Abstract

Background

Biosimilars represent a significant cost savings opportunity for the entire healthcare system. Despite efforts from the United States Food and Drug Administration, adoption has not been as successful as originally hoped. Perceived barriers to adoption of biosimilars have been described previously, but more knowledge is needed. Further, increased understanding is needed surrounding commercial payer preferences of biosimilars.

Methods

A survey to assess perceived barriers to biosimilar adoption was dispersed to healthcare leaders who work in health-systems, physician practices, and the pharmaceutical industry. Policies from the top 15 commercial payers, by covered lives, were reviewed to collect information surrounding coverage and preferred products to assess if perceptions from healthcare leaders align with payer policies.

Results

The largest number of responses (n = 76) came from health-systems (n = 56), followed by pharmaceutical manufacturers (n = 12), and physician practices (n = 8). Responses from each cohort aligned very closely with the composite results of the group. Responses surrounding safety and efficacy were high amongst all groups, while rebate increases to payers for reference products were of highest concern for adoption. United Healthcare had the most policies preferring biosimilars (6/7, 86%). Filgrastim-sndz (Zarxio), had the most preferred statuses for a biosimilar (10/15, 67%). The infliximab reference product had the most preferred statuses for a reference product (9/15, 60%).

Conclusions

Findings from this study outline the greatest perceived barriers to adoption of biosimilars from a variety of different stakeholders. Rebates from reference product manufacturers to payers was the main deterrent for biosimilar use.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Perceived biosimilar barriers include concerns surrounding safety and efficacy, lack of knowledge on billing, coding, and reimbursement, strategies from reference product manufacturers to prevent competition, regulation surrounding interchangeability, and commercial payers creating rebate driven policies that disadvantage biosimilars. |

Reference manufacturers increasing rebates to payers to keep their product on the preferred formulary tier has been outlined as a significant barrier to adoption. |

Payer results show some biosimilars are heavily disadvantaged compared with their reference biologic, and also outlines a rough timeline of how long payers take to form a stance on a preferred product. |

Overall, the combined results of the study detail where efforts can be made to increase access to biosimilars for patients and healthcare systems. |

1 Introduction

Biological drugs can make management of diseases, particularly inflammatory diseases such as psoriasis, remarkably more effective with tolerable safety [1]. While these drugs can significantly decrease disease burden, as seen with psoriasis, controlling their costs in the drug market has presented a momentous challenge. Less than two percent of Americans use biologics, however, they represent 40% of total spending on prescription drugs, and from 2010 to 2015, biologics represented 70% of the growth in United States (US) drug spending [2].

A solution to control spending on biologics was proposed through the Biologics Price Competition and Innovation Act (BPCIA) of 2009. The BPCIA established an abbreviated pathway for biosimilar approval from the US Food and Drug Administration (FDA) [3]. The ideology was similar to that of the Hatch-Waxman Act of 1984, which created a pathway for generic small-molecule drugs [4]. Further, the FDA published its Biosimilars Action Plan in 2018 that outlines important foundations to balancing innovation and competition of biosimilars in the US [5]. Some estimates predict that biosimilars will reduce direct spending on biologic drugs by US$54 billion from 2017 to 2026, or about 3% of total estimated biologic spending over the same period with a range of US$24 billion to US$150 billion [6]. With many blockbuster biologic drugs newly off patent, and others with patent expiry in the coming years, there has been a growing interest in the development of biosimilars from both generic and traditional innovator biopharmaceutical manufacturers. Additionally, in March 2020, the FDA proceeded with the formal transition of insulin and certain other biologics to a new abbreviated biologic regulatory pathway, pathway 351(k), under the Public Health Service Act to better facilitate development of biosimilar or interchangeable drugs [7]. Previously, these drugs were approved under the 505(b)(2) pathway [8].

From March 2015 to July 2020, the FDA has approved 28 biosimilars referencing nine originator biologics [9]. These numbers demonstrate a strong impact of the biosimilar approval pathway under BPCIA; however, many issues surrounding biosimilar adoption and barriers preventing their entry into the market remain. At time of writing, 18 of the 28 FDA-approved biosimilars have launched into the US market, with nine of them launching since November 2019 (Table 1) [9]. The time difference between approval and launch often exceeds a year, and some of the products have been approved for 4 years with no launch. Survey studies and editorials have demonstrated that specialty physicians and other healthcare professionals have concerns regarding safety and efficacy of biosimilars compared with reference products [10,11,12,13,14]. These studies have indicated other barriers to biosimilar adoption that are associated with uncertainties surrounding regulatory issues including pharmacy-level interchangeability; indication extrapolation for approved biosimilars missing reference product indications; patent litigation settlements and ‘pay-to-delay’ tactics from manufacturers; and complex rebate and pricing challenges that may lead to financial disincentives for health plans to prefer biosimilars.

A strategy that reference product manufacturers have utilized to limit biosimilar adoption has been to negotiate formulary exclusivity with payers to ensure their product remains preferred. The ‘rebate trap’ is when an insurance plan has a financial incentive to favor a higher-priced, higher-rebated reference product as opposed to a lower-priced, lower-rebated biosimilar [15]. Drug manufacturers currently rebate as much as 50% of the price of biologic drugs to have theirs offered as the preferred drug on the formularies of pharmacy benefit managers (PBMs) and insurers. If a payer offers a biosimilar as the preferred drug, payers lose a big piece of those rebates, ultimately costing payers more money. Rebate increases do not typically mean that extra money is going back to the patient either [16].

There are many knowledgeable stakeholders of biosimilar adoption including physicians, clinical pharmacists, and pharmaceutical manufacturers. While this subset of stakeholders has been evaluated before, it included only health systems, and was focused only on infliximab biosimilars [17]. More knowledge is needed from this collective group of stakeholders. The aim of this research is to gain insight into perceptions of biosimilar barriers to market entry and utilization among group purchasing organization (GPO) stakeholders as well as to examine commercial payer medical benefit policies to further characterize this specific perceived barrier to adoption.

2 Methods

The study methods can be characterized into two phases.

2.1 Survey Creation and Dissemination

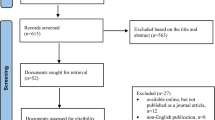

In phase I, a 20-question survey was created by the investigators. All investigators participated in the development and validation of survey questions. A survey template is available in Table 1 of the supplementary appendix (see electronic supplementary material [ESM]). The survey and study methods were approved by the University of Tennessee institutional review board (UT IRB, Nashville, TN, IRB Number 19-06870-XM) on September 18, 2019. Survey dissemination was planned in advance to utilize GPO relationships in attempt to reach as many respondents as possible. Approximately 300 invitations to complete the survey were emailed to health systems, physician practices, and pharmaceutical manufacturers. Email read receipts were utilized to ensure receipt of survey invitations. Health systems and physician practices with members on GPO advisory boards, and manufacturers with contractual relationships with the GPO were surveyed. The data from the survey was managed on a third-party website. The survey responses were collected from November 13, 2019 to March 23, 2020.

2.2 Survey Contents

The survey included 20 items and was designed for completion in 5 minutes or less. Questions were grouped by content and question format. The first five items asked respondents to characterize their demographic information by asking mainly closed-ended questions to indicate the industry they work in; their professional occupation (open-ended); the size of their health system (if applicable); if their health system is for-profit or not-for-profit (if applicable); and if they are involved in formulary decisions (if applicable). The rest of the survey asked respondents to rank items on a 5-point Likert scale from 1 (strongly disagree) to 5 (strongly agree). The first ten items of this section were based on barriers identified in previously published survey studies and editorials [10,11,12, 17]. Two items assessed safety and efficacy of switching patients from a reference to a biosimilar product, and extrapolating the use of a biosimilar the FDA has approved for a single indication to all other approved indications for the reference biologic. Eight items asked respondents to assess likelihood of a barrier to prevent biosimilar adoption from 1 (low likelihood) to 5 (high likelihood), including provider education and general knowledge; provider reluctance to prescribe biosimilars; provider education on billing, coding, and reimbursement; health-system formularies adoption rate; competitiveness of biosimilar price at market entry; patent litigation on manufacturing processes; rebates payments to third party payers; and regulation for substitution and interchangeability. Lastly, respondents were asked to rank biosimilars from 1 (slow adoption) to 5 (fast adoption) based on class of trade or category, including acute care setting; outpatient dialysis center; outpatient infusion center; curative targeted oncology; and outpatient specialty or retail pharmacy.

2.3 Commercial Medical Benefit Policy Analysis

Phase II of the study aimed to research the top 15 commercial medical benefit policies in terms of covered lives for the seven biologics in the US market that currently have biosimilar competition. The seven reference biologics and their respective competitive biosimilars that were studied are Neupogen (filgrastim), Neulasta (pegfilgrastim), Epogen (epoetin-alfa), Avastin (bevacizumab), Herceptin (trastuzumab), Rituxan (rituximab), and Remicade (infliximab). A third-party service was utilized to identify the top 15 commercial payers. The same service was used to obtain the medical benefit policies that were publicly available. This service is a repository of the current policy landscape for all major commercial and government payers. Payer policies are accurate through March 15, 2020. A systematic grading scale was developed to determine the preferred-tier status of all product offerings of the molecule. All products were given one of the following grades: preferred, non-preferred, no preference, covered based on specific indications, unclear, not listed in policy, or no published policy. Criteria for each grade can be found in Table 2 of the supplementary appendix (see ESM). While some policies may not use the exact nomenclature of ‘preferred’ or ‘non-preferred’, many contain other explicit language, such as ‘first-line treatment option’. Designation of a product as ‘not medically necessary’ for FDA-approved indications is interpreted as non-preferred status. Publicly available data on approval dates, launch dates, wholesale acquisition cost prices, and indications were collected for further analysis. All data was collected by a single researcher and analyzed using descriptive statistics to determine outcomes.

3 Results

3.1 Survey Respondent Demographics

A total of 92 respondents attempted the survey, and 76 successfully completed the survey (~ 25% response rate). The 16 respondents that failed to complete the survey were excluded. Table 2 describes respondent characteristics. This table also includes the characteristics of the health systems for respondents that fell in that category. The majority of respondents worked for a health system (n = 56, 74%) with more working in not-for-profit entities than for-profit entities (63% vs 38%). The majority of health systems were 2000+ beds in size (48%). Respondents with number of beds of < 500, 500–999 beds, and 1000–1999 beds were similar (16% vs 18% vs 18%). The majority of health-system respondents were pharmacists (82%), followed by physicians (11%) and business leaders (7%). A majority of respondents worked in pharmacy administration/operations (38%). The remaining respondents work for physician practices (n = 8) and pharmaceutical manufacturers (n = 12). Fifty of the 76 respondents were involved in formulary decisions (66%), with 20 of the 76 respondents being the formulary committee lead (26%).

3.2 Biosimilar Perceptions of Respondents

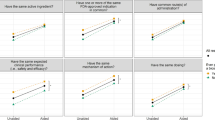

Responses for all survey respondents are shown in Fig. 1. For the first two items, results are ordered by degree of agreement from highest agreement to lowest. Eighty-eight percent of respondents agreed or strongly agreed that switching patients from a reference to a biosimilar is safe and efficacious. Similarly, 78% of respondents agreed or strongly agreed that it is safe and efficacious to extrapolate a biosimilar to all indications that a reference product holds. Percentages were similar for these two items across all respondents based on work environment except for physician practices, of whom 51% agreed or strongly agreed that it is safe and efficacious to extrapolate a biosimilar to all indications that a reference product holds, which is less than other respondents.

Survey results [n = 76]

The next eight items of the survey are displayed in Fig. 1 in order of high to low likelihood of the barrier’s ability to prevent biosimilar adoption. Respondents rated rebate increases of reference biologics to payers as the most likely to prevent adoption (85%). This barrier rated the highest for respondents from health systems (79%), physician practices (38%), and pharmaceutical manufacturers (83%) individually. Physician practice respondents more frequently answered neutrally to these eight items, while pharmaceutical manufacturers responded that health-system formulary slow adoption was the second largest barrier.

The last five items asked the respondents to rank adoption speed ordered from 1 (fastest) to 5 (slowest). Seventy seven percent of respondents rated acute care biosimilars, defined as being used for episodic treatment usually on an inpatient basis, as having a fast or very fast adoption speed, which was the highest of the five items. The remaining biosimilar groups listed in order of fast to slow (percent of respondents that answered ‘fast’ or ‘very fast’) were outpatient dialysis center (51%), curative targeted oncology (42%), outpatient infusion center (32%), and outpatient specialty/retail pharmacy (30%). Results were the same for all three cohorts of respondents, except pharmaceutical manufacturers listed outpatient infusion center biosimilars as slowest, with outpatient specialty/retail pharmacy as second slowest.

3.3 Commercial Medical Benefit Plan Analysis

A total of 89 out of 105 possible coverage statuses were reviewed to determine preferred status (~ 85% publicly available). Table 3 summarizes preferred status of biosimilars among the top 15 commercial medical benefit plans. The payer with the most policies to prefer a biosimilar was United Healthcare (6/7, 86%), who is also the largest commercial payer in terms of covered lives. Seven of the 15 payers (47%) had a clear preference to prefer biosimilars for four or more of the seven molecules. In contrast, seven of the 15 payers (47%) had a clear preference to prefer biosimilars for only two or fewer of the seven molecules. Blue Shield California fell between these numbers with three preferred statuses for biosimilars. Not all policies were readily available at time of evaluation, and Kaiser Foundation Health Plan had no publicly available policies at time of the search. Policies for filgrastim for Blue Cross Blue Shield HCSC (IL, NM, OK, TX, MT); pegfilgrastim for Blue Cross Blue Shield HCSC (IL, NM, OK, TX, MT) and Blue Shield California; bevacizumab and trastuzumab for Blue Shield California and CIGNA; and rituximab and reference infliximab for Blue Shield California could not be located.

The available products in the US for each of the seven molecules are displayed with the number of policies where they have a preferred status in Fig. 2. Some payers listed more than one product as preferred. Zarxio (filgrastim-sndz) had the most preferred statuses with 10/15 (67%). Retacrit (epoetin alfa-apbx) was a close second with 9/15 preferred statuses (60%). The only other biosimilar product with at least five preferred statuses was Inflectra (infliximab-dyyb) with 5/15 (33%); however, it is overruled by its reference competitor Remicade (infliximab), which had preferred status with 9/15 (60%) payers. Two other reference products had preferred statuses, Neulasta (pegfilgrastim) with 3/15 (20%), and Procrit (epoetin alfa) with 1/15 (7%). Six of the policies listed Remicade as the exclusively preferred product, with Neulasta being listed as exclusively preferred on one policy. Procrit was listed as preferred with Retacrit. No products containing the molecule rituximab had a preferred status at time of the search.

Preferred status of biosimilars from top 15 commercial payers

4 Discussion

Barriers to adoption of biosimilars have been identified and reviewed comprehensively in the medical literature [11,12,13,14,15,16,17]. A systematic review was recently performed to compile the available data of healthcare practitioner understanding, perceptions, and prescribing culture of biosimilars [10]. The majority of studies included in this review were set outside of the US (85%) and were primarily composed of specialty physicians (e.g., gastroenterologists and rheumatologists). Another recent study aimed to capture perceptions of biosimilar adoption of professionals that work for managed care organizations (MCOs), PBMs, and specialty pharmacies [12]. While numbers are small, the current survey captured pharmacists, physicians, and business leaders from health systems, physicians from physician practices, and professionals in the pharmaceutical industry. Similar to other studies, the survey respondents represent a unique and diverse group in many different healthcare settings.

Eighty-eight percent of respondents recognized FDA-approved biosimilars as safe and efficacious, and 78% agreed that biosimilar extrapolation to all indications the reference product holds is also safe and effective. The perception of safety and efficacy of indication extrapolation is much higher in this survey compared with the study by Greene et al. [12]. The differences seen between our study and the one previously mentioned could be because a large number of individuals surveyed in our study are involved in the formulary decision-making process, meaning their perceptions could be influenced by the financial incentives associated with using cheaper products at the health-system level. Further, another recent survey study assessed rheumatologist, dermatologist, and gastroenterologist attitudes regarding non-medical switching to a biosimilar in the US. Eighty-four percent of physicians in this survey expressed concern regarding non-medical switching in stable patients, while 60% of physicians believed that non-medical switching may have a positive impact on health-system costs [18]. Our survey did not adequately address this question, but this concept will be important as more biosimilars come to market, especially if interchangeability is possible for some biosimilars as they will likely be treated very similarly to generic small molecule drugs.

Eighty-five percent of respondents rated rebate increases of reference biologics to payers as the highest likelihood to prevent adoption. This perception was rated the highest for all three cohorts of respondents, which may be due to the small number of respondents. Previously referred to as the rebate trap, this barrier makes it difficult for the less expensive biosimilars to compete against the innovator brand product by keeping biosimilars off the health plan preferred drug tier, a tactic that is perceived by many as more pernicious than ordinary price competition. The barrier surrounding interchangeability was not anticipated to be rated the lowest of the group for this section of the survey. However, with the majority of respondents coming from health systems where they control their own formularies, this may not be as big of a perceived barrier compared with someone in a retail pharmacy or outpatient infusion center, where there is a greater need for interchangeability. The last five items of the survey showed that 77% of respondents viewed acute care biosimilars as having the fastest adoption speed. A reason for this fast adoption could be because molecules such as filgrastim saw the earliest biosimilar competition. In contrast, the categories of outpatient infusion center and outpatient specialty/retail pharmacy have seen the slowest adoption. One reason for slow adoption of these products, such as infliximab, may be attributed to patients using them as chronic treatment for inflammatory diseases such as rheumatoid arthritis. Response to these disease types are typically measured on a subjective scale rather than by objective lab values, and if patients are responding well to their current therapy, both they and their treating physician may be reluctant to change to a biosimilar. This same theory may also be applied to filgrastim biosimilars seeing fast adoption since effectiveness for this drug is typically measured objectively by calculation of the absolute neutrophil count. Results were similar for this portion of the survey across the three respondent cohorts.

Given the largest perceived barrier of rebate increases of reference biologics to payers as the highest likelihood to prevent adoption, the top 15 commercial payer policies in the US were evaluated for preferred status of biosimilars and their reference product. The aforementioned survey study stated that slightly more than one third of their respondents reported that their preference for biosimilars and reference biologics was based primarily on contracting rebates [12]. The Magellan Rx Medical Pharmacy Trend Report for 2019 reports that payers need on average at least a 21% discount on a drug in order to preference that drug. This same report states that 63% of payers preference the biosimilar over the reference product [19]. Contrastingly, a recent letter published in the Journal of the American Medical Association observed biosimilar coverage policies from the Tufts Medical Center Specialty Drug Evidence and Coverage Database and found that in 2019, US health plans covered biosimilars as preferred at an astonishingly low rate of only 14% [20].

In this analysis, seven of the 15 payers listed a preferred biosimilar for four or more of the molecules. The same number was found that have a preferred biosimilar for two or fewer of the molecules. Excluding Kaiser Foundation, which had no publicly available policies, for the seven payers with two or fewer preferred biosimilars, the included molecules were filgrastim, epoetin alfa, and infliximab. This coincided as being the three molecules with the most preferred status biosimilars. One important factor to note is that although an infliximab biosimilar had a preferred status on six policies, its reference product had a preferred status on nine policies. Further, the infliximab reference product was listed as the sole preferred product on six policies. This clear preference towards the infliximab reference product may be why respondents perceive outpatient infusion center biosimilars to have slow adoption. One study evaluated 2547 Medicare Part D plans and found that only 10% covered an infliximab biosimilar compared with 96% for the originator [21]. A no preference stance on biosimilars versus originator molecule may be viewed as an at-parity stance since payers do not clearly outline in their policies what products are preferred. This consideration should be weighed for health-system formulary managers and other pharmacoeconomic personnel when determining formulary stance.

The only molecule to have no products with a clear preferred status from all 15 evaluated payers was rituximab. Rituximab is the most recent of the seven molecules that were evaluated to face biosimilar competition, with its first biosimilar coming to market in November 2019. Policies were analyzed through March 15, 2020, and rituximab policies may have been updated during time of the analysis. One may infer that commercial payers are still determining their formulary stance on a preferred agent for rituximab. This same ideology can be further applied. The other two targeted oncology agents are starting to see a preferred stance on biosimilars from some payers with bevacizumab having four preferred status biosimilars, and trastuzumab having three. Both of these molecules first faced biosimilar competition in July 2019. Based on these three molecule launches and payer review, one might conclude it takes somewhere between 6 and 12 months for a payer to determine a preferred status for a molecule’s biosimilar.

5 Limitations

Survey respondents were limited in number with health systems dominating representation over physician practices and manufacturers. No third party was hired to conduct the survey, which may introduce bias since the researchers were responsible for all handling of data. Policies were obtained from a third-party service by the investigators, which may introduce bias. Additional bias may be introduced from health-system respondents as they may overlook clinical limitations in favor of heavy financial influence. The low number of respondents is likely a result of not providing any incentive to fill out the survey. The three cohorts of respondents recorded similar results. An increase in number may have identified different perceptions amongst the cohorts. The survey was closed-ended in design except for one question asking what the respondent’s professional specialty was. The closed-ended design may have precluded assessments of respondents underlying reasoning for how they answered questions. Future considerations would be to gather a larger number of survey respondents with open-ended questions to address these limitations.

Payers have annual review periods at different time points, meaning that preferred products may change at varying times. New biosimilar entrants are happening frequently which may also affect preferred product stance. Further, not all payer data was available for the payers evaluated. This is not only a limitation of this study, but a functional limitation of the commercial payer policy system. A health-system formulary leader attempting to make formulary decisions based on payer preferences would likely run into this same problem. Lastly, the reading and interpretation of payer policies was performed by a single researcher. Often, policies are not written in clear language, leaving much up to interpretation, which may be interpreted differently by a separate researcher or reader.

6 Conclusion

The professionals who responded to the survey have good insight into strategies to overcome biosimilar barriers to adoption. Many of them are involved in formulary decisions at the health-system level and are aware of the potential savings biosimilars can yield. Their responses should inform the medical community of what the greatest perceived barriers are to adoption of these cost-saving therapies. The perception of payer barriers to adoption and the perceptions surrounding fastest versus slowest adoption of certain groups of biosimilars aligned closely to what was found in terms of coverage on payer policies. Further, efforts by regulatory bodies are being made to help ensure a fair playing field. On March 9, 2020, the FDA in collaboration with the Federal Trade Commission (FTC) hosted a workshop to discuss the collaborative efforts to support appropriate adoption of biosimilars, discourage false or misleading statements about biosimilars, and deter anticompetitive behaviors [22]. Efforts such as these outlined by the FDA and FTC will be imperative to ensure a competitive market landscape to reduce cost for biologics. With more biosimilars in the pipeline, payer preferences should be monitored closely while the market matures with multiple biosimilars for the same molecule. Payers will be faced with the decision on which biosimilar(s) to list on the preferred tier. Unless the FDA approves products as interchangeable or state legislatures mandate interchangeability of products, health systems or clinics could potentially be forced to carry multiple biosimilars to ensure they have the proper one for the patient’s payer plan. All of these considerations should be heavily monitored as the next decade of biological medicine begins to ensure patient access and provider or health-system reimbursement.

References

Kamata M, Tada Y. Efficacy and safety of biologics for psoriasis and psoriatic arthritis and their impact on comorbidities: a literature review. Int J Mol Sci. 2020;21(5):1690.

U.S. Food and Drug Administration. Remarks from FDA Commissioner Scott Gottlieb, M.D., as prepared for delivery at the Brookings Institution on the release of the FDA’s Biosimilars Action Plan. FDA. https://www.fda.gov/news-events/press-announcements/remarks-fda-commissioner-scott-gottlieb-md-prepared-delivery-brookings-institution-release-fdas. Accessed 23 Apr 2020.

Patient Protection and Affordable Care Act of 2010. Pub L No. 111-148, 124 Stat 119.

Drug Price Competition and Patent Term Restoration Act of 1984. Pub L No. 98-417, 98 Stat 1585.

U.S. Food and Drug Administration. Biosimilars Action Plan: balancing innovation and competition. FDA. https://www.fda.gov/media/114574/download. Accessed 23 Apr 2020.

Mulcahy AW, Hlavka JP, Case SR. Biosimilar cost savings in the United States: initial experience and future potential. Rand Health Q. 2018;7(4):3.

Insulin Gains New Pathway to Increased Competition. FDA. https://www.fda.gov/news-events/press-announcements/insulin-gains-new-pathway-increased-competition. Accessed 23 Apr 2020.

U.S. Food and Drug Administration. “"Abbreviated Approval Pathways for Drug Product: 505(b)(2) or ANDA?" FDA website. https://www.fda.gov/drugs/cder-small-business-industry-assistance-sbia/abbreviated-approval-pathways-drug-product-505b2-or-anda-september-19-2019-issue#:~:text=A%20505(b)(2,reference%20or%20use%2C%20including%2C%20for. Accessed 1 July 2020

Drugs@FDA: FDA-Approved Drugs. FDA. https://www.accessdata.fda.gov/scripts/cder/daf/. Accessed 23 Apr 2020.

Leonard E, Wascovich M, Oskouei S, Gurz P, Carpenter D. Factors affecting health care provider knowledge and acceptance of biosimilar medicines: a systematic review. J Manag Care Spec Pharm. 2019;25(1):102–12.

Cohen H, Beydoun D, Chien D, et al. Awareness, knowledge, and perceptions of biosimilars among specialty physicians. Adv Ther. 2017;33(12):2160–72.

Greene L, Singh RM, Carden MJ, Pardo CO, Lichtenstein GR. Strategies for overcoming barriers to adopting biosimilars and achieving goals of the biologics price competition and innovation act: a survey of managed care and specialty pharmacy professionals. J Manag Care Spec Pharm. 2019;25(8):904–12.

Boccia R, Jacobs I, Popovian R, de Lima-Lopes G Jr. Can biosimilars help achieve the goals of U.S. health care reform? Cancer Manag Res. 2017;9:197–205.

Academy of Managed Care Pharmacy. AMCP Partnership Forum: biosimilars—ready, set, launch. J Manag Care Spec Pharm. 2016;22(4):434–40.

Sarpatwari A, Barenie R, Curfman G, Darrow JJ, Kesselheim AS. The US biosimilar market: stunted growth and possible reforms. Clin Pharmacol Ther. 2019;105(1):92–100.

Hakims A, Ross JS. Obstacles to the adoption of biosimilars for chronic diseases”. JAMA. 2017;317(21):2163–4.

Oskouei AT. Following the biosimilar breadcrumbs: when health systems and manufacturers approach forks in the road. J Manag Care Spec Pharm. 2017;23(12):1245–8.

Teeple A, Ellis LA, Huff L, et al. Physician attitudes about non-medical switching to biosimilars: results from an online physician survey in the United States. Curr Med Res Opin. 2019;35(4):611–7.

Magellan Rx Management Medical Pharmacy Trend Report, 2019. Tenth Edition. MagellanRx. https://www1.magellanrx.com/documents/2020/03/mrx-medical-pharmacy-trend-report-2019.pdf/. Accessed 1 July 2020.

Chambers JD, Lai RC, Margaretos NM, et al. Coverage for biosimilars vs reference products among US commercial health plans. JAMA. 2020;323(19):1972–3.

Yazdany J, Dudley RA, Lin GA, et al. Out-of-pocket costs for infliximab and its biosimilar for rheumatoid arthritis under Medicare Part D. JAMA. 2018;320(9):931–3.

Public workshop: FDA/FTC workshop on a competitive marketplace for biosimilars. FDA. https://www.fda.gov/drugs/news-events-human-drugs/public-workshop-fdaftc-workshop-competitive-marketplace-biosimilars-03092020-03092020. Updated 7 Apr 2020. Accessed 30 Apr 2020.

RED BOOK Online. Micromedex Healthcare Series [database online]. Greenwood Village, CO: Truven Health Analytics; 2015. Accessed 4 Mar 2020.

Author information

Authors and Affiliations

Contributions

KH: This author helped in the drafting, research, review, and communication to complete the manuscript. JB: This author helped in the research, review, and feedback to complete the manuscript. BB: This author helped in the drafting, review, and feedback to complete the manuscript. KB: This author helped in the review and feedback to complete the manuscript.

Corresponding author

Ethics declarations

Funding

None received.

Conflict of interest

None to report or disclose.

Availability of data and material

Readily available.

Ethics approval

Received from University of Tennessee Institutional Review Board.

Consent to participate

Not applicable.

Consent to publish

Not applicable.

Code availability

Not applicable.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Herndon, K., Braithwaite, J., Berry, B. et al. Biosimilar Perceptions Among Healthcare Professionals and Commercial Medical Benefit Policy Analysis in the United States. BioDrugs 35, 103–112 (2021). https://doi.org/10.1007/s40259-020-00463-6

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40259-020-00463-6