Abstract

In a world increasingly threatened by climate change and its associated risks, there’s an urgent need to actively seek solutions for environmental protection and sustainable economic development. Central to this effort is understanding the role of environmental taxes and productive capacities in shaping environmental outcomes. Focusing on countries within the European Economic Area (EEA), this research uses advanced second-generation econometric techniques to examine this relationship. The use of cross-sectional autoregressive distributive lag (CS-ARDL) and dynamic common correlated effects (DCCE) models allows for a robust examination of panel data and provides reliable results. The results reveal an inverted U-shaped relationship, or Environmental Kuznets Curve (EKC), between GDP growth and environmental degradation in the EEA economies. Furthermore, while our data reveal a significant negative correlation between environmental taxes and CO2 emissions, we find that productive capacities have a more significant impact on reducing these emissions. These findings call for further research into the effectiveness of policies to support productive capacities in achieving environmental protection goals in the EEA.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

In the face of escalating global climate change, the need to bridge the gap between existing climate change mitigation policies and the comprehensive efforts needed to meet the temperature targets of the Paris Agreement is more urgent than ever. The Paris Agreement, signed in 2015, emphasizes the critical need to balance economic growth with environmental sustainability. This need has significantly increased the focus of policymakers and researchers alike on the complex relationship between economic development and environmental protection.

The concept of the environmental Kuznets curve (EKC), an inverted U-shaped relationship between pollution and economic development, was first introduced by Grossman and Krueger (1991). This concept has given rise to two different perspectives on the nature of the relationship between the environment and the economy. One perspective argues that environmental regulation increases the cost of pollution control, leading to negative effects on economic growth (Metcalf 2021). Conversely, another perspective argues that an appropriate level of environmental regulation stimulates technological advancement, drives business growth, and offsets the costs of pollution, thereby promoting economic growth (Ward et al. 2019). This latter view is further supported by Porter and Linde (1995), who coined the term “innovation offsets” to describe the potential benefits from implementing eco-innovations.

UNCTAD (2020) describes productive capacities as comprising three main dimensions: productive resources, entrepreneurial capabilities, and production linkages. These elements together determine a nation’s ability to produce goods and services and are influenced by various factors such as education, technology, infrastructure, and institutions. Environmental taxes, which include carbon and pollution taxes, target activities that have a negative impact on the environment. The primary objective of such taxes is to incentivize individuals and firms to adopt more environmentally friendly practices and technologies, while generating revenues that can be reinvested in environmental protection and other public goods (Baumol and Oates 1988; Metcalf 2021).

While the relationship between Gross Domestic Product (GDP) growth, environmental taxes and environmental degradation has been extensively studied, the role of productive capacities in this relationship has received less attention, especially in the context of the European Economic Area (EEA). This is where our study aims to contribute—by providing evidence that productive capacities play a substantial role in reducing CO2 emissions, even more so than environmental taxes. This finding underscores the need for more research on the effectiveness of policies that promote productive capacities in the context of environmental protection in the EEA.

This study attempts to identify EKC in the economies of the EEA, while also considering the influence of environmental taxes and productive capacities on the quality of the environment. We use advanced econometric techniques, including cross-sectional autoregressive distributive lag (CS-ARDL) and dynamic common correlated effects (DCCE), to analyze a data set for the years 2000 to 2018. We additionally use second-generation panel tests to mitigate the potential spurious results caused by cross-sectional dependence and slope heterogeneity. Based on our findings, we then provide policy recommendations aimed at promoting a more sustainable and inclusive economy in the EEA countries.

The paper is organized as follows: “Background and literature review” section presents a literature review focusing on environmental degradation and related control variables. “Data and methodology” section provides the theoretical framework of our study and details the methodology and estimation procedures used. “Empirical results” section reports and interprets the results of our analysis. “Conclusions and policy recommendations” section concludes our research by discussing the main findings and proposing policy recommendations for improving sustainability in the EEA.

Background and literature review

Environmental taxes and environmental degradation

The relationship between environmental taxes, environmental degradation, and economic development has become an increasingly important focus of recent research. Environmental taxes have emerged as powerful tools with the potential to mitigate the negative externalities that economic activities often generate and to foster a culture of environmental sustainability among firms and individuals alike. They are fiscal instruments that balance and interweave policies that promote economic prosperity while ensuring environmental protection, paving the way for sustainable growth (Eurostat 2013; OECD 2019). For a more comprehensive understanding, environmental taxes can be broadly grouped into four areas: energy, transportation, pollution, and natural resources. The origins of these taxes, particularly carbon taxes and emissions trading schemes, including the “tradable pollution permits” introduced in the United States since the 1960s, can be traced back to the seminal work of Pigou (1920) and Coase (1960). These taxes serve multiple purposes: to achieve environmental goals, to incentivize environmentally friendly activities, and to address non-environmental issues. The EEA has demonstrated a remarkable commitment to the application of environmental taxes, with all member states implementing some form of these levies, covering energy, transportation, and pollution. However, the effectiveness of these fiscal instruments in mitigating environmental degradation remains a subject of ongoing debate.

The positive effects of environmental taxes on climate change and pollution reduction have been substantiated in multiple studies. For example, Szasz (2023) found that environmental taxes mitigate carbon footprints and environmental damage in the United States. Doğan et al. (2022) demonstrated that a tax on carbon emissions can significantly reduce emissions and encourage the use of renewable energy sources in G7 countries. These findings are supported by multiple studies conducted across different regions and countries. Studies conducted for OECD countries (Bashir et al. 2020; He et al. 2023), Colombia (Calderón et al. 2016), Asian economies (Chien et al. 2021), Chile (Vera and Sauma 2015), China (Wang et al. 2023a), Latin American and Caribbean countries (Wolde-Rufael and Mulat-Weldemeskel 2022a), and EEA countries (Ghazouani et al. 2020; Liddle and Lung 2010; Neves et al. 2020; Wang et al. 2022; Wolde-Rufael and Mulat-Weldemeskel 2022b) consistently show the positive impact of environmental tax policies on reducing carbon emissions and improving environmental outcomes.

A strand of literature has highlighted the role of environmental taxes in promoting the adoption of clean technologies and reducing pollutant emissions. For example, Xu et al. (2020) found that the implementation of carbon taxes in European countries promoted the use of electric vehicles, which in turn helped reduce carbon emissions in the automotive sector. In addition, Koval et al. (2022) found that green taxes in European countries increased the adoption of environmentally friendly technologies, which subsequently reduced environmental impacts. Aydin and Esen (2018) examined the effect of total environmental taxes on CO2 emissions in 15 European Union (EU) countries and identified a dual effect of reducing emissions and promoting technological innovation and the development of green technologies.

Another stream of studies has focused on the effects of specific types of environmental taxes. Silajdzic and Mehic (2018) investigated the impact of energy and transport taxes on CO2 emissions in ten transition economies from 1995 to 2015, using the panel cointegration method. Their results confirmed the validity of the EKC hypothesis, showing that energy taxes had a significant and positive effect on CO2 emissions. However, transport taxes did not have a similar statistically significant effect.

Despite the broad consensus on the effectiveness of environmental taxes in reducing environmental degradation, concerns have been raised about their potential negative impact on economic growth. For example, Tu et al. (2022) found that the introduction of a tax on carbon emissions significantly improved environmental quality but resulted in substantial reductions in most economic variables. Nevertheless, Depren et al. (2023) argue that the effectiveness of environmental taxes in achieving their intended goals may vary due to several factors. Their study reveals the heterogeneous effects of environmental taxes on CO2 emissions and concludes that the effectiveness of the European carbon tax system varies across countries, despite overall positive results. Similarly, Delgado et al. (2022) point to the complex, context-specific nature of the relationship between environmental taxes and economic growth.

Building on Pearce’s (1991) theory of the “double dividend” effect of environmental taxes, environmental tax revenues could be channeled to reduce existing tax rates. This tax shift suggests that environmental taxes could generate a double benefit, known as the “green” and “blue” dividends. The “green dividend” refers to the environmental benefits, while the "blue dividend" refers to the reduction in the impact of the existing tax system on factors of production such as capital and labor, thereby stimulating job creation and economic growth (Shayanmehr et al. 2023). However, the potential of these taxes to promote renewable energy has yet to be fully explored. As highlighted by Rafique et al. (2022), Alola et al. (2023), Gyamfi et al. (2023), and Shayanmehr et al. (2023), revenue from environmental taxes could be strategically allocated to renewable energy investments, countering the phenomenon of the “green paradox,” where the prospect of reduced demand may lead to increased production of non-renewable energy sources, thereby exacerbating pollution (Sinn 2008). For example, studies by Dogan et al. (2023) argue for the allocation of environmental tax revenues to renewable energy development. They argue that renewable energy sources can significantly reduce emissions and promote sustainable growth, underscoring the need for a deliberate redirection of environmental tax revenues to the renewable energy sector. In addition, an analysis of G7 countries by Wang et al. (2023c) found that environmental tax revenues, if properly allocated, contribute significantly to renewable energy development.

However, the effectiveness of environmental taxes in achieving environmental and economic goals largely depends on their design and implementation. A study by Li and Masui (2019) found that while environmental taxes help reduce emissions of most pollutants, they may have a negative impact on economic growth. This negative outcome could result from increased production costs and damage to international competitiveness associated with these taxes (Mulatu 2018). Further research by Aydin and Esen (2018) suggests that the economic outcomes of environmental taxes in the EU depend on the specific tax design. They found that beyond a certain threshold, the effectiveness of these taxes may deteriorate. Similarly, Chang et al. (2023) found that poorly designed environmental taxes may lead to negative economic outcomes, such as economic contraction or even bankruptcy of firms, ultimately leading to job losses.

Given the dual effects of environmental taxes—both improving environmental quality and potentially contributing to environmental degradation—their impact on ecological footprints in countries with significant renewable energy consumption warrants further study. A comprehensive understanding of the role of environmental taxes requires a nuanced examination of their purpose; whether they serve primarily as genuine environmental interventions or are designed primarily as revenue raising instruments (Karmaker et al. 2021). The conceptualization of environmental taxes as a new resource for the EU further amplifies their potential role in sustainable development (Palenik and Miklosovic 2018). Parry’s (2012) suggestion that environmental taxes can increase government revenues, thereby providing critical funds for investments in clean technologies, underscores this point. Thus, green taxes not only act as a deterrent to environmentally harmful practices, but also generate resources that can be channeled into sustainable innovation. In addition, the management of the revenues generated by environmental taxes plays a key role in their effectiveness as a tool for environmental protection. In general, revenue from environmental taxes is earmarked for specific purposes, following the principle of special funds for special uses. This ensures that the funds raised by taxing environmentally harmful activities are reinvested in initiatives that mitigate environmental damage and support ecological restoration. This perspective is supported by Kombat and Wätzold (2019), who argue that environmental taxes have been successful in mitigating environmental problems in part because a portion of the tax revenue has been specifically earmarked for environmental protection measures. Thus, the true value of environmental taxes lies not only in their ability to discourage harmful environmental practices, but also in their potential as a source of funding for environmental protection and sustainable development initiatives. However, their effectiveness depends on the purpose of these taxes and how their revenues are managed. Therefore, an in-depth analysis of the role, implementation, and management of environmental taxes is needed to better understand their impact on ecological footprints and their potential role in promoting renewable energy consumption.

Environmental taxes therefore play an important role in promoting environmental sustainability and economic growth. However, their effectiveness is influenced by several factors, including the design of the tax, the expected response of non-renewable energy producers, and the strategic use of tax revenues. This complexity underscores the need for policymakers to take these factors into account when designing and implementing environmental tax policies. Continued empirical research is needed to refine these policies and increase their effectiveness in achieving desired environmental and economic outcomes.

Productive capacities and environmental degradation

It is now recognized that pursuit of both economic growth and environmental protection is feasible due to the relationship between productive capacities, environmental degradation, and economic development in the context of climate change. Pursuit of these objectives relies on types of productive capacities, including human capital, natural capital, energy, transport, information and communication technology (ICT), institutions, private sector, and structural change. The United Nations Conference on Trade and Development (UNCTAD) Productive Capacity Index (PCI) provides a framework for comprehensive evaluation and assessment of national productive capacity, including the country’s its capacity to achieve sustainable economic growth while mitigating climate change. This framework captures the various factors that contribute to economic development while taking account also of environmental sustainability.

Human capital, which encompasses a country’s cumulative knowledge, education, health, skills, and training, is widely recognized as the primary input to inclusive production (Ashraf and Javed 2023; Wang et al. 2023b). Studies conducted across different methodologies, time periods, and geographical contexts consistently emphasize the central role of human capital, particularly its educational component, in promoting sustainable practices and mitigating environmental degradation. Saqib et al. (2023) found a significant relationship between human capital enhancement through education and reduced ecological footprint in 16 European countries from 1990 to 2020, while Meyer (2015) and Baiardi and Morana (2021) highlighted the indispensable role of education in cultivating environmental awareness in Europe. Özbay and Duyar (2022) and Ahmad et al. (2023) demonstrated the significant contribution of higher education to CO2 emission reduction in OECD countries from 1997 to 2019 and 1990 to 2018, respectively. Caglar and Askin (2023) examined the impact of economic globalization, human capital, gross capital formation, and total factor productivity on the ecological footprint in the top 10 competitive industrial performance economies for the period 1990–2018, acknowledging potential negative environmental impacts but emphasizing the positive role of renewable energy consumption and human capital. Mehmood (2022), using annual data from 1984–2017 for a group of 11 countries, noted the potential negative effects of financial development, but suggested that these effects could be mitigated by human capital and institutional quality. Çamkaya et al. (2022) showed that human capital has a negative effect on carbon emissions and ecological footprint in Turkey from 1980 to 2018. Liu et al. (2023) highlighted the positive effects of educational attainment, renewable energy consumption, internet use, and financial development on green growth in China from 1991 to 2019. Wang et al. (2023c) tested the EKC hypothesis based on an aggregate dataset of 208 countries from 1990 to 2018, highlighting the importance of trade openness, human capital, renewable energy consumption, and natural resource rent in achieving carbon neutrality globally. They also found that renewable energy consumption has a better emission reduction effect for countries before the EKC inflection point, while human capital has a better emission reduction effect for countries after the inflection point. Wang et al. (2023b) demonstrated the nexus between natural resources, sustainable energy, human capital, and consumption-based carbon emissions in G-7 economies from 1976 to 2020, emphasizing the role of natural resources, clean energy, and human capital in preserving environmental quality. Karaduman (2022) highlighted the negative correlation between economic globalization and human capital with ecological footprint, while emphasizing the positive relationship between GDP per capita and ecological footprint in emerging economies from 1975 to 2017. Despite the differences, these studies collectively confirm the significant and multifaceted role of human capital in achieving environmental sustainability and solidify its position as a vital asset in shaping the inclusive production of our world.

Natural capital includes natural resources and ecosystems and is crucial for sustaining economic growth and human well-being while also providing a wide range of ecosystem services that support human societies. In the EEAs, the depletion and deterioration of natural capital have been identified as among the main causes of environmental degradation (Abbasi et al. 2021; Du et al. 2022; Farrell et al. 2022; Pascual et al. 2017; Schlaepfer and Lawler 2023). Areas such as energy and transport play a crucial role in promoting sustainable development. Numerous studies indicate that utilizing renewable energy sources and developing more efficient transportation systems can result in reduced greenhouse gas emissions (Chu 2022; Dahmani et al. 2021; Dogan et al. 2020; Khan et al. 2022a, b; Saqib et al. 2022). In many economic sectors, ICTs have the power to reduce environmental impact and improve resources efficiency (Ahmad et al. 2023; Dahmani et al. 2023; Dahmani et al. 2022; Park et al. 2018; Wang et al. 2022; Xie et al. 2023). This strand of work highlights how ICTs contribute by reducing CO2 emissions through more efficient use of resources and sustainable consumption and production practices. ICT applications can increase resource use efficiency, reduce waste and emissions, and support the development of sustainable business models. The involvement of the private sector has been identified as important in several studies that highlight the role of corporate social responsibility and environmental management systems for promoting sustainable development (Biró and Szalmáné Csete 2021; Puig et al. 2022). Private sector innovation can contribute to the development of eco-friendly technologies and processes which reduce the effects of production and consumption on the environment. The productive capacity of private sector industries contributes significantly to environmental degradation (e.g., through the substantial greenhouse gas emissions by the transportation sector, Alkhani 2020). Policies that encourage low-carbon transport options have been shown to be effective in reducing these emissions. The manufacturing sector’ also causes environmental degradation; sustainable manufacturing practices have been found to be effective for reducing the impact on the environment (Quintás and Martínez-Senra 2022; Renukappa et al. 2013). In addition, institutions and structural change are important for promoting sustainable development and reducing environmental degradation; several studies show that effective policy and regulatory frameworks can promote green investment and sustainable business practices (Glass and Newig 2019; Le and Ozturk 2020; Wurzel (2016);;. Institutional frameworks can also play a crucial role in facilitating the transition to low-carbon and resource-efficient economies (Bradley 2022; Cifuentes-Faura 2022). Finally, structural change and particularly the shift towards a circular economy can reduce environmental impacts and promote sustainable growth significantly (Calisto Friant et al. 2021; Moberg et al. 2019; Zhao et al. 2022).

Overall, the literature demonstrates the need for transformative changes to productive capacities including both decarbonization and sustainable production and consumption practices, to mitigate the environmental impacts of these systems on climate change. While there is evidence to suggest that some types of productive capacity promote sustainable development, more research is needed to understand their specific effects in the context of the EEA countries.

Data and methodology

Data specification

We use a balanced annual panel dataset covering all EEA countries over the period 2000 to 2018 (see Table 1). The sample countries are Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, and Sweden. The World Development Indicators (2023) provided data for CO2 emissions per capita (CO2_PC) measured in metric tons, and real GDP per capita (GDPC_PC) measured in constant 2015 US dollars, while the UNCTAD (2023) Productive Capacities Index (CPI) was used to measure productive capacities. We obtained the environmentally related tax revenue from the OECD (2023) database, which was defined as a percentage of GDP. The period of analysis was selected based on the availability of complete data for all variables considered.

Model specification and estimation strategy

The objective of this study is to investigate the impact of environmental-related taxes and productive capacities on climate change. The validity of the relationship is tested using the cointegration panel method based on the long-run relationship between the variables of interest and CO2 emissions. The data used for the study come from a relatively heterogeneous region which underlines the need to consider cross-section dependence and heterogeneity. The functional form of the model can be written as follows:

where LCO2_PC is climate change, LERT is environmental-related tax, LPCI is productive capacity index, LGDP_PC is real GDP per capita, GDP2_PC is GDP per capita squared, and ε is the error term.

The econometric methodology consists of five stages. First, we determine the cross-section dependence of the variables using the Pesaran (2015) test for weak cross-section dependence. Second, we test the slope homogeneity of the cointegration coefficients using the delta test developed by Pesaran and Yamagata (2008). Third, we use the cross-section augmented Im, Pesaran and Shin (CIPS) and cross-section augmented Dickey-Fuller (CADF) developed by Pesaran (2007) to ascertain the level of integration of the variables. Fourth, having established the presence of cointegration relationships using the error-correction-based panel cointegration tests developed by Westerlund (2007), to estimate the long-run cointegration coefficients we apply CS-ARDL and DCCE techniques developed by Chudik et al. (2016) and Chudik and Pesaran (2015). Finally, based on the estimation results we test the validity of the EKC hypothesis. The estimation approaches are well-suited to a panel data setting and allow for estimation of both long- and short-run relationships between the variables. The CS-ARDL method accounts for cross-sectional dependence and yields more efficient coefficient estimates; the DCCE approach enables simultaneous estimation of common and individual effects. We compare the results of both approaches to ensure robust results. Both methods account for cross-section dependence and endogeneity which makes them suitable for dynamic panel data models with small numbers of cross-sectional units and relatively short time periods.

Empirical results

Cross-section dependence tests

The initial step in this analysis is to investigate the potential presence of cross-section dependence in the data. Cross-section dependence can arise from various factors such as common shocks, unobserved factors, or spatial dependence which violate the assumption of independence of observations necessary for standard panel data models. To test for cross-section dependence, we apply the Pesaran (2015) test for weak cross-section dependence. This test is based on correlation among the ordinary least square residuals and evaluates the null hypothesis of no cross-section dependence. Rejection of the null hypothesis indicates presence of cross-section dependence in the data which requires more advanced econometric techniques to account for this dependence.

Table 2 presents the results of the Pesaran (2015) test for weak cross-sectional dependence for all the variables included in the panel data model. The results show the existence of cross-section dependence for all variables which implies that the model error terms are correlated across countries. This means that we need to account for cross-section dependence in the estimation process. The nature of cross-section dependency and the degree to which it affects the estimations must be considered when employing panel data models.

Slope homogeneity tests

The second step tests for slope homogeneity of the explanatory variables across different panel dataset units. We employ the Pesaran and Yamagata (2008) delta test which examines whether the coefficients of the explanatory variables are homogeneous across different panel dataset units. This test is designed to determine whether the impacts of the explanatory variables on the different dependent variable units such as countries are consistent. The null hypothesis of the test is that the coefficients are homogeneous, with the alternative hypothesis being that they are heterogeneous. Rejection of the null hypothesis implies that across different countries the explanatory variables have different impacts on the dependent variable, indicating presence of slope heterogeneity.

Table 3 presents the results of the slope homogeneity test for the variables included in the model. In all cases, the probability values of the variables are less than 0.01 which rejects the null hypothesis of slope homogeneity. Thus, the model coefficients are heterogeneous, and the slopes vary from country to country which calls for heterogeneous panel techniques to account for these data differences.

Second-generation unit root test

In the third step of our study, we conducted unit root tests to examine the stationarity of individual series in the panel. Since our selected series suffers from both cross-section dependence and slope heterogeneity, we use a second-generation unit root test whose robustness and validity are well-known. Specifically, we employ second-generation stationary techniques which allow for identification and correction of the unit root problem while accounting also for cross-section dependence and slope heterogeneity. We conducted the CIPS and CADF tests developed by Pesaran (2007); Table 4 reports the results for levels and first differences. Our findings show that LnPCI is a stationary time series at level I(0), while LnCO2_PC, LnGDP_PC, LnGDP2_PC, and LnERT are non-stationary at their levels but become stationary at the first difference I(1).

Panel cointegration tests

The fourth step of the study investigates long run cointegration between variables. Table 5 presents the results of the Westerlund (2007) cointegration tests, which are particularly useful in the presence of heterogeneous slope coefficients and dependence among individual panel data. The null hypothesis assumes no long-term cointegration among variables, while the alternative hypothesis assumes the opposite. The Westerlund (2007) tests revealed that the null hypothesis of non-cointegration can be rejected at both the individual cross-section and panel level, allowing for the estimation of long-term equilibrium relationships between variables.

Panel regression results

Having confirmed the existence of cointegration relationships among the variables, we employ the CS-ARDL and DCCE estimators developed respectively by Chudik et al. (2016) and Chudik and Pesaran (2015), to estimate the long-run cointegration coefficients. These estimators account for cross-section dependence and slope heterogeneity. The CS-ARDL method provides more efficient coefficient estimates while the DCCE approach allows for simultaneous estimation of common and individual effects. Both methods are suited to dynamic panel data models with small numbers of cross-section units and relatively short time periods which makes them appropriate for our study which uses panel data for EEA countries.

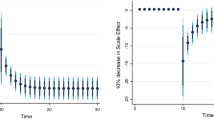

The short-term and long-term results of the CS-ARDL and DCCE models have similar signs and significance but differ slightly in their magnitude (see Table 6). In both models, the error correction term (ECT) ranges from -0.652 to -0.609 indicating that approximately 65.2% and 60.9% of the disequilibrium observed in the previous year was corrected in the current year. Based on the CS-ARDL estimates, the long-run results show that a 1% increase in real GDP per capita leads to a 0.628% increase in CO2 emissions, and that a 1% increase in real GDP per capita squared results in a 0.026% decrease in CO2 emissions. Similarly, in the DCCE model, a 1% increase in real GDP per capita leads to a 0.22% increase in CO2 emissions, while a 1% increase in real GDP per capita squared results in a 0.009% decrease in CO2 emissions. These findings confirm the existence of an EKC in the EEA countries which is consistent with recent research conducted by Bao and Lu (2023) and Simionescu et al. (2022). Chen et al. (2022) also found a positive long-term relationship between economic growth and CO2 emissions for the EEA countries. This relationship is confirmed in Destek et al. (2018) who use a dynamic panel data model to examine the relationship between real income and ecological footprint in 27 EU countries. However, the positive correlation between GDP growth and ecological footprint in EAA countries suggests that the negative impacts of economic growth on the environment might be eased through the implementation of environmental-related taxes and incentives to promote development of productive capacity that responds to environmental issues while also promoting economic growth.

Our analysis, utilizing the CS-ARDL model and DCCE estimator, has revealed a significant negative correlation between productive capacities and CO2 emissions in both short and long-term periods within EEA countries. Specifically, our findings indicate that a 1% rise in productive capacities corresponds with a 0.357% and a 0.308% decrease in overall and per capita CO2 emissions, respectively. This correlation underscores the crucial role of robust productive capacities—characterized by strategic investments in education, renewable energy sources, sustainable transportation infrastructure, digital technologies, and sustainable business practices—in mitigating environmental degradation. In addition, our study revealed a notable inverse relationship between environmental taxes and CO2 emissions. According to the CS-ARDL model, a 1% increment in environmental taxes is associated with a 0.057% reduction in the environmental footprint. This correlation is reinforced by the DCCE model, which shows a 0.048% decrease in CO2 emissions for the same 1% increase in environmental taxes. Interestingly, the coefficient of the productive capacities index exceeds that of environmentally related tax revenue, implying that productive capacities have a more substantial influence on reducing CO2 emissions. This discrepancy could stem from variations in the design and implementation of environmental protection policies and the efficiency of institutions across different EEA economies. These findings not only align with existing research in the field but also underscore the imperative for robust productive capacities and effective environmental policies in reducing CO2 emissions and enhancing environmental quality (as demonstrated in works by Alkhani 2020; Biró and Szalmáné Csete 2021; Bradley 2022; Calisto Friant et al. 2021; Chu 2022; Cifuentes-Faura 2022; Doğan et al. 2022; Du et al. 2022; Ghazouani et al. 2020; Glass and Newig 2019; Le and Ozturk 2020; Moberg et al. 2019; Neves et al. 2020; Oluc et al. 2023; Puig et al. 2022; Quintás and Martínez-Senra 2022; Simionescu et al. 2022; Wang et al. 2022; Wolde-Rufael and Mulat-weldemeskel 2022b; Zhao et al. 2022).

Moreover, our analysis validates the effectiveness of the European Union’s ongoing efforts to minimize pollution transfer and implement carbon tariffs as part of the European Green Deal. Under this initiative, the EU is proactively implementing comprehensive measures, such as the “Fit for 55” package and the Emissions Trading System, to achieve climate neutrality by 2050 (European Parliament 2023). A central element of these efforts is the Carbon Border Adjustment Mechanism, which imposes a carbon levy on imports from countries with less stringent climate regulations, thereby mitigating the risk of carbon leakage.

As a result, it is crucial to consider the economic capacity of nations when designing environmental policies. Countries with robust productive capacities, typically high-income countries, are in a better position to reduce CO2 emissions. At the same time, environmental tax policies can be powerful tools for reducing emissions, although their effectiveness depends on the economic capacity of the countries implementing them. The case of the EU illustrates how such policies can be used, adapted, and strengthened to achieve ambitious environmental goals. Our findings therefore underscore the critical role of environmental taxes and productive capacities in fostering sustainable and inclusive economic transitions, and the need for judicious design and implementation of environmental policies.

Conclusions and policy recommendations

Conclusions

This study aimed to investigate the complex relationships between GDP growth, productive capacities and environmental taxes and their combined effect on environmental quality. To address the methodological challenges, advanced second-generation CS-ARDL and DCCE methods were employed to effectively deal with cross-sectional dependence, slope homogeneity, and endogeneity issues. This robust approach enabled a comprehensive global assessment of the EKC across all 30 EEA countries from 2000 to 2018.

The results confirm the existence of the EKC relationship, suggesting that environmental quality improves once GDP growth reaches a certain threshold. Moreover, a significant negative correlation between environmental taxes and CO2 emissions was observed in both specifications, highlighting the effectiveness of fiscal policy in promoting environmental sustainability. The results also emphasize the crucial role of robust productive capacities in mitigating environmental degradation.

Policy recommendations

Based on these findings, several policy recommendations emerge to balance economic development and environmental sustainability:

First, fostering productive capacities in strategic sectors such as education, renewable energy, sustainable transportation, digital technologies, and sustainable business practices is critical for industrial decarbonization. By incentivizing investment in these sectors, countries can support the development of sustainable infrastructure and encourage the adoption of green technologies.

Second, there is a need to refine environmental tax policies to provide stronger incentives for industries to transition to greener practices while minimizing regressive effects on low-income households. This includes basing minimum tax rates on the actual energy content and environmental performance of fuels and electricity, continuously updating rates based on consumer prices, and broadening the tax base by eliminating exemptions and rebates.

In addition, policymakers should institutionalize and clarify initiatives such as the proposed revision of the Energy Tax Directive as part of the European “Fit for 55” package. The objectives and purpose of this revision should be clearly defined, with a particular focus on encouraging investment in new and innovative green industries and securing green tax revenues. This will facilitate the creation of a green financial system that will drive the transition to a sustainable and inclusive low-carbon economy.

Strengthening institutional capacities is an essential prerequisite for the successful implementation of environmental policies. Policymakers should improve enforcement mechanisms, promote transparency and accountability, and facilitate the sharing of best practices among countries. Improving institutional capacities will enable effective enforcement of environmental regulations and promote the adoption of sustainable practices.

Fostering regional and global cooperation is crucial to addressing the transboundary nature of climate change. Policymakers should encourage cooperation among nations, drawing inspiration from successful initiatives such as the European Green Deal. Refining mechanisms such as the Carbon Border Adjustment Mechanism will help prevent carbon leakage and promote global environmental justice.

Ensuring inclusive and sustainable transitions is paramount. Policymakers should design policies that prevent socio-economic inequalities and protect vulnerable groups during the transition to a low-carbon economy. Providing support, implementing retraining programs and establishing social safety nets for communities heavily dependent on high-carbon industries are critical aspects of this effort.

Promoting green growth through the adoption of green technologies, renewable energy and strong environmental regulations is essential. Policymakers should prioritize investments in sustainable infrastructure, encourage the use of renewable energy sources, and enforce environmentally friendly practices in industry.

Finally, citizen engagement should be strengthened to ensure effective implementation of these policy recommendations. Active citizen participation in energy and environmental development strategies, coupled with increased transparency in energy systems, will foster environmental awareness and promote sustainable practices.

Research limitations and future directions

Despite the significant contributions of this study, it is important to note that the geographical scope of our research is limited to the EEA countries. While this focus provides in-depth insights into the EKC within these countries, it limits the broader applicability of our findings to non-EEA countries with different socio-economic and environmental contexts. In addition, data availability for the variable of productive capacities was restricted to the period 2000–2018, which limits the time span of our analysis.

Future research could broaden the scope by including additional variables such as energy prices, institutional quality, and R&D expenditures to gain a more comprehensive understanding of the dynamics of environmental quality. Studies could also examine variations in environmental degradation and response strategies across countries and time periods. Understanding the gap between policy design and implementation could prove particularly insightful, as this gap can have a significant impact on policy effectiveness.

Data availability

The availability of data and materials is based on personal requests.

References

Abbasi KR, Hussain K, Radulescu M, Ozturk I (2021) Does natural resources depletion and economic growth achieve the carbon neutrality target of the UK? A way forward towards sustainable development. Resour Policy 74:102341. https://doi.org/10.1016/j.resourpol.2021.102341

Ahmad M, Kuldasheva Z, Nasriddinov F, Balbaa ME, Fahlevi M (2023) Is achieving environmental sustainability dependent on information communication technology and globalization? Evidence from selected OECD countries. Environ Technol Innov 31:103178. https://doi.org/10.1016/j.eti.2023.103178

Alkhani R (2020) Understanding Private-Sector Engagement in Sustainable Urban Development and Delivering the Climate Agenda in Northwestern Europe-A Case Study of London and Copenhagen. Sustainability 12(20):8431. https://doi.org/10.3390/su12208431

Alola AA, Muoneke OB, Okere KI, Obekpa HO (2023) Analysing the co-benefit of environmental tax amidst clean energy development in Europe’s largest agrarian economies. J Environ Manag 326:116748. https://doi.org/10.1016/j.jenvman.2022.116748

Ashraf J, Javed A (2023) Food security and environmental degradation: Do institutional quality and human capital make a difference? J Environ Manag 331:117330. https://doi.org/10.1016/j.jenvman.2023.117330

Aydin C, Esen Ö (2018) Reducing CO2 emissions in the EU member states: Do environmental taxes work? J Environ Plan Manag 61(13):2396–2420. https://doi.org/10.1080/09640568.2017.1395731

Baiardi D, Morana C (2021) Climate change awareness: Empirical evidence for the European Union. Energy Econ 96:105163. https://doi.org/10.1016/j.eneco.2021.105163

Bao Z, Lu W (2023) Applicability of the environmental Kuznets curve to construction waste management: A panel analysis of 27 European economies. Resour, Conserv Recycl 188:106667. https://doi.org/10.1016/j.resconrec.2022.106667

Bashir MF, Benjiang MA, Shahbaz M, Jiao Z (2020) The nexus between environmental tax and carbon emissions with the roles of environmental technology and financial development. Plos one 15(11):e0242412. https://doi.org/10.1371/journal.pone.0242412

Baumol WJ, Oates WE (1988) The Theory of Environmental. Policy. https://doi.org/10.1017/cbo9781139173513

Biró K, Szalmáné Csete M (2021) Corporate social responsibility in agribusiness: climate-related empirical findings from Hungary. Environ Dev Sustain 23(4):5674–5694. https://doi.org/10.1007/s10668-020-00838-3

Bradley P (2022) An exploration of institutional approaches in pursuing sustainable development. Sustain Prod Consump 30:623–639. https://doi.org/10.1016/j.spc.2021.12.010

Caglar AE, Askin BE (2023) A path towards green revolution: How do competitive industrial performance and renewable energy consumption influence environmental quality indicators? Renew Energy 205:273–280. https://doi.org/10.1016/j.renene.2023.01.080

Calderón S, Alvarez AC, Loboguerrero AM, Arango S, Calvin K, Kober T, Daenzer K, Fisher-Vanden K (2016) Achieving CO2 reductions in Colombia: Effects of carbon taxes and abatement targets. Energy Econ 56:575–586. https://doi.org/10.1016/j.eneco.2015.05.010

Calisto Friant M, Vermeulen WJV, Salomone R (2021) Analysing European Union circular economy policies: words versus actions. Sustain Prod Consump 27:337–353. https://doi.org/10.1016/j.spc.2020.11.001

Çamkaya S, Karaaslan A, Uçan F (2022) Investigation of the effect of human capital on environmental pollution: empirical evidence from Turkey. Environ Sci Pollut Res 30(9):23925–23937. https://doi.org/10.1007/s11356-022-23923-8

Chang Y, Tian Y, Li G, Pang J (2023) Exploring the economic impacts of carbon tax in China using a dynamic computable general equilibrium model under a perspective of technological progress. J Clean Prod 386:135770. https://doi.org/10.1016/j.jclepro.2022.135770

Chen M, Jiandong W, Saleem H (2022) The role of environmental taxes and stringent environmental policies in attaining the environmental quality: Evidence from OECD and non-OECD countries. Front Environ Sci 10. https://doi.org/10.3389/fenvs.2022.972354

Chien F, Sadiq M, Nawaz MA, Hussain MS, Tran TD, Le Thanh T (2021) A step toward reducing air pollution in top Asian economies: The role of green energy, eco-innovation, and environmental taxes. J Environ Manag 297:113420. https://doi.org/10.1016/j.jenvman.2021.113420

Chu LK (2022) Determinants of ecological footprint in OCED countries: do environmental-related technologies reduce environmental degradation? Environ Sci Pollut Res 29(16):23779–23793. https://doi.org/10.1007/s11356-021-17261-4

Chudik A, Pesaran MH (2015) Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. J Econom 188(2):393–420. https://doi.org/10.1016/j.jeconom.2015.03.007

Chudik A, Mohaddes K, Pesaran MH, Raissi M (2016) Long-Run Effects in Large Heterogeneous Panel Data Models with Cross-Sectionally Correlated Errors. Essays in Honor of Aman Ullah, 85–135. https://doi.org/10.1108/s0731-905320160000036013

Cifuentes-Faura J (2022) European Union policies and their role in combating climate change over the years. Air Qual Atmos Health 15(8):1333–1340. https://doi.org/10.1007/s11869-022-01156-5

Coase RH (1960) The Problem of Social Cost. J Law Econ 3:1–44. https://doi.org/10.1086/466560

Dahmani M, Mabrouki M, Ragni L (2021) Decoupling Analysis of Greenhouse Gas Emissions from Economic Growth: A Case Study of Tunisia. Energies 14(22):7550. https://doi.org/10.3390/en14227550

Dahmani M, Mabrouki M, Ben Youssef A (2022) The Information and Communication Technologies-Economic Growth Nexus in Tunisia: A Cross-Section Dynamic Panel Approach. Montenegrin J Econ 18(2). https://doi.org/10.14254/1800-5845/2022.18-2.14

Dahmani M, Mabrouki M, Ben Youssef A (2023) The ICT, financial development, energy consumption and economic growth nexus in MENA countries: dynamic panel CS-ARDL evidence. Appl Econ 55(10):1114–1128. https://doi.org/10.1080/00036846.2022.2096861

Delgado FJ, Freire-González J, Presno MJ (2022) Environmental taxation in the European Union: Are there common trends? Econ Anal Policy 73:670–682. https://doi.org/10.1016/j.eap.2021.12.019

Depren Ö, Kartal MT, Ayhan F, Kılıç Depren S (2023) Heterogeneous impact of environmental taxes on environmental quality: Tax domain based evidence from the nordic countries by nonparametric quantile approaches. J Environ Manag 329:117031. https://doi.org/10.1016/j.jenvman.2022.117031

Destek MA, Ulucak R, Dogan E (2018) Analyzing the environmental Kuznets curve for the EU countries: the role of ecological footprint. Environ Sci Pollut Res 25(29):29387–29396. https://doi.org/10.1007/s11356-018-2911-4

Dogan E, Altinoz B, Madaleno M, Taskin D (2020) The impact of renewable energy consumption to economic growth: A replication and extension of. Energy Econ 90:104866. https://doi.org/10.1016/j.eneco.2020.104866

Dogan E, Hodžić S, Šikić TF (2023) Do energy and environmental taxes stimulate or inhibit renewable energy deployment in the European Union? Renew Energy 202:1138–1145. https://doi.org/10.1016/j.renene.2022.11.107

Doğan B, Chu LK, Ghosh S, Diep Truong HH, Balsalobre-Lorente D (2022) How environmental taxes and carbon emissions are related in the G7 economies? Renew Energy 187:645–656. https://doi.org/10.1016/j.renene.2022.01.077

Du Q, Wu N, Zhang F, Lei Y, Saeed A (2022) Impact of financial inclusion and human capital on environmental quality: evidence from emerging economies. Environ Sci Pollut Res 29(22):33033–33045. https://doi.org/10.1007/s11356-021-17945-x

European Parliament (2023). Reducing carbon emissions: EU targets and policies. Directorate General for Communication. Ref.: 20180305STO99003. Retrieved from https://www.europarl.europa.eu/pdfs/news/expert/2018/3/story/20180305STO99003/20180305STO99003_en.pdf. Accessed on July 10, 2023

Eurostat (2013) Environmental taxes – a statistical guide. Publications Office of the European Union, Luxembourg. https://doi.org/10.2785/47492

Farrell CA, Aronson J, Daily GC, Hein L, Obst C, Woodworth P, Stout JC (2022) Natural capital approaches: shifting the UN Decade on Ecosystem Restoration from aspiration to reality. Restor Ecol 30(7). https://doi.org/10.1111/rec.v30.710.1111/rec.13613

Ghazouani A, Xia W, Ben Jebli M, Shahzad U (2020) Exploring the Role of Carbon Taxation Policies on CO2 Emissions: Contextual Evidence from Tax Implementation and Non-Implementation European Countries. Sustainability 12(20):8680. https://doi.org/10.3390/su12208680

Glass L-M, Newig J (2019) Governance for achieving the Sustainable Development Goals: How important are participation, policy coherence, reflexivity, adaptation and democratic institutions? Earth Syst Gov 2:100031. https://doi.org/10.1016/j.esg.2019.100031

Grossman G, Krueger A (1991) Environmental Impacts of a North American Free Trade Agreement. https://doi.org/10.3386/w3914

Gyamfi BA, Onifade ST, Erdoğan S, Ali EB (2023) Colligating ecological footprint and economic globalization after COP21: Insights from agricultural value-added and natural resources rents in the E7 economies. Int J Sust Dev World 30(5):500–514. https://doi.org/10.1080/13504509.2023.2166141

He P, Zhang S, Wang L, Ning J (2023) Will environmental taxes help to mitigate climate change? A comparative study based on OECD countries. Econ Anal Policy 78:1440–1464. https://doi.org/10.1016/j.eap.2023.04.032

Karaduman C (2022) The effects of economic globalization and productivity on environmental quality: evidence from newly industrialized countries. Environ Sci Pollut Res 29(1):639–652. https://doi.org/10.1007/s11356-021-15717-1

Karmaker SC, Hosan S, Chapman AJ, Saha BB (2021) The role of environmental taxes on technological innovation. Energy 232:121052. https://doi.org/10.1016/j.energy.2021.121052

Khan SAR, Quddoos MU, Akhtar MH, Rafique A, Hayat M, Gulzar S, Yu Z (2022a) Re-investigating the nexuses of renewable energy, natural resources and transport services: a roadmap towards sustainable development. Environ Sci Pollut Res 29(9):13564–13579. https://doi.org/10.1007/s11356-021-16702-4

Khan Y, Hassan T, Tufail M, Marie M, Imran M, Xiuqin Z (2022b) The nexus between CO2 emissions, human capital, technology transfer, and renewable energy: evidence from Belt and Road countries. Environ Sci Pollut Res 29(39):59816–59834. https://doi.org/10.1007/s11356-022-20020-8

Kombat AM, Wätzold F (2019) The emergence of environmental taxes in Ghana—a public choice analysis. Environ Policy Gov 29(1):46–54. https://doi.org/10.1002/eet.1829. (Portico)

Koval V, Laktionova O, Udovychenko I, Olczak P, Palii S, Prystupa L (2022) Environmental Taxation Assessment on Clean Technologies Reducing Carbon Emissions Cost-Effectively. Sustainability 14(21):14044. https://doi.org/10.3390/su142114044

Le HP, Ozturk I (2020) The impacts of globalization, financial development, government expenditures, and institutional quality on CO2 emissions in the presence of environmental Kuznets curve. Environ Sci Pollut Res 27(18):22680–22697. https://doi.org/10.1007/s11356-020-08812-2

Li G, Masui T (2019) Assessing the impacts of China’s environmental tax using a dynamic computable general equilibrium model. J Clean Prod 208:316–324. https://doi.org/10.1016/j.jclepro.2018.10.016

Liddle B, Lung S (2010) Age-structure, urbanization, and climate change in developed countries: revisiting STIRPAT for disaggregated population and consumption-related environmental impacts. Popul Environ 31(5):317–343. https://doi.org/10.1007/s11111-010-0101-5

Liu D, Wang G, Sun C, Majeed MT, Andlib Z (2023) An analysis of the effects of human capital on green growth: effects and transmission channels. Environ Sci Pollut Res 30(4):10149–10156. https://doi.org/10.1007/s11356-022-22587-8

Mehmood U (2022) Environmental degradation and financial development: do institutional quality and human capital make a difference in G11 nations? Environ Sci Pollut Res 29(25):38017–38025. https://doi.org/10.1007/s11356-022-18825-8

Metcalf GE (2021) Carbon Taxes in Theory and Practice. Annu Rev Resour Econ 13(1):245–265. https://doi.org/10.1146/annurev-resource-102519-113630

Meyer A (2015) Does education increase pro-environmental behavior? Evidence from Europe. Ecol Econ 116:108–121. https://doi.org/10.1016/j.ecolecon.2015.04.018

Moberg KR, Aall C, Dorner F, Reimerson E, Ceron J-P, Sköld B, Sovacool BK, Piana V (2019) Mobility, food and housing: responsibility, individual consumption and demand-side policies in European deep decarbonisation pathways. Energ Effi 12(2):497–519. https://doi.org/10.1007/s12053-018-9708-7

Mulatu A (2018) Environmental regulation and international competitiveness: a critical review. Int J Glob Environ Issues 17(1):41. https://doi.org/10.1504/ijgenvi.2018.10011732

Neves SA, Marques AC, Patrício M (2020) Determinants of CO2 emissions in European Union countries: Does environmental regulation reduce environmental pollution? Econ Anal Policy 68:114–125. https://doi.org/10.1016/j.eap.2020.09.005

OECD (2019) Environmentally related tax revenue accounts: OECD methodological guidelines in line with the SEEA. OECD Publishing, Paris. Retrieved from https://one.oecd.org/document/ENV/EPOC/WPEI(2018)6/REV1/en/pdf. Accessed 19 Feb 2023

OECD (2023) Environmentally related tax revenue. Retrieved from https://stats.oecd.org/Index.aspx?DataSetCode=ERTR. Accessed 19 Feb 2023

Oluc I, Ben Jebli M, Can M, Guzel I, Brusselaers J (2023) The productive capacity and environment: evidence from OECD countries. Environ Sci Pollut Res 30(2):3453–3466. https://doi.org/10.1007/s11356-022-22341-0

Özbay F, Duyar I (2022) Exploring the role of education on environmental quality and renewable energy: Do education levels really matter? Curr Res Environ Sustain 4:100185. https://doi.org/10.1016/j.crsust.2022.100185

Palenik V, Miklosovic T (2018) Concept of Environmental Taxes as EU’s Own Resource and CGE Modelling of its Effects on Slovakia. Ekonomický Časopis/journal of Economics 66(3):268–285

Park Y, Meng F, Baloch MA (2018) The effect of ICT, financial development, growth, and trade openness on CO2 emissions: an empirical analysis. Environ Sci Pollut Res 25(30):30708–30719. https://doi.org/10.1007/s11356-018-3108-6

Parry IWH (2012) Reforming the tax system to promote environmental objectives: An application to Mauritius. Ecol Econ 77:103–112. https://doi.org/10.1016/j.ecolecon.2012.02.014

Pascual U, Balvanera P, Díaz S, Pataki G, Roth E, Stenseke M, Watson RT, Başak Dessane E, Islar M, Kelemen E, Maris V, Quaas M, Subramanian SM, Wittmer H, Adlan A, Ahn S, Al-Hafedh YS, Amankwah E, Asah ST, … Yagi N (2017) Valuing nature’s contributions to people: the IPBES approach. Curr Opin Environ Sustain 26–27, 7–16. https://doi.org/10.1016/j.cosust.2016.12.006

Pearce D (1991) The Role of Carbon Taxes in Adjusting to Global Warming. Econ J 101(407):938. https://doi.org/10.2307/2233865

Pesaran MH (2007) A simple panel unit root test in the presence of cross-section dependence. J Appl Economet 22(2):265–312. https://doi.org/10.1002/jae.951

Pesaran MH (2015) Testing weak cross-sectional dependence in large panels. Economet Rev 34(6–10):1089–1117. https://doi.org/10.1080/07474938.2014.956623

Pesaran MH, Yamagata T (2008) Testing slope homogeneity in large panels. J Econom 142(1):50–93. https://doi.org/10.1016/j.jeconom.2007.05.010

Pigou A (1920) The economics of welfare. Macmillan, London, England

Porter ME, van der Linde C (1995) Toward a New Conception of the Environment-Competitiveness Relationship. J Econ Perspect 9(4):97–118. https://doi.org/10.1257/jep.9.4.97

Puig M, Azarkamand S, Wooldridge C, Selén V, Darbra RM (2022) Insights on the environmental management system of the European port sector. Sci Total Environ 806:150550. https://doi.org/10.1016/j.scitotenv.2021.150550

Quintás MA, Martínez-Senra AI (2022) Are small and medium enterprises defining their business models to reach a symbolic or substantive environmental legitimacy?. J Environ Plan Manag 1–24. https://doi.org/10.1080/09640568.2022.2132476

Rafique MZ, Fareed Z, Ferraz D, Ikram M, Huang S (2022) Exploring the heterogenous impacts of environmental taxes on environmental footprints: An empirical assessment from developed economies. Energy 238:121753. https://doi.org/10.1016/j.energy.2021.121753

Renukappa S, Akintoye A, Egbu C, Goulding J (2013) Carbon emission reduction strategies in the UK industrial sectors: an empirical study. Int J Clim Chang Strat Manag 5(3):304–323. https://doi.org/10.1108/ijccsm-02-2012-0010

Saqib N, Sharif A, Razzaq A, Usman M (2022) Integration of renewable energy and technological innovation in realizing environmental sustainability: the role of human capital in EKC framework. Environ Sci Pollut Res 30(6):16372–16385. https://doi.org/10.1007/s11356-022-23345-6

Saqib N, Ozturk I, Usman M, Sharif A, Razzaq A (2023) Pollution Haven or Halo? How European countries leverage FDI, energy, and human capital to alleviate their ecological footprint. Gondwana Res 116:136–148. https://doi.org/10.1016/j.gr.2022.12.018

Schlaepfer MA, Lawler JJ (2023) Conserving biodiversity in the face of rapid climate change requires a shift in priorities. WIREs Clim Change 14(1). Portico. https://doi.org/10.1002/wcc.798

Shayanmehr S, Radmehr R, Ali EB, Ofori EK, Adebayo TS, Gyamfi BA (2023) How do environmental tax and renewable energy contribute to ecological sustainability? New evidence from top renewable energy countries. Int J Sustain Dev World Ecol 1–21. https://doi.org/10.1080/13504509.2023.2186961

Silajdzic S, Mehic E (2018) Do Environmental Taxes Pay Off? The Impact of Energy and Transport Taxes on CO2 Emissions in Transition Economies. South East Eur J Econ Bus 13(2):126–143. https://doi.org/10.2478/jeb-2018-0016

Simionescu M, Strielkowski W, Gavurova B (2022) Could quality of governance influence pollution? Evidence from the revised Environmental Kuznets Curve in Central and Eastern European countries. Energy Rep 8:809–819. https://doi.org/10.1016/j.egyr.2021.12.031

Sinn H-W (2008) Public policies against global warming: a supply side approach. Int Tax Public Financ 15(4):360–394. https://doi.org/10.1007/s10797-008-9082-z

Szasz J (2023) Which approaches to climate policy decrease carbon dioxide emissions? Evidence from US states, 1997–2017. Energy Res Soc Sci 97:102969. https://doi.org/10.1016/j.erss.2023.102969

Tu Z, Liu B, Jin D, Wei W, Kong J (2022) The Effect of Carbon Emission Taxes on Environmental and Economic Systems. Int J Environ Res Public Health 19(6):3706. https://doi.org/10.3390/ijerph19063706

UNCTAD (2020) Least developed countries report 2020: productive capacities for the new decade. UN and WTO reports and publications. Retrieved from https://unctad.org/meeting/launch-least-developed-countries-report-2020. Accessed 19 Feb 2023

UNCTAD (2023) Productive capacities. United Nations Conference on Trade and Development, United Nations, Geneva, Switzerland. Retrieved from https://unctadstat.unctad.org/wds/ReportFolders/reportFolders.aspx. Accessed 19 Feb 2023

Vera S, Sauma E (2015) Does a carbon tax make sense in countries with still a high potential for energy efficiency? Comparison between the reducing-emissions effects of carbon tax and energy efficiency measures in the Chilean case. Energy 88:478–488. https://doi.org/10.1016/j.energy.2015.05.067

Wang X, Alsaleh M, Abdul-Rahim AS (2022) The role of information and communication technologies in achieving hydropower sustainability: Evidence from European Union economies. Energy Environ 0958305X2211375. https://doi.org/10.1177/0958305x221137566

Wang H, Li Y, Bu G (2023a) How carbon trading policy should be integrated with carbon tax policy-laboratory evidence from a model of the current state of carbon pricing policy in China. Environ Sci Pollut Res 30(9):23851–23869. https://doi.org/10.1007/s11356-022-23787-y

Wang K, Rehman MA, Fahad S, Linzhao Z (2023b) Unleashing the influence of natural resources, sustainable energy and human capital on consumption-based carbon emissions in G-7 Countries. Resour Policy 81:103384. https://doi.org/10.1016/j.resourpol.2023.103384

Wang Q, Zhang F, Li R (2023c) Revisiting the environmental kuznets curve hypothesis in 208 counties: The roles of trade openness, human capital, renewable energy and natural resource rent. Environ Res 216:114637. https://doi.org/10.1016/j.envres.2022.114637

Ward H, Steckel JC, Jakob M (2019) How global climate policy could affect competitiveness. Energy Econ 84:104549. https://doi.org/10.1016/j.eneco.2019.104549

Westerlund J (2007) Testing for Error Correction in Panel Data. Oxford Bull Econ Stat 69(6):709–748. https://doi.org/10.1111/j.1468-0084.2007.00477.x

Wolde-Rufael Y, Mulat-Weldemeskel E (2022a) The moderating role of environmental tax and renewable energy in CO2 emissions in Latin America and Caribbean countries: Evidence from method of moments quantile regression. Environ Challenges 6:100412. https://doi.org/10.1016/j.envc.2021.100412

Wolde-Rufael Y, Mulat-weldemeskel E (2022b) Effectiveness of environmental taxes and environmental stringent policies on CO2 emissions: the European experience. Environ Dev Sustain. https://doi.org/10.1007/s10668-022-02262-1

Wurzel RKW (2016) The European Union in International Climate Change Politics.https://doi.org/10.4324/9781315627199

Xie H, Chang S, Wang Y, Afzal A (2023) The impact of e-commerce on environmental sustainability targets in selected European countries. Econ Res-Ekonomska Istraživanja 36(1):230–242. https://doi.org/10.1080/1331677x.2022.2117718

Xu L, Yilmaz HÜ, Wang Z, Poganietz W-R, Jochem P (2020) Greenhouse gas emissions of electric vehicles in Europe considering different charging strategies. Transp Res Part D: Transp Environm 87:102534. https://doi.org/10.1016/j.trd.2020.102534

Zhao J, Sinha A, Inuwa N, Wang Y, Murshed M, Abbasi KR (2022) Does structural transformation in economy impact inequality in renewable energy productivity? Implications for sustainable development. Renew Energy 189:853–864. https://doi.org/10.1016/j.renene.2022.03.050

Funding

The authors declare that no funds, grants, or other support were received during the preparation of this manuscript.

Author information

Authors and Affiliations

Contributions

All authors contributed to the study conception and design. Data collection, and analysis were performed by Mounir Dahmani. The first draft of the manuscript was written by Mounir Dahmani. Adel Ben Youssef and Mohamed Mabrouki were commented and reviewed previous versions of the manuscript. Supervision of the research: Adel Ben Youssef.

Corresponding author

Ethics declarations

Ethics approval

Not applicable.

Consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Eyup Dogan

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Youssef, A.B., Dahmani, M. & Mabrouki, M. The impact of environmentally related taxes and productive capacities on climate change: Insights from european economic area countries. Environ Sci Pollut Res 30, 99900–99912 (2023). https://doi.org/10.1007/s11356-023-29442-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-023-29442-4