Abstract

Italy’s recent upward trend in the real effective exchange rate (REER) combined with a remarkable decreasing market share has instigated a lively economic debate on the relevance of price factors in shaping export performances. In parallel, concerns about Italy’s weak export competitiveness have been raised in connection to the Eurozone imbalance issue. In this framework, the aim of this paper is to investigate empirically the role of price competitiveness in determining Italy’s export flows, namely the sensitivity of exports to REER dynamics. For this purpose, we undertake an econometric investigation (a cointegration analysis from 1994 to 2014 to estimate jointly the long-run export elasticities to the foreign demand and the REER) conducted on the basis of five price and cost competitiveness indicators (i.e., alternative deflator-based REERs), also taking into account the role of non-price competitiveness factors. Moreover, we disentangle the export elasticities by clustering intra-Eurozone and global flows (both in values and in volumes). Besides assessing the remarkable importance of price competitiveness (the long-run export elasticity to export price-based REER is about − 1.3 for Eurozone flows and − 1.7 for global flows), some robustness tests confirm the absence of significant changes in the price elasticity of exports with regard to the two sub-periods pinpointed by the inception of the Euro. Furthermore, we conduct a sectoral study to determine whether some industries outperform others in terms of export elasticities. The sectoral breakdown indicates that manufacturing and machinery, which together account for 75% of Italian exports, show the highest REER elasticities, albeit with a sizeable impact of non-price factors (particularly for exports of manufactured goods towards the Eurozone). We conclude by drawing some implications from our findings for the current policy debates.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Much speculation about an unhealthy Italian productive system has been raised in recent years, mainly due to the question of external imbalances within the Eurozone combined with an appreciable decrease in Italy’s export market share. In this regard, the economic debate has focused on the alleged weak competitiveness of the so-called Euro area ‘periphery’, within which the consensus view (Bayoumi et al. 2011; Giavazzi and Spaventa 2010; Sinn 2012; Wolf 2011)—substantially endorsed by policy makers (European Commission 2009, 2010)—is generally as follows: (1) the currency union has led to a generalised decrease in interest rates, which has caused increasing and unsustainable private and public indebtedness in peripheral countries; (2) the debt growth has fostered both the domestic and the external demand, which has contributed to boosting the relative prices vis-à-vis other EMU members, especially the so-called ‘core’ countries; (3) the inflation has curbed the export growth in peripheral countries, leading to the creation of persistent external deficits; and (4) the trade deficits depend on the weak competitiveness of peripheral countries, and, within a fixed exchange rate regime, they should be corrected through an internal devaluation journey (that is, by means of lower prices and wages).Footnote 1

Within this framework, it is widely recognised that ‘while Italy’s competitiveness does appear to have eroded, the size of this effect is, frankly, anyone’s guess’.Footnote 2 Specifically, the topic of Italian competitiveness—and more generally of Eurozone deficit countries—has been discussed generously by both mainstream authors, focused on the analysis of productivity-adjusted price indexes (Blanchard 2007; Dieppe et al. 2012; Gaulier and Vicard 2013), and non-mainstream authors,Footnote 3 among whom some scholars have considered price competitiveness as being significantly relevant in shaping Italy’s export flows (Bagnai 2012a; Cesaratto and Stirati 2011).Footnote 4 Besides, other authors have recognised that the competitive advantage of Eurozone surplus countries (especially Germany) depends on non-price competitiveness factors,Footnote 5 namely the product quality, upgraded export baskets, a complete production matrix and export diversification (see Felipe and Kumar 2011). According to this view, intra-EMU price differentials would be ‘only part of the explanation of the disequilibria with a much greater role being played by the composition of exports (…): it is the quality of exports that needs to be improved’ (Simonazzi et al. 2013, p. 671), and therefore greater price competitiveness would not ensure export recovery in deficit countries, especially in Italy, where ‘residual factors, which partly reflect non-price economic restructuring, have supported Italy’s real exports after 2005’ (Lissovolik 2008, p. 1).

Due to the topicality of this issue, as well as its relevance in terms of policy, our contribution intends to develop the existing empirical research, which is to a certain extent still fragmentary, by studying the determinants of Italy’s trade performance and linking the latter to price competitiveness. This involves measuring export elasticities to alternative deflator-based REERs by taking into account the foreign demand dynamics and non-price competitiveness factors, for both total and sectoral exports (10 industries, according to the Standard International Trade Classification) in value and in volume, by distinguishing intra-Eurozone and global flows. Moreover, by means of proper quantitative tools, we aim to provide evidence about the stability of the size of export elasticities within the whole sample under investigation (from 1994 to 2014), particularly with reference to the EMU sub-period individually. Finally, since we consider competitiveness as a structural issue, we conduct an econometric analysis that endorses a long-term perspective; in detail, an error correction methodology (ECM) allows us to estimate jointly the ‘background magnitude’ of Italian export elasticities to price competitiveness and foreign income.

The remainder of this paper is structured as follows. Section 2 provides a general overview of Italian competitiveness in terms of trade flows and their relationships with price competitiveness indicators. Section 3 contains a literature review on trade elasticities, with a particular focus on export elasticities to the REER. Then, Sect. 4 presents the econometric part of the paper, in which we (i) indicate the methodology, (ii) specify the empirical model and (iii) identify sources and dataset creation criteria. Section 5 presents and discusses our findings. Finally, Sect. 6 concludes and draws some implications for current policy debates.

2 A Bird’s-Eye View of Italian Competitiveness

The debate regarding Italy’s weak external competitiveness mainly resulted from two institutional reports that shed light on the existence of current account imbalances within the Eurozone (European Commission 2009, 2010).Footnote 6 In this regard, the analysis of a country’s external performance is usually based on price competitiveness, which is proxied by the real effective exchange rate (REER); the latter is a widespread trade-weighted indicator that represents the dynamics of domestic prices relative to foreign ones through inflation-adjusting nominal exchange rates—different deflators representing prices and costs can be used alternatively for its computation. As far as Italy is concerned, the empirical evidence indicates that the market share losses are actually related to growing indicators of relative prices; as shown in Fig. 1, the decrease in Italy’s market shares is combined with an increase in the REER (i.e., with decreasing price competitiveness), although further factors should be taken into account when analysing export performance, for example foreign demand patterns, non-price competitiveness, international competition and so forth.

Source: Elaboration on WTO and European Commission

Italy’s market shares (ratio of Italy export to global trade flows, bars, left scale) and price competitiveness dynamics; HCPI-based REER in dashed and export price-based REER in solid, right scale, 2005 = 100.

Nevertheless, the Italian case becomes worthy of attention when the external sector is studied in depth. Particularly, after 2000, Italy’s current account balance was negative, and then it turned positive in 2013. To understand which components contributed the most to drawing this path, let us start with the composition of the current account, the shares in the GDP of which are reported in Table 1. According to the data, the Italian current account balance returned to positive mainly due to a decrease in the importing of goods, the value of which dropped by 10% from 2011 to 2013 (while the GDP decreased by 2%). The exporting of goods, however, of which the annual average growth was 2% in this biennium, contributed to a lesser extent than the collapse of imports. Moreover, it is possible to notice that Italy’s trade balance was already positive in 2012 (1.1% of the GDP); therefore, the current account balance was negative due to other components. Finally, in 2014 and 2015, exports of goods experienced far more pronounced growth (+ 3.5% yearly average), combined with a mild recovery of imports (+ 1%).

However, the import and export flows show sizeable differences if we examine the breakdown between intra- and extra-Euro area trade. For this purpose, Fig. 2 indicates the Italian export share of the GDP, which is disentangled into flows towards the Eurozone (EU_11) and other partners (NO_EU); Fig. 3 proposes similar clusters for the import share of the GDP.Footnote 7 With regard to exports, the NO_EU flows have been growing markedly in recent years (over 15% of the GDP), while the Eurozone flows are stable at around 8% of the GDP. As a matter of fact, the increase in the total export share experienced in Italy during the last decade mostly depended on trade outside the Euro area—although the GDP drop after 2007 has to be considered.Footnote 8 Moreover, the NO_EU export share surpassed the EU_11 share suddenly after 1992, as a sign that the Lira devaluation was related to greater extra-EU trade openness.

Source: Elaboration on Eurostat

Italy’s exports of goods (% GDP).

Source: Elaboration on Eurostat

Italy’s imports of goods (% GDP).

As far as imports are concerned, the NO_EU share exceeded the EU_11 share close to 2000. Both ratios exhibit an upward trend, the NO_EU one being significantly steeper (presumably due to imports of energy goods). This juxtaposition appears to be consistent with the idea that the onset of the Euro should have stimulated Italian imports from extra-Eurozone countries due to the appreciated domestic currency. Moreover, the EU_11 import share has remained quite constant since 2011, while the NO_EU import share has dropped by 2% of the GDP; that is, the extra-Eurozone imports have decreased to a greater extent than the GDP.

Finally, regarding the balance of goods, we can observe that the recent Italian trade surplus (2014) derived from a huge extra-Eurozone surplus, whereas a small deficit was experienced in the EU_11. To summarise, the intra-Eurozone trade balance was positive from 1993 to 1998, and then it was persistently negative. On the contrary, the extra-Eurozone trade balance has been positive for most of the time. In some respects, this empirical evidence could be consistent with the price competitiveness argument, and in this framework the real appreciation caused by the EMU may have hampered Italy’s exports within the Euro area. As already stated, the most widespread metric for price competitiveness is the REER, of which increases—caused by currency appreciation or by an increase in relative prices—are generally intended as a loss of price competitiveness (and vice versa), which may lead to a decrease in exports. Figure 4 shows the Italian real effective exchange rate dynamics (CPI-based, 2010 = 100) vis-à-vis 42 global industrialised countries, overlapped by the export and import total flows (of which the annual volumes are listed in Table 2, in parallel with the trade balance and the aforementioned REER). Moreover, in Table 3 we report some Pearson correlations that were calculated for the changes in the REER and the annual growth rate of trade flows—respectively, exports, imports and trade balance.Footnote 9

Source: Elaboration on Eurostat

Italy’s trade flows (solid, billions of 2005 USD) and price competitiveness (dashed, 2010 = 100).

Source: Elaborations on European Commission

Italy’s global export shares (average, minimum and maximum 1994/2014; red bars refer to EU11, green bars to IC37, blue bars to BG4.

During the whole sample under investigation (from 1979 to 2014), export growth was negatively correlated with the REER dynamics (− 0.46), and the correlation was higher (− 0.59 on average) for sub-periods. In addition, although the import growth rate was not strongly correlated with the changes in the REER (0.14), two considerations emerge for sub-periods. Firstly, the strongest correlation (0.47) was registered from 1992 to 1999; this could be related to the Lira depreciation, which, according to the price competitiveness argument, may have stemmed imports. Secondly, from 2000 to 2014, we observe a negative correlation (− 0.40) combined with real appreciation; however, this could be feasible in light of the fact that the so-called ‘income effect’ (that is, endemic GDP growth and a subsequent import slowdown) could have exceeded the so-called ‘price effect’ during this period. Finally, the correlation between the trade balance and the REER was negative and quite high (− 0.56), even though we observe the lowest coefficient (− 0.23) from 2000 to 2014. In addition to the Pearson coefficients (which indicate only the tendency to covary), some preliminary indications of exports’ sensitivity to price factors are identified in Table 4 by regressing (OLS) the annual export growth rates on the REER dynamics (from 1979 to 2014).Footnote 10

Obviously, the real exchange rate dynamics themselves are not sufficient to explain export variability to a large extent (the regression R-square is 0.214), since the flows also depend on the foreign demand; however, the price elasticity is negative and highly significant (β1 = − 0.57). With this point in mind, as all the preliminary tests highlight the relevance of price competitiveness factors to Italy’s exports, it is still interesting to determine whether alternative deflators used in the REER calculation lead to dissimilar results. In this regard, Table 5 indicates the correlation between the Italian annual export growth rate (in volume) and the yearly REER dynamics based, in turn, on five price/cost indexes, namely:

-

1.

the harmonised consumer price index (HCPI), which ensures comparability among countries’ baskets of goods;

-

2.

the unit labour cost (ULC), a widely used metric for cost competitiveness that compares wages with productivity;

-

3.

the unit wage cost (UWC), namely the unit labour cost in the manufacturing sector of the economy, exclusively;

-

4.

the GDP deflator, which accounts for inflation by converting the total output from current into constant prices;

-

5.

the export price index, which tracks the average changes in the prices of exported goods and services.

According to the data, from 1994 to 2014Footnote 11 export growth was remarkably related to the UWC-based REER (− 0.65) and the export price-based REER (− 0.52), while the REERs based on price indexes referring to the whole economy (the HCPI, GDP deflator and ULC) exhibit a lower correlation with exports.Footnote 12

Even in this case, in addition to the Pearson correlations, some early indications of exports’ sensitivity to different price and cost competitiveness metrics are provided by linear regression of the annual export growth on the real effective exchange rate’s yearly variations (Table 6).Footnote 13 As already stated, the REER itself does not explain exports to a great extent: however, the price elasticities of exports—which were estimated using, in turn, five alternative deflator-based REERs—show negative coefficients and are statistically significant. More specifically, the highest coefficient of elasticity (− 1.25) is indicated by the export price-based REER.

Summing up, this introductory overview of Italy’s trade seems to suggest that export dynamics and the balance of goods are more related to the REER than imports.Footnote 14 However, the analyses carried out thus far are basically descriptive, and more sophisticated statistical tools should be used for estimating long-run price and income elasticities simultaneously. In this regard, in the following sections, an econometric model—inspired by a European Commission report—will take into account suggestions deriving from this preliminary analysis of the relevance of price competitiveness to Italy’s exports. More specifically, we will investigate the export elasticities to different deflator-based REERs (which will allow us to distinguish flows by groups of trading partners) as well as with respect to value and volume flows. Let us now examine the literature on this topic to choose an appropriate methodology for our research question.

3 Literature Review

There is a large amount of quantitative literature discussing the determinants of Italy’s trade performance and linking the latter to price competitiveness—that is, attempting to estimate empirically the export elasticity to the real exchange rate. Despite the econometric results being quite mixed, a widespread consensus has emerged on the use of so-called ‘export equations’ as a tool for trade elasticity estimation. To put it simply, export equations try to explain a country’s total or sectoral export variability by simultaneously considering the foreign demand dynamics and the impact of price competitiveness.

With respect to the Eurozone imbalance issue, even institutional analysis has recently made use of this approach. Specifically, through the estimation of a cross-country export equation, the European Commission (2010) argued that Italy lost 4.7% of its export market share from 1999 to 2008 and that this was caused (despite the export annual growth rate being 2% on average) by the real appreciation.Footnote 15 This report clearly stated that Italian exports can be considered to be very sensible to price competitiveness. In fact, notable differences in price elasticities are observable among countries; the data suggest that the same real appreciation would lead Italy—in the long term—to a decrease in exports that is about twice that of Germany.Footnote 16 In detail, the trade elasticities (vs. 60 countries) were estimated by means of an ECM with reference to the period 1980–2000; while the foreign demand coefficients are quite similar (1.08 for Italy and 1.03 for Germany), the export price-based REER elasticity is − 1.72 for Italy and − 0.73 for Germany.

Cointegration-based estimates for export equations were also used by the IMF (Allard et al. 2005), referring to Italy, France, Germany and Spain. On the basis of this analysis, Germany’s exporting of goods was hampered by real appreciation to a lesser extent than Italy’s, and this is reflected in the ULC-based REER elasticities, which are − 0.32 for Germany and − 0.70 for Italy. Moreover, it was argued that the foreign demand and price competitiveness explain the great variability of Italian exports for 1980–2004, while on the contrary the so-called ‘residual factors’ became more significant for 2001–2004.Footnote 17

A further attempt to estimate long-run export elasticities for the whole Eurozone (not on a cross-country basis) was made by the IMF (Bayoumi et al. 2011) through a panel analysis that considered export equations with a variety of deflators, as well as a breakdown in intra- and extra-Eurozone partners: it was claimed that intra-EMU trade is more sensitive to the REER (price elasticity range from − 0.7 to − 1.3) than extra-EMU flows (− 0.1 to − 0.3), and this difference has increased since the onset of the Euro. With respect to the Italian case, it was argued that price competitiveness seems to have worsened during recent years, although different considerations can be put forward for various deflators (in particular, the CPI-based REER shows modest dynamics since 1995, while the ULC and export unit values indicate dramatic real appreciation, ranging from 50 to 110%).

The ECB recently made the only effort to examine the determinants of intra- and extra-Eurozone exports on a cross-country basis (Bobeica et al. 2016), in which standard export equations were estimated (from 1995 to 2013) with respect to five harmonised competitiveness indexes—the HCI based on the PPI, CPI, GDP deflator, ULC and UWC (i.e., ULC in manufacturing), computed by the ECB on the basis of the same methodology and data sources as the REERs—by means of cointegration. The results indicate that price competitiveness is a relatively more important driver of exports outside the Euro area than within the EMU; in particular, Italy’s flows towards non-EMU countries are quite sensitive to the UWC-based HCI (− 0.87), whereas the elasticities to competitiveness indicators regarding the total economy (namely the CPI, GDP deflator and ULC) appear to be more relevant to intra-Euro area exports (ranging from − 0.39 to − 0.58).

An empirical investigation that considered alternative deflator-based REERs was conducted by the Bank of Italy (Giordano and Zollino 2014) by means of cointegration of export equations with respect to four large Euro area countries from 1993 to 2012. According to this analysis, Italy’s export elasticities to the REERs are significantly higher than those of Germany, France and Spain (about − 0.55 for basic price indexes), while productivity-adjusted cost competitiveness metrics—specifically the ULC and UWC—indicate the lowest values of responsiveness. Moreover, an augmented model that takes account of non-price competitiveness (proxied by total factor productivity) was estimated in this research: the relative TFP dynamics proved to be significant, although the REER elasticities were almost unchanged when non-price factors were considered.

Similar analyses based on export equations have been proposed by scholars. Among others, Bagnai and Mongeau Ospina (2014) estimated long-run trade elasticities by means of cointegration within a medium-sized annual econometric model of the Italian economy (from 1960 to 2013): the REER elasticity of Italian exports is − 1.27 vs. the Eurozone core, − 1.92 vs. the Eurozone periphery, − 1.52 vs. other EU countries and − 1.03 vs. the US, while the foreign demand elasticities range from 1.37 vs. BRICs to 3.69 vs. the US. Moreover, Algieri (2015) considered non-price factors within export elasticity estimations (1978–2011), despite the fact that they were included in the form of a stochastic trend (i.e., not as specific exogenous variables); on this basis, the estimated price elasticity is − 0.8 while the non-price elasticity is − 2.9.

Furthermore, the following contributions assessed Italy’s price competitiveness, although they did not estimate trade elasticities specifically. Belke and Dreger (2011) stated that price competitiveness is more relevant than income growth in determining trade imbalances within the Eurozone; therefore, realignment in ULCs—through internal devaluation of the periphery—would be necessary. Moreover, according to Comunale and Hessel (2013), price competitiveness differentials are of course relevant within the Euro area while income dynamics (even stimulated by credit) are the main determinants of intra-Eurozone CA imbalances.

On the basis of this review, we can assert that export equations can be considered as an appropriate tool to answer our research question. Summing up, a general consensus on the relevance of price competitiveness to Italy’s exports seems to have emerged from both institutional and academic contributions due to the fact that the long-run REER elasticities are higher for Italy than for its competitors (especially Germany) while the foreign demand elasticities appear to be similar among Euro area countries.

As anticipated in the introductory section, however, the research on this topic presents some gaps, which this empirical work will try to fill. More specifically, given the just-quoted literature studying the determinants of Italy’s trade performance and linking it to price competitiveness, our contribution aims to improve and expand the existing studies in three main directions. Firstly, as we noted a substantial lack of sectoral investigations (or at least industry-based empirical research), we perform a sector-disaggregated analysis to ascertain whether some industries outperform others in terms of export elasticities. Secondly, a clear distinction between intra-Eurozone and global exports is not so widespread within the existing literature, although this would be interesting in the light of recent internal devaluation policies in the peripheral countries of the Euro area; for this purpose we clearly disentangle export elasticities by clustering intra-Eurozone and global flows. Thirdly, the main focus of our attention in this study is to check the feasible developments in Italy’s price elasticity with respect to the adoption of the Euro, which will also be used for the sake of model stability. To cope with these issues simultaneously, in the rest of the paper, the empirics will involve Italy’s export equations from 1994 to 2014—on both values and volume export flows—which aim at jointly estimating the long-run export elasticities (total and sectoral) to foreign demand and price competitiveness with respect to both Euro area and global trade, by controlling for a proxy for non-price competitiveness and for the EMU structural break (1999).

4 Methodology, Model Specification and Dataset

4.1 Methodology

As argued in the previous section, export equations are designed to represent the relationship between a country’s export flows and some factors that are able to influence them according to economic theory. Turning to the empirics, exports are generally (in the baseline version) a function of the foreign demand and the real effective exchange rate, and this equation is usually expressed in ln–ln form to consider income and price elasticities, respectively. However, the analysis of time series economic data usually involves dealing with non-stationary variables and/or cointegrated processes; accordingly, long-term export elasticity estimations should be conducted by means of a proper methodology that allows the detection of the dynamic relationships. In this regard, in addition to verifying integration and cointegration, preliminary empirical tests on series were conducted.Footnote 18 Firstly, through an augmented Dickey–Fuller test, we verified the presence of a unit root (i.e., non-stationarity). Secondly, the optimal lag length analysis was performed by minimising the Akaike information criterion on the basis of a VAR model.Footnote 19 Thirdly, in accordance with the results above, a Johansen multivariate test (Johansen 1988) was conducted to determine whether the series were cointegrated. In the case that the series were long-run correlated, we would be able to represent the whole cointegrated processes by means of an ECM, as suggested by Engle and Granger (1987). We opted for this methodology as the cointegrating equation,Footnote 20 if any, provides information about the long-run relationships among variables, whilst alternative techniques (that is, those that exploit only variables’ first differences) just allow the estimation of short-term relationships.Footnote 21 Consistently, in the case that the series were proved to be I(1) and cointegrated, we applied the ECM—as stated by Granger (1988)—and the long-run export elasticities would be expressed by the coefficients within the cointegrating equation (EC), as in the Johansen (1988) multivariate cointegration.

4.2 Model Specification

In accordance with both the methodology and the research goal, we defined our export Eq. (1)—each of which includes the cointegrating equationFootnote 22 (2)—as follows:

with:

where X indicates Italy’s exports at time t towards a specific cluster of partners (for the sectoral analyses, we used Xj with j = 0, …, 9); FDt is a proxy for the foreign demand, expressed by Italy’s trading partners’ export-weighted GDP; REERt indicates the real effective exchange rate (based on alternative deflators) relative to each specific cluster of partners; and L represents the highest number of lags considered within the estimations. It is appropriate to clarify that the specified model draws its inspiration from the institutional research undertaken by the European Commission (2010); specifically, although we referred to different export flows (in terms of periods and partners) and considered an alternative—to some extent more sophisticated—proxy for foreign demand,Footnote 23 we used the same methodology for the estimates of export elasticities (namely, the ECM). Accordingly, the coefficients within the cointegrating equation (EC) can be interpreted as long-run elasticities due to the ln–ln form, with respect to the total (Xt) and sectoral exports (X jt ), alternatively. Since a decline in the REER (i.e., increasing price competitiveness) and/or a rise in the foreign demand is supposed to foster export growth, we expect a positive relationship between X and FD (hence a positive γ1) and an inverse relationship between X and REER (hence a negative γ2). Moreover, EC should be interpreted as the temporary deviation of exports from the long-term cointegration relationship, which is expected to be zero in the long run, while its coefficient (α) should be statistically significant to validate the existence of a long-run relationship.Footnote 24

Notably, it can be argued that trade flows might not depend solely on the price competitiveness and foreign demand: as pointed out in previous sections, non-price competitiveness can be relevant in shaping Italy’s export performance, and this can arouse concerns about the model specification of the European Commission (2010)—especially with respect to omitted explanatory variables. To overcome this issue, we opted to take into account the role of non-price factors within the VAR specification (1) as a control variable.Footnote 25 Specifically, in the spirit of the augmented model specification advanced by Giordano and Zollino (2014), we considered total factor productivity as a proxy for non-price competitiveness: this set of factors, among which are innovation, product quality, technological edge, diversification and specialisation, is often considered to be able to ‘affect a country’s export performance alongside price competitiveness’.Footnote 26 Accordingly, to detect the effect of non-price factors as well, we control the export equations for the economy-wide total factor productivity pattern, regarded as a proxy for efficiency; in this framework, increasing TFP is supposed to improve external competitiveness and consequently to enhance exports.Footnote 27 However, it should be noted that we do not control for TFP dynamics when we estimate the long-run export elasticities to productivity-adjusted price competitiveness indicators (i.e., ULC- and UWC-based REERs) to avoid obvious endogeneity biases.Footnote 28

Finally, as far as model stability and robustness are concerned, as suggested by Bayoumi et al. (2011), we considered a dummy variable within Eq. (1) to control for a feasible structural break: in addition to the Euro’s inception, the use of this temporal dummy can be considered as grounded from a statistical standpoint on the basis of a Chow test that was conducted with regard to the two sub-periods under investigation. However, in the robustness section, we carefully test the robustness of our results to the non-inclusion of the dummy variable and to the EMU sub-period only (from 1999 to 2014).

4.3 Dataset Creation

To estimate the Italian export elasticities, we referred to EU Trade Since 1988 by SITC (the Eurostat Comext database) for data on total and sectoral exports (monthly, from 1994 to 2014, quarterly converted and seasonally adjusted when required), which is unbundled according to the Standard International Trade Classification. Moreover, we queried data according to trading partners; we first downloaded series about Italian exports toward the EU11 aggregate, and then we extended the selection to a broader number of partner countries (see Table 7). In detail, we distinguished them into intra-Eurozone and global flows by proposing export equations with respect to the EU11, IC37 and BG42 consistently with the REER’s availability. For the sake of clarity, it is useful to point out that an investigation exclusively referring to extra-Eurozone flows cannot be conducted for data accessibility reasons; specifically, Italy’s REER series are available only vs. the Eurozone (EA), the European Union (EU28), the group of ‘industrialised’ countries (IC37) and the broader group of ‘advanced’ countries, which also includes emerging economies (BG42). Moreover, it should be noted that the IC37 and BG42 include intra-Euro area trade; hence, an investigation of extra-Eurozone flows only would not be performable in our empirical framework (see Table 8 for the share of each cluster in Italy’s total exports). Technically, since Italian exports are expressed in current Euros, we used the data as they are for the ‘value analysis’, whilst the ‘volume analysis’ was achieved by deflating Italy’s export flows with the quarterly GDP deflator.Footnote 29

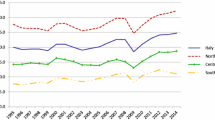

Furthermore, the foreign demand series (FD_EU11, FD_IC37 and FD_BG42) were constructed on the basis of partner countries’ GDPs from the OECD.Stat national quarterly accounts with respect to the EU11 (millions of Euros, current and constant 2010, seasonally adjusted), IC37 and BG42 (millions of PPP dollars, current and constant 2010). In the spirit of the provided literature on the determinants of trade performance involving export equations, we constructed a foreign demand variable by weighting the GDPs of trading partners using Italy’s export shares towards each cluster,Footnote 30 the composition of clusters being determined consistently with the REER availability. Moreover, for extra-Eurozone flows, we converted the foreign demand into Euros using quarterly USD/EUR exchange rates for the sake of comparability with the Italian export flows.Footnote 31 As keenly discussed within the descriptive analyses, our econometrics made use of Italian price and cost competitiveness indicators, specifically five alternative real effective exchange rates, which were adjusted by a variety of deflators (namely the HCPI, ULC, UWC, GDP deflator and export prices). Italy’s quarterly REERs from 1994 to 2014—the dynamics of which are plotted in Fig. 6 (from 6.1 to 6.11)—were provided by the European Commission on the basis of different clusters of trading partners; more specifically, we selected REER vs. EA for the EU11 analysesFootnote 32 and REER vs. IC37 and REER vs. BG42 for the global export flows.Footnote 33 Finally, Italy’s TFP series, used as a proxy for non-price competitiveness, was provided by Ameco (see Fig. 6.12) and referred to the total economy.

Italy’s price and non-price competitiveness (2010 = 100): REERs based on five deflators vs. different partner groups (source: European Commission) and TFP (source: Ameco, code: ZVGDF). Note: REERs are quarterly data. Ameco TFP series is yearly based, then we intra-yearly interpolated by considering its annual dynamics to be equally distributed in each quarter

5 Empirical Findings

On the basis of the identified methodology, the specified model and the dataset creation criteria, this section reports and discusses the results of our estimations, that is, the long-run export elasticities indicated by the cointegrating equations, when a long-run relationship among exports, foreign income and REER emerges, by taking into account non-price competitiveness as a control variable as well as the EMU structural break (1999Q1). In our tables the foreign demand (FD) and price competitiveness (REER) long-run elasticities of the Italian export flows are listed by considering, in turn, five deflator-based REERs and by distinguishing flows according to the EU11, IC37 and BG42 clusters. Finally, the trade elasticities are reported separately for the ‘value’ analysis (Table 9) and the ‘volume’ analysis (Table 10) regarding the total export flows, although the sectoral analyses refer only to the current prices (Tables 11 and 12).

5.1 Total Exports

Let us start by discussing the results from the export equations, which refer to long-run elasticities based on values (i.e., current export prices and nominal foreign demand). According to Table 9, the export elasticities to the foreign demand are remarkably relevant (generally above the unit), while on average the price competitiveness sensitivity is − 1.5 with respect to the EU11 flows when significant. Focusing on export prices only, we specifically estimated an elasticity of − 1.34 to the REER (significant at the 1% level). Expanding the analysis to the IC37, the foreign demand elasticities are quite in line with the European flows (on average 1.3), while the REER elasticity is higher (− 1.89 when export prices are considered). Similar findings emerged from the BG42 flows, in which only the HCPI-REER export elasticity could be estimated (− 1.78) due to data availability. This provides an insight—as we mentioned above—into the fact that outside the Eurozone Italy’s exports can be affected to a greater extent by price than non-price factors, the size of the demand elasticities being similar. In parallel, when the research was conducted using alternative deflator-based REERs, the picture normally became quite mixed, since we did not refer to the export prices uniquely. Nonetheless, the demand elasticities are always significant and not especially steady among different clusters of partners, while it should be noted that a difference is apparent with respect to the ULC- and UWC-REER elasticities. Particularly, the productivity-adjusted competitiveness indicators are not cointegrated with the export flows and foreign demand within the Eurozone, and this can indicate that Italy’s intra-EMU exports are driven by cost competitiveness to a lesser extent than the global flowsFootnote 34; this can also depend on the adjustment by productivity (especially since Italy’s productivity growth has experienced a huge slowdown in recent times). However, we noticed that something similar occurs for the HCPI-based REER elasticity, which becomes higher and statistically significant for global exports; in other words, consumer prices are not the most appropriate metric for the assessment of external competitiveness within the Eurozone. Moreover, partially related to the above, attention should be paid to non-price factors, since the TFP coefficient is positive in all the model specifications and higher for the EU11 flows (1.12 when the export prices are considered compared with 0.60 for the IC37 flows and 0.13 for the BG42 flows). This could be a signal of more pronounced ‘competition on quality’ with respect to the Eurozone partners, in which the exports of Italy can be supposed to face its competitors on technologically sophisticated items.Footnote 35 Furthermore, the dummy coefficients for the structural break are systematically negative and generally significant when extending the study to global trade; bearing in mind that the IC37 embodies the EU11 flows, this might indicate that after the Euro’s inception—and intuitively to some extent due to the exchange rate regime—exports towards extra-EMU countries followed a dissimilar pattern from those towards intra-EMU countries.

Despite the low variability of the estimates (when alternative metrics of price competitiveness or different clusters of partners are considered), we tested whether our findings also hold for volumes. Not surprisingly, lower inconstancy among the coefficients arose from different model specifications when constant price exports and real foreign demand were considered instead of nominal variables (Table 10). In general, for the EU11 the export foreign demand elasticities appear to be moderately higher, while the REER elasticities are lower (− 1.0 on average). Similar to the findings of the value analysis, exports’ sensitivity to price factors is higher for global than for Euro area flows. Still, a non-negligible difference between EU11 and IC37 export elasticities to the HCPI based-REER emerged, and productivity-adjusted REER elasticities could be estimated by cointegration (which proved to be significant despite being lower than the export prices’ REER elasticity). All in all, the volume analysis validates the relevance of price competitiveness to the shaping of Italy’s export flows. Additionally, it raises further questions regarding the consistency of relative prices among EMU countries when measured by consumer price indices, while export price-based deflators appear to be the most suitable for studying external competitiveness, since they consider traded goods uniquely.

Last but not least, the influence of non-price factors proved to be positive in all the specifications, despite being lower and often not significant for the constant prices’ analysis (particularly when the investigation was extended outside the Eurozone). The difference between volumes’ and values’ results with respect to the significance of non-price factors can be ascribed to feasible changes in export composition towards high-quality goods (or upgrades of already-traded goods), as suggested by the so-called ‘transformation’ or ‘restructuring’ argument (see Coltorti 2012; Ginzburg 2012; Lissovolik 2008). An additional element in favour of this interpretation relies on the fact that, according to the literature, nominal export growth has been proved to be driven mainly by increasing export unit values, while the volumes are quite steady (see Lanza and Stanca 2007; Quintieri 2007).

Due to different partners and periods, we are not in a position to compare our results exactly with already-existing analyses. However, two general remarks can be advanced. The first one concerns the size of the trade elasticities; in this regard, it can be argued that the Italian price elasticities estimated in this paper appear to be in line with the ones in previous contributions—particularly the study by the European Commission (2010), which indicates a REER elasticity of − 1.72, although it does not consider non-price competitiveness—while the foreign income elasticities are moderately higher than those existing in the literature. The second one regards the use of alternative deflator-based REERs; in this respect, our estimations confirm the perception according to which different competitiveness metrics lead to rather dissimilar results in terms of exports’ sensitivity to price factors, as well as the fact that the export price-based REER is one of the most appropriate indicators of price competitiveness.

5.2 Sectoral Exports

Furthermore, a sectoral analysis of export values was conducted for the EU11 and IC37 using the export price-based REER, as shown in Table 11 (the GDP deflator-based REER was also used as a robustness check in Table 12). Concerning the flows towards the Eurozone (Table 11, left panel), machinery and transport equipment (sector 7) shows the highest REER elasticity (− 2.37), while manufactured goods (sector 6) indicate an elasticity of − 1.44 to the export price-based REER. Nevertheless, it is also apparent that the sensitivity of manufacturing and machinery items to the foreign demand is significantly higher than that of the total exports. These elements can obviously have some relevant implications for Italian export specialisation, since sectors 6 and 7 together account for more than half of the total Italian exports (see Table 13, which indicates the average share of each sector in the total exports for the EU11 and IC37, alternatively). Moreover, even miscellaneous manufactured articles (sector 8), which account for about 20% of the Italian flows towards the EU11, exhibit an export price REER elasticity of − 0.92, despite the fact that the sectoral elasticity to the foreign demand is considerably lower than on aggregate (0.95). On the contrary, the price sensitivity is virtually zero for chemical items (sector 5), which however exhibit a larger and statistically significant demand elasticity (2.50). The overall EU11 sectoral export picture becomes more complete when also considering the role of non-price competitiveness: notwithstanding the huge sensitivity to price competitiveness (especially for machinery), qualitative factors are highly relevant to and statistically significant for five out of ten branches, namely manufacturing, machinery, miscellaneous, chemicals and crude materials. These results are consistent with the non-price competitiveness argument, assessing the relevance of quality to international trade, which is more pertinent to mature economies, and explicitly considering the effects of a country’s participation in the international fragmentation of production (see Cingolani et al. 2015). Finally, there is no trace of a long-run relationship for sectors 0, 1, 3 and 9 for Italy’s exports towards the Eurozone only: this is definitely connected to the insensitivity of these items to price factors, with a prominent role of the foreign demand in shaping the flows towards the EU11 cluster. Finally, Table 14 (left panel) strengthens our findings, since no evidence of significant changes in the magnitude of elasticities emerge when considering the GDP deflator instead of the export prices in the REER. The only argument of note concerns the REER elasticities of exports towards the EU11, which appear (on average) to be lower but still statistically significant when the GDP deflator based-REER is used instead of the export price-based REER.

Regarding the global flows (Table 11, right panel), the remarkable price elasticities in manufacturing and machinery still hold (− 1.04 and − 1.42, respectively), while the impact on non-price factors is shown to be lower—albeit still relevant and statistically significant for some industries, especially manufactured goods. Moreover, what captures the attention is the high price sensitivity in chemicals, which is proved to be nil for Euro area exports, while it is − 1.23 for global flows (with a large foreign demand elasticity too). For IC37 flows we also estimated the long-run elasticities in the ‘primary’ sector of the economy, especially for food and live animals, in which the role of price competitiveness is highly important (− 2.18 REER elasticity, while agricultural exports towards the Eurozone are not related to price factors) with a negligible effect of TFP. Moreover, the long-run price elasticity for exports of crude materials (sector 2) towards the IC37 is in line with the EU11 flows (− 0.99), for which the EMU foreign demand is a much important driver (2.59) than for the global flows (1.14). Finally, concerning the global flows, no long-run relationship was identified for sector 3 and sector 9, similar to the situation for exports towards the EU11 (due to the insensitivity of these items to the REER). Contrary to what happens for the Eurozone flows, price competitiveness becomes relevant for the primary branches of the economy (namely sector 0 and sector 1) when considering a larger number of partners. Particularly, food items show an REER elasticity of − 2.18, while an REER elasticity of − 1.96 was estimated for beverages and tobacco (in both cases, however, the foreign demand elasticity approaches the value of 2). Even in this case, Table 12 (right panel) reinforces the reliability of our findings, confirming the robustness of our estimates to an alternative metric of price competitiveness (namely, the GDP deflator-based REER instead of the export price-based one).

All in all, the sectoral study confirms the insights of the analysis conducted on aggregate flows: price competitiveness is, on average, more relevant to global than Eurozone exports, while the impact of non-price factors affects Eurozone flows to a greater extent than global flows. Furthermore, the sectoral breakdown indicates that some industries actually outperform others with respect to the size of the REER elasticity of exports, and the most sensitive sectors to price elasticities are manufacturing and machinery, for which the export performances are however positively affected by non-price factors; the latter, even in these specific cases, were proved to be more significant for the Eurozone than for extra-EMU export flows.

5.3 Model Stability

With respect to the robustness of our model, which has already been stressed to some extent by considering alternative metrics of price competitiveness (that is, five REERs based on alternative deflators), we report the long-run export elasticity estimations for the EU11 flows without controlling for the 1999 structural break and with respect to the EMU sub-period only. As far as the EU11 trade price elasticities to non-productivity-adjusted price indicators are concerned (ULC- and UWC-based REERs do not present cointegration), we suggest a comparison between Table 14a (in which sub-periods are not taken into account) and the previous findings (particularly Table 9, top panel, which considers the Euro inception break) to validate the absence of outstanding differences. The export elasticity estimations are not virtually identical (the export price REER elasticity is moderately higher when the structural break is not included in the model specification). Consistently, price elasticities can be considered not solely depending on data from 1994 to 1999, although the Euro inception structural break should be taken into consideration for the estimates of the price competitiveness effect, since the Chow test rejected the hypothesis of no break in 1999Q1 for all the model specifications (see Appendix A4 for an example).Footnote 36

Additionally, the robustness of the export elasticity estimations was carefully tested by considering the EMU sub-period only instead of the whole sample, as in Table 14b. In this specification the estimated long-run elasticities were proved to be lower (the REER elasticity downwards to − 1.18 for export prices and to − 1.19 for the GDP deflator), while no significant differences emerged with respect to the impact of foreign demand and non-price factors. Still, this can be interpreted as an additional element in favour of the ‘transformation’ or ‘restructuring’ argument: while price competitiveness was proved to be always relevant to the shaping of Italy’s export performance, increasing REERs may not always be interpreted as decreasing competitiveness, since higher prices can reflect quality improvement. Indeed, the size of the REER elasticity is not insignificant during the EMU period only, which contributes to indicating that the price elasticity is relevant, even in recent times.Footnote 37 Finally, the lower magnitude of GDP deflator-based REER elasticity (when the EMU sub-period only is considered instead of 1994–2014) might be related to the fact that the GDP deflator is directly affected by the terms of trade, which in turn may be influenced by the exchange rate. In the light of this finding, export price-based REER should be considered as the most reliable indicator for assessing Italy’s price competitiveness.

6 Final Remarks

In the light of the current debate on the relevance of price competitiveness, which is closely related to Italy’s recent upward trend in the REER as well as to its decreasing market shares, the main purpose of this empirical paper was to examine the role of price factors in determining Italian export flows. To this end, we conducted an ECM analysis (from 1994 to 2014) based on single export equations—as an attempt to develop the model specification suggested by the European Commission (2010)—to estimate the long-run elasticities to foreign demand and price competitiveness jointly, with respect to different trading partner groups and, even for robustness, to alternative deflator-based REERs (namely HCPI, ULC, UWC, GDP deflator and export prices). Moreover, since trade flows might not depend solely on price factors and on foreign income, we controlled our estimates for a proxy for non-price competitiveness, namely TFP dynamics, as suggested by the relevant existing literature. For the sake of model stability, the econometric analyses also referred to time-varying factors; in this regard the onset of the Euro was treated as a structural break (verified by Chow tests) and taken into consideration in the model specifications accordingly. Finally, in addition to the total export flows, we performed a sector-disaggregated analysis (10 industries) to determine whether some branches outperform others in terms of export elasticities.

The results from the export equations estimated by means of cointegration suggest that, notwithstanding the considerable effect of the foreign demand and non-price factors, price competitiveness is still relevant in shaping Italy’s export performance. More specifically, the REER elasticities based on price indexes that are not adjusted by productivity are the most significant among all the estimations; particularly, the REER elasticity of exports towards the EU11 is on average − 1.3 when the export prices are considered in different specifications. When we also considered extra-Eurozone flows, the empirics suggest that Italian global export is more sensitive to changes in price competitiveness than intra-EMU flows. Expanding the analysis to global trade, both the REER (− 1.7 on average) and the foreign demand elasticities are relatively higher. Moreover, the impact of non-price factors has been proved to be positive and strongly significant for exports towards the Euro area, while they account for a lesser extent when the focus shifts to global flows.

A sectoral analysis of export flows was also conducted on the basis of the export price-based REER (and, for the sake of robustness, also using the GDP deflator-based REER). For Eurozone flows the highest REER elasticities were estimated for machinery and manufacturing, combined with a relevant impact of both foreign demand and non-price factors. In parallel, for global flows the remarkable price elasticities in manufacturing and machinery still hold, and the impact of non-price factors is relevant and statistically significant, albeit lower than for Eurozone flows separately. Moreover, we recognised sizeable price sensitivity in chemicals for exports outside the Eurozone, while on the contrary Italy’s exports of chemical items were proved to be rigid to price competitiveness in the EMU. Similar reasoning applies to exports in the primary sector, which are responsiveness to price factors for global flows but rigid for Eurozone flows. These elements have non-negligible implications for Italian export specialisation, particularly due to the fact that manufacturing and machinery together account for more than half of the total Italian exports; the sectoral analysis indicates that these industries outperform the others with respect to the size of REER elasticity of exports, as far as the trade performances in these branches are however positively affected by non-price factors (which were proved to be more significant for Eurozone trade than for extra-EMU flows).

According to our empirical findings, along with external demand and non-price factors, price competitiveness can still be considered as a significantly relevant factor to Italian exports, for both intra- and extra-Eurozone trade. Broadly speaking, on the basis of the estimated long-run elasticities, 10% real depreciation (other things being equal) would imply 13% nominal export growth towards the Eurozone, whereas such an increase would be more pronounced with respect to the global flows. As an indication, our empirical findings about price competitiveness can be considered to be conservative if compared with recent Bank of Italy research (Bulligan et al. 2017, p. 26), which indicated a medium-run 3% increase in Italian exports as a result of a 1.5% decrease in export prices due to a reduction of the tax wedge on labour.Footnote 38 From this perspective the recent upward trend in the REER (to be interpreted as a loss of price competitiveness) might actually have hampered Italy’s export growth, which, despite the huge real appreciation, has not experienced a slowdown in absolute terms. Notwithstanding price competitiveness being a key factor in determining Italian exports (and therefore real depreciation possibly representing a useful stimulus for external flows), we consider the recent macroeconomic policies implemented in the Eurozone context to foster deficit countries’ competitiveness to be extremely detrimental in terms of growth and living standards. In fact, these measures mostly concern structural reforms to decrease wages in the European periphery, including Italy, which would additionally damage southern countries’ productive bases (and hence also erode non-price competitiveness, grounded on quality and export diversification) due to their adverse effects on the domestic demand. Contrariwise, we suggest that the external adjustment to rebalance the intra-Eurozone flows should occur along two dimensions. With respect to price competitiveness, a feasible solution to the imbalances can be found in a sort of symmetric process comprising internal revaluation of surplus countries, that is, higher prices and wages in core countries (especially in Germany) that would allow Italy to improve its relative price competitiveness, exchange rate flexibility not being exploitable in the Eurozone context, while it could work with extra-EMU partners. In parallel, with respect to non-price competitiveness, deficit countries need an adequate set of industrial policies (instead of restrictive measures) aimed to enhance the soundness of their productive systems and consequently to extend their export composition.

Notes

Consequently, trade misalignments have been treated by means of austerity measures (i.e., internal devaluation combined with labour market deregulation) aimed at fostering deficit countries’ exports. However, it is reasonable to consider such a narrative as insufficiently persuasive, since this version does not take into account both empirical evidence and theoretical arguments—see Brancaccio (2011), Cesaratto (2010), Cesaratto and Stirati (2011), Paternesi Meloni (2017), Simonazzi et al. (2013), Stockhammer (2011) and Uxó et al. (2011), who indicated a number of reasons for restrictive policies being considered as questionable from a macroeconomic standpoint.

This evocative expression has been borrowed from Bayoumi et al. (2011, p. 5).

With respect to the Eurozone issues, non-mainstream scholars have taken into account the dangers of asymmetric adjustment by means of internal devaluation (i.e., the negative effects on output of decreasing real wages). Particularly, authors who have claimed that the relevance of price competitiveness is scarce have maintained that restrictive policies would damage peripheral countries’ productive base, which would already be ‘too narrow, in quantitative and qualitative terms, to respond effectively to external demand’ (Simonazzi et al. 2013). In parallel, price competitiveness supporters have claimed that Eurozone price differentials should be reabsorbed through a revaluation of surplus countries, since their external performances mainly depend on the wage deflation policies implemented during the early years of the EMU (see Bagnai 2012b; Brancaccio 2008; Cesaratto and Stirati 2011).

According to this argument, it has been asserted that a fixed exchange rate regime can hinder the adjustment of relative prices, while flexible exchange rates (especially in advanced countries in terms of the technological content of products) can contribute to reducing the trade imbalances. Consequently, currency depreciation, which differs from internal devaluation in terms of effectiveness and distributive issues (see Artus 2011), would foster exports in deficit countries without outstanding inflationary effects.

Some criticism of the non-price competitiveness argument was raised by Marin (2010), who asserted that Germany gained price competitiveness through wage moderation and delocalisation: specifically, ‘German firms offshored part of production to the new member states in Eastern Europe, Russia and Ukraine’, where a less stringent institutional environment (in terms of the protection of workers and labour costs) could be exploited in parallel with a kinder currency regime. The argument for outsourcing was also reported, although with different implications, by Stehrer and Stöllinger (2015), who identified a Central European manufacturing core (headquartered in Germany) closely connected with the Eastern European periphery, which in turn significantly strengthened its manufacturing base (see Celi et al. 2018).

In this framework, Blanchard (2007), Giavazzi and Spaventa (2010) and Merler and Pisani-Ferry (2012) underlined the potentially dangerous role—in terms of liquidity and solvency as well as related to a poor productivity dynamics—of persistent CA deficits, even within a currency union. For these reasons, several contributions have considered the role of intra-Euro area trade imbalances in the current European sovereign debt crisis—see Cesaratto (2012), Guerrieri and Esposito (2012) and Sinn (2012), among others.

Within the EU_11 we considered Austria, Belgium, Finland, France, Germany, Ireland, Luxembourg, the Netherlands, Portugal, Spain (which adopted the Euro in 1999) and Greece (which joined the EMU in 2001).

With respect to the responsiveness of external trade to the 2008 global crisis, we noticed that Italy’s import and export shares of the GDP have been significantly reduced, as proof that the decrease in international flows has been more pronounced than the fall in the GDP.

It should be borne in mind that correlations between the REER and the exports may suffer from endogeneity, since the REER is a trade-weighted variable and therefore its dynamics may be driven by changes in the relative importance of partners over time rather than by changes in prices or nominal exchange rates. However, in the econometric part of this paper, we deal with this issue by using proper technicalities.

In addition to supposing this relationship to be linear, we do not actually consider feasible integration and/or cointegration phenomena. This hypothesis will be verified properly in the following, that is, when trade elasticities are estimated.

Alternative deflator-based REERs (vs. 37 industrial countries) are available from 1994 to 2014 (source: European Commission).

However, both the ULC and the UWC can be affected by reverse causality or spurious correlation, since they are adjusted for productivity dynamics: in fact, labour productivity could be considered to be endogenous (or, at least, pro-cyclical), since it may increase with export growth due to the fact that exports are a relevant component of the GDP.

As in the previous analyses of export elasticity, we do not take into account feasible integrated and/or cointegrated series: these hypotheses will be verified in the following sections, that is, when trade elasticities are estimated econometrically.

Consistent with global value chain relationships, in the case that exports were stimulated by real depreciation, one can argue that this might also foster imports (e.g., intermediate inputs or energy). In this regard, the indicator ‘imports content of exports’, assessing the relevance of the international fragmentation of productive processes, increased for Italy from 23% in the mid-1990s to 29% in the mid-2000s (source: OECD.Stat). In this framework Cingolani et al. (2015) confirmed that both Italy and Germany experienced strong growth in the foreign value-added content of exports, despite the fact that Italy’s off-shoring index was the lowest among the EU countries during the period 1999–2011.

However, the same report stated that more than 60% of Italy’s export share variability is explained by factors other than the REER, specifically the foreign demand dynamics and non-price competitiveness.

As stated by the European Commission (2010), ‘(t)he comparison between Germany and Italy is informative of the role played by price competitiveness. If Italy’s real exchange rates had evolved in a similar way to Germany’s since the beginning of 1999, Italy’s export growth would have almost matched that of Germany’s, while in reality it was less than one third its size.’

‘During 2001-04, the contribution of the residuals deserves a careful reading’ (Allard et al. 2005). Although residual factors are not considered as additional regressors, they are generally indicated as non-price competitiveness and sectoral orientation of trade.

Further methodological details, among which are the tests and estimation procedures, are reported in Appendices A1, A2 and A3.

The optimal lag length analysis also considered additional tests, namely Schwarz and Hannan–Quinn. In the case that the alternative tests indicated ambiguous reading results, we controlled the trend of the log-likelihood function. Technical issues are reported in Appendix A4.

Basically, the whole process is made stationary by considering the cointegrating equation. In detail, we estimated a linear combination of variables by means of OLS, and then we considered the residuals; in the case that they were stationary, that is, I(0), variables can be considered to be cointegrated and the error correction term can be included in the export equation to make the process stationary.

Essentially, in case the series are I(1) but are not cointegrated, we could eliminate non-stationarity by using first differences. Nevertheless, we would be not in a position to estimate long-run relationships among variables.

It is worth noting that the error correction term embodies information about the long-run relationships between the levels of variables. In fact, this kind of statistical technique has been developed to combine short- and long-run relationships. However, as already stated, we adopted a long-term perspective for theoretical reasons.

In the European Commission’s (2010) study, the foreign demand proxy is computed as the export-weighted foreign imports for the main trading partners of the Euro area, while in this paper, due to data availability, the foreign demand faced by Italy was computed as the export-share weighted GDP of the trading partners in each cluster in the spirit of Bayoumi et al. (2011).

Error correction methodologies allow for causality; according to Engle and Granger (1987), having estimated the cointegrating equation coefficients (γi), it is possible to evaluate the significance of coefficient α by means of OLS (as the process is now stationary) to capture long-run causality. Notice that coefficient α is a measure of the speed of the adjustment of the process towards the long-run equilibrium. Moreover, reverse causality might be grounded theoretically, since Italy’s export performance might affect the foreign GDP and competitiveness through different channels. This could be tested by means of a VECM methodology, which we considered not to be feasible within our investigation since a similar analysis would suffer from omitted-variable bias.

From an empirical standpoint, it is worth noting that the inclusion of non-price factors in the VAR may have an effect on the cointegrating equation in the case that they actually affected the export dynamics. However, this is consistent with our research goals, since it is appropriate also to consider non-price competitiveness when estimating price and demand elasticities.

More precisely, Giordano and Zollino (2014, p. 6) developed a relative TFP indicator, which compares ‘a country’s performance in total economy efficiency and ability to innovate against the same basket of competitors included in the price competitiveness indicators’. However, the motivation of this indicator lies in the fact that they advanced a cross-country analysis, while our research just referred to Italy’s competitiveness.

Some criticisms about the use of TFP as a proxy for non-price competitiveness can emerge. From a theoretical standpoint, TFP criticisms have been discussed in several contributions—see Birolo (2010), Deleidi and Paternesi Meloni (2014), Ginzburg (2008) and Storm (2017), among others. Moreover, with respect to our model specification, it might be argued that sound productivity dynamics would represent an efficiency advantage for firms, and to some extent this would be passed on to costs and prices, which are already considered within real exchange rates. Consistently, this might produce endogeneity. However, this is not the case in our paper, since we do not cointegrate TFP but just control for its dynamics (proved to be stationary at the 10% confidence level; see Appendix A1) outside the EC. Alternative variables might be taken into consideration as proxies for non-price competitiveness to avoid potential bias (e.g., R&D investment, the number of patents in the manufacturing sector and IC expenditure), and this may stimulate future research due to the analytical criticisms of TFP.

Briefly, if total factor productivity was considered within the export equations, multicollinearity would to some extent emerge with the cost competitiveness indicators, since the latter are adjusted by labour productivity.

Alternatively, export prices could be considered as proper deflators for flows, but quarterly data are not available. Moreover, export prices do not consider the dynamics of input prices (especially semi-finished goods and services), which are relevant to price determination at the firm level. In this regard, the GDP deflator can be considered as a feasible alternative for assessing price competitiveness.

Technically, when calculating the foreign demand proxy, we fixed weights in the initial year to avoid endogeneity issues. We preferred not to use lagged weights, since the export shares exhibited high autocorrelation.

Quarterly nominal exchange rates USD/EUR were computed on the basis of Italy’s GDP and its partners’ GDPs by using current Euros–Dollars (current PPP) for values and constant Euros–constant Dollars (fixed PPP) for volumes. Moreover, we considered only countries for which data are available from 1994 to 2014 to build realistic proxies for the global demand. In detail, the IC37 demand was calculated on the basis of 31 countries (quarterly GDPs are not available for Bulgaria, Croatia, Cyprus, Romania and Malta), while the BG42 demand refers to 34 countries (Russia, Korea and Brazil were added to the IC37 group). Then, we considered only flows with countries for which a reliable proxy for the foreign demand could be calculated (i.e., we excluded exports towards countries that were not represented within the global demand). For a snapshot of the relative incidence of trade partners’ clusters, see Fig. 5.

REER vs. EU11 is not available, so we referred to the whole Eurozone REER (REER vs. EA, 19 countries). Notice that, according to the data, the EU11 incidence in the Euro area Italian flows was about 98% in 1994 and about 96% in 2012.

As in Fig. 5, it is worth noting that REER vs. IC37 refers to the EA plus 18 other countries, while REER vs. BG42 considers 5 additional countries. However, price competitiveness vs. BG42 quarterly data are available only for the HCPI-based REER, so, for this group of trading partners, it was not possible to compare elasticity estimations based on alternative deflators.

It can also be argued that this could result from adjusting the cost competitiveness by productivity. On the basis of the unit labour cost approach, in the case that productivity decreased to a greater extent than wages, real appreciation would be experienced—other things being equal (e.g., wages and productivity dynamics in competitor countries or nominal exchange rate movements). Furthermore, the ambiguous reading of these cost competitiveness metrics could be grounded on the fact that the inverse relationship between productivity and prices (i.e., an increase in productivity leads to an advantage in terms of costs) can be considered not to be immediate.

Some elements concerning this point will be investigated further through the sectoral analysis.

For the sake of completeness, in Appendix A4 we report in detail the analysis conducted on the EU11 Italian exports (values) with respect to the export price-based REER by controlling for the 1999Q1 structural break, which was verified by a Chow test. Similar methodologies and tests were applied to all the model specifications.

The same robustness checks (both the non-inclusion of the dummy variable and the EMU sub-period only) were also performed for the IC37 flows, with virtually identical results.

Particularly, the estimated ‘semi-structural’ macro-econometric model advanced by the Bank of Italy indicated that ‘the response (of export) to (price) competitiveness is gradual but relatively high (2.1) in the long run’ (Bulligan et al. 2017, p. 14). It should also be made clear that the sensitivity of exports to price factors was estimated by means of a different approach from the export equations, and consequently the size of the elasticity is not immediately comparable with our estimates.

References

Algieri B (2015) Price and non-price competitiveness in export demand: empirical evidence from Italy. Empirica 42(1):157–183

Allard C, Catalan M, Everaert L, Sgherri S (2005) Explaining differences in external sector performance among large euro area countries. Approved by IMF European Department, October 12, 2005

Artus P (2011) Improving euro-zone countries' competitiveness: in what ways does a reduction in wages differ from a devaluation of the exchange rate. Natixis-Economic research, 14 September 2011, No. 664

Bagnai A (2012a) Il tramonto dell’euro. Imprimatur editore, Novembre 2012

Bagnai A (2012b) Crisi finanziaria e governo dell’economia. Costituzionalismo.it, Gennaio 2012

Bagnai A, Mongeau Ospina C (2014) The a/simmetrie annual macroeconometric model of the Italian economy: structure and properties. A/working papers series 1405, Italian Association for the Study of Economic Asymmetries

Bayoumi T, Harmsen R, Turunen J (2011) Euro area export performance and competitiveness. IMF working paper no. 140

Belke A, Dreger C (2011) Current account imbalances in the euro area: catching up or competitiveness? Deutsches institut für wirtschaftsforschung, discussion paper, Berlin 02-11

Birolo A (2010) La produttività: un concetto teorico e statistico ambiguo. In: Feltrin P, Tattara G (eds) Crescere per competere: Le piccole e medie imprese in un mondo globale. Bruno Mondadori, Milano

Blanchard O (2007) Current account deficits in rich countries. IMF Pap 54(2):191–219

Bobeica E, Christodoulopoulou S, Tkačevs O (2016) The role of price and cost competitiveness for intra- and extra-euro area trade of euro area countries. ECB working paper no 1941, July

Brancaccio E (2008) Deficit commerciale, crisi di bilancio e politica deflazionista. Studi economici, n. 96-2008/3

Brancaccio E (2011) Crisi dell’unità europea e standard retributivo. Diritti lavori mercati, ii

Bulligan G, Busetti F, Caivano M, Cova P, Fantino D, Locarno A, Rodano ML (2017) The Bank of Italy econometric model: an update of the main equations and model elasticities. Working paper no. 1130, July 2017

Celi G, Ginzburg A, Guarascio D, Simonazzi A (2018) Crisis in the European Monetary Union: a core-periphery perspective. Routledge, Abingdon (forthcoming)

Cesaratto S (2010) Alle origini della crisi europea in corso: spunti critici a margine di due rapporti della Commissione. Dipartimento di Economia Politica, Università di degli Studi di Siena, n.596

Cesaratto S (2012) Controversial and novel features of the Eurozone crisis as a balance of payment crisis. Dipartimento di Economia Politica, Università di degli Studi di Siena, n.640

Cesaratto S, Stirati A (2011) Germany and the European and global crisis. Dipartimento di Economia Politica, Università di degli Studi di Siena, n.607

Cingolani I, Felice G, Tajoli L (2015) External Imbalances in the European Union and International Fragmentation of Production: is there a link? Centro Studi Luca d’Agliano Development Studies, n. 386/2015

Coltorti F (2012) L’industria italiana tra declino e trasformazione: un quadro di riferimento. “QA rivista dell’Associazione Rossi-Doria”, 2/2012

Comunale M, Hessel J (2013) Current account imbalances in the euro area: competitiveness or financial cycle? DNB working paper n.433

Deleidi M, Paternesi Meloni W (2014) Italian economic trends and labor market reforms: a 50-years overview. ASTRIL working paper n.12/2014

Dieppe A et al (2012) Competitiveness and external imbalances within the euro area. ECB occasional paper series n. 139, December

Engle RF, Granger CWJ (1987) Cointegration and error correction: representation, estimation and testing. Econometrica 55:251–276

European Commission (2009) Competitiveness developments within the euro area, vol 8, n.1/2009

European Commission (2010) The impact of the global crisis on competitiveness and current account divergences in the euro area, vol 9, n.1/2010

Felipe J, Kumar U (2011) Unit labor costs in the Eurozone: the competitiveness debate again. Levy Economics Institute of Bard College working paper no. 651

Gaulier G, Vicard V (2013) The signatures of euro-area imbalances: export performance and the composition of ULC growth. ECB Compnet policy brief 02/2013

Giavazzi F, Spaventa L (2010) Why the current account may matter in a monetary union, lessons from the financial crisis in the euro area. Discussion paper 8008, Centre for Economic Policy Research

Ginzburg A (2008) Le nuove PMI: strategie di riposizionamento, qualificazione e specializzazione del sistema produttivo reggiano. Camera di commercio, industria, artigianato e agricoltura di Reggio Emilia, Dicembre 2008

Ginzburg A (2012) Sviluppo trainato dalla produttività o dalle connessioni: due diverse prospettive di analisi e di intervento pubblico nella realtà economica italiana. Economia & Lavoro, saggi, pp 67–93

Giordano C, Zollino F (2014) Exploring price and non-price determinants of trade flows in the largest euro-area countries. Banca d’Italia, occasional papers, n. 233, September 2014