Abstract

The plastic industry is widely spread in the world, with plastic injection moulding being the most popular technique due to its high efficiency and cost-effectiveness. In the competitive scenario, when thousands of pieces are produced per day, it is important for the manufacturers to evaluate and improvise the cost per component and productivity rate as even a small change can bring significant improvements in the profits. Various cost factors are considered for cost estimation of plastic injection-moulded component such as material, mould, processing and post-processing costs. Mould cost being very high is a major cost component and differs when using straight drilled conventional cooling channels compared to the one using channels conforming to the shape of the component. For parts having an intricate shape and high precision, it is always recommended to use conformal cooling channels as they reduce the defects and cycle time. The manufacturing cost also depends on component size, number of cavities, cycle time and labour cost. Another important parameter influencing production cost is the cycle time and cooling time. With the use of conformal cooling channels, processing cost can be reduced by reducing cycle time, thereby improving the production rate. In this paper, a comparative economic analysis is performed for a plastic injection-moulded product manufactured using conventional cooling channels with the one manufactured using conformal cooling channels.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Injection moulding is the most popular technique for plastic processing owing to its high efficiency and cost-effectiveness. Therefore, it has emerged enormously worldwide for making basic and complex plastic parts. Many design customizations are carried out to meet the requirements of the consumer while controlling part rejections. Conformal cooling is proven to improve cycle time and product quality for complex-shaped customized components. Previous researches substantiate that conformally cooled channels in plastic injection moulding reduce cooling time, thereby shortening the production cycle to an economic length and improving product quality compared to conventional mouldin [1,2,3,4]. However, conformal cooling channels need to be manufactured using non-traditional processes which increases the mould cost compared to the conventional approach.

The mould (which is sometimes called the die) refers to tooling used in the injection moulding process and is the major contributor in the overall production cost. The moulds are majorly made of stainless steel. However, aluminium can also be used for cost reduction. The manufacturing cost of these moulds depends on various factors such as size of the part, number of cavities, surface finish required and complexity of the part. The initial cost of the mould is high; however, with large production volumes, cost per piece decreases. Total manufacturing cost involves many other variables including material used, labour, cycle time, maintenance cost, overhead cost, assembly cost and other costs.

Cycle time is another parameter that significantly influences the cost of injection-moulded component. Therefore, it is essential to reduce cooling time by improvising conformal cooling channels for improving the overall production rate and cost. Conformal channels are placed in close proximity with the cavity to provide maximum heat dissipation and improvement in overall quality of the finished product. Conformal channels also reduce defects caused due to uneven solidification rate resulting in fewer rejections.

Therefore, cost estimation and economic analysis of injection-moulded component is essential for manufacturers to develop an understanding of various parameters influencing overall productivity and compare the overall production cost involved in two approaches. Furthermore, breakeven analysis is to be carried out to justify the use of conformally cooled injection moulds for a given production volume.

This paper aims at developing cost models for plastic injection-moulded components using conformal cooling channels with those using conventional cooling channels. Furthermore, it aims at comparative economic analysis and breakeven analysis for the selected approaches in injection moulding using a case study approach. Many researchers have done a detailed study of cost models and developed a costing equation. Franchetti and Kress (2016) developed a cost model for plastic injection-moulded component, which included material cost, mould cost, processing cost and post-processing cost as the main costing heads. The breakeven analysis emphasized that injection moulding is a cost-effective choice for larger batch size. It was concluded that injection moulding offers speed and cost benefits compared to AM for large production runs [5]. Turc et al. (2017) developed a cost model for injection-moulded cost having three main components, namely mould cost, equipment cost and material cost. The software developed estimated mould cost considering design aspects such as part dimensions, geometric shape, internal and external undercuts. It was concluded that cavity complexity greatly affects initial mould cost [6]. Cooling channels complexity negatively affects the mould cost, which may delay the breakeven point. Minguella-Canela et al. (2020) performed an economic analysis of redesigned cooling inserts with conformal cooling channels using additive manufacturing. Various cost components were preparation costs, annual costs of equipment and tooling, processing cost per part and cost of other factors independent of batch size. Simulation of conformal cooling channels revealed the decrease in injection material temperature distribution that positively affects reduction in the cooling time and cycle time [7]. Huang et al. (2017), while presenting a case study of injection mould tooling using distributed additive manufacturing, developed a life cycle cost (LCC) model considering four major cost components: material cost, machine cost, labour cost and energy cost. Few other factors considered in LCCs for designing, process planning, assembling and testing in mould manufacturing, as well as inspection, diagnosis, disassembly and assembly in mould maintenance and repair [8]. Charalambis et al. (2017) while analysing integration of additive manufacturing with plastic injection moulding utilized a cost model for injection-moulded parts considering three major components: mould cost, material cost and processing cost. Three cost components are mainly influenced by the part size, geometry, complexity and material. Cost per part is also highly influenced by production volume. Mould cost mainly comprises the cost of mould base and inserts, which are dependent on number of cavities. Material cost considered the weight of part, runners and sprue, whereas processing cost included set-up cost, machining cost considering hourly capacity of the machine and hourly cost of operators. Economic analysis proved that AM inserts provide cost savings only for pilot production, whereas for large batch sizes conventional manufacturing approach is more suitable [9]. Vasco and Barreiros (2019) evaluated economic impact of AM conformal cooling channels in the injection moulding process. They considered tool costs, material costs and energy costs. Breakeven analysis carried out by comparing production costs and injection cycle for conventional and conformal cooling approach revealed that higher production volume can justify the use of conformally cooled injection moulds [10]. Kampker et al. (2020) performed economic analysis for integrated additive manufacturing with injection moulding for the fabrication of polymer tools. The cost model included tool cost per part over the tool life, processing cost per part and material cost per part. Furthermore, tool manufacturing cost mainly included the cost for mould base and tool inserts. The mould base cost was depreciated over its life cycle (roughly two million injection shots), while the cost of inserts was depreciated over the required job size for more accurate cost per part. Material cost was calculated considering total weight of the material considering part, runner, sprue weights and wastage. Processing cost per part included machine set-up cost, operator and machine cost per part. The cost model developed can be utilized for economic assessment and selection of the mould manufacturing method considering the requirements of use case [11]. Tosello et al. (2018) developed cost models for the comparison of injection moulding with additive manufacturing. Three main cost components included tool cost, material cost and production cost. The comparison proved that AM inserts in moulding provide cost savings as tool cost is the major contributor and a reduction in time required to manufacture inserts compared to CNC inserts. However, the tool life for metal inserts manufactured with CNC was found to be much higher compared to AM inserts. Therefore, it was concluded that integrating AM with injection moulding is advisable for small production volume and is suitable for pilot production to achieve higher operational effectiveness [12]. Patil et al. (2016) discussed about additive manufacturing like rapid prototyping with metal powder deposition techniques for making various components [13].

From the literature reviewed, it is evident that many researchers have developed cost models for injection-moulded components and conducted breakeven analysis for estimating economic lots. Conformally cooled injection moulds have been preferred for complex geometries due to improved cycle time and product quality. However, its effect on the product cost needs to be analysed and compared with the conventional approach. Therefore, it is crucial to perform economic analysis and breakeven analysis of conformally cooled injection moulds.

Methodology

The methodology includes the development of an extended cost model for injection moulding part using conventional and conformal cooling channels followed by economic analysis and breakeven analysis for two approaches using a case study of the spray bottle funnel. Figure 1 indicates the details of spray bottle funnel used for comparative economic analysis of conformal and conventional cooling approach in plastic injection moulding process.

Details of spray bottle funnel

A methodology flow chart is explained in Fig. 2 to give an overview of the costing.

Methodology flow chart

Cost Model for Injection-Moulded Component

It is a generic formula derived from all the major costs included in making a finished part using injection moulding process.

Major sub-heads in the cost of moulded component are material cost, mould making cost (tooling cost), processing cost and post-processing cost. The following components are considered under various sub-heads for calculating the cost of plastic injection-moulded part.

Raw Material Cost (C RM)

In plastic injection moulding process, raw material cost is the total cost of resin needed to make one part, including the material used in the sprue and runners. The per-piece material cost is calculated by multiplying the total weight of material used in one injection cycle with the price of the resin and then dividing this by the number of cavities in the mould (i.e. the number of parts produced per cycle). Rejection losses are also to be considered for accurate estimation of material cost.

Cycle Time (t c)

The cycle time comprises injection time, packing time, cooling time and ejection time. Cooling time takes most of the cycle time as compared to other time components.

Mould Cost (CM)

The mould cost is basically comprised of mould design cost, mould material cost and mould manufacturing cost including the cost of cooling channels. The cost of material used for mould depends on part dimensions, total mould volume with margins and passage for the cooling channels. The margins are generally 1.5″–2″ from the part. It also depends on depth of the part and number of cavities. The mould cost also includes the core and cavity making charges. The material cost varies with the material selected for the mould and is generally Steel P25.

In conventional approach, straight drilled channels can be prepared by using drilling or milling process, whereas the conformal approach requires non-conventional processes such as wire electro-discharge machining (EDM), additive manufacturing. Accordingly, the cost of cooling channel significantly differs for the two approaches.

Processing Cost (Cp)

It refers to the cost of manufacturing one component considering the machine shift rate (machine and labour cost) and production rate considering process efficiency. Cycle time being the main factor influencing production rate, choice of cooling channel significantly affects this cost component.

Miscellaneous Overheads (C MO)

These overheads include factory rent, power consumption, water charges and many other costs related to property and trade.

Assembly Cost (C A)

It is the cost of labour required for mould assembly and machine set-up.

Mould Maintenance Cost (C MM)

This is the cost of preventive and corrective maintenance required in machine operations.

Post-Processing Cost (C PP)

Post-processing includes part ejection, gate cutting, inspection and packaging costs.

Transportation Cost (C TP)

This cost includes transportation changers for raw material and finished product.

The cost model developed for plastic injection-moulded component considering various cost factors as explained above is mentioned in Eqs. (1) and (2).

For the part under consideration, around 5% of part rejections per shift are observed. Therefore, production per shift with allowance is computed after considering rejections due to scrap.

Nomenclature for various terms used in the cost model is mentioned in Table 1.

Furthermore, comparative economic analysis is performed for a case study of spray bottle funnel manufactured using conventional and conformal cooling approach.

Results and Discussion

Economic Analysis Using Case Study of a Spray Bottle Funnel

In this case study, the cost estimation for a spray bottle has been carried out for conventional and conformal cooling approaches. The spray bottle is made of the material polypropylene copolymer plastic granules (PPCP). This material is a colourless and non-inflammable solid, widely used in making industrial products such as boxes, food containers, industrial packaging, home care, surgical equipment, appliances, toys and other applications. Gross weight of raw material required per component comprises shot weight, runner weight, rejection loss and miscellaneous loss which is considered for calculating raw material cost per component.

The machine tonnage depends on the clamping force required. For the component under consideration, press with 120 ton capacity is used. A number of cavities play a significant role for plastic pieces ranging from 50 to 100 gm. The number of cavities also depends upon the product type and machine tonnage. In a generalized way, for part weight between 50 to 100 gm, a die of four cavities can be considered.

The mould cost for plastic injection is calculated considering raw material cost, channel cost, design cost, assembly cost and miscellaneous overhead. Designing cost is generally considered as 2% of overall mould cost. The machining cost is also a major cost component involving different types of machining processes used to make mould and cooling channels. Generally, production volume may not be accurately defined at the time of mould manufacturing; therefore, mould cost per component is roughly calculated considering mould tool life of 20 million pieces. Cooling channel cost also included in the mould cost, which depends on the intricacy of the channel designed and overall length of the channel. Conventional straight drilled channels generally have lower cost than the moulds having channels that are conformal.

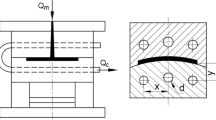

Figure 3 provides design of conventional and conformal cooling channels designed for spray bottle funnel used in the current analysis. The cooling channels were designed using SolidWorks 20. The channel diameter is 10 mm and is equally spaced for both conventional and conformal approach. The channel length is 20000 mm and has water as a coolant.

Cooling channels design for spray bottle funnel

For conventional cooling channels, the channel diameter is 10 mm and these channels are placed at specified distance from the part centre. The channels are placed parallel to each other at a distance of 60 mm. As a general rule, followed by the injection moulding design engineers, the channels should be placed at a distance of 2–2.5 times the channel diameter. The more near the channels are placed, faster cooling can be achieved, and this contributes to less cycle time. In this design, there are four channels used at a constant distance of 30 mm from the maximum diameter of the cavity wall. The maximum diameter of the part is 65.97 mm.

For conformal channels, the channel diameter is 10 mm and these channels are conforming to shape of the funnel. The channels are placed at equal distance to each other. The channels are made in the form of the semicircle near the part and straight channels away from the part. The channels are placed at such a distance that they carry the maximum heat away so as to enhance the cooling. There are four conformal channels placed at a distance of 60 mm with each other. Depending on the shape of the part, the channel placement of the bottom of the funnel is 30 mm. This distance is same throughout the funnel, and the distance of the channel from the top part cavity is 30 mm. The distance between mould and the channel is 60 mm approximately in both configurations. It is same for both the channels as it is necessary while clamping the mould in the injection moulding machine set-up.

Table 2 provides the details of mould and cooling channel costing, and Table 3 provides the details of mould cost calculations for the part using conventional and conformal cooling channels.

Table 4 provides a comparative economic analysis of spray bottle funnel manufactured with plastic injection moulding using conventional and conformal cooling channels. The data represented in Tables 2, 3 and 4 are obtained from a plastic mould manufacturing company, Yashasvi Plasto Tech, Vasai, Maharashtra. Based on the mould manufacturing cost, the total material cost, design cost, cooling channel cost and total cost are calculated. Various cost components are calculated based on the component geometry, component weight, raw material and runner weight specified by the manufacturer.

The table indicates that mould cost per component is higher for conformal approach due to special machining required for making conformal cooling channels; however, this gets compensated due to lower processing cost per component on account of reduction in the cooling time. The conformal cooling approach may not be economic for small production batches; however, mould cost per component gets significantly reduced for larger production volumes. Therefore, it is necessary to carry out breakeven analysis for the manufactures to justify selection of conformal cooling approach for a particular product.

Figure 4 provides proportions of various cost components for manufacturing spray bottle funnel with conventional and conformally cooled injection moulds.

Proportions of cost components for conformal versus conventional approach

Figure 5 graphically represents the unit cost versus production volume for conventional and conformal cooling approach. It is evident that the unit cost in conformal cooling approach is higher compared to conventional approach for low production volumes; however, the margin goes on decreasing with an increase in the production volume. Therefore, it is necessary to perform breakeven analysis to identify the minimum production volume that economically justifies the use of conformal cooling channels.

Production cost versus production volume

Breakeven Analysis for Spray Bottle Funnel

Breakeven analysis is carried out to identify the minimum production volume that justifies increased mould cost with conformal cooling channels by reducing processing cost achieved through economies of scale. Figure 6 provides the results of breakeven analysis indicating the breakeven point of 70,824 production pieces.

Breakeven analysis for spray bottle funnel

Therefore, it can be concluded that for the part selected in present analysis, conformally cooled injection moulds can be economically opted for production volume greater than the breakeven quantity.

Conclusion

The research findings presented in this paper provide a framework and methodology for cost estimation, economic analysis and breakeven analysis of plastic injection moulding using conformal cooling channels compared to conventional approach. Conformal cooling is proven to improve the production quality compared to conventional approach for intricate plastic parts. However, the plastic component manufacturers need to carefully investigate its economic implications as even the slightest change in per-piece production cost has huge financial implications due to large volume of plastic production.

The results obtained in the present paper indicate that conformal cooling leads to an increase in the mould cost due to intricate cooling channels which may not be justified for small production batches. However, it also reduces per-piece production cost by improving production rate with reduction in the cooling time. Therefore, breakeven analysis becomes essential to compute minimum economic production volume that justifies the use of conformally cooled channels.

For the case study of spray bottle funnel selected in the current paper, total cost per component is obtained as Rs. 15.91 with conventional cooling channels and Rs. 14.01 for conformal cooling channels. Breakeven analysis indicated that the conformal cooling approach may not be economically viable for small production batches but is justified for more than 70,824 pieces.

The methodology and framework implemented in this paper can be adopted in the industry with appropriate modifications based on the component under consideration. These economic considerations are essential for plastic component manufacturers while making decisions regarding selection of conformal cooling approach as against the conventional approach.

In this paper, comparison between conventional and conformal cooling was carried out for spray bottle funnel using a conformal cooling channel design. Economic analysis was performed by considering EDM as the manufacturing process for conformal cooling channel. Considering these limitations, the research can be furthered by considering different components, optimizing cooling channel designs and exploring the economic aspects of other manufacturing processes.

References

E. Vojnová, The benefits of a conforming cooling systems the molds in injection moulding process. Procedia Eng 149, 535–543 (2016)

S.Z.A. Rahim, S. Sharif, A.M. Zain, S.M. Nasir, R. Mohd Saad, Improving the quality and productivity of molded parts with a new design of conformal cooling channels for the injection molding process. Adv Polym Technol (2016). https://doi.org/10.1002/adv.21524

C.C. Kuo, Z.F. Jiang, Numerical and experimental investigations of a conformally cooled maraging steel injection molding tool fabricated by direct metal printing. Int J Adv Manuf Technol 104(9), 4169–4181 (2019)

Saifullah, A. B. M., & Masood, S. H. (2007, December). Cycle time reduction in injection moulding with conformal cooling channels. In Proceedings of the International Conference on Mechanical Engineering (pp. 29–31).

M. Franchetti, C. Kress, An economic analysis comparing the cost feasibility of replacing injection molding processes with emerging additive manufacturing techniques. Int J Adv Manuf Technol 88(9–12), 2573–2579 (2017)

Turc, C. G., Cărăuşu, C., & Belgiu, G. (2017, August). Cost analysis in injection moulded plastic parts designing. In IOP Conference Series: Materials Science and Engineering (Vol. 227, No. 1, p. 012132). IOP Publishing

Minguella-Canela, J., Morales Planas, S., los Santos-López, D., & Antonia, M. (2020). SLM Manufacturing Redesign of Cooling Inserts for High Production Steel Moulds and Benchmarking with Other Industrial Additive Manufacturing Strategies. Materials, 13(21), 4843

R. Huang, M.E. Riddle, D. Graziano, S. Das, S. Nimbalkar, J. Cresko, E. Masanet, Environmental and economic implications of distributed additive manufacturing: the case of injection mold tooling. J. Ind. Ecol. 21(S1), S130–S143 (2017)

Charalambis, A., Kerbache, L., Tosello, G., Pedersen, D. B., & Mischkot, M. (2017, October). Economic analysis of additive manufacturing integration in injection molding process chain. In International Conference on Industrial Engineering and Systems Management (IESM 2017), October

J. Vasco, F.M. Barreiros, A. Nabais, N. Reis, Additive manufacturing applied to injection moulding: technical and economic impact. Rap Prototyp J (2019). https://doi.org/10.1108/RPJ-07-2018-0179

Kampker, A., Ayvaz, P., & Lukas, G. (2020). Direct polymer additive tooling-economic analysis of additive manufacturing technologies for fabrication of polymer tools for injection molding. In Key Engineering Materials (Vol. 843, pp. 9–18). Trans Tech Publications Ltd

G. Tosello, A. Charalambis, L. Kerbache, M. Mischkot, D.B. Pedersen, M. Calaon, H.N. Hansen, Value chain and production cost optimization by integrating additive manufacturing in injection molding process chain. Int J Adv Manuf Technol 100(1–4), 783–795 (2019)

Patil, S. N., Mulay, A. V., & Ahuja, B. B. (2018). Development of experimental setup of metal rapid prototyping machine using selective laser sintering technique. J Inst Eng (India): Series C, 99(2), 159–167.

Funding

No funding was received for conducting this study.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Singh, D., Joshi, K. & Patil, B. Comparative Economic Analysis of Injection-Moulded Component with Conventional and Conformal Cooling Channels. J. Inst. Eng. India Ser. C 103, 307–317 (2022). https://doi.org/10.1007/s40032-021-00778-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40032-021-00778-5