1997), “On persistence in mutual fund performance,” Journal of Finance, 52 (1), 57–82.

Chou, P-U., Wei, K. C. J., and Chung, H. (2007), “Sources of contrarian profits in the Japanese stock market,” Journal of Empirical Finance, 14 (3), 261–286.

Cochrane, J. (2001), Asset Pricing. Princeton, NJ: Princeton University Press.

Constantinides, G. (1986), “Capital market equilibrium with transaction costs,” Journal of Political Economy, 94 (4), 842–862.

Fama, E. F. and French, K. R. (1993), “Common risk factors in the returns on stock and bonds,” Journal of Financial Economics, 33 (1), 3–56.

Fama, E. F. and French, K. R. (1998), “Value versus growth: the international evidence,” Journal of Finance, 53 (6), 1975–1999.

Fama, E. F. and MacBeth, J. D. (1973), “Risk, return, and equilibrium: empirical tests,” Journal of Political Economy, 81 (3), 607–636.

Gibbons, M., Ross, S., and Shanken, J. (1989), “A test of the effuciency of a given portfolio,” Econometrica, 55 (5), 1121–1152.

Hansen, L. P. and Jagannathan, R. (1997), “Assessing specification errors in stochastic discount factor models,” Journal of Finance, 52 (1), 557–590.

IIhara, Y., Kato H., and Tokunaga, T. (2004), “The winner–loser effect in Japanese stock returns,” Japan and the World Economy, 16 (4), 471–485.

Jagannathan, R., Kubota K., and Takehara, H. (1998), “Relationship between labor-income risk and average return: empirical evidence from the Japanese stock market,” Journal of Business, 71 (1), 319–347.

Jegadeesh, N. and Titman, S. (1993), “Returns to buying winners and selling losers: implications for stock market efficiency,” Journal of Finance, 48 (1), 65–91.

Kubota, K. and Takehara, H. (2003), “Financial sector risk and the stock returns: evidence from Tokyo Stock Exchange Firms,” Asia-Pacific Financial Markets, 10 (1), 1–28.

Kubota, K. and Takehara, H. (2010), “Expected return, liquidity risk, and contrarian strategy: evidence from the Tokyo Stock Exchange,” Managerial Finance, 36 (8), 655–679.

Pastor, L. and Stambaugh, R. (2003), “Liquidity risk and expected stock returns,” Journal of Political Economy, 111 (3), 642–685.

Author information

Authors and Affiliations

Copyright information

© 2015 Keiichi Kubota & Hitoshi Takehara

About this chapter

Cite this chapter

Kubota, K., Takehara, H. (2015). Risk and Return on the Tokyo Stock Exchange. In: Reform and Price Discovery at the Tokyo Stock Exchange: From 1990 to 2012. Palgrave Pivot, New York. https://doi.org/10.1057/9781137540393_4

Download citation

DOI: https://doi.org/10.1057/9781137540393_4

Publisher Name: Palgrave Pivot, New York

Print ISBN: 978-1-349-50700-9

Online ISBN: 978-1-137-54039-3

eBook Packages: Palgrave Economics & Finance CollectionEconomics and Finance (R0)