Abstract

This paper examines how stock returns respond to oil prices with monthly data from 1990 to 2020 for 12 major economies: 6 oil-exporting countries and 6 oil-importing countries. Combining short and long-run empirical approaches in country-by-country analyses, we first document varying effects of oil price returns in the short-term, while increases in volatility (changes in VIX or geopolitical risk) have negative effects on stock markets. Dynamic OLS (DOLS) estimators show in the long-run positive oil price effects on stock markets for oil-exporters and relatively weaker negative evidence for oil-importers. Interest rate increases have strong negative effects in the long run. Panel analyses shed further light on these results along with structural breaks. Our findings suggest complementary insights from the DOLS long-run approach: oil prices and bond yields have expected signs and volatility has mixed effects on stock markets.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Despite different perspectives in examining the relationship between oil price and the stock market, the evidence has been mixed. This conundrum continues to engender new studies that attempt to shed light on this relationship. In this vein, we combine dynamic ordinary least squares (DOLS), a long-run econometric technique that has received little or no attention in stock market-oil price research, with a short-run method to investigate the association between oil price and the aggregate stock market.

Research on the economic link between stock returns and oil price returns is well-documented. One strand of literature employs econometric techniques such as cointegration methods to focus on the long-run perspective (Sahu et al. 2014; Alamgir and Bin Amin 2021). Additionally, researchers consider the stock return—oil price nexus for oil-importing and oil-exporting countries with contrasting findings (Bouri 2015; and Gupta 2016). Besides, there are papers that use a panel set of countries (Arouri and Rault 2012; Westerlund and Sharma 2019). Most studies concentrate on the response of stock price to oil prices in developed economies such as the U.S., UK, Australia, Canada, and other European countries (Am and Shanmugasundaram 2017). On the other hand, Sharma et al. (2018), Alamgir and Bin Amin (2021), among others, focus on emerging markets. Using Vector Autoregressive (VAR) models, some authors consider the response of the stock market to shocks in oil prices (Sadorsky 1999; Papapetrou 2001; Kang and Ratti 2013). For instance, Kilian and Park (2009) apply Kilian (2009) to the U.S. stock market and report that stock market returns do not respond to supply-side shocks, while positive (negative) responses are observed after aggregate demand (precautionary demand) shocks. Arampatzidis et al. (2021) find results, consistent with Kilian and Park (2009), for the aggregate stock market and for forty-nine U.S. industry-specific portfolios. In contrast, Cunado and de Gracia (2014) suggest that oil supply shock is the main driver of a negative and significant impact of oil price changes on most European stock market returns, whereas the effect of oil price change triggered by demand shock can be either positive or negative. Others examine the time-varying relationship between oil shocks and stock market performance using either multivariate Generalized Autoregressive Conditional Heteroskedasticity (GARCH) models, Time-Varying Parameter Vector Autoregressive models, and others (Lee and Zeng 2011; Moya–Martínez et al. 2014). The measure of the stock market also varies from aggregate indices to sectors and to firm-level evidence. Notwithstanding these various perspectives that shed light on the stock market—oil price nexus, the findings are inconclusive while the relationship also misses evidence combining short and long-run approaches.

In this paper we complement long-run DOLS with evidence on return predictability more commonly associated with short-run effects to examine the impact of changes in West Texas Intermediate (WTI) oil price on aggregate stock markets. We also use monthly data from 1990 to 2020 which provides a sufficiently long time-span to better ascertain the properties of cointegrated variables by implementing the DOLS methodology. The long length of the sample period is important given that some authors document a time-varying oil-stock market relationship (Filis et al. 2011; Sadorsky 2012). Lothian (1990) argues that the difference in the length of a data series may be crucial. Our sample countries include six oil-exporting and six oil-importing countries, with equal representation of emerging and advanced economies in each set.

For our short-run specification, we first follow Narayan (2019) and include a measure of uncertainty, namely market volatility index (VIX) or geopolitical risk (Gpr). In other analyses, we augment our models with discount rates to examine the effects of monetary policy in our set-up. Starting with country-by-country OLS regressions with fixed or flexible lag-lengths, we document that the effects of oil price returns vary in the short-term: from changing signs in Brazil (formerly an oil importer and more recently a major oil producer) to negative effects for 3 oil exporters to no effects for 2 oil exporters. Thus, the relationship is ambiguous for oil-exporters using the Narayan (2019) model. By contrast, we observe negative oil price effects on stock markets for all 6 oil importers, though the relationship is not significant in 2 of these markets. We also find that Johansen cointegration tests confirm the existence of long-run trends between stock market indices, oil prices, VIX, and long bond yields; the result of this tests justify the use of DOLS to generate estimates for the long-run. The distinctive result with the DOLS is that the oil price effect on stock markets now becomes positive and significant for all oil-exporting economies with coefficients varying from 0.077 in the U.S to 0.736 in Brazil. Interest rate changes have negative effects in 10 (almost one to one: -1.048 in Mexico, -1.101 in Russia, -0.909 in the U.S., and 0.920 in Germany) out of 12 countries. VIX has mixed effects in the long-run, in contrast to its always negative effects in short-run modelling. In further analysis, we employ fixed effects panel regressions which are known to yield more robust findings compared to individual-specific studies. Panel analysis increases the precision of estimators and provides more reliable inferences, which leads us to pool the data into two sets comprising our sample of oil-exporting and oil-importing countries. The panel analysis corroborates our findings with country-by-country regressions. While the effect of oil price on the stock markets of net oil exporters may appear to be negative or unclear in predictive regressions, long-run econometric methods uncover significant gains in these stock markets when oil prices go up.

This study adds to debate on the heterogeneity of the effect of oil price movements on stock markets of oil-exporting countries versus oil-importing countries. Studies for oil-exporting countries suggest a positive relationship between oil and stock prices, while studies of oil-importing countries report a decline in stock prices as oil price rises (Sadorsky 1999; Park and Ratti 2008; Bjornland 2009; Cunado and de Gracia 2014). There is contradictory evidence, however. Using Nonlinear Autoregressive Distributed Lag, Alamgir and Bin Amin (2021) document a positive relationship between the world oil price and stock market index for 4 selected South Asian countries. They specifically note that the “tendency for stocks to move along with world oil prices is entirely unexpected, especially in countries like Bangladesh, India, Pakistan, and Sri Lanka, net importers of oil” (Alamgir and Bin Amin 2021, p. 699). Similarly, Prabheesh et al. (2020) find a positive co-movement between oil price returns and stock price returns during the COVID-19 period for China, India, Japan, and Korea. Cong et al. (2008) employ a multivariate vector auto-regression and report that oil price shocks do not have statistically significant effects on the real stock returns of most Chinese stock market indices, except for the indices of manufacturing and some oil companies.

Our paper complements these studies by providing evidence that DOLS techniques clearly identify positive effects of oil price changes on stock markets of oil exporters relative to the negative oil price effects for oil importers. This observation is important, particularly given that even studies that decomposed oil price shocks, such as Cunado and de Gracia (2014), document findings that contradict Kilian and Park (2009). Moreover, in spite of various econometric techniques (including SVAR, GARCH, Vector Error Correction Models, wavelength analyses, among others) employed by other studies, the lack of consensus in findings remains unresolved. We also provide evidence based on panel data which supports time series studies, such as Mollick and Assefa (2013), who document that VIX exerts a negative impact on stock markets.

The rest of this paper is organized as follows. Section 2 lists the data sources and reviews the data properties; Section 3 introduces the empirical models; Section 4 presents the results and Section 5 concludes this article.

2 The data

We collect monthly data from January 1990 to July 2020. We start from 1990 because it is the earliest year for the availability of stock market indices for our sample countries on Datastream. We examine six oil-exporting and six oil-exporting countries – with an equal representation of emerging and developed markets in each category to account for the nature of economies. The oil-exporting countries include Brazil, Mexico, Russia, Canada, Norway and U.S. Brazil, Mexico and Russia are major emerging markets, with Brazil increasing its oil production in 2007–2008,Footnote 1 and the other two (Mexico and Russia) being major oil producers, although Mexico has declining trends and Russia is now the second largest world oil producer according to EIA reports. Canada and Norway are two examples of small open economies and major oil producers. The U.S. has become a major oil producer after 2010 after technological advances in oil production with shale and tight oil drilling. Our oil-importing group includes Japan, Germany, Switzerland, India, China and South Africa. Data on long-term (10-year) government bond yields and stock market indices are from Datastream. Due to the date when the bonds were first issued, data on long-term government yields for Brazil, Mexico and Russia are not available until September 2002, October 1999 and March 2003 respectively. We obtain data on VIX from the Federal Reserve Economic Data (FRED). Data on geopolitical risk (Gpr) is sourced from the updated dataset of Caldara and Iacoviello (2022): https://www.matteoiacoviello.com/gpr.htm.

Definitions of variables are as follows: Stock_ret represents ln(Stock Index Pricet/Stock Index Pricet-1); geopolitical risk comes from Caldara and Iacoviello (2022),who calculate the Gpr by counting the number of articles related to geopolitical risk in each newspaper (11 national and international newspapers) for each month (as a share of the total number of news articles). The index is normalized to average value of 100 in the 2000–2009 decade. We use the first difference of Gpr (Gpr_d) in the empirical models. 30-day implied volatility of options on the S&P 500 is measured by the popular VIX index and Vix_d is the first-difference of Vix. In contrast to Gpr, VIX captures volatility as incorporated in put options on S&P 500 in the U.S. Oil_ret is calculated as ln(Crude WTI oil Pricet/Crude WTI oil Pricet-1). Yield on 10-year government bond is represented by Ltgby and Ltgby_d is first-difference of Ltgby.

Panel A1 of Table 1 shows, for the whole period from 1990 to 2020, that averages of stock market index returns are higher in emerging oil markets, ranging from 0.8% (Russia) to 4% (Brazil) per month, compared to lower returns in advanced oil economies (0.3% in Norway to 0.6% in the U.S.). Stock returns are, however, more volatile in emerging markets with standard deviations ranging from 6.6% in Mexico to 13.2% in Brazil and 14% per month in Russia. On average, interest rates (measured by long-term government yields) have decreased more in emerging market economies, with declines ranging from 0.03% in Mexico to 0.16% in Brazil. They are also more volatile in these countries. On the other hand, advanced economies have average interest rate declines between 0.02% in Japan and 0.03% in Norway. Comparing emerging markets with advanced economies, the results in Panel A2 which is based on oil-importers, are similar to those documented in Panel A1. Specifically, stock returns were lowest in Japan (-0.05%) and highest in India (0.92%), while the average standard deviation is slightly higher for emerging markets (6.21% in South Africa to 8.57% in India). Average oil return is 0.16% per month but highly volatile (standard deviation of 9.91%), while the average changes in geopolitical risk and VIX are 0.08 and 0.01 respectively.

The correlation matrices by country are reported in Table 2. Panel A shows that for oil-exporting countries, interest rate changes are negatively correlated with stock index returns in all emerging markets, while it is positive and statistically significant in the U.S. and less so in Canada and Norway. Oil price returns are positively and significantly correlated with stock index returns in all countries, although the correlation is weaker for Brazil—statistically significant only at 10%. The correlations for oil-importers are in Panel B. interest rate changes have a positive and significant correlation with stock index returns in Japan and China, while the association is negative and significant in South Africa. Surprisingly, oil price return has a statistically significant positive correlation in three oil-importing markets (Japan, India and South Africa), though the relationship is not significant for China, Switzerland and Germany. Changes in Vix (Vix_d) are negatively and significantly correlated with stock index returns across all countries in our sample, with only China characterized by a statistical significance of less than 10%. By contrast, changes in Gpr (Gpr_d) are negatively and significantly correlated with stock index returns in only three countries, namely, Norway, Germany and Switzerland. Vix_d and Gpr_d are not significantly related which may appear surprising given the well-documented literature that suggests that financial markets tend to be volatile around times of political uncertainty (Aysana et al. 2019; and Gkillas et al. 2020). However, this insignificant correlation between Vix_d and Gpr_d is consistent with the fact that these two risk measures represent very different information sets from either volatility in U.S. stock markets or acts or threats in world conflicts and wars.

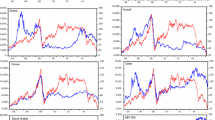

We explore the data further to observe trends in the series (in levels) over the sample period. In Fig. 1, it appears there is a positive relationship between stock index price and oil price in Brazil, Canada, Norway, Mexico and Russia, consistent with the preliminary evidence from the correlation matrices in Table 2. For the U.S., the relationship is less clear based on the time series trends. Similarly, visual inspection of the graphs does not reveal a well-defined relationship for oil-importing countries. However, the relationship between oil price and stock market indices seems to be negative in Japan and China, but positive for India.

Trends in oil prices and stock indices in selected countries. Notes: This figure presents movements of oil prices ($ per barrel) and stock indices over our sample period, January 1990 to July 2020. The left-hand axis pertains to oil prices and the right-hand axis pertains to stock indices. Graph was created with Eviews

3 The empirical models for short and long run: OLS and DOLS

We adapt the model by Narayan (2019), who examines the predictability of oil price news. Specifically, we use oil returns (Oil_ret) for actual oil price movements in a month instead of oil price news. To control for volatility, we replace squared stock returns in Narayan’s model with changes in Vix (Vix_d) or changes in Gpr (Gpr_d). We use Vix since it is a more widely-used proxy for volatility in stock markets, as well as the more recent proxy of uncertainty by Caldara and Iacoviello (2022) for geopolitical risks. This way, our two proxies for uncertainty take the role of news intrinsic to the oil market present in Narayan (2019). Lagged stock returns control for autocorrelation. The modified Narayan (2019) model is as follows:

with variables defined as before. We choose four lags based on the Akaike Information Criterion for each country. As robustness check to the predictive returns approach by Narayan (2019), we include a data dependent procedure based on Campbell and Perron (1991) for optimally selecting the lags in the RHS of Eq. (1). The procedure avoids over-parametrization and tends to perform well in economic and financial applications.Footnote 2 The model is estimated using ordinary least squares and standard errors are corrected for heteroscedasticity using the White approach. In the specification of Eq. (1), oil_ret, Vix_d and Ltgby_d (included in our augmented model) are considered exogeneous while stock return is endogeneous (Narayan and Sharma 2011; and Narayan and Gupta 2015). We also perform Granger causality tests to observe exogeneity of oil_ret, Vix_d and Ltgby_d. In general, the test results, available upon request, indicate that these variables are exogenous though the evidence is weaker (10 percent level of significance) for oil_ret for our oil-exporters panel set.

We next augment Eq. (1) with central banks’ monetary stance using long-term government bond yield (Ltgby). Assefa et al. (2017) document a negative impact of interest rates on stock returns in developed markets in line with the expected cash flow hypothesis. While our modified Narayan (2019) model relates to the short-run, we also explore the long-run relationship between the stock market and oil prices. Specifically, we use a long-run estimator of a potential cointegrating relationship for each country. Thus, we first conduct a unit root test for each variable. Internet Appendix Table A1 shows that stock indices, oil price, VIX, and long-term interest rates contain a unit root and that the series are integrated of order one. Next, for each country, we test for the presence of cointegration. The results of these tests in Internet Appendix Table A2 suggest in most cases strong evidence of a single cointegrating vector for stock index, oil price, VIX, and long-term government rates.Footnote 3 The null of zero cointegration vectors is always rejected while the null of one cointegration vectors cannot be rejected at the 5% level. To estimate the parameters of the cointegrating vector efficiently, we follow Stock and Watson (1993) and Lettau and Ludvigson (2001), who apply the DOLS methodology for consumption-wealth ratio for predicting stock returns. Specifically, we employ the single equation DOLS method below:

where: ln_stock_index, ln_oilpr, ln_vix and ln_ltgby are the natural log of stock market index, oil price, Vix and Ltgby respectively. Notably, unlike the modified Narayan specification in Eq. (1) which uses variables in their return or differenced form, Eq. (2) is based on series in levels, augmented by leads and lags of the difference of right-hand side variables following Lettau and Ludvigson (2001), whose focus is on consumption as explained by asset holdings and labour income. The κ for optimal lag lengths are employed in two ways: by Akaike information criteria and the flexible data dependent procedure described above. Our methodology in this paper, therefore, combines short-run estimations of stationary series (in returns or first-differences) with long-run estimates of non-stationary series in levels.

A legitimate concern is the possible challenge in achieving a consistent estimate of the parameters in Eq. (2) since ln_stock_index, ln_oilpr, ln_vix and ln_ltgby may be endogenously determined. Lettau and Ludvigson (2001) discuss how the asymptotic properties of cointegrated variables is applied by DOLS to overcome this challenge. Specifically, the DOLS specification adds leads and lags of the first difference of the right-hand side variables to eliminate the effects of possible regressor endogeneity on the distribution of the least-squares estimator. This also addresses potential simultaneity and serial correlation in the series. Lettau and Ludvigson (2001) emphasize that the estimates of β1, β2 and β3 will be consistent, though µt may be correlated with the regressors ln_oilpr, ln_vix and ln_ltgby. This is because “OLS estimates of cointegrating parameters are "superconsistent," converging to the true parameter values at a rate proportional to the sample size T rather than proportional to √T as in ordinary applications” (Lettau and Ludvigson 2001, p.823). DOLS can also be employed irrespective of the order of integration of the variables.

4 Results

4.1 Short-run relationship

We estimate Eq. (1) and subsequently incorporate long-term treasury rates (Ltgby) to control for monetary policy. For brevity, we report only the results of the model augmented with Ltgby in Table 3 since both results tell a consistent story. While our inferences are robust to the approach of lag-length used, we present only findings based on flexible lag selection also for space reasons.Footnote 4

Panel A in Table 3 deals with oil-exporting countries. We find that stock returns depend positively on its past returns in Brazil (up to fourth lagged return), positively on fourth lagged stock return for Russia, negatively and positively for first month and second month respectively in Canada, and negatively and positively on first month and fifth month lagged stock returns in the U.S. Besides, oil price returns appear as negative and statistically significant at 4 lags for Russia (-0.181), Canada (-0.057), and Norway (-0.097). For Brazil the coefficient of oil price returns changes from positive and significant at lag 5 to negative and significant at lag 3; this variability of δ-coefficients for oil price returns may well reflect the fact that Brazil was net importer of oil and then became a major producer in the middle of the sample. The net effect in Brazil is slightly positive: 0.210 versus -0.190 for the statistically significant betas. However, Mexico and the U.S. have no statistically significant δ-coefficients. Thus, the impact of oil price on our sample oil-exporting countries is inconclusive (positive, negative or no significance), which matches the mixed findings by prior studies as highlighted earlier in the Introduction of this paper. We recognize that panel data has advantages over the use of cross-sectional or time series data. It also has more observations, which increases degrees of freedom, enhances estimation efficiency and minimizes multicollinearity issues (Wang 2012). Consequently, in further analysis, we estimate Eq. (1) by pooling the oil-exporting countries in Column 7. We include country fixed effects to account for unobserved country-heterogeneity.

Similar to the country-by-country results, the panel regression confirms that the direction of the oil return-stock link for oil-exporters is ambiguous: the relationship is negative at lags 1 (-0.032) and 4 (-0.082) while it is positive at lag 5 (0.031), yielding a total negative effect of -0.083.This conundrum leads us to apply next a long-run methodology to achieve a more precise perspective on the oil price-stock market link.

In the case of oil-importers in Panel B, we observe that stock returns are negatively associated with the prior one month’s stock return for Switzerland and prior four month’s stock return for South Africa; however, it is positively related with one- and four-month lagged stock returns for China. Examining the impact of oil price returns, we observe that four-month lagged oil price returns have negative and statistically significant effects on the aggregate stock market in Japan (-0.075) and Switzerland (-0.046). Additionally, we find negative and significant coefficient for oil price returns at lag 3 in China (-0.199) and South Africa (-0.061). Although the results for Germany and India are not statistically significant, the effect of oil price return is negative. Using a panel regression in Column 14 analogous to that of Column 7, the result is consistently negative for oil-importers at lags 3 (-0.036) and 4 (-0.051) which yield a total negative effect of -0.087. Overall, the evidence suggests an inverse relationship between oil price return and the stock market for oil-importing countries in line with Cunado and de Gracia (2014) and Am and Shanmugasundaram (2017). Higher oil prices increase the cost of production for oil-importers, which depresses aggregate stock prices.

Changes in Vix (Vix_d) have very strong negative effects in all twelve countries at lag 1 (and at between lags 4 to 6 for a few sample countries), except Russia, which implies that lagged volatility is quickly reflected in stock returns. Increases in put option volatility in S&P 500 are incorporated in equity markets within the month; the order of magnitude of the coefficient is highly economically significant ranging from -0.313 in India to -0.604 in Brazil, though it is lower for China (-0.148) and Germany (-0.222). Clearly, the evidence is overwhelming for a strong negative VIX effect. Additionally, we find evidence of a statistically significant and positive Ltgby effect for Russia and India, while in Japan the effect alternates from positive in lag 1 to negative in lag 2. On the other hand, monetary policy change is associated with a significant and negative impact on the stock markets of U.S. (lags 1 and 4), Canada (lag 1) and Mexico (lag 3), Germany (lag 4), Switzerland (lag 5), and China (lag 2), but it has no effects in Norway and South Africa. In sum, the results suggest that the effect of Ltgby_d on stocks seems to be market-dependent and not very consistent across countries—at least from the short-run perspective. For both panel sets of countries in Columns 7 and 14, Vix_d has an economically large negative effects (-0.507 in column 7 and -0.337 in column 14) within the first month. The impact of monetary policy, Ltgby_d, is relatively smaller. It is negative for oil-exporters (-0.014) at the first lag while it is not statistically significant (-0.010) for oil-importers. In further panel regressions in the internet Appendix Table A3, apart from country fixed effects, we also include year fixed effects to control for unobserved variables that change over the period but are constant across countries. We find that the broad conclusions of our inferences are unchanged.

Choi and Hammoudeh (2010), and Filis et al. (2011), among others, contend that geopolitical developments drive the relationship between oil prices and stock market. Therefore, we also estimate the modified Narayan (2019) model by controlling for geopolitical risk changes (Gpr_d) while we drop oil price returns due to the positive correlation between geopolitical risks and oil prices (0.132), statistically significant at 1% level in Table 2. We report these results in the internet Appendix Table A3. Interestingly, both Vix_d and Gpr_d have negative coefficients as expected. VIX volatility effect is more quickly incorporated into the stock market, while the effect for global uncertainty, Gpr_d, is significant usually with a delay of two months or more.

Our findings are qualitatively similar when we control for contemporaneous effects of the right-hand side variables in all our estimations. Overall, we find clear evidence that changes in volatility (Vix_d and Gpr_d) or monetary policy (Ltgby_d) are statistically significant in stock returns. More importantly, Vix_d has a strong and more robust forecasting ability for stock returns due to the immediate effect and the size of its coefficient in eleven stock markets. While the evidence strongly supports a negative relationship between stock market returns and oil price returns in oil-importing countries, the more puzzling behavior seems to be the sensitivity of the δ-coefficients of oil price returns for oil-exporters. It could be that the overall stock markets are too diverse (in the sense of mixing many sectors) to respond clearly to increases in oil prices. An alternative explanation may also be that the relationship between the stock market and oil price reflects a long-run phenomenon. In this paper, our goal is to examine this possibility through estimating the long-run-oriented DOLS model specified in Eq. (2) with a long sample period, although we acknowledge that several other explanations are possible.

4.2 Long-run relationship

Using the flexible lag length, we consider Eq. (2) to examine the long-run impacts of oil prices and other variables on the aggregate stock market. Following Campbell and Perron’s (1991) procedure, we start with 3 leads and 3 lags of the first differences of the regressors and eventually and systematically settle on an optimal lead/lag for each country.Footnote 5 Interpretation of the results of the DOLS is based on β1, β2 and β3 in Eq. (2) and ignores the coefficient estimates of the first differences which are only added to address issues of possible endogeneity and serial correlation (Stock and Watson 1993; Lettau and Ludvigson 2001).

In Panel A of Table 4, we first report the results for oil-exporting countries which reveal that oil price has long-run positive effect on stock index price for all six countries. Specifically, a 1% rise in oil prices is associated with increases in the stock index price by percentage points ranging from 0.08% per month in the U.S. to 0.74% per month in Brazil. This result is supported in Column 7 where we pool all the oil-exporters. The panel regression, with country fixed effects, shows that a 1% increase in oil prices raises stock market index by 0.29% per month for the group of oil-exporters in the long-run. The clear-cut positive relationship stands in contrast to the inconclusive results obtained in Panel A of Table 3 for the short-run approach. Next, we consider oil-importers in Panel B. We observe that oil price has a negative long-run impact in all the six oil-importing countries; however, the relationship is only significant for Japan, Switzerland, and India, where we report that a 1% increase in oil prices is associated with between 0.15% to 1.95% decrease in stock index prices. In the panel regression in Column 14, we also note that the effect is negative and significant. Specifically, a 1% increase in oil prices is associated with a 0.45% fall in the stock market index in the long-run for oil-importers. Taken together, the long-run evidence reinforces the short-run results in Table 3 that there is a negative link between oil prices and aggregate stock markets for oil-importing countries. Overall, while the relationship for oil-exporters was less clear with the short-run Narayan (2019) model, the long-run DOLS yields a positive impact of oil price on stock indices for these markets, as well as negative effects in oil-importing stock markets. This strongly suggests the need for long-run-oriented econometric techniques to complement short-run methods in this area of research.

The findings are hitherto consistent with the argument that oil price increases generally boost the economies of oil-exporting countries which may benefit from increased oil revenues while oil-importing countries are more disadvantaged due to rising costs of energy. Bjornland (2009) suggests that oil price increases will increase an oil-exporting country’s income which will lead to greater expenditure and investments. This would then trigger a rise in productivity and a decline in unemployment. The consequent effect is a positive impact on the stock market. In contrast, for an oil-importing economy, increases in oil price will translate into higher costs of production since oil is a critical factor of production (Arouri and Nguyen 2010). These higher costs may reflect in higher consumer prices and a resultant depression of demand (Abel et al. 2014), leading to downward pressure on stock markets (Sadorsky 1999).

In Table 4, we also observe that the effect of Vix is ambiguous for oil-exporters while it is negative and statistically significant for all the six oil-importers. In panel regressions, the Vix-coefficient is positive (0.083), but negative (-0.403) for oil-importers. Thus, the mixed effects of Vix in the long-run contrasts with its pervasive negative impact using the Narayan (2019) model. On the other hand, the impact of Ltgby on stock index price is negative and immediate for all oil-exporters and the corresponding panel regression in Panel A. Ltgby is also negative in five out of six oil-importers in Panel B, although the effect is significant in only Germany, China and Switzerland. The result for South Africa suggests, however, a positive (0.182) and statistically significant effect of monetary policy. Nevertheless, the panel regression in Column 14 indicates a negative and statistically significant coefficient (-0.563) on how aggregate stock markets react to rising bond yields. This leads to an opposite conclusion to what is found for Vix: the result for Ltgby is negative and stronger with the long-run methodology, unlike our observation of ambiguous findings for bond yields with the short-run model in Table 3. The result for Ltgby is economically appealing since interest rates discount future cash flows according to the negative stock-interest relationship in the long-run, despite variations in the short-run.Footnote 6

In unreported results and for robustness purposes, we also employ a Dynamic Common Correlated Effects (DCCE) model developed by Pesaran (2006) to account for possible cross-sectional dependencies between our sample countries. We find that these estimations yield qualitatively similar results. The results are also robust to inclusion of a dummy in the regression analyses or the DCCE model to control for the financial crisis period, which is December 2007 to June 2009 according to the National Bureau of Economic Research (NBER) definition. In order to avoid any confounding effects of the recent outbreak of the COVID-19 pandemic in March 2020, we re-examine all our estimations from January 1990 to January 2020 (instead of July 2020) and note that our inferences remain unaffected.

4.3 Controlling for structural breaks in the stock-oil price relationship

We take into account time-varying relationship between oil and stock prices highlighted by previous studies (Filis et al. 2011; Sadorsky 2012). This is particularly imperative given the long-span of our data over three decades. Thus, we first test for Bai and Perron (2003) structural breaks based on our two panel sets of oil-exporting and oil-importing countries; we do not use individual sample time series due to the limited number of observations for each country which is exacerbated by missing data for some countries. The test initially yields multiple breaks at April 2004 and October 2008 for the oil-exporting panel set. Further tests on each of these dates show that the null of no structural break at April 2004 is accepted at 5% while the null is rejected for October 2008. Datta et al. (2021), who examine the correlations between stock and oil returns, also find a breakpoint of September 2008. In the case of oil-importers, the structural break indicates five multiple breaks with two confirmed by further tests: April 1998 and September 2002. We re-estimate Eqs. (1) and (2) for our two panel subsets and sub-periods based on these structural break dates. Table 5 provides the results with DOLS regressions. For oil-exporters, the coefficient of oil price is 0.068 for the pre-break which is significantly higher than 0.045 for post-October 2008 according to a chi-square test of equality of coefficients. Considering oil-importers, we do not find statistically significant results across all the sub-periods, although the relationship between oil price and stock price is negative for two of the three sub-periods.Footnote 7

In sum, applying Bai and Perron (2003) structural break tests we find evidence of a time-varying association between oil and stock prices. These results offer some support for our earlier results. When pooling the data, the stock-oil relationship becomes clearly positive for oil-exporters compared to a seemingly negative relationship using the short-run approach.

5 Concluding remarks

Despite the widely researched links between stock market and oil prices, we are not aware of studies that address both long-run and short-run perspectives together as we do in this paper. We examine how WTI oil prices impact aggregate stock markets with a long sample period spanning over three decades from 1990 to 2020, while accounting for long bond yields and uncertainty measures. We propose an interpretation combining dynamic specifications in the short-run with stable long-run relationships. The short run evidence suggests negative effects of oil on stocks (with lags, in delayed response) for both oil-exporters and importers. However, applying DOLS, the relationship is reversed in the long-run for oil-exporters. For three decades, the DOLS estimators yield stock prices moving up with oil prices for oil-exporting countries, consistent with expectations and prior studies. Moreover, volatility measures (equity VIX and geopolitical risks, GPR) have negative and immediate effects in the short-run and mixed effects in the long-run. A possible explanation is the argument by Brandt and Gao (2019, p. 65) that geopolitical news such as terrorism or natural disasters usually occur abruptly and are typically short in duration, giving rise to a short impact duration because “prices may be driven by the next influential news a few days later”. Furthermore, we find negative coefficients of long bond yields in the long-run, consistent with higher interest rates discounting expected cash flows and making stock prices fall; but the direction of the effects is more heterogeneous in the short-run.

We attribute the change in these magnitudes and directions of coefficients to the empirical methodology to identify long versus short run effects of oil on stock markets. Our conclusions remain even after accounting for time-varying relationships over the sample period. The results of this study have vital implications for investors. Identifying the short- and long-run effects of oil price, monetary policy and financial as well as geopolitical uncertainties are important for the choice of investment horizons. Our findings may also be of relevance to decision-makers as they consider the short and long-run effects of monetary policies on stock markets. While the response is mixed in the short-run for both oil-exporters and oil-importers, the long-run coefficient of interest rates is estimated to be negative. Further investigation into the causes of changes in the direction of the short-run relationship between long-term government bond yields and the stock market represents an interesting avenue of research.

Notes

Brazil in the second half of the 2000s had several new oil field discoveries as discussed by Rodrigues and Sauer (2015) on the economic gains of pre-salt oil fields.

We use a maximum of 6 lags and check the statistical significance of the last lag at 5%. If the last lag is not statistically significant, we reduce it by one and reassess, until the specification finally reported in the table.

Since we use the transformed versions of these variables in Eq. (2), we also present the corresponding cointegration results in Internet Appendix Table A2 to show that the results are qualitatively similar. We also substitute VIX with GPR and obtain similar Johansen cointegration test results, which are available upon request.

Estimates based on fixed lag selection for all our regressions are available upon request.

We report estimations that use k = 3: 3 leads and 3 lags. We also try with various lead/lag length in implementing the DOLS regression in Eq. (2) and our main conclusions remain unchanged.

In the internet Appendix Table A5, when we include both country and year fixed effects, all our inferences for the long-run model remain unaffected with the exception that the coefficient of oil is still negative for oil-importers but becomes statistically insignificant (coefficient = -1.193; t-statistic = -0.84).

Pooled estimations in the supplemental appendix of Narayan (2019) in Table A6 with structural breaks show that the short-run response of the stock market appears mostly negative for oil-exporters (at longer lags) in the 2 subsamples, a counterintuitive result, and mostly negative (at various lags) for oil-importers in the 3 subsamples.

References

Abel AB, Bernanke BS, Croushore D (2014) Macroeconomics, 9th edn. Pearson, New York, USA

Alamgir F, Bin Amin S (2021) The nexus between oil price and stock market: Evidence from South Asia. Energy Rep 7:693–703

Am MA, Shanmugasundaram G (2017) Nexus between crude oil price, exchange rate and stock market: Evidence from oil exporting and importing economies. Int J Humanit Manag Sci 5(1):41–43

Arampatzidis I, Dergiades T, Kaufmann RK, Panagiotidis T (2021) Oil and the U.S. stock market: Implications for low carbon policies. Energy Econ 103:105588

Arouri MEH, Nguyen DK (2010) Oil prices, stock markets and portfolio investment: evidence from sector analysis in Europe over the last decade. Energy Policy 38:4528–4539

Arouri MEH, Rault C (2012) Oil prices and stock markets in GCC countries: empirical evidence from panel analysis. Int J Financ Econ 17(3):242–253

Assefa TA, Esqueda O, Mollick AV (2017) Stock returns and interest rates around the world: A panel data Approach. J Econ Bus 89:20–35

Aysana AF, Demir E, Gozgor G, Lau CKM (2019) Effects of the geopolitical risks on Bitcoin returns and volatility. Res Int Bus Financ 47:511–518

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Economet 18(1):1–22

Bjornland CH (2009) Oil price shocks and stock market booms in an oil exporting country. Scottish J Polit Econ 2(5):232–254

Bouri E (2015) Oil volatility shocks and the stock markets of oil-importing MENA economies: a tale from the financial crisis. Energy Econ 51:590–598

Brandt MW, Gao L (2019) Macro fundamentals or geopolitical events? A textual analysis of news events for crude oil. J Empir Financ 51:64–94

Caldara D, Iacoviello M (2022) Measuring geopolitical risk. Am Econ Rev 112(4):1194–1225

Campbell JY, Perron P (1991) Pitfalls and opportunities: what macroeconomists should know about unit roots. NBER Macroeconomics Annual. MIT Press, Cambridge

Choi K, Hammoudeh S (2010) Volatility behavior of oil, industrial commodity and stock markets in a regime-switching environment. Energy Policy 38(8):4388–4399

Cong RG, Wei YM, Jiao JL, Fan Y (2008) Relationships between oil price shocks and stock market: An empirical analysis from China. Energy Policy 36:3544–3553

Cunado J, de Gracia FP (2014) Oil price shocks and stock market returns: Evidence for some European countries. Energy Econ 42:365–377

Datta D, Johannsen BK, Kwon H, Vigfusson RJ (2021) Oil, equities, and the zero lower bound. Am Econ J Macroecon 13(2):214–253

Filis G, Degiannakis S, Floros C (2011) Dynamic correlation between stock market and oil prices: The case of oil-importing and oil-exporting countries. Int Rev Financ Anal 20(3):152–164

Gkillas K, Gupta R, Pierdzioch C (2020) Forecasting realized gold volatility: Is there a role of geopolitical risks? Financ Res Lett 35:101280

Gupta K (2016) Oil price shocks, competition, and oil and gas stock returns-global evidence. Energy Econ 57:140–153

Kang W, Ratti RA (2013) Oil shocks, policy uncertainty and stock market return. J Int Finan Markets Inst Money 26:305–318

Kilian L (2009) Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. Am Econ Rev 99(3):1053–1069

Kilian L, Park C (2009) The impact of oil price shocks on the U.S. stock market. Int Econ Rev 50(4):1267–1287

Lee C, Zeng J (2011) The impact of oil price shocks on stock market activities: asymmetric effect with quantile regression. Math Comput Simul 81:1910–1920

Lettau M, Ludvigson S (2001) Consumption, aggregate wealth, and expected stock returns. J Financ 56(3):815–849

Lothian JR (1990) A century plus of Japanese exchange rate behaviour. Jpn World Econ 2:47–70

Mollick AV, Assefa T (2013) U.S. stock returns and oil prices: The tale from daily data and the 2008–2009 financial crisis. Energy Econ 36:1–18

Moya–Martínez P, Ferrer–Lapeña R, Escribano–Sotos F (2014) Oil price risk in the Spanish stock market: An industry perspective. Econ Model 37:280–290

Narayan PK (2019) Can stale oil price news predict stock returns? Energy Econ 83:430–444

Narayan PK, Gupta R (2015) Has oil price predicted stock returns for over a century? Energy Econ 48:18–23

Narayan PK, Sharma S (2011) New evidence on oil price and firm returns. J Bank Finance 35:3253–3262

Papapetrou E (2001) Oil price shocks, stock market, economic activity and employment in Greece. Energy Econ 23(5):511–532

Park J, Ratti RA (2008) Oil price shocks and stock markets in the U.S. and 13 European countries. Energy Econ 30(50):2587–2608

Pesaran MH (2006) Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica 74:967–1012

Prabheesh KP, Padhan R, Garg B (2020) COVID-19 and the Oil Price – Stock Market Nexus: Evidence from net oil-importing countries. Energy Res Lett 1(2):1–4

Rodrigues LA, Sauer IL (2015) Exploratory assessment of economic gains of a pre-salt oil field in Brazil. Energy Policy 87:486–495

Sadorsky P (1999) Oil price shocks and stock market activity. Energy Econ 21:449–469

Sadorsky P (2012) Correlations and volatility spillovers between oil prices and the stock prices of clean energy and technology companies. Energy Econ 34(1):248–255

Sahu TN, Bandopadhyay K, Mondal D (2014) An empirical study on the dynamic relationship between oil prices and Indian stock market. Manag Financ 40(2):200–215

Sharma A, Giri S, Vardhan H, Surange S, Shetty R, Shetty V (2018) Relationship between crude oil prices and stock market: Evidence from India. Int J Energy Econ Policy 8(4):331–337

Stock JH (1987) Asymptotic properties of least squares estimators of cointegrating vectors. Econometrica 55:113–144

Stock JH, Watson M (1993) A simple estimator of cointegrating vectors in higher order integrated systems. Econometrica 61(4):783–820

Wang KM (2012) Modelling the nonlinear relationship between CO2 emissions from oil and economic growth. Econ Model 29(5):1537–1547

Westerlund J, Sharma SS (2019) Panel evidence on the ability of oil returns in the G7 area. Energy Econ 77:3–12

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflicts of interest/Competing interests

The authors declare that they have no conflict of interest. Also, this study did not receive grant funding of any kind.

Additional information

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

This manuscript has not been published elsewhere and has not been submitted simultaneously for publication elsewhere.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Osah, T.T., Mollick, A.V. Stock and oil price returns in international markets: Identifying short and long-run effects. J Econ Finan 47, 116–141 (2023). https://doi.org/10.1007/s12197-022-09602-x

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12197-022-09602-x