Abstract

Objective

The Affordable Care Act is currently in the roll-out phase. To gauge the likely implications of the national policy we analyze how the Massachusetts Health Care Reform Act impacted various hospitalization outcomes in each of the 25 major diagnostic categories (MDC).

Methods

We utilize a difference-in-difference approach to identify the impact of the Massachusetts reform on insurance coverage and patient outcomes. This identification is achieved using six years of data from the Nationwide Inpatient Sample from the Healthcare Cost and Utilization Project. We report MDC-specific estimates of the impact of the reform on insurance coverage and type as well as length of stay, number of diagnoses, and number of procedures.

Results

The requirement of universal insurance coverage increased the probability of being covered by insurance. This increase was in part a result of an increase in the probability of being covered by Medicaid. The percentage of admissions covered by private insurance fell. The number of diagnoses rose as a result of the law in the vast majority of diagnostic categories. Our results related to length of stay suggest that looking at aggregate results hides a wealth of information. The most disparate outcomes were pregnancy related. The length of stay for new-born babies and neonates rose dramatically. In aggregate, this increase serves to mute decreases across other diagnoses. Also, the number of procedures fell within the MDCs for pregnancy and child birth and that for new-born babies and neonates.

Conclusions

The Massachusetts Health Care Reform appears to have been effective at increasing insurance take-up rates. These increases may have come at the cost of lower private insurance coverage. The number of diagnoses per admission was increased by the policy across nearly all MDCs. Understanding the changes in length of stay as a result of the Massachusetts reform, and perhaps the Affordable Care Act, requires MDC-specific analysis. It appears that the most important distinction to make is to differentiate care related to new-born babies and neonates from that related to other diagnostic categories.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Universal health insurance decreases the probability of being uninsured |

Universal health insurance increases the number of diagnoses in most categories |

1 Introduction

In March 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. One of the primary goals of the legislation is to achieve close to universal enrollment in health insurance. Since not all of the features of the law will become effective until 2020, we can only speculate about its full impact at this point. The PPACA, however, was modeled after the Massachusetts health insurance law, known as Chapter 58, which was signed into law by Mitt Romney in 2006. Chapter 58 was also designed to bring about nearly universal health-insurance coverage within its jurisdiction. For the purpose of this study, some of the more important features of Chapter 58 are an expansion of subsidized insurance provision for low-income individuals; the employer mandate that requires employers with 11 or more full-time equivalent employees to provide health insurance coverage with a certain contribution to the workers’ health-insurance premium; and the individual mandate that requires Massachusetts adults to have a minimum standard of coverage. The individual mandate makes Massachusetts’s Chapter 58 the first law that requires individuals to purchase health insurance. (See The Massachusetts Health Insurance Connector Authority [1] for more details about these and other provisions of the law).

In their latest report, The Massachusetts Health Insurance Connector (MHIC) Authority [2] claims success in achieving many of the goals laid out in the law. As of 2008, Massachusetts had the highest health-insurance coverage rate in the USA. Several studies support the claims of increased enrollment as a result of the law [3–6]. The MHIC Authority claims to achieve this success without a significant replacement of private insurance with public insurance (crowd-out), and with high compliance. The suggestion of a lack of crowd-out is supported by the findings of Long et al. [4]; however, they are disputed by Yelowitz and Cannon [5] who find evidence in the Current Population Survey for the year 2008 that the mandate induced uninsured residents to conceal their true insurance status. Furthermore, they also find that subsidized health insurance crowds out private insurance among low-income adults and children. The MHIC Authority has been curiously silent on this finding. In addition, Yelowitz and Cannon also find that the law caused a slow-down in migration of young adults into Massachusetts.

Chapter 58 presents health-care providers with a complex mix of provision of care incentives that differ by the presence and type of health insurance. Also, while the primary goal of Chapter 58 was to increase insurance take-up rates, the act also caries provisions related to measuring and improving the quality and efficiency of care delivery. Even for those most intimately associated with health-care provision, predicting changes in patient outcomes as a result of Chapter 58 proved difficult. Cozad [7] suggests that industry preparation for health-insurance expansion revealed both uncertainty and caution. Providers, Cozad suggests, chose excess capacity rather than the possibility of turning patients away. Cozad and Wichmann [8] point to a reduction in the technical efficiency of health-care provision as a result of excess capacity build-up in anticipation of health-insurance expansion.

The first study to analyze the impact of the Massachusetts mandate using inpatient hospital data is by Kolstad and Kowalski [6]. They use a difference-in-difference framework to compare various outcomes before and after the law was enacted relative to changes in other states. The authors find evidence for crowd-out among the hospitalized population (there is no evidence for crowd-out based on their analysis of the Current Population Survey, though). Furthermore, Kolstad and Kowalski also find no evidence that the number of discharges changed after the health-care reform. The authors, however, find that the law significantly decreased length of stay, especially for long hospital stays. The magnitude of this change, 0.05 days, which is approximately 1 % of the mean stay, is rather small, though. At the same time, the Massachusetts reform does not seem to have altered the trend in cost growth. Using hospital level data, Cozad [7] agrees with the lack of change in the demand of care, but provides a much larger estimate of a 27 % reduction in average length of stay. These disparate results highlight the need for more work in this area.

Changes in emergency room (ER) utilization could serve as an important litmus test of policy performance. A reduction in ER visits would be seen as an improvement in the efficiency of health-care delivery. While very costly to providers, these visits are the primary form of health-care service utilization for many uninsured. Expanding health insurance could decrease ER visits if insured individuals seek out alternatives including preventive care. At the same time, lower out-of-pocket expenses, brought about by a near universal health-insurance coverage, could increase the use of ER visits. Estimates of the impact on ER visits are inconclusive. In a straight forward analysis of the trends, Chen et al. [9] look at quarterly ER visits to see whether health-insurance expansion decreased or increased use of ER resources (both inpatient and outpatient ER use)Footnote 1 and find no evidence for a change in trend after the Massachusetts Health Care Reform compared to trends in surrounding states. The lack of a clear change in trend could be explained by the results of Miller [10]. The paper investigates the impact of the Massachusetts Health Care Reform on outpatient ER visits. She takes advantage of the fact that counties vary in the fraction of residents with and without insurance. Her argument is that the impact of the law will be stronger in counties with lower insurance propensity before 2007. She also uses a state level analysis with some northeastern states serving as the comparison group. She finds that the law has decreased ER visits that can be treated in a physician’s office, and that it has increased visits for non-preventable emergency situations. Using different outcomes, Kolstad and Kowalski [6] and Cozad [7] find that Chapter 58 reduced ER utilization. Kolstad and Kowalski find that inpatient admissions originating from the ER declined (by 5.2 %) after the Massachusetts reform, which may indicate better use of preventive care, while Cozad finds that ambulance trips were reduced by 16 % in the wake of the law.

We contribute by examining how patient outcomes change by major diagnostic category (MDC), which could help mitigate the inefficiencies created by uninformed capacity build-up. Data on hospital utilization also contain information on insurance status, allowing for an analysis of the primary purpose of the law. MDCs are created based on the principal International Classification of Diseases, Ninth Revision, Clinical Modification (ICD-9-CM) diagnoses that are grouped into one of 23 mutually exclusive MDCs corresponding to a single organ system or into MDC 24 (trauma) or MDC 25 [Human immunodeficiency virus (HIV) infections]. Building on the work by Kolstad and Kowalski [6] we investigate whether the Massachusetts Health Care Reform had differential impact across MDCs (for a list of the MDCs see the Appendix). Examining the impact of the law by MDC allows for the possibility of uncovering more granular effects that may be masked by an analysis at a more aggregate level.

2 Data and Methodology

To analyze the impact of the Massachusetts Health Care Reform we use the Nationwide Inpatient Sample (NIS) from the Healthcare Cost and Utilization Project [11]. The NIS contains data on a 20 % sample of US community hospitals. Data are available for all discharges in a year when the hospital is included in the sample; however, the sampled hospitals may change from year to year. Our sample is restricted to Massachusetts and other northeastern states (namely, New York, Connecticut, Maryland, Vermont, and Rhode Island) for the 2004 to 2009 time period.Footnote 2 Using this sample, both years before and after the law are included to allow for a difference-in-difference analysis. The sample is further restricted to those below the age of 65 years. The unit of observation is a hospital discharge. Since individuals may be hospitalized several times a year we may have multiple information for the same individual, yet due to the lack of individual identifiers we cannot control for such reoccurrence.

The first outcome we analyze related to the primary purpose of the law, namely universal health insurance, is insurance status. The NIS is not the ideal data set to analyze this outcome because the data are not representative of the general population; rather the sample is selective of those who are treated in hospitals. Nonetheless, the NIS can be used to analyze what happened to the composition of patients. Since the main objective of the law was to increase the number of individuals with insurance, we expect that the probability that a patient pays out-of-pocket decreases, and in line with making Medicaid eligibility more generous, we expect that the probability of having Medicaid increases. It is harder to form expectations about the proportion of those with private insurance. The ratio could increase given that employers have to provide insurance and individuals are required to carry some health-insurance coverage. The mandate provision alone would increase the share of privately insured individuals. On the other hand, more generous public insurance could crowd-out private insurance provision. Thus, it is an empirical question that has gained wide attention because Massachusetts’ experience can be looked at as a prediction of what we can expect when all of the provisions of the federal health-care reform come into effect.

In creating the main independent variable of interest, we follow Kolstad and Kowalski [6] who acknowledge that some features of the law came into effect later than others, and therefore use two variables: one (called After) for the time periods after 2007 Q3, and a separate one (called During) for the time periods from 2006 Q3 to 2007 Q3. The main reason for doing this is that while the Medicaid expansion took place right after the law was signed, another important change, the individual requirement came into effect in July 2007. Since Massachusetts did not provide information in Q4 in years 2006 and 2007, those quarters are discarded from the sample.

We estimate the following model:

where Y iht is one of the outcome variables such as payer or insurance type, length-of-stay, number of diagnoses, number of procedures for discharge i, in hospital h, in time t. In the case of a binary outcome variable we estimate a linear probability model. Our coefficients of main interest are α and β, two coefficients that measure the magnitude of the Massachusetts Health Care Reform on the given outcome variable relative to the control states. A set of individual and hospital characteristics, such as age, sex, a dummy for race (1 if black or Hispanic and 0 otherwise), three dummy variables for the median household income for the zip code of the individual’s residence, and two dummy variables for hospital size, as well as a constant are included in X.Footnote 3 The models also include quarter fixed effects and hospital fixed effects. Hospital fixed effects are especially important given that hospitals change in the sample. Not including hospital controls could bias the results in the likely case that different hospitals have different patient profiles. For instance, if hospitals whose patient profiles include a proportionately larger frequency of more serious cases are selected in the sample in health-care reform years, not controlling for hospitals could result in spurious correlation.

3 Results

Table 1 lists the major diagnostic categories along with the means and standard deviations of our dependent variables of interest, in Massachusetts before the law went into effect.Footnote 4 MDCs are listed in order of the number of discharges in the data covering the six states: Massachusetts along with the control states during the 2004 to 2009 time period. The most frequent diagnostic groups are pregnancy (MDC 14) and new-born babies (MDC 15) both well over 600,000 discharges while the least frequent inpatient hospitalization is burns (MDC 22) with a little over 4000 discharges in the analyzed time period.

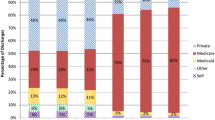

The first column of Table 2 in the appendix shows the coefficient estimates α and β of Eq. 1 when the outcome variable is 1 if the primary payer is Medicaid and 0 otherwise. Models are estimated separately for each MDC and only the main coefficients of interest are reported, but all models include the variables from Eq. 1.Footnote 5 Coefficient estimates are positive in the After period for all MDCs, with the exception of burns, suggesting that the probability of paying with Medicaid increased because of the reform. The coefficients in the After period are also overwhelmingly significant with 24 of the 25 MDCs being statistically significant. The magnitude of the increase is around 2 or 3 percentage points and ranges from as small as 2.2 percentage points to as high as 10.6 percentage points in the case of alcohol/drug use category. The results suggest that the law already increased the probability of Medicaid payment between Q3 2006 and Q3 2007, and that in most cases this increase is also present after July 2007.

The second column of Table 2 presents the estimates of the main coefficients when the outcome variable is 1 if the patient is privately insured and 0 otherwise. The estimates are overwhelmingly negative suggesting that the law decreased the probability of paying with private insurance. However, there are more disease categories where the coefficient estimates are not significantly different from zero here than in the models predicting payment by Medicaid.

The third column of Table 2 presents coefficient estimates from the model estimating the probability of being uninsured [the outcome variable is 1 if primary payer is the patient, or the patient is not charged for the treatment (for instance, charity care) and 0 otherwise]. Similar to coefficients in the second column, most of the coefficients are negative; however, they are in this case overwhelmingly statistically significantly different from zero. The results are especially strong for the MDC of alcohol/drug use, in which case the probability of being uninsured decreased by about 10 percentage points after the law, which is almost a 50 percent drop considering that before the law about 23 % of this group was uninsured.

The fourth column of Table 2 shows the impact of the law on length of stay. Coefficient estimates suggest that the law (at least marginally) significantly reduced length of stay in the following larger MDC groups: diseases of the circulatory system (by around 6.4 %), diseases of the musculoskeletal system (by 7.7 %), diseases related to alcohol/drug use (by 15.1 %), as well as four further, smaller MDCs: infectious and parasitic diseases (by 9.5 %), injuries, poisonings and toxic effect of drugs (by 11.4 %), and factors influencing health status (by 11.3 %). At the same time, length of stay increased by about 11.1 % in the category of new-born babies and neonates.

Column 5 of Table 2 shows coefficient estimates of models predicting the number of diagnoses on each discharge. The outcome variable is truncated at 15, because Massachusetts reports up to 15 diagnoses during the analyzed time period. Even though some of the control states report up to 30 diagnoses, in order to be consistent with the Massachusetts data, we truncated those to 15 as well. Less than 3 % of the discharges have more than 15 diagnoses in our sample. Results suggest that the law increased the number of diagnoses by between 3.7 and 15 %. The new-born babies and neonates MDC is again an exception as the number of diagnoses decreased by 3 % due to the law.

Finally, column 6 of Table 2 presents the impact on number of procedures. There is no consistent pattern for the impact on the number of procedures. Nine of the 25 categories had at least one (at least marginally) significantly negative coefficient, while another seven had positive and significant coefficients, the remaining nine categories had no significant impact. The two largest MDCs, the pregnancy and childbirth related groups, had a decrease in the number of procedures due to the law, while the third largest category, the diseases of the circulatory system, had more procedures after the law came into effect.

4 Discussion

The purpose of this work was to examine the impact of the Massachusetts reform on insurance coverage and patient outcomes. The results, taken as a whole, demonstrate that the reform decreased the percent of patient visits that were uninsured. Very few of the MDC-specific results related to the probability of being uninsured were both positive and significant; of the few that were, the results for After and During were contrary in sign. Similarly, the percentage of patient visits that were privately insured fell as a result of the policy change.

One way that our results could be misconstrued would be to assume that these results imply that more individuals are insured and that the reform led to crowd-out. The data do not speak to insurance coverage or patient outcomes for individuals, but for patient visits. In certain disease categories the positive coefficient in the Medicaid model and the negative private coefficient could suggest that the Massachusetts Health Care Reform caused crowd-out. However, this evidence could be driven by factors other than crowd-out. For instance, it could be that the law changed treatment methods such as intensity (either on the demand side and/or on the supply side) and Medicaid patients became more frequent users of hospital services. It could also be that (the same number of) Medicaid patients went for inpatient treatments more often. Our results speak more directly to the main concern for health-care providers, meeting an uncertain change in demand efficiently. In many ways the bottom line is the provision of care and the cost and resource demand of doing so. From this perspective, patient visit makes for a more informative unit of observation.

Our results also provide finer detail by breaking down changes in insurance coverage and patient outcomes by MDC. We show that the law differentially impacted disease categories. For instance, while Kolstad and Kowalski [6] find that length of stay decreased by 1 %, we show that, once we break up the data into MDCs, the decrease is quite pronounced on certain groups; however, the category responsible for a large fraction of inpatient stays, new-born babies and neonates, had longer stays after the law. This increase was also reflected in the pregnancy category. The broader results suggest that these two MDCs are different and should be examined separately from the others.

While our results reveal heterogeneity in the impact of the Massachusetts reform, they do little to inform the underlying cause. It may be that changes in insurance coverage are driving the differences in patient outcomes. These disparate changes could also be driven by changes in other aspects of the underlying patient mix. Alternatively, it could be that other aspects of Chapter 58 are causing the MDC specific results. For example, it could be that the creation of the Health Care Quality and Cost Council is influencing the behavior of health-care providers. Informing the underlying causes of the disparate impacts, while outside of the scope of this paper, remains fertile ground for future research.

5 Concluding remarks

The MHIC Authority claims initial success with improving access to routine care by reducing the uninsurance rate. Our results indicate a mixed effect. The probability of a patient being covered by Medicaid increased because of the law, while the probability of being covered by private insurance decreased. In addition, our results show that the law differentially impacted disease categories.

While we are beginning to obtain insight into the effect of near universal insurance, a few important questions remain. For example, how much does universal health insurance cost and does universal health insurance contribute to improved health outcomes? Proponents of health-care reform argue that universal health insurance will slow the growth rate of health-care costs, but opponents argue that it will escalate health-care costs even faster. As Bebinger [12] says about the Massachusetts Health Care Reform: “[IT] has one big Achilles’ heel: rapidly rising health-care costs threaten to scuttle hundreds of other programs in the state budget…” Evaluating the economic effectiveness of Massachusetts’ Chapter 58 requires understanding the full costs of the program. The implications of the effectiveness of Chapter 58 are worthy of study and they become even more relevant given the similarities between the regulation under study and the Patient Protection and Affordable Care Act.

Notes

In this paper, emergency room (ER) visits that result in admission to the hospital are considered inpatient ER use and those that do not are considered outpatient ER use.

Kolstad and Kowalski [6] investigate on a sample ranging from 2004 to 2008; however, instead of just some northeastern states they include 41 states as a control group in their sample.

Income and hospital size dummy variables are used as defined in the NIS. Income is a quartile classification of median household income for the patients’ zip code. The income quartiles are updated annually. In 2006 the quartiles were less than $37,999, $38,000–$46,999, $47,000–$61,999, and greater than $62,000, respectively. Hospital size is based on an urban-teaching status matrix. For example, for an urban teaching hospital, small, medium, and large hospitals are defined as less than 249 beds, 250–424 beds, and more than 425 beds, respectively.

Please see the Electronic Supplementary Material for full details of summary statistics and model estimation.

References

Report to the Massachusetts Legislature: Implementation of the Health Care Reform Law, Chapter 58, 2006–2008. The Massachusetts Health Insurance Connector Authority 2008.

Report to the Massachusetts Legislature: Implementation of the Health Care Reform, Fiscal Year 2010. The Massachusetts Health Insurance Connector Authority 2010.

Chandra A, Gruber J, McKnight R. The importance of the individual mandate—evidence from Massachusetts. N Engl J Med. 2011;364(4):293–5.

Long SK, Stockley K, Yemane A. Another look at the impacts of health reform in Massachusetts: evidence using new data and a stronger model. Am Econ Rev Pap Proc. 2009;99(2):508–11.

Yelowitz A, Cannon MF. The Massachusetts health plan: much pain, little gain. Policy Analysis Working Paper 657. 2010.

Kolstand JT, Kowalski AE. The impact of health care reform on hospital and preventive care: evidence from Massachusetts. J Public Econ. 2012;96(11–12):909–29.

Cozad M. Better to be safe than sorry? The supply side effects of Massachusetts health care reform on hospitals. Working Paper, Furman University. 2012.

Cozad M, Wichmann B. Efficiency of health care delivery systems: effects of health insurance coverage. Appl Econ. 2013;4(29):4082–94.

Chen C, Scheffler G, Chandra A. Massachusetts’ health care reform and emergency department utilization. N Engl J Med. 2011;365(e25):1–3.

Miller S. The effect of insurance on outpatient emergency room visits: an analysis of the 2006 Massachusetts health reform. J Public Econ. 2012;96(11–12):893–908.

HCUP Nationwide Inpatient Sample (NIS). Rockville, MD: Healthcare Cost and Utilitization Project (HCUP), Agency for Healthcare Research and Quality; 2004–2008.

Bebinger M. Mission not yet accomplished? Massachusetts contemplates major moves on cost containment. Health Aff. 2009;28(3):1373–81.

Acknowledgments

We would like to thank the Editor, Tim Wrightson and two anonymous reviewers for helpful comments. The authors alone are responsible for findings and views contained in this paper.

Financial support from the Rea and Lillian Steele Summer Grant and the Center for Faculty Scholarship, both at the Valdosta State University, for A. Cseh is gratefully acknowledged. B. Koford would like to acknowledge support from the Smith Research Fellowship, John B. Goddard School of Business and Economics, Weber State University.

Conflict of interest

The authors have no conflicts of interest to declare.

Author contributions

A. Cseh designed and estimated the econometric models and is the lead author. A. Cseh, B. Koford, and R. Phelps contributed to the discussion and evaluation of the literature, interpretation of data, and writing of the manuscript. The authors share responsibility for guaranteeing the content of this research.

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendix

Appendix

See Table 2.

Rights and permissions

About this article

Cite this article

Cseh, A., Koford, B.C. & Phelps, R.T. Hospital Utilization and Universal Health Insurance Coverage: Evidence from the Massachusetts Health Care Reform Act. Appl Health Econ Health Policy 13, 627–635 (2015). https://doi.org/10.1007/s40258-015-0178-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40258-015-0178-1