Abstract

Recent urban population explosion in developing countries demands for several policy considerations. Is India ready for it? In this perspective, we assess the impact of economic reforms on urbanization in India for the period of 1991–2016. It is found that economic reform variables (except import of goods and services as % of GDP) have a positive effect on urbanization. The vector error correction model shows that economic reforms have influenced only on total urban population with a very slower rate with the speed of adjustment of 0.003. The short-run effect is also negligible. Granger causality test shows that there is no causal relationship between them. Therefore, we conclude that economic reforms do not promote urbanization in India. Our results also support the Krugman and Elizondo (J Dev Econ 49:137–150, 1996) hypothesis about the relationship between trade policy and urban agglomerations. Finally, we suggest that we need to promote urbanization through encouraging export for higher and sustainable economic growth in India.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Developing countries such as India has been experiencing an urban population explosion in recent years through a transformation of the country’s economy from rural to urban which is characteristic of the current development process. Urbanization indeed is a phenomenon whose time has arrived, with more than 50% of India’s population soon going to live in urban areas. It is interesting to see how Indian economic policies have promoted urbanization over the years. However, urbanization is a multi-dimensional process, comprising structural change, generation of agglomeration economies emanating from clustering of economic activity, resulting in size-class distribution of cities. This multi-dimensional process when ably supported by policy environment interacts in more than one ways with the economy. On one hand, economic policies and reforms either enable/disable the process of urbanization, by making migration easier, by providing infrastructure in the cities, by making structural shift possible. On the other hand, urbanization also fuels in economic growth, by generating operational economies for businesses, by improving quality of lives of citizens and by providing huge sources of tax revenue to the Governments. Agglomeration economics has also effect on rural poverty (Partridge and Rickman 2008) and in the knowledge-intensive services (Marrocu et al. 2013).

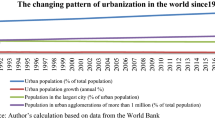

The nature and pattern of urbanization in India have changed significantly since 1991, i.e., the year when India started its economic reforms through trade liberalization, financial deregulation, making improvements in supervisory and regulatory systems and policies to make them more conducive to privatization and Foreign Direct Investment (FDI) (Gopinath 2008). Economic reforms have also had a positive effect on India’s FDI inflows, economic growth and trade volume. The average annual economic growth in India was about 4% in 1960–1990, but it increased to about 7% in 1991–2016. Also, the average Merchandise trade (% of GDP) increased from 9.97% in 1960–1990 to 26.57% in 1991–2016. Foreign direct investment and net inflows (% of GDP) increased from 0.03% in 1975–1990 to 1.23% in 1991–2016. On the other hand, India’s urban population increased from 217.18 million in 1991 to 377.10 million in 2011, constituting an increase of about 73.63%. The percentage of urban in total population saw an increase from 25.72 to 31.16% during the same time period. The number of towns and cities also increased from 4615 in 1991 to 7935 in 2011, accounting for an increase of over 72%. The above figures indicate that economic reforms and the consequent higher level of economic growth, higher trade performance and higher investment may have had direct links with the urbanization process in the country. It is evident that cities have played a significant role in driving higher economic growth in India (Tripathi 2013a; Tripathi and Mahey 2017). For instance, the contribution of urban as a % of total Net Domestic Product (NDP) increased from 37.65% in 1970–1971 to 53% in 2011–2012. Urban economic growth rate was also very high in this period, i.e., about 15% from 1970–1971 to 2004–2005 at current prices.

In this perspective, the present paper tries to understand the impact of economic reforms on urbanization in India. Among the important policy initiatives impacting the process of urbanization in India, it is important to mention that the 74th Constitutional Amendment (CAA), 1993, the most significant reform which for the first time ever in India identified urban local bodies (ULBs) as statutory bodies, and led to devolution of functional and fiscal powers to these ULBs. Another significant reform came up through Jawaharlal Nehru national urban renewal mission in 2005, which was the first initiative from the central government in a mission mode, realizing the importance of renewing the urban spaces in India.

Recently, urbanization in India has gained a significant fillip from the central government. Government policies, such as ‘Smart city mission’, Atal Mission for Rejuvenation and Urban Transformation (AMRUT), and North Eastern Region Urban Development Programme (NERUDP) try to incentivize India’s current urbanization. Whether policies promote urbanization or not, urbanization is indeed happening, and it certainly is an inevitable part of the country’s development process. Therefore, it is time to ask whether the reform which was started in 1991 has indeed promoted urbanization or we need a distinct reform initiative by focusing solely on urbanization in India. All available indicators show that Indian cities are poorly managed; they are haphazardly unplanned and crippled by exploding number of vehicles, higher energy consumption, air and noise pollution, street violence, traffic congestion traffic injuries, fatalities, etc. (Tripathi and Kaur 2017). It is worth noting here that cities have played a significant role in driving economic development and offering better living standards to populations across the developed world. Therefore, harnessing the development potential of urbanization for economic development is critical, and it raises questions of fundamental policy importance. How can cities be made more productive and efficient? How can the quality of city life be improved? All these questions are crucial in the current juncture, and proper empirical research is urgently needed for formulating appropriate policies. This paper aims to fill this research gap.

The impact of on urbanization in India is analyzed in this paper based on data for the period from 1991 to 2016. India initiated major reforms in 1991 and hence the choice of 1991 as the base year. Therefore, analysis by considering study period from 1991 to 2016 measures the “with reforms” impact on urbanization. However, an analysis “With and without reforms”, using data before and after 1991, would be a better reflector of impact of reforms on urbanization. Hence, as per the availability of data we consider study period from 1960 to 1990 to analyze the “without reforms” impact on urbanization.

Data for this paper are mainly from World Development Indicators from The World Bank.Footnote 1 In this paper, economic reforms are being captured through export of goods and services as % of GDP, import of goods and services as % of GDP, growth rate of GDP, GDP per capita and life expectancy at birth, and urbanization is measured by four proxy variables; urban population as % of total population, total urban population, population in urban agglomeration of more than 1 million, and population in the largest city to % of urban population. Vector error correction model is used to analyze the relationship.

The rest of the article is organized as follows: The next two sections present a brief review of literature and theoretical framework to find out the research gap and setting up the background for the empirical analysis. Empirical framework and results are presented in the subsequent two sections, respectively. Finally, major conclusions and implications are given in the last section.

2 Review of literature

2.1 Urbanization and economic growth

Various economic theories establish that structural change is an inevitable component of economic growth. In Lewis (1954) model, shifting of labor from primitive agriculture sector to manufacturing triggers growth by generating investible surplus, in the process of structural change giving birth to agglomeration economies, both internal and external.

The historical scholarship (Bairoch 1993; Hohenberg and Lees 1985; Hohenberg and Paul 2004) found a positive relationship among urbanization, spatial inequality, industrialization and economic development. More rigorous econometrics models have been used in Henderson (2003) and Brülhart and Sbergami (2009) to measure the impact of urbanization in economic growth and supported Williamson (1965) hypothesis suggesting that agglomerations matter mostly at early stages of development. Martin and Ottaviano (1999) model growth and geographic agglomeration as “mutually self-reinforcing processes”. They suggest that economic agglomeration in one region drives growth because it reduces the cost of innovation in that region through a pecuniary externality due to transaction costs. Growth fosters agglomeration because, as the sector at the origin of innovation expands, new firms tend to locate close to this sector. Fujita and Thisse (2002) found that “growth and agglomeration go hand-in-hand”. Baldwin and Martin (2004) stress the result that, given localized spillovers, “spatial agglomeration is conducive to growth”.

Such discussions suggest that urbanization is a part of development process. The relationship between urbanization and economic growth could be unidirectional/bidirectional and linear/nonlinear.

2.2 Economic reforms in India

Though several East Asian countries achieved higher economic growth through reforms earlier, India only started systematic reforms in 1991 due to wake of an extremely severe balance of payment crises (Ahluwalia 2002).Footnote 2 After 1991, Indian economic becomes more open and allows private sector with higher foreign investment. The reforms have brought many positive changes on Indian economy. Data from World Development Indicators show that the average growth rate from 1992–1993 to 2016–2017 was around 6.85% which puts India as one of the fastest growing countries in the world. Poverty headcount ratio at national poverty lines (% of population) also has fallen from 45.3% in 1993 to 21.9% in 2011. The combined central and state fiscal deficit reduced from 9.4% of GDP in 1990–1991 to 7% in both 1991–1992 and 1992–1993 and it was over by 1993.

Now we discuss about major changes under economic reforms in India. Changes in industrial and trade policies are the main ingredient of 1991s reforms in India. Industrial policies are restructured to welcome higher and new private investment and subsequently to use advance technologies. Industrial licensing by central government was almost abolished. Reforms are also made in trade policy. Import licensing was relaxed for capital goods and intermediates. India adopted flexible exchange rate regime. The weighted average import duty rate decreased from the very high level of 72.5% in 1991–1992 to 24.6% in 1996–1997. The policies also helped to import a wide range of items to export houses and trading houses by providing self-certification under advance license system. Permission was also given to trading houses with 51% foreign equity for the promotions of exports. Social sectors such as health and education also are affected in the post-reform period. The central government expenditure on social services and rural development increased from 7.6% of total expenditure in 1990–1991 to 10.2% in 2000–2001.

There is vast body of literature which measures the impact of economic reforms on economic growth in India. For example, Virmani (2004) argued that economic policy and policy reform over the last few decades have been motivated by the need to accelerate growth or equivalently to reverse a decline in growth rate. Nisa and Nisa (2008) illustrated that after the introduction of economic reforms in 1991, India has become one of the fastest growing economy of the world.

Now we assess the impact of economic reforms on export and import in India. Sahni (2014) found that India’s export performance improved significantly during the post-reform period and there has been a perceptible change in the value, composition and direction of India’s exports. Sharma and Dhiman (2014) mentioned after reforms India became the 19th largest merchandise exporter in the world, with a share of 1.7% of the global trade and the 12th largest importer with a share of 2.5% of global imports in 2012. Bhat (2011) found that the post-reform period in India has witnessed significant changes in the trend, pattern and structure of external trade. Pillania (2008) argued that Indian economy and foreign trade are on a growth trajectory. Economic reform in 1991 has increased trade growth and composition of trade has dominated by manufactured goods and services. However, India’s services exports share in global exports is more than double of that of Indian manufacturing exports. Maheswari (2017) supported that India’s foreign trade has significantly changed in the post-reform period. India’s total imports have increased by more than 14 folds during the last two decades, from Rs. 1094.73 crores in 1990–1991 to Rs. 15,555.05 crores in 2012–2013. The percentage growth of imports was increased from − 2.6% in 1991–1992 to 5.65% in 2012–2013. Singh’s (2014) study showed that though the total exports and imports both have improved, the growth rate of imports is higher in comparison to the growth rate of exports. Sahu (2017) examined the India’s foreign trade pre- and post-liberalization in India. The study found that the total trade after liberalization has been significantly higher than the total trade before liberalization and the imports were more than the exports in all the years. Similar results are also found in Kumar and Sood (2016) and Yadav (2018).

Turning now to measure the impact of reforms on health outcome in India, the average life expectancy at birth in India was about 50 years from 1960 to 1990. But it has increased to 64 years from 1991 to 2018. This is due to the increase in health expenditure in India. Ansari and Rehmani (2016) found that after post-reforms, there has been a remarkable improvement in the overall performance of the insurance sector in India, particularly in terms of insurance density and penetration. Dev and Mooij (2002), Prabhu (1994), Panchamukhi (2000) and Joshi (2006) also found that increasing trend in central government’s spending on India’s health sector.

The above review of literature clearly suggests that economic reforms did not distinguish between rural and urban India and also it did not promote urbanization in India. This stands as the major drawback as without urbanization one country cannot develop because resource may not be used more productively without urbanization. This paper tries to empirically measure this phenomenon and recommends that if the economic reforms did not promote urbanization; how we could promote it now as it is clear that we need urbanization desperately for higher economic growth. In fact, McKinsey Global Institute (2010) predicted that India could achieve double-digit growth if India pursues a new operating model for its cities.

2.3 India’s urbanization

Among the recent studies in India mostly, post-liberalization, Mathur (2005) argued that post-liberalization urban growth was driven by the substantial growth of the urban population and changes in the share of employment in the manufacturing and service sectors. Bhagat (2011) found that the declining trend in the urban population growth rate observed during 1980s and 1990s was reversed at the national level, and level of urbanization increased faster during 2001–2011. Cali (2009) found that the level of urbanization and that of economic development seem to go hand within Indian states over time. Chadchan and Shankar (2012) addressed the various complex urban issues associated with the present pattern of urban development through review of urban development of selected metropolitan cities of India. Abhishek et al. (2017) found that initial population and capital city status have a strong positive impact on city growth; proximity to cities causes nearby cities to be larger; these results are consistent throughout 3 years, i.e., 1991, 2001 and 2011. Choudhuri et al. (2017) showed that there is a fair amount of variation in the growth of towns across all categories of states in India. Tripathi (2017) suggested that improvement of infrastructure facilities may not significantly increase population agglomeration in the large cities in India.

In the context of linking urbanization and economic growth, Sridhar (2010) established the links between urbanization and economic growth in India. Tripathi (2013a) using data from various sources and using new economic geography model found that India’s agglomeration economies are policy induced as well as market determined, and offer evidence of the strong positive effect of agglomeration on urban economic growth in India’s urban system. Tripathi and Mahey (2017) investigated the relevant determinates of urbanization and its impact on economic growth for the Indian state of Punjab. The analysis established the positive link between urban agglomeration and economic growth at state level.

In the perspective of linking agricultural growth with urbanization, Tripathi and Rani (2018) show that overall agricultural activities have a negative effect on urbanization. Kalamkar (2009) showed that population growth has resulted in a downward trend in per capita availability of forest and agricultural land since the 1950s. Narayan (2016) investigates the causal relationship between economic growth and urbanisation in India, using World Development Indicators (WDI) data pertaining to the period 1960–2013. The estimated results for India indicate that economic growth has had a positive causal effect on urbanisation, while urbanisation, in turn, has not had any causal effect on economic growth.

Urbanization has also impacted on poverty, inequality and wellbeing of the city dwellers in India. Based on a wide range of variables basis of certain economic, social, demographic, health and education, Mitra (2014) computed the wellbeing index for each of the slum households in the sample of four cities. He found that large cities tend to improve the wellbeing of the population even among the low income households. Kundu (2006) found that as of 1999–2000, the per capita monthly consumption expenditure of million plus cities was Rs. 1070, about 53% higher than that of small towns. Tripathi (2013b) found that higher level of urban economic growth and large city population agglomerations reduces poverty and increases extent of inequality. Tripathi (2017) suggest that the upcoming “Smart cities” in India will emerge as a greater platform for future development of urban India, only if these cities ensure equitable distribution of the fruits of urban economic growth to the poorer section of urban dwellers. The Urban Poverty Report by the Government of India (2009) found that across the Indian states, poverty is negatively correlated with the level of urbanization. Other studies (World Bank 2010; Gangopadhyay et al. 2010) have also found that the poverty level in large cities is much lower than that in the small towns, though their method of analysis was different from earlier researchers. Gibson et al. (2017) found that growth of secondary towns may do more to reduce rural poverty than big city growth, although cities may eventually take over towns as the drivers of rural poverty reduction.

The above review of literature suggests that quantitative research work on urbanization of India by considering cross section data is very rich. However, time series data analysis on urban issues is very much deficient. Most importantly, economic reforms have taken a significant place in economic research in India as one of the main landmarks of development policies. Therefore, linking urbanization with economic reforms stands as one of the important research agendas to promote urbanization for higher and sustainable economic growth in India. This issue forms the main goal of the present paper.

3 Theoretical framework

This part of discussion is mainly derived from Ades and Glaeser (1995).

Several urban theorist from Thünen (1826) to Krugman (1991) suggested that when transport cost is more expensive, activities will group together to save it. In other words, it says that urban concentration will be higher when transportation is more costly. Based on this idea, Krugman and Elizondo (1996) constructed a theoretical model to build up the link between trade policy and urban development. In their model, international firms supply the main city and the hinterland equally well. However, domestic firms pay lower transport costs when serving their own location; domestic prices, net of travel, are lower where domestic firms are concentrated. With lower tariffs, cheaper imported goods are a large part of consumption. Imports are not cheaper in the central city so spread over space to save congestion costs. With protection, domestic suppliers cake over the market. Firms locate near to central city to lower prices and net transport costs for the domestic goods. Workers then migrate to the city to pay lower prices for domestic goods. This theory argues that protectionism generates larger central cities. Ades and Glaeser (1995) empirical exercise supported this theory and found that high tariffs, high costs of internal trade, and low levels of international trade increase the degree of concentration. But free trade does not always decrease urban concentration, e.g., London and Buenos Aires. Nitsch (2006), using a panel data set of more than 110 countries for the period from 1970 through 2000, found that previous results of a negative association between trade openness and the size of a country’s largest city are not robust and it disappears completely once reverse causality and the endogeneity of trade are accounted for. In this paper, we try to assess the impact of economic reforms which significantly liberalized trade on urban concentration in India based on main theoretical work by Krugman and Elizondo (1996).

4 Data and methodology

It is difficult to appreciate multi-dimensional urbanization process, and even more difficult is to study the drivers/enablers of the process, by gathering appropriate data and finding suitable methodology to reach significant, justifiable findings. However, based on the availability of data, we use time series analysis to analyze the impact of economic reforms on urbanization. Data for dependent and independent variables are collected from the World Development Indicators for the period from 1991 to 2016. EViews10 software has been used to calculate the results. Based on urban and development literature, we consider the following variables and functional form to assess the relationship.

whereas urbanization is measured by considering the following four variables, i.e., urban population as % of total population (UPP), total urban population (UP), population in urban agglomeration of more than 1 million (PUA), and population in largest city to % of urban population (PLC), economic reforms are being captured through export of goods & services as % of GDP (EGS), import of goods and services as % of GDP (IGS), growth rate of GDP (GDPG), GDP per capita (GDPPC) and life expectancy at birth (LEB). Table 1 presents the definition of variables and transformation of variables for the analysis.

4.1 Choice of variables for regression analysis

What follows is a discussion about the choice of dependent and independent variables. As Virmani (2004) and Nisa and Nisa (2008) found that after reforms economic growth in India has improved significantly; we consider GDP growth rate and GDP per capita to measure the economic reforms in India.

A vast body of literature, e.g., Sahni (2014), Sharma and Dhiman (2014), Bhat (2011), Pillania (2008), Maheswari (2017), Singh (2014), Sahu (2017), Kumar and Sood (2016) and Yadav (2018) found that economic reforms have increased trade volume by rising both exports and imports. Therefore, export of goods and services (% of GDP) and import of goods and services (% of GDP) are considered to capture the economic reforms in India. These indicators are also used to measure the trade openness by Sarkar and Bhattacharyya (2005) to assess the impact of trade liberalization on economic growth for India and Korea.

Economic reform has also increased health outcome and well-being of the Indian citizen [Ansari and Rehmani (2016), Dev and Mooij (2002), Prabhu (1994), Panchamukhi (2000), Joshi (2006) and Ahluwalia (2002)]. Therefore, life expectancy at birth is used as an Outcome of economic reforms in India.

As and where available, this paper uses four proxy variables, i.e., urban population as % of total population, total urban population, population in urban agglomeration of more than 1 million, and population in largest city to % of urban population to measure urbanization in India. Selection of these indicators is mainly based on Henderson (2003), Brülhart and Sbergami (2009) and India’s urbanization context. Though India’s urban population increased from 78.94 million in 1961 to 377.10 million in 2011 but in percent terms, the increase remains very low at about 31.16 in 2011. The Indian percentage figure is lower than the developed countries like the United States of America (82.1%) and Japan (90.5%) in 2010. It is also lower than in other fast growing developing countries such as China (49.2%), Brazil (84.3), and Russian Federation (73.7%) in 2010 (Tripathi 2015). Therefore, it is very important to see how economic reforms have impacted not only total urbanization but also on percentage of urbanization in India. ‘Population in urban agglomeration of more than 1 million’ and ‘population in largest city to % of urban population’ also considered for the analysis as India’s urban population is mainly concentrated in and around class I (population more than 1 lakh) cities. The percentage share of urban population in class I cities increased from 51.42 in 1961 to 70% in 2011. Also, the number of Class I cities increased from 394 in 2001 to 468 in 2011. Also needs to be analyzed are the forward and backward linkages between reforms and population change in the large cities. Krugman and Elizondo (1996) explains the existence of large giant cities as a consequence of the strong forward and backward linkages that come up when manufacturing tries to serve a small domestic market. Large cities are an unintended byproduct of import-substitution policies and trade liberalization has a negative effect on the population size of the cities. This indicates that population size of large cities has a link with trade policy. This issue has been analyzed in this paper.

4.2 Unit root or stationary tests

To test the causality and co-integration between the economic reforms and urbanization, at first, the stationary properties of the time series were checked by unit root test. Several tests are available for this test, such as Dickey Fuller test, augmented dickey fuller (ADF) test, Phillips—Perron (PP), and KPSS test. In this context, Arltová and Fedorová (2016) suggested that the most suitable tests for very short time series are the ADF and PP tests. However, the ADF test is one of the most commonly used unit root tests since its crucial advantage remains in its simple construction and feasibility. Therefore, this paper uses augmented dickey fuller (ADF) test which is based on the following regression equation with a constant and a trend in the form as follows:

where Δ is the first difference operator and \(u_{t}\) is the stochastic error term and k is the number of lags in the dependent variable, the null hypothesis (\(H_{0}\)) of a unit root indicates that the coefficient of \(Y_{t - 1}\) is zero while alternative hypothesis (\(H_{1}\)) implies \(Y_{t}\) is stationary. If the null hypothesis is rejected, then the series is stationary and no differencing in the series is essential to establish stationarity.

4.3 Testing for co-integration

The second step to examine the causality and co-integration involves searching for common stochastic trend between the concerned variables. For empirical examination, Johansen–Juselius co-integration technique is used in this study. In this technique, two test statistics known as the trace statistic and the maximum eigen value are used to identify the number of co-integrating vectors. Those statistics help us to verify if the resultant dynamic system is stable or not. The trace test statistics for the null hypothesis indicate that there are at most r distinct co-integrating vector.

where λI are the N-r smallest squared canonical correlations between Xt-k and ΔXt (where Xt = (upp/up/pua/plc, egs, igs, gdpg, gdppc, leb) and where all variables in Xt are assumed I(1)), corrected for the effects of the lagged differences of the Xt process.

The maximum eigenvalue statistic for testing the null hypothesis of at most r co-integrating vectors against the alternative hypothesis of r +1 co-integrating vectors is given by

Johansen (1988) shows that Eqs. (1) and (2) have non-standard distributions under the null hypothesis and provide approximate critical values for the statistic.

4.4 Vector error correction model

The co-integration among variables solely shows a long-run equilibrium relationship though there could be disequilibrium in the short run. To investigate the short-run dynamics among the concerned time series variables, vector error correction model (VECM) has been developed and used in this study.

The standard error correction model (ECM) considers the following form:

where \(\hat{\epsilon}_{t - 1} = \left({Y_{t - 1} - \hat{Y}_{t - 1}} \right)\) is one-period lagged value of the error from the co-integration regression and \(w_{t}\) is the error term in the ECM. When \(\hat{\epsilon}_{t - 1}\) is non-zero, there is disequilibrium in the short run. However, equilibrium will be restored in the long run if and only if \(\lambda < 0\).

5 Empirical results

Table 2 presents the descriptive statistics of the variables used for analysis. We consider study period from 1991 to 2016 as “with reforms” and study period from 1960 to 1990 as “without reforms” for the analysis as economic reforms started from 1991 onwards in India. Yearly time series data are used for the analysis. All the variables except GDPG in “without reforms” period are presented in the logarithmic form. As few years data in “without reforms” period of GDPG are negative, we consider it without taking the logarithmic form. Standard deviations (Std. Dev.) are very low for almost all the variables which indicate that the extent of variation or dispersion of data values is very minimal. The positive skewness values of UP, PLC, and GDPPC indicate that these variables are concentrated on the left of the figure in “Without reforms” period. The positive skewness values of UPP, PUA, PLC, and GDPPC indicate that in these variables the mass of the distribution is concentrated on the left of the figure in “with reforms” period. On the other hand, the negative skewness values of UP, EGS, IGS, GDPG, and LEB specify that the mass of the distribution is concentrated on the right of the figure of these variables in “with reforms” period. Jarque–Bera test shows that expect PLC in “with reforms” period and GDPG from the both the periods, data for all other variables follow the normal distribution.

To evaluate the long-run relationship between economic reforms and urbanization, the stationarity properties of the data are checked using the augmented dickey fuller (ADF) test. Table 3 shows that except the variables used to measure urbanization, all other variables (egs, igs, gdpg, gdppc, leb) are stationary in the first differenced series, i.e., I(1). When time series data are not stationary at their level form, they usually become stationary in the first difference. Among the urbanization variables, total urban population (up) is I(1) and other variables are I(2). As most of the variables follow I(1) process, the paper looks for the long-run relationship among the variables.

Table 4 reports the Johansen–Juselius co-integration result. Co-integration of the variables was tested by taking it in the non-stationary form. The results show that the null hypothesis of no co-integration, i.e., r = 0, is rejected for almost all variables used in the regression model. This is because either λtrace or λmax is larger than the critical value at least at 1% significant level. The results provide evidence that there is at least one co-integrating vector in each case. In some cases, there is even more than one vector. Johansen’s tests for co-integration results clearly state that the long-run relationship exists among considering variables. In other words, the results show that that there is a co-integration relationship among the economic agency variables (EGS, IGS, GDPG, GDPPC, LEB) and urbanization (UPP/UP/PUA/PLC) in India, that is, a long-term stable equilibrium relationship.

Table 5 presents the normalized co-integrating coefficients from the Johansen test for co-integrations. The results are presented by considering first lag as higher order lags are not considered due to data limitation. The signs of the normalized co-integrating coefficients are reversed to enable proper interpretation. First, we explain the results in “without reforms” periods. Results show that export of goods and services as % of GDP, GDP per capita, and life expectancy at birth all have positive and statistically significant effect (at 1% level) on urbanization as measured by urban population as % of total population. For instance, a 10% increase in GDP per capita increases urban population as % of total population by about 0.5%. In contrast, GDP growth rate has negative effect and import of goods and services as % of GDP has no effect on urban population as % of total population. GDP growth rates, life expectancy at birth and import of goods and services as % of GDP have positive effect on total urban population. While export of goods and services as % of GDP has positive effect, import of goods and services as % of GDP has no effect on total urban population in “without reform” India. In the same time, exports of goods and services as % of GDP, GDP per capita, and life expectancy at birth have positive effect on population in urban agglomerations of more than 1 million (% of total population). In contrast, GDP growth rate and import of goods and services as % of GDP have negative effect on population in urban agglomerations of more than 1 million (% of total population). Finally, except export of goods and services as % of GDP all other variables have negative effect on population in the largest city (% of urban population).

Now, we discuss the results for the “with reform periods”. The co-integrating equation results show that dependent variables are significantly influenced by the independent variables. Almost all the independent variables have a statistically significant (1% level) effect on urbanization. Export of goods and services as % of GDP has a positive effect on urbanization as measured by urban population as % of total population, total urban population, population in urban agglomeration of more than 1 million, and population in largest city to % of urban population. For example, the results show that a 100% increase in export of goods and services as % of GDP increases total urban population by 13.5%. On the contrary, import of goods and services as % of GDP has a negative effect on urbanization in India. A 100% increase in import of goods and services as % of GDP leads to decrease in total urban population by 14.5%. Growth rate of GDP has a positive effect on urbanization as measured by urban population as % of total population, total urban population, and population in largest city to % of urban population. However, growth rate of GDP has a negative effect on population in urban agglomeration of more than 1 million. An increase of 10% in GDP growth rate leads to 0.03% increase in the percentage of urban population. GDP per capita also has a positive effect on urbanization variables except population in the largest city to % of total urban population. Finally, life expectancy at birth has a positive effect on urbanization. The results indicate that a 10% increase in life expectancy at birth leads to reduction of 10.7% in urban population as % of total population.

As there is co-integration among non-stationary variables, the study estimates vector error correction (VEC) model for studying both short-run and long-run causality. Most importantly, the co-integrating equation is interpreted as the long-run equilibrium relationship and the VEC model allows one to study the short-run deviations from this long-run relationship. In other words, to verify whether there is a short-term fluctuation relationship between the agency variables of economic reforms (EGS, IGS, GDPG, GDPPC, and LEB) and urbanization level (UPP/UP/PUA/PLC), a short-term fluctuation model is built to explore the relationship between short-term volatility and long-term equilibrium.

Table 6 presents the estimated results of the VEC model. Results from the first equation relating to four dependent variables are presented separately. We first discuss results from “with reforms” period as our main goal is to see the impact of economic reforms on urbanization in India. Therefore, we first focus on regression models 5, 6 7, and 8. As urbanization variables, i.e., urban population as % of total population, population in urban agglomeration of more than 1 million and population in the largest city to % of urban population are all found stationary at second difference, the study uses second differenced data of these variables to estimate VECM model as VECM requires stationary data. On the other hand, as total urban population data are stationary at first difference, the study uses it without making any difference for the estimation. E-views automatically make one difference in case of VECM (restricted VAR) operation. Therefore, the variable is introduced in the following order in EVIEWS, i.e., DUPP/UP/DPUA/DPLC, EGS, IGS, GDPG, GDPPC, and LEB. As data are used for limited time periods, we only use the first lag of the all the variables for our econometrics models. Results show that R2 values are very high for regression model 6 which indicates the better model fitting of our data. The study also calculates the adjusted R2, as it adjusts for the number of explanatory terms in a model, i.e., it incorporates the model’s degrees of freedom. High values of adjusted R2 for regression model 6 indicate a high percentage of total variation in the dependent variable of the regression models. The F statistics values also are significant for regression model 6 which indicates that our regression models as a whole have statistically significant predictive capability. However, regression models 5, 7 and 8 do not show higher value of R2 and significant values of F statistics which indicates that these regression models do not fit properly with the data used in the study. The insignificant observed R square values of Heteroskedasticity ARCH effect and Breusch-Godfrey Serial correlation LM test clearly show that the results obtained are free from Heteroskedasticity and serial correlations. However, regression model 8 suffers from Heteroskedasticity ARCH effect. The insignificant

Durbin–Watson statistics indicate that the regression models used in the study are free from autocorrelation problem. The insignificant Q-Statistics indicate that there is no problem of lag selections. Finally, as R2 values are less than Durbin–Watson statistics, the regression results are not spurious regressions. Based on these desirable tests for finding a good regression model, regression model 6 is chosen as it qualifies all the required tests.

The coefficient of co-integrated model or coefficient of the error correction term is statistically significant and negative for regression model 6, i.e., for total urban population. This implies that changes in economic reforms which are being captured through export of goods and services as % of GDP, import of goods and services as % of GDP, growth rate of GDP. GDP per capita and life expectancy at birth, exert influence on total urban population in the long run. In other words, there is a long-run causality running from economic reforms to urbanization as measured by total urban population. In the error correction model above, the coefficient of the error correction term is—0.002715, which is consistent with the reverse correction mechanism. The greater the last period deviates from the long-term equilibrium, the greater the amount of correction in the current period. When the short-term fluctuations deviate from the long-term equilibrium, the system will pull the non-equilibrium state back to equilibrium with adjust intensity of 0.0027. According to this estimation, the speed of adjustment is slow.Footnote 4

The results also indicate that economic reforms have no influence, i.e., no long-run causality running from economic reforms to urbanization as measured by urban population as % of total population, population in urban agglomeration of more than 1 million, and population in largest city to % of urban population. Regression model 6 shows that life expectancy at birth has a significant effect on total urban population in the short run. However, in regression models 5, 7 and 8, none of the variables which measure economic reforms are found to have any impact on urbanization as measured by urban population as % of total population, population in urban agglomeration of more than 1 million, and population in largest city to % of urban population.

Normalizing with respect to the coefficient for variables as measured for urbanization yields the following co-integrating relationship in the Johansen long-run equation from VEC Model in Table 7.

Since a double logarithmic functional form is used here, the coefficients can be interpreted as having long-term elasticities. As regression model 6 is the best fitting model, only the sign conditions of regression model 10 are considered. It is thus found that the coefficients of export of goods and services as % of GDP, GDP per capita, life expectancy at birth are positive, whereas the coefficients of import of goods and services as % of GDP and growth rate of GDP are negative. The signs are same as the earlier results of normalized co-integrating coefficients from the Johansen test for co-integrations except the sign of growth rate of GDP. To test whether the coefficients are significant, linear restrictions (LR test) are conducted by considering Chi square values of Wald statistics. Each test variables used to measure the economic reforms are tested individually for significance; the test showed that there is a short-run causality running from lag of only one independent variable, i.e., life expectancy of birth to total urban population in India.

When compared to “without reform” period, the error correction terms from regression models 1–4 are not statistically significant. This indicates that export of goods and services as % of GDP, import of goods and services as % of GDP, growth rate of GDP. GDP per capita and life expectancy at birth do not influence on urbanization in the long run. In other words, there is no long-run causality running from these variables to urbanization in India.

As per the theoretical review of literature, we found that there is a bidirectional relationship between urbanization and economic growth. Co-integration test and error correction model can only show that there is a long-term equilibrium and short-term fluctuation relationship between the variables of economic reforms and urbanization in India; it cannot, however, explain whether there is a causal relationship between them.

Therefore, Granger causality test is used to do further verification.Footnote 5 As the considered variables are not found stationary at level, Granger Causality test was done by considering first or second differences of the variables. Separate vector auto-regressive models (VAR) were used for separate dependent variables (UPP/UP/PUA/PLC) to find out the optimal lag length. VAR model test could be done up to only 3 lags with our limited number of observations. Finally to select the optimal lag, the minimum value of Akaike information criterion (AIC) was used.

From the Granger causality test results (Table 8), it can be seen that there is no Granger causality between the variables at the optimal lag periods. Most importantly, total urban population (up) does not Granger Cause growth rate of GDP (GDPG); GDPG does not Granger Cause UP; UP does not Granger Cause GDP per capita (GDPPC); GDPPC does not Granger Cause UP in both “without reforms” and “with reforms” periods. This indicates that urbanization as measured by total urban population neither causes growth rate of GDP or GDP per capita and vice versa. However, in “with reform” period the results also show that UP does Granger Cause import of goods and services as % of GDP (IGS), but IGS does not Granger Cause UP. The results imply that urbanization as measured by total urban population promotes economic reforms through higher import in India. Granger causality test in “Without reforms” period shows that import of goods and services as % of GDP does Granger Cause urban population (% of total) and total urban population in India. This result is very important as it supports the prediction made in Krugman and Elizondo (1996) which states that large cities are an unintended by-product of import-substitution policies and trade liberalization has a negative effect on the population size of the cities. Urban population (% of total) and total urban population also have impact in life expectancy at birth. GDP growth rate has impact on population in urban agglomerations of more than 1 million (% of total population) and population in the largest city (% of urban population).

6 Conclusions and policy implications

This paper investigates the impact of economic reforms on urbanization in India. As India started its major economic reforms in 1991, “with reform” study period spans the years 1991 to 2016. To better comparison of pre- and post-reforms India, we also analyze data by considering “without reforms” India from 1960 to 1990. Urbanization is measured by four alternative variables, i.e., urban population as % of total population, total urban population, population in urban agglomeration of more than 1 million, and population in largest city to % of urban population. On the other hand, economic reforms are being captured through export of goods and services as % of GDP, import of goods and services as % of GDP, growth rate of GDP, GDP per capita and life expectancy at birth. The choice of appropriate variables for the analysis is based on available development and urbanization literature and also availability of data.

Augmented Dickey—Fuller (ADF) tests were conducted to check the stationarity of the data. Further, Johansen–Juselius co-integration test was conducted to find out the long-run relationship between economic reforms and urbanization. The results show that there is a long-run relationship between them. Co-integrating equation results show that agency of economic reform variables (except import of goods and services as % of GDP) has a positive effect on urbanization in “with reform” period. “Without reforms” analysis shows that agency of economic reform variables (except exports of goods and services as % of GDP) has a positive effect on urbanization in “with reform” period. This clearly indicates that the impact of exports and imports on urbanization has changed due to reforms in 1991.

Based on co-integration results, vector error correction model was estimated to study the both short-run and long-run causality. “With reforms” period results show that economic reforms have influenced only on total urban population and not on the other variables which measure urbanization. However, the speed of adjustment is very slow with adjust intensity 0.0027. The study did not find any causality running between/among rest of the variables in any other form. Except one variable, i.e., life expectancy no other short-run effect is seen having any significant effect on total urban population in the short run. In contrast, “without reforms” period does not have any impact on urbanization in India. But again life expectancy has a short-run effect on population in the largest city (% of urban population).

Granger causality test was executed to test the direction of causal relationship between urbanization and economic reforms. Akaike information criterion (AIC) was used to select the optimal lag. The results show that there is no causal relationship between the variables; only total urban population does Granger Cause import of goods and services as % of GDP in “with reforms” period. “With and without reforms” analysis supports the Krugman and Elizondo hypothesis (1996) and finds the reasons behind emergence of large cities in India.

Finally coming to policy options, we suggest that there is need for promotion of export for speeding up the process of urbanization in India. The export–import policy (EXIM Policy) announced under the Foreign Trade (Development and Regulation Act), 1992, for promotion of export in India through elimination of licensing, quantitative restrictions and other regulatory and discretionary controls. In addition to that India also initiated the Special Economic Zone (SEZ) policy from April 1, 2000. The main goals of SEZs are to improve foreign investment and to offer internationally competitive and hassle-free environment for exports. Presently, eight functional SEZs are located in India. Recent government is trying to increase India’s share in global exports to 5% by 2020 from just 1.6% in 2017. World Bank data show that exports of goods and services (% of GDP) increased from 4.5% in 1960 to 19.12% in 2016. However, India’s export faces several problems such as poor quality, higher production cost, deficiency in export promoting infrastructure and institutional rigidities. Therefore, we suggest that India needs to increase export for promotion of urbanization and economic growth. Based on Krugman and Elizondo hypothesis (1996), it will also help to curb the population size in the large cities and will promote urbanization through medium and small city development. This will lead to reduce the regional imbalances in India.

Indian cities are the engine of economic growth, i.e., urbanization has positive impact on economic growth. Therefore, we need to promote urbanization in India. However, consideration of other variables such as city size distribution, structural shifts in the employment shares etc to establish the relationship between economic reforms and urbanization calls for the future research.

Notes

Data available from the following web link: https://data.worldbank.org/.

Here, the discussion on economic reforms is mainly derived from Ahluwalia (2002).

The coefficient of the error correction term is negative and statistically significant. Therefore, it is consistent with error correcting behavior. The bigger the (negative) statistically significant coefficient, more rapid is the correction. Desirable values of ECM should lie between − 1 to 0. The coefficient being negative (− 0.0027) and significant means that the system corrects its previous period disequilibrium at a speed of 0.27% and it indicates a very slow speed of adjustment of disequilibrium correction for reaching long run equilibrium steady state position.

Though Aristotle introduced a theory of causality, for the first time in human thought, but Clive W.J. Granger has proposed a first working definition of causality, which is called Granger causality in 1969. Hoover (2006) states that Granger-causality is the most influential approach to causality in economics. Recently, Sims (1972) provided a test of causality. However, one obvious limitation of Sims’ test is that it uses more regressors (due to inclusion of leading terms) and suffers from low degree of freedom. Therefore, we use Granger causality test for our analysis.

References

Abhishek N, Jenamani M, Mahanty B (2017) Urban growth in Indian cities: are the driving forces really changing? Habitat Int 69:48–57

Ades AF, Glaeser EL (1995) Trade and circuses: explaining urban giants. Q J Econ 110:195–227

Ahluwalia MS (2002) Economic reforms in India since 1991: has gradualism worked. J Econ Perspect 16(7):67–88

Ansari SJ, Rehmani A (2016) Economic reforms and its impact on the insurance industry in India. Int J Appl Res 2(4):121–124

Arltová M, Fedorová D (2016) Selection of unit root test on the basis of length of the time series and value of AR(1) parameter. Statistika 96(3):47–64

Bairoch P (1993) Economics and world history: myths and paradoxes. Chicago University Press, Chicago

Baldwin RE, Martin P (2004) Agglomeration and regional growth. In: Henderson VJ, Jacques-François T (eds) Handbook of regional and urban economics, vol. 4: cities and geography. Elsevier, North-Holland

Bhagat RB (2011) Emerging pattern of urbanisation in India. Econ Polit Weekly 46(34):10–12

Bhat TP (2011). Structural changes in India’s foreign trade. Working Paper, Institute for Studies in Industrial Development, New Delhi

Brülhart M, Sbergami F (2009) Agglomeration and growth: cross-country evidence. J Urban Econ 65:48–63

Cali M (2009) Urbanization, inequality, and economic growth: evidence from Indian states. Background Paper, World Development Report 2009, World Bank

Chadchan J, Shankar R (2012) An analysis of urban growth trends in the post-economic reforms period in India. Int J Sustainab Built Environ 1:36–49

Choudhuri B, Chatterjee B, Mazumdar M, Karim S (2017) Income ranking of Indian states and their pattern of urbanization. In: Denis E, Zerah MH (eds) Subaltern urbanization in India. Exploring urban change in South Asia. Springer, New Delhi

Dev SM, Mooij S (2002) Social sector expenditures in the 1990s analysis of central and state budgets. Econ Polit Weekly 37(9):853–866

Fujita M, Thisse J-F (2002) Economics of agglomeration: cities, industrial location, and regional growth. Cambridge University Press, Cambridge

Gangopadhyay S, Lanjouw P, Vishwanath T, Yoshida N (2010) Identifying pockets of poverty: insights from poverty mapping experiments in Andhra Pradesh, Orissa and West Bengal. Indian J Hum Dev 4(1):5–28

Gibson J, Datt G, Murgai R, Ravallion M (2017) For India’s rural poor, growing towns matter more than growing cities. World Bank 98:413–429

Gopinath S (2008) Development through planning, markets or decentralisation. Seminar Paper Presented at Indian Institute of Technology, Mumbai, January 21, 2008

Government of India (2009) India: urban poverty report 2009. Ministry of Housing and Urban Poverty Alleviation and Oxford University Press, New Delhi

Henderson JV (2003) The urbanization process and economic growth: the so-what question. J Econ Growth 8:47–71

Hohenberg PM (2004) The historical geography of European cities: an interpretative essay. In: Henderson JV, Jacques-François T (eds) Handbook of regional and urban economics, vol. 4: cities and geography. Elsevier, North-Holland

Hohenberg PM, Lees LH (1985) The making of urban Europe, 1000–1950. Harvard University Press, Harvard

Hoover Kevin D (2006) Causality in economics and econometrics. An entry for the new palgrave dictionary of economics. Palgrave Macmillan, New York

Johansen S (1988) Statistical analysis of cointegrating vectors. J Econ Dyn Control 12(2–3):231–254

Joshi S (2006) Impact of economic reforms on social sector expenditure in India. Econ Polit Weekly 41(4):358–365

Kalamkar SS (2009) Urbanization and agriculture growth in India. Indian J Agric Econ 64(3):442–461

Krugman P (1991) Increasing returns and economic geography. J Polit Econ 99:483–499

Krugman P, Elizondo RL (1996) Trade policy and third world metropolis. J Dev Econ 49:137–150

Kumar S, Sood A (2016) India’s foreign trade and balance of payments position in pre and post reforms period—an evaluation. J Econ Soc Dev 12(2):1–9

Kundu A (2006). Trends and patterns of urbanization and their economic implications. India Infrastructure Report 2006, Oxford University Press, New Delhi, Chap 2, pp 27–41

Lewis W Arthur (1954) Economic development with unlimited supplies of labor. Manch School Econ Soc Stud 22:139–191

Maheswari T (2017). Growth and structure of India’s foreign trade in the post-reform period www.indiastat.com. Accessed February–March

Marrocu E, Paci R, Usai S (2013) Productivity growth in the old and new europe: the role of agglomeration externalities. J Reg Sci 53:418–442

Martin P, Ottaviano G (1999) Growing locations: industry location in a model of endogenous growth. Eur Econ Rev 43:281–302

Mathur OP (2005) Impact of globalization on cities and city-related policies in India. In: Richardson HW, Bae C-HC (eds) Globalization and urban development. Springer, Berlin, pp 43–58

McKinsey Global Institute (2010): India’s urban awakening: building inclusive cities, sustaining economic growth. McKinsey Global Institute, San Francisco. www.mckinsey.com/mgi/publications/india_urbanization/index.asp. Accessed 5 Nov 2012

Mitra A (2014) Agglomeration economies and wellbeing: evidence from India. Athens J Health 1(1):23–36

Narayan L (2016) Relationship between urbanisation and economic growth: a causality analysis for India. Indian J Econ Dev 12(2):237–242

Nisa S, Nisa Z (2008) Economic reforms and its impact on developing countries—a case of India, SSRN. https://ssrn.com/abstract=1112583. http://doi.org/10.2139/ssrn.1112583. Accessed 2 Jan 2017

Nitsch V (2006) Trade openness and urban concentration: new evidence. J Econ Integr 21:340–362

Panchamukhi PR (2000) Social impact of economic reforms in india: a critical appraisal’. Econ Polit Weekly 35(10):836–847

Partridge MD, Rickman DS (2008) Distance From urban agglomeration economies and rural poverty. J Reg Sci 48:285–310

Pillania RK (2008) An exploratory study of Indian foreign trade. J Appl Econ Sci III 3(5):281–292

Prabhu KS (1994) The budget and structural adjustment with a human face. Econ Polit Weekly 29(16/17):1011–1028

Sahni P (2014) Trends in India’s exports: a comparative study of pre and post reform period. J Econ Finance 3(2):8–18

Sahu KK (2017) A comparative study of performance of india’s trade in pre and post liberalization period. Asian Reson 6(3):61–67

Sarkar P, Bhattacharyya B (2005) Trade liberalisation and growth: case studies of India and Korea. Econ Polit Wkly 40(53):5635–5641

Sharma M, Dhiman R (2014) Study of post—reform period of Indian exports: a review. Rev Bus Technol Res (RBTR) 11(1):1–9

Sims CA (1972) Money, income, and causality. Am Econ Rev 62:540–555

Singh AP (2014) Performance of foreign trade in India in the post-liberalization era. Int J Hum Soc Sci Educ 1(10):11–17

Sridhar KS (2010) Determinants of city growth and output in India. Rev Urban Reg Dev Stud 22:22–38

Thünen JH (1826) Der Isolierte Staat in Beziehung Auf Landwirtschaft Und Nationalökonomie. Hamburg, Perthes: Translated from German by Wartenberg, C. M. 1966, Von Thünen’s Isolated State. Pergamon Press, Oxford

Tripathi S (2013a) Do large agglomerations lead to economic growth? Evidence from urban India. Rev Urban Reg Dev Stud 25(3):176–200

Tripathi S (2013b) Does higher economic growth reduce poverty and increase inequality? Evidence from urban India. Indian J Hum Dev 7(1):109–137

Tripathi S (2015) An overview of India’s urbanization, urban economic growth and urban equity”. Int J Econ Empir Res 3(3):115–127

Tripathi S (2017) Relationship between Infrastructure and Population Agglomeration in Urban India: an empirical Assessment, Working paper no. 731, Asian Development Bank Institute, Japan

Tripathi S, Kaur S (2017) Do negative externalities have any impact on population agglomerations?. Evidence from Urban India, MPRA Paper No, p 76897

Tripathi S, Mahey K (2017) Urbanization and economic growth in Punjab (India): an empirical analysis. Urban Res Pract 10(4):379–402

Tripathi S, Rani C (2018) The impact of agricultural activities on urbanization: evidence and implications for India. Int J Urban Sci 22(1):123–144

Virmani A (2004). Economic reforms: policy and institutions some lessons from Indian reforms, Working Paper No. 121, Indian Council For Research On International Economic Relations, New Delhi. http://icrier.org/pdf/wp121.pdf. Accessed 10 Jan 2017

Williamson JG (1965) Regional inequality and the process of national development. Econ Dev Cult Change 13:3–45

World Bank (2010) Perspectives on poverty in india: stylized facts from survey data, India poverty assessment, poverty reduction and economic management network. The World Bank, Washington DC

Yadav P (2018) A comparative study of India’s foreign trade in pre and post reform era. Apeejay-J Manage Sci Technol 5(2):95–108

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

About this article

Cite this article

Tripathi, S. Do economic reforms promote urbanization in India?. Asia-Pac J Reg Sci 3, 647–674 (2019). https://doi.org/10.1007/s41685-019-00117-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41685-019-00117-8