Abstract

This study examines the long memory properties in the volatility of the foreign exchange markets of Egypt, Ghana, Kenya, Nigeria and South Africa. Applying the FIEGARCH model to daily data from June 2, 1997, to December 31, 2021, we find long memory in the second moment of return innovations across all five countries' foreign exchange markets and significant first-order positive autocorrelation. To isolate spurious long memory, we perform a structural break test and find that structural breaks in all five foreign exchange markets do not affect long memory. The findings may have implications for risk management. Historical volatility-based investment methods can generate risk-adjusted returns innovations. Long memory may indicate unexploited profit for risk-seeking speculators and international investors in these countries' financial assets. Also, official intervention should be random and rule-changing to reduce currency market predictability.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Africa's foreign currency market has modernised rapidly due to its increased participation in the international investment market. International investors seeking exposure to Africa's fast-growing economies have increased the demand for ease of currency convertibility. To some degree, African countries' foreign exchange markets are affected by international investors' investments in domestic bond and stock markets or real sectors. International investors may reverse portfolio investments in Africa if their risk appetite decreases and advanced economies improve or raise sovereign interest rates, causing market volatility.

The rapid economic transition across Africa has driven the foreign exchange market's growth. According to the International Monetary Fund (2023a), Sub-Saharan Africa had a real GDP of 4.8% in 2021, while advanced economies had 5.1%. The real GDP figure for sub-Saharan Africa is forecasted to change to 4.2% in 2024, whereas that of the advanced economies is expected to change to 1.3% for the same period. As investors favour frontier market investments, African foreign exchange markets are expected to grow in the coming years.

Long memory in financial returns allows some investors to predict return movement and volatility and make profitable decisions. Long memory is present when there is statistical dependence in financial data. A hyperbolic decay rate characterises the autocorrelation functions of volatility measures. If long memory exists in these markets, the markets would be classified as inefficient.

Statistical dependence has been documented in other financial data. Nagayasu (2003) found long memory in the Japanese equity market, while Sadique and Silvapulle (2001) found it in seven Asian stock markets. Similarly, Assaf and Cavalcante (2005) reported long memory in Brazilian stock market volatility. After applying fractional integrated autoregressive moving average—General Autoregressive Conditional Heteroskedasticity (ARFIMA-GARCH) model to monthly consumer price index rates data from 1955 to 2014, Belkhouja and Mootamri (2016) found long memory persistence in inflation dynamics in the US, Japan, Canada, UK, Germany, France. Wang and Wu (2012) found persistent volatility in energy futures market daily closing price data from January 2, 1985, to December 14, 2010. Using Baillie et al. (1996) Fractional Integrated General Autoregressive Conditional Heteroskedasticity (FIGARCH) model, Charfeddine (2014) observed long memory in volatility in energy futures data from January 2, 1985, to May 14, 2013. (1996). Also, Kuttu (2018a) used the FIEGARCH model of Bollerslev and Mikkelsen (1996) and discovered long memory in Ghanaian, Kenyan, Nigerian, and South African equities market volatility.

Evidence of long memory has also been documented in the foreign exchange market. Tse (1998) used the FIGARCH model of Baillie et al. (1996) to find long memory in the Yen-US dollar exchange rate. Similarly, Chikili et al (2012) identified long memory in dollar-euro and dollar-British pound exchange rate volatility using univariate Fractional Integrated Asymmetric Power Autoregressive Conditional Heteroskedasticity. After applying the FIGARCH model, Vats (2011) reported long memory in volatility in the US dollar exchange rates of Chinese renminbi, Indonesia rupiah, and Taiwan dollar in Asia. Mensi et al. (2014) used the ARFIMA–FIGARCH model to find long memory in conditional volatility for Saudi exchange rates against the US dollar, Euro, British pound, and Japanese yen.

Long memory features in international financial markets have been studied as possible explanations for market efficiency. Many studies on long memory in African currency markets explored statistical dependency in the first moment, while others used symmetric heteroskedastic models in the second. However, Kuttu (2018b) found volatility asymmetry in these markets. Structural breaks affect long memory in currency markets, but previous studies ignored this. However, Breitung and Eickmeier (2011) argue that ignoring structure breaks can lead to spurious estimates.

Given the forgoing, this study uses the Fractional Integrated Exponential GARCH (FIEGARCH) model of Bollerslev and Mikkelsen to evaluate long memory in Egypt, Ghana, Kenya, Nigeria, and South Africa's foreign currency markets (1996). Structured breaks in the data are also considered.

The countries in this study are import-dependent and export largely agricultural, mining, and oil products in dollars. These make them relatively more exposed to commodity price shocks. Remittances, tourism, and foreign donor flows also remain a crucial source of foreign exchange. In addition, portfolio investors, foreign multinationals, and international banks have an active role, particularly in the Eurobond and the local currency markets. Other important features that influence the exchange rate in these countries are the fiscal situation, government debt, external debt, inflation, monetary policy, and the political cycle.

Few studies have examined the long memory dynamics in African foreign exchange markets. Aron (1997) used cointegration on monthly data from January 1970 to February 1995 and concluded that exchange rates in South Africa are predictable. Using cointegration, Aron and Ayogu (1997) found similar results. Sifunjo et al. (2008) used run tests, unit root tests, and Ljung-Box Q-statistics to establish that the Kenyan foreign currency market is inefficient from January 1994 to June 2007. Ayogu (1997) found Nigeria's foreign exchange market inefficient using a likelihood ratio test on data from January 1 to December 31, 1993. Chiwira and Muyambiri (2012) found the market inefficient, using Augmented Dickey-Fuller, autocorrelation, Kolmogorov–Smirnov, Runs, and Phillips-Perron unit root tests on Botswana's 2004 –2008 foreign exchange data. Aidoo et al. (2012) found significant long memory in Ghana's cedi/dollar exchange rate using rescaled-range and modified tests on monthly data from January 1990 to January 2012. Ebuh et al (2022) used a fractional cointegrated vector autoregressive model on the US dollar-naira, euro-naira, yen-naira, British pound-naira, Indian rupee-Naira, and Chinese yuan-Naira and discovered long memory in the Nigerian currency market.

Very few studies on African currency markets used GARCH models to analyse long memory in the second moment used symmetric volatility model. However, Kuttu (2018b) contends that official foreign exchange market intervention causes volatility asymmetry. When using Fractional Integrated GARCH (FIGARCH) of Baillie et al. (1996), Jefferis and Thupayagale (2011) found significant long memory in the rand/dollar exchange rate. This finding is confirmed by May and Farrell (2018), who used FIGARCH and Fractionally Integrated Asymmetric Power ARCH on rand/US dollar, euro, British pound, and Japanese yen data from March 13, 1995, to August 13, 2010. Boateng et al. (2020) found comparable results in the South African currency market. Similarly, for Ghana, Omane-Adjepong et al (2018) reported significant long-range dependence on the Ghanaian foreign exchange market after they applied ARFIMA–FIGARCH cedi/dollar exchange rate data that span Amy 31, 1999 to November 30, 2017.

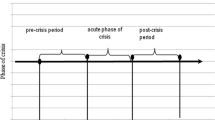

Following the above discussion, this study applies an asymmetric volatility model and examines the long memory features of the volatility on the foreign exchange markets of Egypt, Ghana, Kenya, Nigeria and South Africa. Additionally, we perform a structural break test to determine whether structural breaks influence the statistical dependence in these foreign exchange markets. According to Breitung and Eickmeier (2011), large economic events or monetary policy changes might affect variables in empirical studies. Some are more subtle, yet they nonetheless change the structure of the economy. Ignoring structure breaks can lead to spurious results.

We focus on these countries because, according to the World Bank (2023), Egypt is the largest economy in North Africa (with a GDP of $424.7 billion at 2021 prices), Kenya is the largest in East Africa (with a GDP of $109.7 billion at 2021 prices), South Africa is the largest in Southern Africa (with a GDP of $419 billion at 2019 prices), and Nigeria is the largest in W Africa. Ghana is added because the World Bank (2021) promoted it as an African success storey before the COVID-19 epidemic (with a GDP of $68.3 billion in 2019 and $79.2 billion in 2021 values). These countries also have strong equities markets that can enable international investors diversify into emerging and frontier economies.

The Bollerslev and Mikkelsen (1996) FIEGARCH model is used to examine how long memory affects volatility in the Egyptian, Ghanaian, Kenyan, Nigerian, and South African foreign currency markets. The study spans June 2, 1997, to December 31, 2021.

The paper makes two contributions to African foreign currency market efficiency studies. To this author's knowledge, this is the first study to use the FIEGARCH model of Bollerslev and Mikkelsen (1996) to examine long memory in African foreign exchange markets. Omane-Adjepong, Boako, and Alagidede (2018) and Jefferis and Thupayagale (2011) explore long memory in Ghanaian and South African foreign exchange markets using a FIGARCH model. To make the FIGARCH model stationary with positive conditional variance, complicated and intractable restrictions must be imposed. Also, according to Kuttu (2018b), the FIGARCH model does not nest the volatility asymmetry in the African foreign exchange markets. The FIEGARCH model applied in this study requires no non-negativity or invertibility constraints. Also, the conditional variances can oscillate,and so-called leverage effects—asymmetry between positive and negative shocks of equal magnitude from the same source—are taken into account.

The findings indicate a long memory of volatility in the foreign exchange markets of Egypt, Ghana, Kenya, Nigeria and South Africa. Structural break analysis carried out on the five foreign exchange markets shows that the long memory dependence identified is not a function of time; hence, it is not spurious.

The findings in this study may have implications for risk management. Given that volatility affects hedge ratios, derivative pricing, value-at-risk, and trading and hedging tactics, market players may benefit from identifying long memory in foreign currency return volatility. Volatility helps price and hedge derivative strategies, therefore, persistence in volatility may help investors price long-term derivative contracts (Bollerslev & Mikkelsen 1996). The conditional volatility in these markets has long memory and substantial first-order autocorrelation, implying predictable first- and second-moment dynamics. To reduce market predictability, gorvenment intervention should be unpredictable with changing rules.

The following is the outline for the remainder of the paper. What follows is an explanation of the long memory model. Data and preliminary statistical properties are presented in Sect. 3. In Sect. 4, we present and analyse the empirical results. The paper is concluded in Sect. 7.

2 Methodology

2.1 The FIEGARCH model

We model the long-term memory effect in FX market volatility by presuming that the following autoregressive process (AR) generates the currency market returns, \({r}_{t,}\):

where \({\varepsilon }_{t}=\sqrt{{h}_{t}}{\epsilon }_{t}\), and \({\epsilon }_{t}\backsim NID(\mathrm{0,1})\) and \({h}_{t}\) and \({\epsilon }_{t}^{2}\) are conditional and the unconditional variances of \({\varepsilon }_{t}\), respectively.

As a means of accommodating volatility asymmetry, Bollerslev and Mikkelsen (1996) extend the FIGARCH model of Baillie et al. (1996) to FIEGARCH, which is equivalent to Nelson's (1991) Exponential GARCH model. While the FIGARCH model requires that the estimated parameters adhere to non-negativity constraints, the FIEGARCH model can be considered well-specified even without these requirements. The FIEGARCH \(\left(p,d,q\right)\) has the variance, \({h}_{t}\), form Eq. (1) modelled as follows:

where \(\delta\) denotes the non-trading day count dummy, \(\psi\) captures the high frequency effects and \(\phi\) denotes the long-term effects. The leverage effect is represented by \(g\left({z}_{t-1}\right)={\varphi }_{{z}_{t-1}}+\gamma \left[\left|{z}_{t-1}\right|-E\left|{z}_{t-1}\right|\right]\), the first term, \({\varphi }_{{z}_{t}}\), is the sign effect and the second term, \(\left(\gamma \left[\left|{z}_{t-1}\right|-E\left|{z}_{t-1}\right|\right]\right)\), is the magnitude effect. When \(d=0\), the FIEGARCH model nests the EGARCH of Nelson (1991) model, and when \(d=1\), it reduces to IEGARCH. The FIEGARCH parsimonious separate the movements in the long-run and short-run volatility, the fractionally differencing parameter \(d\) captures the long-run component and the lag polynomials capture the short-run component. When the \(d\) parameter is within the interval \(0<d<1\), Fama's weak-form efficient market hypothesis is easily rejected (1970). Nonetheless, parameters above one indicates a non-stationary process, while parameters below zero indicate a stationary and non-invertible process. These imply that the return series are stochastic and lack predictable structures.

To maximise the log-likelihood function via Quasi-Maximum Likelihood Estimation (QMLE), we employ the BFGS algorithm (in RATS™ 8.2) proposed by Broyden (1970), Fletcher (1970), Goldfarb (1970), and Shanno (1970) due to the non-linearity of the log-likelihood function in the parameters. According to Bollerslev and Wooldridge (1992), the QMLE is robust to the distribution of the disturbance term.

2.2 The Bai and Perron model

To identify spurious long memory, we apply Bai and Perron (1998, 2003) methodology to examine structural breaks in return series of the five countries. Bai and Perron (1998, 2003) consider the following linear regression with \(m\) breaks and \(m+1\) regimes:

where \(j\)=1,…..,\(m+1\). In Eq. (3), \({y}_{t}\) is the observed dependable variable at time \(t\); \({x}_{t} (p \times 1)\) and \({z}_{t} (q \times 1)\) are vectors of covariates and \(\eta\) and \({\lambda }_{j}\) \((j=1,\dots \dots ., m+1)\) are the corresponding vector coefficients; \({u}_{t}\) is the error term at time \(t\). Choi et al. (2010) have argued that \({u}_{t}\) may be serially correlated and heteroskedastic. The break points, \({T}_{1}+1,\dots \dots \dots ,{T}_{m+1}\), are treated as unknown, and By employing this technique, we are able to approximate not only the breaks but also the unknown regression coefficients. Specifically, Bai and Perron (1998, 2003) offered three separate statistics for identifying breaks; these are:

-

1.

the \(supF\) type test of no structural break (\(m=0)\) versus \(m=k\) breaks

-

2.

\(l\) versus \(l+1\) breaks, labelled \(sup{F}_{T}\left(l+1|l\right)\)

-

3.

double maximum tests: \(UD max{F}_{T}\left(M,q\right)and WD max{F}_{T}(M,q)\)

The results show three distinct information criteria: sequential estimates, the modified Schwarz criterion (LWZ), and the Bayesian Information Criterion (BIC). Since the BIC and LWZ tests produce misleading results when serial correlation errors are present, Bai and Perron's (1998, 2003) methodology relies on applying the \(sup{F}_{T}\left(l+1|l\right)\) test in sequential order to address this issue.

3 Data and preliminary statistical properties

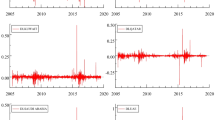

The data set includes continuously compounded daily returns from June 2, 1997, to December 31, 2021. Dollar exchange rate per local currency is our exchange rate market proxy. Thus, the dollar exchange rate for the Egyptian pound, Ghanaian cedi, Kenyan shilling, Nigerian naira, and South African rand. The use of the dollar per local currency is predicated on the fact that the US dollar is a vehicle currency actively used for transactions in the global currency, and the external reserves of these countries, which the central bank used to maintain exchange rate stability, are denominated in US dollar. Since Standard & Poor's started keeping track of data for Ghana, Kenya, and Nigeria in the middle to late 1997, the sample date starts from June 2, 1997. The data were obtained from DataStream.

Table 1 shows positive skewness in all foreign exchange markets, indicating more positive shocks than negative shocks. These foreign exchange markets should yield good returns for investors. We find leptokurtosis in each of the five markets, and normality is rejected. Applying a nonlinear model is compatible with rejecting normality. Standardised residuals and squared standardised residuals of the return series are dependent. Every series has a significant ARCH effect, supporting a heteroskedastic model. Finally, Dickey and Fuller (1979) unit root test rejected the null hypothesis in every series.

4 Empirical results

The quasi-maximum likelihood estimations for AR(2)-FIGARCH (Eqs. 1 and 2) for the five countries are reported in Table 2. As the number of parameters in the model increases, the penalty from the Schwarz information criterion becomes larger, and the AR(2)-FIEGARCH is the best model that the AIC always chooses. Therefore, the results from the AR(2)-FIEGARCH model are the only ones that are presented.

As shown in Table 4, for all five currency markets, the first-order autocorrelation, \({\beta }_{1}\), is positive and statistically significant. As a result, the return process is not completely random and there is some predictability in the currency market. For each of the five currency markets, the second-order autocorrelation, \({\beta}_{2}\), is statistically significant and negative. An explanation for this might lie in the so-called mean-reversion behaviour of returns in the foreign exchange market (Ding et al. 1993).

All currency markets exhibit very significant values for the parameters \(\varphi\) and \(\gamma\), which represent the news impact function in the FIEGARCH model. Specifically, for every country, \(\gamma\) is statistical significance. This indicates that the conditional variance is impacted asymmetrically by positive and negative shocks to the returns. A negative value for the asymmetric parameter, \(\varphi\), indicates that volatility is asymmetric.

For all markets, the non-trading day count, \(\delta ,\) is statistically significant. Importantly, it shows that in Egypt, Ghana, Kenya, and Nigeria, the weekend and holiday components of the daily variance amount to approximately 7%, 4%, 12%, 7%, and 3%, respectively.

For each of the five foreign exchange markets under consideration, the point estimate of the asymmetric long memory parameter, \(d\), falls within the range of 0 to 1, suggesting that the underlying series is stationary and exhibits long memory in the conditional variance. This provides evidence of persistent volatility, which can be utilised to predict volatility values across all five currency markets. It is worth noting that economically, the long-memory coefficient for South Africa is not significant in the full sample and in the two sub-samples. This may be attributed to comparatively fewer rigidities and the relative breadth and depth of the South African foreign exchange market.

Egyptian, Ghanaian, Kenyan, Nigerian, and South African foreign exchange markets have long memories, disproving the weak-form efficient market hypothesis. This shows previous volatility can predict current volatility.

Diagnostic results from Panel B of Table 2 show a mean of zero and a variance of one for all currency markets. This suggests that the model is well-specified. The standardised and squared standardised residuals are not serially correlated.

In Table 3, the sign test, joint test, and positive and negative sign bias tests for volatility specification are not statistically significant. Since return series have long memory with asymmetrical volatility, the FIEGARCH model can capture their conditional volatility better.

According to Ryden et al. (1998), Liu (2000), and Granger and Hyung (2004), long memory in financial return volatility is spurious due to unaccounted structural breaks. We used Bai and Perron's (1998, 2003) structural break analysis to identify spurious long memory. The method allows for many structural breaks in the data series.

5 Structural breaks

Based on the structural break procedure outlined by Bai and Perron (1998, 2003) in Table 4, it was observed that Egypt, Kenya, and Nigeria each had two structural breaks, while Ghana and South Africa each had one structural break during the sample period. The structural break points for Egypt were on January 1, 2003, and January 9, 2013; Kenya’s was on May 13, 1999, and February 25, 2011; and Nigeria’s was on October 25, 2000, and January 8, 2009. Ghana and South Africa had one structural break on November 24, 2008, and April 19, 2000, respectively. The data for the five countries were split on their respective structural break dates for further long memory examination.

From Table 5 and 6, the parameters \(\varphi\) and \(\gamma\), and the non-trading day count, \(\delta\), are significant across all sub-sample. Also, for all the five countries, the long memory parameter, \(d\), is significant across all sub-samples. Clearly, the results indicate that the long memory statistical properties on these markets are not a function of time. Further, the diagnostic tests in Panel B of Table 5 and 6, and in Table 7 and 8 show that the model is well specified. These findings are complementary and therefore, suggest that long memory found in the five foreign exchange markets is not spurious. Also, we compute how long it takes for a unit shock to subside by half, the so-called half-life which is given by \({\text{log}}\left(0.5\right)/log\left(\phi \right)\). We find that it takes approximately 2.4 days, 2.5 days. 2.3 days, 3.7 days and 1.9 days for unit shock to dissipate by half for Egypt, Ghana, Kenya, Nigeria and South Africa, respectively.

6 Discussion

The first-order positive autocorrelation and long memory in volatility memory on the five foreign currency markets show a relationship between recent and distant results and volatility. Also, past returns and volatility may be used to predict future returns and volatility, especially over long horizons. Similar findings have been reported by Aidoo et al. (2012) for Ghana and Jefferis and Thupayagale (2011) for South Africa.

Predictability in returns and volatility may indicate inefficiency, and long memory in volatilty may favour foreign exchange speculators because new information will not be arbitraged away quickly. However, for South Africa, this economic benefit may be limited, given that the long memory coefficient is economically insignificant.

The findings of long memory volatility in the foreign exchange markets of Egypt, Ghana, Kenya, Nigeria and South Africa suggest market inefficiency, with South Africa relatively less inefficient given the economically insignificant long memory coefficient. Egypt, Ghana, Kenya, and Nigeria have adopted a mixture of fixed and managed float over the sample period. The International Monetary Fund (2023b) has stated that, at the end of 2022, Ghana and Kenya follow a crawl-like arrangement, whereas Nigeria and Egypt, follow a stabilised arrangement. However, South Africa follows a free-floating framework. With this crawl-like and stabilised arrangement, the government can intervene in the foreign exchange market. The government can influence the exchange rate, but it is not committed to maintaining a fixed exchange rate or imposing strict limits on it.

If their currency depreciates significantly from its target rate, Dutta and Leon (2002) argue that governments are more likely to intervene because persistent depreciation affects foreign currency debt service and net exports.

Exchange targeting is common in developing nations like Africa, which relies on exports for growth (Calvo et al. 1995). Due to fiscal and financial market shocks, Egypt, Ghana, Kenya, and Nigeria's central banks have intervened heavily in their foreign exchange markets. These interventions alter currency values for a extended period of time. The presence of long memory in all five foreign exchange markets indicate that the markets are inefficient.

Similar findings, for foreign exchange market inefficiency, have been documented by Aron (1997) and Aron and Ayogu (1997) for South Africa, Sifunjo et al. (2008) for Kenya, Ayogu (1997) for Nigeria, and Chiwira and Muyambiri (2012) for Botswana. However, for the foreign exchange markets, the greater predictability brought about by long-term volatility memory is unlikely to produce arbitrage opportunities for smart-money investors. This is due to the fact that increasing levels of predictability are also associated with higher levels of volatility.

Long memory in exchange rate volatility shows that purchasing financial assets in several currencies would not hedge currency risk due to the non-random volatility innovation process. International investors in local equities, bond markets, and foreign direct investors can predict the local currency-dollar exchange rate, to some extent. Unexpected economic data or dramatic political events in any of the countries being analysed can create currency market surges in the short term. Structural weakness in Egypt, Ghana, Kenya, Nigeria, and, to some extent, South Africa—weak industrial bases, high debt burden, high fiscal deficits, macroeconomic instability, and occasional foreign currency shortages—may make any exploitable benefit from the long memory identified in all currency markets fleeting.

El-Masry and Badr (2021), Amewu et al. (2022), Shitemi et al. (2023), Fasanya and Akinwale (2022), and Iyke and Ho (2021) found currency and stock market links in Egypt, Ghana, Kenya, Nigeria, and South Africa. All five currency markets demonstrate long memory, indicating that exchange rate shocks last longer and may affect equities markets.

According to Ghosh et al (2010), each African country's currency rate regime depends on its macroeconomic fundamentals and unique conditions. African currency rate regimes have varied throughout time.

International Monetary Fund (2023b) classifies Ghana and Kenya's exchange rate anchor as a crawl-like arrangement with an inflation-targeting monetary framework in its 2023 annual report on exchange rate arrangement and restrictions. Similarly, the International Monetary Fund (2023b) has classified that of Nigeria and Egypt as having a stabilised arrangement. Nigeria and Egypt, respectively, have monetary aggregate target monetary framework and other monetary frameworks with no nominal anchor. However, Egypt monitors various indicators in conducting monetary policy. Lastly, South Africa has a floating monetary framework anchored on an inflation-targeting monetary policy framework.

Leiderman and Bufman (2000) claim a crawl-like arrangement can reduce inflation. However, cross-border capital flow contradicts this. For instance, increasing domestic real interest rates to combat inflation may increase capital inflows and leads to nominal exchange appreciation. Leiderman and Bufman (2000) further suggest that a narrow exchange rate volatility band may distort investors' perception of exchange rate risk. Capital inflows may be large when domestic and foreign interest rates diverge. Finally, the crawl-like arrangement may conflict with other objectives of monetary policy, such as inflation targeting, because the level of interest rate needed to achieve a particular inflation target may be markedly different from the level suitable for maintaining the currency volatility band.

The findings should be seen in light of the unique dynamics that characterise African foreign exchange markets and not on the statistical properties alone. For example, Africa’s foreign exchange markets are characterised mainly by an occasional lack of foreign currency liquidity. Supply of hard currency is largely dependent on raw commodities exported and the amount of foreign currency reserve held by the central banks. The supply of foreign currency in the foreign exchange markets is affected by fluctuations in commodity prices because of the underdeveloped manufacturing base.

This notwithstanding, the findings have risk management and policy implications. Given the long memory identified in all five currency markets, Lasfer et al. (2003) have argued that, in a currency market where past innovation can be used to predict future innovation, any investment strategies based on historical volatility can generate risk-adjusted returns innovations. The presence of long memory may indicate that unexploited profit exists for risk-seeking speculators and international investors in these countries’ financial assets. However, given the unique characteristics found in these exchange rate markets, a risk averse investor may not find the exploitable profit large enough to account for the inherent risk in these markets.

Also, forecasters can use the current spot rate of the exchange rate of the five countries’ currencies to forecast the future spot rate and may have implications for purchasing power parity (Kuttu 2018b). From a policy perspective, it has been contended by Dutta and Leon (2002), Mohanty and Klau (2004), and Calvo, Reinhart and Vegh (1995) that monetary authorities tend to support depreciation rather than appreciation because it has the potential to impact net exports and the cost of servicing debt denominated in foreign currency. This creates a large shock, given a finite sample, this could make the market predictable. Hence, official intervention should be random, with changing rules to make the market less predictable. Also, monetary authorities should continue to clamp down very hard on the illegal parallel markets in the various countries to render foreign exchange market policy more effective, and hence, reduce the predictability of the currency markets.

7 Conclusion

This study analysed the second-moment long-term memory in the context of the Egyptian, Ghanaian, Kenyan, Nigerian, and South African currency markets. Using data collected between June 2, 1997, and December 31, 2021, we estimated the FIEGARCH model developed by Bollerslev and Mikkelsen (1996)..

According to the findings, the Egyptian, Ghanaian, Kenyan, Nigerian, and South African foreign exchange markets exhibit significant long memory. The results of the structural break analysis did not indicate the presence of spurious long memory. We do, however, find that South Africa's long memory coefficient is economically insignificant. Bollerslev and Wright (2000) have argued that high-frequency data gives a clearer picture of long memory than relatively low-frequency data. Hence, we recommend that future studies should re-examine this issue using tick data, should this become available.

This notwithstanding, the findings imply that past innovations can be used to forecast current innovations, which disproves the weak-form efficient market theory. This affects the efficiency of allocation and, more broadly, the role of the currency markets in driving economic expansion. The risk management approach to take might be influenced by the results presented in this paper. Specifically, emerging and frontier markets investors can incorporate some level of exploitative risk in their prediction model to take advantage of the inefficiencies presented in these markets. Furthermore, the findings have implications for derivative pricing and portfolio diversification, especially in South Africa, which has a derivatives market. Also, official intervention should be random, with changing rules to make the market less predictable.

8 Data availability

The data used for this study was sourced from Thomson Reuters Datastream, a secondary data provider. Most universities in the world have access to this data.

References

Aidoo EN, Bashiru IIS, Ababio KA, Nsowah-Nuamah NN, Munyakazi L (2012) Analysis of Long Memory Dynamics in Exchange Rate. The Empirical Economics Letters 11:745–754

Amewu G, Junior PO, Amenyitor EA (2022) Co-movement between equity index and exchange rate: fresh evidence from Covid-19 era. Scientific African 16:e01146

Aron J (1997) Foreign exchange market efficiency tests in South Africa. Department of Economics, Oxford University Press Southern Africa (Pty) Ltd, Centre for the Study of African Economies

Aron J, Ayogu M (1997) Foreign exchange market efficiency tests in Sub-Saharan Africa: Econometric analysis and implications for policy. J Afr Econ 6:150–192

Assaf A, Cavalcante J (2005) Long-range dependence in the returns and volatility of the Brazilian stock market. European Review of Economics and Finance 5:5–20

Ayogu MD (1997) Return predictability: Evidence from Nigeria’s foreign exchange parallel market. J Afr Econ 6:296–313

Bai J, Perron P (1998) Estimating and testing linear models with multiple structural changes. Econometrica 66:47–78

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Economet 18:1–22

Baillie RT, Bollerslev T, Mikkelsen H (1996) Fractionally integrated generalised autoregressive conditional heteroskedasticity. Journal of Econometrics 74:3–30

Belkhouja M, Mootamri I (2016) Long memory and structural change in the G7 inflation dynamics. Econ Model 54:450–462

Boateng A, Claudio-Quiroga G, Gil-Alana LA (2020) Exchange rate dynamics in South Africa. Appl Econ 52:2339–2352

Bollerslev T, Mikkelsen HO (1996) Modelling and pricing long memory in stock market volatility. Journal of Econometrics 73:151–184

Bollerslev T, Wooldridge JM (1992) Quasi-maximum likelihood estimation and inference in dynamic models with time-varying variances. Economet Rev 11:143–172

Bollerslev T, Wright JH (2000) Semiparametric estimation of long-memory volatility dependencies: The role of high-frequency data. Journal of Econometrics 98:81–106

Breitung J, Eickmeier S (2011) Testing for structural breaks in dynamic factor models. Journal of Econometrics 163:71–84

Broyden CG (1970) The convergence of a class of double-rank minimisation algorithms: 2. The new algorithm. IMA J Appl Math 6:222–231

Calvo GA, Reinhart CM, Végh CA (1995) Targeting the real exchange rate: Theory and evidence. J Dev Econ 47:97–133

Charfeddine C (2014) True or spurious long memory in volatility: Further evidence on the energy futures markets. Energy Policy 71:76–93

Chiwira O, Muyambiri B (2012) A test of weak form efficiency for the Botswana stock exchange (2004–2008). British Journal of Economics, Management & Trade 2:83–91

Chikili W, Aloui C, Nguyen DK (2012) Asymmetric effects and long memory in dynamic volatility relationships between stock returns and exchange rates. J Int Finan Markets Inst Money 22:738–757

Choi K, Yu WC, Zivot E (2010) Long memory versus structural breaks in modeling and forecasting realised volatility. J Int Money Financ 29:857–875

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74:427–431

Ding Z, Granger CWJ, Engle RF (1993) A long memory property of stock returns and a new model. J Empir Financ 1:83–106

Dutta J, Leon H (2002) Dread of depreciation: measuring real exchange rate interventions. IMF Working Paper WP/02/63, Washington, DC.

Ebuh GU, Usman STS, N, (2022) Long memory in nominal exchange rates in Nigeria: An examination using fractionally integrated and cointegrated models with structural breaks. Contaduría y Administración 67:16

El-Masry AA, Badr OM (2021) Stock market performance and foreign exchange market in Egypt: does 25th January revolution matter? Int J Emerg Mark 16:1048–1076

Fletcher R (1970) A new approach to variable metric algorithms. Comput J 13:317–322

Ghosh A, Ostry J, Tsangarides C (2010) Toward a stable system of exchange rates. IMF Occasional Paper, 270.

Goldfarb D (1970) A family of variable-metric methods derived by variational means. Math Comput 24:23–26

Granger CWJ, Hyung N (2004) Occasional structural breaks and long memory with an application to the S&P 500 absolute stock returns. J Empir Financ 11:399–421

International Monetary Fund (2023a) World Economic Outlook: Navigating Global Divergences. IMF, Washington, DC

International Monetary Fund (2023b) Annual Report on Exchange Arrangements and Exchange Restrictions: Overview 2022. IMF, Washington, DC

Iyke BN, Ho SY (2021) Exchange rate exposure in the South African stock market before and during the COVID-19 pandemic. Financ Res Lett 43:102000

Jefferis K, Thupayagale P (2011) Real versus spurious long-memory volatility in foreign exchange data: Evidence from the rand against the G4 currencies. Stud Econ Econ 35:71–93

Kuttu S (2018a) Modelling long memory in volatility in sub-Saharan African equity markets. Res Int Bus Financ 44:176–185

Kuttu S (2018b) Asymmetric mean reversion and volatility in African real exchange rates. Journal of Economics and Finance 42:575–590

Lasfer M, Melnik A, Thomas D (2003) Short-term reaction of stock markets in stressful circumstances. J Bank Finance 27:1959–1977

Leiderman L, Bufman G (2000) Inflation targeting under a crawling band exchange rate regime: lessons from Israel. Inflation Targeting in Practice: Strategic and Operational Issues and Application to Emerging Market Economies, IMF, Washington DC, 70–79.

Liu M (2000) Modelling long memory in stock market volatility. Journal of Econometrics 99:139–171

May C, Farrell G (2018) Modelling exchange rate volatility dynamics: Empirical evidence from South Africa. Stud Econ Econ 42:71–113

Mensi W, Hammoudeh S, Yoon SM (2014) Structural breaks and long memory in modelling and forecasting volatility of foreign exchange markets of oil exporters: The importance of scheduled and unscheduled news announcements. Int Rev Econ Financ 30:101–119

Mohanty MS, Klau M (2004) Monetary policy rules in emerging market economies: issues and evidence. Bank for International Settlements Working Paper no. 149, Basel, Switzerland

Nagayasu J (2003) The efficiency of the Japanese equity market. IMF Working Paper. WP/03/142.

Nelson D (1991) Conditional heteroskedasticity in stock returns: A new approach. Econometrica 59:347–370

Omane-Adjepong M, Boako G, Alagidede P (2018) Modelling heterogeneous speculation in Ghana’s foreign exchange market: Evidence from ARFIMA-FIGARCH and Semi-Parametric methods. MPRA Paper 86617, University Library of Munich, Germany.

Ryden T, Terasvirta T, Asbrink S (1998) Stylised facts of daily return series and the hidden Markov model. J Appl Economet 13:217–244

Sadique S, Silvapulle P (2001) Long-term memory in stock market returns: International evidence. Int J Financ Econ 6:59–67

Shanno DF (1970) Conditioning of quasi-Newton methods for function minimisation. Math Comput 24:647–656

Shitemi S, Maingi M, Egessa R (2023) Effects of Exchange Rate on Performance of Equity Funds in Kenya. African Journal of Empirical Research 4(2):891–897

Sifunjo EK, Ngugi WR, Ganesh P, Gituro W (2008) An analysis of the efficiency of the foreign exchange market in Kenya. Economics Bulletin 14:1–13

Tse YK (1998) The conditional heteroskedasticity of the Yen-Dollar exchange rate. J Appl Economet 13:49–55

Vats A (2011) Long memory in returns and volatility: Evidence from foreign exchange market of Asian countries. The International Journal of Applied Economics and Finance 5:245–256

Wang Y, Wu C (2012) Long memory in energy futures markets: Further evidence. Resour Policy 37:261–272

World Bank (2023) Global Economic Prospects, January 2023. World Bank, Washington, DC. https://doi.org/10.1586/978-1-4648-1906-3.License:CreativeCommonsAttributionCCBY3.0IGO

World Bank (2021) Ghana Rising: Accelerating Economic Transformation and Creating Jobs. Washington, DC: World Bank

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Declarations

Financial support from the University of Ghana Business School is gratefully acknowledged.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Kuttu, S., Abor, J.Y. & Amewu, G. Long memory in volatility in foreign exchange markets: evidence from selected countries in Africa. J Econ Finan 48, 462–482 (2024). https://doi.org/10.1007/s12197-024-09668-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12197-024-09668-9