Abstract

The growing relevance of sustainability reporting (SR) has dramatically surged advocacy and interest among both academicians and practitioners. However, few studies have attempted to holistically encapsulate global research on sustainability reporting. The present study employed scientometric analysis on sustainability reporting based 1434 articles extracted from the Web of Science database, published between 1992 and 2022, to comprehensively map the intellectual structure of this field. Domain visualizations were constructed using CiteSpace software to identify networks of co-authorship, keywords, subject categories, institutions, and countries engaged in publishing on SR along with co-citation and cluster analysis. The findings revealed that significant contributions in SR research have originated primarily from developed countries, underscoring the necessity for more research in the context of developing and emerging countries. SR field was found characterized by cohesive research sub-communities but lacked global cooperation. Existing studies in the SR research domain focused mainly on subject categories of business, management, environmental studies, green and sustainable science technology, environmental sciences, and business finance. Analysis of most co-cited authors and content analysis of highly co-cited articles were performed, detailing pioneer works in the field. The principal topics in the body of literature were identified via clusters of co-citations between documents and keywords. Future research focus areas include exploring the link between circular economy and SR, the role of social media, blockchain, artificial intelligence, and other digital technologies in SR, attention on the MSME sector, mandatory reporting, assessment of real impact of SR on investor sentiments and financial analysts’ valuations, assurance, standardization, financial-sector inclusive research, materiality issues, and understanding niche themes of SR, inclusive of monothematic reporting. Implications of the study for policymakers, companies, society, and academia were examined.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Background

Rising concerns about climate change, gender inequality, racial injustice, forest fires, biodiversity loss, water scarcity, governance failures, irreparable environmental and social damage, and the global coronavirus pandemic serve as constant wake-up calls urging people around the world to recognize the necessity of incorporating sustainability into every aspect of their lives—personal, organizational, and planetary. In light of the urgent need to establish corporate responsibility and accountability for the consumption of finite planetary resources, support for sustainability reporting (SR) has steadily increased over the years. Goal 12.6 of the UN’s sustainable development goals (SDG) mandates businesses to incorporate sustainability data into their reporting cycles, recognizing SR as a crucial tool for enabling the transition to sustainable business models, a sustainable global economy, and ultimately helping to build a sustainable planet for all.

SR acts as a key instrument in mitigating environmental damage (Alazzani and Wan-Hussin 2013), yields higher profitability (Conca et al. 2020), lowers the cost of equity capital (Gerged et al. 2020), enhances firm and market value (Radhouane et al. 2018), improves financial analysts’ accuracy (Ferrer et al. 2020), fosters a positive reputation (Abbas et al. 2022a; Abbas et al. 2023), increases stakeholder trust, and mitigates firms’ risk (Benlemlih et al. 2018).

Although no standard definition of “sustainability reporting” exists as of 2023, the age-old pioneer sustainability reporting standard setter, Global Reporting Initiative (GRI), defines sustainability reporting as “an organization’s practice of reporting publicly on its economic, environmental, and/or social impacts, and hence its contributions – positive or negative – toward the goal of sustainable development” (GRI 2016, p. 3). Various reporting terms are encompassed within or are used in conjunction with the term “sustainability reporting,” each associated with a unique serving purpose and reporting foci, as depicted and defined in Fig. 1.

Reporting terms used synonymously or in conjunction with the umbrella term “sustainability reporting” (author’s own elaboration)

The information demands of SR stakeholders have evolved over time, demonstrating a shift towards more thorough reporting systems, greater stakeholder expectations, and deeper comprehension of the importance of SR. The progression of information expectations among various stakeholders with regards to SR from the 1960s to the present is shown in Fig. 2. Stakeholders’ “mere disclosure ask” has transitioned from reporting on different issues to a “real information ask” for precise disclosures on paths and strategies adopted for establishing sustainable business models. This illustrates the evolving and developing global understanding and interpretation of the true meaning of sustainability. The World Commission on Environment and Development (WCED) Brundtland Commission 1987 initiated the need for sustainable development and various landmark events over the years, including the Kyoto Protocol 2002, the era of major financial and governance scams (such as the Enron scam), the UN SDG Agenda 2030 (set in 2015), the Paris Agreement 2016, and pandemics along with the United Nations Climate Change Convention (UNCCC) conferences held in 2021 (COP26) and 2022 (COP27) have fueled and advanced the global sustainability propaganda. These global events aimed at advancing advocacy for sustainability coupled with heightened investor interest in quality reporting enactment of varied reporting laws, regulations, and stock exchange requirements rising shareholder and stakeholder ESG activism (Thun and Zülch 2023); and a growing understanding of the impact of sustainability issues on corporate value underpin the major factors driving the espousal of SR (KPMG 2020).

Evolution of information expectations from sustainability reporting (authors’ own elaboration)

The SR domain remains relatively more complex than the financial reporting domain because of the lack of a universal reporting standard, the need to cater to diverse stakeholders, and the issue of reporting inconsistency and competing metrics. Major SR standard-setting bodies include the Carbon Disclosure Project (CDP), the Climate Disclosure Standards Board (CDSB), GRI, the Value Reporting Foundation (merged entity of the International Integrated Reporting Council (IIRC)), the Sustainability Accounting Standards Board (SASB), and Task Force on Climate-Related Financial Disclosures (TCFD). As of 2023, the SR field is entering a new era because of recent significant advancements that mark attempts to standardize the SR domain and increase the impact, transparency, and effectiveness of sustainability disclosures. While the European Commission (EU) issued its own standard-setting mandate for the European Financial Reporting Advisory Group (EFRAG), the International Sustainability Standards Board (ISSB) was announced by the International Financial Reporting Standards (IFRS) Foundation to mandate ESG disclosures during COP26. In order to replace the current NFRD (Non-financial Reporting Directive) in 2022, the EU Corporate Sustainability Reporting Directive (CSRD) planned to extend the SR criteria. Increased adoption of the TCFD framework and the introduction of an EU taxonomy are intended to create standardized climate disclosures.

Existing literature review studies

Regarding academic literature, to the best of our knowledge, 60 review studies have been published between 1976 and 2023 in the SR domain, each with a special research focus, as detailed in Table 1.

Contribution of the present study

Our scientometric analysis differs from others in several ways. Current bibliometrics either have poor data coverage (Bosi et al. 2022), lack thorough analysis, use narrow keyword search strings (Pasko et al. 2021), or are narrowly focused (Di Vaio et al. 2020; Gulluscio et al. 2020). We contribute to the lack of scientometric reviews in the SR field and offer a comprehensive examination of the intellectual, social, and conceptual framework of the sustainability reporting domain to give researchers a broad overview of the topic. This study shall assist stakeholders, including both industry and academia, in examining the developmental stages of the domain, as well as its prospects, based on data from over 30 years. We provide a state-of-the-art understanding of the SR field by addressing important research questions. The research objectives and associated scientometric techniques applied in this study are summarized in Table 2.

The contribution of this study is that it is not just confined to scientometric measurements. A thorough cluster analysis was performed along with a review of 60 literature reviews published between 1976 and 2023, a thorough synthetization of theoretical foundations underpinning SR literature, and content analysis of highly cited articles. This article closes the current knowledge and awareness gap. As discussed in detail at the end of the research paper, this study has numerous ramifications for decision-makers in government, business, society, and academia.

The rest of the article is structured as follows: the “Theories underpinning SR literature” section details the theoretical foundations of the SR literature, the “Research methodology” section illustrates the research methodology used, the “Visualizations, data analysis, and research results” section discusses the analysis of the created visualizations and networks, the “Future research avenues (response to RQ3)” section suggests areas for future research work, the “Conclusions and implications of the study” section concludes the research and enumerates the implications, and the “Limitations of the study” section specifies limitations of the study.

Theories underpinning SR literature

The extant academic literature of SR is underpinned by varied theories. Table 3 summarizes these theories and enlists the highly cited papers associated to the theory and its application to the SR field.

Legitimacy theory (Lindblom 1994; Suchman 1995) postulates that organizations need to abide by the social contract, undertaking socially acceptable behavior in exchange for approval of their objectives which guarantees them the license to operate (Deegan 2002) and their continued existence in the society (Reverte 2009). Accordingly, SR practices are adopted by firms in response to political and social pressures (Cho and Patten 2007) to either gain, maintain, or repair moral, pragmatic, or cognitive organizational legitimacy (Suchman 1995). A firm tends to use SR as a legitimation tool (Chen and Roberts 2010) to communicate its image as a good corporate citizen (Mahadeo et al. 2011) possessing values congruent to that of society as a whole (Lindblom 1994).

While SR researchers mostly apply the legitimacy theory in context to the “bourgeois” political economy theory which considers the society as pluralistic and unified (Bebbington et al. 2014), stakeholder theory (Freeman 1984; Clarkson 1995) embraces the view that some groups within the society are more powerful than others (Woodward et al. 1996). This theory recognizes that apart from shareholders, the expectations of the broader audience (Freeman 1984) and the societal call for responsible business conduct need to be addressed (Hahn and Kühnen 2013). SR serves as a dialogic instrument between the firm and its stakeholders for the negotiation of sustainability-linked contracts (Roberts 1992).

Unlike legitimacy and stakeholder theory which suggest that SR is a deliberate managerial act, institutional theory (Meyer and Rowan 1977; DiMaggio and Powell 1983) postulates sustainability disclosures as a means to comply with institutional norms and rules (Chen and Roberts 2010) to manage the ESG impacts on their business operations (Adams and Larrinaga‐González 2007). DiMaggio and Powell (1983) posited that isomorphic change is crucial for firms’ survival, which occurs through three mechanisms, namely, “coercive” isomorphism, “normative” isomorphism, and “mimetic” isomorphism. This theory explains why there is homogenization of SR practices within organizational fields, for instance, within a sector or country, providing a clear understanding of the accounting approaches of the constituent companies and society (Rahman et al. 2019).

Proprietary costs theory propounds that managers assess the costs and benefits of reporting and refrain from disclosing proprietary information which can tarnish the firm (Dye 1985; Verrecchia 1983, 1990). Proprietary costs include internal costs of production and release of reports, and external costs arise from competitors utilizing the published information for their own advantage (Prencipe 2004). Firms are incentivized to disclose voluntarily only when it either fetches benefits in the form of reduced equity (Botosan 1997; Botosan and Plumlee 2002) or debt costs (Sengupta 1998) or helps in traversing the information gap without adversely affecting the firm value.

Both voluntary disclosure theory (Clarkson et al. 2008, 2011) and signaling theory (Spence 1973) suggest that due to existing information asymmetry between the firm and its stakeholders, companies use reporting as a proactive measure (Connelly et al. 2010) to signal and convey their sustainability values, practices, and impacts. Large number of stakeholders, more importantly, the influential equity and debtholders, and the media can considerably influence the company to consistently seek legitimacy via signaling ESG efforts in its reports (Hahn and Kühnen 2013). It is important to note here that while VDT necessarily stems from the need to reveal superior sustainability performance, with the aim to unravel its true nature and improve firm value, the signaling theory may or may not emanate from definite ESG performance and commitment. As a matter of fact, SR may be used for “greenwashing” (Mahoney and Qian 2013) or to camouflage or rather deviate stakeholders from firm’s poor environmental practices, as also discovered by Clarkson et al. (2011) who found greater environment disclosures by higher pollution indexed firms in the perusal of impression management. Investors that are considerate of the ESG criterion in their capital allocation decisions must be cautious of such firms.

As per the resource dependency approach theory (Aldrich and Pfeffer 1976; Pfeffer and Salancik 1978, 2003), an organization is not self-contained and depends on its environment for external resources which ensures its continued existence and growth (Chen and Roberts 2010). This theory, focused on businesses’ competence to attain relevant resources, implies that firms and their managers would need to meet the expectations and needs of capital providers for smooth and easy access to financing which may include disclosure of quality ESG information. Past research has also testified that meaningful and credible sustainability-related reporting ensures better as well as cheaper access to both equity and debt financing (Dhaliwal et al. 2011; Hamrouni et al. 2019; Kordsachia 2020).

Agency theory suggests that an asymmetric information gap exists between the principals and the agents (Jensen and Meckling 1976). The agents possessing superior information act opportunistically and take decisions that maximize their own interests. Company managers (agents) resort to various communication channels (Brammer and Pavelin 2008) including sustainability reporting to bridge this gap, mitigate agency issues problems, and reduce agency costs.

Research methodology

Research method

The knowledge domain of sustainability reporting underwent a scientific mapping using scientometrics, which plays a crucial role in addressing our research questions. The term “scientometrics” originated from the Russian equivalent term naukometriya, introduced by Vassily V. in 1969. According to Tague-Sutcliffe (1992), scientometrics involves the quantitative study of science as a discipline or economic activity. It is considered a part of the sociology of science and finds applications in science policy-making. Various studies across disciplines, such as Zhao (2017), Li et al. (2021), Pedroso et al. (2022), and Singhania et al. (2023a), have utilized the scientometric review method to gain unbiased and in-depth insights by leveraging its power of domain visualizations and associated analyses.

Scientometric reviews provide a quantitative assessment of the research topic, setting them apart from traditional subjective reviews. Klarin and Suseno (2023) highlight that this approach relies on sophisticated algorithms, enabling a fair and objective analysis of the research field. Scientometric reviews offer a comprehensive understanding by examining all academic works related to a particular subject, allowing for a complete mapping of the research field based on quantitative measurements. This quantitative justification is a key distinction between scientometric reviews and other types of reviews. While general synthesis literature provides a qualitative analysis without empirical findings, scientometric reviews utilize analytical methods, such as mapping and visualization, to offer empirical evidence. Chen and Song (2019) note that scientometric approaches facilitate content analysis, including the identification of influential themes, trends, and publications within a given subject. By using scientometric software like CiteSpace, which provides information on citation bursts and sigma scores, researchers can identify the significance and novelty of studies across different time periods in an unbiased manner. While scientometric studies (Singhania et al. 2023b) are very similar to bibliometric studies (Mehmood et al. 2023a; Mehmood et al. 2023b), scientometric software and mapping techniques offer more nuanced observations and visualizations, providing information on citation bursts and sigma scores. This comprehensive approach helps identify significant changes in academic subjects over time. Considering the aforementioned justifications, we prefer the scientometric analysis approach over other literature review methods. Its ability to provide objective insights, visual representations, and quantitative measurements strengthens the analysis of the sustainability reporting knowledge domain.

Research process

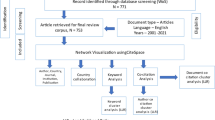

Stepwise research process followed for review is depicted in Fig. 3. Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) guidelines (Moher et al. 2009) were followed for the conduct of the present review as depicted in Fig. 4, detailed as follows:

-

Step 1: Database selection

Research process

PRISMA flow chart

Clarivate Analytics’ WoS was the source database for this study. This is because WoS is considered the most thorough owing to its scientific soundness. It includes the most pertinent and significant journals in its record offering better coverage and widened scope of published research as noted by Olawumi and Chan (2018), in context of sustainability research, as well as other research fields (Aryadoust et al. 2019). This database provides requisite metadata essential for conducting an effective scientometric analysis (Carvalho et al. 2013).

-

Step 2: Keyword strategy

A valid and representative keyword string formation was essential to retrieve relevant articles from the research field. Thus, pre-reading of the SR domain was undertaken to arrive at relevant and effective keywords to collect quality data. Reading exercise revealed multiple terminologies used interchangeably for SR. Targeted Boolean keyword search string used for the present study was.

Use of inverted commas and avoidance of the fuzzy term “*” was made to lower data contamination and generate more focused results.

-

Step 3: Defining the inclusion/exclusion criteria

A well-defined inclusion/exclusion criterion eliminated research bias and enhanced the objectivity, transparency, and repeatability of the study. According to the present study’s review protocol, a research study was included in the dataset if it was a peer-reviewed journal article published in the English language and related to the field of SR. The other data records containing research in document formats other than articles such as editorials and conference papers, papers published in other languages, and irrelevant studies were outside the scope of this paper.

-

Step 4: data extraction and data cleaning/filtration

The keyword run in WoS (field search limited to “TOPIC”) made without any restriction of time period, yielded 2331 data records, of which post-filtering for “article” document type published in English led to 2109 journal documents. Relevancy checks were undertaken at different stages, as shown in the PRISMA flow chart in Fig. 4. A data record of 1434 articles spanning from 1992 to 2022 was finally selected for the review.

-

Step 5: Data analytical tool

CiteSpace version 5.6.R5 (64 bit) scientometric software developed by Chaomei Chen was used to analyze retrieved indexed research corpus. CiteSpace offers a practical tool for detailed analysis of a research field with its innovative combination of computational and visualization techniques that enabled qualitative and quantitative mapping of the knowledge domain. This scientometric tool offers greater clarity and interpretability of visualizations compared to previous visualization tools (Chen 2006).

Visualizations, data analysis, and research results

Before delving into the specifics of each network and associated analysis, it is important to understand the meaning of temporal and structural metrics used and specific software properties and criteria applied for the conduct of the study. These have been detailed in Appendices 1 and 2 respectively.

The LBY (look back years) and LRY (link retaining factor) were set to − 1 for this study implying that all references cited in each of the selected 1434 bibliographic records were considered and all the links to a node in the network were retained respectively. The percentage of nodes to label e was set at 5%. One-year time slicing was used, and the top N = 50 was selected. This meant that the 50 most cited items from each year were selected to construct the visualization networks in this paper. Chen (2014) suggested “Pathfinder” as a theoretically better choice for removing excessive and redundant links from the network. Hence, it was used for pruning the merged network for better visualization outputs.

Annual scientific production (response to RQ1.1)

To analyze research trends of the SR field, annual distribution of 1434 bibliographic records from 1992–2022 was summarized in Fig. 5. First paper on SR was published in 1992 advocating the role of green reporting for controlling and possibly reducing pollution caused by corporate activities (Huizing and Carel Dekker 1992). The year 2010 marked the beginning of an increasing trend in publications in SR, with an annual average growth rate approximated to 27.56%. A total of 79.64% of total publications were published during 2015–2022. Rising trend and recency of the publications signal the surging interest in SR.

Annual scientific production (1992–2022)

Dual-map overlay of disciplines and network of co-occurring subject categories (response to RQ1.2)

A publication portfolio analysis was conducted by constructing a dual-map overlay, and the spread of sustainability reporting literature across specific subject categories was gauged by building a network of co-occurring subject categories based on the collected 1434 WoS bibliographic records.

A dual-map overlay provides a macroscopic view of the disciplines of the journals in which the articles are published along with the disciplines of the journals of cited articles of each publication in the dataset (Chen et al. 2014). The generated overlay map of the dataset was superimposed on a global basemap of scientific literature embedded in CiteSpace as shown in Fig. 6. The left pane of the basemap illustrates the network of the citing journals’ disciplines, and the right pane of the basemap exhibits the network of the cited journals’ disciplines. The thick blue-cyan curves at the bottom of the overlay map suggest that sustainability reporting literature is majorly published in the disciplines of social sciences, economics, psychology, politics, and education. There are research studies in other disciplines as well, but the number remains relatively small.

A dual-map overlay of sustainability reporting literature

Each publication in the WoS dataset is assigned one or more subject categories based on the scope of the journal in which it is published. Network of co-occurring subject categories was produced which generated 43 nodes and 72 links as depicted in Fig. 7. The modularity (Q) is 0.7469 and the mean silhouette value (S) stood at 0.961. The node size represents the count of articles within each subject category as defined by the Web of Science database. The links provide insights into the structure and patterns of research areas, helping researchers understand the interdisciplinary connections, knowledge diffusion, and trends within a particular field. When two subjects frequently appear together in publications, a link is established between them, indicating a relationship or similarity in terms of the research topics they cover. Out of a total of 60 identified subject categories, six (6) subject categories emerged dominant with more than 200 publications: business (333 articles), management (322 articles), environmental studies (317), green sustainable science technology (275), business finance (243), and environmental sciences (207). Other subject areas producing increasing publications in this field include ethics, environmental engineering, economics, and public administration. A citation frequency count of more than 300 was observed in 5 categories: business and economics (frequency = 662), environmental sciences and technology (410), business (332), management (318), and environmental studies (314).

Network of co-occurring WoS subject categories

Interdisciplinarity of this research field is evident from studies in numerous other subject areas including hospitality, leisure, sports tourism, development studies, ecology, communication, law, operations research and management science, biodiversity conservation, energy and fuels, international relations, and regional and urban planning. A probe into the agenda of these multidisciplinary studies revealed advocacy of adoption of sustainability reporting as a means of mitigating environmental damage (Alazzani and Wan-Hussin 2013), fostering investment efficiency (Anwar and Malik 2020), improving firm performance (Assaf et al. 2012; Hongming et al. 2020), building a trustworthy corporate reputation (Fuoli 2018), facilitating smooth running of capital markets (Garrido-Miralles et al. 2016), improving global environmental management (Kareiva et al. 2015), and promoting human rights (Martin-Ortega and Hoekstra 2019) among others. Other objectives of these studies included investigating if sustainability disclosures mirror company’s actual sustainability practices and strategy or remain mere legitimacy tools (Junior 2017), studying sustainability reporting practices of specific industries (Kennedy Nyahunzvi 2013) and countries (Hąbek 2014), and identifying the determinants of sustainability disclosures (Greco et al. 2012) and materiality assessments (Guix et al. 2019). It is clear that research on sustainability reporting crosses disciplinary boundaries and subject areas due to its importance as a key instrument for establishing accountability across a range of sectors and nations.

Citation bursts, centrality scores, and sigma values

The burstness of subject categories is useful in the revelation of the most active research areas in the development of the field (Chen et al. 2014). Strong citation bursts were identified in six subject categories: ethics (burst strength = 10.19; 2003–2010), business (10.03; 2000–2010), social sciences—other topics (8.55; 2003–2009), environmental engineering (7.83; 2015–2016), business and economics (7.07; 2000–2008), and business and finance (6.55; 2014–2015). High betweenness centrality as represented by purple trims in the network was observed in six subject categories: environmental engineering (centrality = 1.18), environmental sciences (1.16), economics (1.03), engineering (0.97), environmental studies (0.9), business (0.79), and management (0.79). It is important to note here that there are categories such as environmental engineering, economics, and engineering which have high centrality but comparatively low-frequency values. This implies that sustainability reporting articles are not sporadically present in various categories. Instead, there are well-established journals and researchers publishing in this domain. Also, high sigma values of ∑ = 441.57 and ∑ = 336.07 were observed in environmental engineering and business categories respectively indicating the publication of novel research on sustainability reporting in these subjects.

Network of countries and institutions (response to RQ1.3)

A research power network was generated based on the scholarly contributions made by countries and institutions to map the geographical distribution of research manuscripts of this field along with conducting an affiliation analysis as shown in Fig. 8. The produced network contained 174 nodes and 232 links with a density, modularity, and mean silhouette score of 0.0154, 0.805, and 0.9383 respectively. The low-density score suggested that although there were various nodes in the network, very close connections between the nodes were not established. The simultaneous selection of the “country” node and the “institution” node in the CiteSpace software yielded this network where the node size denotes the total article production by a particular country/institution (Zhao 2017).

Network of countries and institutions

Out of a total of 79 countries, 10 pioneering countries were identified as research hubs as depicted in Table 4. European countries emerged as dominant contributors to this field followed by Australia and USA. People’s Republic of China was the only Asian country with significant studies in the domain. The quantum of article production from these regions is a testimony to the advancement of this research area in these countries. Country analysis revealed an evident need for more sustainability reporting–themed studies from the Asian and South American continents. Presently, globalization with respect to the adoption of sustainability reporting practices, standardization of approach, and localization of thought are the three major imperatives needed to foster the agenda of this research field. It is thus essential for academicians, industry leaders, and political lobbies across the world to come together to promote research in this area to make reporting on sustainability standardized, meaningful, and purposeful for all stakeholders.

Furthermore, ten (10) institutions with considerable research activity as per the indexed research corpus were also identified as shown in Table 5. University of Salamanca and University of Pretoria both with frequency values of 19 each appeared as eminent publication centers around the world. The frequency analysis of this network is based on the title words of the total institutes recognized as contributors to the field (Niazi and Hussain 2011).

Citation bursts, centrality scores, and sigma values

Strong citation bursts visually portrayed by red nodes in the network were observed in countries such as the USA (burst strength = 9.20, 2005–2012), France (burst strength = 4.65, 2015–2016), Switzerland (burst strength = 4.44, 2016–2017), Australia (burst strength = 4.32, 2005–2009), and Canada (burst strength = 4.31, 2000–2012) and at institutions such as University of South Australia (burst strength = 4.84, 2011–2015), University of Amsterdam (burst strength = 3.31, 2010–2011), Monash University (burst strength = 3.22, 2013–2015), University of Leeds (burst strength = 2.87, 2011–2015), and University of Granada (burst strength = 2.72, 2013–2015).

Five (5) country nodes exhibited high betweenness centrality of 7.0 and above, represented by purple rings in the network: Netherlands (centrality = 1.07), Portugal (1.01), England (0.84), Canada (0.78), and Australia (0.72). At the institution node level, 5 institutions received a centrality score of 0.02 each: University of Pretoria, Macquarie University, University of Waikato, RMIT University, and Wuhan University. These region and institution nodes are key focal points that play a pivotal role by acting as key exchange platforms for research in this field (Olawumi and Chan 2018). Additionally, USA and Netherlands with high sigma (∑) values of 26.84 and 22.09 respectively in the country category and University of Pretoria and Macquarie University with high sigma (∑) values of 1.09 and 1.06 respectively in the institution category represent nodes that produced high-quality novel academic research in the field.

Co-authorship network (response to RQ1.4)

Co-authorship implies research collaboration between two or more researchers who come together for a common project jointly reporting research results on a topic. Co-authorship network is a social network of a research field, identifying the structure of academic societies within it (Savić et al. 2019). Selection of the “author” node in CiteSpace software generated a network of co-authorships in the SR field with 129 nodes (total number of researchers with top published papers) and 91 links (total number of co-authored relationships) as per Fig. 9. The density of the network was 0.011, while the modularity (Q) and the mean silhouette (S) values which defined the overall structural properties of the network stood at 0.9519 and 0.5246 respectively implying a loosely connected co-author network with significant sparseness, as can clearly be seen in the visualization. It can be concluded that even though researchers have co-authored in this field, the overall intensity of co-operations among all the authors is weak and lacks interconnectivity.

Co-authorship network

The sustainability reporting sector was found characterized by coherent linkages between particular co-authorship sub-communities but minimal or negligible interactions among the nearby nodes, indicating a strongly concentrated but poorly globalized SR research community. The members in the network exhibited a low tendency toward forming various other clusters indicating repeat collaborations among the same set of researchers only. Also, two-authored and three-authored associations were the most common type of research coalitions found in the network.

The color of the links in the network signifies the time of formation of collaboration among the researchers. The gray, purple, and blue links indicate old co-authorships and the green for middle-year collaborations, whereas the yellowish, orangish, and reddish colors are for relatively more recent author co-operations. The thickness of the links between the members indicates the strength of the connection between them.

The top authors who garnered high citation frequencies by collaborating with peer researchers in the network were identified: Warren Maroun (frequency = 13) (author’s country: South Africa), Isabel-Maria Garcia-Sanchez (11) (Spain), Charl De Villiers (10) (New Zealand), John Dumay (9) (Australia), Nicola Raimo (8) (Italy), Filippo Vitolla (8) (Italy), Michele Rubino (8) (Italy), Lazaro Rodriguez-Ariza (6) (Spain), Olivier Boiral (5) (Canada), Charles H. Cho (5) (UK), and Merve Kilic (5) (Turkey).

Citation bursts, centrality scores, and sigma values

Author collaboration that received the strongest citation burst of 2.43 belonged to a well-knitted association between three authors namely Nicola Raimo, Filippo Vitolla, and Michele Rubino. Out of the collected 1434 WoS records,15 research studies were found co-authored by them which were themed around aspects of integrated reporting and intellectual capital disclosures. These are recent research articles published between 2018 and 2020, and thus, the links within these researchers are thus represented by red and orange colors. Also, the thickness of the links around these author nodes testified to the strong relationship among them.

Only two authors namely Lazaro Rodriguez-Ariza and Isabel-Maria Garcia-Sanchez observed betweenness centrality, though a small value, of 0.01 each. Investigation of these authors’ publications in the research corpus revealed that both these authors together collaborate with other researchers and are a part of 3 strong co-authoring teams. These are as follows: Jose-Valeriano Frias-Aceituno, Lazaro Rodriguez-Ariza, and Isabel-Maria Garcia-Sanchez; Beatriz Aibar-Guzman, Cristina Aibar-Guzman, Lazaro Rodriguez-Ariza, and Isabel-Maria Garcia-Sanchez; and Maria-Elena Gomez-Miranda, Fatima David, Lazaro Rodriguez-Ariza, and Isabel-Maria Garcia-Sanchez. The formation of the first collaboration relationship is relatively old (indicated by the blue link in the top right of the network), whereas the other two are more recent author associations (represented by the red and orange links).

No single co-authoring sub-community emerged as dominant in terms of creating most novel research studies as a team, and hence, sigma values were observed constant for all.

Network of co-occurring keywords (response to RQ1.5)

Keywords provide an accurate summarization of fundamental information contained in a paper. Keyword co-occurrence analysis helps in identifying the past, present, and emerging trends and topics of a research field. In the WoS database, each publication record contains two types of keywords, namely, author’s keywords and keywords plus. Former keywords are provided by authors in their research papers, while the latter reflects the frequently appearing keywords in the titles of the paper’s cited references generated via a special algorithm unique to Clarivate Analytics.

A network of co-occurring keywords was generated based on both the types of keywords appearing in the 1434 WoS records as presented in Fig. 10, which produced 172 nodes and 283 links with a modularity (Q) of 0.6932 and a mean silhouette (S) of 0.7927. The density of the network observed at 0.0192 indicated that though there are numerous keywords, the proximity of connections between them is low. The node size (shaped as plus signs) and the font size of each word in the network appeared proportional to the frequency of a keyword appearing in the collected data.

Network of co-occurring keywords

A citation frequency of 100 and above was observed in 13 keywords as per the network summary representing the extensively used terms in the field: “corporate social responsibility” (frequency = 357), “performance” (240), “disclosure” (238), “sustainability reporting” (223), “sustainability” (195), “management” (174), “integrated reporting” (157), “CSR” (155), “determinant” (149), “governance” (129), “legitimacy” (123), “environmental disclosure” (108), and “impact” (103).

Citation bursts, centrality scores, and sigma values

Burst patterns of keywords revealed the active hot topics of a research domain during the corresponding burst years (burst duration). Twenty-seven (27) keywords received strong citation bursts as presented in Fig. 11, represented by red nodes in the visualization. The top 10 keywords with high betweenness centrality include “CSR” (centrality = 0.30), “organization” (0.29), “legitimacy” (0.22), “integrated reporting” (0.21), “institutionalization” (0.20), “corporate” (0.18), “stakeholder” (0.18), “impact” (0.18), “sustainable development” (0.17), and “sustainability” (0.18). These words with purple trims around their nodes in the network connect various topics and have a considerable influence on the development of the field. It is important to note here that words such as “sustainable development,” “sustainability,” “CSR,” “legitimacy,” “integrated reporting,” “management,” and “impact” received both high frequencies and centrality scores. This implied that words are indicative of dominant research themes of the area. Additionally, ten (10) keywords with high sigma values of 1.5 and above were identified: “sustainable development” (∑ = 3.87), “business” (1.99), “institutionalization” (1.97), “corporate” (1.92), “CSR” (1.86), “thinking” (1.57), “stakeholder” (1.53), “ethics” (1.52), “information asymmetry” (1.50), and “perception” (1.50). These keywords with large sigma values indicate association to studies propagating novel research ideas in the field.

Keywords’ citation bursts

Co-citation analysis (response to RQ1.6)

Co-citation analysis assessed the proximity between two items (Niazi and Hussain 2011) by measuring the number of times they were cited together in research studies implying a close relationship between them and the research ideas they aimed to propagate in the domain. Two types of co-citation analysis namely author co-citation analysis (ACA) and document co-citation analysis (DCA) were conducted to identify the most prominent and influential authors and major reference documents of the SR field.

Author co-citation analysis (response to RQ1.6a)

Co-citation analysis of authors maps the frequency with which the scholarly works of two authors are cited together in a publication. Selection of the “cited author” node in the CiteSpace software facilitated this category of analysis.

The network generated from the dataset yielded 359 nodes and 1079 links with a 0.0168 density as shown in Fig. 12. Exhibiting a modularity (Q) of 0.6888 and a mean silhouette score of 0.882, the nodes in the network represent the co-citation frequency of each author, and the links signify the relationships between the authors based on the co-citation frequency.

Author co-citation network

The authors with a co-citation frequency count of 160 and above include Rob Gray (frequency = 391, author’s country: UK), Craig Deegan (338, Australia), KPMG (330, headquarters: Netherlands), Ans Kolk (269, Netherlands), Carol A. Adams (228, UK), Charl de Villiers (208, New Zealand), Brendan O’ Dwyer (202, Netherlands), Charles H. Cho (200, Canada), James Guthrie (175, Australia), Robert Gibson Eccles (169, UK), Dennis M. Patten (167, USA), and Global Reporting Initiative (GRI) (166, headquarters: Netherlands). The diversity in the country affiliations of the highly cited authors indicates that the uptake of sustainability reporting research work has been global. It is important to observe that KPMG which is one of the big four accounting organizations of the world has often been cited in the literature. Upon further investigation, it was found that International Surveys of Corporate Responsibility Reporting conducted and published by KPMG are pioneering works that attract scholarly attention in this field.

Citation bursts, centrality scores, and sigma values

One hundred twenty-two (122) authors received a sudden surge in their article’s citations within a short span of time. Out of these, the top 44 authors with the strongest citation bursts have been displayed in Fig. 13. The top five authors exhibiting high betweenness centrality represented by purple trims in the visualization are Rob Gray (centrality = 0.97) followed by Craig Deegan (0.58), Ans Kolk (0.53), Carol A. Adams (0.43), and John Elkington (0.27). Carol A. Adams received the highest sigma value in the network (∑ = 3.07) followed by Dave Owen (3.06), Robin W. Roberts (2.85), Dennis M. Patten (2.50), and James Guthrie (1.68). These authors’ sigma values signify the novelty of research studies published by these authors.

Top 44 strongest authors’ citation bursts

From the above analysis, it is evident that Professor Rob Gray has played a pioneering role in the development of this field. His path-breaking research published in myriad journals has been cited over 33,000 times to date. Additionally, the research works of the other leading authors discussed in this section deserve extensive study as they are the thought leaders of this research field who have made notable contributions and have had significant impacts in shaping the research realm of sustainability reporting.

Document co-citation analysis (response to RQ1.6b)

Document co-citation analysis facilitates the mapping of the intellectual structure of the sustainability reporting research field through a network of cited references of the 1434 bibliographic records in the dataset. This analysis assesses the quantity as well as the authority of references cited by documents in the dataset (Zhao 2017). The frequency with which two articles are cited together by other articles in the research corpus is represented by the links in the document co-citation network. Each node in the network represents a cited document marked with the name of the first author and the year of publication. Fixing the node type to “reference” in the CiteSpace software outputs this category of analysis.

The document co-citation network of the dataset generated 392 nodes and 1401 links with a density of 0.0183 as depicted in Fig. 14. The network had a modularity (Q) of 0.6617 and a mean silhouette (S) of 0.6946. Eleven (11) co-cited documents with 90 or more co-citation counts were observed: Gray et al. (1995) (frequency = 152), Deegan (2002) (141), DiMaggio and Powell (1983) (128), Freeman (1984) (127), Suchman (1995) (124), Clarkson et al. (2008) (frequency = 120), Simnett et al. (2009) (115), Hahn and Kühnen (2013) (109), de Villiers et al. (2014) (100), Cho and Patten (2007) (99), and Flower (2015) (90).

Document co-citation network

The content analysis of the top 10 highly cited references as per the WoS citation metric was performed to assess the themes of these papers as presented in Table 6.

Citation bursts, centrality scores, and sigma values

A total list of twenty-eight references was generated from the dataset which demonstrated strong citation bursts each with a minimum burst duration of 2 years as depicted in Fig. 15. The red rings in the network represent the document citation bursts. It is worthy to note here that the first citation burst in the case of both document citation bursts (Fig. 15) and keyword citation bursts (Fig. 11) was observed in the year 2000. The year 2000 which also marks the year in which the first version of GRI reporting guidelines (G1) was published signifies the year of the beginning of scholarly research attention in this research field. The top three documents with the strongest burst strengths were: de Villiers et al. (2014) (burst strength = 16.97, burst duration = 2018–2020), Flower (2015) (16.35, 2017–2020), and Hahn and Kühnen (2013) (13.53, 2016–2020). Gray et al. (1996) (burst duration: 2000–2008), Elkington (1997) (2006–2012), and Deegan and Gordon (1996) (2008–2014) represented the top three documents with the longest burst durations.

Top 28 references with the strongest citation bursts

Documents with high betweenness centrality represented by the purple rings in the network in Fig. 14. are Roberts (1992) (centrality = 0.37), Eccles and Krzus (2010) (0.25), Adams (2015) (0.15), Prado-Lorenzo et al. (2009) (0.14), and Lamberton (2005) (0.13). These documents with high centrality signified influential research papers in the field.

The documents with sigma values of 14 and above in the dataset represent the novel research studies of the field: Roberts (1992) (∑ = 18.74), Adams (2015) (16.93), Flower (2015) (15.10), and Gray et al. (1995) (14.48).

Clustering analysis (response to RQ2)

Clustering facilitates the grouping of large data into small representative units, each of which indicates a common research theme or topic of the field. The members of each cluster are related to each other and are significantly different from the components of other clusters.

CiteSpace software decomposes large datasets into manageable clusters using three alternative algorithms: tf*idf (term frequency–inverse document frequency) (Salton et al. 1975) alternatively termed as latent semantic indexing (LSI), log-likelihood ratio (LLR) tests (Dunning 1993), and mutual information (MI). The keyword and document clustering analysis of this study are based on the LLR clustering algorithm which details the uniqueness of each cluster (Chen et al. 2010). The software specifies the size, silhouette value, and mean year of each cluster in the network. The size indicates the number of members constituting a cluster, while the mean year spells out whether the cluster is formed from recent or old research papers by stating the average year of publication of an individual cluster. The silhouette value ranges from 0 to 1 and indicates the homogeneity of a cluster, where the highest value of 1 signifies perfect consistency among the members. Furthermore, when the network generating the clusters exhibits a high silhouette value coupled with a relatively high modularity score, clustering is deemed appropriate and is considered to produce useful analysis. The visualizations of clustering analysis in this paper use a multi-colored approach wherein each cluster shaped in the form of a convex hull and cluster label is represented by a unique color with the label size being proportional to the size of the cluster.

Keyword clustering analysis (response to RQ2a)

Descriptive analysis

Eleven (11) clusters were identified through the LLR algorithm based on both authors’ keywords and keyword plus of the 1434 WoS publication records as shown in Fig. 16. The individual cluster silhouette values range between 0.735 and 1 indicating high internal homogeneity of clusters. The high mean silhouette and modularity scores of the entire cluster network at S = 0.7927 and Q = 0.6932 respectively imply that the analysis of the generated clustering will be useful thereby producing valid results. The properties of each cluster have been detailed in Table 7. The size of clusters ranges between 10 and 22 constituents. The mean year column shows that clusters #8 and #9 are membered by relatively recent publications (2015–2016) compared to other clusters (2010–2013).

Keywords’ cluster network

Identification of cluster themes

Cluster label and top terms (LLR) of each cluster were indicative of a particular theme or issue of SR. Inter-relationships between keywords of each cluster were identified to understand the underpinning themes of these terms in context to the SR domain. Cluster #0 keywords pointed toward conceiving access to credible sustainability information from a rights-based perspective. Cluster #1 keywords are themed around a common concern of mismatch between words and actions of corporates wherein significant differences are usually observed in claims and commitments made in sustainability reports vis-à-vis actual operational levels of corporate responsibility and sustainability within a firm. Cluster #2 is related to the application of agency theory in gauging the effect of managerial attitudes and board characteristics on the adoption, extent, and quality of SR. Label of cluster #3 termed AIS-SEA design stands for accounting information systems—social and environmental accounting, highlighting the need for building high-quality information systems by means of dialogic engagement to effectively meet the needs of multiple stakeholders eyeing SR. Cluster #4 referred to the institutional pressures firms face to issue a sustainability report, while cluster #5 emphasized the role of quality sustainability disclosures in boosting social performance and the image of the organization. Cluster #6 keywords referred to case studies in the domain involving content analysis of linguistic and visual rhetoric of reports often concluding uptake of sustainability reports as a means for gaining legitimacy or managing a crisis. Cluster #7 related to private and public firm comparison studies aimed at understanding the motivations of each to publish a sustainability report. Information asymmetry appeared to be a dominant factor affecting the decision to publish possibly due to intense non-owner stakeholders’ pressure. Cluster #8 related to research aimed at exploring possible linkages between the ownership structure of a firm and the quantum and quality of sustainability disclosures, while cluster #9 emphasized the need for assurance of sustainability reports for more valid and credible disclosures. Cluster #10 keywords thread toward research studies which link ESG disclosures and environment-friendly actions of a firm, highlighting the need for obligatory pressures or formalized systems of reporting for standardization in industries in which only a few firms voluntarily and pro-actively report on environmental social and governance issues.

Document clustering analysis (response to RQ2b)

Descriptive analysis

The decomposition of the document co-citation network resulted in the formation of twelve (12) salient clusters consisting of related references that represent a common research theme as depicted in Fig. 17. The document clustering analysis shall generate reliable results as the network in entirety exhibits reasonable modularity at Q = 0.6617 and a mean silhouette score of S = 0.6946. The cluster members show satisfactory internal consistency among them with individual cluster silhouette values ranging between 0.608 and 0.95 as observed in the cluster summary detailed in Table 8. Cluster #0 with 55 references represents the largest cluster of the network constituted by cited papers published between 1991 and 2018. Cluster #3 with an average year of publication in 2013 is formed by relatively recent publications compared to others in the network.

Document co-citation clusters

Identification of cluster themes

The research theme of a document co-citation cluster is deduced from the representative document which is essentially the research reference with the highest observed co-citation frequency within each cluster. The representative document of cluster #0 labeled “environmental performance accountability” was published by Lamberton (2005) who emphasized the need for comprehensive reporting on sustainability as a means of holding organizations accountable for their continuing unsustainable activities. He further pointed out that organizations usually have a tendency to escape such reporting models as their widespread adoption and implementation call for significant resource commitments. Cluster #1 is themed around a research paper titled “Corporate social reporting for different audiences: the case of multinational corporations in Spain” (Sotorrío and Sánchez 2010) which observed significant differences in social reporting policies of MNCs with respect to global and local audiences. The study identified company visibility and resources as the explanatory factors for the differing degrees of disclosures. Cluster #2 labeled “corporate sustainability” is represented by a research paper published in 2013 by Markus J. Milne and Rob Gray (Milne and Gray 2013), who critiqued the sustainability reporting approaches and practices whereby corporate sustainability has become synonymous with just the act of incorporating ESG metrics into reporting models. This functional approach has defeated the purpose of sustainability reporting which aims to awaken genuine ecological concern within the corporates. According to the authors, focus on just the triple bottom line approach (people, planet, and profits) as a congener to corporate sustainability and its institutionalization and reinforcement by the Global Reporting Initiative (GRI) reporting guidelines fails to push businesses to re-frame unsustainable business models. The representative document of cluster #3 is by Daub (2007) which proposed a comprehensive and novel methodological approach to effectively assess the quality of sustainability reports. Two representative documents each with a co-citation frequency of 63 were observed within cluster #4. The research study authored by Clarkson et al. (2008) empirically investigated the relationship between environmental performance and environmental disclosures and observed a positive association between them, while the second study published by Michelon et al. (2015) empirically tested the connection between CSR reporting practices and quality of disclosures concluding the symbolic use of sustainability-based reporting tools. Cluster #5 is themed around the representative paper titled “Assurance on Sustainability Reports: An International Comparison” (Simnett et al. 2009) which analyzed the assurance practices in 31 countries and found that companies aiming to build a good corporate image are more likely to adopt assurance for enhancing the credibility of their reports. The representative document of cluster #6 Churet and Eccles (2014) linked integrated reporting practices to enhanced quality of ESG management over the long term. The representative study of cluster #7 Fifka (2013) investigated the empirical literature on the determinants of corporate responsibility reporting categorizing them according to geographical origin while that of cluster #8 assessed the non-financial reports of Greek companies suggesting room for improvement in reporting practices for better stakeholder engagement. Cluster #9 is based on the representative document by Tschopp and Huefner (2015) which compared the evolution of the CSR reporting field vis-à-vis the financial reporting field. The representative document of cluster #10 Brown et al. (2009) examined the trajectory of successful institutionalization of GRI questioning the power of “commodified” information to mobilize and empower civil society members. Cluster #11 is themed around the research study by Clarkson et al. (2011) which emphasized the need for mandatory reporting regimes and regulatory policy for more meaningful environmental disclosures.

Future research avenues (response to RQ3)

Based on our findings, certain research gaps were observed which could provide useful impetus for fostering more purposeful and fruitful future research work in SR. A dearth of SR research studies was observed in developing countries particularly in Asian and South American continents. With current field agendas centering around the globalization of SR practices, standardization of reporting approaches, and localization of efforts for SR implementation, it is essential for academicians, industry leaders, and political lobbies across the globe to come together to promote meaningful research in this area.

While strong niche author collaborations were observed, overall interconnectedness within the entire global academic community producing SR-themed studies was lacking. Therefore, global academic conferences and author meets centered exclusively on SR research themes should be encouraged. Additionally, future research coalitions between authors of developed and developing worlds could lead to the production of more global multi-perspective research work, helping to understand the implementation challenges of varied regions. Academic research of this nature would be useful for practitioners, governments, policymakers, and other stakeholders to address relevant issues and advance the field.

Based on the assessment of 1434 bibliometric records and 60 domain-based literature reviews coupled with the clustering and content analysis conducted in the present study, specific relevant research themes were identified, as detailed in Table 9.

Conclusions and implications of the study

Main research findings

The rising number of global sustainability fallouts has heightened the need to establish business accountability for the limited planetary resources. Over the years, SR has emerged as a vital tool to foster the agenda of embedding sustainability as a core value necessary for both the survival and success of any business. SR domain has witnessed marked growth with increasing advocacy and understanding of ESG issues among various stakeholders.

Our scientometric review was based on 1434 relevant research studies retrieved from WoS spanning 1992–2022; using CiteSpace software (V 5.6.R5) provides an in-depth, holistic overview of the SR field. Varied domain knowledge networks and powerful visualizations were generated, and associated metrics, namely, citation bursts, centrality values, modularity scores, mean silhouettes, network densities, number of network links, and nodes, were analyzed to provide a meaningful synthesis and snapshot of the area.

Annual scientific production plots revealed an increasing publication trend in studies pertaining to the SR field. Of the total publications, 79.64% were published between 2015 and 2022 indicating that the academic interest in this field is recent and will continue to fuel in the future. The publication portfolio analysis portrayed by a dual-map overlay revealed the dominance of sustainability reporting literature in the social sciences, economics, psychology, politics, and education disciplines. The network of subject categories revealed six dominant subject categories with more than 200 publications: business (333 articles), management (322 articles), environmental studies (317 articles), green sustainable science technology (275 articles), business finance (243 articles), and environmental sciences (207 articles). Several interdisciplinary studies have evidenced the pervasiveness of propaganda for sustainability reporting across various academic research communities.

A network of countries and institutions indicated the origin of the majority of research work from EU, followed by Australia and the USA. China was the only Asian country with significant studies on SR. University of Salamanca, Macquarie University, University of Pretoria, University of Witwatersrand, and University of Auckland emerged as the most productive institutions contributing to the SR research domain. The co-authorship network revealed cohesive relationships between individual co-authorship sub-communities but weak overall intensity in cooperation among the global academic community working on SR. Two- and three-author associations were the most common forms of research coalitions observed. Keywords “sustainable development,” “sustainability,” “CSR,” “legitimacy,” “integrated reporting,” “management,” and “impact” received high frequencies and centrality scores indicating central research topics of SR.

Rob Gray, Warren Maroun, Charl de Villiers, Craig Deegan, Ans Kolk, Carol A. Adams, Brendan O’ Dwyer, Charles H. Cho, James Guthrie, Robert Gibson Eccles, Dennis M. Patten, GRI, and KPMG with high-frequency counts emerged as prime thought leaders as observed in author co-citation analysis. The diversity in the country affiliations of authors testified to the global uptake of sustainability reporting research work.

Documents by Gray et al. (1995) and Deegan (2002) received high co-citation frequencies, while Dhaliwal et al. (2011) and Clarkson et al. (2008) were observed as the most highly cited publications. Roberts (1992), Eccles and Krzus (2010), and Adams (2015), with high centrality values, and De Villiers et al. (2014), Flower (2015), and Hahn and Kühnen (2013) represented influential papers with strong citation bursts.

Descriptive and content analyses of both keyword and document clusters were performed to identify the most prominent research themes and emerging research topics of SR. Clustering analysis grouped the research corpus of 1434 data records into 11 keyword representative clusters and 12 document representative clusters. The dominant research themes that surfaced from clustering analyses were the use of rhetoric in reports that considered SR as a mere legitimacy and impression/crisis management tool; assessment of the impact of managerial attitudes and board characteristics on the uptake and quality of reporting; relevance of dialogic engagement with varied stakeholders; prevalent institutional pressures to report; issue of information asymmetry; integrated reporting practices; assurance of sustainability reports; advocacy for mandatory reporting regimes; need for quality and comprehensive disclosures; role of ownership structures in determining adoption, extent, and quality of SR; and exploration of links and differences between actual environmental performance and corresponding disclosures.

Future research focus areas include links between circular economy and SR; the role of social media; the application of blockchain, artificial intelligence, and other digital technologies in SR; attention to the MSME sector, mandatory reporting, assessment of the real impact of SR on investor sentiments, and financial analysts’ valuations, assurance, standardization, financial sector inclusive research, materiality issues; and understanding niche themes of SR inclusive of monothematic reporting.

Implications

This study provides valuable insights for stakeholders including policymakers, firms, society, and academia. It serves as a ready reference for orienting and optimizing new sustainable finance research endeavors (Table 10).

Limitations of the study

This study has several limitations. Firstly, data was retrieved from WoS only, ignoring other databases. Furthermore, only peer-reviewed English-language articles were selected for review. These limitations may be addressed by the inclusivity of more databases, other document types, and studies published in other languages in future research publications. Secondly, choice of keywords, use of fuzzy terms, and differently arranged keyword search strings with other Boolean operators may lead to varying search results. Thus, search query used for data collection by us cannot be concluded as the most comprehensive keyword string for capturing all research studies of SR. Thirdly, scientometric reviews have an intrinsic weakness in measuring the research output in publication counts and citations over the quality of the study. Finally, there is a possibility that the output of the CiteSpace software used in the study may itself be affected by algorithm noise and sampling bias.

Data availability

The datasets generated and/or analyzed during the current study are available from the corresponding author on reasonable request.

References

Abbas YA, Mehmood W, Lazim YY, Aman-Ullah A (2022a) Sustainability reporting and corporate reputation of Malaysian IPO companies. Environ Sci Pollut Res 29(52):78726–78738. https://doi.org/10.1007/s11356-022-21320-9

Abbas YA, Mehmood W, Manhal Aliessa MH, Aman-Ullah A (2022b) Level of sustainability reporting of Malaysian IPO companies. Environ Sci Pollut Res 29(46):69527–69539. https://doi.org/10.1007/s11356-022-20727-8

Abbas YA, Mehmood W, Ali A, Aman-Ullah A (2023) Sustainability reporting and corporate financial performance of IPOs: witnessing emerging market. Environ Sci Pollut Res. https://doi.org/10.1007/s11356-023-28446-4

Adams CA (2015) The International Integrated Reporting Council: a call to action. Crit Perspect Account 27:23–28. https://doi.org/10.1016/j.cpa.2014.07.001

Adams CA, Larrinaga C (2019) Progress: engaging with organisations in pursuit of improved sustainability accounting and performance. Account, Audit Account J 32(8):2367–2394. https://doi.org/10.1108/AAAJ-03-2018-3399

Adams CA, Larrinaga-González C (2007) Engaging with organisations in pursuit of improved sustainability accounting and performance. Account, Audit Account J 20(3):333–355. https://doi.org/10.1108/09513570710748535

Alazzani A, Wan-Hussin WN (2013) Global Reporting Initiative’s environmental reporting: a study of oil and gas companies. Ecol Ind 32:19–24. https://doi.org/10.1016/j.ecolind.2013.02.019

Aldrich HE, Pfeffer J (1976) Environments of organizations. Ann Rev Sociol 2:79–105. https://doi.org/10.1146/annurev.so.02.080176.000455

Alewine HC (2010) A model for conducting experimental environmental accounting research. Sustain Account, Manag Policy J 1(2):256–291. https://doi.org/10.1108/20408021011089275

Ali W, Frynas JG, Mahmood Z (2017) Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: a literature review: determinants of CSR disclosure. Corp Soc Responsib Environ Manag 24(4):273–294. https://doi.org/10.1002/csr.1410

Al-Tuwaijri SA, Christensen TE, Hughes KE (2004) The relations among environmental disclosure, environmental performance, and economic performance: a simultaneous equations approach. Acc Organ Soc 29(5–6):447–471. https://doi.org/10.1016/S0361-3682(03)00032-1

Anwar R, Malik JA (2020) When does corporate social responsibility disclosure affect investment efficiency? A New answer to an old question. SAGE Open 10(2):215824402093112. https://doi.org/10.1177/2158244020931121

Aryadoust V, Tan HAH, Ng LY (2019) A scientometric review of Rasch measurement: the rise and progress of a specialty. Front Psychol 10:2197. https://doi.org/10.3389/fpsyg.2019.02197

Ascui F, Lovell H (2011) As frames collide: making sense of carbon accounting. Account, Audit Account J 24(8):978–999. https://doi.org/10.1108/09513571111184724

Assaf AG, Josiassen A, Cvelbar LK (2012) Does triple bottom line reporting improve hotel performance? Int J Hosp Manag 31(2):596–600. https://doi.org/10.1016/j.ijhm.2011.08.005

Bakarich KM, Castonguay J“Jack”, O’Brien PE (2020) The use of blockchains to enhance sustainability reporting and assurance*. Account Perspect 19(4):389–412. https://doi.org/10.1111/1911-3838.12241

Baker M, Schaltegger S (2015) Pragmatism and new directions in social and environmental accountability research. Account, Audit Account J 28(2):263–294. https://doi.org/10.1108/AAAJ-08-2012-01079

Bebbington J (1997) Engagement, education and sustainability: a review essay on environmental accounting. Account, Audit Account J 10(3):365–381. https://doi.org/10.1108/09513579710178115

Bebbington J, Brown J, Frame B, Thomson I (2007) Theorizing engagement: the potential of a critical dialogic approach. Account, Audit Account J 20(3):356–381. https://doi.org/10.1108/09513570710748544

Bebbington J, Russell S, Thomson I (2017) Accounting and sustainable development: reflections and propositions. Crit Perspect Account 48:21–34. https://doi.org/10.1016/j.cpa.2017.06.002

Bebbington J, Unerman J, O'Dwyer B (eds) (2014) Sustainability accounting and accountability (2nd ed.). Routledge. https://doi.org/10.4324/9781315848419

Benlemlih M, Shaukat A, Qiu Y, Trojanowski G (2018) Environmental and social disclosures and firm risk. J Bus Ethics 152(3):613–626. https://doi.org/10.1007/s10551-016-3285-5

Benvenuto M, Aufiero C, Viola C (2023) A systematic literature review on the determinants of sustainability reporting systems. Heliyon 9(4):e14893. https://doi.org/10.1016/j.heliyon.2023.e14893

Berthelot S, Cormier D, Magnan M (2003) Environmental disclosure research: review and synthesis. J Account Lit 22:1–44

Bewley K, Li Y (2000) Disclosure of environmental information by Canadian manufacturing companies: a voluntary disclosure perspective. In: Advances in Environmental Accounting & Management, vol. 1. Emerald (MCB UP), pp. 201–226. https://doi.org/10.1016/S1479-3598(00)01011-6

Bosi MK, Lajuni N, Wellfren AC, Lim TS (2022) Sustainability reporting through environmental, social, and governance: a bibliometric review. Sustainability 14(19):12071. https://doi.org/10.3390/su141912071

Botosan CA (1997) Disclosure level and the cost of equity capital. Account Rev 72:323–249

Botosan CA, Plumlee MA (2002) A re-examination of disclosure level and the expected cost of equity capital. J Account Res 40(1):21–40. https://doi.org/10.1111/1475-679X.00037

Brammer S, Pavelin S (2008) Factors influencing the quality of corporate environmental disclosure. Bus Strateg Environ 17:120–136. https://doi.org/10.1002/bse.506

Brooks C, Oikonomou I (2018) The effects of environmental, social and governance disclosures and performance on firm value: a review of the literature in accounting and finance. Br Account Rev 50(1):1–15. https://doi.org/10.1016/j.bar.2017.11.005

Brown HS, de Jong M, Levy DL (2009) Building institutions based on information disclosure: lessons from GRI’s sustainability reporting. J Clean Prod 17(6):571–580. https://doi.org/10.1016/j.jclepro.2008.12.009

Burritt RL, Schaltegger S (2010) Sustainability accounting and reporting: fad or trend? Account, Audit Account J 23(7):829–846. https://doi.org/10.1108/09513571011080144

Carvalho MM, Fleury A, Lopes AP (2013) An overview of the literature on technology roadmapping (TRM): contributions and trends. Technol Forecast Soc Chang 80(7):1418–1437. https://doi.org/10.1016/j.techfore.2012.11.008

Ceulemans K, Molderez I, Van Liedekerke L (2015) Sustainability reporting in higher education: a comprehensive review of the recent literature and paths for further research. J Clean Prod 106:127–143. https://doi.org/10.1016/j.jclepro.2014.09.052

Chen C (2006) CiteSpace II: detecting and visualizing emerging trends and transient patterns in scientific literature. J Am Soc Inform Sci Technol 57(3):359–377. https://doi.org/10.1002/asi.20317

Chen JC, Roberts RW (2010) Toward a more coherent understanding of the organization–society relationship: a theoretical consideration for social and environmental accounting research. J Bus Ethics 97(4):651–665. https://doi.org/10.1007/s10551-010-0531-0

Chen C, Song M (2019) Visualizing a field of research: a methodology of systematic scientometric reviews. Plos One 14(10):e0223994. https://doi.org/10.1371/journal.pone.0223994

Chen C, Ibekwe-SanJuan F, Hou J (2010) The structure and dynamics of cocitation clusters: a multiple perspective cocitation analysis. J Am Soc Inf Sci 61(7):1386–1409. https://doi.org/10.1002/asi

Chen C, Dubin R, Kim MC (2014) Emerging trends and new developments in regenerative medicine: a scientometric update (2000–2014). Expert Opin Biol Ther 14(9):1295–1317. https://doi.org/10.1517/14712598.2014.920813

Chen C (2014) The CiteSpace manual. http://cluster.ischool.drexel.edu/~cchen/citespace/CiteSpaceManual.pdf

Cho CH, Patten DM (2007) The role of environmental disclosures as tools of legitimacy: a research note. Acc Organ Soc 32(7–8):639–647. https://doi.org/10.1016/j.aos.2006.09.009

Christ KL, Burritt RL (2017) Supply chain-oriented corporate water accounting: a research agenda. Sustain Account, Manag Policy J 8(2):216–242. https://doi.org/10.1108/SAMPJ-05-2016-0029

Churet C, Eccles RG (2014) Integrated reporting, quality of management, and financial performance. J Appl Corp Financ 26(1):56–64. https://doi.org/10.1111/jacf.12054

Clarkson MBE (1995) A stakeholder framework for analyzing and evaluation of corporate social performance. Acad Manag Rev 20:92–117. https://doi.org/10.5465/amr.1995.9503271994

Clarkson PM, Li Y, Richardson GD, Vasvari FP (2008) Revisiting the relation between environmental performance and environmental disclosure: an empirical analysis. Acc Organ Soc 33(4–5):303–327. https://doi.org/10.1016/j.aos.2007.05.003

Clarkson PM, Overell MB, Chapple L (2011) Environmental reporting and its relation to corporate environmental performance. Abacus 47(1):27–60. https://doi.org/10.1111/j.1467-6281.2011.00330.x

Comoli M, Tettamanzi P, Murgolo M (2023) Accounting for ‘ESG’ under disruptions: a systematic literature network analysis. Sustainability 15(8):6633. https://doi.org/10.3390/su15086633

Conca L, Manta F, Morrone D, Toma P (2020) The impact of direct environmental, social, and governance reporting: empirical evidence in European-listed companies in the agri-food sector. Bus Strateg Environ 30(2):1080–1093. https://doi.org/10.1002/bse.2672

Connelly BL, Hoskisson RE, Tihanyi L, Certo ST (2010) Ownership as a form of corporate governance: ownership as a form of corporate governance. J Manag Stud 47(8):1561–1589. https://doi.org/10.1111/j.1467-6486.2010.00929.x

Cooper SM, Owen DL (2007) Corporate social reporting and stakeholder accountability: the missing link. Acc Organ Soc 32(7–8):649–667

Daub C-H (2007) Assessing the quality of sustainability reporting: an alternative methodological approach. J Clean Prod 15(1):75–85. https://doi.org/10.1016/j.jclepro.2005.08.013

de Villiers C, Rinaldi L, Unerman J (2014) Integrated reporting: insights, gaps and an agenda for future research. Account, Audit Account J 27(7):1042–1067. https://doi.org/10.1108/AAAJ-06-2014-1736

Deegan C (2002) Introduction: The legitimising effect of social and environmental disclosures – a theoretical foundation. Account, Audit Account J 15(3):282–311. https://doi.org/10.1108/09513570210435852

Deegan C (2017) Twenty five years of social and environmental accounting research within critical perspectives of accounting: hits, misses and ways forward. Crit Perspect Account 43:65–87. https://doi.org/10.1016/j.cpa.2016.06.005

Deegan C, Gordon B (1996) A study of the environmental disclosure practices of Australian corporations. Account Bus Res 26(3):187–199. https://doi.org/10.1080/00014788.1996.9729510

Dhaliwal DS, Li OZ, Tsang A, Yang YG (2011) Voluntary nonfinancial disclosure and the cost of equity capital: the initiation of corporate social responsibility reporting. Account Rev 86(1):59–100. https://doi.org/10.2308/accr.00000005

Di Vaio A, Palladino R, Hassan R, Alvino F (2020) Human resources disclosure in the EU Directive 2014/95/EU perspective: a systematic literature review. J Clean Prod 257:120509. https://doi.org/10.1016/j.jclepro.2020.120509

Dienes D, Sassen R, Fischer J (2016) What are the drivers of sustainability reporting? A systematic review. Sustain Account, Manag Policy J 7(2):154–189. https://doi.org/10.1108/SAMPJ-08-2014-0050

DiMaggio PJ, Powell WW (1983) The iron cage revisited: institutional isomorphism and collective rationality in organizational fields. Am Sociol Rev 48(2):147. https://doi.org/10.2307/2095101

Dumay J, Bernardi C, Guthrie J, Demartini P (2016) Integrated reporting: a structured literature review. Account Forum 40(3):166–185. https://doi.org/10.1016/j.accfor.2016.06.001

Dunning T (1993) Accurate methods for the statistics of surprise and coincidence. Comput Linguist 19(1):61–74

Dye R (1985) Disclosure of nonproprietary information. J Account Res 23(1):123–145