Abstract

In this paper we highlight the joint dynamic behavior of three key variables in labor market. Precisely, by means of a structural VAR we employ labor productivity, real wage and unemployment to identify the structural shocks affecting their pattern, in the long and short-run. We will label them as technology, markup and aggregate demand shocks, respectively. The impulse responses of each variable to shocks provide the measure of their (relative) elasticity in explaining the behavior of labor market in six OECD countries, namely Italy, France, Spain, Germany, UK and USA. We find that: (1) the conditional correlations between productivity and real wage are positive for both supply and demand shocks, (2) the impulse responses show a persistent increase of both productivity and real wage to supply shocks, (3) the level of unemployment shows a persistent decrease when hit by a positive demand shock. The main result of our analysis is that Keynesian policies can have permanent effect on the labor market equilibrium.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In this paper we highlight the role of real shocks in explaining the joint dynamic behavior of three key variables in labor market. Precisely, by means of a structural VAR model (hereinafter, SVAR) we use labor productivity, real wage and unemployment to identify the structural shocks affecting their pattern in the long and short-run. We will label them as technology, markup and aggregate demand shocks, respectively. Then, the impulse responses of each variable to shocks provide the measure of their (relative) elasticity in explaining the behavior of labor market for six OECD countries, namely Italy, France, Spain, Germany, UK and USA.

As it is well known, the theoretical relationship among labor productivity, real wages and unemployment is mixed. On the one hand, labor market models which rely on aggregate demand shocks predict procyclical real wages and unemployment (see e.g., Gamber and Joutz 1993). On the other hand, labor market models which rely on aggregate supply shocks predict that aggregate demand shocks have no long run impact on real wages and unemployment (Balmaseda et al. 2000; Blanchard and Johnson 2013; Blanchard and Galì 2007). These conflicting views are also fed by the mixed empirical evidence which suggest that the behavior of real wage and productivity is of little use for distinguishing among competing theories (Gordon 1995). However, to the extent that movements in these variables are produced by supply and demand shocks, the aim of this paper is to identify the structural shocks which impinge upon their dynamics.

The identification of the structural shocks can be achieved by means of alternative methodologies (Enders 2014). Among these, we will follow the one provided by Blanchard and Quah (1989) and other authors (Gamber and Joutz 1993; Clarida and Galì 1994; Balmaseda et al. 2000; Gambetti and Pistoresi 2004; Saltari and Travaglini 2009). Precisely, the identification is achieved by imposing restrictions on the matrix of long-run multipliers of the estimated VAR model in order to interpret the reduced form innovations as structural shocks resulting from different sources. To distinguish among shocks, we will assume that only technology shock affects the stochastic component of labor productivity in the long-run. There is an extensive body of empirical literature that justifies this assumption (Galì 1999; Gamber and Joutz 1993). This literature is also consistent with a large class of theoretical models of labor market (Galì 1999; Blanchard et al. 1997; Saltari and Travaglini 2009; Saltari et al. 2010). Then, as in Gambetti and Pistoresi (2004), and in Blanchard and Johnson (2013), we will assume that the markup shocks will affect the real wages in the long-run. Finally, we identify the demand shocks by imposing the restriction that aggregate demand shocks do not affect the productivity in the long-run, but that aggregate demand shocks have no long-run impact on the growth of real wage (Gamber and Joutz 1993; Saltari et al. 2010; Calcagnini and Travaglini 2014).

Using this identification’s scheme, we provide a simple interpretation of the observed jointly movements in productivity, real wage and unemployment. These movements are consistent with the dynamic properties of a standard Solow’s growth model where technology shocks affect labor productivity in the long-run, and where the long-run component of real wages is driven by productivity and markup shocks, but not from aggregate demand shocks. However, in our model the aggregate demand shocks have permanent effects on the level of unemployment in the long run. Similar results can also be obtained in an insider–outsider framework consistent with the hysteresis assumption (Blanchard and Summers 1986; Balmaseda et al. 2000).

The added value of the present paper lies in three main features. First, our theoretical model provides new insights compared to Balmasseda et al. (2000), and Gambetti and Pistoresi (2004). Precisely, we propose an identification scheme ordered in labor productivity, real wage and unemployment. This ordering is derived from an AD-AS model capturing the main characteristics of the European economies. We show that technology shocks determine the growth rate of the economies through the variation of labor productivity. This is different from Balmasseda et al. (2000) which, using an implicit assumption of continuous equilibrium, employ the real wage to proxy the shocks in technology, for a group of OECD countries. Also, our set up is different from the AD-AS version of Gambetti and Pistoresi (2004) where the aggregate demand is not affected by technology shocks, and where a labor supply function shapes the firms’ behavior as in an insider–outsider model of labor market. Contrariwise, in our model the aggregate demand is (at least partially) affected by technology shocks. These shocks affect both the value of income (in effective units) and the “natural” level of unemployment. As it will become clear below, these assumptions are accepted by the data.

As second point, we extend, on the empirical ground, the period of observation until the more recent years (from 1960 to 2017). The previous literature arrives at most at 1999. Our longer time horizon provides additional information about the heterogeneous impacts of the structural shocks beating the European labor markets. Importantly, the present analysis accounts for how the main European countries and USA react to the same structural shocks, and for how the asymmetric adjustments of any single economy shape costs and benefits of the shared policies. Lastly, our identification scheme is based upon the evidence that the level of unemployment is an I(1) process. The stationary tests confirm this empirical property for all countries under consideration, and provide further elements of novelty compared to the response functions analyzed in the previous papers and their policy implications.

We get three main results. For all countries analyzed in the paper (Italy, France, Spain, Germany, UK and USA) the conditional correlations between productivity and real wage are positive for both supply and demand shocks. Then, the impulse responses show a persistent increase of both productivity and real wage to supply shocks. Finally, the level of unemployment shows a persistent decrease after a positive aggregate demand shock. This latter evidence provides a renewed perspective on the European policies designed to reduce unemployment. Indeed, it poses again the idea that Keynesian policies can have long-lasting effects on the labor market equilibrium, without depressing labor productivity and real wage in the long run. Therefore, our analysis revives the view of the unemployment productivity trade-off schedule (Gordon 1995) and of the possibility that countercyclical demand policies can decreases unemployment without crowding out productivity and real wages in the long run.

The paper is organized as follows. The next section presents a simplified labor market model derived from a modified AD-AS framework. In Sect. 3, we discuss the implementation of the SVAR model, the statistical properties of the variables included in the analysis, and the dynamic features of the impulse response functions. Finally, Sect. 4 concludes with some policy implications.

2 The theoretical model

Our interpretation of the structural shocks is motivated by a Keynesian view of the economy. Our labor market is basically a modified version of the AD-AS model in which real wage is settled one period in advance. Three structural shocks—technology, markup and aggregate demand shocks—affect the movements of the economy. These shocks stems from different sources, namely labor productivity, real wage and unemployment. Importantly, in this paper we intentionally rule out the role of labor market regulation in affecting the observed dynamics of unemployment and productivity. In fact, the most recent literature has already analyzed this point (Daveri et al. 2005; Saltari and Travaglini 2009; Calcagnini et al. 2017). But, less attention has been devoted to study the role of output regulation in affecting unemployment and productivity (Blanchard and Giavazzi 2003). Therefore, our aim is to focus on the relationship between output regulation and economic growth in order to get additional information on the magnitude and sign of the conditional correlation between unemployment and productivity. We believe that our evidence can be useful to qualify the previous findings and to quantify the importance of output regulation in determining the functioning of the European labor markets, and the impact of changes in output regulation on employment and productivity.

The AD-AS model consists of the following five structural equations:

where \(y_{t}\), \(p_{t}\), \(n_{t}\), \(w_{t}\), \(\bar{n}\) denotes respectively the (logs of) labor productivity, price level, employment, nominal wages, full employment. Parameters \(d_{t}\), \(\theta_{t} ,\) \(\mu_{t}\), represent nominal expenditure (reflecting both fiscal and monetary policies), productivity (both technical progress and capital accumulation) and markup shift factors.

Equation (1) is the aggregate demand function. The productivity shock \(\theta_{t}\) is allowed to affect aggregate demand directly through the parameter \(\alpha\). Equation (2) is the aggregate supply function whose changes also depend on the shock \(\theta_{t}\). Then, Eq. (3) is the price setting rule. It is affected by both the productivity and markup \(\mu_{t }\) shocks. Finally, Eqs. (4) and (5) represent the wage setting rule. As in Fischer (1977) and Blanchard and Quah (1989) nominal wages are chosen in the economy one period in advance and are set to achieve (expected) full employment. Hence, Eq. (5) states that wage fluctuations depend both on \(w^{ *}\) as well as on markup and demand shocks (Gambetti and Pistoresi 2004).Footnote 1

To close the model we must specify the stochastic process driving the shift factors \(\theta_{t} ,\) \(\mu_{t} ,\) \(d_{t}\). We assume that these process are pure random walks so that

where \(\Delta\) is the first difference. By assumption the shocks \(\varepsilon_{t}^{s}\),\(\varepsilon_{t}^{\mu } \varepsilon_{t}^{d}\), are uncorrelated i.i.d. disturbances. To solve the system, let’s define unemployment as \(u = \bar{n} - n_{t}\). Then, simple calculation provides the following solution (see Appendix 1):

The system (9)–(11) characterizes the functioning of the underlying labor market. It satisfies our hypotheses about the jointly dynamic variations (\(\Delta )\) of the three variables, labor productivity \((y_{t} - n_{t} )\), real wage \((w_{t} - p_{t} )\) and unemployment \(u_{t}\). Notice that the orthogonality of the shocks, and their causal relationship, strictly depend on the structure of the underlying AD-AS model. Indeed, the estimated reduced form (9)–(11) not only provides the causal relationship among the variables, but also gives the possibility to recover all the information present in the primitive system (1)–(5). In other words, our long-run restrictions allow to identify the underlying structural shocks among the original variables and to solve the identification problem. For example, our model implies that the real wage is affected by the supply shocks \(\varepsilon_{t}^{s}\), and by the markup shocks \(\varepsilon_{t}^{\mu }\). Also, demand side shocks \(\varepsilon_{t}^{d}\) have long-run effect on the level of unemployment \(u_{t}\), but not on the other two variables. So, using a trivariate VAR we can decompose the primitive variables, and recover the three structural shocks. Then, we can test if the data accept our theoretical restrictions. These shocks are used to generate the impulse responses and the variance decomposition of structural shocks.

Further note that, in the long-run, the growth of labor productivity \(\Delta (y_{t} - n_{t} )\) is only driven by technology shocks \(\varepsilon_{t}^{s}\). Then, the growth of real wages \(\Delta (w_{t} - p_{t} )\) is driven by both technology and markup shocks in the long run. Finally, changes in unemployment \(\Delta u_{t}\) are determined by technology, markup, and demand shocks. Therefore, Eq. (11) implies that the level of unemployment \(u_{t}\) is not stationary and the structural shocks may have long-run impact on its “natural” rate.

On the empirical ground, the system (9)–(11) also implies that the matrix \(C(1)\) of the long-run multipliers of the estimated SVAR must be lower triangular to achieve the identification. It can be written as

that is

This system provides the long-run moving average representation of our empirical model, derived from our theoretical assumptions. We will use this specification to identify the structural shocks and the dynamic impacts of these shocks on the growth rates of the three variables under consideration.

3 The empirical model

The first step of our empirical investigation consists in estimating the following three variable VAR system:

where \(X_{t}\) is a vector which includes the variables \([\Delta \left( {y - n} \right),\Delta (w - p),\Delta u]\). \(A(L)\) is a \(k\)th order matrix of lag polynomials in the lag operator \(L\) with all its roots outside the unit circle. \(\delta_{t}\) is a vector of deterministic terms (including a constant), and \(\tau_{t}\) is a vector of zero-mean independent and identically distributed random variables innovations. Omitting the deterministic components of the variables, it is possible to represent \(X_{t}\) as a moving average

Equation (16) is the VAR reduced form. Here innovations (\(\tau_{t} )\) are expressed as linear combinations of the structural shocks \(\tau_{t} = K\varepsilon_{t}\), whose moving-average representation is

The coefficients of \(C(L)\) can be identified by introducing long-run restrictions to determine the matrix \(K\) univocally. Some of these restrictions are obtained by assuming the absence of long-run impact of some shocks on some of the variables under consideration. Assuming that the matrix of long-run multipliers \(C(1)\) is lower triangular, \(K\) can be obtained by estimating the VAR summarized in Eq. (14).

4 Results

We use annual data from the AMECO database covering the period 1960–2016. Labor productivity is computed as (log of) GDP per person employed. The real wage (RW) is the (log of) real compensation per employee. We use total unemployment as defined by Eurostat. The first difference of the (log of) original series provides the growth rates for each variable.

4.1 Stationarity

The stationarity properties of the variables included in the VAR determine the estimation, the impulse responses and the variance decomposition of the SVAR model. To test for stationarity we ran a battery of unit root tests (ADF—Augmented Dickey Fuller; ADF/GLS—Augmented DF with Generalized Least Squares and KPSS—Kwiatkowski–Phillips–Schmidt–Shin). Results are reported in Appendix 2. From the inspection of the data (Tables 1, 2, 3) emerges that all the variables under consideration, and for all the countries, are I(1) processes. This means that the series have at least one unit root. This also implies that to get a robust estimation of the VAR model, the first difference \([\Delta \left( {w - p} \right), \Delta y, \Delta u]\) of the original series is employed to run the empirical analysis. Then, using the cumulated responses of the first differences we can rebuild the variables in level and compute the new steady state of the economy after the shock.

4.2 Impulse responses

Two different VAR specifications have been computed to test for the robustness of the empirical analysis. In the first case (specification 1) a linear trend is removed from the series of the unemployment, and a mean growth shift is removed from the labor productivity and the real wage, after 1979. In the second case (specification 2) we employ the raw data. We use AIC, SC and HQ tests to compute the optimal number of lags. In both scenarios, the dynamic structure of the VAR requires two lags and a constant. Since the two empirical specifications are similar in their dynamic structure and responses we only report here the statistical analysis of specification 2.

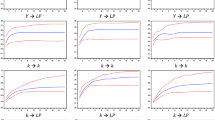

Figures 1, 2, 3, 4, 5 and 6 show the impulse response functions with 90% confidence intervals for technology, markup, and demand shocks of the three variables for our OECD countries under consideration. The black solid line describes the impulse response of any single variable to an initial one-unit shock. Pink area represents the 90% bootstrap confidence interval computed using 1000 bootstrap replications.

Impulse responses for France

Impulse responses for Germany

Impulse responses for Italy

Impulse responses for Spain

Impulse responses for UK

Impulse responses for USA

4.3 Labor productivity

The responses of labor productivity to the structural shocks (technology, markup and aggregate demand) is consistent with our theoretical model. Labor productivity reacts positively to a technology shock at all frequencies, while the responses to the markup and aggregate demand shocks are relevant only in the short-run, but tends to vanishes as time passes. Precisely, a positive technological shock increase labor productivity, reaching the new long-run equilibrium after about 4–6 years. Something different happens in Germany and UK where a moderate movements in the short run and long run emerges from our identification scheme. Importantly, the technology shock permanently affects the growth rate of labor productivity. Then, a negative markup shock immediately decreases labor productivity in Germany and Spain and more gradually in Italy, UK and USA. The initial impact is positive only for France. After the initial negative effect, productivity remains for some years at its minimum level (maximum for France) before go back (in some cases with a cyclical pattern) to its starting level. In the case of Spain, the adjustment to the original level is linear, with productivity gradually recovering after the initial shock. However, the effect of the markup shock vanishes after about 6–10 years. Notably, except for Spain, markup shocks explain only a residual fraction of the overall variance in productivity, less than 5% in the first year and about zero for longer horizons. Finally, a positive aggregate demand shock causes a transitory increase in productivity in all the countries under analysis. Following the initial demand shock the productivity, gradually returns to its initial steady state following a cyclical pattern in the case of Germany, Spain and UK. The impact of demand shocks on the variance of labor productivity in the short run is weak in Germany and Spain, while it appears to be more important in France, Italy, UK and USA. Notice however that for the USA the effect of a positive shock in aggregate demand is relevant in the short run and accounts for slightly less than 40%.

4.4 Real wage

The real wage tends to increase both in the short and long run, in response to a positive technology shock and a negative markup shock. The impulse responses of real wages are similar to that of labor productivity. They react to the initial shocks converging towards the new steady state after about 6–8 years. However, the response of real wage is not as much significant as that of productivity in each period. Further, a technology shock explains the variance of real wage for less than 20% of the total variance in both the short and long run in France and the UK. In the remaining countries we have short-run fluctuations ranging from 20% in Italy and 65% in Spain. In all the countries, except for Spain and Germany, we detect a raising importance of technological shocks in the long run. Notice that the real wage immediately increases also in response to a negative markup shock raising steadily for the first 3–5 years. After about 8–10 periods it reaches the new long-run steady state. Hence, the impact of a markup shock on real wages is permanent and significant. It represents the main source of variation to real wage in both the short and the long run for France and the UK. In the short-run it explains 80% or more of the total variance in France, Italy and the UK, something less in Germany, Spain and USA. In the long-run the explained variance tends to lose importance gradually, following the pattern of their technological shocks. This a common trend for all the countries with the exceptions of Spain and Germany. The effect is particularly marked for the UK where the markup shocks explain nearly 90% of the forecast error variance. Furthermore, it is worth noting that the real wage reacts with a countercyclical behavior (in the short run) in response to a positive demand shock. Afterwards, it gradually returns to its initial level in 4–10 periods, with an adjustment process which is usually cyclical and in some cases hump-shaped. The only exception is the USA where the positive response in the short run is a sign of procyclicality coherent with the findings of Gamber and Joutz (1993) and Balmaseda et al. (2000). All in all, from the analysis emerges that the demand shock is not responsible for real wage variation since the share of explained variance (except for the UK) is almost zero at each horizon.

4.5 Unemployment

After a technology shock the level of unemployment initially increase in the short-run (the first 1–2 years) in France, UK and USA. Then, it shows a sharp decrease towards its new steady state. In the case of Germany and Spain we observe a permanent decrease of unemployment level just in the first periods. The role of technology shocks in explaining the unemployment fluctuation is of small importance since they are responsible for less than 10% in the short-run, and less than 20% in the long-run for the entire sample made exception for Spain. Then, a (negative) markup shock has a positive impact on the level of unemployment in the short run in all the countries under analysis. The most notable aspect is that the decreasing of unemployment in response to a markup shock is permanent even in the long run, with the exception of Spain. Initially, the unemployment level falls below its initial value, reaching a lowest peak after about 1–2 periods. Then, the initial effect tends to vanish and, in about 6–10 years, the unemployment converges (in most of the cases following a cyclical path) towards the new equilibrium whose value is smaller than the initial one. As said, the response to a negative markup shock is different for Spain where, after an initial reduction, the level of unemployment raises steadily. In addition, the effect of a markup shock is negligible in France and Spain, where it is responsible for less than 5% of movements in the short and long-run. More significant is its impact in Germany, Italy and USA where the explained variance is something more than 20% in the short run (12% in the UK) and 10% in the long-run (something less in the UK and Germany). Finally, an aggregate demand shock has a positive and permanent effect on unemployment in all the countries. This fact is consistent with Keynesian theories where the expansion of aggregate demand reduces unemployment. Note however that in the present analysis this happens not only in the short but also in the long run. Unemployment drops immediately and converges towards the new (and smaller) steady state level after 6–10 years. Note that, the demand shock is the main source of fluctuations in unemployment. It accounts from roughly 60–98% of the total variance in the short-run, and approximately 78–90% in the long-run.

4.6 Variance decomposition

The impulse response functions show the effects of structural shocks on the adjustment path of variables in the model. Forecast error variance decompositions measures the contribution of each type of shock to the forecast error variance. Both of these computations are useful in assessing how shocks to economic variables rebound throughout the system. Here the below Figs. 7 and 8 reports the forecast-error variance decomposition of the three variables at various horizons representing years after years the contributions of the shocks to the forecast errors variance of the variables in the VAR.

FEVD for France, Germany and Italy

FEVD for Spain, UK and US

From the variance decomposition we get that technology shocks dominate the labor productivity in the short and in the long-run. In France, Italy, UK and USA an important role is also played by demand shocks in the short-run. The effect of markup shocks on productivity is negligible in most of the countries (Italy and USA), more consistent in others (France and Germany) and has a remarkably effect on Spain and UK.

With regards to real wage, technological shocks accounts in the short-run for less than 20% of the variance in France, UK and Italy and more than 50% for Germany, USA and Spain (where the explained variance is near 65%). In the long-run, it tends to increase everywhere, except for Germany and Spain. In the USA, Germany, Italy and Spain these shocks largely dominate the others in the long run. For all the remaining countries under analysis the variance of real wage is largely explained by the markup shock (in the UK they are near 90%). Aggregate demand shocks are largely insignificant in explaining real wage variance. Only in the case of UK they constitute a negligible share of the variance in the short-run.

Lastly, the variance of unemployment is largely explained by aggregate demand shocks in the short and long-run. They contribute to its fluctuations from 60 to 98% in the short-run, and 78–90% in the long-run. In France, Germany, Italy and the UK the role of aggregate demand is particularly relevant. Markup shocks are especially important for the UK, USA and partially for Italy where they constitutes a consistent part of the variance. The same kind of shock is less relevant to explain the variance of unemployment in France and Spain. Finally, technology shocks are relevant for explaining the variance of unemployment in Spain and USA. But, the same shocks are less important in Italy where their contributions to the unemployment fluctuation is significantly lower than the other shocks.

4.7 Concluding remarks

In this paper we assess the impact of the jointly dynamic responses of productivity, real wages, and unemployment to three structural shocks—namely technology, markup and aggregate demand—for five European countries and the USA, during the period 1960–2017. The structural shocks are identified by imposing long-run restrictions to the multipliers of the estimated VAR model. The restrictions are derived from a modified version of the AD-AS model in which real wage is settled one period in advance. The empirical results are coherent with the main implications of our theoretical model.

A (positive) technology shock raises productivity and real wages both in short and the long run. It also reduces the level of unemployment in the long run. A (negative) markup shock decreases productivity growth only in the short-run, but permanently reduces the level of unemployment. Hence, institutional changes in output markets can raise employment without modifying labor market regulation (Blanchard and Giavazzi 2003). Finally a (positive) aggregate demand shock decreases unemployment in the long run, without negative effects on productivity and real wage. These outcomes are consistent with the Keynesian view according to which the level of employment also depends on aggregate demand, not only on changes in technology and relative prices.Footnote 2

The empirical results of our analysis depend on the stationarity properties of the variables included in the empirical model (Lastrapes 2002). Their patterns are coherent with the implications of our AD-AS model. Further, our findings are in line with the more recent literature on this topic. Precisely, Gambetti and Pistoresi (2004) show that positive demand shocks can reduce the level of unemployment in the long run, and significantly affect productivity and real wage in the short run. This result is certainly in contrast with the technology bias hypothesis, and the view that aggregate demand expansion can slowdown economic growth in the long run (Marchetti and Nucci 2001). In fact, we do not detect negative impact of aggregate demand shock on technology and real wage in the long run. Furthermore, in our model a negative markup shock has a positive long-run impact on the real wage and a negative long-run impact on unemployment. This is detected not only for Italy (as in Gambetti and Pistoresi 2004) but also for the other main European countries and the USA. Finally, positive technology shocks increase productivity growth and real wage with an elasticity close to one in the long run, and reduces significantly the level of unemployment. This latter result is different from that of Gamber and Joutz (1993) where technology shocks do not affect unemployment in the long run. This finding depends on the non-stationarity of the unemployment time series. Of course, this fact also suggests the importance of labor market elasticity and its variation around the business cycle (Giersch 1985).

Some policy implications can be derived from our findings. First of all, aggregate demand policies can raise steadily the level of employment. This would suggest some rethinking of the European authorities on the austerity policies implemented over the last 10 years. Expansionary fiscal and monetary policies may have long lasting effect on the level of employment without crowding out productivity and real wage. Then, the deregulation policies in output market may positively affect the unemployment in the long run. Finally, technology progress and investment can increase both productivity and real wages in the long run. We believe that these findings should be enhanced to shoot down unemployment in European countries. In other words, demand side policies should go hand in hand with supply side policies to reduce European unemployment.

Some issues are left out from the present analysis. As said above, we do not study how changes in labor market regulations affect the level of unemployment. And we do not analyze how these changes affect technology and investments. In fact, a large literature on this topic exists, and provides heterogeneous results. On one hand, a stricter labor regulation may raise the adjustment costs of both labor and capital, decreasing innovation and investment. On the other hand, it may stimulate firms to invest and innovate to recover productivity and profits in the long run. This is a controversial issue (Calcagnini et al. 2017). However, to investigate the issue a helpful strategy would be to add new variables in our model. But, a problem with this type of decomposition is that there are many types of shocks; and, as it is recognized by Blanchard and Quah (1989), the SVAR approach is limited by its ability to identify at most only as many types of shocks as there are variables. In addition, the explanatory power of the additional structural shocks can be very small. For all these reasons, in this paper we preferred to investigate and identify a trivariate model. And for the same reasons, the inclusion in our framework of additional variables (e.g. the Employment Protection Legislation index to capture the tightness of the labor market) is left for our future research.

5 Appendix 1

Let’s start from Eq. (4). It states that wages are set so that \(E_{t - 1} N_{t} = \bar{N}.\) Rearranging (2) for \(n_{t}\) and substituting into (4) we obtain

Plugging (3) into (1) and factoring out \(\theta_{t}\) we get

Then substituting (20) into (19) yields

Which can be rewritten as

Now, since \(W_{t}\) is set one period in advance, it is not a random value in (t − 1). Therefore, we can use this expression to get:

Then, differencing (20) and using the first difference of (23) we obtain:

Finally, from Eqs. (1), (2) and (3) we can easily recover \({\text{N}}_{t}\) and then differencing to obtain:

Thus, combining \(\Delta y_{t}\) and \(\Delta n_{t}\) we get:

In the same way, differencing (5) and using the difference version of (3):

6 Appendix 2

6.1 Tests for unit roots

Notes

Following the literature (i.e. in Fischer 1977; Blanchard and Quah 1989; Enders 2014; Calcagnini et al. 2016) we use a structural VAR in discrete time to test our theoretical model. This is a standard procedure. The empirical analysis in continuous time is left for future research (for example, Federici et al. 2012).

Ball et al. (1999) shows that monetary and fiscal can have long-run effects on the level of unemployment.

References

Ball, L., Mankiw, N. G., & Nordhaus, W. D. (1999). Aggregate demand and long-run unemployment. Brookings Papers on Economic Activity, 1999, 189–251.

Balmaseda, M., Dolado, J. J., & López-Salido, J. D. (2000). The dynamic effects of shocks to labour markets: Evidence from OECD countries. Oxford Economic Papers, 52, 3–23.

Blanchard, O., & Galí, J. (2007). Real wage rigidities and the new Keynesian model. Journal of Money, Credit and Banking, 39(s1), 35–65.

Blanchard, O., & Giavazzi, F. (2003). Macroeconomic effects of regulation and deregulation in goods and labor markets. The Quarterly Journal of Economics, 118(3), 879–907.

Blanchard, O. J., & Johnson, D. R. (2013). Macroeconomics (6th ed.). Boston: Pearson.

Blanchard, O. J., Nordhaus, W. D., & Phelps, E. S. (1997). The medium run. Brookings Papers on Economic Activity, 2, 89–158.

Blanchard, O. J., & Quah, D. (1989). The dynamic effects of aggregate demand and supply disturbances. The American Economic Review, 79, 655–673.

Blanchard, O. J., & Summers, L. H. (1986). Hysteresis and the European unemployment problem. In S. Fischer (Ed.), NBER macroeconomics annual 1986 (Vol. 1, pp. 15–90). Cambridge: MIT Press.

Calcagnini, G., Giombini, G., & Travaglini, G. (2016). Modelling energy intensity, pollution per capita and productivity in Italy: A structural VAR approach. Renewable and Sustainable Energy Reviews, 59, 1482–1492.

Calcagnini, G., Giombini, G., & Travaglini, G. (2017). A Schumpeterian model of investment and innovation with labor market regulation. Economics of Innovation and New Technology, 18, 1–24.

Calcagnini, G., & Travaglini, G. (2014). A time series analysis of labor productivity. Italy versus the European countries and the US. Economic Modelling, 36, 622–628.

Clarida, R., & Gali, J. (1994). Sources of real exchange-rate fluctuations: How important are nominal shocks? Carnegie-Rochester Conference Series on Public Policy, 41, 1–56.

Daveri, F., Jona-Lasinio, C., & Zollino, F. (2005). Italy’s decline: Getting the facts right. Giornale degli Economisti e Annali di Economia, 64, 365–421.

Elliott, G., Rothenberg, T. J., & Stock, J. H. (1992). Efficient tests for an autoregressive unit root. NBER Technical Working Papers 0130, National Bureau of Economic Research, Inc.

Elliott, G., Rothenberg, T. J., & Stock, J. H. (1996). Efficient tests for an autoregressive unit root. Econometrica, 64(4), 813–836.

Enders, W. (2014). Applied econometric time series (4th ed.). New York: Wiley.

Federici, D., Saltari, E., Clifford, R. W., & Giannetti, M. (2012). Technological adoption with imperfect markets in the Italian economy. Studies in Nonlinear Dynamics & Econometrics, 16(2), 1–30.

Fischer, S. (1977). Long-term contracts, rational expectations, and the optimal money supply rule. Journal of Political Economy, 85(1), 191–205.

Fuller, W. A. (1996). Introduction to statistical time series. New York: Wiley.

Gali, J. (1999). Technology, employment, and the business cycle: Do technology shocks explain aggregate fluctuations? American Economic Review, 89(1), 249–271.

Gamber, E. N., & Joutz, F. L. (1993). An application of estimating structural vector autoregression models with long-run restrictions. Journal of Macroeconomics, 15(4), 723–745.

Gambetti, L., & Pistoresi, L. (2004). Policy matters. The long run effects of aggregate demand and markup shocks on the Italian unemployment rate. Empirical Economics, 29(2), 209–226.

Giersch, H. (1985). Eurosclerosis. No. 112. Kieler Diskussionsbeiträge.

Gordon, R. J. (1995). Is there a tradeoff between unemployment and productivity growth?. Cambridge: National Bureau of Economic Research.

Kwiatkowski, D., Phillips, P., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics, 54(1–3), 159–178.

Lastrapes, W. D. (2002). Real wages and aggregate demand shocks: Contradictory evidence from VARs. Journal of Economics and Business, 54(4), 389–413.

Marchetti, D. J., & Nucci, F. (2001). Unobserved factor utilization, technology shocks and business cycles. No. 392. Bank of Italy, Economic Research and International Relations Area.

Saltari, E., & Travaglini, G. (2009). The productivity slowdown puzzle. Technological and non-technological shocks in the labor market. International Economic Journal, 23(4), 483–509.

Saltari, E., Travaglini, G., Wymer, C. R. (2010). Investment, productivity and employment in the Italian economy. The Economics of Imperfect Markets (Physica-Verlag HD), 7, 113–136.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Travaglini, G., Bellocchi, A. How supply and demand shocks affect productivity and unemployment growth: evidence from OECD countries. Econ Polit 35, 955–979 (2018). https://doi.org/10.1007/s40888-018-0127-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40888-018-0127-1