Abstract

This study meticulously examines the intricate relationships between Carbon Dioxide CO2 emissions and key economic indicators across different income strata of 83 countries over 1995–2020 period. We employ panel unit root tests, panel cointegration tests, Fully Modified Least Squares (FMOLS), Arellano-Bond dynamic panel-data estimation models, and panel threshold analysis to discern the underlying dynamics. Our findings reveal a heterogeneous impact of economic indicators on CO2 emissions across different income groups, thereby affirming the inconclusive nature of the Environmental Kuznets Curve (EKC) hypothesis across income brackets. Specifically, the real GDP per capita associated with the EKC turning point closely aligns with existing literature, yet the impact of the square of per-capita GDP is observed to be income group-specific. While the EKC hypothesis is observed to be applicable to middle and high-income countries, it is found to be inapplicable to low-income countries. Additionally, the results indicate significant variations in the relationships between CO2 emissions and other economic variables, such as population growth, trade openness, and livestock production, across different income levels. This underscores the necessity for tailored policy approaches that account for the unique environmental and economic dynamics encountered by each income group. Our study contributes to the existing literature by providing a comprehensive and nuanced understanding of the relationships between CO2 emissions and economic development indicators across diverse economic contexts, thereby highlighting the importance of customized strategies in addressing the multifaceted challenges posed by climate change. A one-size-fits-all strategy may not be effective in addressing the challenges posed by climate change across diverse economic contexts.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Since the days of Adam Smith and industrial revolution, material wellbeing or commodity fetishism has been the obsession of mainstream economics. The economic development and growth are not only considered inseparable but are also believed to be impossible without increased production of goods and services even though that leads to increased emission of greenhouse gases, especially carbon dioxide (CO2). The Global CO2 emissions were 185 times higher in 2019 than they were in 1850. The historical concentration of industry and wealth in developed countries means that they are responsible for 79% of the CO2 emission from 1850 to 2011 (Busch 2015).

The relationship between carbon dioxide (CO2) emissions and Gross Domestic Product (GDP) has been the subject of increasing scholarly interest, primarily due to the intertwined nature of economic growth and environmental sustainability. The escalating threat of climate change is irrefutable and widely attributed to anthropogenic CO2 emissions, primarily from the burning of fossil fuels (IPCC 2014). Concurrently, economic growth, which is crucial to improving living standards and reducing poverty, is a significant driver of these emissions (Stern 2017; Ansari 2022; Wang et al. 2023). Therefore, understanding the dynamic relationship between GDP and CO2 emissions is crucial for the development of sustainable policies and strategies that can harmonize economic growth with environmental conservation.

The Environmental Kuznets Curve (EKC) hypothesis postulates that economic development initially leads to a deterioration in the environment, but after a certain point, further increase in income starts to improve environmental conditions (Grossman and Krueger 1991). However, empirical support for this hypothesis, especially concerning CO2 emissions, has been inconsistent (Stern 2004; Nicolli and Vona 2016; Ansari 2022). Moreover, most research has focused on this relationship at a global level or for specific income groups, often neglecting to consider the nuanced differences between low, middle-, and high-income countries. Such differences could influence the emissions-GDP relationship due to varying economic structures, energy consumption patterns, and technological efficiencies (Shahbaz et al. 2012).

The developing countries like China and India in recent years have exhibited high economic growth along with high CO2 emission. Between 1991 and 2019, the CO2 emissions have quadrupled in both China and India.Footnote 1 Similarly, the converse is true for the less developed countries. Strikingly, although both historical and contemporary evidence affirm the existence of a positive relationship between economic growth/development and environmental deterioration, in recent years, the relationship at extreme points appears to be little ambiguous (Pata and Yurtkuran 2023; Ansari 2022; Wang et al. 2023). At the absolute levels, CO2 emissions of developed countries have plateaued or tapered off, whereas that of developing countries like China, India, Russia, etc., though way behind in terms average living standards, have either surpassed or have come closer to levels of the former (Moreau et al. 2019). As per the world development indicators, the developed countries like Norway, Sweden, Denmark, Switzerland have low per capita CO2 emissions despite having high per capita GDP, on the contrary, the developing countries such as Russia, Kazakhstan, South Africa, Algeria etc. have low GDP per capita in spite of having high per capita emissions of CO2. As a result, the developed and developing countries are not on the same page as far as climate change redressal is concerned. Emphasizing on irreversibility of commodity production and relying on technological solutions for environmental concerns, the developed countries put the onus on developing countries (Rogelj and Schleussner 2019) On the contrary, the developing countries not only consider their CO2 emissions to be substantially low—viewing from per capita perspective, but also relegate technological solutions on the grounds economy (Chen and Taylor 2020).

In this research, we propose to delve deeper into the dynamic relationship between CO2 emissions and GDP for low, middle, and high-income countries separately. By examining these groups distinctly, this study intends to contribute to the literature on economic growth, environmental sustainability, and policy development in a differentiated global context. This study explores the causal connection between CO2 emissions and GDP growth for 83 countries (divided into three groups of countries based on income levels: low-income countries; a group of countries with middle income; a group of high-income countries) covering the yearly time frame of 1995–2020 (Fig. 1). Against this backdrop the major research question that arises is do the developing countries emit less CO2, in per capita terms, in comparison to that of the developed countries? In other words, will a richer economy worsen the environmental quality even further due to increased emissions, or will an increase in per capita GDP not only increase the living standards but also contribute to a better, less polluted planet? In particular, does relationship exists between per capita GDP and per capita CO2 emissions for different levels of income? However, in order to examine the relevance of aforesaid research question, we review and trace gap in available literature.

Selected countries based on World bank classification

This article is structured as follows. The subsequent section delineates the brief review of literature, followed by the methodology and data sources, encompassing the model specification, functional relationships, and the variables employed in the research. Subsequently, the fourth segment delves into a comprehensive analysis of the econometric outcomes derived from the models and expounds on their implications. The concluding section encapsulates the key takeaways, and outlines the limitations of the research.

The Review of Literature

Empirically, there are at least three hypothesis that explore the connection between environmental degradation and GDP, viz; Environmental Kuznets Curve (EKC), Environmental Brundtland Curve (EBC), and the Environmental Daly curve (EDC) (Bratt 2012). The EKC hypothesis presupposes an inverted “U” shaped relationship between the two, i.e. an increasing level of GDP would initially increase environmental problems until a certain level of GDP, from which the environmental problems starts to decline owing to adoption of eco-friendly technology, environmental norms and other factors (Ahmad et al. 2021). In contrast to EKC, the EBC suggests that there is an “U” shaped relationship which implies that the poorest and wealthiest countries have the higher levels of environmental problems (Pata and Yurtkuran 2023). Finally, the EDC hypothesizes an increasing levels of pollution with an increasing GDP that keeps on going, without any turning point. Of course, it suggests that till certain levels of GDP, the rate of increase in pollution levels be marginal but ultimately it will rise monotonically, may be at an exponential rate (Esmaeili et al. 2023). The available empirical literature provides diverse evidence against the aforesaid hypothesis.

Extant research widely considered the relationship between economic growth and CO2 emissions under the environmental inverted U-shape Kuznets hypothesis (EIUKH). This is because of three effects, the scale, the composition, and the technique (Grossman and Krueger 1991). At the beginning of the economic growth, the scale effects will have an adverse environmental impact that may contribute to higher CO2 emissions. As countries sustained the economic growth for a while, the composition and the technique effects will lead to a decline in CO2 emission. However, there is no unanimity in the literature about the exact nexus (Bashir et al. 2021). The diverse results because of choice of contexts, time period, explanatory variables, and methodological adaptation (Adewuyi and Awodumi 2017; Shahbaz and Sinha 2019).

There are three contested hypotheses. First: causality running from energy consumption to economic growth; second: causality from economic growth to energy consumption; third: bidirectional causality (Mardani et al. 2019; Tugcu et al. 2012). Gorus and Aydin (2019) investigated the EIUKH in the MENA region employing the Granger causality method for 1975–2014 and detected no causal nexus between economic growth and CO2. But the study observed a bidirectional link between energy consumption and emission level in the intermediate and the long run. Halkos and Bampatsou (2019) adopted a conditional nonparametric frontier analysis to a sample of 73 economies over the period 1980–2014 and identified that the impact of economic growth on the environment depends upon the country’s stage of development and region.

Ivanovski et al. (2021) examine the nexus between renewable and non-renewable energy consumption on economic growth for 39 OECD and non-OECD nations using non-parametric methods from 1990 to 2015. They identified both renewable and the non-renewable energy consumption is positively correlated with economic growth. Their results for OECD and non-OECD counties differ considerably. In OECD nations, non-renewable energy consumption is developing into more critical over time, but renewable energy consumption has little effect on economic growth. Both renewable and non-renewable energy consumption have a positive effect on economic growth for non-OECD countries. Renewable and non-renewable energy turns out to complement for non-OECD countries, supporting Shahbaz et al.’s (2018) results. Erdogan et al. (2020) reinforce the EKC hypothesis for 25 OECD countries. They use cross-section dependence and cross-section independence methods in the period from 1990 to 2014. Examine the relationship between energy, environment, and economic growth for a set of 27 EU countries, Sharma et al. (2021) found bidirectional negative causality for renewable energy and GDP, and bidirectional positive causality for non-renewable energy and GDP. Jun et al. (2021) researched the relationship among globalization, non-renewable energy consumption, economic growth, and CO2 emission for selected South Asian economies during 1985–2018, applying a fully modified ordinary least square. They support the EKC hypothesis, and globalization and non-renewable energy consumption increase CO2 emissions. Similarly, Uzair Ali et al. (2020) studied the impact of economic development on CO2 emission in India, Pakistan, and Bangladesh using panel autoregressive distributed lags model for 1971–2014, and documented relationship is inverted U-shaped. Ahmad et al. (2021) presented contrasting results for developing countries. They found Brazil, China, India, Malaysia, the Russian Federation, Thailand, and Turkey support the EIUKH, but Mexico, Philippines, Indonesia, and South Africa do not. Using a unique long-time data set for United Kingdom, Amar (2021) lends creditable support to EIUKH.

The studies such as Erdogan et al (2020), Jun et al. (2021), Uzair Ali et al. (2020) etc., support the EKC hypothesis, while the studies such as, Gorus and Aydin (2019), Ansari (2022) Bandyopadhyay and Rej (2021), Ozturk (2010), Holtz-Eakin and Selden (1995) reject the same. Yet there are a few studies such as Ahmad et al. (2021), Dinda (2004), Amar (2021), Stern et al. (1996), etc. that provide mixed evidence on the existence of EKC hypothesis. A few of the studies that reject or provide mixed evidence for EKC, either support the EBC or the EDC.

Erdogan et al. (2020) supports EKC hypothesis for 25 OECD countries. They used cross-sectional dependence and independence methods to examine the relationship between energy, environment, and economic growth for a set of 27 EU countries during the period from 1990 to 2014. Jun et al. (2021) explored the relationship among globalization, non-renewable energy consumption, economic growth, and CO2 emission for select South Asian economies during 1985–2018, by applying a fully modified ordinary least square. They found evidence in support of EKC hypothesis. Similarly, Uzair Ali et al. (2020) studied the impact of economic development on CO2 emission in India, Pakistan, and Bangladesh using panel autoregressive distributed lags model for 1971–2014, and documented relationship as inverted U-shaped.

On the contrary, Gorus and Aydin (2019) investigated the EKC hypothesis in the Middle East and North Africa (MENA) region for 1975–2014 period using Granger causality method but detected no causal nexus between economic growth and CO2. Ansari (2022) explored the empirical validity of EKC for ASEAN countries between 1991–2006, using second generation: CADF and CIPS unit root tests, Westerlund cointegration test, fully modified ordinary least square (FMOLS) and Pooled Mean Group (PMG). The study found the existence of unidirectional causality between economic growth and environmental degradation which supports EDC and rejects the EKC hypothesis. Bandyopadhyay and Rej (2021) examined the dynamic linkages between GDP and CO2 emissions in India for the period 1978–2019 after controlling the effects of nuclear energy consumptions, foreign direct investment (FDI), and trade openness. The study adopted robust econometric modelling by taking the presence of structural break into consideration. Interestingly, the study found either inverted “N” or “J” shaped relationship between GDP and CO2 emissions in India. Thus, the study rejects the validity of EKC hypothesis in the context of India for the period between 1978–2019. A similar result was found by Acaravci and Ozturk (2010) while examining the relationship between economic growth, carbon dioxide (CO2) emissions and, energy consumption in European countries, using a cointegration test. A positive long-run relationship between the said variable was found for few countries but across the board, the study did not find the same. In other words, the study (Acaravci and Ozturk 2010) while rejecting the EKC hypothesis found some evidence in support of EDC. A similar result was also found by Holtz-Eakin and Selden (1995). Using the panel data for 130 countries, Holtz-Eakin and Selden (1995) found that the existence of a diminishing propensity to emit CO2 emissions as the economies develop. However, the study suggests that although the marginal propensity to emit diminishes with a growing economy, the accumulative CO2 emissions globally increases at an annual rate. Finally, by performing a sensitivity analysis, the authors maintain that the pace of economic growth does not dramatically alter the future levels of carbon dioxide emissions. Thus, the study supports EBC hypothesis while rejecting the EKC hypothesis.

Apart from supporting or rejecting the EKC hypothesis, there are a few studies such as Ahmad et al. (2021), Dinda (2004), Amar (2021) that provide mixed evidence on EKC hypothesis. Ahmad et al. (2021) presented contrasting results for developing countries. They found Brazil, China, India, Malaysia, the Russian Federation, Thailand, and Turkey support EKC hypothesis, but Mexico, Philippines, Indonesia, and South Africa do not. Similarly, Dinda (2004) found mixed evidence for EKC hypothesis, after controlling for factors like income elasticity of environmental quality demand, the scale effect, the technological and composition effects, international trade, market mechanism, legal restrictions, etc. Also, the study (Dinda 2004) suggests that there is no specific per capita income level that represents the turning point at which environmental degradation starts to decrease. Stern et al. (1996) found that in some cases economic growth affects the environment in a way consistent with the EKC, and in other cases, there was no consistency with the EKC hypothesis at all. The authors suggest the difference in outcome could be due to differences in the incentives to preserve the environment. They conclude that the EKC cannot be applied in reality without strong incentives from policymakers and a general willingness from the civilians to reduce environmental degradation.

Thus, there is no unanimity over the relationship between GDP and environmental degradation especially CO2 emissions. Nevertheless, the diverse finding may be viewed in terms of three contested causal relationships. First: causality running from energy consumption to economic growth; second: causality from economic growth to energy consumption; third: bidirectional causality (Mardani et al. 2019).

Halkos and Bampatsou (2019) adopted a conditional nonparametric frontier analysis to a sample of 73 economies over the period 1980–2014 and identified that the impact of economic growth on the environment depends upon the country’s stage of development and region. Ivanovski et al. (2021) examined the nexus between renewable and non-renewable energy consumption on economic growth for 39 OECD and non-OECD nations using non-parametric methods from 1990 to 2015. They identified both renewable and the non-renewable energy consumption is positively correlated with economic growth. Their results for OECD and non-OECD counties differ considerably. In OECD nations, non-renewable energy consumption is developing into more critical over time, but renewable energy consumption has little effect on economic growth. Both renewable and non-renewable energy consumption have a positive effect on economic growth for non-OECD countries. Renewable and non-renewable energy turns out to complement for non-OECD countries.

Ansari (2022) scrutinized the EKC hypothesis in ASEAN nations between 1991 and 2016, using consumption-based emissions (CO2 emission) and footprint-based emissions (ecological footprint) as environmental proxies. The study revealed that while the inverted U-shaped hypothesis was valid when using ecological footprint, it was not valid with CO2 emissions. Wang et al. (2023) conducted a comprehensive analysis of the impact of trade openness, human capital, renewable energy, and natural resource rent on carbon emissions within the EKC framework, using data from 208 countries from 1990 to 2018. The results indicated that the EKC hypothesis was valid at the global level when considering these factors, and revealed heterogeneous effects of renewable energy consumption and human capital on carbon emissions before and after the EKC turning point. Notably, the study found that trade openness only mitigated carbon emissions in countries with weak decoupling after the EKC turning points, and that natural resource rents increased carbon emissions in most countries.

Pata and Yurtkuran (2023) investigated the impact of globalization and income on ecological footprint in five highly globalized European Union countries from 1970 to 2018. The study, which incorporated smooth structural changes, found that the EKC hypothesis was valid for Switzerland and Denmark, while a U-shaped relationship was observed for Sweden and Austria. Furthermore, the study found that globalization promoted environmental sustainability in Switzerland and the Netherlands. Ponce and Manlangit (2023) examined the relationship between CO2 emissions, real per capita GDP, and energy consumption in the ASEAN region from 1960 to 2021. The study found robust empirical evidence supporting the EKC hypothesis, indicating a per capita income turning point beyond which CO2 emissions and real income begin to decouple, highlighting the importance of reducing fossil fuel use and adopting coordinated strategic plans among ASEAN member states to reduce carbon dioxide emissions.

Thus, the available empirical literature although unanimously support a connection between economic growth and environmental degradation, their findings differ in terms of degree and direction. Moreover, the existing literature does not throw enough light on the threshold limits beyond which the degree and direction of relationship between economic growth and environmental degradation changes. However, to best of our knowledge, none of the studies used dynamic panel threshold model for the different levels of income groups of countries (low, middle and high income) in examining the relationship between CO2 emission and economic growth. Since there is possibility of lagged relationships between CO2 emission and economic growth, dynamic panel models better will provide better estimates than the static panel data models (Baltagi and Baltagi 2021). Further, in vast majority of the studies mentioned above, the focus has been entirely on the standard formulation of the EKC rather than examining the plausibility of different environmental curves for different groups of countries. The present study there for intends to fill this knowledge gap.

Methodology and Sources of data

Data Source

The study used panel data of 83 countries, classified into three income groups, low, middle and high-income countries as per prevailing World Bank classification (on the basis of their GNI per capita) for lower-middle income, upper middle income and upper income categories, respectively. This study uses the data covering the period from 1995 to 2020. All the data are from the World Development Indicators online database (WDI 2023). The dependent variable Carbon dioxide (CO2) emissions are expressed in tons CO2 emitted per capita for one period.

The dependent variable, CO2 emission is measured in metric tons per capita from individual nations. Our key independent variable GDP per-capita, measured in 2010 years US dollars’ value. The expected outcome varies with different theories. To test for polynomial form, the variable (GDP per-capita) squared is included. Apart from the key independent variable, taking the clue from literature, we have used several control variables such Renewable Electricity (Shang et al 2022), Non-Renewable Electricity, Livestock production (Bor et al. 2022), Population growth (Husnain et al 2023) and Trade Openness (Sharif et al. 2022; Wang et al. 2023).

The energy sector contributes more than two-third of global greenhouse gas emission (IEA 2020). Hence, energy output is considered as a relevant variable in our model. The variable, Renewable Electricity, is the share of electricity generated by renewable power sources, in percent. Renewable electricity production emits less CO2 than non-renewable electricity production; therefore, the expected correlation between renewable electricity output and carbon dioxide emissions should be negative. Unlike renewable electricity, the electricity production made from coal sources should have a positive effect on the CO2 emission level. Producing electricity from coal sources is still common, despite the high levels of CO2 being emitted. The variable Electricity Coal measures the share of electricity produced from coal sources, in percent.

Livestock production demands a high amount of natural resources and contributes to environmental degradation by emitting out greenhouse gases, such as CO2 (Thornton and Herrero 2010; Rojas-Downing et al. 2017; Sikiru et al. 2023). The livestock index measures the value of the production of commodities such as food, fiber, and skins. A higher livestock index is expected to increase CO2 emissions. Although livestock production is a part of GDP it is unlikely to be significantly correlated with any other dependent variable. However, based on our review and economic rationality variables of our interest are presented in Table 1, as well as their measure, expected sign and economic implication.

Older population and younger population have negative and positive influence, respectively, on CO2 emissions. It is estimated that a 1% increase in the proportion of elderly results in 0.4% decrease in CO2 emissions (Kim et al. 2020). Thus, aging is considered as an explanatory variable and is represented through population growth. Finally, trade openness has increased the world material production significantly and thereby has influenced CO2 emissions. Hence we have considered Trade openness (i.e. Trade % of GDP) as a potential variable in explaining variations in CO2 emissions across the country and over time.

Econometric Specification

The specification of our empirical model is grounded in an extensive review of prevailing literature. Drawing on the frameworks established by Erdogan et al. (2020), Jun et al. (2021), Ansari (2022), Ongan et al. (2023), and Anwar et al. (2023), we have formulated the subsequent model for rigorous empirical analysis:

where, \(P{C}_{-}GDP\) is per-capita GDP, \({P{C}_{-}GDP}^{2}\) is square of per-capita GDP, PG is population growth, TO is trade openness, RE is renewable electricity production, EGC is electricity generated from coal, LPI is the livestock production index. See Table 1 for details. The general econometric model we applied is given in Eq. 1

where, i denotes the cross-section (country) index, and t is the time series index. Equation 1 is used to explore non-linearity in the aforesaid relationship. In this investigation, multiple panel unit root examinations are utilized to ascertain the integration order of the selected variables. The study employs the more dependable and well-behaved panel unit root tests as suggested by Levin et al., (2002) and the Fisher-type tests recommended by Maddala and Wu (1999), grounded on the augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) tests. Gutierrez (2003), through Monte Carlo simulations, demonstrated that the Kao (1999) residual cointegration test surpasses the performance of the tests developed by Pedroni, particularly in scenarios characterized by a small time-series dimension of the panel (Pedroni 1999, 2004). Consequently, the present study leverages the Kao (1999) test to examine the long-term association between Carbon Dioxide emissions and economic development indicators across low, middle, and high-income nations. Additionally, the Fully Modified Least Squares (FMLs) model, formulated by Phillips and Hansen (1990), and more recently employed by Aminu et al. (2023) to explore the environmental Kuznets Curve in 13 Sub-Saharan African economies, is utilized in conjunction with the dynamic panel model developed by Arellano and Bond (1991) to comprehend the relationship between CO2 emissions and various economic development indicators. To ensure the robustness of the findings, a panel threshold model is incorporated into the analysis.

Results and Discussion

Stylized Facts

The summary statistics are delineated in Table 2. The mean CO2 emissions per capita is approximately 8 metric tons for high-income countries, while middle-income and low-income countries exhibit mean emissions of about 4 and 1.1 metric tons, respectively. Regarding GDP per capita, it is observed that low-income countries register the lowest values, whereas high-income countries exhibit the highest. In terms of the variability of per capita CO2 emissions, high-income countries exhibit the greatest fluctuations, while low-income countries manifest the least volatility across all nations. Concerning the mean trade openness, defined as the ratio of traded volume to total GDP, high-income countries display the highest ratio, whereas low-income countries register the lowest. Notably, the proportion of electricity generated from coal is highest in high-income countries (HIC), whereas it is lowest in low-income countries (LIC). Conversely, in terms of the percentage of electricity derived from renewable resources, the trend is inverse; it is highest for LIC and lowest for HIC.

Scatter plots presented in Fig. 2 indicates a possible relation between per capita emission and per capita GDP for countries in different income groups. When viewed across all data, preliminary findings point out the fact that basic industrialization implies higher emissions but to establish a link between wealth and CO2 further analysis is attempted in the subsequent sections. In fact, the distribution of CO2 emissions across different categories of countries indicates that the richer economies are the major contributors of the CO2 emissions (69%), while the lower economies contribute comparatively less (only 6% of total). The distribution provides a strong indication of the relative sensitivity of global emissions to the income of the countries.

Source: World Development Indicators

Per capita emission vs. per capita GDP.

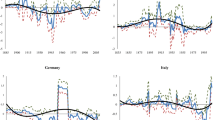

However, looking at the change in CO2 emissions and GDP for different economies gives us a fair idea to establish a relationship for different income level countries (Fig. 3). For high-income countries, the level of CO2 emissions started declining after a certain level of GDP was reached. Possibly, with the help of scientific enhancements to curb the CO2 emissions, increasing awareness regarding the ill effects of Carbon Dioxide emissions, stringent government regulations on emissions standards, as the economies grow, the level of CO2 emissions started decreasing. To establish a further concrete relationship, a detailed statistical analysis needs to be done. For middle-income countries, industrialization comes into the picture as well and the level of CO2 emissions continuously increased. Though the emissions are at a steep increasing level, the point to be noted is that the comparison between the level of emission of high and middle-income countries provides a different picture. For low-income countries, they have low carbon dioxide emissions as compared to middle and high-income countries now but with the increase in GDP per capita, their emissions will rise. Thus, prima facie, it appears that the data under consideration supports the possibility of EKC in the case of high income countries, while in the case of middle and low income countries it supports EDC. The results of detailed statistical analysis based on dynamic panel data presented below may provide an accurate picture.

Source: World Development Indicators

CO2 emissions and GDP trends.

2: Results from Econometric Analysis

The analysis of the panel data begins with an examination of the integration properties of the variables included in each model. Since no single test is likely to be definitive in this rapidly-evolving area of econometric research (McCoskey and Selden 1998), we use several panel unit root tests in this study, although the null hypothesis remains the same. Table 3, reports panel unit root test estimates for low, middle, and high-income countries. It is observed that all the variables exhibit unit roots in level form for the low-income countries which implies non-stationarity of variables in the level form. The unit root results are similar for the middle as well as high-income countries. The same panel unit root tests were conducted by transforming all variables into first difference as shown in Table 4 for different income countries. All the tests show that the variables are stationary at first differences. Hence, we conclude that the first differenced variables are stationary so that panel variable are integrated of order one, I (1).

Since all panel variables are found to be integrated of order one I (1), we proceed with the panel Cointegration test to find out the long-run relationship between Carbon Dioxide emissions and economic development indicators. The results of the Kao Cointegration test and Pedroni test for cointegration offer intriguing insights into the long-term relationships between variables for different income groups. Specifically, the Kao Cointegration test results indicate a long-term relationship for middle-income countries as all the test statistics are statistically significant (Table 5). This suggests that the variables under consideration share a common stochastic trend in the long run for middle-income countries. However, for low and high-income countries, some of the test statistics are not significant, thereby providing inconclusive evidence of cointegration. This implies that for low and high-income countries, it is not possible to definitively assert that the variables move together in the long run.

Similarly, the Pedroni test for cointegration reveals that cointegration is observed for middle and high-income groups as all the test statistics are significant. This affirms the existence of a long-term equilibrium relationship between the variables for these income groups. Conversely, for low-income countries, the results remain inconclusive as some of the test statistics are not significant. This suggests that there is insufficient evidence to confirm a long-term relationship between the variables for low-income countries.

The inconclusive evidence of cointegration for low and high-income countries in the Kao test and for low-income countries in the Pedroni test may be attributed to various factors. For instance, structural differences, economic instability, and policy inconsistencies in low-income countries might result in weaker long-term relationships between the variables (Narayan and Smyth 2005). Additionally, the heterogeneity in economic structures, technological efficiencies, and energy consumption patterns across different income groups (Shahbaz et al. 2012) could also account for the varying results.

These findings underscore the necessity of adopting a differentiated approach to policy formulation and implementation across different income groups. Policies aimed at addressing issues related to economic growth, environmental sustainability, and other relevant factors should be tailored to the specific characteristics and long-term relationships observed in each income group. Moreover, the results indicate a need for further research to elucidate the factors contributing to the inconclusive evidence of cointegration in low and high-income countries, as this would aid in the development of more effective and targeted policies (Ongan et al. 2023; Anwar et al. 2023). We conduct the poolability test before proceeding further. In the analysis employing the Roy–Zellner criterion for poolability, the chi-square statistic is observed to be 41,751.13, which is statistically significant at the 1% level, thereby implying the appropriateness of pooling the data. This inference is congruent with the results obtained from the F-test (F(82, 2151) = 276.45, p value < 0.001), further corroborating the decision for poolability.

The analysis using the Fully Modified Least Squares (FMOLS) and Arellano-Bond linear dynamic panel-data estimation models reveals insightful differences in the relationships between various economic and environmental variables and CO2 emissions across different income groups. In the FMOLS model, GDP per capita demonstrates a positive and statistically significant relationship with CO2 emissions across all income levels, aligning with the widespread acknowledgment in the literature that economic growth is a primary driver of emissions (Stern 2017; Wang et al. 2023). However, the squared term of GDP per capita, employed to investigate the Environmental Kuznets Curve (EKC) hypothesis, exhibits a negative and significant coefficient for all countries, except for low-income countries, where the relationship is insignificant. This result partially supports the EKC hypothesis, suggesting that it may not be applicable to low-income countries. This divergence highlights the nuanced differences between income groups and supports previous studies that have found inconsistent empirical support for the EKC hypothesis, especially concerning CO2 emissions (Stern 2004; Ansari 2022).

In contrast, the Arellano-Bond model shows that GDP per capita has a positive and significant relationship with emissions only for middle and low-income countries, while the relationship is insignificant for high-income countries and all countries combined. This result suggests that in this model, economic growth is a more significant driver of emissions in middle and low-income countries. The squared term of GDP per capita exhibits a negative and significant coefficient for all countries and middle-income countries but is insignificant for high and low-income countries. This finding implies that the EKC hypothesis holds for middle-income countries in this model but not for high and low-income countries.

The differing results for the GDP per capita and its squared term across the two models and income groups underline the complexity of the relationship between economic growth and CO2 emissions. It underscores the importance of considering different income levels and models when assessing this relationship. It also highlights the need for a more differentiated approach in policy development, as a one-size-fits-all strategy may not be effective in addressing the challenges posed by climate change across diverse economic contexts (Wang et al. 2023; Ansari 2022).

Moreover, the analysis also reveals significant variations in the relationships between other variables, such as trade openness, renewable electricity, coal electricity, and livestock production index, and CO2 emissions across different income levels and models. For instance, in the FMOLS model, the coefficients for population growth are positive and statistically significant across all income levels, indicating that an increase in population correlates with an increase in CO2 emissions. This result is consistent with the broader literature that has highlighted the significant impact of population growth on environmental degradation (Shahbaz et al. 2012).

However, in the Arellano-Bond model, the coefficient for population growth is only statistically significant for low-income countries, while it is insignificant for all countries, high, and middle-income countries. This suggests that, in the dynamic panel model, population growth is a significant driver of emissions only in low-income countries. This difference in results across the two models highlights the sensitivity of the relationship between population growth and CO2 emissions to the model specification and underscores the complexity of this relationship.

The differing results for population growth across the two models and income groups further emphasize the necessity of a differentiated approach in policy development. It is evident that the drivers of CO2 emissions vary across different income levels and models, and therefore, a one-size-fits-all strategy may not be effective in addressing the challenges posed by climate change across diverse economic contexts.

In the FMOLS model, the coefficients for trade openness are negative and statistically significant for all countries, high, and middle-income countries, indicating that increased trade openness is associated with a decrease in CO2 emissions in these groups. However, the coefficient for trade openness is statistically insignificant for low-income countries, suggesting that, in this income group, trade openness does not have a significant impact on CO2 emissions. These results align with the argument that trade openness can lead to a decrease in CO2 emissions by facilitating the transfer of cleaner technologies and promoting efficiency gains (Frankel and Rose 2005).

Contrastingly, in the Arellano-Bond model, the coefficient for trade openness is positive and statistically significant only for low-income countries, while it is insignificant for all countries, high, and middle-income countries. This suggests that, in the dynamic panel model, increased trade openness is associated with an increase in CO2 emissions only in low-income countries. This divergent result for low-income countries in the Arellano-Bond model might be attributed to the 'pollution haven hypothesis', which suggests that trade openness can lead to an increase in emissions in developing countries as they tend to attract pollution-intensive industries from developed countries (Copeland and Taylor 2004; Esmaeili et al. 2023).

In the FMOLS model, the coefficient for LPI is positive and statistically significant for all countries, middle, and low-income countries, suggesting that an increase in livestock production is associated with an increase in CO2 emissions in these groups. However, the coefficient for LPI is statistically insignificant for high-income countries, indicating that livestock production does not have a significant impact on CO2 emissions in this income group. This result is consistent with the existing literature that highlights the substantial contribution of livestock production to greenhouse gas emissions, particularly in developing countries where the sector is often less efficient and more emissions-intensive (Gerber et al. 2013).

Conversely, in the Arellano–Bond model, the coefficient for LPI is positive and statistically significant for high-income countries, while it is negative and statistically significant for middle and low-income countries. The coefficient for all countries is statistically insignificant. This result suggests that in the dynamic panel model, an increase in livestock production is associated with an increase in CO2 emissions in high-income countries, while it is associated with a decrease in emissions in middle and low-income countries. This contrasting result may be due to the fact that high-income countries often have more intensive livestock production systems, which can lead to higher emissions per unit of output (Steinfeld et al. 2006) (Tables 6 and 7).

In a bid to advance the understanding and for robustness check of our previous results, this study leverages panel threshold analysis. Significantly, the findings denote that the real GDP per capita associated with the EKC turning point is approximately $19,725, an observation that aligns closely with the $19,203 reported by Wang et al. (2023) for 208 countries between 1990–2018. Noteworthy is the heterogeneous impact of the square of per-capita GDP both prior and subsequent to crossing this threshold. Specifically, this impact is negative and statistically significant before the threshold but becomes insignificant thereafter. This pattern is consistently observed across high-income countries. However, in the case of middle-income countries, the effect of per-capita GDP squared is negative and statistically significant both before and after surpassing the threshold. Intriguingly, for low-income countries, both the per-capita GDP and its square proved to be statistically insignificant, thereby suggesting that the EKC hypothesis is not applicable to this income bracket. A similar heterogeneity in results was also observed for variables such as population growth, trade openness, and livestock production.

This discernment of the nuanced relationships between CO2 emissions and economic indicators, as unveiled by the panel threshold model, underscores the imperative for income group-specific policy approaches. Additionally, it illuminates the heterogeneity inherent in the environmental and economic dynamics of different countries, thereby emphasizing the necessity for customized strategies to address the unique challenges encountered by each income group. Indeed, these findings resonate with recent literature that highlights the varied impacts of economic indicators on environmental outcomes across different income groups (Shahbaz et al. 2021; Zhang et al. 2022). For instance, the heterogeneous effects of trade openness and population growth across income groups corroborate the findings of Nguyen et al. (2020), who noted significant variations in the environmental consequences of trade liberalization and demographic changes across different economic contexts.

Conclusion and Policy Implications

There is inconclusive evidence of cointegration for low-income countries, whereas for middle income countries there is long run relationship. The results indicate that the relationship between various economic and environmental variables, particularly GDP per capita and its squared term, and CO2 emissions varies significantly across different income levels. This underscores the importance of considering the nuanced differences between countries at different stages of economic development when designing policies and strategies to combat climate change. Further research is needed to delve deeper into these differences and develop more targeted and effective policies to harmonize economic growth with environmental conservation across diverse global contexts. It is evident that the impact of population growth trade openness on emissions is not uniform across different income levels. The results indicate that the relationship between livestock production and CO2 emissions varies significantly across different income levels and models. This highlights the need for targeted policies that consider the specific characteristics of the livestock sector in different income groups. It also underscores the importance of promoting sustainable livestock production practices that can contribute to a reduction in CO2 emissions while supporting food security and rural development.

This study elucidates the complex interplay between CO2 emissions and key economic indicators across different income groups. The observed heterogeneity in the impacts of these variables reinforces the necessity for tailored policy interventions and underscores the limitations of a one-size-fits-all approach. As countries strive to harmonize economic growth with environmental sustainability, it is imperative to consider the unique characteristics and challenges faced by each income group, as highlighted by this study. A one-size-fits-all strategy may not be effective in addressing the challenges posed by climate change across diverse economic contexts.

Limitations of the Study

The empirical analysis in this study is made using variables chosen with a theoretical background supporting the expected outcome, however, all relevant possible variables did not have available data. For example, deforestation is a large anthropogenic source of CO2 emitted in the atmosphere (Van der Werf et al. 2010) has been omitted owing to unavailability of any reliable data.

Data availability

Not applicable.

Notes

https://ourworldindata.org/co2-emissions, accessed on July 15 2023.

References

Acaravci, A., and I. Ozturk. 2010. On the relationship between energy consumption, CO2 emissions and economic growth in Europe. Energy 35 (12): 5412–5420.

Adewuyi, A.O., and O.B. Awodumi. 2017. Renewable and non-renewable energy-growth-emissions linkages: Review of emerging trends with policy implications. Renewable and Sustainable Energy Reviews 69: 275–291.

Ahmad, M., A. Muslija, and E. Satrovic. 2021. Does economic prosperity lead to environmental sustainability in developing economies? Environmental Kuznets curve theory. Environmental Science and Pollution Research 28 (18): 22588–22601.

Amar, A.B. 2021. Economic growth and environment in the United Kingdom: Robust evidence using more than 250 years data. Environmental Economics and Policy Studies 23: 667–681. https://doi.org/10.1007/s10018-020-00300-8.

Aminu, N., N. Clifton, and S. Mahe. 2023. From pollution to prosperity: Investigating the Environmental Kuznets curve and pollution-haven hypothesis in sub-Saharan Africa’s industrial sector. Journal of Environmental Management 342: 118147.

Ansari, M.A. 2022. Re-visiting the Environmental Kuznets curve for ASEAN: A comparison between ecological footprint and carbon dioxide emissions. Renewable and Sustainable Energy Reviews 168: 112867.

Anwar, A., A. Barut, F. Pala, N. Kilinc-Ata, E. Kaya, and D.T.Q. Lien. 2023. A different look at the environmental Kuznets curve from the perspective of environmental deterioration and economic policy uncertainty: Evidence from fragile countries. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-023-28761-w.

Arellano, M., and S. Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58 (2): 277–297.

Baltagi, B.H. 2021. Dynamic panel data models. In Econometric analysis of panel data. Springer texts in business and economics, 187–228. Cham: Springer.

Bandyopadhyay, A., and S. Rej. 2021. Can nuclear energy fuel an environmentally sustainable economic growth? Revisiting the EKC hypothesis for India. Environmental Science and Pollution Research 28: 63065–63086.

Bashir, M.F., B. Ma, M.A. Bashir, and L. Shahzad. 2021. Scientific data-driven evaluation of academic publications on environmental Kuznets curve. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-021-13110-.

Bor, Ö., T. Omay, P. Iren, and C. Aktan. 2022. The effects of energy-intensive meat production on CO2 emissions: Evidence from extended environmental Kuznets framework. Environmental Science and Pollution Research 29 (19): 27805–27818.

Bratt, L. 2012. Three totally different environmental/GDP curves. Sustainable Development-Education, Business and Management-Architecture and Building Construction-Agriculture and Food Security, 283–314.

Busch, J. 2015. Climate change & development in three charts. Climate Change and Development. https://www.cgdev.org/blog/climate-change-and-development-three-charts. Accessed Sept 2021

Chen, Q., and D. Taylor. 2020. Economic development and pollution emissions in Singapore: Evidence in support of the Environmental Kuznets Curve hypothesis and its implications for regional sustainability. Journal of Cleaner Production 243: 118637.

Copeland, B. R., and M.S. Taylor. 2004. Trade, growth, and the environment. Journal of Economic Literature 42 (1): 7–71.

Dinda, S. 2004. Environmental Kuznets curve hypothesis: A survey. Ecological Economics 49 (4): 431–455.

Erdogan, S., I. Okumus, and A.E. Guzel. 2020. Revisiting the Environmental Kuznets Curve hypothesis in OECD countries: The role of renewable, non-renewable energy, and oil prices. Environmental Science and Pollution Research 27 (19): 23655–23663.

Esmaeili, P., D.B. Lorente, and A. Anwar. 2023. Revisiting the environmental Kuznetz curve and pollution haven hypothesis in N-11 economies: Fresh evidence from panel quantile regression. Environmental Research 228: 115844.

Frankel, J. A., and A.K. Rose. 2005. Is trade good or bad for the environment? Sorting out the causality. Review of Economics and Statistics 87 (1): 85–91.

Gerber, P. J., H. Steinfeld, B. Henderson, A. Mottet, C. Opio, J. Dijkman, et al. 2013. Tackling climate change through livestock: A global assessment of emissions and mitigation opportunities. Food and Agriculture Organization of the United Nations (FAO).

Gorus, M.S., and M. Aydin. 2019. The relationship between energy consumption, economic growth, and CO2 emission in MENA countries: Causality analysis in the frequency domain. Energy 168: 815–822.

Grossman, G.M., and A.B. Krueger. 1991. Environmental impacts of a North American free trade agreement. Working Paper No: 3914, NBER, Cambridge, MA. https://www.nber.org/system/files/working_papers/w3914/w3914.pdf.

Gutierrez, L. 2003. On the power of panel cointegration tests: A Monte Carlo comparison. Economics Letters. 80 (1): 105–111.

Halkos, G.E., and C. Bampatsou. 2019. Economic growth and environmental degradation: A conditional nonparametric frontier analysis. Environmental Economics and Policy Studies 21 (2): 325–347.

Holtz-Eakin, D., and T.M. Selden. 1995. Stoking the fires? CO2 emissions and economic growth. Journal of Public Economics 57 (1): 85–101.

Husnain, M.I.U., S.D. Beyene, and K. Aruga. 2023. Investigating the energy-environmental Kuznets curve under panel quantile regression: A global perspective. Environmental Science and Pollution Research 30 (8): 20527–20546.

IEA. 2020. If the energy sector is to tackle climate change, it must also think about water. (IEA, Producer). https://www.iea.org: Paris https://www.iea.org/commentaries/if-the-energy-sector-is-to-tackle-climate-change-it-must-also-think-about-water. Accessed Oct 2021.

IPCC. 2014. Summary for policymakers In: Climate change 2014: Impacts, adaptation, and vulnerability. Part A: Global and sectoral aspects. Contribution of working Group II to the fifth assessment report of the intergovernmental panel on climate change. https://epic.awi.de/id/eprint/37530/1/IPCC_AR5_SYR_Final.pdf. Accessed 20 Aug 2023.

Ivanovski, K., A. Hailemariam, and R. Smyth. 2021. The effect of renewable and non-renewable energy consumption on economic growth: Non-parametric evidence. Journal of Cleaner Production 286: 124956.

Jun, W., et al. 2021. Does globalization matter for environmental degradation? Nexus among energy consumption, economic growth, and carbon dioxide emission. Energy Policy 153: 112230.

Kao, C. 1999. Spurious regression and residual-based tests for cointegration in panel data. Journal of Econometrics 90 (1): 1–44.

Kim, J., H. Lim, and H.H. Joe. 2020. Do aging and low fertility reduce carbon emissions in Korea? Evidence from IPAT augmented EKC analysis. International Journal of Environmental Research and Public Health 17 (8): 2972.

Levin, A., C.F. Lin, and C.S.J. Chu. 2002. Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics 108 (1): 1–24.

Maddala, G.S., and S. Wu. 1999. A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics 61 (S1): 631–652.

Mardani, A., et al. 2019. Carbon dioxide (CO2) emissions and economic growth: A systematic review of two decades of research from 1995 to 2017. Science of the Total Environment 649: 31–49.

McCoskey, S. K., and T.M. Selden. 1998. Health care expenditures and GDP: Panel data unit root test results. Journal of Health Economics 17 (3): 369–376.

Moreau, V., C.A.D.O. Neves, and F. Vuille. 2019. Is decoupling a red herring? The role of structural effects and energy policies in Europe. Energy Policy 128: 243–252.

Nguyen, C.P., C. Schinckus, and T. Dinh Su. 2020. Economic integration and CO2 emissions: Evidence from emerging economies. Climate and Development 12 (4): 369–384.

Nicolli, F., and F. Vona. 2016. Heterogeneous policies, heterogeneous technologies: The case of renewable energy. Energy Economics 56: 190–204.

Ongan, S., C. Işık, A. Amin, U. Bulut, A. Rehman, R. Alvarado, et al. 2023. Are economic growth and environmental pollution a dilemma? Environmental Science and Pollution Research 30 (17): 49591–49604.

Ozturk, I. 2010. A literature survey on energy–growth nexus. Energy Policy 38 (1): 340–349.

Pata, U.K., and S. Yurtkuran. 2023. Is the EKC hypothesis valid in the five highly globalized countries of the European Union? An empirical investigation with smooth structural shifts. Environmental Monitoring and Assessment 195 (1): 17.

Pedroni, P. 1999. Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics 61 (S1): 653–670.

Pedroni, P. 2004. Panel cointegration: Asymptotic and finite sample properties of pooled time series tests with an application to the PPP hypothesis. Econ Theory 20: 597–625.

Phillips, P.C., and B.E. Hansen. 1990. Statistical inference in instrumental variables regression with I (1) processes. The Review of Economic Studies 57 (1): 99–125.

Ponce, B.J.H., and A.T. Manlangit. 2023. Carbon dioxide emissions and the Environmental Kuznets Curve: evidence from the Association of Southeast Asian Nations. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-023-29370-3.

Rogelj, J., and C.F. Schleussner. 2019. Unintentional unfairness when applying new greenhouse gas emissions metrics at country level. Environmental Research Letters 14 (11): 114039.

Rojas-Downing, M.M., A. Pouyan Nejadhashemi, T. Harrigan, and S.A. Woznicki. 2017. Climate change and livestock: Impacts, adaptation, and mitigation. Climate Risk Management 16: 145–163.

Shahbaz, M., and A. Sinha. 2019. Environmental Kuznets curve for CO2 emissions: A literature survey. Journal of Economic Studies 46 (1): 106–168. https://doi.org/10.1108/JES-09-2017-0249.

Shahbaz, M., M. Zakaria, S.J.H. Shahzad, and M.K. Mahalik. 2018. The energy consumption and economic growth nexus in top ten energy-consuming countries: Fresh evidence from using the quantile-on-quantile approach. Energy Economics 71: 282–301.

Shahbaz, M., H.H. Lean, and M.S. Shabbir. 2012. Environmental Kuznets curve hypothesis in Pakistan: Cointegration and Granger causality. Renewable and Sustainable Energy Reviews 16 (5): 2947–2953.

Shahbaz, M., R. Sharma, A. Sinha, and Z. Jiao. 2021. Analyzing nonlinear impact of economic growth drivers on CO2 emissions: Designing an SDG framework for India. Energy Policy 148: 111965.

Sharif, T., M.M.M. Uddin, and C. Alexiou. 2022. Testing the moderating role of trade openness on the environmental Kuznets curve hypothesis: a novel approach. Annals of Operations Research. https://doi.org/10.1007/s10479-021-04501-6.

Sharma, G.D., A.K. Tiwari, B. Erkut, and H.S. Mundi. 2021. Exploring the nexus between non-renewable and renewable energy consumptions and economic development: Evidence from panel estimations. Renewable and Sustainable Energy Reviews 146: 111–152.

Sikiru, A.B., S.M. Velayyudhan, M.R.R. Nair, S. Veerasamy, and J.O. Makinde. 2023. Sustaining livestock production under the changing climate: Africa scenario for Nigeria resilience and adaptation actions. In Climate change impacts on Nigeria: Environment and sustainable development, 233–259. Cham: Springer International Publishing.

Shang, Y., D. Han, G. Gozgor, M.K. Mahalik, and B.K. Sahoo. 2022. The impact of climate policy uncertainty on renewable and non-renewable energy demand in the United States. Renewable Energy 197: 654–667.

Stern, D.I. 2004. The rise and fall of the environmental Kuznets curve. World Development 32 (8): 1419–1439.

Stern, D.I. 2017. The environmental Kuznets curve after 25 years. Journal of Bioeconomics 19: 7–28.

Stern, D.I., M.S. Common, and E.B. Barbier. 1996. Economic growth and environmental degradation: The environmental Kuznets curve and sustainable development. World Development 24 (7): 1151–1160.

Thornton, P.K., and M. Herrero. 2010. Potential for reduced methane and carbon dioxide emissions from livestock and pasture management in the tropics. Proceedings of the National Academy of Sciences 107 (46): 19667–19672.

Tugcu, C.T., I. Ozturk, and A. Aslan. 2012. Renewable and non-renewable energy consumption and economic growth relationship revisited: Evidence from G7 countries. Energy Economics 34 (6): 1942–1950.

Uzair Ali, M., et al. 2020. CO2 emission, economic development, fossil fuel consumption and population density in India, Pakistan and Bangladesh: A panel investigation. International Journal of Finance & Economics. https://doi.org/10.1002/ijfe.2134.

Van der Werf, G.R., et al. 2010. Global fire emissions and the contribution of deforestation, savanna, forest, agricultural, and peat fires (1997–2009). Atmospheric Chemistry and Physics 10 (23): 11707–11735.

Wang, Q., F. Zhang, and R. Li. 2023. Revisiting the Environmental Kuznets Curve hypothesis in 208 counties: The roles of trade openness, human capital, renewable energy and natural resource rent. Environmental Research 216: 114637.

World Development Indictors, WDI. 2023. https://data.worldbank.org/ Accessed 4th Mar 2023.

Zhang, D., M. Zheng, G.F. Feng, and C.P. Chang, 2022. Does an environmental policy bring to green innovation in renewable energy?. Renewable Energy 195: 1113–1124.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Mohapatra, B.B., Kumari, A., Mohapatra, S. et al. Dynamic Relationship Between Carbon Dioxide Emissions and Gross Domestic Product for Low, Middle- and High-Income Countries. J. Quant. Econ. 21, 873–898 (2023). https://doi.org/10.1007/s40953-023-00369-4

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40953-023-00369-4