Abstract

This study examines the pace and pattern of employment in India during the last four decades using the Employment-Unemployment Survey (EUS) (1983 to 2011–12) and Periodic Labour Force Survey (PLFS) (2017–18 to 2020–21). The estimates reflect that, notwithstanding the impressive economic growth, aided by demographic dividend, the economy has witnessed a low sustained employment generation. The present analysis reflects a notable increase in both output growth and employment between the years 1983 and 2004-05. However, subsequent to this period, there exists a distinct phase of economic development characterised by a lack of job creation from 2004–05 to 2017-18 and a rebound thereafter. The concerning divergence between Gross Value Added (GVA) growth and employment growth is reflected in the continued dominance of agriculture in terms of employment share even when its GVA share is dismal. Besides, the low employment elasticities of non-farm sectors including industry and services indicate the inability of the non-farm sector to absorb additional labour force and hence sluggish employment opportunities. The slow rate of employment growth during the period of high economic growth failed to bring down overall unemployment. Consequentially, the findings serve as a rebuttal to the claim of ‘slow’ structural transformation. Not only that the labour market is characterising by significant gender disparity, but there is also a growing level of unemployment for the highly educated youth than the less educated. Apparently, economic growth rather than creating more jobs has resulted in net labour displacement as can be seen from the disaggregated analysis of Labour Force Participation Rate (LFPR), Work Force Participation Rate (WFPR), and unemployment rate. The discourse of falling and lower employment elasticities and strong GVA growth painting a discordant picture of the economy calls for an urgent policy redressal in expanding the human capacity to participate in the new economic and social opportunities.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

India at 75 continues to be a fascinating story of a nation rich with economic, social, and cultural diversity. Three quintessential socio-economic-political forces such as democracy (stable political environment), demand (vibrant market and skillful youth-led information, communication, and technological revolution), and demographic dividend (working-age population) are the defining characteristics of the Indian economic outlook. The Indian economy underwent a significant structural transformation with a comprehensive set of economic reforms since 1991, and it was expected to accomplish access to resources through employment generation. The demographic dividend would entail new jobs for its newly added young labour force. While India has entered the 21st century buoyed by new-found confidence in its economic prosperity, however notwithstanding the impressive economic growth beginning the mid-1990s, being one among the countable few during the times of the collapsed global economy, this has hardly been translated into any significant employment generation, and in turn, the large underprivileged are quite untouched by the rapid economic prosperity; especially since the late 2000 the “human face” of reforms remains elusive!

Unfortunately, the post-independence efforts to make the growth process more inclusive at best ended up as the politics of ‘populism’. The Nehruvian socialism fostered the petit bourgeoisie; the “intermediate regime” defining the politics of Indian policymaking (Mody 2006). The piecemeal and ad-hoc policymaking, in trying to appease diverse interest groups in the guile of inclusion, has succeeded very little in being inclusive insofar as benefiting the large underprivileged. Notwithstanding the change in the composition of the intermediate class and their influence with the emergence of and realignment of new groups during reforms, policymaking continues to vacillate between the interests of the powerful new ‘elite’ and the growing political assertiveness of a large underprivileged social class (Vaidyanathan 2007). The experiences at the state level highlighting the tension conflict between market-oriented reforms and political democracy led to an intensification of these tensions. Therefore, maintaining a delicate balance between the two rests directly on the “delivery” of structural changes and policies that satisfy many interest groups, including the larger poor (Rao 2007). But, for that to happen, the democratic state must first determine which economic reforms would be politically as well as socially sustainable. Any quintessential policy strategy must aim at mobilising fiscal resources for the provision of basic education, employment, health, and infrastructure that is accessible to the large underprivileged rural mass. Towards this end, growing unemployment seriously disarrays socio-political inclusion and economic order.

The uproar over high employment growth from 1999 to 2004 (Himanshu 2011; Padhi & Himja 2023) ignores changing employment structure. The slowing of employment growth is primarily due to sectors with better growth potential registering low growth in employment. The agriculture sector continues to be the largest employment potential, whereas the non-agricultural sectors have not created enough employment opportunities to affect a shift of workforce. The Indian economy is showing two distinct trends i.e., higher economic growth in conjunction with slower labour force growth. The employment decline that began in the 1990s and was followed by a recovery in 2004–05 has now reached a stage of near stagnant in 2011–12. This trend has been the subject of discussion in a variety of employment narratives.Footnote 1 Studies (Meherotra & Parida, 2021) highlight that the LFPR reflect a U-shaped relationship as the countries progress from low to a higher level of economic development. In recent periods, the total decrease in employment growth is due to a decline in the female labour participation rate (Padhi & Himja 2023; Padhi & Motkuri 2021; Ghose 2013a, b; Kannan & Ravindran 2012, Thomas 2012; Saha et al. 2013; Neff et al., 2012, Srivastava & Srivastava 2010, Padhi et al. 2019, Abraham 2009). This has alarmingly emerged as a gargantuan socio-economic problem of “jobless growth”.

Nath and Basole (2021) analysed the decline in employment during 2011–12 to 2017–18. A study of Padhi and Triveni (2021) highlighted the growing informality in formal sector jobs in recent times. Also, the International Labour Organization (ILO) (2021) study further emphasises that between 2000 and 2019 in India, the number of young people who were not in employment or in education (NEET) varied by sex, their access to educational opportunities, and social security. Further, almost 55% of the workforce is self-employed in India, which is higher than in the US economy, whereas 33% of the workforce were self-employed (Everlance 2018). These households are frequently abandoned and left with little security. The fast-evolving employment structure is increasingly built on non-standard employment types (casual, contract, fixed term, etc.), which are intertwined with social hierarchy and discrimination, resulting in new kinds of precariousness while extending general disparity in labour market. Increasing informality of the labour market and seasonal/circular migration networks have coexisted with labour market segmentation (Srivastava 2019). Padhi & Himja (2023) also highlight that despite the output growth in the non-farm sector, it has failed to absorb adequately the labour force entering the job market. Mehrotra and Parida (2021) show that both the supply and demand side factors are responsible for the employment-related stagnation of India’s structural change. To make things difficult, the foremost transformation in the world-of-work over the last decade has been the advent of online digital labour platforms in the Indian economy. It is estimated that by 2029–30, the gig and platform economy is anticipated to grow to 23.5 million, according to NITI Aayog (2022). As most of these workers are present in the informal sector without any job security, provisioning of decent employment would be the biggest challenge in India in the near future. The sluggish and disproportional growth of employment in most of the crucial sectors of the economy such as agriculture and industry pose a formidable challenge in sustaining economic growth. In the years 2019–20 to 2021–22, the COVID-19 pandemic has had a profound impact on the world of work as well as lives and livelihoods with lost man-days and gross domestic product (GDP). According to Estupinan et al. (2020), the predicted monthly wage loss of casual workers, salaried personnel and regular employees is ₹33.8 thousand crore (in 2017–18 prices). The pandemic’s devastating effects on formal and informal businesses, on wage-dependent and own-account employees in India, are highlighted by ILO (2021).

Given this backdrop, we examine the evolving employment and output growth scenario, and labour market situation in the Indian economy during the last four decades: 1983 to 2020–21. Specifically, we look at the changing contours of labour force participation in the context of changing demographic trends over a longer time frame. To probe further “jobless growth”, we carefully examine the underlying relationship between the pattern and pace of employment growth and the output growth between 1983 to 2020–21 as well as the sharply declining employment elasticities.

2 Data and Methodology

The analysis is based on the unit-level NSSO Employment and Unemployment Survey data for 10 points of time from the NSSO-EUS 38th (1983) to 68th (2011–12) round as well as the recent PLFS (PLFS-I:2017–18, PLFS-II:2018–19, PLFS-III:2019–20, and PLFS-IV:2020–21). It is important to emphasise that there are some differences between the most recent PLFS survey and the earlier NSSO-EUS survey. As explained in the study of Padhi and Motkuri (2021), it is worth noting that the PLFS differs from the quinquennial EUS in terms of its frequency. While the EUS is conducted every five years, the PLFS is carried out annually in rural areas and quarterly in urban areas. Both surveys employ the stratified random sampling procedure, yet they differ in terms of the criterion used for the second-stage stratum. The previous NSSO-EUS survey classified households based on consumer spending and/or livelihoods, whereas the PLFS divided households into three segments within the selected PSU, depending on the presence of educated household members (Padhi & Motkuri, 2021, Mitra & Srivastava, 2021). Like earlier NSSO-EUS, the PLFS survey also gathers a wide range of information related to labour and employment in India. It also provides complete information with respect to LFPR, WFPR, employment status, unemployment rate (UR),Footnote 2 informality, etc.

However, there are no further differences in the usual status. Both the NSSO-EUS and PLFS (I, II, III & IV) provide the details of the economic status of the population based on their involvement in various parameters such as self-employed, regular, casual, unemployed, and out of labour force. From the NSSO employment and unemployment sets of data, relevant calculations have been made using the census-adjusted weights.Footnote 3 Here, employment is measured based on the data on the usual principal and subsidiary category approach (UPSS).Footnote 4 We classified the industries in accordance with NIC-2004 (required concordance has been done). We have estimated the GVA growth, income growth, and employment elasticity based on 2011–12 base period.

3 Pace and Pattern of Employment: 1983 to 2020–21

This section comprehensively examines the long-run trends and patterns in LFPR, WFPR and UR in India since 1980’s. It also delineates aggregate level, sector-wise and sub-sector-wise spatial and temporal dimensions of output and employment and their elasticities from 1983 to 2020–21 as well as for separate periods in detail. This exercise enables us to draw meaningful comparisons and analysis of the pace of output growth, employment patterns, labour market structure, and structural transformation of the Indian economy.

3.1 India’s Labour Market: Trends and Pattern: 1983 to 2020–21

The long-term analysis clearly shows that the fundamental changes in the labour market and employment trends have been slow and gradual (see Table 1). However, there have been some perceptible changes that may also be noted here. In 2020–21, the total labour force in India stood at an estimated 556.1 million. Out of this total, 292.2 million (54.9%) were self-employed, 121.1 million (22.8%) were in regular employment and an estimated 118.6 million (22.3%) were in casual employment. The number of unemployed people declined from 26.4 million in 2019–20 to 24.3 million in 2020–21 in India, while an additional 119 million people were not added to the potential labour force during the same. The estimates show that self-employment has been the chief driver of the Indian job market. The predominance of own-account work and family work’s contribution reduces as national income rises providing for family obligations is practically non-existent in high-income nations (Gomis et al. 2020).

3.2 Demographic, Employment, and Unemployment Changes Across Age Cohorts

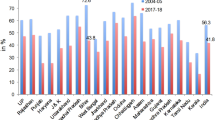

Figure 1 presents a synoptic view of trends in gender-wise (across age-cohorts) UR and LFPR. The estimates reflect the percentage of male LFPR was significantly higher than the female counterpart (gender disparity). From 1983 to 2017–18, the long-run relationship between unemployment and labour force participation rate was noted at the aggregate level. This clearly reflects the persistence of gender-based disparity in terms of participation.

Source: Computed from the unit level datasets of different NSSO and PLFS

Unemployment rates and labour force participation rates.

It is interesting to note that, following the life-cycle hypothesis, the long-run WFPR exhibits a pattern characterised by an inverted U-shaped curve, whereas the unemployment curve demonstrates an L-shaped curve when analysed across different age cohorts. (see Figs. 2 and 3). The estimates show that after a drop in the level of WFPR, the UR rises. This is a reflection of India’s growing unemployment problem (Mehrotra 2013; Srivastava 2017).

Source: Computed from the unit level datasets of different NSSO and PLFS

Age-specific workforce participation rates (WFPR).

Source: Computed from the unit level datasets of different NSSO and PLFS

Age-specific unemployment rates (UR).

The population pyramid along with the LFPR and UR across genders is presented in Fig. 4. We are not considering here 0–14 years of age group given that they are prohibited by law to work (child labour). Over the past forty years, there has been a considerable change in the population structure, as seen by the demographic pyramid (see Fig. 4). The estimates reflect that the UR is much higher for the youth population (15–29) as compared to the other groups. The UR also significantly differs across age cohorts among male and female. During 2011–12 to 2017–18, there is a dramatic increase in the unemployment level for the youth population. Even if they are willing to work, young people have challenges in getting employment in the labour market. Over the last one and half decade there is a subsequent decline in the level of LFPR across age cohorts. The level of LFPR is highest for the age cohort 30–34 to 45–49 and is quite low for the younger and older age cohorts. In the recent period (PLFS-2020-21), there is a marginal increase in LFPR. Naidu (2015) reports that between 2005 and 2012, close to 25 million women left the labour market. Across different age cohorts, unemployment is lower for the female labour force. This difference may be attributed to the lower LFPR, structural differences, cultural and social barriers, and the female labour force has poor educational attainment. The LFPR among females is showing a distressing picture compared with their male counterparts. The onset of 1991 reforms have produced a greater disadvantage to female workers, especially rural females (Chadha & Sahu 2002). According to Rahul (2019), Indian working women are plagued by short- and long-term, structural problems. During 2004–05 to 2018–19, there is a significant decline in the level of female employment. This is mostly because the female labour force is still in the domestic work and their job condition is much more precarious in the current form of development. Women who work in the labour market are frequently subjected to unsustainable casual labour, that limits their capacity to obtain a greater income, exploits them via prolonged work hours and poor-paying rates, and suppresses their ability to express their voice (Arora 2012). After the age of 50, the probability of an individual participating in the labour force plummets precipitously and this characteristic of the labour supply envisages that the overall LFPR will be under significant downward pressure due to enduring shifts in the age distribution of population (Fallick 2007).

Source: Computed from the unit-level datasets of different NSSO EUS and PLFS

Percentage of population, LFPR, and unemployment rate across age cohorts and its gender composition

3.3 Trends in LFPR & WFPR Across Gender and Sectors

The changing employment trends reported here are primarily based on the various thick rounds of NSSO-EUS and recent PLFS survey. The employment estimates in Table 2 show the long-run trends in LFPR for young (aged 15–29) as well as working age groups (15–59 years) across gender and sectors. The estimates reflect that, from 1983 to 2018–19, there is a rapid decline in the overall LFPR of women; it was even halved. The studies have cited several reasons for this decline such as lack of work opportunities for women, increased girls’ and women’s enrolment in schools, lower income levels, and mismeasurement of female LFPR (Klasen & Pieters 2015; World Bank 2009). The estimates also reflect the decline of rural youth (15–29) female labour force participation rate (50% to 21%) is much larger as compared to the urban female 20% to 18%) from 1983 to 2020–21. At the aggregate level, there is a 20% decline in LFPR for females during this time period for the youth category. While for the working-age population (15–59), the decline in the rural female LFPR is from 55% to 34% from 1983 to 2020–21. This clearly highlights the persistence of gender-based disparity in the LFPR in rural and urban areas and the decline of LFPR is higher for females as compared to the male counterpart (from 1983 to 2020–21).

Following the above analysis, Table 3 show a long-term sluggish WFPR of both male and female. The gender disparity in access to employment in the labour market has been a persistent phenomenon that have been observed in the years. The overall Female WFPR for those aged 15–59 in 2020–21 stood at 32.46%, a full 44.55 percentage points below that of men. Further, the total percentage of male WFPR (81.10%) in the same year for aged 15–59 years is more than twice the rate for female adults (33.79%). There are also considerable differences in labour market opportunities. The rural male WFPR shows a persistent decline from 1983 to 2018–19 among the younger aged (15–29 years). Between 1983 to 2020–21, the urban male WFPR dropped by 26.1 percentage points in this category. The rural female WFPR among younger age category has halved to 19.9% in 2020–21 from 49.4% in 1983.

Overall, India experienced a trend of a prolonged period of falling male and female participation rates till 2017–18 and only marginally improved thereafter. Rural non-farm employment (NFE), which generates most of the rural income in India and serves as a risk mitigator, has a special ability for recovery despite the impact of shocks. It is also distinguished by a relatively high rise in female employment and socially disadvantaged groups (Singh & Pattanaik 2020, Kumar et al. 2020). The downward drift in WFPR and increase in unemployment in the recent period along with the global COVID-19 pandemic led to a downturn in the economy might be reflective of future uncertainties.

There exists a voluminous literature examining the declining trend in female employment (Dubey et al. 2017; Mehrotra & Sinha 2017; Naidu 2016; Neetha (2014). Globally, gender inequality is an issue that shows up in both unequal working conditions and access to the labour market (ILO 2019a). The low LFPR might be due to low employment prospects for women due to socio-cultural factors that were deep-rooted in Indian society and the lower possibility of women obtaining paid jobs. Numerous studies have shown that females typically earn less than men, are often kept at bay in definite occupations and industries and are under-represented in high-paid employment (Bertrand 2018; Blau & Kahn 2017; Cortes & Pan 2018). The workers continue to experience job insecurity since the informal employment created by fundamental restructuring does not offer healthcare or unemployment insurance (Binswanger-Mkhize 2013).

3.4 Trends in Unemployment

Table 4 shows the long-term unemployment rate in the working-age and youth population. Over four decades (1983- to 2020–21) for the working-age population the estimates show that the male UR increased from 2.46% in 1983 to 2.70 in 1999–2000, dropped to 2.28% in 2011–12 again risen the steepest point of 6.67 in 2017–18, and then fell to 5.05 in 2020–21 (see Table 4). Further, the urban unemployment rate is quite higher as compared to the rural unemployment rate across genders. Although there is an overall decline in the unemployment levels in the preceding two years as compared to 2017–18, the 5.05% of unemployment further unfolds the magnitude of the dwindling employment. By implication, it indicates the continuation of structural fissures and imperfections in the labour market (Gomis et al. 2020 (ILO)). Mitra and Singh (2019) highlight the reasons for an increase in unemployment with an increase in per capita income, including less labour might be utilised in the production process and “the income may disproportionately originate from the sector, which employs a very small segment of labour on account of productivity gains.” An increase in unemployment also implies an excess supply of labour might lead to a cheaper labour supply. Several surveys point out to the lower educational attainment of the masses contributes to the current employment crisis (Bhandari & Dubey 2019).

The long-term trend showing the steepest rise in the UR in the ‘aged 15–29 years’ corroborates our previous section findings that their respective WFPR also declined. It would be natural to assert that highly educated youth would prefer high order, highly skilled, and secure form employment with written contracts along with other privileges and typically prefer higher pay jobs. Growing educational enrolment led by an increase in awareness (education effect), and an increase in family income (income effect) discourages the LF participation of the younger population (aged 15–29 years). Higher education denotes the possibility of an increase in the quality of manpower so that more families no longer face the stigma of low productivity. From 2011–12 to 2017–18, the UR of rural females increased from 1.60 to 3.85% in the 15–59 years age group. The estimated urban UR for the aged ‘15–59 years’ was 6.50% for males and 9.24% for females in the year 2020–21. Further, the unfolding magnitude of the worsening unemployment scenario of urban females is considerably bigger than that of urban males.

The UR rises with education level overall years (see Table 5). The UR for the illiterate and less educated class (below primary) was 0.57 and 1.13% respectively while, for the highly educated class (graduates & above), it was 14.73% in 2020–21 for the age group ‘15–29 years’. This pattern follows across the years. According to Mitra and Singh (2019), an increase in the UR in recent periods and a declining share of informal employment might indicate that the labour prefers to remain unemployed rather than residually being absorbed in petty activities. The phase of ‘2011–12 to 2017–18’ marks a sudden jump in the unemployment rate of ‘graduation & above category’ from 7.81 to 16.8%.

3.5 Linking GVA Growth and Employment Growth

Table 6 shows the sector-wise pace and pattern of output-employment growth from 1983 to 2020–21. The mainstream view has been that the post-reform Indian economy has defied the “Hindu Growth Rate” of 3.5% between 1950 and 1980 (Singh & Kumar 2021; Rodrik & Subramanian 2005). The estimates highlight that the Spell II (1987–88 to 1993–94) and Spell VI (2011–12 to 2017–18) periods witnessed a spike in average GVA growth of 5.65 and 6.81%, respectively. However, from 2016 to 2022, the economy was hit by three shocks: a sudden demonetization in 2016, the enactments of the Goods and Services Tax in 2017, and the global outbreak of Covid-19 in 2019–2021. These shocks are widely believed to have a significant negative impact on output growth and employment. However, in the aftermath of 2018–19, there is an increase in employment and production growth. A long-term review of employment and output patterns finds that the economy witnessed stagnant employment growth, and this was happening amid an upswing in the economy. For example, from 2011–12 to 2017–18, negative employment growth of -0.54 was observed, notwithstanding strong GVA growth of 6.81%. While GVA growth is a prerequisite, but not enough to reduce unemployment. Similar sort of findings was corroborated by Abubakar and Nurudeen (2019) and Kannan and Raveendran (2019) that even if Indian output growth keeps on rising, there is a rise in joblessness. Roy (2016) has also mentioned that premature or precipitate ‘de-industrialization’ has been a major obstacle in the path of sustainability and dispersal of high growth in India. In this context, Abubakar and Nurudeen (2019) argue that Okun’s law holds true for the Indian economy as they find that to realise desired 1% drop in UR, the nominal GDP growth rate must rise by 2.5%.

Further, the estimates reflect that from 1983 to 2020–21, the long-term growth of agriculture is the lowest of all the sectors. It registered negative employment growth of − 0.16% in 1983 to 1987–88 (Spell-I period), fell to − 2.65% in 2011–12 to 2017–18 (Spell-VI), and stood at − 2.27% from 2011–12 to 2018–19 (Spell-VII) period. It is widely acclaimed that India requires its agricultural growth rate to be around 4.0 and 4.5% for significant poverty reduction (Rao & Radhakrishna 1999). With agriculture growth trickling down through the labour market outcomes, it increases the overall economic well-being; whereas the benefits of the equity in distribution depend on the structure of the economy and its institutional performances (Cervantes-Godoy & Dewbre 2010).

Further, the manufacturing job growth was highest among all sectors during Spell IV (1999–2000 to 2004–05), but subsequently fell and went negative (− 0.53%) during 2011–12 to 2018–19. It is to be acknowledge that manufacturing sector has a multiplier impact on job creation. The National Manufacturing Policy (GOI 2011) stated that the sector needs to grow by 12–14% in order to contribute at least 25% of the National GDP. According to Kaldor’s first law, GDP will grow faster if manufacturing grows at a faster pace (Kaldor 1966, 1967). However, the estimates highlight that during Spell VIII (2011–12 to 2020–21), manufacturing sector witnessed a very low employment share of 0.20% against a comfortable growth of 5.32%; however much below the striking growth of 8.56% in Spell V. Given the pride of place asserted to manufacturing as the engine of growth, the sector’s secular sluggish GVA share and employment share is worrisome (Roy 2016). The employment share of manufacturing has never exceeded 12.8% (2011) and it dropped to 11.5% in 2015–16; highlighing the slow structural change of the Indian economy (Mehrotra & Parida 2019). Bhandari and Dubey (2019) reinforce this evidence by stating that the initial pace of the shift in the structure of economic activity has been considerably slower. Further, the industrial revolution phase in India was scanty and slower and did not proceed quickly enough to absorb the employees who left their traditional occupations (Basole & Narayan 2020).

Cantore et.al. (2017) aptly remarks that India, indeed, has “missed the manufacturing bus” and has instead picked up “service-led growth”. There is a fall in the non-farm employment growth from 4.8% in Spell-I to 2.75% in Spell-II and rose to 4.7% in Spell IV. Ding et al. (2020), point out two ways that economic growth affects employment. First, despite the economy’s healthy growth rate, falling employment reflects the economy’s “crowding-out” effect has an impact on employment. Second, when growth shrinks, and employment expands, it indicates an “absorption” effect on employment brought about by the economy. Thus, the Indian economy has experienced both the “crowding-out” effect as well as the “absorption” effect.

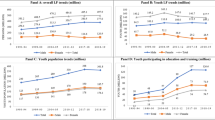

Table 7 shows sectoral shares of GVA and employment over the three and half decades. The disaggregated statistics show an apparent shift in sectoral shares of GVA from agriculture to non-agriculture sectors. Between 1983 and 2020–21, the GVA share of the agriculture and allied sector fell from 41.6% to 16.3%, while the share of the non-agricultural sector rose from 62.0% to 83.7%. The employment contribution from the agricultural sector is falling steadily from 68.6 to 43.7% during the same period (see Fig. 5). While agriculture makes up 16.3% of India’s overall GVA only, it employs roughly 43.7% of the country’s workforce in 2020–21. As Basole (2022) highlights the rate of structural change and the rate of job creation in India is slow and the share of workforce employed in agriculture is larger than it should be. Mehrotra and Parida (2021) argue that the structural change was slowed as a result of the ineffective demand for skilled employees in the non-farm sectors, which led to increased open unemployment and discouraged labour force. They also argue that the employment crisis has had a negative impact on GDP growth, prevalence of poverty and stagnating real wages. The pattern of growth is in contrast to the conventional models of growth and development; wherein structural shifts are noted from agriculture to industry and later towards the services sector. Overall, we find a surge in output and employment from 1987–88 to 2004–05, followed by jobless growth from 2004–05 to 2018–19 and a trifling rebound thereafter (Table 8).

Source: Computed from the unit-level datasets of different NSSO EUS, PLFS, and from MOSPI

Structural change in GVA share and employment share (in %).

The labour absorption potential lies heavily in the agro-based industries. Empirical evidence reveals that the agriculture sector ceased employing additional workforce, rather it started to lay off a large portion of its workforce. Ghose and Kumar (2021) argue that employment in non-agricultural industries is being generated at a sluggish rate and was mostly filled by educated people and it is unable to absorb the manpower abandoning agriculture. Yet, the upside potential of the industry sector has yet to be realised. The employment proportion in the industry increased from 13.7% in 1983 to 25.4% in 2018–19 and again fell slightly to 24.4% in 2020–21. In addition, the sector that contributed 30.5% of GVA in 2004–05 is nearly stable at 29.6% in 2019–20. While the size of the services has seen remarkable growth in GVA share from 33.7% in 1983 to 53.6% in 2020–21. The percentage engaged with the services went up steadily from 17.7% in 1983 to 24.8% in 2004–05, topping the proportion employed in the sector of the industry for the first time, and reaching 31.8% in 2020–21. According to Roy and Chatterjee (2015), the expansion of employment in the service sector must only be seen as a supply-push occurrence or one driven by demand. Cai and Wang (2008), Das and N’Diaye (2013) and Zhang et al. (2011) argue that China has already achieved, or is on the verge of reaching, the Lewis Turning Point, i.e. the phase of economic development where the rural surplus labour disappears, and is absorbed by the manufacturing sector, which also causes rise in agricultural and unskilled industrial real wage rates. In India, as Reddy (2013) observes, real wages have been steadily rising since 1995, and has accelerated since 2007, at least in developed states such as, Punjab, Haryana, and Tamil Nadu. These advanced states in India claimed to have been crossed the Lewis Turning Point. Further, Mehta (2018) claims that the Indian economy is moving towards better employment opportunities or increasing formal jobs and Lewis’s Turning Point (LTP) is in effect. The investment in research and development in agriculture would be more successful in its social impact by generating higher agricultural productivity and employment. Further, Fig. 6 reflects the gender-based employment participation across different sectors in India. The estimates show that most of the females are still engaged in agriculture followed by manufacturing and other services. The female employment participation in agriculture has declined from 81% in 1983 to 60% in 2020–21. While male agricultural participation has declined from 62% to 37% during this period. Followed by this, most of the males are engaged in trade, hotel-restaurant, and construction-related activities.

Source: Computed from the unit level datasets of different NSSO EUS, PLFS rounds

Employment participation across different sectors among genders

3.6 Employment Elasticity in India

The falling trend in total employment against an increasing trend in economic growth is frequently interpreted in terms of employment elasticity (employment growth as a percentage of GDP growth) (Rao & Chatterjee, 2015; Padhi & Himja 2023). The sign and magnitude of employment elasticity of different sectors depend upon the positive output growth. The employment elasticityFootnote 5 (it has been computed based on the compound annual growth rates [CAGR]) can be calculated as,Footnote 6

Basole (2022) asserts that it is crucial to proceed cautiously when evaluating these elasticity numbers for two reasons. First, the rate of population expansion has a significant impact on aggregate employment growth, but the availability of labour has little effect on GDP growth. As a result, GDP growth and employment growth are likely to be inversely related. Second, even a low employment elasticity may point to a level of job creation that is acceptable provided GDP growth is strong enough or the rise in the working-age population is moderate enough. Table 4 shows sector-wise \(Ee\) over the periods. The long-term trends reveal that \(Ee\) is significantly higher in the industrial (0.534) and service sectors (0.450) than in agriculture (0.107). A lower \(Ee\) (0.27) indicates that the economy’s overall GVA growth is not a strong driver of employment. As noted by Ding et.al., (2020), from 1983 to 2020–21, both sectoral and overall \(Ee\) are positive (except for negative absolute values for few years indicating that, to some extent, economic growth exerted a pull-function on job creation in India. Basu and Das (2016) point out a sharp decline in employment elasticity from 0.79 during 1977–78 to 1982–83 to 0.17 during 2009–10 to 2011–12.

When we look at sub-sectors, the employment elasticity of the construction sector (1.051), followed by finance and real estate (0.898) was found to be positive than the other sectors. As per mining &; querying is concerned, the long-run (from 1983 to 2020–21) employment elasticity is negative (− 0.036). India’s \(Ee\) is the highest during Spell IV (1999–2000 to 2004–2005), with a value of 0.488. The negative \(Ee\) shows the ability to generate employment steadily deteriorated. From 2004–05 to 2011–12 and 2011–12 to 2018–19, agriculture witnessed negative employment elasticity i.e. − 0.5 and − 0.77, respectively, indicating shift away from agriculture. Overall \(Ee\) report extreme negative values in Spell VI (2011–12 to 2017–18) and Spell VII (2011–12 to 2018–19). The negative overall \(Ee\) implies that other sectors of the economy are unable to absorb the labour that is quitting agriculture and also indicates a slowdown in the growth of employment opportunities in these sectors. Although during 2011–12 to 2020–21 employment elasticity has been rising and stood at 0.276, it yet to reach the previous heights. Interestingly, the industrial sector sheds comparatively more employment than the service sector. Agriculture has the least potential to create jobs out of the three sectors.

The positive \(Ee\) of agriculture during 2011–12 to 2020–21 indicates more people added to the agriculture led by labour market disruptions in the other sectors of the economy led by post-COVID 19 pandemic. Estimates reflect that not only agriculture, employment growth in the manufacturing sector also picked up during the last half of the 2020s. Goswami and Kujur (2023) argue that direct labour risk-reducing tactics in India reduced employment in both urban and rural regions, whereas indirect risk-reduction labour tactics affected just urban areas. They also point out that the moderating impact underscores the significance of Keynesian interventionist resilience strategies that protect workers and limit risks during the crisis. The deceleration in employment elasticity in the prominent sectors may not be able to fill the growth and employment gap.

The long-run analysis shows that the economy witnessing stagnating employment growth rate, weakening employment elasticity, breaking down output employment relationship, slow structural transformation, and brewing structural problems in labour market such as, low female labour force participation (FLFP) and jobless output growth resulting in a rise in unemployment. The phase of high growth without generating employment during the last decade will not fill the output employment gap and will raise severe concerns about the sustainability of diffusion of growth and absorbing the excess workforce led by demographic dividend. Inadequate infrastructure, skilled manpower and a complex regulatory environment have constrained labour employment. Although the growth-employment parameters improved aftermath from 2018–19 to 2020–21, appropriate policy redressal should be taken to leverage the growth potentiality of various sectors. “The “demographic dividend” argument ignores the fact that available workers are not automatically absorbed to deliver high growth Chandrasekhar et al. (2006). The demographic window of opportunity that India has today can be exploited provided that well laid out strategic policies are adopted and implemented”. Several studies have found that Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA), public works projects, and poverty alleviation measures have a favourable influence on the lives and livelihoods of rural people. MGNREGA type of public projects tend to drive out private sector employment while raising wages in rural areas by 5% (Imbert & Papp 2015), increase in LFP among female (Afridi et al. 2016), improvement in low-caste working bargaining power, increasing rural wage levels, and fall in reliance on high-caste employers (Breitkreuz et al. 2017).

4 Conclusion and Policy Implications

The analysis of the pace and pattern of long-term employment and growth clearly highlights that India’s economic growth is not followed by adequate employment generation. The growth performance is defined by dominating yet unpredictable and volatile service sector, low agricultural output growth, and jobless growth in the manufacturing industry. The ‘slow’ structural transformation being noted from agriculture to industry and later towards the services sector is in contrast to the conventional models of growth and development. We find a surge in output growth and employment from 1987–88 to 2004–05, followed by ‘jobless growth’ from 2004–05 to 2018–19 and a subsequent trifling rebound thereafter. The secular decline in employment elasticities and stagnant employment growth reflects that the link between GVA growth and job creation weakened over time. The slow rate of employment growth during the period of high economic growth failed to bring down overall unemployment. Further, the slow industrial growth may be labour-displacing in its effect. Even though agriculture has the least potential to create jobs and agriculture only makes up 16.3% of India’s overall GVA, yet it employs comparatively higher workforce of around 43.7% in 2020–21. This serves as a rebuttal to the claim of ‘slow’ structural change. Even though agriculture continues to be the largest employment provider, it has seen severe employment setbacks. Despite losing GVA share over the decades, agriculture stays dominant in terms of employment share.

The labour market scenario in India is littered with multifold challenges. The estimates highlight the prevalence of gender disparity as an enduring element of the Indian labour market. The employment prospects for the less educated in the urban areas are sluggish. The increasing unemployment situation for urban women is noticeably greater than for urban men. In contrast to the illiterate and less educated groups, the highly educated youth experience higher job losses. In nutshell, the discourse of falling and lower employment elasticities and strong GVA growth painting a discordant picture of the economy calls for an urgent policy redressal in expanding the human capacity to participate in the new economic and social opportunities. The policy suggestion that follows from our analysis is that a conscious policy effort must be made in identify labour-intensive industrial set up that of manufacturing sector, which will have high linkage effects, in order to achieve inclusive growth. When employment follows growth over longer periods, more resources are made available for expanding human capacity, which in turn enables people to contribute more to growth. As empirical evidence has shown that along with the number of jobs creation in the growth process, it is equally important to look into the quality and decency of jobs too; for there is a strong linkage between productivity and decency of jobs. India’s recent attempt in improving the areas of health and education may have a favourable influence on the conversion of rising labour into a high-quality workforce with low-cost employment.

Notes

The percentage of unemployed people in the entire labour force is known as the unemployment rate (UR).

Please see Report No. 554, the 68th NSSO Employment and Unemployment Survey, for more information on how population projections were calculated. “The census adjustment has been done on the basis of census and NSSO employment data sets. First the weighted NSSO population figure is estimated from the concerned NSSO employment and unemployment rounds both for rural-urban and male and female differently after that the given figures are divided by the concerned census population figures. After getting the ratios, they are multiplied with the multiplier figures to get the census adjusted weights.”

“In this approach the status of activity on which a person spent relatively longer time of the preceding 365 days from the date of survey is considered as the principal usual activity of the person (MOSPI, 2012). Accordingly, a person is considered working or employed, if the person was engaged for a relatively longer time during the past year in one or more work related activities”. Details can be found in the NSSO employment and unemployment reports that are issued afterwards. The employment and unemployment numbers from the NSSO are directly used in this approach.”

Employment elasticity of output measures the responsiveness of employment with responsiveness change in output.

In the case \(Ee\) <o, employment falls as the economy grows. Having \(Ee\) =1, indicates that employment is growing at the same rate as the economy, when \(Ee\) = zero, employment does not grow at all even during an economic boom.

References

NITI Aayog. 2022. India’s Booming Gig and Platform Economy: Perspectives and Recommendations on the Future of Work. Retrieved from https://www.niti.gov.in/sites/default/files/2022-06/25th_June_Final_Report_27062022.pdf

Abraham, V. 2009. Employment Growth in Rural India: Distress-Driven? Economic and Political Weekly 18: 97–104.

Abubakar, J., and I. Nurudeen. 2019. Economic Growth in India, is it a Jobless Growth? An Empirical Examination Using Okun’s Law. The Indian Journal of Labour Economics 62: 307–317.

Afridi, F., A. Mukhopadhyay, and S. Sahoo. 2016. Female Labor Force Participation and Child Education in India: Evidence from the National Rural Employment Guarantee Scheme. IZA Journal of Labor & Development 5 (1): 7.

Arora, P. 2012. The Rigid Employment Protection Legislations in India and its Impact on the Economy: Is Flexicurity a Viable Solution. NALSAR Stud. l. Rev. 7: 40.

Basole, A. 2022. Structural Transformation and Employment Generation in India: Past Performance and the Way Forward. The Indian Journal of Labour Economics 65 (2): 295–320.

Basole, A., and A. Narayan. 2020. Long-run Performance of the Organised Manufacturing Sector in India: An Analysis of Sub-Periods and Industry-Level Trends. Economic and Political Weekly 55 (10): 35–44.

Basu, Deepankar and Debarashi Das. 2016. Employment Elasticity in India and the US, 1977–2011

Bertrand, M. 2018. Coase Lecture: The Glass Ceiling. Economica 85 (338): 205–231. https://doi.org/10.1111/ecca.12264.

Bhandari, L., & Dubey, A. 2019. Emerging Employment Patterns of 21st Century India. Indicus Foundation White Paper, 11.

Binswanger-Mkhize, H.P. 2013. The Stunted Structural Transformation of the Indian Economy. Economic and Political Weekly 48 (26–27): 5–13.

Blau, F.D., and L.M. Kahn. 2017. The Gender Wage Gap: Extent, Trends, and Explanations. Journal of Economic Literature 55 (3): 789–865. https://doi.org/10.1257/jel.20160995.

Breitkreuz, R., C.-J. Stanton, N. Brady, J. Pattison-Williams, E. King, C. Mishra, and B. Swallow. 2017. The Mahatma Gandhi National Rural Employment Guarantee Scheme: A Policy Solution to Rural Poverty in India? Development Policy Review 35 (3): 397–417.

Cai, F., and M. Wang. 2008. A Counterfactual of Unlimited Surplus Labour in Rural China. China World Economic 16: 51–65.

Cantore, Nicola, Michele Clara, Alejandro Lavopa, and Camelia Soare. 2017. Manufacturing as an Engine of Growth: Which is the Best Fuel?”. Structural Change and Economic Dynamics 42: 56–66.

Cervantes-Godoy, D. and J. Dewbre. 2010. Economic Importance of Agriculture for Poverty Reduction. OECD Food, Agriculture and Fisheries Working Papers, No. 23. OECD Publishing https://doi.org/10.1787/5kmmv9s20944-en.

Chadha, G.K., and P.P. Sahu. 2002. Post-Reform Setbacks on Rural Employment: Issues that Need Further Scrutiny. Economic and Political Weekly 37 (21): 1998–2026.

Chandrasekhar, C.P., Jayati Ghosh, and Anamitra Roychowdhury. 2006. The Demographic Dividend and Young India’s Economic Future. Economic and Political Weekly 2006: 5055–5064.

Cortes, P., and J. Pan. 2018. Occupation and Gender. In The Oxford Handbook of Women and the Economy, ed. S.L. Averett, L.M. Argys, and S.D. Hoffman, 425–452. Oxford: Oxford University Press. https://doi.org/10.1093/oxfordhb/9780190628963.013.12.

Das, M., and P. N’Diaye. 2013. Chronicle of a Decline Foretold: Has China Reached the Lewis Turning Point? IMF Working Paper 13/26. Washington D.C.

Ding, YingYing, Zheng Li, Xiaojun Ge, and Hu. Yu. 2020. Empirical Analysis of the Synergy of the Three Sectors’ Development and Labor Employment. Technological Forecasting and Social Change 160: 120223.

Dubey, A., W. Olsen, and K. Sen. 2017. The Decline in the Labour Force Participation of Rural Women in India: Taking a Long-Run View. The Indian Journal of Labour Economics 60 (4): 589–612.

Estupinan, X., S. Gupta, M. Sharma, and B. Birla. 2020. Impact of COVID-19 Pandemic on Labour Supply, Wages and Gross Value Added in India. The Indian Economic Journal 68 (4): 572–592.

Everlance 2018. Self-Employment Statistics in the US.Retrieved from https://www.everlance.com/blog/self-employment-statistics/ March 28, 2020.

Fallick, Bruce, and Jonathan F. Pingle. 2007. A Cohort-based Model of Labor Force Participation. Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C. Retrieved from https://www.federalreserve.gov/PUBS/FEDS/2007/200709/200709pap.pdf

Ghose, Ajit K., and Abhishek Kumar. 2021. India’s Deepening Employment Crisis in the Time of Rapid Economic Growth. The Indian Journal of Labour Economics 64 (2): 247–279.

Ghose, Ajit K. 2013. The Enigma of Women in the Labourforce, Indian Journal of Labour Economics, 56 (4): .

Ghose, Jayati 2013. The Strange Case of the Jobs that did not Appear: Structural Change, Employment and Social Patterns in India, Presidential Address, 55th Annual Conference, The Indian Society of Labour Economics, held during 16–18 December at CESP, JNU, New Delhi.

Gomis, Roger, Steven Kapsos, and Ste Kuhn. 2020. World Employment and Social Outlook: Trends 2020. Geneva: ILO.

Goswami, Diti, and Sandeep Kumar Kujur. 2023. Risk-Reducing Strategies and Labour Vulnerability during the pandemic in India. International Journal of Disaster Risk Reduction 93: 103763.

Himanshu. 2011. Employment Trends in India: A Re-examination. Economic and Political Weekly 46 (37): 43–59.

Hirway, Indira. 2012. Missing Labourforce: An Explanation. Economic and Political Weekly 47 (37): 43–59.

International Labour Organization (ILO). 2019a. A quantum leap for gender equality: For a better future of work for all (Geneva).

ILO 2021. Situation Analysis on the COVID-19 Pandemic’s Impact on Enterprises and Workers in the Formal and Informal Economy in India. ILO DWT for South Asia and Country Office for India. Retrieved from https://www.ilo.org/wcmsp5/groups/public/---asia/---ro-bangkok/---sro-new_delhi/documents/publication/wcms_798079.pdf

Imbert, C., and J. Papp. 2015. Labor Market Effects of Social Programs: Evidence from India’s Employment Guarantee. American Economic Journal: Applied Economics 7 (2): 233–263.

Kaldor, N. 1966. Causes of the Slow Rate of Economic Growth of the United Kingdom. Cambridge University Press.

Kaldor, N. 1967. Strategic Factors in Economic Development. Ithaca: Cornell University Press.

Kannan, K.P., and G. Raveendran. 2019. From Jobless to Job-Loss Growth: Gainers and Losers During 2012–2018. Economic and Political Weekly 54 (44): 38–44.

Kannan, K.P., and G. Ravindran. 2012. Counting and Profiling the Missing Labour Force. Economic and Political Weekly 47 (6): 77–80.

Klasen, S., and J. Pieters. 2015. What Explains the Stagnation of Female Labor Force Participation in Urban India? The World Bank Economic Review 29 (3): 449–478.

Kumar, M.S., and P.P. Sahu. 2013. Employment Growth, Education and Skills in India: Emerging Perspectives. Indian Journal of Labour Economics 56 (1): 95–122.

Kumar, A., N. Deka, S. Bathla, S. Saroj, and S.K. Srivastava. 2020. Rural Non-Farm Employment in Eastern India: Implications for Economic Well-Being. The Indian Journal of Labour Economics 63: 657–676.

Majid, N. 2021. Young Persons Not in Employment and Education (NEET) in India: 2000–2019. International Labor Organization Research Brief, March (March 2020).

Mehrotra, S., and J.K. Parida. 2021. Stalled Structural Change Brings an Employment Crisis in India. The Indian Journal of Labour Economics 64 (2): 281–308.

Mehrotra, S., and S. Sinha. 2017. Explaining Falling Female Employment During a High Growth Period. Economic & Political Weekly 52 (39): 54–62.

Mehrotra, Santosh, Ankita Gandhi, Bimal Kishore Sahoo, and Partha Saha. 2012. Creating Employment in the Twelfth Five-Year Plan. Economic and Political Weekly 47 (19): 63–73.

Mehrotra, Santosh, Ankita Gandhi, Partha Saha, and Bimal Kishore Sahoo. 2013. Turnaround in India’s Employment Story: Silver Lining amidst Joblessness and Informalisation? Economic and Political Weekly 48 (35): 87–96.

Mehrotra, S. and J. Parida, 2019. India’s Employment Crisis: Rising Education Levels and Falling Non-agricultural Job Growth, Azim Premji University.

Mehta, Balwant Singh. 2018. India’s Pace of Moving Towards Lewis Turning Point. Amity Journal of Economics 3 (1): 15–34.

Mitra and Srivastava 2021. Reliability of PLFS 2019–20 data, Economic and Political Weekly, Vol LVI, No 39

Mitra, Arup, and Jitender Singh. 2019. Rising Unemployment in India: A Statewise Analysis from 1993–94 to 2017–18. Economic and Political Weekly 54 (50): 12–16.

Mitra, A. 2013. Insights into Inclusive Growth, Employment and Wellbeing in India, Springer New Delhi.

Mody, Ashoka. 2006. Inclusive Growth: K N Raj on Economic Development, Orient Longman, Hyderabad, for Sameeksha Trust.

Nagaraj, R. 2008. India’s Recent Economic Growth: A Closer Look. Economic and Political Weekly 43 (15): 55–61.

Naidu, S. 2015. Missing Women Workers: Explaining the Decline in Women’s Labor-Force Participation in India. Dollars & Sense 320: 30.

Naidu, S.C. 2016. Domestic Labour and Female Labour Force Participation: Adding a Piece to the Puzzle. Economic and Political Weekly 51 (44–45): 101–108.

Nath, P. and A. Basole 2021. Did Employment Rise or Fall in India Between 2011 to 2017? estimating absolute changes in the workforce, Economic and Political Weekly, Vol LVI No 34.

Neetha, N. 2014. Crisis in Female Employment. Economic and Political Weekly 49 (47): 50–59.

Neff, Daniel, Kunal Sen, and Veronika Kling. 2012. The Puzzling Decline in Rural Women’s Labourforce Participation in India: A Reexamination. Indian Journal of Labour Economics 55 (3): 407–429.

Padhi, B., and V. Motkuri. 2021. Labour Force and Employment Growth in India. Economic & Political Weekly 56 (47): 59.

Padhi, B., and P.P. Sahu. 2016. Jobless Growth and Challenges of Skill in India: The Emerging Regional Pattern, Paper Presented in the 58th Annual Conference, The Indian Society of Labour Economics, held during 24–26 November 2016 at IIT Guwahati, Assam.

Padhi, B., and H. Sharma. 2023. Changing Contours of Growth and Employment in the Indian Labour Market: A Sectoral Decomposition Approach. Structural Change and Economic Dynamics. https://doi.org/10.1016/j.strueco.2023.08.004.

Padhi, B., U.S. Mishra, and U. Pattanayak. 2019. Gender Based Wage Discrimination in Indian Urban Labour Market: An Assessment. The Indian Journal of Labour Economics 62 (3): 361–388.

Padhi, B. and Triveni. T. 2021. Employment and Informality in the Indian Labour Market: Emerging Trends, Labour & Development, Vol. 28, No.1

Papola, T. S. and Sahu 2012. Growth and Structure of Employment: Long-Term and Post-Reform Performance and the Emerging Challenge, ISID Occasional Paper Series 2012/01.

Rahul, M. 2019. Never Done, Poorly Paid, and Vanishing: Female Employment and Labour Force Participation in India. Economic and Political Weekly, 54(19).

Rao, D.T. 2007. Economic Reforms: Lofty Rhetoric. Hallucinated Politics and Electoral Backlash, Review of Development and Changes 12 (1): 129–138.

Rao, C.H.H., and R. Radhakrishna. 1999. National Food Security: Policy Perspective for India’. In Food Security Diversification and Resource Management: Refocusing of Agriculture, ed. G.H. Peter and J.V. Braun. Ashgate: International Association of Agricultural Economics.

Reddy, A. 2013. Trends in Rural Wage Rates: Whether India Reached Lewis Turning Point. Trends in Rural Wage Rates: Whether India Reached Lewis Turning Point.

Rodrik, D., and A. Subramanian. 2005. From ‘Hindu Growth’ to Productivity Surge: The Mystery of the Indian Growth Transition. IMF Staff Papers 52 (2): 193–228.

Roy, Satyaki. 2016. Faltering Manufacturing Growth and Employment: Is ‘Making’the Answer? Economic & Political Weekly 51 (13): 35–42.

Roy Choudhury, P., and B. Chatterjee. 2015. Analyzing “Jobless Growth” in Post-Liberalisation India: A Decomposition Approach. The Indian Journal of Labour Economics 58 (4): 577–608.

Saha, Partha, Ankita Gandhi, Kamala Devi and Sharmistha Sinha. 2013. Low Female Employment in a Period of High Growth: Insights from Primary Survey in Uttar Pradesh and Gujarat, IAMR Report No. 9/2013, Institute of Applied Manpower Research, Planning Commission, Government of India, New Delhi.

Singh, P., and S. Kumar. 2021. Demographic Dividend in the Age of Neoliberal Capitalism: An Analysis of Employment and Employability in India. The Indian Journal of Labour Economics 64 (3): 595–619.

Singh, P., and F. Pattanaik. 2020. Unequal Reward for Equal Work? Understanding Women’s Work and Wage Discrimination in India Through the Meniscus of Social Hierarchy. Contemporary Voice of Dalit 12 (1): 19–36.

Srivastava, R. 2019. Emerging Dynamics of Labour Market Inequality in India: Migration, Informality, Segmentation and Social Discrimination. The Indian Journal of Labour Economics 62: 147–171.

Srivastava, Nisha, and Ravi Srivastava. 2010. Women, Work and Employment Outcome in Rural India. Economic and Political Weekly 45 (28): 49–63.

Sundaram, K. 2001. Employment-Unemployment Situation in the Nineties: Some Results from NSS 55th Round Survey. Economic and Political Weekly 36 (11): 931–940.

Sundaram, K. 2013. Some Recent Trends in Population, Employment and Poverty in India: An Analysis. Indian Economic Review 48 (1): 83–128.

Thomas, J.J. 2012. India’s Labour Market During the 2000s; Surveying the Changes. Economic and Political Weekly 47 (51): 22.

Unni, J., and G. Raveendran. 2007. Growth of Employment (1993–94 to 2004–05): Illusion of Inclusiveness? Economic and Political Weekly 20: 196–199.

Vaidyanathan, A. 2007. Discussing “Inclusive Growth’ Ahead of Its Time”, Economic and Political Weekly, July 28

World Bank. 2009. Female Labor Force Participation in Turkey: Trends, Determinants and Policy Framework. Washington, DC: World Bank.

Zhang, X., J. Yang, and S. Wang. 2011. China has Reached the Lewis Turning Point. China Economic Review 22: 542–554.

Funding

No supports received or sought from any funding organisation for preparation of this work.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflicts of interest

Views presented in the paper are personal views of the author.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Padhi, B., Tripati Rao, D. & Triveni, T. Discerning the Long-Term Pace and Patterns of Employment in India. Ind. J. Labour Econ. 66, 975–1004 (2023). https://doi.org/10.1007/s41027-023-00462-5

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41027-023-00462-5