Abstract

Post 2005 in India, a number of public policy initiatives were introduced to strengthen existing programs for welfare of the ever-increasing population aged 60 years and older. Using a National Transfer Accounts framework, this paper attempts to assess the implications of policy changes by evaluating changes in lifecycle deficit and changes in public and familial support of the elderly especially in meeting their lifecycle deficit between 2004 and 05 and 2011–12. It found that labour income of the elderly increased marginally during 2004–2012, but the level of consumption of the elderly marginally slipped down. Lifecycle deficit (LCD) of the elderly population aged 60 years and older declined due to the intertwining effect of increased labour income and declining consumption. Familial support to the elderly did not improve between 2004 and 2012, instead their net contribution to intra-household transfers is greater than their benefits. Asset based reallocation remains the main source of financing the LCD of the elderly. Benefits of the elderly in meeting their lifecycle deficit from policy changes is nominal.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

In many developing countries, public welfare measures are largely concentrated on human resource development and maternal and child health care, while social security of the elderly has not been given adequate priority. This is also partly due to the fact that, traditionally in most Asian countries, family is the source of support and care of elderly. Evidence of elderly co-residence with their children and grandchildren in developing countries, among others, are found in the works of Bongaarts and Zimmer (2002), Zimmer (2005); Knodel and Debavalya (1997); Knodel et. al. (2000); Gupta and Pillai (2002), Croll (2006) and Silverstein et al. (2006). Further, this also used to be the case for India as evident from Rajan and Kumar (2003) that in 1992–93, 33.8 percent of elderly lived with children and grandchildren. Co- residing with the elderly and the ‘filial piety’ rendered towards them has its roots in the Hindu Dharma of revering the elders for their wisdom (Bisht & Sinha, 1981) and honouring Shasti Poorthi (meaning a person reaching 60 years in Sanskrit, Borooah, 2016).However, in today's changing scenario in India, the joint family system is also undergoing transition into a nuclear family system and the familial support for the elderly is dwindling (Jadhav et al., 2013).This is also evidenced from the findings of other studies that show a marked increase in the proportion of older persons living alone, shown earlier at 4 percent (Chaudhuri & Roy, 2009) and rose to 12.8 percent in 2010 (Arokiasamy et al., 2011). At the same time, the elderly population is on the rise. India’s social security, like most other developing countries, is not well founded and is ill-prepared to respond to the ever-increasing elderly population and changing dynamics of filial support. Rajasekhar et al. (2017) have highlighted the fact that schemes, such as the National Pension Scheme (NPS) Lite and Atal Pension Yojana (APY) are inadequate to meet the social security needs of low income workers. Kaushal (2014) in their investigation of the causal relationship between IGNOAPS (Indira Gandhi National Old Age Pension Scheme) and households’ welfare have found a marginal positive significant effect on the welfare of recipients’ households. Ladusingh and Thangjam (2018) opined that elderly in India continue to work even after the post-retirement age of 60 years as the benefits from public sponsored national old age pension and social support schemes are inadequate. Ladusingh and Maharana (2018), making a comparative assessment of the adequacy of social security of select Asian countries, have concluded that most of the lifecycle deficits of the elderly are financed by asset-based reallocation. Nonetheless, in recent times, the country has taken some policy initiatives to broaden the social security net. This paper is an extension of the previous analysis (Ladusingh, 2013) to newly available micro data of 2011–12. It attempts to provide an assessment of the implications of post-2005 policy reforms on intergenerational public and familial supports of the elderly in India. It does this by assessing the changes between 2004 and 05 and 2011–12 in lifecycle deficit, and public and private intergenerational transfers for financing the lifecycle deficit. The findings shall be key policy inputs for strengthening social security of the elderly.

Post 2005 policy reforms

Post 2005, a number of policy initiatives that address the welfare of the elderly have been implemented. Policy reforms post 2005 and up to 2012 are highlighted in this section in view of the period of assessment considered in this study. Keeping in mind that about 90 percent of the labour force in India is in an unorganised sector and to extend social security to workers in this sector, the Government of India (GoI) passed the Unorganised Workers Social Security Act (UWSSA) in 2008. This is tied with three schemes, namely, Rashtriya Swasthya Bima Yojana (RSBY), Aam Admi Bima Yojana (AABY) and the National Pension Scheme- Swavalamban (NPS-S) which are health insurance, life insurance and pension schemes respectively, largely for the population below the poverty line and workers in the unorganised sector. Under RSBY, health insurance coverage is provided for a maximum of five members of the household from below the poverty line (BPL) and cover hospitalisation expenses up to Rs. 30,000. Aam Admi Bima Yojana (AABY) provides death and disability cover to persons between the ages of 18 to 59 years, insurance cover for a sum of Rs. 30,000 on natural death, Rs. 75,000 on death due to accident, Rs. 37,500 for partial permanent disability (loss of one eye or one limb) due to accident and Rs. 75,000 for total permanent disability (loss of two eyes or two limbs or loss of one eye and one limb) due to accident. The Scheme also provides an add-on-benefit, wherein Scholarship of Rs 100 per month per child is paid on a half-yearly basis to a maximum of two children per member, studying in 9th to 12th standard. The premium for availing benefits under AABY scheme is Rs. 200 per month. The entitlement under the National Pension Scheme-Swavalamban (NPS-S), now renamed as Atal Pension Yojana (APY), for persons below 40 years under the scheme on reaching 60 years is Rs. 5000 per month and any persons working in the unorganised sector can join the scheme by contribution of Rs. 1000 to Rs. 12,000 per annum. In the APY scheme, the government contributed Rs. 1000 per annum to all who joined APY from 2011 to 12. For employees in the organised sector, Government introduced the New Pension Scheme (NPS) from 2004, which is a defined contribution scheme wherein employees joining service afterwards have to contribute a minimum of 10 percent of their salary and there is a matching 10 percent contribution by the government. Other flagship programmes are the National Rural Health Mission (NRHM) to provide accessible, affordable, and quality health services in rural areas with a special emphasis on elderly care, and the Mahatma Gandhi National Rural Employment Guarantee Act (MANREGA) enhancing the livelihood and security of people in rural areas by guaranteeing one hundred days of wage employment— both the programmes were launched in 2005. The minimum wages under MANREGA was initially Rs. 100 per day, which has been enhanced now and varies by state from Rs. 163 in Bihar to Rs. 500 in Kerala. The Janani Suraksha Yojana (JSY) scheme under NRHM provides a cash compensation of Rs. 1400 to all women in low performing states and Rs. 700 to ST/SC and BPL women in high performing states for institutional delivery in government /private accredited health facilities. Government is also continuing the National Old Age Pension (NOAP), which was launched in 1995, now renamed as the Indira Gandhi National Old Age Pension (IGNOAP) in 2007, to provide comprehensive old age poverty alleviation as a major component of the National Social Assistance Programme (NSAP). Destitute persons aged 65 years and above are eligible for NOAP and entitlement in the beginning, when it was initiated, was Rs. 75 per month but has now been enhanced to Rs. 200 (Ladusingh, 2013). The Indira Gandhi National Widow Pension Scheme (IGNWPS) was launched in 2007 and entitlement is Rs. 300 per month for widows aged 40 years and above that are from BPL households. Likewise, the Indira Gandhi National Disability Pension Scheme (IGNDPS), introduced in 2009, provides assistance of Rs. 500 per month by federal and state governments to persons from BPL households aged 18 years and above with multiple or severe disability. The National Programme for Health Care of Elderly (NPHCE) was launched in 2010 to provide preventive, curative, and rehabilitative services to the elderly.

Need for the study

In the post 2005 reform period, pertinent questions that equally concern researchers and policy makers in India are: Whether the social security of elderly has improved post the 2005 public reforms? If not, how are elderly meeting their lifecycle deficits between 2004 and 05 and 2011–12?

To address the previously mentioned questions, it is important to assess the changes in labour income, consumption of public and private goods and services, and means of supporting lifecycle deficits by age in general, and by the elderly, in particular. In the Indian context, till now, no such study is available and hence, able to provide answers to the previously mentioned questions. One of the reasons for the dearth of such studies is the lack of unit level data pertaining to household income and expenditure at regular time intervals or on a yearly basis. Further, it required some time period for policies to trickle down to targeted beneficiaries. Taking the opportunity of recently available data, after a gap of seven years, this paper makes an assessment of changes in economic flows for individuals across a range of ages between 2004 and 05 and 2011–12 and considers the means of financing of lifecycle deficits by individuals of various ages. The results of the study shall not only be able to provide answers to the previously mentioned questions but shall also be beneficial in monitoring the efficacy of the post-2005 policy reforms.

Sources of data

Unit level data on labour income and consumption for health, education and other goods and services from two rounds of the India Human Development Survey 2004–05 and 2011–12 (Desai et al., 2008, 2012) are used in the analysis. Both rounds of the India Human Development Survey (IHDS) were nationally representative and covered all states and union territories in India (except Andaman Nicobar and Lakshadweep). For this study, the cross-sectional unit level data for the two rounds are being used. Two sets of questionnaires for household and individuals were completed by face-to-face interview. Labour income of individual household members and also expenditure of households for health, education and others were collected from every representative sampled household in IHDS, whereas in the NSSO (National Sample Survey Organisation) employment and unemployment survey, consumption expenditure survey data were collected not from the same sampled households. Thus, IHDS data is more adaptable for the present study. Age distributions by single years at two points of time from the Office of the Registrar General of India (2006 and 2011) were also utilised. National Accounts Statistics for the financial year 2004–05 and 2011–12 were extracted from the reports of Central Statistical Organization (2008, 2015), Ministry of Statistics and Programme Implementation, Government of India.

Methodology

Economic lifecycle of individuals can be studied more comprehensively in terms of age patterns of labour income and consumption. Lifecycle deficit (LCD) across ages is the excess of consumption over labour income. It is high for children and the elderly; while for individuals in the prime working age, consumption is less than their income. Consumption can be publicly funded, self-financed, financed by other members of the household, or borrowed. On the other hand, the LCD of individuals can be financed through familial support by intra- and inter-household transfers, and asset-based reallocation–that is, income from savings and assets and public transfers, either in cash or in kind, through various government programs and targeted interventions including social security. From the perspective of an individual in the National Transfer Accounts (NTA) framework (United Nations, 2013), the balancing of the excess of consumption (C) over labour income (\({Y}_{l}\)) over the lifecycle by intergenerational public and private transfers and public and private asset-based reallocation is represented as:

where \({\tau }_{g}^{+}\) and \({\tau }_{f}^{+}\) are intergenerational public and private transfer inflows and similarly \({\tau }_{g}^{-}\) and \({\tau }_{f}^{-}\) are corresponding transfer outflows. These transfers are from the perspective of individuals. YA is the asset income from capital, property and credit, and S is the saving treated as residuals. The NTA method captures the familial, the public transfers and asset-based reallocations of the population of a country integrating age into the National Accounts. It therefore has an edge over other methods of intergenerational familial and public economic support system of a specified economy.

Labour income is estimated as the sum of compensation of employees, labour’s share of operating surplus or entrepreneurial income, and net compensation of employees from the rest of the world (ROW). Compensation of employees is equal to wages and salaries and an employer’s social contributions. In the absence of information on the labour share of mixed income, two-third of total mixed income is assumed to be the entrepreneurial income. The age profile of employee compensation is estimated using survey data. The age profile of labour income of the self-employed and family workers is also estimated from the survey with unreported income being imputed by mean reported income controlling for age, education, and industry.

Age allocation of private expenditure on food is based on the assumption that individual food consumption of members in a household is proportional to an equivalence scale that is taken as 0.4 for children below 4 years of age, then increases linearly from 0.4 to 1 for individuals between 4 and 20 years and to be constant at 1 thereafter for individuals 20 years and above. Age profile of food consumption is then estimated applying this equivalence scale to the household expenditure available from consumer expenditure surveys.

For the age allocation on non-food expenditure, excluding housing and durables, we have adopted the same equivalence scale as in the case of food expenditure. When it comes to methodologies for individual’s age allocation of public expenditure on education, health, and others, we have used corresponding age patterns from data sources that have information pertaining to age.

Definitions

The definition of components of public and private consumptions and that of labour income used in the NTA framework used in this study are provided in Table 1 as follows:

Macro controls

The macro aggregate control figures extracted from the National Accounts of India for 2004–05 and 2011–12 and used in the study are shown in Table 2.

Results

Lifecycle accounts

The lifecycle accounts and annual aggregate flows for the accounting years 2004–05 and 2011–12, by sectors, for India are shown in Table 3.

Noticeable features of the lifecycle accounts include increases in the consumption levels of persons under 20, 20–29 and above 65 years from 32.4 to 35.6, from 19.1 to 20.7 and from 6.5 to 7.1 percent of total consumption respectively between 2004 and 05 and 2011–12. The change is mainly accounted for by the increase in the share of public consumption by persons under 20 years from 35.6 to 50 percent during the aforesaid period of 7 years. Further, the share of private consumption by persons under 20 and above 65 years has increased from 29 to 35.7, and 6.7 to 7.3 percent respectively. The contribution to labour income by these two age groups also increased from 3.7 to 9.5, and from 2.2 to 4.9 percent respectively between 2004 and 05 and 2011–12. The increase in the share of labour income for persons aged 50–64 years was from 19.2 to 22.4 percent, but for persons in the prime working age group of 30–49 years, there was a decline of 12.2 points from 54.3 percent in the above-mentioned period.

Change in labour income

Labour income and consumption of public and private (household) funded resources, goods and services together account for the lifecycle deficit (LCD). Figure 1 shows the per capita age profiles of labour income for 2004–05 and 2011–12. For comparability, the labour income is standardised by the corresponding period, which means per capita labour income of persons aged 30–49 years. It may be noted that the age pattern of labour income for 2004–05 is characterised by entries into the labour market at very young ages as child labourers, then accelerating steeply with age up to 35 years, then remaining marginally above the mean per capita income of those aged 30–49 years in the age range 35–55 years, the prime working years, and thereafter withdrawals from the labour market due to retirement. At the retirement age of 58–60 years, labour income fell by 50 percent from 0.8 to 0.4 of the mean per capita income of 30–49 years. There is limited opportunity for the elderly in the labour market as evident from the labour income of below 20 percent of mean per capita income of persons 30–49 years after 60 years of age. The age pattern of labour income for 2011–12 is distinctively different from that of 2004–05. The per capita income of 2011–12, in most parts of the lifecycle, is higher than that of 2004–05. When the labour income peaks at the age of 58 years, it is 1.3 times the mean per capita income of 30–49 years. There is also a steep fall in labour income in the post-retirement age of 60 years as in 2004–05, but the emergence of opportunity for the elderly to be engaged in the labour market with higher returns is evident in 2011–12. The finding is in agreement with that of Ladusingh and Thangjam (2018), who concluded that the elderly continue to work in post-retirement as the benefit from public sponsored schemes is inadequate. The post 2005 public reforms in India clearly provide employment opportunities to individuals and bring considerable enhancement in levels of income. This due to re-enforcement in the implementation of MANREGA and enhancement from Rs. 100 to Rs. 500 in many states in India. Further, the growth of hospitality industries and expansion of retail markets both online and through part-time jobs have led to enhanced earnings of people of all ages in general and youth, in particular. Employment opportunities are mainly in the informal sector as the retirement age of persons in the public sector has not altered during the period 2004–05 to 2011–12.

Age patterns of labour income for 2004–05 and 2011–12

Changing pattern of consumption

The other component of the lifecycle deficit (LCD) is the public and private consumption in monetary terms. It includes consumption for health, education, and others from public and household resources. Age patterns of per capita consumption for 2004–05 and 2011–12, standardised by mean per capita income of persons aged 30–49 years of the corresponding accounting year, are shown in Fig. 2. Two remarkable changes in the age pattern of consumption of 2011–12 as compared with that of 2004–05 are evident. The first change is the decline in the per capita consumption of adults from age 35 till age 65, from 74 to 70 percent, then rising with advancing age to 74 percent of the mean per capita income of persons aged 30–49 years. The consumption level of adults aged 35 years and above in 2004–05 was between 71 and 74 percent of the mean per capita income of those aged 30–49 years in the corresponding accounting year. The declining pattern of per capita consumption in 2011–12 reflects the fact that post 2005, public reforms were not adequate to smooth out consumption of by the ever-increasing elderly population. This is despite the fact that per capita income levels of the elderly have increased over the years. The plausible reasons being that the elderly play significant role in the welfare of household members particularly in supporting the education of their grandchildren.

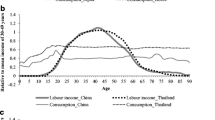

Age patterns of consumption for 2004–05 and 2011–12

The other noticeable change in the age pattern of per capita consumption in 2011–12 is the huge elevation in the consumption level which is 57 percent of the mean per capita income of 30–49 years for children under 10 years, then accelerates with increasing age to attain a peak of 84 percent for persons aged 23–25 years, the stage of higher education, before dropping down to 71 percent at the age of 35 years. This clearly indicates the fact that post 2005 public reforms in India are favouring the younger population, while the elderly have not gained substantially from recent policy initiatives as far as the consumption is concerned. It is only partly due to the fact that the 7 years period from 2004 to 05 to 2011–12 is too short for the benefits of post-2005 policy reforms to trickle down to the beneficiaries. A closer assessment of disaggregated consumption for public and private education shown in Fig. 3a, b supports the aforesaid inference to a considerable extent.

a Change in public education b Change in private education

Per capita public and private consumption for healthcare in 2011–12 fell lower than the level in 2004–05 though there is a spike in public health consumption in the age range 25 to 35 years mainly because of the benefits of maternal and childcare from the NRHM. Private consumption for goods and services other than for education and health in 2011–12 declined among adults but rose for those aged less than 20 years in comparison to that of 2004–05. But for the public consumption for goods and services other than for education and health there have been increases from 5.84 percent of the mean per capita income of 30–49 years in 2004–05 to 6.35 percent in 2011–12.

Changing pattern of lifecycle deficit

An excess of consumption, both public and private counted together, over labour income is the lifecycle deficit (LCD). Age patterns of per capita LCD for 2004–05 and 2011–12 are shown in Fig. 4. Life cycle deficits are standardised by the mean per capita income of 30–49 years of corresponding accounting years. The age patterns of LCD for 2004–05 and 2011–12 are similar in two aspects— elderly and young populations consume more than their labour income, while the labour income of adults in the working ages surpasses the consumption. However, there are considerable differentials in the level of LCD across ages.

Age patterns of lifecycle deficit for 2004–05 and 2011–12

As children’s consumption increases over time, particularly for public and private financed education, the LCD of children below 10 years shoots up from 40 to above 51 percent of the mean per capita income of persons aged 30–49 in 2011–12, in comparison to an increase from 20 to 40 percent in 2004–05. On the other hand, in post-retirement ages, the LCD of persons aged 60–80 years reduced substantially in 2011–12, but for persons older than 80 years, LCD is at par with that of 2004–05. This can be attributed to the intertwining of increases in per capita income in post-retirement ages and low benefits from the post-2005 public reforms for the elderly.

Financing the lifecycle deficit

Intra-household monetary transfers among members of households is a significant means of support for younger members of households. Figure 4a shows that the net intra-household transfer monetary benefit for persons aged less than 20 years increased considerably from 7 to 11 percent of the mean per capita income of persons aged 30–49 years during 2004–2012. This was also the case for persons aged 20–29 years, recording a marginal increase during the same period. Further, it can also be noticed that persons in the working ages, and even the elderly, are the main contributors of intra-household monetary supports to younger household members. A distinguishing feature of intra-household transfer is that net transfers of persons aged 50–64 and those older than 65 years are negative, meaning that they contribute more than they receive via intra-household transfer. Additionally, the contributions of the elderly have increased substantially during 2004–2012. This result is contrary to the hypothesis that children provide old age support to elderly. Fig. 5b, on the other hand, shows the age pattern of asset-based reallocation, that is, liquidations of assets, shares, and bonds to finance LCD. It is evident that for persons older than 30 years, one of the main means of financing lifecycle deficit (LCD) is asset-based reallocation and it increases with advancing ages. The reliance on asset-based reallocation to meet LCD by elderly 65 years and older has marginally increased in 2011–12, as compared to that in 2004–05. This suggests that policy reforms post 2005 dedicated to enhancing the welfare of the elderly are yet to make an impact on the means of meeting their LCD, at least during the period 2004–05 to 2011–12. It is expected that in the long run the benefit of the various schemes embedded in the policy reforms will trickle down to meet the larger proportion of the LCD of elderly population.

a Net intra-household transfer b Private asset-based allocation by age age in 2004–05 and 2011–12 in 2004–05 and 2011–12

Labour income, net familial (private) and public transfers, private and public asset-based reallocations are the major means of financing LCD in the NTA framework. Figure 6 portrays the changing shares of the aforesaid means of meeting LCD for the elderly older than 60 years between 2004 and 05 and 2011–12. There is a marginal increase in meeting the LCD of 60 years and older persons by labour income from 35.1 to 37.7 percent during 2004–2012 and it is the induce effect of an increase in income in post-retirement age. Another noticeable feature of the post-2005 public policy changes is the emerging upward trend from to 1.6 to 2.1 percent of LCD of the elderly being met by net public transfers during the aforesaid period. However, asset-based reallocations remain the main source of financing the LCD of the elderly and its share of making up the LCD of the elderly has increased from 63.9 to 65.3 percent. This clearly signals that the benefits of post-2005 policy reforms, as far as meeting the LCD of the elderly, is marginal and that these benefits have not been able to make an impact on the welfare of the elderly, as far as supporting their LCD is concerned. Neither has the familial support to the elderly been improved during 2004–2012; rather, the elderly net contribution to intra-household transfer is more than what they benefit and has increased from 8.9 to 12.2 percent of LCD during 2004–2012.

Sources of support of elderly older than 60 years in 2004–05 and 2011–12

Conclusion

In recent times, particularly after 2005, a number of public policy initiatives have either been introduced or have been framed to strengthen the existing programs in India for the welfare of the ever-increasing population aged 60 years and older. Using a NTA framework, this paper makes an attempt to assess the implications of policy changes in labour income, consumption, lifecycle deficit and changes, especially in meeting the lifecycle deficit of individuals by age in general, and the elderly aged 60 years and above in particular. It has been found that policy initiatives have been instrumental in marginally enhancing the labour income of the elderly from 2004 to 05 to 2011–12. However, the level of consumption of the elderly has slipped down, while that of children has increased significantly during this period. The consumption level of elderly persons should have increased with the increase in labour income of the elderly to sustain their well-being. Declining consumption levels, despite increases in labour income, indicates that post-2005 policy initiatives are not enhancing the welfare of the elderly population.

The lifecycle deficit (LCD) of the elderly population aged 60 years and older declined due to the intertwining effect of increases in labour income and declining consumption. The means of supporting the LCD are own labour income, public and familial transfers, and asset-based reallocations. It was found that the contribution of labour income in meeting the LCD of the elderly has improved, while public transfers for other goods and services have registered marginal increases as a consequence of policy initiatives. However, the intra-household financial support of the elderly has not registered any improvement and, on the contrary, during 2004–05 to 2011–12, the contribution of the elderly to supporting other family members, particularly grandchildren, registered a substantial increase. This is also in agreement with the findings of Ladusingh and Narayana (2011). The dependence on private asset-based reallocations, that is, income from assets, bonds, savings, and the liquidation of property has remained the main source of financing the LCD of the elderly and dependence on asset-based reallocations increased marginally. This is also the case for many Asian countries as found by Ladusingh and Maharana (2018).

Public policies and programmes in India for the elderly fall far short of what can be termed as social security policy as most of the post 2005 policies are more in the form of means-tested assistance schemes. It is not only that the coverage of such schemes are low, but benefit levels are also meagre. This is what is reflected from the present study. One feasible means to reduce the LCD of the elderly, as has been evidenced from the paper, is to enhance the age of retirement and bring about legislation to make the labour market elderly-friendly. This may include, providing tax incentives to firms employing a minimum number of elderly workers. This can be complemented by making provisions of publicly sponsored vocational centres for skill enhancement of elderly people to make them employable. Expanding the scope of MANREGA by increasing the maximum days’ work and raising the daily wage rate would also serve as a medium for reducing the LCD. The findings also point to the fact that benefits to the elderly from transfers of public sponsored programs and schemes has marginally increased after the post 2005 reforms, but is heavily tilted in favour of children. With declining fertility and improvements to infant and child mortality, public policies should work out an optimum balance of targeted public funding for children and the elderly population. There is scope to widen coverage and enhance the tax revenue rate for developing and implementation of a sustainable social security policy in the true sense. The present rate is much lower, when compared to average tax rates of OECD countries, and India is yet to emerge from the window of demographic dividend. It is also a reality that public programs and policies alone cannot provide adequate support to the ever-increasing elderly population, but can tighten implementation of existing provisions, such as, ‘The Maintenance and Welfare of Parents and Senior Citizens Act, 2007 (Government of India, 2007)’.

References

Arokiasamy, P., Bloom, D., Lee, J., Feeney, K., and Ozolins, M. (2011). Longitudinal aging study in India: vision, design, implementation, and some early results. PGDA Working paper No. 82, Harvard Initiative for Global Health. http”// www.hsph.harvard.edu/pgda/working accessed on January 31, 2016.

Bisht, S., & Sinha, D. (1981). Socialization, family and psychology differentiation. In D. Sinha (Ed.) Socialization of the Indian child (pp. 41–54). New Delhi: Concept.

Bongaarts, J., & Zimmer, Z. (2002). Living arrangements of older adults in the developing world: An analysis of demographic and health survey household surveys. The Journals of Gerontology Series b: Psychological Sciences and Social Sciences, 57(3), S145–S157.

Borooah, V. K. (2016). Gender disparities in health outcomes of elderly persons in India. Journal of South Asian Development, 11(3), 328–359.

Central Statistical Organization. (2008). National Accounts Statistics 2008. New Delhi: Ministry of Statistics and Programme Implementation, Government of India.

Central Statistical Organization. (2015). National Accounts Statistics 2015. New Delhi: Ministry of Statistics and Programme Implementation, Government of India.

Chaudhuri, A., & Roy, K. (2009). Gender differences in living arrangements among older persons in India. Journal of Asian and African Studies, 44(3), 259–277.

Croll, E. J. (2006). The intergenerational contract in the changing Asian family. Oxford Development Studies, 34(4), 473–491.

Desai, S and Vanneman R (2012). India Human Development Survey-II (2011-12). ICPSR 36151-v2. Ann Arbor, MI: Inter-university Consortium for Political and Social Research [distributor], 2015-07-31. http: //doi.org/10.3886/ICPSR36151.v2.

Desai, S., Dubey, A., Shariff, A., & Venneman, R. (2008). India Human Development Survey 2005. New Delhi: National Council of Applied Economic Research (New Delhi) and Ann Arbor: Inter-university Consortium for Political and Social Research. Available on: http://www.icpsr.umich.edu/ICPSR/access/index.html.

Government of India. (2007). The Maintenance and Welfare of Parents and Senior Citizens Act, 2007′,Ministry of Social Justice & Empowerment Justice & Empowerment. http://socialjustice.nic.in/oldageact.php. Accessed 25 April 2017.

Gupta, R., & Pillai, V. K. (2002). Elder care giving in South Asian families: Implications for social service. Journal of Comparative Family Studies, 33, 565–576.

Jadhav, A., Sathyanarayana, K. M., Kuma, S., & James, K. S. (2013). Living Arrangements of the Elderly in India: Who lives alone and what are the patterns of familial support. Busan, Korea: IUSSP.

Kaushal, N. (2014). How public pension affects elderly labor supply and well-being: Evidence from India. World Development, 56, 214–225.

Knodel, J., & Debavalya, N. (1997). Living arrangements and support among the elderly in South-East Asia: An introduction. Asia Pacific Population Journal, 12, 5–16.

Knodel, J., Friedman, J., Si Anh, T., & Cuong, B. T. (2000). Intergenerational exchanges in Vietnam: Family size, sex composition, and the location of children. Population Studies, 54(1), 89–104.

Ladusingh, L. (2013). Lifecycle deficit, intergenerational public and familial support system in India. Asian Population Studies, 9(1), 78–100.

Ladusingh, L., & Maharana, B. (2018). How sustainable is the familial support of elderly in Asia? Journal of Population Ageing, 11(4), 349–366.

Ladusingh, L., & Thangjam, M. (2018). Gender differential in occupation and income among the elderly in India. Ageing International, 43(2), 174–189.

Ladusingh, L., & Narayana, M. R. (2011). The role of familial transfers in supporting the lifecycle deficit in India. In R. Lee & A. Mason (Eds.), Population aging and the generational economy: A global perspective (pp. 459–474). Edward Elgar.

Rajan, S. I., & Kumar, S. (2003). Living arrangements among Indian elderly: New evidence from national family health survey. Economic and Political Weekly, 38(1), 75–80.

Rajasekhar, D., Kesavan, S., & Manjula, R. (2017). Are our contributory pension schemes failing the Poor? Economic & Political Weekly, 52(27), 77–85.

Silverstein, M., Cong, Z., & Li, S. (2006). Intergenerational transfers and living arrangements of older people in rural China: Consequences for psychological well-being. The Journals of Gerontology Series b: Psychological Sciences and Social Sciences, 61(5), S256–S266.

United Nations. (2013). National transfer accounts manual: Measuring and Analysing the Generational Economy. Population Division, Department of Economics and Social Affairs, New York.

Zimmer, Z. (2005). Health and living arrangement transitions among China’s oldest-old. Research on Aging, 27(5), 526–555.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Ladusingh, L., Thangjam, M. Policy reforms and changing intergenerational support of elderly in India. J Pop Research 38, 401–416 (2021). https://doi.org/10.1007/s12546-021-09275-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12546-021-09275-z