Abstract

The study applies a BEKK GARCH-M model to examine the effect of uncertainty on the levels of inflation and output growth in Nigeria. The results suggest a significant positive effect of inflation uncertainty on the level of inflation, supporting the Cukierman and Meltzer (Econometrica 54(5):1099–1128, 1987) hypothesis. In addition, uncertainty about inflation is found to be detrimental to output growth, supporting the Friedman’s (J Political Econ 85(3):451–472, 1977) hypothesis as it connotes greater risk to investment. Uncertainty about growth does not have a significant effect on both the levels of inflation and output growth. The evidence suggests the need to minimize inflation uncertainty to avoid its adverse effects on the economy by treating positive oil price shocks as temporal. In addition, the need to build domestic buffers through structural reforms to diversify the economy cannot be overemphasized in Nigeria.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Monetary Policy stance in Nigeria has always been contractionary in a bid to combat rising inflation and ensure sustainable output growth as the economy is exposed to global commodity price shock due to undiversified economic activities. This has called for concern from stakeholders on the need for policy stance to support real sector growth, especially in a low growth era but the monetary authority always argues that the Nigerian case is a paradox where output growth is low and dwindling amidst rising inflation and alarming unemployment rate (CBN 2015; Eregha 2021). It is therefore imperative for empirical study to gauge the dynamic linkages among inflation, output growth, and their uncertainties in Nigeria to provide evidence for policymakers. This is the focus of this study and to the best of our knowledge, there is dearth of such studies in Nigeria.

In Nigeria, the oil sector’s contribution to GDP hovers around 10.0% while non-oil sector contributes a significant 90.0%. Paradoxically, the same non-oil sector that contributes this significant share in domestic production only accounts for less than 10.0% of export earnings while the oil sector takes a lead of approximately 90.0% (Eregha et al. 2019). Also, fiscal position depends so much on oil revenue as the government often treats positive oil price shock as permanent. Thus, the economy is susceptible to global uncertainties and terms of trade shock that affect the fiscal position and impact on domestic prices. This is aggravated by supply constraints resulting in rising cost of production and a crowding-out effect on private investment as public debt rises uncontrollably (DMO 2018; Eregha et al. 2016). Consequently, real growth has been fragile hovering on an average of roughly 2.0% prior to 2020 amidst a population growth of around 3.0% (DMO 2018). This characterizes both real and nominal uncertainties and the imperativeness to empirically underscore the dynamic relationship among real output growth, inflation, and their uncertainties in Nigeria.

Interestingly, the dynamic linkages between inflation and output growth and their uncertainties have been controversial both theoretically and empirically (Bhar and Malik 2010). While there is a plethora of studies on these connections, the consensus in the literature is unclear and the evidence is mixed (Narayan and Narayan 2013). Theoretically, Friedman (1977) and Ball (1992) showed that rising inflation causes nominal uncertainty which invariably becomes a drag to output growth due to price distortionary effect that engenders inefficient resource allocation. However, Pourgerami and Maskus (1987) opined for a negative effect. They suggested that rising inflation only leads to a decrease in inflation uncertainty as economic agents utilize more resources in forecasting future inflation.

Cukierman and Meltzer (1987) and Holland (1995) provided support for the reverse causality running from nominal uncertainty to inflation as policymakers create surprise inflation to spur growth. On the effect of inflation uncertainty, while Friedman (1977) supported a negative effect on output growth, Dotsey and Sarte (2000) opined for a positive effect, arguing that increasing nominal uncertainty may cause precautionary savings that later boost investment and thereby spur growth. On the effect of real uncertainty, Black (1987), and Blackburn (1999) suggested a positive effect on output growth, while Pindyck (1990), and Ramey and Ramey (1991) supported a negative effect, and Friedman (1968) suggesting that there should be independence between output growth and its uncertainty.

On the effect of real uncertainty on inflation, Devereux (1989) showed a positive effect, and on the relationship between inflation uncertainty and output growth uncertainty, Taylor (1981) and Fuhrer (1997) showed a trade-off between them due to stabilization objective of the policymaker, while Logue and Sweeney (1981) insinuated a positive effect of growth uncertainty on inflation uncertainty. On inflation-growth nexus, Bruno and Easterly (1998) provided support for a positive effect, while Jones and Manuelli (1995), De Gregorio (1996), supported a negative link.

From the empirical literature, Grier and Perry (1998), Bhar and Malik (2010), Mehrara and Tavakolian (2010), Hasanov and Omay (2011), Heidari et al. (2013), and Narayan and Narayan (2013) showed empirical evidence supporting rising inflation to spur inflationary uncertainty. On the other hand, Karanasos et al. (2004), Narayan and Narayan (2013), and Ndoricimpa (2015) showed inflation uncertainty to raise inflation while Grier et al. (2004) found otherwise. Fountas (2001); Fountas et al. (2002) and Heidari et al. (2013) found evidence of a drag on growth from inflation uncertainty, Ndoricimpa (2015) found a spurring effect on growth. Caporale and Mckiernan (1998), Grier and Perry (2000) and Narayan and Narayan (2013) found a positive effect of real uncertainty on growth but Henry and Olekalns (2002), and Ndoricimpa (2015) found a negative correlation while Fountas et al. (2002) found no evidence.

The literature is replete with mixed and imprecise results (Bhar and Malik 2010) and Heidari et al. (2013) called for more studies. Thus, this study contributes to the literature on the connection between nominal uncertainty and real uncertainty and their effects on inflation and output growth for Nigeria by using the Grier et al. (2004) asymmetric multivariate GARCH-M modeling approach for generating uncertainty as also used by Ndoricimpa (2015) for the South Africa case. This is at variance with previous studies, especially in Nigeria that used the one-step approach in GARCH-in-Mean model (Olayinka and Hassan 2010). While Bhar and Malik (2010) and Heidari et al. (2013) among others employed this same approach but this present study is significant as it focuses on the Nigerian economy that is characterized by fragile real growth and dwindling inflationary trend due to terms of trade shock and supply constraints to unravel the dynamics for similar economies. The choice of the Grier et al. (2004) asymmetric multivariate GARCH-M approach is not farfetched as it allows one to jointly generate the uncertainty measures of inflation and output growth and analyzed their effects simultaneously while overcoming the misspecification problem arising from imposing diagonal and symmetric restrictions on the variance–covariance matric of output growth and inflation. The rest of the paper is organized thus. Section 2 highlights the methodology used; Sect. 3 presents the empirical analysis while Sect. 4 concludes the study.

Methodology

To examine the effects of uncertainty on the levels of inflation and output growth in Nigeria, this study follows Grier et al. (2004) and applies a BEKKFootnote 1 GARCH-M model in which the conditional means of inflation (\(\pi_{t}\)) and output growth (\(y_{t}\)) are in form of VARMA (Vector Autoregressive Moving Average) GARCH-M model, where the conditional standard deviations of output growth and inflation are included as explanatory variables in each conditional mean equation. The methodology was also applied by Ndoricimpa (2015) for the case of South Africa. The specification of the conditional means of inflation (\(\pi_{t}\)) and output growth \((y_{t} )\) is as follows:

with \(\varepsilon_{t} |\Omega_{t} \; \sim \;N\left( {0,H_{t} } \right)\), where \(\Omega_{t}\) represents the information set available at time t. In addition, \(\left( {\varepsilon_{y,t}^{2} } \right) = h_{y,t}\), \(\left( {\varepsilon_{\pi ,t}^{2} } \right) = h_{\pi ,t}\), \(E\left( {\varepsilon_{y,t} \varepsilon_{\pi ,t} } \right) = h_{y\pi ,t}\).

where \((83) \, Cov( - \pi ,r_{m} ) = Var(\pi ) - Cov(\pi ,R_{m} )\) is the conditional variance–covariance matrix, \(R_{m}\) is the conditional variance of output growth, \((Cov( - \pi ,r_{m} ))\) is the conditional variance of inflation, \((Cov(\pi ,R_{m} ))\) are the conditional covariances between inflation and output growth, \(E_{t}\) is the vector of error terms, \(E_{t}^{*}\) is the matrix of constant terms, \((84) \, N_{t} = E_{t} - E_{t - 1} = \lambda (E_{t}^{*} - E_{t - 1} ) = \lambda \eta_{t} - \lambda (E_{t - 1} - E_{t - 1}^{*} )\) is the matrix of Autoregressive coefficients, \(\lambda\) is the matrix of in-mean coefficients and \(\eta_{t}\) is the matrix of Moving Average coefficients. Important to note is that in GARCH models, uncertainty (volatility) is captured by the conditional variance which is simply the variance of the one-step ahead forecasting error.

To avoid the problem of misspecification, this study first considers an asymmetric BEKK model where the conditional variance–covariance matrix is written as:

where \(C = \left[ {\begin{array}{*{20}c} {c_{yy} } & 0 \\ {c_{\pi y} } & {c_{\pi \pi } } \\ \end{array} } \right];A = \left[ {\begin{array}{*{20}c} {\alpha_{yy} } & {\alpha_{y\pi } } \\ {\alpha_{\pi y} } & {\alpha_{\pi \pi } } \\ \end{array} } \right];B = \left[ {\begin{array}{*{20}c} {\beta_{yy} } & {\beta_{y\pi } } \\ {\beta_{\pi y} } & {\beta_{\pi \pi } } \\ \end{array} } \right];D = \left[ {\begin{array}{*{20}c} {\delta_{yy} } & {\delta_{y\pi } } \\ {\delta_{\pi y} } & {\delta_{\pi \pi } } \\ \end{array} } \right];\omega = \left[ {\begin{array}{*{20}c} {\omega_{y,t} } \\ {\omega_{\pi ,t} } \\ \end{array} } \right]\).

In Eq. (2), C is a lower triangular matrix of constant terms, A is a matrix of ARCH coefficients which captures the ARCH effects and B is a matrix of GARCH coefficients capturing the GARCH effects. The diagonal elements in matrix A show the impact of own past shocks on the current conditional variance, the diagonal elements in Matrix B represent the impact of own past volatility on the current conditional variance, while the off-diagonal elements in matrices A and B represent the volatility spillovers’ effects (Xu and Sun 2010). Asymmetry in the conditional variance–covariance matrix is captured by the matrix D which is the matrix of asymmetric coefficients. The BEKK model becomes symmetric if asymmetric coefficients are statistically jointly equal to 0, i.e. \(\delta_{ij} = 0\), for all \(i,j = y,\pi\).

Equation (2) can also be written as follows:

From Eq. 1 (the conditional mean equations), the effect of uncertainty on the level of inflation and output growth can be examined. The effect of output growth uncertainty and inflation uncertainty on output growth can be assessed by respectively testing the null hypotheses that \(\psi_{yy} = 0\) and \(\psi_{y\pi } = 0\). A positive and significant \(\psi_{yy}\) would mean a positive effect of output growth uncertainty on output growth (Black hypothesis), while a negative and significant \(\psi_{yy}\) would imply a negative effect of output growth uncertainty on output growth, supporting the views of Pindyck (1990) and Ramey and Ramey (1991). A positive and significant \(\psi_{y\pi }\) would mean a positive effect of inflation uncertainty on output growth (Dotsey–Sarte hypothesis), while a negative and significant \(\psi_{y\pi }\) would mean a negative effect of inflation uncertainty on output growth [Friedman (1977) hypothesis].

Similarly, testing the effect of uncertainty, nominal and real, on the level of inflation is conducted by respectively testing whether \(\psi_{\pi y} = 0\) and \(\psi_{\pi \pi } = 0\). A positive and significant \(\psi_{\pi y}\) would imply a positive effect of output growth uncertainty on inflation (the Devereux hypothesis) while a negative and significant \(\psi_{\pi y}\) would imply a negative effect of output growth uncertainty on inflation. On the other hand, a positive and significant \(\psi_{\pi \pi }\) would mean a positive effect of inflation uncertainty on inflation (Cukierman-Meltzer hypothesis), while a negative and significant \(\psi_{\pi \pi }\) would mean a negative effect of inflation uncertainty on inflation [the stabilization hypothesis of Holland (1995)].

Empirical results and discussion

Quarterly data on inflation and output growth for Nigeria are used for the period 1986:1 to 2017:4. Data were obtained from the Central Bank of Nigeria. The choice of the period of study is due to data availability. This also captures the period Nigeria introduced the Structural Adjustment Programme where prices and interest rates were deregulated. Summary statistics in panel A of Table 1 show that inflation, \(\pi\) is positively skewed while output growth, \(y\) is negatively skewed. However, both variables display leptokurtic behavior. Non-normality of the two variables is confirmed by Jarque–Bera (1987) test. A look at the variance shows that inflation is more volatile than output growth.

We conduct some tests, including unit root test and ARCH test, before any further analysis. Unit root test is conducted to assess the order of integration of the series, while ARCH test helps checking for the evidence of conditional heteroscedasticity in the data, that is, whether the variances of the series are time-varying. As Grier and Perry (1998) point out, one should be able to reject the null hypothesis of constant variance before estimating a GARCH model and generate uncertainty measures. The DF-GLS test which was developed by Elliott et al. (1996), is used to test for unit root in the series. It first transforms the time series via a generalized least squares (GLS) regression before performing the unit root test. Elliott et al. (1996) have shown that DF-GLS test has significantly greater power than the previous versions of the augmented Dickey–Fuller test. We also use other two tests accounting for breaks in the series, suggested by Zivot and Andrews (1992), and Clemente et al. (1998). Indeed, Bai–Perron breakpoint test (see, Table 2) suggests the presence of 2 breaks in both series, inflation and output growth.

DF-GLS test (see Panel B, Table 1) rejects the null hypothesis of a unit root in inflation and output growth series. Unit root tests accounting for breaks (see Table 3) reach also the same conclusion. Inflation and output growth series are hence stationary processes; there is, therefore, no need to difference them when estimating the mean equations. Testing for the presence of ARCH effects in the series is done using LM-ARCH test of Engle (1982). ARCH test (see Panel B, Table 1) suggests that inflation and output growth series exhibit significant volatility clustering, implying that the variances of inflation and output growth are not constant but time-varying.

Since the presence of ARCH effects is confirmed, we proceed to estimate our asymmetric BEKK GARCH-MFootnote 2 model. The estimation results are in Table 4. To assess the adequacy of the GARCH model estimated, that is, to check whether the conditional mean and the conditional variance–covariance equations are well specified, we apply the usual diagnostic tests on GARCH models, Ljung–Box test and McLeod-Li test. The results in Panel C of Table 4 show that at 5% level, Ljung–Box test indicates that there is no serial correlation of 5th and 10th order in the standardized residuals of the inflation mean equation. In contrast, the same test rejects the null hypothesis of no serial correlation of 5th and 10th order in the standardized residuals of the output growth mean equation, which can question the adequacy of the output growth mean equation, although the multivariate Q variant test seems to reject the null hypothesis of no serial correlation. Similarly, McLeod–Li test indicates that the squares of the standardized residuals of inflation and output growth equations are also serially independent at 5% level, implying that there are no remaining ARCH/GARCH effects.

In addition, we conduct some coefficient restriction tests in the Mean equation and conditional variance–covariance equations, to check whether some of the coefficients are not redundant (see Table 4, panel B). In this regard, we test for the hypotheses of diagonal VARMA, no GARCH, no GARCH-M, no asymmetry, and diagonal GARCH. The results show that all the hypotheses are rejected at 1% significance level, except for the hypotheses of no asymmetry and diagonal GARCH. Rejecting the hypothesis of no GARCH confirms that the conditional variance–covariance matrix is heteroscedastic, that is, the conditional variances of inflation and output growth are time-varying. Coefficient restriction tests confirm that the form of the mean equation adopted (Vector Autoregressive Moving average, VARMA plus the in-mean coefficients included) properly captures the dynamics of inflation and output growth, but that the form of the conditional variance–covariance matrix adopted (asymmetry and non-diagonality) does not adequately capture the dynamics of the conditional variance of inflation and output growth. The results point rather to a more simplified model where the conditional variance–covariance matrix is symmetric and diagonal. Consequently, we re-estimate the mean and conditional variance–covariance equations by considering symmetry and diagonality. The estimation results are in Table 5, and the diagnostic tests (see, Panel C) indicate that the conditional mean and conditional variance–covariance equations are well specified. Indeed, Ljung–Box test indicates that there is no serial correlation of 5th and 10th order in the standardized residuals from the mean equations. Similarly, McLeod–Li test indicates that the squares of the standardized residuals are also serially independent at 5 percent, implying that there are no remaining ARCH/GARCH effects.

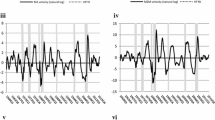

The derived conditional standard deviations of inflation and output growth capturing inflation uncertainty and output growth uncertainty are in Fig. 1.

Inflation uncertainty and output growth uncertainty for Nigeria

Figure 1 indicates that inflation uncertainty (volatility) was prevalent in the 1980s and 1990s, but it has however been moderate since around 1995. The greatest output growth uncertainty was also recorded in the 1980s and early 1990s. These volatile trends to both inflation and real growth can be attributed to the response of the economy to the introduction of the structural adjustment program and oil price shocks through terms of trade shock as the country deregulate interest rates and move away from fixed exchange rate system. On average, inflation uncertainty seems to have been higher than output growth uncertainty. The uncertainty about inflation arise more in these periods as the economy was hit by unprecedented negative exogenous commodity price shock and lack of policy synergy to curtail the situation. The reason is not farfetched as Nigeria always treats positive oil price shock as permanent experience hence, in periods of negative price shock; it becomes difficult to ensure fiscal discipline leading to pro-cyclicality instead of counter-cyclicality of fiscal response.

Next, we focus on the objective of the study which is to examine the effect of uncertainty, nominal and real, on the levels of inflation and output growth in Nigeria.

The estimation results in Table 5 (panel A) suggest a positive and significant effect of inflation uncertainty on the level of inflation (the null hypothesis that \(\psi_{\pi \pi } = 0\) is rejected at 1% level), with an estimated coefficient of inflation uncertainty equal to \((\psi_{\pi \pi } = 1.043)\). This supports hence the Cukierman–Meltzer hypothesis. Indeed, Cukierman and Meltzer (1987) argue that an increase in inflation uncertainty leads to an increase in the level of inflation as policymakers create surprise inflation to stimulate output. Our findings on the relationship between the level of inflation and its uncertainty, contradict those of Bamanga et al. (2016) and Hegerty (2012) that supported the Friedman’s hypothesis. We find however that output growth uncertainty does not significantly affect the level of inflation (the null hypothesis that \(\psi_{\pi y} = 0\) cannot be rejected even at 10% level). This is contrary to Devereux (1989)’s prediction of a positive effect of output growth uncertainty on the level of inflation. According to Devereux (1989), more uncertainty about output growth causes a reduction in the optimal amount of wage indexation and induces the policymaker to engineer more inflation surprises. Suffice to say that this is best applied for more developed countries with proper wage indexation to price changes.

Regarding the effect of inflation uncertainty on output growth, the results indicate a robust significant effect of inflation uncertainty (the null hypothesis that \(\psi_{y\pi } = 0\) is rejected at 1%). The coefficient of inflation uncertainty in the output growth means equation, is negative, equal to \(\psi_{y\pi } = - 0.055\). This suggests a negative effect of inflation uncertainty on output growth in Nigeria, supporting the Friedman’s (1977) hypothesis. Indeed, inflation uncertainty creates greater risk for savers and investors, distorting hence their decisions to save or to invest as well as reducing the efficiency of resource allocation (Holland 1995). As Friedman (1977) points out, inflation uncertainty renders the market prices system less efficient for coordinating economic activity. And according to Fischer and Modigliani (1978), inflation uncertainty leads to the change in the pattern of asset accumulation and the shortening of contracts, reducing hence the rate of investment by firms. It should be noted that Idowu and Hassan (2010) reached the same conclusion for Nigeria, but Odim et al. (2015) concluded a positive effect of inflation uncertainty on output growth.

On the effect of real uncertainty, the results suggest an insignificant effect of output growth uncertainty on output growth (the null hypothesis that \(\psi_{yy} = 0\) fails to be rejected even at 10% level), supporting Friedman’s (1968) hypothesis of an independent relationship between the two variables. According to Friedman (1968), output fluctuations around its natural rate are due to price misperceptions in response to monetary shocks, whereas changes in the growth rate of output arise from real factors such as technology. The proponents of the independent relationship between output growth uncertainty and output growth argue that output growth and its business cycle component (uncertainty) can be decomposed into two distinct components, which can then be analyzed separately.

The analysis of elements in matrices A and B gives the following intuition. The diagonal elements in Matrix B, \(\beta_{yy}\) and \(\beta_{\pi \pi }\) are statistically significant (\(\beta_{\pi \pi }\) is significant at 5% level, while \(\beta_{yy}\) is significant at 10% level), implying that own past volatility (uncertainty) affects the conditional variances of inflation and output growth in Nigeria. In addition, the results show that \(\alpha_{\pi \pi }\) in the diagonal elements in Matrix A is statistically significant at 10% level, suggesting that own past shocks affect the conditional variances of inflation.

Causality tests and impulse response functions

To confirm the findings obtained with the BEKK GARCH-M Model, Granger causality tests and analysis of impulse response functions are used. In Granger causality testing, different lags are used as in previous studies in this area (see, for instance, Fountas and Karanasos 2007; Bhar and Malik 2010). Granger causality test results (see, Table 6) confirm the findings of the BEKK GARCH-M Model. Inflation uncertainty is found to Granger-cause the level of inflation with a positive-sum of the lagged coefficients; similarly inflation uncertainty Granger causes output growth with a negative sum of the lagged coefficients. We also find independence relationship between the level of inflation and output growth uncertainty, as well as between output growth and growth uncertainty. Causality tests further give other insights into the relationship among the variables. An increase in the level of inflation causes an increase in inflation uncertainty; and output growth increase causes a reduction in inflation uncertainty and growth uncertainty.

Generalized impulse response functions obtained from a VAR model of inflation (INF), output growth (GR), inflation uncertainty (INFUNC), and growth uncertainty (GRUNC), are reported in Fig. 2. They confirm that inflation uncertainty increases the level of inflation although the effect seems to be minor. They also confirm that a shock in inflation uncertainty has an effect on output growth and that a shock in growth uncertainty does not have an effect on output growth. An increase in output growth reduces inflation uncertainty and growth uncertainty, while an increase in the level of inflation increases growth uncertainty.

Generalized impulse response functions

Concluding remarks

The study examines the effect of real and nominal uncertainties on inflation and output growth in Nigeria using a BEKK GARCH-M model suggested by Grier et al. (2004) and interesting findings are established. First, the results support the Cukierman and Meltzer (1987) hypothesis of a positive effect of inflation uncertainty on the level of inflation. This implies that inflation uncertainty impedes on investment decisions as that results in real output decline. The aftermath effect is to spur domestic prices to climb as supply falls. Second, uncertainty about inflation was found to be detrimental to output growth, supporting the Friedman’s (1977) hypothesis. The intuition is through divestment to cause a drag on real output growth as inflation uncertainty connotes risks to investors to hold back investment decisions. Finally, real growth uncertainty does not have a significant effect on both the levels of inflation and output growth. This intuition is that inflation and real output growth dynamics are not associated with expectation about domestic real growth uncertainty in Nigeria. As an oil-dependent economy, real and nominal uncertainties are attributed to the economy’s exposure to exogenous external shock than domestic factors. This is because oil price shocks affect the fiscal position directly that causes a drag on real output growth while at the same time affecting domestic prices through terms of trade shock. Thus, it is imperative for the government not to treat positive oil price shock as permanent and also build domestic buffers through structural reforms to engender economic diversification along revenue and export earnings.

Notes

BEKK model is a multivariate GARCH model developed by Engle and Kroner (1995) and was named after Baba, Engle, Kraft and Kroner. BEKK model is preferred in this study because it ensures the positive definiteness of the conditional variance–covariance matrix unlike the other variants of multivariate GARCH models.

In estimating the mean equation, we consider p = q = 1 and the diagnostic tests confirm that the mean equation is well specified with that lag order.

References

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Econom 8(1):1–22

Ball L (1992) Why does high inflation raise inflation uncertainty? J Monet Econ 29(3):371–388

Bamanga M, Musa U, Salihu A, Udoette US, Adejo VA, Edem ON, Bukar H, Chidinma T (2016) Inflation and inflation uncertainty in Nigeria: a test of the Friedman’s hypothesis. CBN J Appl Stat 7(1):147–169

Bhar R, Malik G (2010) Inflation, inflation uncertainty and output growth in the USA. Physica A 389(23):5503–5510

Black F (1987) Business cycles and equilibrium. Basill Blackwell, New York

Blackburn K (1999) Can stabilization policy reduce long-run growth? Econ J 109(452):67–77

Bruno M, Easterly W (1998) Inflation crises and long-run growth. J Monet Econ 41:3–26

Caporale T, McKiernan B (1998) The Fischer black hypothesis: some time-series. South Econ J 64(3):765–771

CBN (2015). The Central Bank of Nigeria Communique No. 104 of the Monetary Policy Committe. November. Abuja. CBN

Clemente LJ, Montañés A, Reyes M (1998) Testing for a unit root in variables with a double change in the mean. Econ Lett 59(2):175–182

Cukierman A, Meltzer A (1987) A theory of ambiguity, credibility, and inflation under discretion and asymmetry information. Econometrica 54(5):1099–1128

De Gregorio J (1996) Inflation, growth and central banks: theory and evidence. Policy research working papers, 1575, The World Bank

Devereux M (1989) A positive theory of inflation and inflation variance. Econ Inq 27(1):105–116

DMO (2018) Nigeria’s Debt Management Office Annual Report and Statement of Accounts. Abuja. Debt Management Office

Dotsey M, Sarte PD (2000) Inflation uncertainty and growth in a cash-in-advance economy. J Monet Econ 45:631–655

Elliott GR, Rothenberg TJ, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64:813–836

Engle RF (1982) Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50:987–1006

Engle RF, Kroner KF (1995) Multivariate simultaneous generalized ARCH. Econom Theor 11(1):122–150

Eregha PB (2021) Asymmetric response of CPI Inflation to exchange rates in oil-dependent developing economy: the case of Nigeria. Econ Chang Restruct. https://doi.org/10.1007/s10644-021-09339-3

Eregha PB, Ndoricimpa A, Olakojo S, Nchake M, Nyangoro O, Togba E (2016) Nigeria: should the government float or devalue the Naira? Afr Dev Rev 28(3):247–263

Eregha PB, Vincent O, Osuji E (2019) The economics of growth fragility in Nigeria. Working papers 19/061, European Xtramile Centre of African Studies (EXCAS)

Fischer S, Modigliani F (1978) Towards an understanding of the real effects and costs of inflation. Rev World Econ Weltwirtschaftliches Arch 114(4):810–833

Fountas S (2001) The relationship between inflation and inflation uncertainty in the UK 1885–1998. Econ Lett 74:77–83

Fountas S, Karanasos M (2007) Inflation, output growth, and nominal and real uncertainty: empirical evidence for the G7. J Int Money Financ 26:229–250

Fountas S, Karanasos M, Kim J (2002) Inflation and output growth uncertainty and their relationship with inflation and output growth. Econ Lett 75:293–301

Friedman M (1968) The role of monetary policy. Am Econ Rev 58(1):1–17

Friedman M (1977) Nobel lecture: inflation and unemployment. J Political Econ 85(3):451–472

Fuhrer JC (1997) Inflation/output variance trade-offs and optimal monetary policy. J Money Credit Bank 29(2):214–234

Grier KB, Perry MJ (1998) On inflation and inflation uncertainty in the G7 countries. J Int Money Finance 17:671–689

Grier KB, Perry MJ (2000) The effects of real and nominal uncertainty on inflation and output growth: some GARCH-M evidence. J Appl Econom 15:45–58

Grier KB, Henry OT, Olekalns N, Shields K (2004) The asymmetric effects of uncertainty on inflation and output growth. J Appl Econom 19:551–565

Hasanov M, Omay T (2011) The relationship between inflation, output growth, and their uncertainties: evidence from selected CEE countries. Emerg Mark Finance Trade 47(3):5–20

Hegerty SW (2012) Does high inflation lead to increased inflation uncertainty? Evidence from nine African countries. Afr Econ Bus Rev 10(2):196–221

Heidari H, Katircioglu ST, Bashir S (2013) Inflation, inflation uncertainty and growth in the Iranian economy: an application of BGARCH-M model with BEKK approach. J Bus Econ Manag 14(5):819–832

Henry OT, Olekalns N (2002) The effect of recessions on the relationship between output variability and growth. South Econ J 68(3):683–692

Holland AS (1995) Inflation and uncertainty: tests for temporal ordering. J Money Credit Bank 27(3):827–837

Idowu OK, Hassan Y (2010) Inflation volatility and economic growth in Nigeria: a preliminary investigation. J Econ Theory 4(2):44–49

Jones LE, Manuelli RE (1995) Growth and the effects of inflation. J Econ Dyn Control 19:1405–1428

Karanasos M, Karanassou M, Fountas S (2004) Analyzing US inflation by a GARCH model with simultaneous feedback. WSEAS Trans Inf Sci Appl 1(2):767–772

Logue DE, Sweeney RJ (1981) Inflation and real growth: some empirical results: note. J Money Credit Bank 13(4):497–501

Mehrara M, Tavakolian H (2010) Inflation, growth and their uncertainties: a bivariate GARCH evidence for Iran. Iran Econ Rev 15(1):83–100

Narayan PK, Narayan S (2013) The inflation-output nexus: empirical evidence from India, Brazil, and South Africa. Res Int Bus Finance 28:19–34

Ndoricimpa A (2015) Inflation, output growth and their uncertainties in South Africa: empirical evidence from an asymmetric multivariate GARCH-M model. Appl Econom 39(3):5–17

Odim OU, Ugbe SN, Ifeanyi OM (2015) Inflation uncertainty and output growth in Nigeria. J Res Humanit Soc Sci 3(1):32–41

Olayinka KI, Hassan Y (2010) Inflation volatility and economic growth in Nigeria: a preliminary Investigation. J Econ Theory 4(2):44–49

Pindyck R (1990) Irreversibility, uncertainty and investment. NBER working paper series, working paper no. 3307.

Pourgerami A, Maskus KE (1987) The effects of inflation on the predictability of price changes in Latin America: some estimates and policy implications. World Dev 15(2):287–290

Ramey G, Ramey VA (1991) Technology commitment and the cost of economic fluctuations. NBER working paper series, working paper no. 3755

Taylor JB (1981) On the relation between the variability of inflation and the average inflation rate. In: Cornegie-Rochester conference series on public policy, vol 15, pp 57–86

Xu Y, Sun Y (2010) Dynamic linkages between China and US equity markets under two recent financial crises, Unpublished Master’s dissertation, Lund University, School of Economics and Management

Zivot E, Andrews D (1992) Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J Bus Econ Stat 10(3):251–270

Funding

The study receives no funding from any organization.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interests

There are no competing or coflicting interests regarding the submission.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Earlier version of the article is published as working papers: European Xtramile Centre of African Studies Working Paper 19/060 & African Governance and Development Institute Working Paper 19/060.

Rights and permissions

About this article

Cite this article

Eregha, P.B., Ndoricimpa, A. Inflation, output growth and their uncertainties: some multivariate GARCH-M evidence for Nigeria. J. Soc. Econ. Dev. 24, 197–210 (2022). https://doi.org/10.1007/s40847-022-00177-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40847-022-00177-1