Abstract

I compare two approaches from the recent literature on how to account for tax planning and its uncertainty in a valuation framework [the separate view of Drake et al. (J Account Audit Financ 34(1):151–176, 2019) vs. the composite view of Jacob and Schütt (Eur Account Rev 29(3):409–435, 2020)], emphasizing measurement issues of tax planning and firm heterogeneity. Replication analyses and extensive robustness tests suggest that only considering tax planning and it’s uncertainty jointly and connecting them to firm value via income leads to consistent results, implying that higher uncertainty-adjusted tax planning amplifies the positive association between pre-tax income and firm value. However, the economic magnitude of this association depends on the measurement approach, ranging between 0.8 and 12.91%. Conversely, the separate view produces inconsistent results in all tests. These conclusions are not affected by incorporating recent losses (Dyreng et al. in Tax avoidance or recent losses? Working Paper, 2021) when an appropriate tax planning measure is chosen. While the results become insignificant when effective tax rates are used, applying the measure of Henry and Sansing (Rev Account Stud 23:1042–1070, 2018) mitigates this problem. Moreover, the positive value implication of uncertainty-adjusted tax planning is particularly pronounced for firms with low leverage whose debt tax shield and debt overhang are relatively small. The logic of jointly measuring tax planning and its uncertainty seems to be extendable to a variety of measures and to provide a more suitable measure than traditional isolated effective tax rates in a valuation framework.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

This paper analyses the link between corporate tax planning (TP), tax uncertainty (TU), and firm value (FV) for the case of listed German firms by (i) comparing two recent approaches to account for TU in a valuation framework (Drake et al. 2019; Jacob and Schütt 2020), (ii) assessing the dependence of results on the measurement of TP, especially in the presence of losses (Henry and Sansing 2018; Dyreng et al. 2021), and (iii) examining firm heterogeneity in the responsiveness of firm valuation to TP. From a traditional net present value perspective, TP leads to lower tax burdens and higher after-tax cash flows for firms, increasing their value. However, negative effects such as reputational costs (Gallemore et al. 2014) or higher tax-induced uncertainty (Guenther et al. 2019) can mitigate these positive effects. Recently, two approaches to incorporate TU in a valuation framework have been developed: the separate view by Drake et al. (2019) which treats TP and TU as distinct constructs and connects them directly to FV, and the composite view by Jacob and Schütt (2020) which combines TP and TU into one measure and links them indirectly to FV through pre-tax income. Drake et al. (2019) find that TP (TU) is positively (negatively) associated with FV, while TU dampens the positive relationship between TP and FV. Jacob and Schütt (2020) provide evidence that the positive association between pre-tax income and FV is enhanced by higher values of uncertainty-weighted TP (measured by the Tax Planning Score, TPS), and provide a rationale for why the separate view might suffer from model misspecification: TP and TU should be considered together, because investors need to build expectations for the future based on past information. In doing so, they care about the information content (i.e., the uncertainty) of the effective tax burden, not just its amount.

Despite the notion of Jacob and Schütt (2020) about potential misspecification of the separate view, Drake et al. (2019) have received more attention by subsequent studies: They are cited significantly more often than Jacob and Schütt (2020),Footnote 1 and the insight that TP and TU should be considered together is not yet widespread in the literature—despite the fact that the earliest version of Jacob and Schütt (2020) is published as a working paper since 2013 (Jacob and Schütt 2013). In addition, the TP literature on valuation since 2020 only considers TP and TU separately (e.g., Irawan and Turwanto 2020; Firmansyah and Widodo 2021; Firmansyah et al. 2022; Seifzadeh 2022), while the role of TU is often completely neglected (e.g., Chukwudi et al. 2020; Khuong et al. 2020; Rudyanto and Pirzada 2021; Arora and Gill 2022; Inger and Stekelberg 2022). Similarly, recent studies examining the association between TP, TU, and various economic outcomes do not include the TPS as a measure (Dhawan et al. 2020; He et al. 2020; Osswald 2020; Dos Santos and Rezende 2020; Abernathy et al. 2021; Gkikopoulos et al. 2021; Adams et al. 2022; Purwaka et al. 2022).Footnote 2 One reason for not using the Jacob and Schütt (2020) model and measure could be that the composite view does not come without caveats. A disadvantage of measuring TP and TU together is that it is difficult to interpret composite values in an intuitive or plausible way. Likewise, the relative importance of TP and TU in valuation might be diluted if they are combined. After all, the model in Jacob and Schütt (2020) is based on debatable theoretical assumptions (e.g., simplifying abstractions in the residual income model and the way investors form expectations) and could also be more subject to measurement error than Drake et al. (2019) due to combining TP and TU in a very specific specification. Therefore, the separate view might still more accurately capture the differential impact of TP and TU on FV and might be easier to interpret.

Hence, a comparison of both approaches in terms of their robustness and suitability in a valuation framework seems useful, since a comprehensive investigation of both views has not yet been conducted. In addition, this paper extends the analysis by examining (i) the dependence of results on the choice how to measure TP and (ii) the heterogeneity of firms in their responses. The accounting literature to date has relied on various TP measures (e.g., GAAP or cash ETRs, book tax differences) and empirical specifications (e.g, control variables), so it is not clear how the results depend on (at times arbitrary) measurement choices (De Simone et al. 2020). In particular, Henry and Sansing (2018) point out that TP studies may suffer from data truncation bias due to the exclusion of loss-making firms, which are often omitted because it is difficult to interpret traditional TP measures when losses are present. They develop a new TP measure (Delta MVA) that is interpretable in loss cases. However, similar to the TPS, this measure has not been widely applied in the recent literature. Related to this, Dyreng et al. (2021) demonstrate that low ETRs are likely to be misinterpreted as incremental TP, when in fact they are an accidental byproduct of recent losses. It could be that the expected—and in Jacob and Schütt (2020) documented—positive association between (uncertainty-adjusted) TP and FV changes when these aspects are taken into account.

Moreover, not much attention has been paid to the question for which type of firms the relationship between TP and FV is particularly pronounced. Since both views investigate equity valuation and Jacob and Schütt (2020) in particular rely on the residual income model, they naturally abstract from the impact of debt. However, there are at least two arguments why debt is meaningful for equity valuation. First, prior literature has shown that firms’ leverage can have a negative impact on their equity value due to increased danger of debt overhang and default risk (Myers 1977; Cai and Zhang 2011). Second, the value of the debt tax shield declines with lower effective tax rates (and thus higher TP) due to the deductibility of interest expense from the tax base (e.g., Kruschwitz and Löffler 2006). Therefore, the level of firms’ debt holdings is likely to moderate investors’ equity valuation of TP. In addition, the role of available resources of firms is also investigated, as prior literature has shown that costs of TP can influence the intensity of its impact on economic outcomes (e.g., Eichfelder and Vaillancourt 2014; Hundsdoerfer and Jacob 2019).

The results from the replication and comparison of both views indicate that only the composite view with the TPS leads to robust and consistent results. Nonetheless, the economic magnitude of the positive association between uncertainty-weighted TP and FV depends on the used TP measure and time horizon: on average, a one unit increase in the TPS leads to a 0.8–12.91% increase in the positive association between pre-tax income and the market-to-book ratio. Conversely, the separate view yields inconsistent results, most of which are not statistically significant and vary widely across different measures and control settings.

Regarding the role of losses in measuring TP, the results of the composite view are robust to (i) applying the measure of Henry and Sansing (2018) to the TPS logic in a loss sample, and (ii) the Dyreng et al. (2021) approach to control for incidental TP when an appropriate measure is used. While the results with ETRs become insignificant similar to Dyreng et al. (2021), using the Henry and Sansing (2018) measure leaves the baseline results of the composite view unaffected.

Lastly, I find robust evidence that the positive relationship between the TPS, pre-tax income, and FV is especially pronounced in low leveraged firms, confirming the intuition that TP (apart from debt financing) is more beneficial when the debt tax shield and issue of debt overhang are relatively small. There is also some evidence that firms with less resources receive stronger positive value implications of uncertainty-weighted TP, which could be explained by benefits from TP being valued relatively stronger in firms for which (cash) benefits from TP are larger. These results, however, are not robust in all specifications.

This paper contributes to the literature in several ways. First, by replicating the separate and composite view for the case of listed German firms, the role of TP and TU in valuation is assessed in a new capital market environment. At the same time, the comparison of both views can guide future studies on which approach should be used—especially since the composite view has not received much attention yet. Second, the analyses contribute to the literature on the importance of methodological choices in empirical TP studies (De Simone et al. 2020) by showing how estimates vary with different TP measures that are frequently applied. Arbitrarily selecting only one or a few of them when reporting results might bear the risk of over- or understating the economic magnitude of associations. Third, the analyses also contribute to the discussion how losses affect TP measures and outcomes (Henry and Sansing 2018), and to the question recently raised in Dyreng et al. (2021) whether previous firm losses lead to misinterpretation of TP measures. While this also appears to be an issue in a valuation framework, the results depend on the measure used. In particular, the measure of Henry and Sansing (2018) seems to be well suited to account for recent losses in a valuation framework. Lastly, this paper also contributes to the literature documenting heterogeneous responses of corporate economic outcomes to taxes and TP (e.g., Büttner et al. 2011; Zwick and Mahon 2017; Jacob et al. 2022).

The remainder of the paper is structured as follows. Section 2 briefly discusses and summarizes related literature. Section 3 recapitulates the intuition and theoretical background of the separate and composite view. The empirical approach and data are described in Sect. 4, while the results are presented in Sect. 5. Finally, Sect. 6 concludes.

2 Related literature

The literature on the relationship between TP and FV generally consists of several strands that either directly address the issue or have indirect implications for valuation.Footnote 3 Taxes can affect FV through at least three channels: (i) taxes directly affect firms’ after-tax cash flows and earnings; (ii) taxes affect the after-tax cost of capital (Sikes and Verrecchia 2020); and (iii) taxes determine the degree of risk sharing with the government (Desai and Dharmapala 2009). TP activities affect the first channel positively, as lower tax payments lead to higher after-tax cash flows and profits. However, TP can also increase the uncertainty of future after-tax outcomes, i.e., they become more volatile. If investors prefer a smooth development of earnings (Neuman 2014), their required return would increase. Thus, closely related to the objectives of this paper are studies on the association between TP and the cost of equity (CoE). A similar reasoning applies to the third channel: the lower the effective tax burden, the higher the share of risk borne by the firm rather than by the government. How investors ultimately value TP depends on which effect dominates. The literature directly addressing this issue is relatively sparse (Hanlon and Heitzman 2010). Studies published after the contributions this paper focuses on (Drake et al. 2019 and Jacob and Schütt 2020) primarily investigate TP and FV in emerging markets (e.g., Irawan and Turwanto 2020; Firmansyah and Widodo 2021; Firmansyah et al. 2022; Seifzadeh 2022). In the following, the strands are summarized, starting with the link between TP and the CoE.

Tax planning and the cost of equity A considerable part of the empirical literature argues that corporate TP induces non-diversifiable risk that leads to higher CoE. Most of these studies assume that the risk associated with TP arises from uncertainty about future tax policy (Brown et al. 2014) and affects economic risk through investment returns (Guenther et al. 2017). Brown et al. (2014) show that investors perceive TP benefits as risky during periods of high uncertainty in the tax policy environment. This, in turn, increases the investors’ risk assessment of investments. Heitzman and Ogneva (2019) use US data and distinguish between periods under Republican and Democratic administrations. Their findings of a positive association between TP and stock returns are almost entirely explained by the “tax-friendly” Republican terms. Sikes and Verrecchia (2020) show that aggregate TP at the industry level is associated with higher CoE, as the uncertainty of a firm’s future cash flows increases with the uncertainty of TP activities in the firm’s industry. These results suggest negative value implications of TP as investors demand a higher future return on investment, which depresses current value.

Conversely, studies examining the direct relationship between firm-level TP and CoE (e.g., Hutchens and Rego 2013; Goh et al. 2016) suggest that TP can also have a positive effect on CoE, implying that they decrease the higher a firm’s TP level is. However, Hutchens and Rego (2013) argue that this depends on the type of TP and show that the uncertainty caused by some TP strategies can instead lead to higher CoE. The results in Hanlon and Slemrod (2009) have already supported this by showing a negative correlation between stock prices and the aggressiveness of TP. Overall, the literature on the association between TP and CoE provides mixed results and relies on models that only focus on TP or uncertainty separately.

Tax planning, risk and firm value Desai and Dharmapala (2009) place emphasis on agency theory, which recognizes the difference between ownership and control of firms, and find that the association between TP and FV depends strongly on the quality of corporate governance. Also in Kim et al. (2011), a positive association between TP and the risk of an abnormally large decline in stock prices is attributed to the agency principle. These earlier studies (as well as most of those on CoE) have not considered the uncertainty of TP as a unique concept. Vello and Martinez (2012) find that more efficient TP strategies significantly reduce market risk, depending on good corporate governance. In contrast, Assidi (2015) conducts a case study for 40 listed French companies and finds a positive relationship between ETRs, or their volatility, and firm risk. Hutchens and Rego (2015) relate various measures of tax risk to firm risk and find that only the volatility of cash ETRs and book-tax differences are significantly associated with firm risk. Other measures show either a negative association or none at all. Brooks et al. (2016) examine the relationship between tax payments and financial performance in the United Kingdom, finding that firms’ ETRs do not affect stock returns but are negatively associated with market risk. Nesbitt et al. (2017) show for a sample of firms affected by the Luxembourg Leaks that investors responded positively to the exposure, which could be explained by a reduction in uncertainty. Finally, Guenther et al. (2017) conceptually distinguish between TU, TP and tax aggressiveness and document a positive association between TU and firm risk. However, they do not find a direct association between TP itself and firm risk.

Considering that TU might affect value-relevant outcomes, two recent studies offer approaches to empirically account for both TP and TU. Drake et al. (2019) treat the degree of TP and its uncertainty as distinct constructs, while Jacob and Schütt (2020) combine them into a composite measure (Tax Planning Score, TPS). Unlike previous studies, Jacob and Schütt (2020) do not attempt to examine a direct relationship between TP, TU, and FV, but suggest that their relation is determined by pre-tax income channels, while Drake et al. (2019) interact measures of TP (ETRs) with measures of TU (volatility of ETRs) and link them directly to FV. The value of the firm decreases with TU and increases with the degree of TP, while this positive association is attenuated by TU. In Jacob and Schütt (2020), firms with higher TPS values, which increases with the degree of TP and decreases with TU, experience a stronger positive relationship between pre-tax income and FV.Footnote 4

Jacob and Schütt (2020) provide empirical tests to assess whether past ETRs (ETR volatilities) are appropriate predictors of future ETRs (ETR volatilities) and emphasize the need to weight available tax information according to its information content for investors. However, studies published after these two papers do not seem to have acknowledged Jacob and Schütt (2020)’s valuation model—in particular, the notion that TP and TU should be considered together. Irawan and Turwanto (2020); Firmansyah and Widodo (2021) and Firmansyah et al. (2022) apply Drake et al. (2019)’s approach to Indonesian firms and find mixed results: Irawan and Turwanto (2020) find that both TP and TU are positively associated with FV, while TU moderates this relationship. Firmansyah and Widodo (2021) do not interact both concepts, finding that TP (TU) is positively (negatively) associated with FV. When TP and TU are interacted in Firmansyah et al. (2022), the results are similar to Drake et al. (2019). In addition, Khuong et al. (2020) examine TP and firm performance in Vietnam and find mixed results, and Seifzadeh (2022) focus on the role of managerial ability in the relation between TP and FV in Iran, finding a negative association between TP and FV that is less strong in firms with high ability managers. In these two studies, TU as a concept is completely neglected. The same is true for Chukwudi et al. (2020), who examine public firms in Nigeria, Rudyanto and Pirzada (2021) claiming that sustainability reporting could moderate the link between TP and FV, Arora and Gill (2022) showing that TP is negatively associated with FV, and Inger and Stekelberg (2022), who provide evidence that only socially responsible TP is positively valued by investors. In all of these studies, Jacob and Schütt (2020) is not cited (except for Irawan and Turwanto 2020), while Drake et al. (2019) is, and the composite approach is therefore not acknowledged.

To sum up, although the earliest version of Jacob and Schütt (2020) is in circulation since 2013 (Jacob and Schütt 2013), their valuation model is not widely used in the literature. The same is true for the joint measure TPS, which is not included in studies on the relation between TP and FV, or the connection of TP/TU to other economic outcomes (Dhawan et al. 2020; He et al. 2020; Osswald 2020; Dos Santos and Rezende 2020; Abernathy et al. 2021; Gkikopoulos et al. 2021; Adams et al. 2022; Purwaka et al. 2022). To the best of my knowledge, the study by Brooks et al. (2016) is the only one that explicitly refers to the TPS as a measure, but does not conduct analyses with it. Thus, in the following, different empirical specifications and TP measures are applied to the separate and composite views to evaluate the notion of Jacob and Schütt (2020) that TP and TU should be considered jointly, before turning to potential extensions.

3 Theoretical background and intuition

3.1 Separate view

Drake et al. (2019) derive their hypotheses from prior empirical work, where TP is allegedly associated with higher FV on average. However, as described above, the literature does not find this positive relationship for all forms of TP. The separate view relies on the CAPM logic that non-diversifiable risk leads to higher risk premia and on the model extension of Sikes and Verrecchia (2020) from Lambert et al. (2007). In this framework, the uncertainty of firms’ after-tax cash flows increases with the uncertainty of the TP strategies of the entire market or industry in which the firms operate. Drake et al. (2019) conclude that higher TU should lead to lower FV and lower positive value implications of TP.

This logic is subject to some caveats. First, the Sikes and Verrecchia (2020) model develops a framework in which aggregate TP of industries is the main variable of interest, not individual firm-level tax outcomes. Second, while there is a clear trade-off between risk and return in the CAPM model, the relationship between the degree of TP and it’s uncertainty is not as clear. The results in Guenther et al. (2017; 2019) suggest that lower ETRs are actually more persistent on average than high rates, implying that high TP can be achieved by relatively riskless strategies that do not induce much uncertainty. Lastly, separating TP and TU theoretically implies that investors perceive both concepts as value-relevant independently of each other.

While Drake et al. (2019) do not develop a clear theoretical argument as to why the separate consideration of TP and TU is appropriate, the intuitions in favor and against this can be reduced to the following. TP can be broadly defined as a spectrum of activities that reduce tax liability (Hanlon and Heitzman 2010). This can include high-risk and even gray-area strategies, as well as actions that are persistent and do not carry the risk of penalties, tax policy uncertainty, and reputational costs. On the one hand, separating TP and TU may not recognize this heterogeneity of strategies. On the other hand, it is also possible that TP and TU are related to FV independently. As Guenther et al. (2017) show, aside from the persistence of ETRs, tax risk is positively associated with firm risk, while the level of TP is not. This indicates that it may be important to separate the two concepts to determine which one is more important, or whether only one of the two affects FV—similar to firm risk.

3.2 Composite view

The composite view is based on the residual income model (Feltham and Ohlson 1995) and provides a rationale for the need to consider TP and TU together. According to the model of Jacob and Schütt (2020), the current market value of firm i at time t can be written as follows:

where M is the market value, B is the book value, RI is the residual income and r is the CoE. The after-tax residual income in t is: \(RI_{i,t} = \delta _{i,t} \cdot (I_{i,t}^{pretax} - r^{pretax} \cdot B_{i,t-1})\), where I is the after-tax income and \(\delta\) is a tax multiplier. Future \(\delta\) outcomes are assumed to fluctuate around their mean: \(\delta _{i,t+1}=\mu _{\delta }+\epsilon _{i,t+1}\). Eq. 1 can then be expressed as:

where D is a discount factor that takes into account the future evolution of income. The key parameter of interest, \(\mu _{\delta }\), is uncertain. Jacob and Schütt (2020) assume that investors rely on information about the past tax rate volatility to determine the expected value of future tax rates today. Average future tax rates are uncertain along two dimensions: both statutory tax rates, s, and firm ETRs, \(\tau\), are uncertain, while they are both assumed to be normally distributed. Dividing both sides of Eq. 2 by the book value, and writing out the tax term \({\mathbb {E}}_{i,t} \left[ \mu _{\delta }\right]\), gives:

which is the final valuation formula in Jacob and Schütt (2020). The factor right before \(D_{i,t}\) formally expresses the intuition that the more volatile tax rates are expected to be (\(\sigma _{s}\) and \(\sigma _{\tau }\)), the lower the information content (the higher the uncertainty). Thus, the tax parameter is an uncertainty-weighted tax rate, implying that investors rely on past information to form expectations. Jacob and Schütt (2020) develop the Tax Planning Score (TPS) to estimate the tax parameter, which relates the level of TP to the corresponding uncertainty (see Sect. 4). The main difference with Drake et al. (2019) with respect to TP can be found here, as TP and TU are not assumed to be independent. Moreover, the tax term interacts with pre-tax income (\(RI^{pretax}/B\)).

Taken together, the composite view differs from Drake et al. (2019) in two key ways: (i) the way TP and TU are linked to FV (indirectly through pre-tax income rather than directly), and (ii) the way TP and TU are measured (jointly rather than separately). Although the theoretical considerations of Jacob and Schütt (2020) imply that treating TP and TU separately is likely to be misspecified, a disadvantage of measuring TP and TU together is that it becomes impossible to evaluate their incremental effects. Weighting TP by its uncertainty may also result in composite values that are difficult to compare across firms or interpret in a plausible way. For example, a firm with an ETR of 10% and a volatility of 90% would have the same uncertainty-weighted TP value under the TPS logic as a firm with an ETR of 90% and a volatility of 10%. Therefore, considering them separately might still produce results that are easier to interpret and also more accurately explore the potentially different effects of TP and TU on FV.

3.3 Extensions

Losses and measurement

While especially Jacob and Schütt (2020) emphasize the need to measure TP carefully, neither approach explores the role of losses. Henry and Sansing (2018) have already shown that relying on samples with only positive income (as both studies do) can result in data truncation bias. In a recent working paper, Dyreng et al. (2021) argue and provide evidence that the results of TP studies may be inflated by measuring incidental TP due to prior loss years rather than incremental TP independent of loss carryforwards. They show that ETRs are systematically lower the more prior loss years there are. Without recognizing the role of losses, these small values would simply be interpreted as high TP. Even when measures are calculated over multiple years, as in Drake et al. (2019) and Jacob and Schütt (2020), they could still be affected by loss years that precede the relevant time window. The empirical approach of Dyreng et al. (2021) to investigate this issue is to control for recent losses in the regressions. Since most previous studies used ETRs, their analyses and replications focus only on these (e.g., for Hasan et al. 2014). While the separate view is likely similarly affected (at least when ETRs are used), it is not clear whether the TPS measure is also biased by recent losses, since TP is weighted by it’s volatility. To be affected similarly to isolated ETRs, TPS values would have to increase systematically with the number of recent loss years. Furthermore, Henry and Sansing (2018) have already developed a TP measure, Delta MVA (\(D\_MVA\)), that is explicitly designed to capture TP when losses are present. Thus, it may be that their measure is better suited to capture the role of recent losses. Further analyses after replicating the composite and separate views will therefore focus on these issues.

Firm heterogeneity

An aspect that is unrelated to measurement issues and has not yet been investigated in either approach is the question for which type of firms the proposed positive relationship between TP (adjusted for uncertainty) and FV is particularly pronounced. Naturally, since the residual income model expresses the market value of equity, the role of debt is not considered in the composite approach. Debt, however, can have an impact on the equity valuation of firms due to its influence on future investments (Myers 1977) and default risk. As Cai and Zhang (2011) show, changes in firms’ leverage ratios are negatively associated with stock prices, especially for highly leveraged firms. In addition, standard valuation models that are based on a discounted cash flow (DCF) logic suggest that there is a debt tax shield due to the deductibility of debt interest from the firm’s tax base, in the form (Kruschwitz and Löffler 2006):

where \(Tax_{t}^{u}\) and \(Tax_{t}^{l}\) represent the tax payments of an unleveraged and a leveraged firm, respectively, \(\tau\) is the ETR, and i is the (debt) interest rate. The association between TP and FV is likely to be less pronounced for highly leveraged firms, because (i) debt overhang (Myers 1977) and default risk (Cai and Zhang 2011) become more of an issue, and (ii) debt and TP can be viewed as substitutes to some extent: the higher the leverage (Debt), the higher the debt tax shield. Accordingly, more TP (a lower \(\tau\)) might become less valuable if there is a high debt tax shield: the larger \(\tau\), the greater the benefit of debt-induced deductions.

Moreover, previous studies have shown that the costs of tax compliance and TP activities are quasi-fixed (e.g., Eichfelder and Vaillancourt 2014; Hundsdoerfer and Jacob 2019). Firms that have more resources (e.g., large and high cash flow firms) may benefit more from TP than their counterparts, since their marginal costs of engaging in TP are lower. On the other hand, firms with less resources are more capital constrained, so they could gain larger relative cash flow benefits from TP than their peers. I refrain from making a clear prediction about which type of these firms responds more strongly and leave this question open for empirical investigation in the additional analyses.

4 Method and data

4.1 Measures of tax planning and tax uncertainty

The analyses follow the broad definition of TP by Hanlon and Heitzman (2010), where corporate TP comprises all activities that reduce the firm’s tax liability. This has the merit of including both high-risk and riskless planning strategies. The most common measures used by prior literature are effective tax rates (ETRs), which relate income tax expense or cash taxes paid to the tax base. While cash ETRs (CETRs) incorporate tax deferral strategies, GAAP ETRs (GETRs) exclude them by definition. Since this study relies on data for German corporations from Datastream (see Sect. 4.3), where cash taxes paid structurally have many missings, I use the GETR as the main measure for the baseline analyses. However, GETRs are more susceptible to be biased by earnings management, since both the numerator and denominator consist of balance sheet items. Therefore, in line with Drake et al. (2019) and Jacob and Schütt (2020), CETRs are also used.Footnote 5 To further assess robustness, I use book tax differences (BTD), their permanent component (PBTD), and the measure of Henry and Sansing (2018) (\(D\_MVA\)) which is designed to account for loss years and will therefore play a larger role in the additional analyses in Sect. 5.2.

Dyreng et al. (2008) suggest to calculate long-run measures over 10 years to reduce potential measurement errors due to year-to-year fluctuations. However, this procedure results in a significant loss of variation and observations. I therefore calculate the GETR (and all other measures) over a rolling 5 year window as follows:

Turning to TU, empirical proxies differ in their ability to capture different types of tax aggressiveness (Blouin 2014). While provisions for unrecognized tax benefits (UTB) are commonly used in US samples (e.g., Lisowsky et al. 2013; Ciconte et al. 2016), German accounting rules do not require firms to disclose these items. In the replication analyses, I rely on ETR volatilities as a measure of TU, since they capture the dispersion of potential tax outcomes. In a valuation framework, investors need to rely on past information that is available to them in a timely manner, while Guenther et al. (2017) provide evidence that the volatility of ETRs is an appropriate measure of tax risk. Consistent with the definition of TP in Eq. 5, TU is therefore calculated as the standard deviation of the GETR over a rolling 5 year window:

Finally, TP and TU are combined to calculate the Tax Planning Score (TPS), which relates the level of TP to the associated uncertainty:

The TPS increases with TP (numerator) and decreases with TU (denominator), recognizing that firms can achieve certain levels of GETRs with different corresponding risk. Jacob and Schütt (2020) note that they are agnostic about the basis of their composite measure. Their logic only postulates that some measure of TP should be in the numerator, while a measure of TU should be in the denominator according to Eq. 3. Therefore, I calculate all the measures described with the CETR, BTD, PBTD, and D_MVA as alternative proxies. Table 1 shows all tax variables, along with their description.

4.2 Empirical strategy

The first objective of this paper is to evaluate the separate and composite view in the same capital environment. For this exercise, I select the control variables as close as possible to the two original studies.Footnote 6 The two views are replicated by applying the following OLS regressions:

for the Drake et al. (2019) model. Equation 3 can be written as a reduced-form OLS regression equation of the composite view as:

where \(MTB_{i,t}\) is the market-to-book ratio of firm i in year t, TP is a measure of the degree of tax planning, TU measures tax uncertainty, TPS is the Tax Planning Score, CoE is the cost of equity (approximated by the stock return plus the risk-free interest rate), PI and VolPI are the pre-tax income (scaled by the book value of common equity in line with Jacob and Schütt 2020) and its volatility, SalesGrowth is the growth of sales over 5 years, X is a vector of additional controls (including cash flow volatility, stock price volatility, leverage, and depreciation expense), and \(\theta _i\) and \(\gamma _t\) are firm and year fixed effects, respectively.Footnote 7 In all analyses, the tax planning measures are standardized such that higher values of the variable TP always imply a higher degree of tax planning. All control variables are winsorized at the first and 99th percentiles.

According to the intuition behind the separate view, \(\alpha _1\) in Eq. 8 is expected to be positive, \(\alpha _2\) negative, and \(\alpha _3\) also negative. The coefficient of interest in Eq. 9, \(\beta _3\), is expected to be positive, since a higher TPS should amplify the positive association between pre-tax income and FV (\(\beta _1>0\)). To assess the robustness of both approaches, I apply different measures of TP and TU to Eqs. 8 and 9, as well as different control settings that are oriented on specifications from prior literature. The dispersion of coefficient estimates across specifications is compared to assess whether the results depend on the measurement of firm characteristics that are commonly controlled for and operationalized in different ways (e.g., firm size, debt, operational risk).Footnote 8

In the final step, I extend the results of Drake et al. (2019) and Jacob and Schütt (2020) by examining (i) the role of recent losses on TP outcomes, and (ii) firm heterogeneity in responses. For the loss analysis, I run the baseline model with a sample that includes loss years and add two indicator variables, as proposed by Dyreng et al. (2021) (Loss5 and \(Loss5\%)\) to control for incidental TP. While all previous TP and TU measures are used, a particular focus is on the TP measure of Henry and Sansing (2018), which is designed to capture TP in the presence of losses. For the heterogeneity analyses, I divide the sample into high and low value firms in terms of leverage, firm size, and cash flows. In addition, I interact the term \(TPS \cdot PI\) in Eq. 9 with the respective heterogeneity variable. A description of all variables can be found in Table 1.

4.3 Data and descriptive statistics

The balance sheet and equity data of publicly listed German firms for the sample period 2008–2018 stem from Datastream by Thomson Reuters. Information on the yield of ten-year German government bonds is acquired from the German Central Bank (German: Deutsche Bundesbank) as a measure of the risk-free rate of return for calculating the CoE. Since long-run measures over 5 years are used in the main specification, data on tax expense and pre-tax income must be available from 2004 onward. I rely on GAAP ETRs in the main analysis because cash taxes paid is a variable that is relatively rare in the German data.Footnote 9 When replicating the separate and composite view, the sample is restricted to firm-years with positive pre-tax income and income tax expense. Starting with 6667 firm-year observations for all publicly listed German firms that are active in the last sample year and for which information on pre-tax income and income tax expense is available, 1915 observations with negative pre-tax income and 348 (180) observations with negative income tax expense (cash taxes paid) are dropped.Footnote 10 Finally, 2199 observations are dropped due to the long-run horizons of the TP measures and missing information on the other control variables, resulting in a final sample with 2035 firm-year observations.

Table 2 presents the descriptive statistics of the TP measures and main variables. The ETRs are winsorized at 0 and 1, while all other variables are winsorized at the first and 99th percentiles. The average firm has a market-to-book ratio of 2.51 and pre-tax return to equity (PI) of 0.20. There appears to be a large variation in the sample regarding the TPS depending on how it is measured. The logic behind the composite measure implies only that a measure of TP should be in the numerator, while a measure of TU should be in the denominator—there is no particular indication of which exact measure to use. The smallest TPS means can be found when book tax differences are used for calculation. Interestingly, the mean of \(D\_MVA\) is negative, indicating that the average firm in the sample is "tax favored", in contrast to Henry and Sansing (2018). When loss firms are included, the mean of the measure becomes larger, but remains negative (see Table 7).

Figure 1 graphically displays the distribution of the market-to-book ratio across GETR deciles (Panel 1a), GETR volatility deciles (Panel 1b), and TPS deciles (Panel 1c). The market-to-book ratio increases in the bottom GETR deciles and shrinks in the upper deciles, while the highest firm values are found in the middle. Contrary to the intuition that high TP is associated with a high FV, the lowest GETRs tend to be associated with a relatively low FV. The relationship between TU and FV is much clearer, as the highest market-to-book ratios in Panel 1b are distributed in the lowest volatility deciles. This could be an explanation for the inconclusive GETR distribution: Low GETRs could be obtained by risky strategies that are negatively valued by investors, while the relationship between TU and TP could be non-linear (Guenther et al. 2017; Jacob and Schütt 2020). When both measures are combined in Panel 1c, the FV generally increases with higher TPS values.Footnote 11 Fig. 1 provides preliminary evidence that the composite view may be better suited to account for TU in a valuation framework.

MTB and tax planning, tax uncertainty, and TPS. Notes: This figure shows the distribution of the market-to-book ratio (MTB) over TP deciles (GAAP effective tax rate, GETR), TU deciles (GETR volatility), and Tax Planning Score (TPS) deciles. The GETR is winsorized at 0 and 1. All other variables are winsorized at the first and 99th percentiles. In Panel (a), the highest firm values are found in the middle of the GETR distribution, while the lowest and highest deciles show similar values. Panel (b) shows a clear negative relationship between TU and FV. Higher TPS values tend to be associated with a higher market-to-book ratio (Panel c)

5 Regression results

5.1 Comparing the separate and composite views

5.1.1 Replication results

Starting with the replication of both views, the direction of the associations and the statistical significance of the coefficient estimates, as an indicator of the fit of the models, are compared.Footnote 12 Table 3 contains the results of estimating Eq. 8 to replicate the separate view. The first three columns report the coefficients without firm fixed effects, while the last three columns include all fixed effects. Control variables are added gradually rather than immediately to test the robustness of specifications. The coefficient estimates show that, as expected, there is a large positive association between pre-tax income and the market-to-book ratio. This association seems to be moderated by operating risk (negative and significant coefficients for the interaction terms of PI and its volatility and cash flow volatility).

Regarding the TP variables of interest, there is neither systematic evidence that the degree of TP has positive value implications (since there are negative coefficients on TP), that TU has negative value implications (although most of the coefficients on TU are negative, they are not statistically significant), nor that TU moderates the association between TP and FV in the expected way: The coefficients on the interaction term between TP and TU are positive across most columns and mostly not statistically significant. Hence, the separate view does not yield significant results consistent with the intuition of Drake et al. (2019). Table 3 rather suggests that measures of operational volatility in the separate view are much more important than tax-related information (VolPI, VolCF, VolP).

As for the composite view, Table 4 shows the results of estimating Eq. 9. The columns refer to the same specifications as before. First, I again find positive and highly significant coefficients for PI. According to the estimate in column (6), a one unit increase in PI is associated with an increase in firm value of 4.688. Therefore, a one standard deviation increase in PI (14.7%) is associated with an increase in the market-to-book ratio of 27.45%, evaluated at sample mean values.Footnote 13 As depicted in Table 6, the magnitude of this coefficient depends on the time horizon used to measure TP. Second, the coefficient for TPS is slightly negative. However, the model of Jacob and Schütt (2020) makes no prediction about the direct relationship between the TPS and FV.Footnote 14 Most importantly, the estimates for the interaction term between TPS and PI are positive and significant at the 1%-level, consistent with the theoretical prediction. The economic magnitude of the association is relatively small when using the GETR as a measure: In the most comprehensive model (6), a one unit increase in TPS increases the coefficient of PI by 0.037, which is about 0.8% compared to the baseline coefficient of PI.Footnote 15 The association between TPS, PI and FV does not appear to be driven by operational volatility, as the interaction term of TPS with VolP (VolCF) is very small and insignificant (only marginally significant and small).

Taken together, Tables 3 and 4 show that the separate view does not yield coherent results, while the TPS-specification produces consistent results. The next subsection investigates if these remarks are robust to applying different TP measures and control settings.

5.1.2 Robustness of both views

Measuring tax planning

To ensure that the baseline results are not driven by arbitrary choices of how to measure TP and TU, I rerun the baseline regressions using the CETR and different time horizons over which the proxies are calculated (5, 8, and 10 years). In addition, I use the 5-year variants of book tax differences (BTD), their permanent component (PBTD), and the measure of Henry and Sansing (2018) (\(D\_MVA)\), basing these measures on both income tax expense (GAAP) and cash taxes (Cash). Table 5 presents the results for the separate view, while Table 6 contains the TPS model. All specifications include firm fixed effects, year fixed effects, and the full set of control variables. Note that fewer observations are available for the 8- and 10-year variants because additional years are needed to perform the rolling window calculations. The coefficient estimates in Table 5 are standardized for comparison because ETRs have a very different unit of measurement than book tax differences and the Henry and Sansing (2018) measure. The baseline conclusions for the separate view are not sensitive to the measure used.

Almost all specifications with ETRs (Panel A) do not yield coefficients with a consistent sign, nor is the main interaction statistically significant in the expected way. The only measure that yields results consistent with Drake et al. (2019) is BTD based on income tax expense. However, the interaction term is not significant.

In contrast, the coefficients for the interaction term of TPS and PI in Table 6 are more stable in terms of their statistical significance. Interestingly, the magnitude of the coefficient tends to be larger when the CETR is used and longer time horizons are applied. A last result worth noting is that applying the Henry and Sansing (2018) measure to the TPS logic yields robust results (Table 6, Panel B), and the coefficients are significant even in the separate model if D_MVA is based on income tax expense (however, the coefficient on TP has the wrong sign). Since losses were included in the calculation of the measure, this could indicate that the presence of past losses may not be a huge concern (Dyreng et al. 2021) if an appropriate measure is used. Overall, the composite view is more robust to the choice of the TP measure, but the results also suggest that the economic size of the association varies across measures.Footnote 16

Control settings

A major problem in conducting empirical analyses based on conditioning approaches is the choice of control variables. Omitted and unobserved variables that are correlated with the dependent and independent variables could bias the observed associations. While the inclusion of firm fixed effects is commonly used to mitigate this problem, it cannot be completely ruled out. Moreover, prior studies have made different choices about how to measure firm characteristics, and the direction of causality is often ambiguous, since it is not clear whether the independent variables affect the dependent variable or vice versa.Footnote 17 As a final robustness check, I run the baseline regressions with 13 different settings oriented on models from previous studies.Footnote 18 By comparing how the coefficient estimates vary across different choices how to operationalize broad concepts (e.g., firm size either as total assets, sales, or market value), the robustness of the models can be assessed. Figure 2 displays the coefficient estimates for the separate view with the GETR across control settings, while Fig. 3 shows the composite view. The dashed bars for each interaction coefficient indicate the 95% confidence intervals.Footnote 19

Separate view—control settings. Note: This figure presents the results from performing regressions for the separate view (Eq. 8) with altering control variables using the GETR. The x-axis shows the applied control setting (see Table A.1 in Online Appendix A). Coefficient estimates for TP, TU, and their interaction are denoted on the y-axis (for point estimates, see Table A.2 in Online Appendix A). All main variables are defined as in the baseline analysis and are described in more detail in Table 1

The estimates for the separate view are spread over a much larger range compared to the TPS specifications. This is especially true for the interaction term between TP and TU. While the coefficients for TP and TU are relatively stable (although their sign sometimes changes across models), the estimate for the interaction ranges from \(-\)2.580 to 4.386. Figure 3 shows that the coefficient for the interaction between TPS and PI ranges only from 0.026 to 0.064. Finally, the coefficients for the separate view are not statistically significant in most cases and only marginally significant in two cases (see also Table A.2 in Online Appendix A). For the composite view, all coefficients on the interaction term are significant at the 1% level.

Composite view—control settings. Note: This figure presents the results from performing regressions for the composite view (Eq. 9) with altering control variables using the TPS based on the GETR. The x-axis shows the applied control setting (see Table A.1 in Online Appendix A). Coefficient estimates for PI, TPS, and their interaction are denoted on the y-axis (for point estimates, see Table A.3 in Online Appendix A). All main variables are defined as in the baseline analysis and are described in more detail in Table 1

Since all previous analyses indicate that the composite view is better suited to yield consistent results in a valuation framework, the following additional analyses are performed primarily with the TPS and model of Jacob and Schütt (2020).

5.2 The role of losses: incidental vs. incremental TP

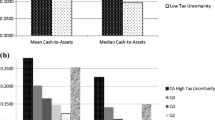

Dyreng et al. (2021) point out in a recent working paper that the role of losses has been largely neglected in the TP literature. The robustness tests in Table 6 have already shown that the baseline results are robust when the measurement method of Henry and Sansing (2018) is applied to include years with losses in the TPS calculation. However, this analysis was conducted with the same sample on which the other measures are based, covering only firm years with positive pre-tax income and tax expense. Therefore, loss years were only included in the calculation of the Henry and Sansing (2018) measure. Dyreng et al. (2021) replicate specifications of selected previous studies and show that their results become insignificant once recent losses are accounted for (e.g., for Hasan et al. 2014).

Table 7 shows the distribution of the mean and median values of the GETR, Delta MVA, the TPS based on the GETR, and on Delta MVA over the number of losses in the last 5 years (0–5). Although the mean GETR does not decrease as monotonically with the number of loss years (when fewer than 2 loss years are documented) as in Dyreng et al. (2021), there is a clear trend that supports the notion that previous loss years are associated with lower GETRs. Without considering this, these values would simply indicate a high level of TP.

Conversely, the values of the TPS based on the GETR do not systematically increase with the number of losses. This could be due to the fact that not only the level of TP but also its volatility is used for calculation, which could partially counteract the random increase of TP. However, the very large number of the TPS (GETR) at 5 previous loss years indicates that the highest value of uncertainty-adjusted TP is at most previous losses, similar to the isolated GETR. The Henry and Sansing (2018) measure, in contrast, shows the opposite pattern: D_MVA (the corresponding TPS) actually increases (decreases) with the number of loss years, implying less (uncertainty-adjusted) TP. This indicates that Delta MVA may not be affected by recent losses in the way that Dyreng et al. (2021) identify as problematic.

The empirical approach of Dyreng et al. (2021) to account for the potential bias of losses is applied to the analyses of this paper by adding the variable Loss5 or \(Loss5\%\) to regression Eq. 9.Footnote 20Loss5 is an indicator variable that equals 1 if pre-tax income was negative in at least one of the previous 5 years, while \(Loss5\%\) is the percentage of loss years in the previous 5 years (i.e., if all of the previous 5 years were loss years, this variable would take the value 1).

Table 8 reports the results. The first two columns show the separate view with the GETR, while columns 3–4 show the TPS results based on the GETR. The last two columns focus on the analyses that use the Henry and Sansing (2018) measure to calculate the TPS. Table A.6 in Online Appendix A shows the results of the loss analysis for the TPS with the other measures.

Controlling for recent losses seems to affect the results when ETRs are used. The coefficients become insignificant and are essentially zero even when the TPS and the composite view is used. This is consistent with the descriptive evidence in Table 7: While the GETRs decrease with the number of recent losses and the GETR-based TPS has the highest value when most of the previous losses are present, in contrast, the TPS based on Henry and Sansing (2018) decreases with the number of previous losses. The key takeaway is that whether the composite view is robust to the distinction between incidental and incremental TP seems to depend on how TP is measured. Table A.6 in Online Appendix A shows that using book tax differences as a basis of the TPS is similarly robust, while using the CETR is again problematic.Footnote 21 This supports the results of Dyreng et al. (2021) since they also use ETRs as TP measures (because most of the previous literature did), but it also raises the question whether their conclusions hold for other measurement approaches.

5.3 Heterogeneity

As described in Sect. 3.3, the question of what type of firms drive the results, or for which firms the documented positive link between uncertainty-weighted TP, pre-tax income and FV is particularly strong, has not yet been explored. I focus on two possible heterogeneity dimensions: leverage (measured by the total debt to equity ratio, Leverage) and available resources, operationalized by two concepts (firm size, measured by market value, Size and liquidity, proxied by cash flows, CashflowFootnote 22).

Regression Eq. 9 is performed by splitting the sample into high and low leverage (big and small, high and low cash flow) firms. A firm is considered highly leveraged (big, high cash flow) if it belongs to the top quintile of each distribution. Table A.7 in Online Appendix A shows the results when median splits are performed. I expect that the link between TP and FV is less pronounced for highly leveraged firms, as default risk becomes more of an issue, and debt overhang could become a problem that affects the equity value (Myers 1977; Cai and Zhang 2011). In addition, the tax benefits from debt-related deductions decrease as TP increases. With respect to available resources, there is no clear prediction. On the one hand, bigger and high cash flow firms tend to have more resources for TP and lower relative planning costs (Eichfelder and Vaillancourt 2014; Hundsdoerfer and Jacob 2019). On the other hand, firms with less resources could derive a larger relative (cash flow) advantage from TP activities.

Table 9 shows the results of Eq. 9 after splitting the sample, and when interacting \(TPS \cdot PI\) with the respective heterogeneity indicator. The sample splits show that the positive association between TPS and PI is statistically significant only for firms with low leverage, small firms, and firms with low cash flows. The only significant interaction term, however, is observed for leverage: the negative sign means that the still significant positive association between the TPS, PI, and FV becomes smaller (and possibly even cancels out) as the leverage becomes higher. This supports the notion that the higher the debt tax shield, the lower uncertainty-adjusted TP is valued. The results of splitting the sample by size and cash flow can be seen as an indication that the benefits of TP are valued relatively higher in firms for which improving available resources through TP is more important. However, since the interaction terms are not statistically significant, these results should be interpreted with caution. The main conclusions also apply qualitatively when choosing the median as the cut-off to divide the sample (see Table A.7 in Online Appendix A), as well as using alternative measures for the heterogeneity concepts (see Table A.8 in Online Appendix A).

6 Conclusion

This paper empirically provides support for the notion of Jacob and Schütt (2020) that TP and TU should be considered jointly in a valuation framework, and that their link to FV is better investigated indirectly through income channels. Since the composite view and the TPS have not been as widely recognized in recent studies, this should be taken more seriously in future empirical research. Nonetheless, as the robustness tests have shown, coefficient estimates can vary considerably across measurement choices—even in the composite view. The TPS logic can be extended to a wide range of measures without losing its qualitative robustness, but the quantitative interpretation of results might differ. Therefore, for future empirical studies, it seems advisable to apply different TP measures to interpret more carefully the economic significance of results and not just rely on one arbitrary point estimate. Related to measurement issues, the additional analyses have shown that whether the composite view works well when including loss-making firms and controlling for recent losses depends on the basis of the TPS. Similar to Dyreng et al. (2021), specifications that rely on ETRs appear to be biased by recent losses, while using the Henry and Sansing (2018) measure designed to measure TP in the presence of losses mitigates this problem. Therefore, while Dyreng et al. (2021) conclude that recent losses likely affect the conclusions drawn from TP analyses, this may depend on the careful choice of the TP measure. To confirm and generalize this, however, a comprehensive replication of previous studies similar to Dyreng et al. (2021) with different measurement approaches is needed. The measure of Henry and Sansing (2018) seems to be a promising candidate for this exercise, either in isolation (e.g., for replication of Hasan et al. 2014) or also as the basis of the TPS when uncertainty of TP needs to be accounted for (e.g., Sikes and Verrecchia 2020).

A potential reason that studies have not picked up on the TPS could be that its use does not come without caveats. By applying a composite measure, the incremental impact of TP and TU cannot be properly assessed. Further research is needed in this regard, as the simulations in Jacob and Schütt (2020) and the empirical results of this paper suggest that simply separating the two concepts in standard conditioning approaches risks a strong dependence on measurement and control setting choices (see also Online Appendix B). Nevertheless, the robustness and additional analyses with the TPS-based specifications indicate that the use of the TPS may be beneficial for future empirical studies on the role of corporate TP not only in valuation but also in other areas of business economics, such as the capital structure choice of firms (Faccio and Xu 2015)—as the heterogeneity analyses suggest that leverage can have an impact on how positively uncertainty-weighted TP is valued—as well as the determinants of the (equity) cost of capital (Cook et al. 2017), or stock returns (Heitzman and Ogneva 2019), where TU has not yet been explicitly considered.

Data availability statement

The dataset generated for the current study stems from Datastream by Thomson Reuters and is not publicly available without a user’s license. Information on how to obtain it and reproduce the analyses is available from the author on request.

Notes

Jacob and Schütt (2020) note that "in any setting where expectations about future tax rates are important, adequately incorporating tax uncertainty is crucial for assessing the role of tax avoidance." (p. 411) There is no apparent reason indicating that the conclusions about the need to include TU in TP analyses are exclusive to the topic of valuation.

For example, studies examining the association between TP and the cost of equity (CoE) (Goh et al. 2016; Cook et al. 2017) or stock returns (Heitzman and Ogneva 2019) do not directly address the relationship with FV, but CoE are relevant in valuation formulas and are often measured by market returns.

A potential limitation of the data base with respect to the TP measures—particularly ETRs—is that variation in ETRs may be partly driven by foreign tax rates, as the firms in the sample operate internationally. Due to data limitations, the (weighted) tax rates of the group to which the firm belongs—or is a parent of—are not available.

For example, the CoE are only part of the composite approach in the replication analyses. When changing the control settings in Sect. 5.1.2, the exact same specifications are applied to both views.

Jacob and Schütt (2020) use industry fixed effects in their main analyses, while I use firm fixed effects throughout to control for unobserved firm characteristics. Hence, Eq. 9 exploits variation in the average TPS (and the other variables) within firms over time, while controlling for industry fixed also considers cross-sectional variation between firms.

If the objective of previous studies differs slightly from the direct investigation of FV implications of TP, the control settings are adjusted. For example, controlling for the book-to-market ratio (Cook et al. 2017; Sikes and Verrecchia 2020) when the market-to-book ratio is the dependent variable clearly leads to biased estimates, so this variable is excluded from the respective settings.

The item "Cashflow Taxation" in Datastream has almost twice as many missings as income tax expense. Cash ETRs and other measures are used in robustness analyses.

When the Henry and Sansing (2018) measure is calculated, these restrictions are not required. However, in the replication and corresponding robustness analyses, I use this measure for the same sample as the GETR to ensure that the results are not driven by different firms in the samples. Additional analyses in Sect. 5.2 rely on the full sample including loss years.

This is confirmed when the TPS is regressed on FV in isolation, see Table B.9 in Online Appendix B.

Note that insignificant coefficients on the TP variables could not only stem from measurement error (separately vs. jointly), but also from investors not processing tax information efficiently. The separate view also implies that investors deem TP and TU as (equally) value relevant, while the TPS-model relies on the notion that the degree of TP needs to be adjusted by its information content (it’s uncertainty).

Calculated as 0.689 (\(=4.688/(1/0.147)\)) divided by the sample mean of MTB of 2.510, see Table 2.

When regressing the TPS on FV without interactions, the coefficient is positive and highly significant throughout all models (see Table B.9 in Online Appendix B), which confirms the illustrative graphical representation in Fig. 1c. Moreover, the positive coefficient for the interaction of TPS and PI in Table 4 outweighs the coefficient for TPS, indicating an overall positive relationship.

Hence, if the mean firm increases its TPS by one unit, the positive association between a one standard deviation increase in PI and the market-to-book ratio increases from 27.45% to 27.67% (\(27.45\% \cdot 1.008\)). As Table 6 shows, increasing the TPS by one unit amplifies the positive association between PI and FV at most by 4.96% (12.91%, 4.27%, 6.05%) for the GETR (CETR, BTD GAAP, D_MVA) as the basis for TPS, depending on the time horizon.

In supplemental analyses in Online Appendix B, I attempt to reconcile the separate and composite views by translating the logic of the former into the latter and vice versa. Although the estimates from this exercise are difficult to interpret, the results indicate that the separate view performs more robustly when it is applied through income channels. Nevertheless, the notion of Jacob and Schütt (2020), p. 428 regarding potential misspecification is still confirmed.

For example, many of the control variables in the valuation literature, as well as (components of) the market-to-book ratio itself, are often used as independent variables in studies on the determinants of TP (e.g., Mills 1998; Dyreng et al. 2008, 2010). The same applies to control variables calculated in a similar way as the dependent variable (e.g., CoE/CoC when stock price is used as an approximation).

Table A.1 in Online Appendix A provides an overview of the variables used. Due to data limitations, not all variables in the studies could be used. However, the specifications were replicated as closely as possible and show considerable variation in settings.

Table A.2 (Table A.3) in Online Appendix A shows the point estimates for the separate view (composite view).

When using the loss sample, a problem is that the values of PI are potentially implausible or difficult to interpret when negative values of pre-tax income and common equity are present. In these cases, I set PI to zero and add a control indicator equal to one if PI was affected by this transformation so as not to lose observations. The results and conclusions regarding the TP variables are essentially unchanged (i) without this transformation (but the coefficients on PI become insignificant and sometimes marginally negative), and (ii) when the final estimation sample is restricted to positive values of PI after all other measures have been calculated while including loss years.

Henry and Sansing (2018) note that their measure is very similar to book tax differences (p. 1052 f.; see also Table 1), but negative income tax expense is included. The second difference they highlight is the use of cash taxes paid. To avoid losing too many observations, the main analyses here rely on income tax expense. However, the main conclusions of this paper also apply when D_MVA is calculated on a cash basis.

Since the item cash holdings in Datastream has more missings than cash flows, the latter is used here. Table A.8 in Online Appendix A shows the results when alternative measures are used, i.e., only long term debt for leverage, sales for firm size, and cash holdings for liquidity. The results are qualitatively unchanged.

References

Abernathy JL, Finley AR, Rapley ET, Stekelberg J (2021) External auditor responses to tax risk. J Account Audit Financ 36(3):489–516

Adams MT, Inger KK, Meckfessel MD, Maher JJ (2022) Tax-related restatements and tax avoidance behavior. J Account Audit Financ p. 0148558X221115482

Arora TS, Gill S (2022) Impact of corporate tax aggressiveness on firm value: evidence from India. Manag Financ 48(2):313–333

Assidi S (2015) Tax risk and stock return volatility: case study for French firms. Int J Bus Contin Risk Manag 6(2):137–146

Blouin J (2014) Defining and measuring tax planning aggressiveness. Natl Tax J 67(4):875–899

Brooks C, Godfrey C, Hillenbrand C, Money K (2016) Do investors care about corporate taxes? J Corp Finan 38:218–248

Brown J, Lin K, Moore JA, Wellman L (2014) Tax policy uncertainty and the perceived riskiness of tax savings, Arizona State University, Oregon State University, and University of Illinois at Chicago working paper

Büttner T, Overesch M, Wamser G (2011) Tax status and tax response heterogeneity of multinationals’ debt finance. FinanzArchiv/Public Financ Anal pp. 103–122

Cai J, Zhang Z (2011) Leverage change, debt overhang, and stock prices. J Corp Finan 17(3):391–402

Chukwudi UV, Okonkwo OT, Asika ER (2020) Effect of tax planning on firm value of quoted consumer goods manufacturing firms in Nigeria. Int J Finan Bank Res 6(1):1–10

Ciconte W, Donohoe MP, Lisowsky P, Mayberry M (2016) Predictable uncertainty: the relation between unrecognized tax benefits and future income tax cash outflows, Available at SSRN 2390150

Cook KA, Moser WJ, Omer TC (2017) Tax avoidance and ex ante cost of capital. J Bus Financ Account 44(7–8):1109–1136

De Simone L, Nickerson J, Seidman J, Stomberg B (2020) How reliably do empirical tests identify tax avoidance? Contemp Account Res 37(3):1536–1561

Desai MA, Dharmapala D (2009) Corporate tax avoidance and firm value. Rev Econ Stat 91(3):537–546

Dhawan A, Ma L, Kim MH (2020) Effect of corporate tax avoidance activities on firm bankruptcy risk. J Contemp Account Econ 16(2):100187

Dos Santos RB, Rezende AJ (2020) The reputational costs of tax avoidance in financial institutions. In: Conference Paper

Drake KD, Lusch SJ, Stekelberg J (2019) Does tax risk affect investor valuation of tax avoidance? J Account Audit Financ 34(1):151–176

Dyreng SD, Hanlon M, Maydew EL (2008) Long-run corporate tax avoidance. Account Rev 83(1):61–82

Dyreng SD, Hanlon M, Maydew EL (2010) The effects of executives on corporate tax avoidance. Account Rev 85(4):1163–1189

Dyreng S, Lewellen C, Lindsey B, Hills R (2021) Tax avoidance or recent losses? Working Paper

Eichfelder S, Vaillancourt F (2014) Tax compliance costs: a review of cost burdens and cost structures. Hacienda Pública Española/Rev Publ Econ 210:111–148

Faccio M, Xu J (2015) Taxes and capital structure. J Financ Quant Anal 50(3):277–300

Feltham GA, Ohlson JA (1995) Valuation and clean surplus accounting for operating and financial activities. Contemp Account Res 11(2):689–731

Firmansyah A, Widodo TT (2021) Does investors respond to tax avoidance and tax risk? Stewardship perspective. Bina Ekonomi 25(1):23–40

Firmansyah A, Febrian W, Falbo TD (2022) The role of corporate governance and tax risk in Indonesia investor response to tax avoidance and tax aggressiveness. Jurnal Riset Akuntansi Terpadu 15(1):11–27

Gallemore J, Maydew EL, Thornock JR (2014) The reputational costs of tax avoidance. Contemp Account Res 31(4):1103–1133

Gkikopoulos S, Lee E, Stathopoulos K (2021) Does corporate tax planning affect firm productivity? Available at SSRN 3856522

Goh BW, Lee J, Lim CY, Shevlin T (2016) The effect of corporate tax avoidance on the cost of equity. Account Rev 91(6):1647–1670

Guenther DA, Matsunaga SR, Williams BM (2017) Is tax avoidance related to firm risk? Account Rev 92(1):115–136

Guenther DA, Wilson RJ, Wu K (2019) Tax uncertainty and incremental tax avoidance. Account Rev 94(2):229–247

Hanlon M, Heitzman S (2010) A review of tax research. J Account Econ 50(2–3):127–178

Hanlon M, Slemrod J (2009) What does tax aggressiveness signal? Evidence from stock price reactions to news about tax shelter involvement. J Public Econ 93(1–2):126–141

Hasan I, Hoi CKS, Wu Q, Zhang H (2014) Beauty is in the eye of the beholder: the effect of corporate tax avoidance on the cost of bank loans. J Financ Econ 113(1):109–130

He G, Ren HM, Taffler R (2020) The impact of corporate tax avoidance on analyst coverage and forecasts. Rev Quant Financ Acc 54(2):447–477

Heitzman SM, Ogneva M (2019) Industry tax planning and stock returns. Account Rev 94(5):219–246

Henry E, Sansing R (2018) Corporate tax avoidance: data truncation and loss firms. Rev Account Stud 23:1042–1070

Hundsdoerfer J, Jacob M (2019) Conforming tax planning and firms’ cost behavior. Available at SSRN 3430726

Hutchens M, Rego S (2013) Tax risk and the cost of equity capital. Indiana University working paper

Hutchens M, Rego SO (2015) Does greater tax risk lead to increased firm risk? Available at SSRN 2186564

Inger K, Stekelberg J (2022) Valuation implications of socially responsible tax avoidance: evidence from the electricity industry. J Account Public Policy 41(4):106959

Irawan F, Turwanto T (2020) The effect of tax avoidance on firm value with tax risk as moderating variable. Test Eng Manag 83:9696–9707

Jacob M, Schütt HH (2020) Firm valuation and the uncertainty of future tax avoidance. Eur Account Rev 29(3):409–435

Jacob M, Wentland K, Wentland SA (2022) Real effects of tax uncertainty: evidence from firm capital investments. Manag Sci 68(6):4065–4089

Jacob M, Schütt HH (2013) Firm valuation and the uncertainty of future tax avoidance.Arqus-Arbeitskreis Quantitative Steuerlehre

Khuong NV, Liem NT, Thu PA, Khanh THT (2020) Does corporate tax avoidance explain firm performance? Evidence from an emerging economy. Cogent Bus Manag 7(1):1780101

Kim J-B, Li Y, Zhang L (2011) Corporate tax avoidance and stock price crash risk: firm-level analysis. J Financ Econ 100(3):639–662

Kruschwitz L, Löffler A (2006) Discounted cash flow: a theory of the valuation of firms. John Wiley and Sons, Hoboken

Lambert R, Leuz C, Verrecchia RE (2007) Accounting information, disclosure, and the cost of capital. J Account Res 45(2):385–420

Lisowsky P, Robinson L, Schmidt A (2013) Do publicly disclosed tax reserves tell us about privately disclosed tax shelter activity? J Account Res 51(3):583–629

Mills LF (1998) Book-tax differences and internal revenue service adjustments. J Account Res 36(2):343–356

Myers SC (1977) Determinants of corporate borrowing. J Financ Econ 5(2):147–175

Nesbitt WL, Outslay E, Persson A (2017) The relation between tax risk and firm value: Evidence from the luxembourg tax leaks. Available at SSRN 2901143

Neuman SS (2014) Effective tax strategies: it’s not just minimization. Available at SSRN 2496994

Osswald B (2020) Does tax risk attenuate the positive association between internal and external information quality? The University of Wisconsin-Madison

Purwaka AJ, Firmansyah A, Qadri RA, Dinarjito A, Arfiansyah Z et al (2022) Cost of capital, corporate tax plannings, and corporate social responsibility disclosure. Jurnal Akuntansi 26(1):1–22

Rudyanto A, Pirzada K (2021) The role of sustainability reporting in shareholder perception of tax avoidance. Soc Responsib J 17(5):669–685

Seifzadeh M (2022) The effectiveness of management ability on firm value and tax avoidance. J Risk Financ Manag 15(11):539

Sikes S, Verrecchia RE (2020) Aggregate corporate tax avoidance and cost of capital. Available at SSRN 3662733

Vello A, Martinez AL (2012) Efficient tax planning: an analysis of its relationship with market risk. Available at SSRN 2140000

Zwick E, Mahon J (2017) Tax policy and heterogeneous investment behavior. Am Econ Rev 107(1):217–248

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The author declares that no funds, grants, or other support were received during the preparation of this manuscript. The author has no relevant financial or non-financial interests to disclose. The author has no affiliations with or involvement in any organization or entity with any financial interest or non-financial interest in the subject matter or materials discussed in this manuscript.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The author would like to thank Sebastian Eichfelder, Martin Jacob, two anonymous reviewers for the 2022 European Accounting Review Annual Conference, as well as two anonymous reviewers at Journal of Business Economics and Jochen Hundsdoerfer (Editor) for helpful comments and suggestions. The interpretation of results, opinions and potential errors are solely the author’s responsibility. Information on how the data used in this study can be obtained is available upon request. There are no competing interests to declare.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Knaisch, J. How to account for tax planning and its uncertainty in firm valuation?. J Bus Econ 94, 579–611 (2024). https://doi.org/10.1007/s11573-023-01177-1

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11573-023-01177-1